Finance for Managers Report: Financial Analysis and Recommendations

VerifiedAdded on 2020/06/06

|14

|3403

|193

Report

AI Summary

This report, prepared for a Finance for Managers course, delves into crucial aspects of financial management within a business context. It begins by outlining the objectives and needs of financial records, detailing methods of recording financial data, and evaluating the legal and business requirements of financial reporting. The report then analyzes the effectiveness of stakeholders and compares management accounting with financial accounting. Budgetary control processes, including planning and forecasting, are examined, along with various costing techniques such as fixed, variable, and marginal costing. The core of the report involves the computation and interpretation of variances, covering material, labor, and overhead costs, along with sales variances. Finally, the report explores working capital components, their management, and the importance of values in financial decision-making, concluding with recommendations for enhancing business profitability. The report also includes an operating statement and detailed variance analysis to assess the company's financial performance.

Finance for Managers

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1: Objectives and needs of financial records............................................................................1

1.2: Methods of recording financial data....................................................................................1

1.3: Evaluation of legal and business needs of financial reporting.............................................2

1.4: Analyse effectiveness of stakeholders.................................................................................2

3.1: Comparison..........................................................................................................................3

3.2: Budgetary control process....................................................................................................3

3.4: Various costing techniques..................................................................................................4

TASK 2............................................................................................................................................5

3.3: Computation of variances....................................................................................................5

TASK 3............................................................................................................................................8

4.1: Computation ........................................................................................................................8

4.2: Importance of values............................................................................................................9

4.3: Value require to examine viability in a project....................................................................9

2.1: Working capital components.............................................................................................10

2.2: Management of working capital .......................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1: Objectives and needs of financial records............................................................................1

1.2: Methods of recording financial data....................................................................................1

1.3: Evaluation of legal and business needs of financial reporting.............................................2

1.4: Analyse effectiveness of stakeholders.................................................................................2

3.1: Comparison..........................................................................................................................3

3.2: Budgetary control process....................................................................................................3

3.4: Various costing techniques..................................................................................................4

TASK 2............................................................................................................................................5

3.3: Computation of variances....................................................................................................5

TASK 3............................................................................................................................................8

4.1: Computation ........................................................................................................................8

4.2: Importance of values............................................................................................................9

4.3: Value require to examine viability in a project....................................................................9

2.1: Working capital components.............................................................................................10

2.2: Management of working capital .......................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Finance is the utmost important aspect for every business enterprise in order to manage

its everyday transactions. It can be arising from various sources such as internal as well as

external. It is the primary role of managers to arrange sources in respect to meet certain

operational activities of an organisation (Malkiel, 2013). This project report provides necessary

purpose of record keeping or tools those are collected from daily operations. Use of budgetary

control steps to analyse recording of financial data in the company. Further, few calculation is

being done to determine stability and performance during the time. The overall analysis is

providing crucial recommendation to make business more profitability in future time.

TASK 1

1.1: Objectives and needs of financial records

Financial records are one for the formal ways of recording financial transaction those are

incur by the company during their daily activities. It would be applicable for all types of business

entity such as sole trader, company or any other enterprises. It will be consisting of a statement

of retained profits, cash flow, profit and loss statements and balance sheet. They require this for

maintain tax benefits for the company (Moffett, Stonehill and Eiteman, 2014).

Purpose and requirements:

Legal requirements: Companies act entity financial statements used to prepare in

accordance with applicable accounting standards under section 291.

Tax requirements: Tax appear in some form in every three financial statements.

Deferred tax liability can be considered in the long-term liabilities section of the balance

sheet. It would specify, whether companies are paying taxes as per the decided policies of

the country.

Internal control requirements: By the help of this, company can easily be able to

decided total amount of expenses and incomes company is paying within an accounting

period.

1.2: Methods of recording financial data

There are various tools and techniques which can be use by the managers in order to

maintain their financial information. From the use of those techniques in more systematic and

1

Finance is the utmost important aspect for every business enterprise in order to manage

its everyday transactions. It can be arising from various sources such as internal as well as

external. It is the primary role of managers to arrange sources in respect to meet certain

operational activities of an organisation (Malkiel, 2013). This project report provides necessary

purpose of record keeping or tools those are collected from daily operations. Use of budgetary

control steps to analyse recording of financial data in the company. Further, few calculation is

being done to determine stability and performance during the time. The overall analysis is

providing crucial recommendation to make business more profitability in future time.

TASK 1

1.1: Objectives and needs of financial records

Financial records are one for the formal ways of recording financial transaction those are

incur by the company during their daily activities. It would be applicable for all types of business

entity such as sole trader, company or any other enterprises. It will be consisting of a statement

of retained profits, cash flow, profit and loss statements and balance sheet. They require this for

maintain tax benefits for the company (Moffett, Stonehill and Eiteman, 2014).

Purpose and requirements:

Legal requirements: Companies act entity financial statements used to prepare in

accordance with applicable accounting standards under section 291.

Tax requirements: Tax appear in some form in every three financial statements.

Deferred tax liability can be considered in the long-term liabilities section of the balance

sheet. It would specify, whether companies are paying taxes as per the decided policies of

the country.

Internal control requirements: By the help of this, company can easily be able to

decided total amount of expenses and incomes company is paying within an accounting

period.

1.2: Methods of recording financial data

There are various tools and techniques which can be use by the managers in order to

maintain their financial information. From the use of those techniques in more systematic and

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

quick manner chances of getting positive results would be increased. Some of them are mention

underneath:

Double entry bookkeeping: It is an effective system that is used for the purpose of

posting all types of financial entries (Renz, 2016). It provides valuable information that

every accounts would have double impacts on the statements.

Day book and ledger: A purchases day book is an accounting ledger in which buying

transaction are recorded effectively. All the financial transaction is recorded into ledger

books.

The trail balance: A statements of all the debts and credit in a double account book with

any disagreement indicating an errors are analysing through this trail balance. After

recording all the transaction into the ledger then posted into the trail balance.

1.3: Evaluation of legal and business needs of financial reporting

It has been observed that several nations have determine their own accounting techniques

and tools over the period of time. In order to maintain and regulate balance in regularity among

respective statements such kind of decision is been made. There are forced toward standardizing

rules and regulation those are made by IASB.

Financial reporting requirements for sole traders: A personal finance are more closely

linked business operations than with any other types of business structure. The financial account

of sole trader companies of trading accounting. Self-employed sole traders and most partnerships

do not need to create a formal profit and loss statements.

Public limited companies: It is utmost important for the public limited company to

prepared financial statements so that to issues shares as well as bring IPO. It will assist in

arranging all the essential options those are helpful in generating maximum profitability.

Private limited companies; It is mandatory for every private limited company to hold an

AGM in every year for the data for closing the financial year. they are required to maintain

proper records of data which will be helpful in presenting it in front of various investors.

1.4: Analyse effectiveness of stakeholders

In every business organisation, stakeholder is playing an important role in order to

maintain proper balance between their business growth and performances. They make huge

impacts over business operation either directly or indirectly. The most crucial parties those are

consists under this are managers, employee's, owners and board members. All of them are

2

underneath:

Double entry bookkeeping: It is an effective system that is used for the purpose of

posting all types of financial entries (Renz, 2016). It provides valuable information that

every accounts would have double impacts on the statements.

Day book and ledger: A purchases day book is an accounting ledger in which buying

transaction are recorded effectively. All the financial transaction is recorded into ledger

books.

The trail balance: A statements of all the debts and credit in a double account book with

any disagreement indicating an errors are analysing through this trail balance. After

recording all the transaction into the ledger then posted into the trail balance.

1.3: Evaluation of legal and business needs of financial reporting

It has been observed that several nations have determine their own accounting techniques

and tools over the period of time. In order to maintain and regulate balance in regularity among

respective statements such kind of decision is been made. There are forced toward standardizing

rules and regulation those are made by IASB.

Financial reporting requirements for sole traders: A personal finance are more closely

linked business operations than with any other types of business structure. The financial account

of sole trader companies of trading accounting. Self-employed sole traders and most partnerships

do not need to create a formal profit and loss statements.

Public limited companies: It is utmost important for the public limited company to

prepared financial statements so that to issues shares as well as bring IPO. It will assist in

arranging all the essential options those are helpful in generating maximum profitability.

Private limited companies; It is mandatory for every private limited company to hold an

AGM in every year for the data for closing the financial year. they are required to maintain

proper records of data which will be helpful in presenting it in front of various investors.

1.4: Analyse effectiveness of stakeholders

In every business organisation, stakeholder is playing an important role in order to

maintain proper balance between their business growth and performances. They make huge

impacts over business operation either directly or indirectly. The most crucial parties those are

consists under this are managers, employee's, owners and board members. All of them are

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

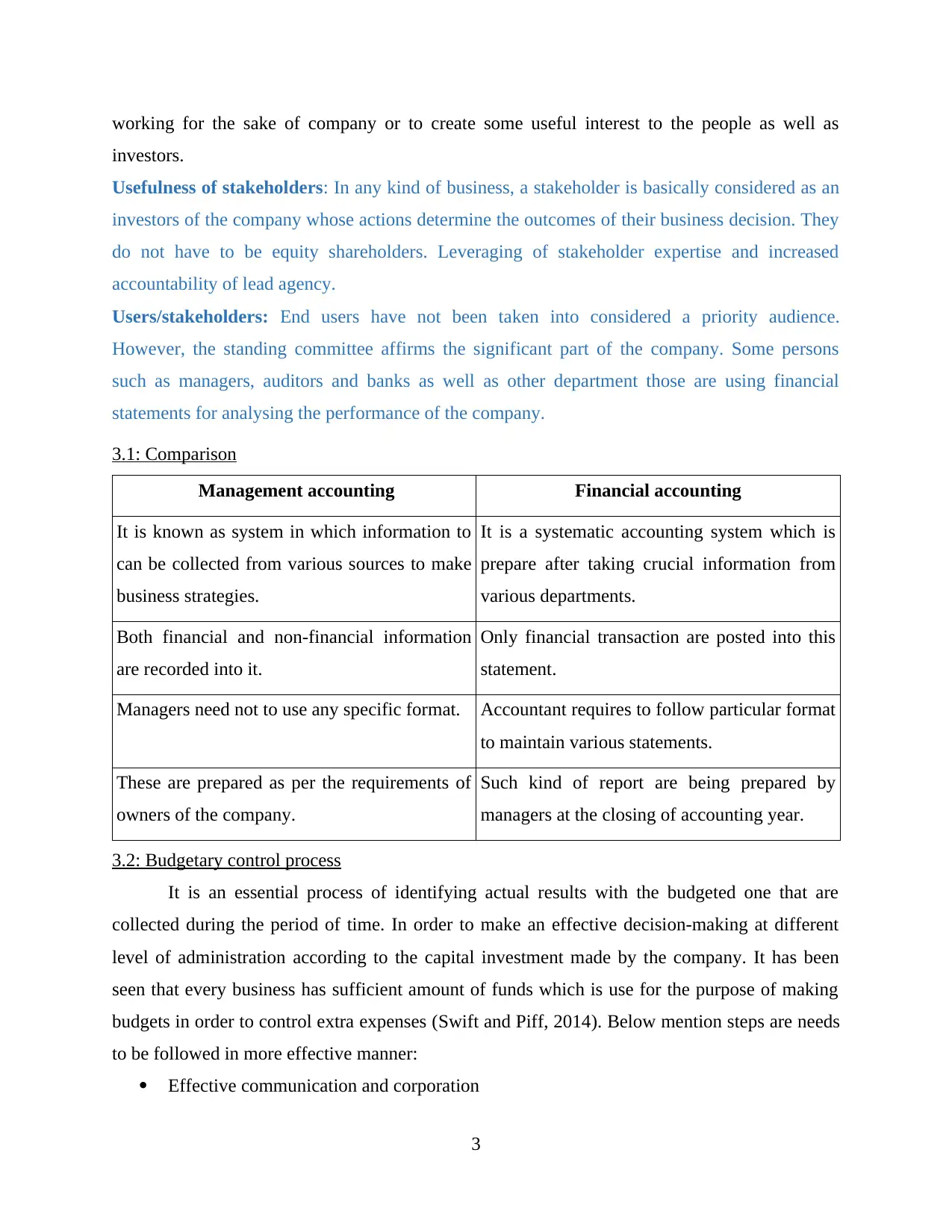

working for the sake of company or to create some useful interest to the people as well as

investors.

Usefulness of stakeholders: In any kind of business, a stakeholder is basically considered as an

investors of the company whose actions determine the outcomes of their business decision. They

do not have to be equity shareholders. Leveraging of stakeholder expertise and increased

accountability of lead agency.

Users/stakeholders: End users have not been taken into considered a priority audience.

However, the standing committee affirms the significant part of the company. Some persons

such as managers, auditors and banks as well as other department those are using financial

statements for analysing the performance of the company.

3.1: Comparison

Management accounting Financial accounting

It is known as system in which information to

can be collected from various sources to make

business strategies.

It is a systematic accounting system which is

prepare after taking crucial information from

various departments.

Both financial and non-financial information

are recorded into it.

Only financial transaction are posted into this

statement.

Managers need not to use any specific format. Accountant requires to follow particular format

to maintain various statements.

These are prepared as per the requirements of

owners of the company.

Such kind of report are being prepared by

managers at the closing of accounting year.

3.2: Budgetary control process

It is an essential process of identifying actual results with the budgeted one that are

collected during the period of time. In order to make an effective decision-making at different

level of administration according to the capital investment made by the company. It has been

seen that every business has sufficient amount of funds which is use for the purpose of making

budgets in order to control extra expenses (Swift and Piff, 2014). Below mention steps are needs

to be followed in more effective manner:

Effective communication and corporation

3

investors.

Usefulness of stakeholders: In any kind of business, a stakeholder is basically considered as an

investors of the company whose actions determine the outcomes of their business decision. They

do not have to be equity shareholders. Leveraging of stakeholder expertise and increased

accountability of lead agency.

Users/stakeholders: End users have not been taken into considered a priority audience.

However, the standing committee affirms the significant part of the company. Some persons

such as managers, auditors and banks as well as other department those are using financial

statements for analysing the performance of the company.

3.1: Comparison

Management accounting Financial accounting

It is known as system in which information to

can be collected from various sources to make

business strategies.

It is a systematic accounting system which is

prepare after taking crucial information from

various departments.

Both financial and non-financial information

are recorded into it.

Only financial transaction are posted into this

statement.

Managers need not to use any specific format. Accountant requires to follow particular format

to maintain various statements.

These are prepared as per the requirements of

owners of the company.

Such kind of report are being prepared by

managers at the closing of accounting year.

3.2: Budgetary control process

It is an essential process of identifying actual results with the budgeted one that are

collected during the period of time. In order to make an effective decision-making at different

level of administration according to the capital investment made by the company. It has been

seen that every business has sufficient amount of funds which is use for the purpose of making

budgets in order to control extra expenses (Swift and Piff, 2014). Below mention steps are needs

to be followed in more effective manner:

Effective communication and corporation

3

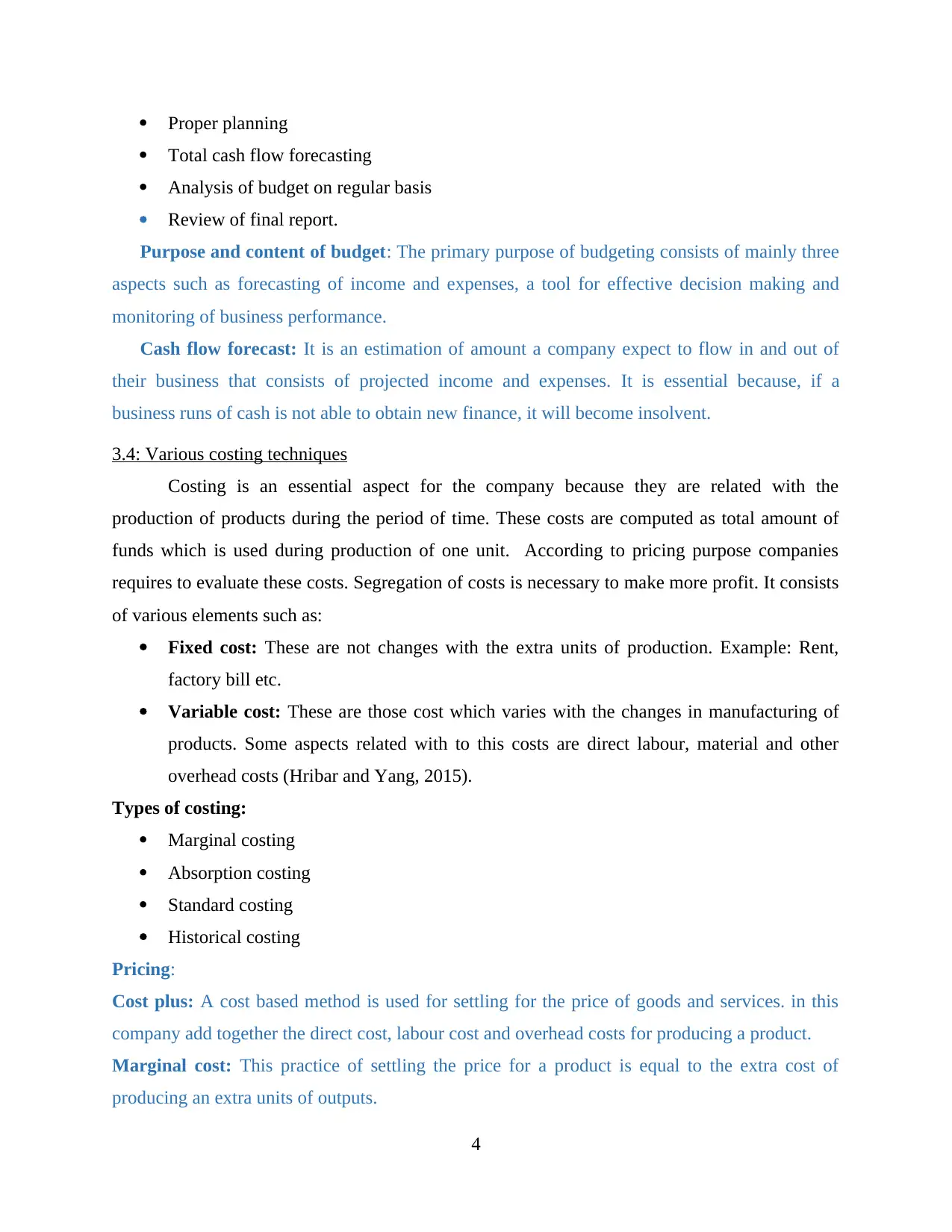

Proper planning

Total cash flow forecasting

Analysis of budget on regular basis

Review of final report.

Purpose and content of budget: The primary purpose of budgeting consists of mainly three

aspects such as forecasting of income and expenses, a tool for effective decision making and

monitoring of business performance.

Cash flow forecast: It is an estimation of amount a company expect to flow in and out of

their business that consists of projected income and expenses. It is essential because, if a

business runs of cash is not able to obtain new finance, it will become insolvent.

3.4: Various costing techniques

Costing is an essential aspect for the company because they are related with the

production of products during the period of time. These costs are computed as total amount of

funds which is used during production of one unit. According to pricing purpose companies

requires to evaluate these costs. Segregation of costs is necessary to make more profit. It consists

of various elements such as:

Fixed cost: These are not changes with the extra units of production. Example: Rent,

factory bill etc.

Variable cost: These are those cost which varies with the changes in manufacturing of

products. Some aspects related with to this costs are direct labour, material and other

overhead costs (Hribar and Yang, 2015).

Types of costing:

Marginal costing

Absorption costing

Standard costing

Historical costing

Pricing:

Cost plus: A cost based method is used for settling for the price of goods and services. in this

company add together the direct cost, labour cost and overhead costs for producing a product.

Marginal cost: This practice of settling the price for a product is equal to the extra cost of

producing an extra units of outputs.

4

Total cash flow forecasting

Analysis of budget on regular basis

Review of final report.

Purpose and content of budget: The primary purpose of budgeting consists of mainly three

aspects such as forecasting of income and expenses, a tool for effective decision making and

monitoring of business performance.

Cash flow forecast: It is an estimation of amount a company expect to flow in and out of

their business that consists of projected income and expenses. It is essential because, if a

business runs of cash is not able to obtain new finance, it will become insolvent.

3.4: Various costing techniques

Costing is an essential aspect for the company because they are related with the

production of products during the period of time. These costs are computed as total amount of

funds which is used during production of one unit. According to pricing purpose companies

requires to evaluate these costs. Segregation of costs is necessary to make more profit. It consists

of various elements such as:

Fixed cost: These are not changes with the extra units of production. Example: Rent,

factory bill etc.

Variable cost: These are those cost which varies with the changes in manufacturing of

products. Some aspects related with to this costs are direct labour, material and other

overhead costs (Hribar and Yang, 2015).

Types of costing:

Marginal costing

Absorption costing

Standard costing

Historical costing

Pricing:

Cost plus: A cost based method is used for settling for the price of goods and services. in this

company add together the direct cost, labour cost and overhead costs for producing a product.

Marginal cost: This practice of settling the price for a product is equal to the extra cost of

producing an extra units of outputs.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2

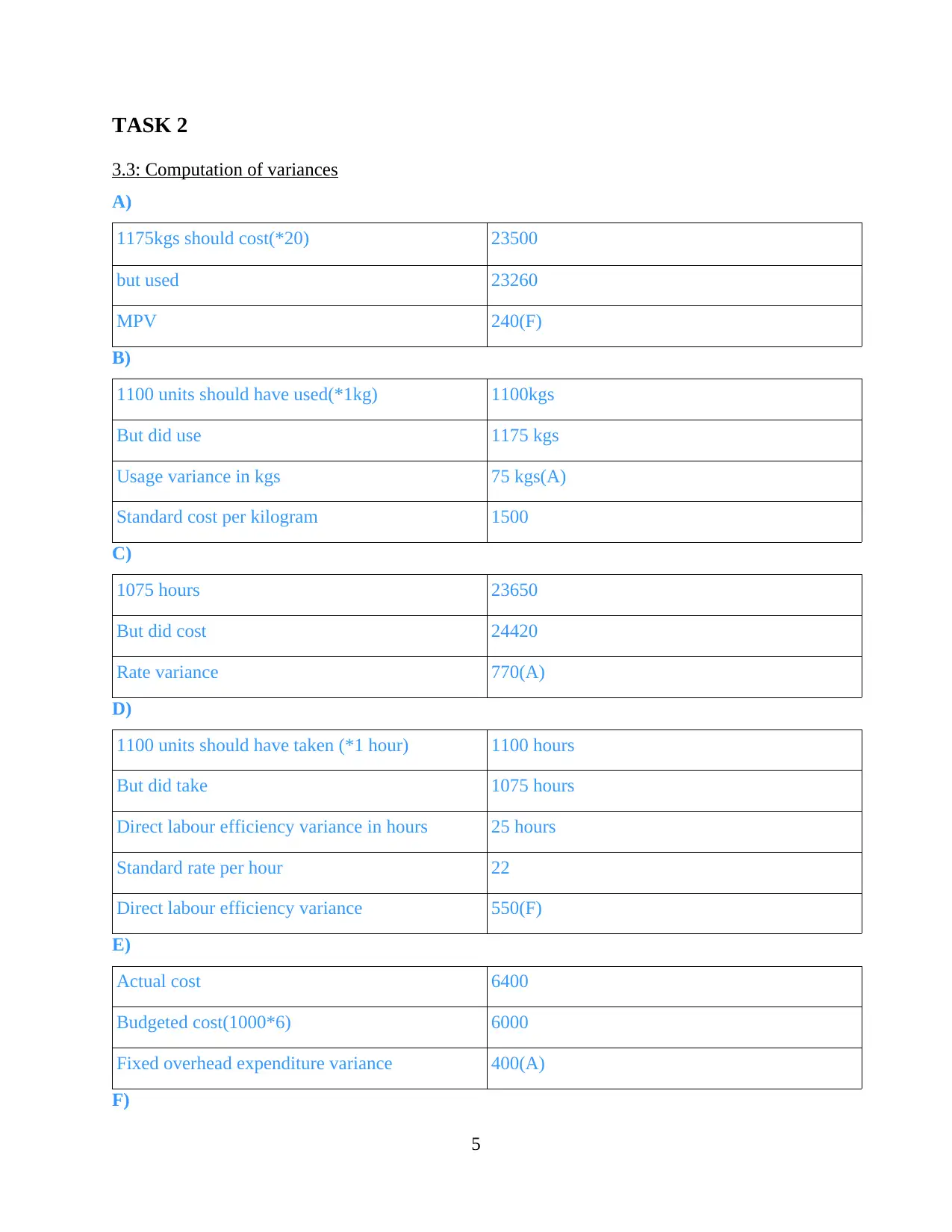

3.3: Computation of variances

A)

1175kgs should cost(*20) 23500

but used 23260

MPV 240(F)

B)

1100 units should have used(*1kg) 1100kgs

But did use 1175 kgs

Usage variance in kgs 75 kgs(A)

Standard cost per kilogram 1500

C)

1075 hours 23650

But did cost 24420

Rate variance 770(A)

D)

1100 units should have taken (*1 hour) 1100 hours

But did take 1075 hours

Direct labour efficiency variance in hours 25 hours

Standard rate per hour 22

Direct labour efficiency variance 550(F)

E)

Actual cost 6400

Budgeted cost(1000*6) 6000

Fixed overhead expenditure variance 400(A)

F)

5

3.3: Computation of variances

A)

1175kgs should cost(*20) 23500

but used 23260

MPV 240(F)

B)

1100 units should have used(*1kg) 1100kgs

But did use 1175 kgs

Usage variance in kgs 75 kgs(A)

Standard cost per kilogram 1500

C)

1075 hours 23650

But did cost 24420

Rate variance 770(A)

D)

1100 units should have taken (*1 hour) 1100 hours

But did take 1075 hours

Direct labour efficiency variance in hours 25 hours

Standard rate per hour 22

Direct labour efficiency variance 550(F)

E)

Actual cost 6400

Budgeted cost(1000*6) 6000

Fixed overhead expenditure variance 400(A)

F)

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

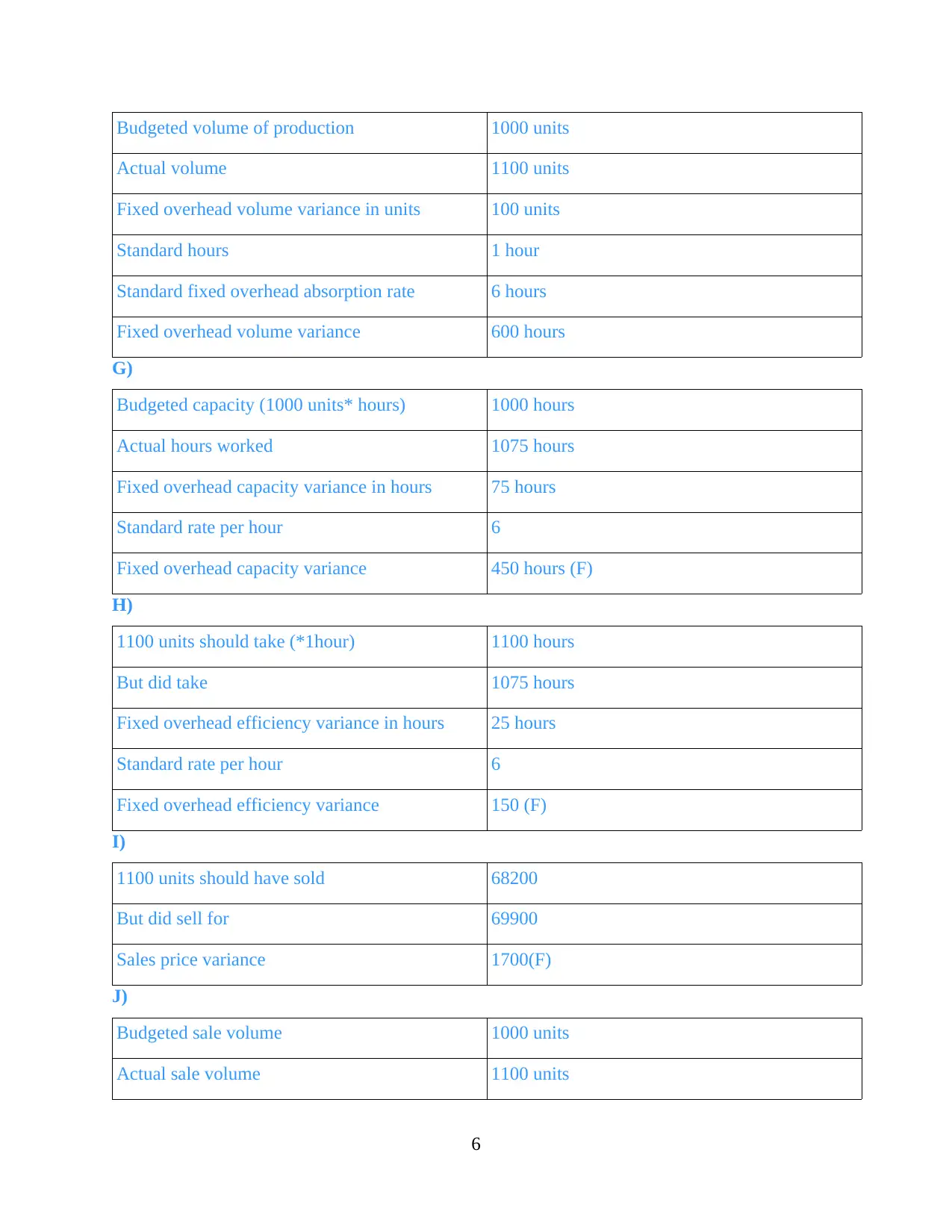

Budgeted volume of production 1000 units

Actual volume 1100 units

Fixed overhead volume variance in units 100 units

Standard hours 1 hour

Standard fixed overhead absorption rate 6 hours

Fixed overhead volume variance 600 hours

G)

Budgeted capacity (1000 units* hours) 1000 hours

Actual hours worked 1075 hours

Fixed overhead capacity variance in hours 75 hours

Standard rate per hour 6

Fixed overhead capacity variance 450 hours (F)

H)

1100 units should take (*1hour) 1100 hours

But did take 1075 hours

Fixed overhead efficiency variance in hours 25 hours

Standard rate per hour 6

Fixed overhead efficiency variance 150 (F)

I)

1100 units should have sold 68200

But did sell for 69900

Sales price variance 1700(F)

J)

Budgeted sale volume 1000 units

Actual sale volume 1100 units

6

Actual volume 1100 units

Fixed overhead volume variance in units 100 units

Standard hours 1 hour

Standard fixed overhead absorption rate 6 hours

Fixed overhead volume variance 600 hours

G)

Budgeted capacity (1000 units* hours) 1000 hours

Actual hours worked 1075 hours

Fixed overhead capacity variance in hours 75 hours

Standard rate per hour 6

Fixed overhead capacity variance 450 hours (F)

H)

1100 units should take (*1hour) 1100 hours

But did take 1075 hours

Fixed overhead efficiency variance in hours 25 hours

Standard rate per hour 6

Fixed overhead efficiency variance 150 (F)

I)

1100 units should have sold 68200

But did sell for 69900

Sales price variance 1700(F)

J)

Budgeted sale volume 1000 units

Actual sale volume 1100 units

6

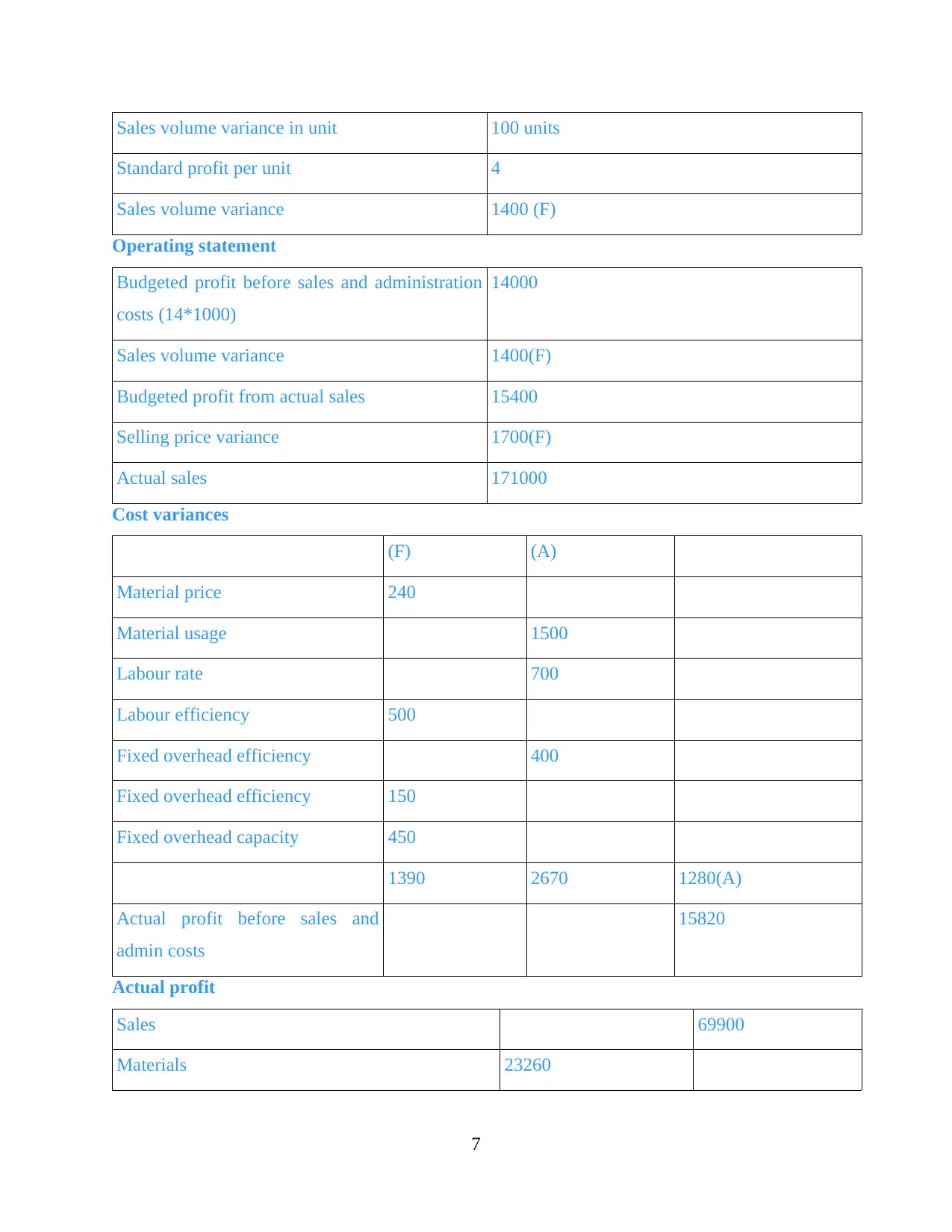

Sales volume variance in unit 100 units

Standard profit per unit 4

Sales volume variance 1400 (F)

Operating statement

Budgeted profit before sales and administration

costs (14*1000)

14000

Sales volume variance 1400(F)

Budgeted profit from actual sales 15400

Selling price variance 1700(F)

Actual sales 171000

Cost variances

(F) (A)

Material price 240

Material usage 1500

Labour rate 700

Labour efficiency 500

Fixed overhead efficiency 400

Fixed overhead efficiency 150

Fixed overhead capacity 450

1390 2670 1280(A)

Actual profit before sales and

admin costs

15820

Actual profit

Sales 69900

Materials 23260

7

Standard profit per unit 4

Sales volume variance 1400 (F)

Operating statement

Budgeted profit before sales and administration

costs (14*1000)

14000

Sales volume variance 1400(F)

Budgeted profit from actual sales 15400

Selling price variance 1700(F)

Actual sales 171000

Cost variances

(F) (A)

Material price 240

Material usage 1500

Labour rate 700

Labour efficiency 500

Fixed overhead efficiency 400

Fixed overhead efficiency 150

Fixed overhead capacity 450

1390 2670 1280(A)

Actual profit before sales and

admin costs

15820

Actual profit

Sales 69900

Materials 23260

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Labours 24420

Fixed overhead 6400

54080

Actual profit before sales and admin costs 15820

Variance: It is known as comparison among budgeted or forecasted cost of total income

generate from various activities.

Sales variance: With the above calculation, it has been seen that standard price per units

is identify as 62. Actual sale was incurred to 63.54 per units. The results are more favourable. At

1100units of actual output they are selling 69900.

Direct labour: Total standard units of labour is about 22 per units. But it was actually

occurring to be 22.72. Is provide adverse outcomes because actual cost is more than the standard

units.

Direct material: They are able to meet the standard units which 20 per units. Under this

situation they are at favourable situations.

Fixed overhead: With total overhead cost of 6400. They are charged with 6 per units but

it is actually occurring as 5.8 per units.

TASK 3

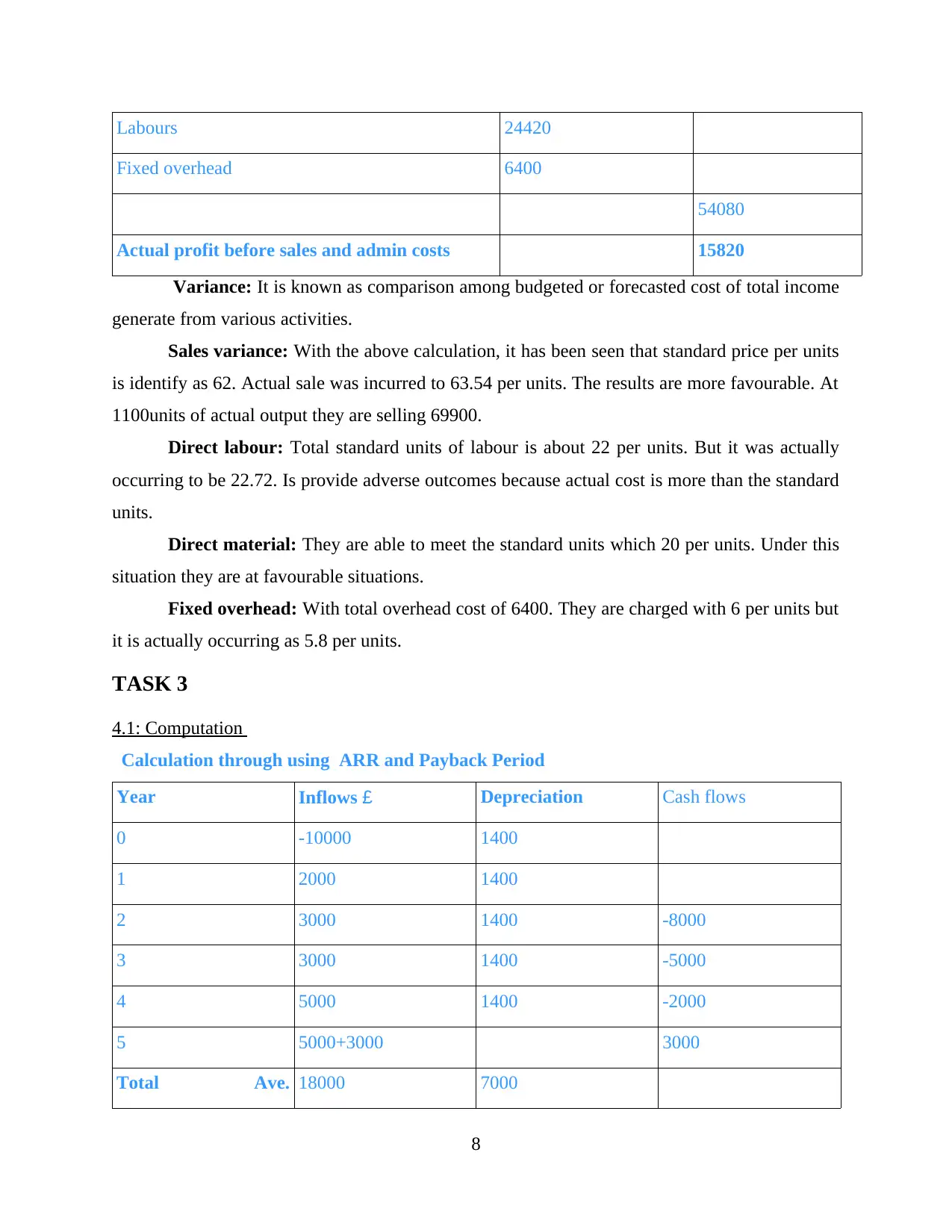

4.1: Computation

Calculation through using ARR and Payback Period

Year Inflows £ Depreciation Cash flows

0 -10000 1400

1 2000 1400

2 3000 1400 -8000

3 3000 1400 -5000

4 5000 1400 -2000

5 5000+3000 3000

Total Ave. 18000 7000

8

Fixed overhead 6400

54080

Actual profit before sales and admin costs 15820

Variance: It is known as comparison among budgeted or forecasted cost of total income

generate from various activities.

Sales variance: With the above calculation, it has been seen that standard price per units

is identify as 62. Actual sale was incurred to 63.54 per units. The results are more favourable. At

1100units of actual output they are selling 69900.

Direct labour: Total standard units of labour is about 22 per units. But it was actually

occurring to be 22.72. Is provide adverse outcomes because actual cost is more than the standard

units.

Direct material: They are able to meet the standard units which 20 per units. Under this

situation they are at favourable situations.

Fixed overhead: With total overhead cost of 6400. They are charged with 6 per units but

it is actually occurring as 5.8 per units.

TASK 3

4.1: Computation

Calculation through using ARR and Payback Period

Year Inflows £ Depreciation Cash flows

0 -10000 1400

1 2000 1400

2 3000 1400 -8000

3 3000 1400 -5000

4 5000 1400 -2000

5 5000+3000 3000

Total Ave. 18000 7000

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting Income

ARR 33.00%

Payback period 3.4 years

ARR= Averages Accounting Profit

Average investment

Average accounting profit = Total cash flows - depreciation/project life

= 2000+3000+3000+5000+5000-7000/2

= 2200

Average investment = Initial investment+scrap value/2

= 10000+3000/2

= 6500

ARR = 2200/6500*100

= 33%

Payback period method: Initial investment

Cash inflows per period

PBP = 3+2000/5000

= 3.4 years

Working note:

1. Evaluation of Depreciation:

Initial investment = 10,000

Total life =5 years

Salvage value = 3,000

Depreciation = 10000-3000 = 7000

4.2: Importance of values

It is crucial for every business to create effective results by formulating accountable

information. The profit of the company is totally depending upon amount of capital invested

under a given project (Fee, Hadlock and Pierce, 2013). In above situation, total initial amount of

10000 is being invested which is useful for the purpose of making budgets.

9

ARR 33.00%

Payback period 3.4 years

ARR= Averages Accounting Profit

Average investment

Average accounting profit = Total cash flows - depreciation/project life

= 2000+3000+3000+5000+5000-7000/2

= 2200

Average investment = Initial investment+scrap value/2

= 10000+3000/2

= 6500

ARR = 2200/6500*100

= 33%

Payback period method: Initial investment

Cash inflows per period

PBP = 3+2000/5000

= 3.4 years

Working note:

1. Evaluation of Depreciation:

Initial investment = 10,000

Total life =5 years

Salvage value = 3,000

Depreciation = 10000-3000 = 7000

4.2: Importance of values

It is crucial for every business to create effective results by formulating accountable

information. The profit of the company is totally depending upon amount of capital invested

under a given project (Fee, Hadlock and Pierce, 2013). In above situation, total initial amount of

10000 is being invested which is useful for the purpose of making budgets.

9

According to the information collected by using ARR, long term impacts can be

analysing in more specific manner.

Strength of ARR:

ARR is based on accounting data, therefore, other special report is not needed for

determining ARR.

It is easy to calculate and understand.

Weakness of ARR:

It ignores the time value of money.

It also does not take into account the cash flow from investments

Strength of payback period:

This method offers plenty of benefits such as a company has certain time need in terms of

how long a project will take to pay for their investments.

Weakness of payback period: It used to deliver to no data regarding the rate of return

while comparing two or more project options.

4.3: Value require to examine viability in a project

With the use of ARR which is use as an unaccounted capital investment tools used in

order to analyse projects those are having minimum recovery period. These are generally used

for the purpose of ranking. According to the amount of return they are getting in initial time is

marked as 1st. In case of payback period minimum amount of time use by a project is marked as

first rank. There are various sources of finance available for the company. it can be collected

from internal as well as external sources.

Internal sources:

Owners investments

Retained profits

Sale of stock

External sources:

Bank loan

Equity share

Debenture

Venture capital

10

analysing in more specific manner.

Strength of ARR:

ARR is based on accounting data, therefore, other special report is not needed for

determining ARR.

It is easy to calculate and understand.

Weakness of ARR:

It ignores the time value of money.

It also does not take into account the cash flow from investments

Strength of payback period:

This method offers plenty of benefits such as a company has certain time need in terms of

how long a project will take to pay for their investments.

Weakness of payback period: It used to deliver to no data regarding the rate of return

while comparing two or more project options.

4.3: Value require to examine viability in a project

With the use of ARR which is use as an unaccounted capital investment tools used in

order to analyse projects those are having minimum recovery period. These are generally used

for the purpose of ranking. According to the amount of return they are getting in initial time is

marked as 1st. In case of payback period minimum amount of time use by a project is marked as

first rank. There are various sources of finance available for the company. it can be collected

from internal as well as external sources.

Internal sources:

Owners investments

Retained profits

Sale of stock

External sources:

Bank loan

Equity share

Debenture

Venture capital

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.