Management Accounting Report: Techniques for Prime Furniture (Finance)

VerifiedAdded on 2022/12/27

|17

|3871

|97

Report

AI Summary

This report delves into the application of management accounting principles within the context of Prime Furniture Ltd. It begins by examining absorption and marginal costing methods, comparing their approaches to cost and profit assessment, and illustrating their application with numerical examples. The report then explores various management accounting techniques, including cash budgeting, capital budgeting, and ratio analysis, detailing their advantages and disadvantages for Prime Furniture's planning processes. It further analyzes how these tools can address monetary challenges and contribute to sustainable success. The report provides a comprehensive overview of financial planning and control, offering insights into decision-making for improved business performance and profitability. The report concludes with a summary of key findings and recommendations for Prime Furniture.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

TASK 2............................................................................................................................................3

P3. Assessing cost and profit with the help of absorption and marginal costing method...........3

P4 Explaining the different types of management accounting techniques that can be used by

prime furniture.............................................................................................................................5

Explaining the advantages and disadvantages of different types of planning tools with regards

to Prime Furniture........................................................................................................................9

P5. Assessing how management accounting tool can be used by Prime Furniture for

responding monetary problems..................................................................................................11

Analyzing & evaluating how management accounting planning tools helps in maintaining a

sustainable success;...................................................................................................................12

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

TASK 2............................................................................................................................................3

P3. Assessing cost and profit with the help of absorption and marginal costing method...........3

P4 Explaining the different types of management accounting techniques that can be used by

prime furniture.............................................................................................................................5

Explaining the advantages and disadvantages of different types of planning tools with regards

to Prime Furniture........................................................................................................................9

P5. Assessing how management accounting tool can be used by Prime Furniture for

responding monetary problems..................................................................................................11

Analyzing & evaluating how management accounting planning tools helps in maintaining a

sustainable success;...................................................................................................................12

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION

Management accounting is highly significant which lays focus on preparing and

providing specific information to the managers for decision making. In the context of business

organization, management accounting helps in exerting effectual control on undesirable activities

and thereby leads performance improvement. By applying the tools of MA organization can get

appropriate information within suitable time frame and thereby become able to implement

competent framework for business success. The present report is based on the case scenario of

Prime Furniture ltd which offers unique products or services to the customers at suitable prices.

In this, report will provide deeper insight about the tools & techniques that can be used by the

firm for planning purpose. Besides this, it will also shed light on the significance of marginal and

absorption costing method for the assessment of both cost as well as profitability. Further, report

will also depict managerial accounting techniques which help in dealing with monetary problems

effectually.

TASK 2

P3. Assessing cost and profit with the help of absorption and marginal costing method

There are mainly two techniques which business units undertake for doing analysis of

both cost and profitability. Marginal costing technique is undertaken by the company for

determining total cost associated with production aspect. However, in this technique, only

variable expenses are included while assessing production cost. This in turn leads the problem of

under-recovery of overheads and closing stock (Shields, 2015). On the other side, absorption

costing method emphasizes on capturing all the costs associated with production related

activities. In addition to this, in this, overheads are allocated referring the related cost-Centre

(Cooper, Ezzamel and Qu, 2017). This method is effectual as it complies with GAAP and

provides assistance in preparing reports in relation to accounting & stock.

Calculation of cost per unit in different costing method is as follows:

Particulars Absorption costing (in £) Marginal costing (in £)

Variable cost 52000 / 80000 52000 / 80000

Management accounting is highly significant which lays focus on preparing and

providing specific information to the managers for decision making. In the context of business

organization, management accounting helps in exerting effectual control on undesirable activities

and thereby leads performance improvement. By applying the tools of MA organization can get

appropriate information within suitable time frame and thereby become able to implement

competent framework for business success. The present report is based on the case scenario of

Prime Furniture ltd which offers unique products or services to the customers at suitable prices.

In this, report will provide deeper insight about the tools & techniques that can be used by the

firm for planning purpose. Besides this, it will also shed light on the significance of marginal and

absorption costing method for the assessment of both cost as well as profitability. Further, report

will also depict managerial accounting techniques which help in dealing with monetary problems

effectually.

TASK 2

P3. Assessing cost and profit with the help of absorption and marginal costing method

There are mainly two techniques which business units undertake for doing analysis of

both cost and profitability. Marginal costing technique is undertaken by the company for

determining total cost associated with production aspect. However, in this technique, only

variable expenses are included while assessing production cost. This in turn leads the problem of

under-recovery of overheads and closing stock (Shields, 2015). On the other side, absorption

costing method emphasizes on capturing all the costs associated with production related

activities. In addition to this, in this, overheads are allocated referring the related cost-Centre

(Cooper, Ezzamel and Qu, 2017). This method is effectual as it complies with GAAP and

provides assistance in preparing reports in relation to accounting & stock.

Calculation of cost per unit in different costing method is as follows:

Particulars Absorption costing (in £) Marginal costing (in £)

Variable cost 52000 / 80000 52000 / 80000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= .65 = .65

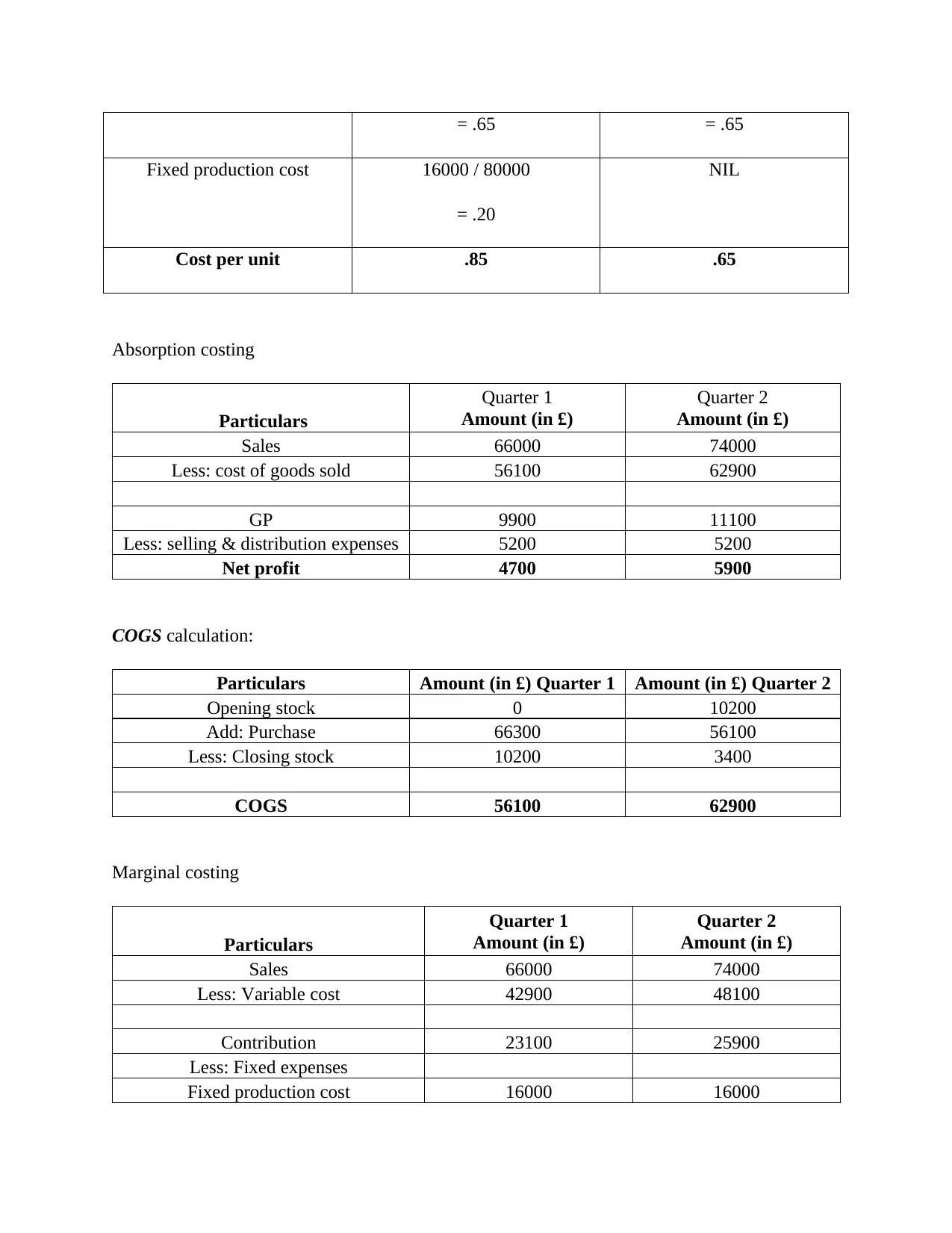

Fixed production cost 16000 / 80000

= .20

NIL

Cost per unit .85 .65

Absorption costing

Particulars

Quarter 1

Amount (in £)

Quarter 2

Amount (in £)

Sales 66000 74000

Less: cost of goods sold 56100 62900

GP 9900 11100

Less: selling & distribution expenses 5200 5200

Net profit 4700 5900

COGS calculation:

Particulars Amount (in £) Quarter 1 Amount (in £) Quarter 2

Opening stock 0 10200

Add: Purchase 66300 56100

Less: Closing stock 10200 3400

COGS 56100 62900

Marginal costing

Particulars

Quarter 1

Amount (in £)

Quarter 2

Amount (in £)

Sales 66000 74000

Less: Variable cost 42900 48100

Contribution 23100 25900

Less: Fixed expenses

Fixed production cost 16000 16000

Fixed production cost 16000 / 80000

= .20

NIL

Cost per unit .85 .65

Absorption costing

Particulars

Quarter 1

Amount (in £)

Quarter 2

Amount (in £)

Sales 66000 74000

Less: cost of goods sold 56100 62900

GP 9900 11100

Less: selling & distribution expenses 5200 5200

Net profit 4700 5900

COGS calculation:

Particulars Amount (in £) Quarter 1 Amount (in £) Quarter 2

Opening stock 0 10200

Add: Purchase 66300 56100

Less: Closing stock 10200 3400

COGS 56100 62900

Marginal costing

Particulars

Quarter 1

Amount (in £)

Quarter 2

Amount (in £)

Sales 66000 74000

Less: Variable cost 42900 48100

Contribution 23100 25900

Less: Fixed expenses

Fixed production cost 16000 16000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

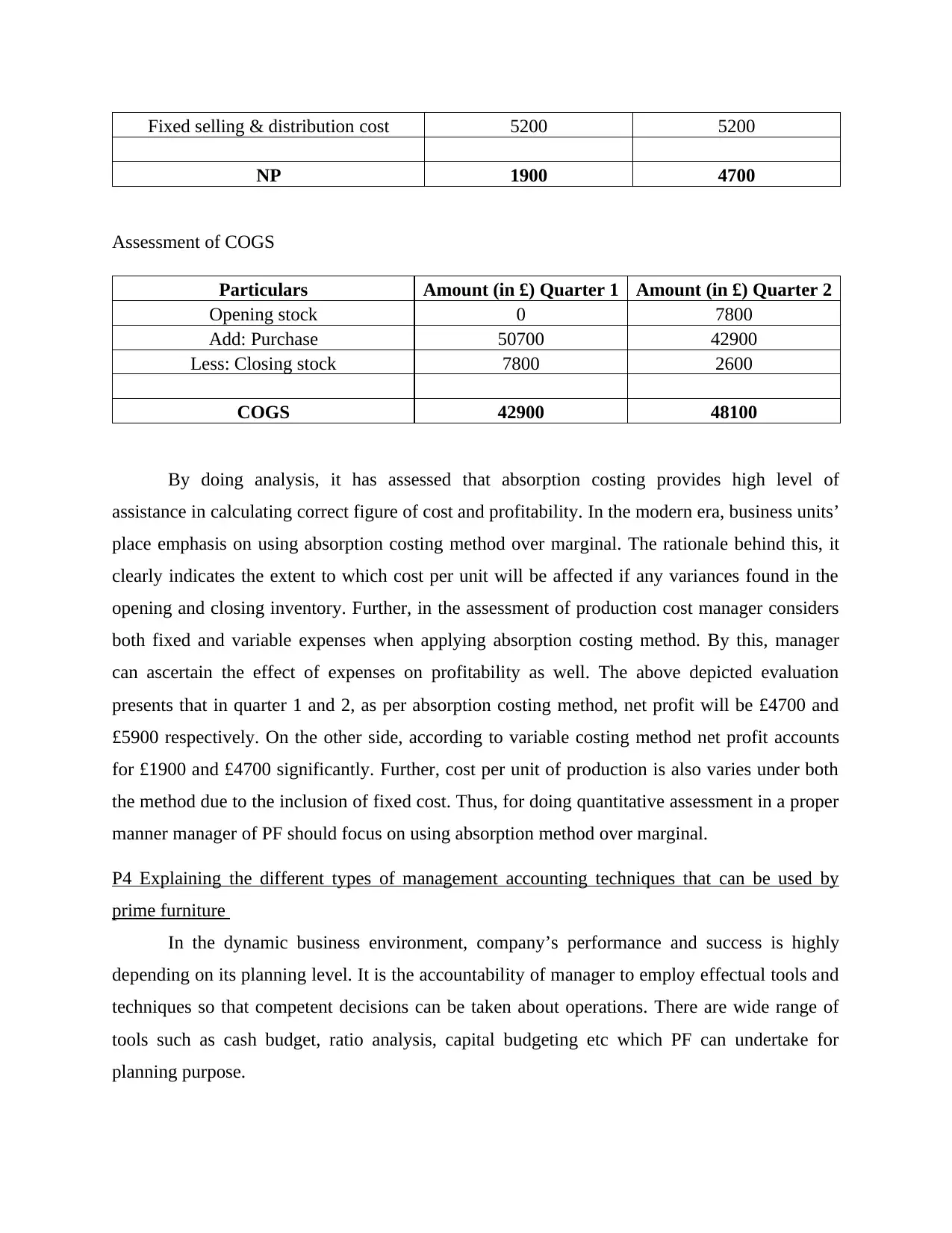

Fixed selling & distribution cost 5200 5200

NP 1900 4700

Assessment of COGS

Particulars Amount (in £) Quarter 1 Amount (in £) Quarter 2

Opening stock 0 7800

Add: Purchase 50700 42900

Less: Closing stock 7800 2600

COGS 42900 48100

By doing analysis, it has assessed that absorption costing provides high level of

assistance in calculating correct figure of cost and profitability. In the modern era, business units’

place emphasis on using absorption costing method over marginal. The rationale behind this, it

clearly indicates the extent to which cost per unit will be affected if any variances found in the

opening and closing inventory. Further, in the assessment of production cost manager considers

both fixed and variable expenses when applying absorption costing method. By this, manager

can ascertain the effect of expenses on profitability as well. The above depicted evaluation

presents that in quarter 1 and 2, as per absorption costing method, net profit will be £4700 and

£5900 respectively. On the other side, according to variable costing method net profit accounts

for £1900 and £4700 significantly. Further, cost per unit of production is also varies under both

the method due to the inclusion of fixed cost. Thus, for doing quantitative assessment in a proper

manner manager of PF should focus on using absorption method over marginal.

P4 Explaining the different types of management accounting techniques that can be used by

prime furniture

In the dynamic business environment, company’s performance and success is highly

depending on its planning level. It is the accountability of manager to employ effectual tools and

techniques so that competent decisions can be taken about operations. There are wide range of

tools such as cash budget, ratio analysis, capital budgeting etc which PF can undertake for

planning purpose.

NP 1900 4700

Assessment of COGS

Particulars Amount (in £) Quarter 1 Amount (in £) Quarter 2

Opening stock 0 7800

Add: Purchase 50700 42900

Less: Closing stock 7800 2600

COGS 42900 48100

By doing analysis, it has assessed that absorption costing provides high level of

assistance in calculating correct figure of cost and profitability. In the modern era, business units’

place emphasis on using absorption costing method over marginal. The rationale behind this, it

clearly indicates the extent to which cost per unit will be affected if any variances found in the

opening and closing inventory. Further, in the assessment of production cost manager considers

both fixed and variable expenses when applying absorption costing method. By this, manager

can ascertain the effect of expenses on profitability as well. The above depicted evaluation

presents that in quarter 1 and 2, as per absorption costing method, net profit will be £4700 and

£5900 respectively. On the other side, according to variable costing method net profit accounts

for £1900 and £4700 significantly. Further, cost per unit of production is also varies under both

the method due to the inclusion of fixed cost. Thus, for doing quantitative assessment in a proper

manner manager of PF should focus on using absorption method over marginal.

P4 Explaining the different types of management accounting techniques that can be used by

prime furniture

In the dynamic business environment, company’s performance and success is highly

depending on its planning level. It is the accountability of manager to employ effectual tools and

techniques so that competent decisions can be taken about operations. There are wide range of

tools such as cash budget, ratio analysis, capital budgeting etc which PF can undertake for

planning purpose.

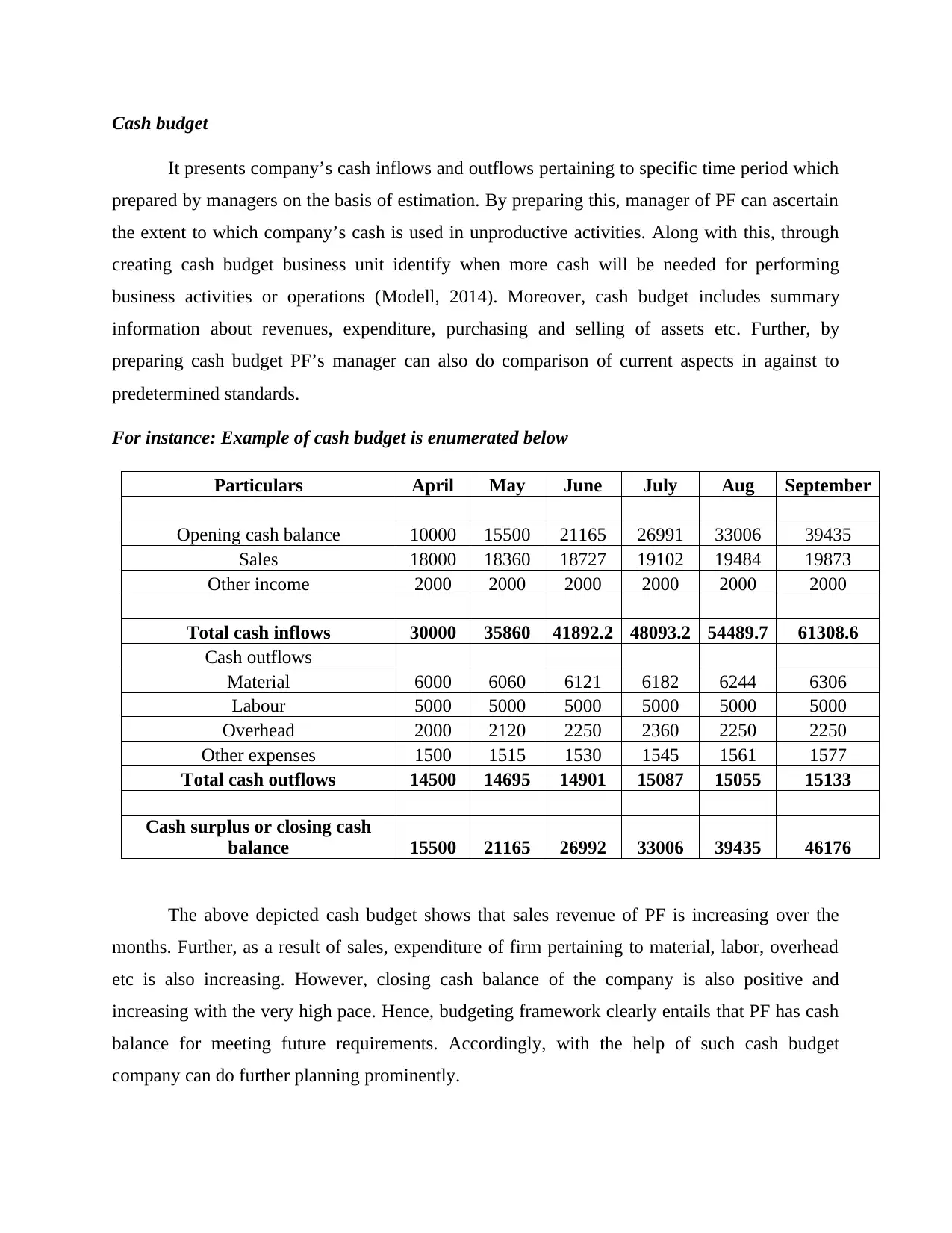

Cash budget

It presents company’s cash inflows and outflows pertaining to specific time period which

prepared by managers on the basis of estimation. By preparing this, manager of PF can ascertain

the extent to which company’s cash is used in unproductive activities. Along with this, through

creating cash budget business unit identify when more cash will be needed for performing

business activities or operations (Modell, 2014). Moreover, cash budget includes summary

information about revenues, expenditure, purchasing and selling of assets etc. Further, by

preparing cash budget PF’s manager can also do comparison of current aspects in against to

predetermined standards.

For instance: Example of cash budget is enumerated below

Particulars April May June July Aug September

Opening cash balance 10000 15500 21165 26991 33006 39435

Sales 18000 18360 18727 19102 19484 19873

Other income 2000 2000 2000 2000 2000 2000

Total cash inflows 30000 35860 41892.2 48093.2 54489.7 61308.6

Cash outflows

Material 6000 6060 6121 6182 6244 6306

Labour 5000 5000 5000 5000 5000 5000

Overhead 2000 2120 2250 2360 2250 2250

Other expenses 1500 1515 1530 1545 1561 1577

Total cash outflows 14500 14695 14901 15087 15055 15133

Cash surplus or closing cash

balance 15500 21165 26992 33006 39435 46176

The above depicted cash budget shows that sales revenue of PF is increasing over the

months. Further, as a result of sales, expenditure of firm pertaining to material, labor, overhead

etc is also increasing. However, closing cash balance of the company is also positive and

increasing with the very high pace. Hence, budgeting framework clearly entails that PF has cash

balance for meeting future requirements. Accordingly, with the help of such cash budget

company can do further planning prominently.

It presents company’s cash inflows and outflows pertaining to specific time period which

prepared by managers on the basis of estimation. By preparing this, manager of PF can ascertain

the extent to which company’s cash is used in unproductive activities. Along with this, through

creating cash budget business unit identify when more cash will be needed for performing

business activities or operations (Modell, 2014). Moreover, cash budget includes summary

information about revenues, expenditure, purchasing and selling of assets etc. Further, by

preparing cash budget PF’s manager can also do comparison of current aspects in against to

predetermined standards.

For instance: Example of cash budget is enumerated below

Particulars April May June July Aug September

Opening cash balance 10000 15500 21165 26991 33006 39435

Sales 18000 18360 18727 19102 19484 19873

Other income 2000 2000 2000 2000 2000 2000

Total cash inflows 30000 35860 41892.2 48093.2 54489.7 61308.6

Cash outflows

Material 6000 6060 6121 6182 6244 6306

Labour 5000 5000 5000 5000 5000 5000

Overhead 2000 2120 2250 2360 2250 2250

Other expenses 1500 1515 1530 1545 1561 1577

Total cash outflows 14500 14695 14901 15087 15055 15133

Cash surplus or closing cash

balance 15500 21165 26992 33006 39435 46176

The above depicted cash budget shows that sales revenue of PF is increasing over the

months. Further, as a result of sales, expenditure of firm pertaining to material, labor, overhead

etc is also increasing. However, closing cash balance of the company is also positive and

increasing with the very high pace. Hence, budgeting framework clearly entails that PF has cash

balance for meeting future requirements. Accordingly, with the help of such cash budget

company can do further planning prominently.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

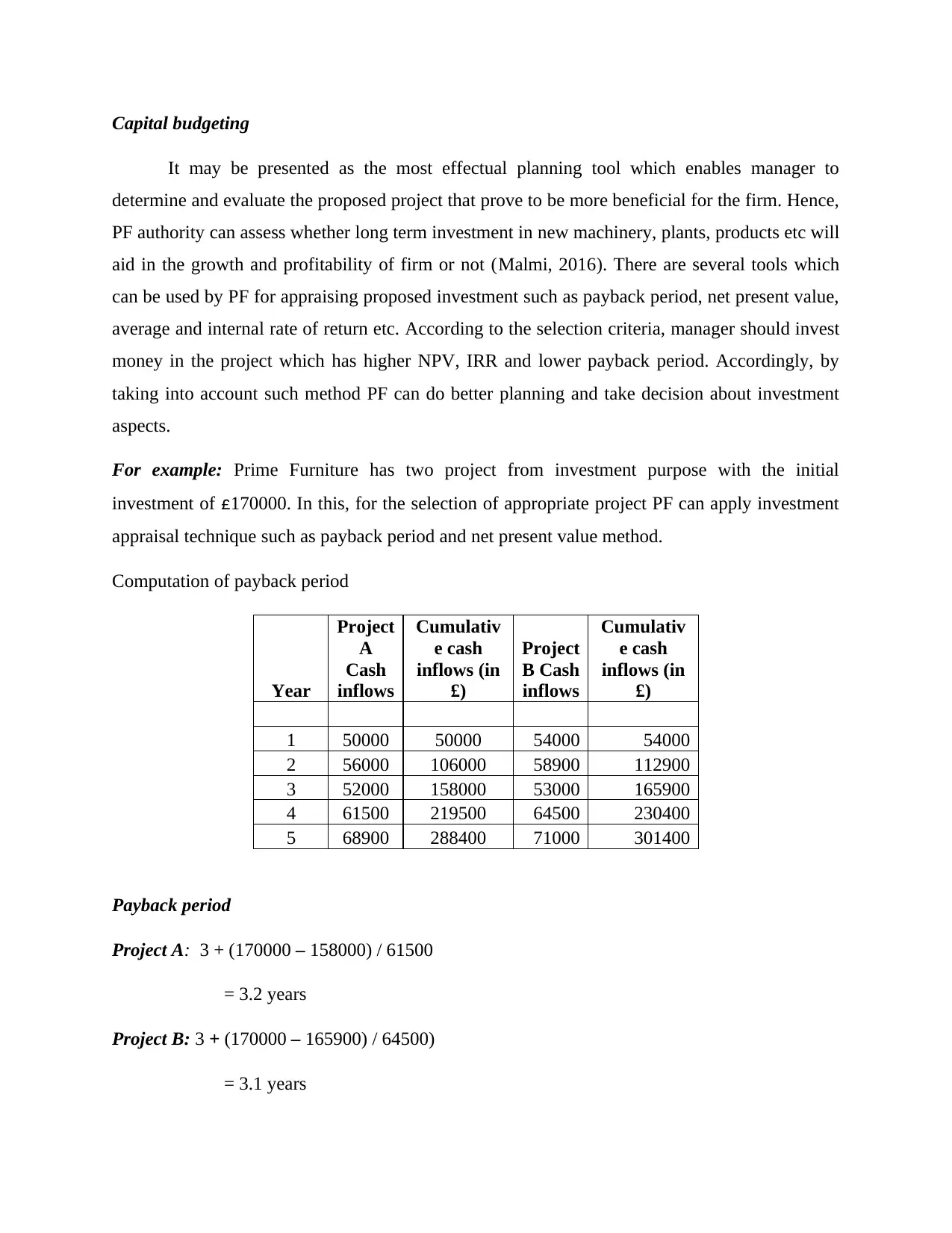

Capital budgeting

It may be presented as the most effectual planning tool which enables manager to

determine and evaluate the proposed project that prove to be more beneficial for the firm. Hence,

PF authority can assess whether long term investment in new machinery, plants, products etc will

aid in the growth and profitability of firm or not (Malmi, 2016). There are several tools which

can be used by PF for appraising proposed investment such as payback period, net present value,

average and internal rate of return etc. According to the selection criteria, manager should invest

money in the project which has higher NPV, IRR and lower payback period. Accordingly, by

taking into account such method PF can do better planning and take decision about investment

aspects.

For example: Prime Furniture has two project from investment purpose with the initial

investment of £170000. In this, for the selection of appropriate project PF can apply investment

appraisal technique such as payback period and net present value method.

Computation of payback period

Year

Project

A

Cash

inflows

Cumulativ

e cash

inflows (in

£)

Project

B Cash

inflows

Cumulativ

e cash

inflows (in

£)

1 50000 50000 54000 54000

2 56000 106000 58900 112900

3 52000 158000 53000 165900

4 61500 219500 64500 230400

5 68900 288400 71000 301400

Payback period

Project A: 3 + (170000 – 158000) / 61500

= 3.2 years

Project B: 3 + (170000 – 165900) / 64500)

= 3.1 years

It may be presented as the most effectual planning tool which enables manager to

determine and evaluate the proposed project that prove to be more beneficial for the firm. Hence,

PF authority can assess whether long term investment in new machinery, plants, products etc will

aid in the growth and profitability of firm or not (Malmi, 2016). There are several tools which

can be used by PF for appraising proposed investment such as payback period, net present value,

average and internal rate of return etc. According to the selection criteria, manager should invest

money in the project which has higher NPV, IRR and lower payback period. Accordingly, by

taking into account such method PF can do better planning and take decision about investment

aspects.

For example: Prime Furniture has two project from investment purpose with the initial

investment of £170000. In this, for the selection of appropriate project PF can apply investment

appraisal technique such as payback period and net present value method.

Computation of payback period

Year

Project

A

Cash

inflows

Cumulativ

e cash

inflows (in

£)

Project

B Cash

inflows

Cumulativ

e cash

inflows (in

£)

1 50000 50000 54000 54000

2 56000 106000 58900 112900

3 52000 158000 53000 165900

4 61500 219500 64500 230400

5 68900 288400 71000 301400

Payback period

Project A: 3 + (170000 – 158000) / 61500

= 3.2 years

Project B: 3 + (170000 – 165900) / 64500)

= 3.1 years

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Calculation of NPV

Year

PV factors

@10%

Project A Cash

inflows

Discou

nted

cash

inflows

Project B Cash

inflows

Discou

nted

cash

inflows

1 0.909 50000 45455 54000 49091

2 0.826 56000 46281 58900 48678

3 0.751 52000 39068 53000 39820

4 0.683 61500 42005 64500 44054

5 0.621 68900 42781 71000 44085

Total discounted

cash inflow 215591 225728

Initial investment 170000 170000

NPV (Total

discounted cash

inflows - initial

investment) 45591 55728

As per the above assessment, manager of PF should select and invest money in project 2.

Moreover, in the case of project 2, company will recoup amount of initial investment within the

period of 3 years and one month. Thereafter, business unit will start to earn profit and contributes

in the attainment of organizational objectives. Further, by applying time value of money concept,

it has assessed that firm will generate positive and higher return in project 2 over others. Hence,

referring overall evaluation it can be said that investment in project 2 will prove to be more

beneficial for the firm.

Ratio analysis

It is a quantitative tool which helps in gaining deeper insight about company’s position

and performance from several perspectives such as liquidity, efficiency, profitability &

Year

PV factors

@10%

Project A Cash

inflows

Discou

nted

cash

inflows

Project B Cash

inflows

Discou

nted

cash

inflows

1 0.909 50000 45455 54000 49091

2 0.826 56000 46281 58900 48678

3 0.751 52000 39068 53000 39820

4 0.683 61500 42005 64500 44054

5 0.621 68900 42781 71000 44085

Total discounted

cash inflow 215591 225728

Initial investment 170000 170000

NPV (Total

discounted cash

inflows - initial

investment) 45591 55728

As per the above assessment, manager of PF should select and invest money in project 2.

Moreover, in the case of project 2, company will recoup amount of initial investment within the

period of 3 years and one month. Thereafter, business unit will start to earn profit and contributes

in the attainment of organizational objectives. Further, by applying time value of money concept,

it has assessed that firm will generate positive and higher return in project 2 over others. Hence,

referring overall evaluation it can be said that investment in project 2 will prove to be more

beneficial for the firm.

Ratio analysis

It is a quantitative tool which helps in gaining deeper insight about company’s position

and performance from several perspectives such as liquidity, efficiency, profitability &

efficiency. By undertaking ratio analysis tool PF can summarize its financial statements in the

best possible manner (Lavia López and Hiebl, 2015). Through this, manager of business unit can

assess how company is performing over the years. Hence, by evaluating current position

business organization can take significant decisions for future growth.

Explaining the advantages and disadvantages of different types of planning tools with regards to

Prime Furniture

There are several advantages and disadvantages which manager of PF should keep in

mind while taking decisions about planning tools.

Capital budgeting

Advantages

Helps in doing evaluation of long term investment plans through considering risk, return

and investment opportunities.

Risks pertaining to loss and other aspects can be examined by the manager of PF through

applying capital budgeting tools (Azudin and Mansor, 2018).

Provides assistance in maximizing shareholders wealth by avoiding situation pertaining

to under or over investment.

Disadvantages

This tool is highly relied and based on estimation which in turn limits its significance

level.

Decision taken on the basis of capital budgeting tools are highly risky in nature because it

directly impacts company’s success.

Further, it offers solution or framework for decision making by considering only financial

factors. On the other side, non-financial factors also have significant impact on long term

investment

Cash budget

Advantages

best possible manner (Lavia López and Hiebl, 2015). Through this, manager of business unit can

assess how company is performing over the years. Hence, by evaluating current position

business organization can take significant decisions for future growth.

Explaining the advantages and disadvantages of different types of planning tools with regards to

Prime Furniture

There are several advantages and disadvantages which manager of PF should keep in

mind while taking decisions about planning tools.

Capital budgeting

Advantages

Helps in doing evaluation of long term investment plans through considering risk, return

and investment opportunities.

Risks pertaining to loss and other aspects can be examined by the manager of PF through

applying capital budgeting tools (Azudin and Mansor, 2018).

Provides assistance in maximizing shareholders wealth by avoiding situation pertaining

to under or over investment.

Disadvantages

This tool is highly relied and based on estimation which in turn limits its significance

level.

Decision taken on the basis of capital budgeting tools are highly risky in nature because it

directly impacts company’s success.

Further, it offers solution or framework for decision making by considering only financial

factors. On the other side, non-financial factors also have significant impact on long term

investment

Cash budget

Advantages

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

By preparing cash budget business unit can deal with the contingent situation more

effectually.

Ensures availability of more resources and growth by exerting control on expenses (Wu

and Wang, 2020).

Provides input for assessing deficits which may arise in the near future and gives

indication for taking corrective measures.

Disadvantages

It is based on the estimation of future events regarding receipt and payment. Hence, due

to the absence of having factual knowledge and aspects manager face difficulty in

drafting suitable cash budget.

Lack of flexibility, non-financial factors and rigidness also limits effectualness of cash

budget.

At the time of preparing cash budget managers do manipulation due to ulterior motives.

Moreover, with the motive to develop effective image in the mind of customers managers

usually underestimate budgeted expenses which in turn results into inappropriate

financial framework (The Disadvantages of a Cash Budget, 2021).

Ratio analysis

Advantages

By doing ratio analysis PF can do better forecast and planning about future activities.

Helps in making proper estimation while creating budget for the upcoming time period.

Operational efficiency can be measures and evaluated by PF with the help of ratio

analysis tool (Taschner and Charifzadeh, 2020).

Offers basis for decision making through inter-firm comparison and thereby controls both

cost as well as performance.

Disadvantages

effectually.

Ensures availability of more resources and growth by exerting control on expenses (Wu

and Wang, 2020).

Provides input for assessing deficits which may arise in the near future and gives

indication for taking corrective measures.

Disadvantages

It is based on the estimation of future events regarding receipt and payment. Hence, due

to the absence of having factual knowledge and aspects manager face difficulty in

drafting suitable cash budget.

Lack of flexibility, non-financial factors and rigidness also limits effectualness of cash

budget.

At the time of preparing cash budget managers do manipulation due to ulterior motives.

Moreover, with the motive to develop effective image in the mind of customers managers

usually underestimate budgeted expenses which in turn results into inappropriate

financial framework (The Disadvantages of a Cash Budget, 2021).

Ratio analysis

Advantages

By doing ratio analysis PF can do better forecast and planning about future activities.

Helps in making proper estimation while creating budget for the upcoming time period.

Operational efficiency can be measures and evaluated by PF with the help of ratio

analysis tool (Taschner and Charifzadeh, 2020).

Offers basis for decision making through inter-firm comparison and thereby controls both

cost as well as performance.

Disadvantages

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Lack of standard comparison as different companies follow varied accounting rules

and principles.

It is based on historical data, whereas management is taking decision about future

aspects.

Along with this, ratio analysis tool ignores qualitative aspects while presenting results

for decision making.

P5. Assessing how management accounting tool can be used by Prime Furniture for responding

monetary problems

In the business unit, occurrence of problems are usual which in turn directly impacts

profit, growth and overall performance. Hence, in order to avoid problems and related impact

manager of Prime Furniture can employ below mentioned tools and technique such as:

Balance scorecard

PF can use balance scorecard tool for the management and implementation of strategy.

By using this tool PF can align vision with strategic objectives, targets, measures and business

initiatives. Hence, by applying performance metric PF can make improvement in the internal

business functions and resulting outcomes. Through undertaking quantitative assessment

managers can do better decision about business aspects (What Is A Balanced Scorecard?, 2021).

The rationale behind this, such tool helps in evaluating business performance from numerous

perspectives such as financial, earning & growth, customer and business process. In this way,

such measurement tool can be used by the firm for decision making and achieving success.

Benchmarking

PF can use this tool for the purpose of measuring products, services and processes in

against to the business units which are performing well within industry. By undertaking this,

management team can understand position where PF lies as compared to the market leaders

(What is Benchmarking?, 2021). Hence, by taking into account results manager of PF can assess

areas which need improvements in terms of business process re-engineering or others.

Key-performance indicators

and principles.

It is based on historical data, whereas management is taking decision about future

aspects.

Along with this, ratio analysis tool ignores qualitative aspects while presenting results

for decision making.

P5. Assessing how management accounting tool can be used by Prime Furniture for responding

monetary problems

In the business unit, occurrence of problems are usual which in turn directly impacts

profit, growth and overall performance. Hence, in order to avoid problems and related impact

manager of Prime Furniture can employ below mentioned tools and technique such as:

Balance scorecard

PF can use balance scorecard tool for the management and implementation of strategy.

By using this tool PF can align vision with strategic objectives, targets, measures and business

initiatives. Hence, by applying performance metric PF can make improvement in the internal

business functions and resulting outcomes. Through undertaking quantitative assessment

managers can do better decision about business aspects (What Is A Balanced Scorecard?, 2021).

The rationale behind this, such tool helps in evaluating business performance from numerous

perspectives such as financial, earning & growth, customer and business process. In this way,

such measurement tool can be used by the firm for decision making and achieving success.

Benchmarking

PF can use this tool for the purpose of measuring products, services and processes in

against to the business units which are performing well within industry. By undertaking this,

management team can understand position where PF lies as compared to the market leaders

(What is Benchmarking?, 2021). Hence, by taking into account results manager of PF can assess

areas which need improvements in terms of business process re-engineering or others.

Key-performance indicators

It may be presented as a set of quantifiable set of performance measurements which help

in assessing the extent to which firm attained targets or key objectives (Shields, 2015). With

regards to PF, KPI’s mainly include sales, profit, market share etc. Hence, referring such KPI’s

firm can evaluate progress and thereby takes decision in relation to strategic as well as tactical

aspects.

Variance analysis

PF can use variance analysis for assessing and dealing with the deviations found in

company’s performance. Moreover, it clearly exhibits difference which take place between

actual and budgeted figures (Schuster, Heinemann and Cleary, 2021). By this, manager can

ascertain causes for such deviations assesses and thereby takes measure for improving

undesirable results.

Analyzing & evaluating how management accounting planning tools helps in maintaining a

sustainable success;

Balance scorecard

Benefits Drawbacks

Fosters effectual communication

within an organization.

Motivates firm to apply innovative

and process improvement methods for

fulfilling corporate goals.

It is highly systematic tool which

clearly indicates company’s

performance.

Expensive and time consuming

practice due to which managers

avoid to use this technique.

BS approach requires lots of data from

various departments. Hence, if

managers of different departments fail

to serve appropriate information then

it may result into inappropriate

strategic framework (Modell, 2014).

Along with this, for attaining success

referring BS tool supportive or

prominent leadership style is required.

In the absence of this, manager would

in assessing the extent to which firm attained targets or key objectives (Shields, 2015). With

regards to PF, KPI’s mainly include sales, profit, market share etc. Hence, referring such KPI’s

firm can evaluate progress and thereby takes decision in relation to strategic as well as tactical

aspects.

Variance analysis

PF can use variance analysis for assessing and dealing with the deviations found in

company’s performance. Moreover, it clearly exhibits difference which take place between

actual and budgeted figures (Schuster, Heinemann and Cleary, 2021). By this, manager can

ascertain causes for such deviations assesses and thereby takes measure for improving

undesirable results.

Analyzing & evaluating how management accounting planning tools helps in maintaining a

sustainable success;

Balance scorecard

Benefits Drawbacks

Fosters effectual communication

within an organization.

Motivates firm to apply innovative

and process improvement methods for

fulfilling corporate goals.

It is highly systematic tool which

clearly indicates company’s

performance.

Expensive and time consuming

practice due to which managers

avoid to use this technique.

BS approach requires lots of data from

various departments. Hence, if

managers of different departments fail

to serve appropriate information then

it may result into inappropriate

strategic framework (Modell, 2014).

Along with this, for attaining success

referring BS tool supportive or

prominent leadership style is required.

In the absence of this, manager would

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.