Financial Performance Analysis of Gulf Stone Company SAOG (ECM05EKM)

VerifiedAdded on 2023/01/19

|21

|5218

|76

Report

AI Summary

This report presents a comprehensive financial analysis of Gulf Stone Company SAOG, a company listed on the Muscat Securities Market (MSM). The analysis begins with an evaluation of the company's financial performance over three years, utilizing horizontal and vertical analysis techniques on both the income statement and balance sheet to assess profitability and financial position. The report then delves into capital budgeting, applying the Internal Rate of Return (IRR) method to evaluate potential projects and provides recommendations based on literature reviews and non-financial factors. Finally, it conducts a cost-volume-profit (CVP) analysis to assess its role in business decision-making. The report incorporates literature reviews to support its findings and recommendations, offering a detailed examination of the company's financial health and potential investment strategies.

Page 1 of 21

Financial Analysis for Managers (ECM05EKM)

Financial Analysis for Managers (ECM05EKM)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Page 2 of 21

Contents

Introduction......................................................................................................................................3

Part 1: Evaluation of financial performance of a company listed in the Muscat Securities (MSM)

through using the trend analysis......................................................................................................4

Introduction..................................................................................................................................4

Task A: Comparative Income Statement and balance sheet for last 3 years through using

Horizontal and Vertical Analysis techniques...............................................................................4

A.1: Income Statement-Profitability Position..............................................................................4

A.1.1: Vertical Analysis of Income Statement............................................................................4

A.1.2: Horizontal Analysis of Income Statement........................................................................5

A.2: Balance sheet – financial position........................................................................................7

A.2.1: Vertical Analysis of Balance Sheet...................................................................................7

A.2.2: Horizontal Analysis of Balance Sheet..............................................................................9

Task B: Analysis and Literature Review...................................................................................12

B.1: Literature Review about Vertical and Horizontal Analysis...............................................12

B.2: Profitability Position..........................................................................................................12

B.3: Financial Position...............................................................................................................12

Summary....................................................................................................................................13

Part 2: Capital Budgeting...............................................................................................................14

Task A: Application of Internal Rate of Return in the given Scenario......................................14

Task B: Recommendations through using literature review......................................................15

B.1: Literature review of Internal Rate of Return......................................................................15

B.2: Recommendations based on calculations, LR and Non- financial factors.........................16

Task C: Analysis with literature review.....................................................................................16

C.1: Analysis based on Literature Review and other non-financial factors provided in the

scenario......................................................................................................................................16

C.2: Analysis based on literature review of other relevant non-financial factors......................17

Part 3: Cost-volume-profit analysis..............................................................................................18

Task A: Calculations..................................................................................................................18

Task B: Most Profitable Scenario..............................................................................................19

Task C: Evaluate the role of CVP analysis in taking business decisions..................................19

Contents

Introduction......................................................................................................................................3

Part 1: Evaluation of financial performance of a company listed in the Muscat Securities (MSM)

through using the trend analysis......................................................................................................4

Introduction..................................................................................................................................4

Task A: Comparative Income Statement and balance sheet for last 3 years through using

Horizontal and Vertical Analysis techniques...............................................................................4

A.1: Income Statement-Profitability Position..............................................................................4

A.1.1: Vertical Analysis of Income Statement............................................................................4

A.1.2: Horizontal Analysis of Income Statement........................................................................5

A.2: Balance sheet – financial position........................................................................................7

A.2.1: Vertical Analysis of Balance Sheet...................................................................................7

A.2.2: Horizontal Analysis of Balance Sheet..............................................................................9

Task B: Analysis and Literature Review...................................................................................12

B.1: Literature Review about Vertical and Horizontal Analysis...............................................12

B.2: Profitability Position..........................................................................................................12

B.3: Financial Position...............................................................................................................12

Summary....................................................................................................................................13

Part 2: Capital Budgeting...............................................................................................................14

Task A: Application of Internal Rate of Return in the given Scenario......................................14

Task B: Recommendations through using literature review......................................................15

B.1: Literature review of Internal Rate of Return......................................................................15

B.2: Recommendations based on calculations, LR and Non- financial factors.........................16

Task C: Analysis with literature review.....................................................................................16

C.1: Analysis based on Literature Review and other non-financial factors provided in the

scenario......................................................................................................................................16

C.2: Analysis based on literature review of other relevant non-financial factors......................17

Part 3: Cost-volume-profit analysis..............................................................................................18

Task A: Calculations..................................................................................................................18

Task B: Most Profitable Scenario..............................................................................................19

Task C: Evaluate the role of CVP analysis in taking business decisions..................................19

Page 3 of 21

References......................................................................................................................................20

References......................................................................................................................................20

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Page 4 of 21

Introduction

The present report has been developed for providing an understanding of the various

financial analytical and investment appraisal techniques that are used for developing an

understanding of the present as well as future growth prospects of a company. In this context, the

report has primarily carried out evaluation of the financial performance of a company listed in

the Muscat Securities Exchange (MSM). This is done by presenting a comparison of the income

statements and the balance sheet for 3 years with the use of horizontal and vertical analysis. This

is followed by analyzing the profitability and financial position of the selected company and

providing recommendations to improve its financial position. This is followed by presenting an

evaluation of the investment technique of Internal Rate of Return (IRR) for evaluating the

feasibility of projects planned to be undertaken by City Cinemas. Lastly, it has conducted a cost-

volume-profit analysis for presenting its usefulness in taking business decisions.

Introduction

The present report has been developed for providing an understanding of the various

financial analytical and investment appraisal techniques that are used for developing an

understanding of the present as well as future growth prospects of a company. In this context, the

report has primarily carried out evaluation of the financial performance of a company listed in

the Muscat Securities Exchange (MSM). This is done by presenting a comparison of the income

statements and the balance sheet for 3 years with the use of horizontal and vertical analysis. This

is followed by analyzing the profitability and financial position of the selected company and

providing recommendations to improve its financial position. This is followed by presenting an

evaluation of the investment technique of Internal Rate of Return (IRR) for evaluating the

feasibility of projects planned to be undertaken by City Cinemas. Lastly, it has conducted a cost-

volume-profit analysis for presenting its usefulness in taking business decisions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Page 5 of 21

Part 1: Evaluation of financial performance of a company listed in the Muscat Securities

(MSM) through using the trend analysis

Introduction

This part of the report has presented a financial analysis of the selected company known

as Gulf Stone Company SAOG. This has been carried out by developing and presenting a

comparison of the income and balance sheet for the company over a period of 3 years with the

use of horizontal and vertical analysis technique. This is followed by conducting an examination

of the profitability and financial position of the selected company and providing it

recommendations on the basis of overall findings generated from the literature review.

The case company selected is Gulf Stone Company SAOG, that is involved in

manufacturing and selling of quartz based engineered stone products. The main products

developed by the company include quartz slabs, tiles, mirror, glass effects, color chips and

metallic effects. The products manufactured by the company are used in developing floors,

interior of walls, tables, swimming pools, corporate offices and other types of construction (Gulf

Stone company, 2018).

Task A: Comparative Income Statement and balance sheet for last 3 years through using

Horizontal and Vertical Analysis techniques

A.1: Income Statement-Profitability Position

A.1.1: Vertical Analysis of Income Statement

Golf Stone Company SAOG

Comparative Income Statement

For years Ended 31 st December 2018

Income Statement for three years

Particulars 2016 2017 2018

RO RO RO

Net Revenue 3320618.00 3295489.00 4986748.00

Cost of sales (2915590.00) (2628439.00) (3832091.00)

Gross Profit 405028.00 667050.00 1154657.00

Operating Expenses/Income

Allowance / reversal on impairment

of financial assets - net (38262.00)

General and administrative expenses (331408.00) (332200.00) (345035.00)

Selling and marketing expense (323040.00) (309194.00) (352040.00)

Other income 3406.00 26697.00 21450.00

Profit from operations (284276.00) 52353.00 479032.00

Part 1: Evaluation of financial performance of a company listed in the Muscat Securities

(MSM) through using the trend analysis

Introduction

This part of the report has presented a financial analysis of the selected company known

as Gulf Stone Company SAOG. This has been carried out by developing and presenting a

comparison of the income and balance sheet for the company over a period of 3 years with the

use of horizontal and vertical analysis technique. This is followed by conducting an examination

of the profitability and financial position of the selected company and providing it

recommendations on the basis of overall findings generated from the literature review.

The case company selected is Gulf Stone Company SAOG, that is involved in

manufacturing and selling of quartz based engineered stone products. The main products

developed by the company include quartz slabs, tiles, mirror, glass effects, color chips and

metallic effects. The products manufactured by the company are used in developing floors,

interior of walls, tables, swimming pools, corporate offices and other types of construction (Gulf

Stone company, 2018).

Task A: Comparative Income Statement and balance sheet for last 3 years through using

Horizontal and Vertical Analysis techniques

A.1: Income Statement-Profitability Position

A.1.1: Vertical Analysis of Income Statement

Golf Stone Company SAOG

Comparative Income Statement

For years Ended 31 st December 2018

Income Statement for three years

Particulars 2016 2017 2018

RO RO RO

Net Revenue 3320618.00 3295489.00 4986748.00

Cost of sales (2915590.00) (2628439.00) (3832091.00)

Gross Profit 405028.00 667050.00 1154657.00

Operating Expenses/Income

Allowance / reversal on impairment

of financial assets - net (38262.00)

General and administrative expenses (331408.00) (332200.00) (345035.00)

Selling and marketing expense (323040.00) (309194.00) (352040.00)

Other income 3406.00 26697.00 21450.00

Profit from operations (284276.00) 52353.00 479032.00

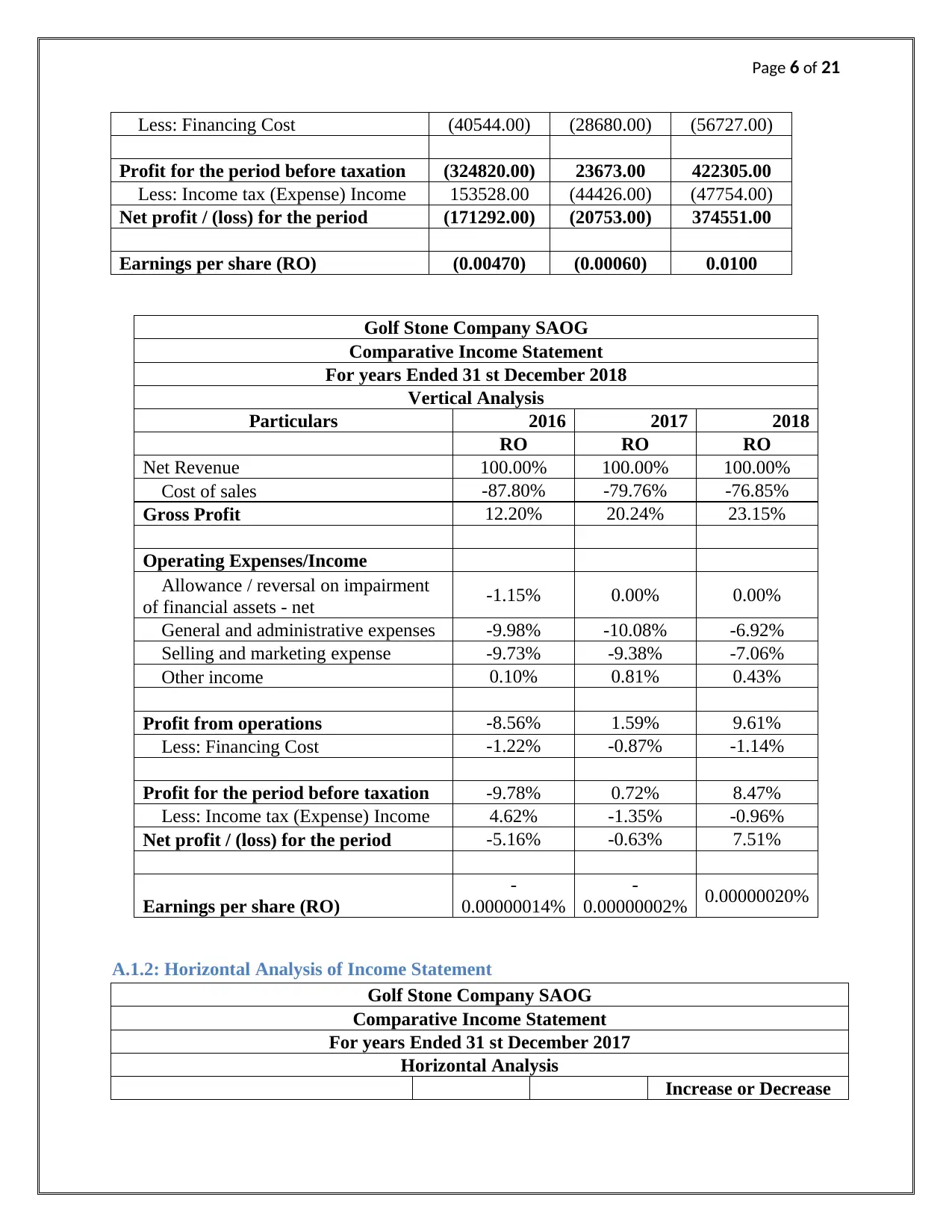

Page 6 of 21

Less: Financing Cost (40544.00) (28680.00) (56727.00)

Profit for the period before taxation (324820.00) 23673.00 422305.00

Less: Income tax (Expense) Income 153528.00 (44426.00) (47754.00)

Net profit / (loss) for the period (171292.00) (20753.00) 374551.00

Earnings per share (RO) (0.00470) (0.00060) 0.0100

Golf Stone Company SAOG

Comparative Income Statement

For years Ended 31 st December 2018

Vertical Analysis

Particulars 2016 2017 2018

RO RO RO

Net Revenue 100.00% 100.00% 100.00%

Cost of sales -87.80% -79.76% -76.85%

Gross Profit 12.20% 20.24% 23.15%

Operating Expenses/Income

Allowance / reversal on impairment

of financial assets - net -1.15% 0.00% 0.00%

General and administrative expenses -9.98% -10.08% -6.92%

Selling and marketing expense -9.73% -9.38% -7.06%

Other income 0.10% 0.81% 0.43%

Profit from operations -8.56% 1.59% 9.61%

Less: Financing Cost -1.22% -0.87% -1.14%

Profit for the period before taxation -9.78% 0.72% 8.47%

Less: Income tax (Expense) Income 4.62% -1.35% -0.96%

Net profit / (loss) for the period -5.16% -0.63% 7.51%

Earnings per share (RO)

-

0.00000014%

-

0.00000002% 0.00000020%

A.1.2: Horizontal Analysis of Income Statement

Golf Stone Company SAOG

Comparative Income Statement

For years Ended 31 st December 2017

Horizontal Analysis

Increase or Decrease

Less: Financing Cost (40544.00) (28680.00) (56727.00)

Profit for the period before taxation (324820.00) 23673.00 422305.00

Less: Income tax (Expense) Income 153528.00 (44426.00) (47754.00)

Net profit / (loss) for the period (171292.00) (20753.00) 374551.00

Earnings per share (RO) (0.00470) (0.00060) 0.0100

Golf Stone Company SAOG

Comparative Income Statement

For years Ended 31 st December 2018

Vertical Analysis

Particulars 2016 2017 2018

RO RO RO

Net Revenue 100.00% 100.00% 100.00%

Cost of sales -87.80% -79.76% -76.85%

Gross Profit 12.20% 20.24% 23.15%

Operating Expenses/Income

Allowance / reversal on impairment

of financial assets - net -1.15% 0.00% 0.00%

General and administrative expenses -9.98% -10.08% -6.92%

Selling and marketing expense -9.73% -9.38% -7.06%

Other income 0.10% 0.81% 0.43%

Profit from operations -8.56% 1.59% 9.61%

Less: Financing Cost -1.22% -0.87% -1.14%

Profit for the period before taxation -9.78% 0.72% 8.47%

Less: Income tax (Expense) Income 4.62% -1.35% -0.96%

Net profit / (loss) for the period -5.16% -0.63% 7.51%

Earnings per share (RO)

-

0.00000014%

-

0.00000002% 0.00000020%

A.1.2: Horizontal Analysis of Income Statement

Golf Stone Company SAOG

Comparative Income Statement

For years Ended 31 st December 2017

Horizontal Analysis

Increase or Decrease

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Page 7 of 21

Particulars 2017 2016 Amount Percent

RO RO

Net Revenue 3295489.00 4986748.00 (1691259.00

) -33.92%

Cost of sales

(2628439.00

)

(3832091.00

) 1203652.00 -31.41%

Gross Profit 667050.00 1154657.00 (487607.00) -42.23%

Operating Expenses/Income

Allowance / reversal on

impairment of financial assets - net

General and administrative

expenses (332200.00) (345035.00) 12835.00 -3.72%

Selling and marketing expense (309194.00) (352040.00) 42846.00 -12.17%

Other income 26697.00 21450.00 5247.00 24.46%

Profit from operations 52353.00 479032.00 (426679.00) -89.07%

Less: Financing Cost (28680.00) (56727.00) 28047.00 -49.44%

Profit for the period before

taxation 23673.00 422305.00 (398632.00) -94.39%

Less: Income tax (Expense)

Income (44426.00) (47754.00) 3328.00

Net profit / (loss) for the period

(20753.00) 374551.00 (395304.00)

-

105.54

%

Earnings per share (RO)

(0.00060) 0.0100 (0.01060)

-

106.00

%

Golf Stone Company SAOG

Comparative Income Statement

For years Ended 31 st December 2018

Horizontal Analysis

Increase or Decrease

Particulars 2018 2017 Amount Percent

RO RO

Net Revenue 3320618.00 3295489.00 25129.00 0.76%

Cost of sales

(2915590.00

)

(2628439.00

)

(287151.00

) 10.92%

Gross Profit 405028.00 667050.00 (262022.00

) -39.28%

Particulars 2017 2016 Amount Percent

RO RO

Net Revenue 3295489.00 4986748.00 (1691259.00

) -33.92%

Cost of sales

(2628439.00

)

(3832091.00

) 1203652.00 -31.41%

Gross Profit 667050.00 1154657.00 (487607.00) -42.23%

Operating Expenses/Income

Allowance / reversal on

impairment of financial assets - net

General and administrative

expenses (332200.00) (345035.00) 12835.00 -3.72%

Selling and marketing expense (309194.00) (352040.00) 42846.00 -12.17%

Other income 26697.00 21450.00 5247.00 24.46%

Profit from operations 52353.00 479032.00 (426679.00) -89.07%

Less: Financing Cost (28680.00) (56727.00) 28047.00 -49.44%

Profit for the period before

taxation 23673.00 422305.00 (398632.00) -94.39%

Less: Income tax (Expense)

Income (44426.00) (47754.00) 3328.00

Net profit / (loss) for the period

(20753.00) 374551.00 (395304.00)

-

105.54

%

Earnings per share (RO)

(0.00060) 0.0100 (0.01060)

-

106.00

%

Golf Stone Company SAOG

Comparative Income Statement

For years Ended 31 st December 2018

Horizontal Analysis

Increase or Decrease

Particulars 2018 2017 Amount Percent

RO RO

Net Revenue 3320618.00 3295489.00 25129.00 0.76%

Cost of sales

(2915590.00

)

(2628439.00

)

(287151.00

) 10.92%

Gross Profit 405028.00 667050.00 (262022.00

) -39.28%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Page 8 of 21

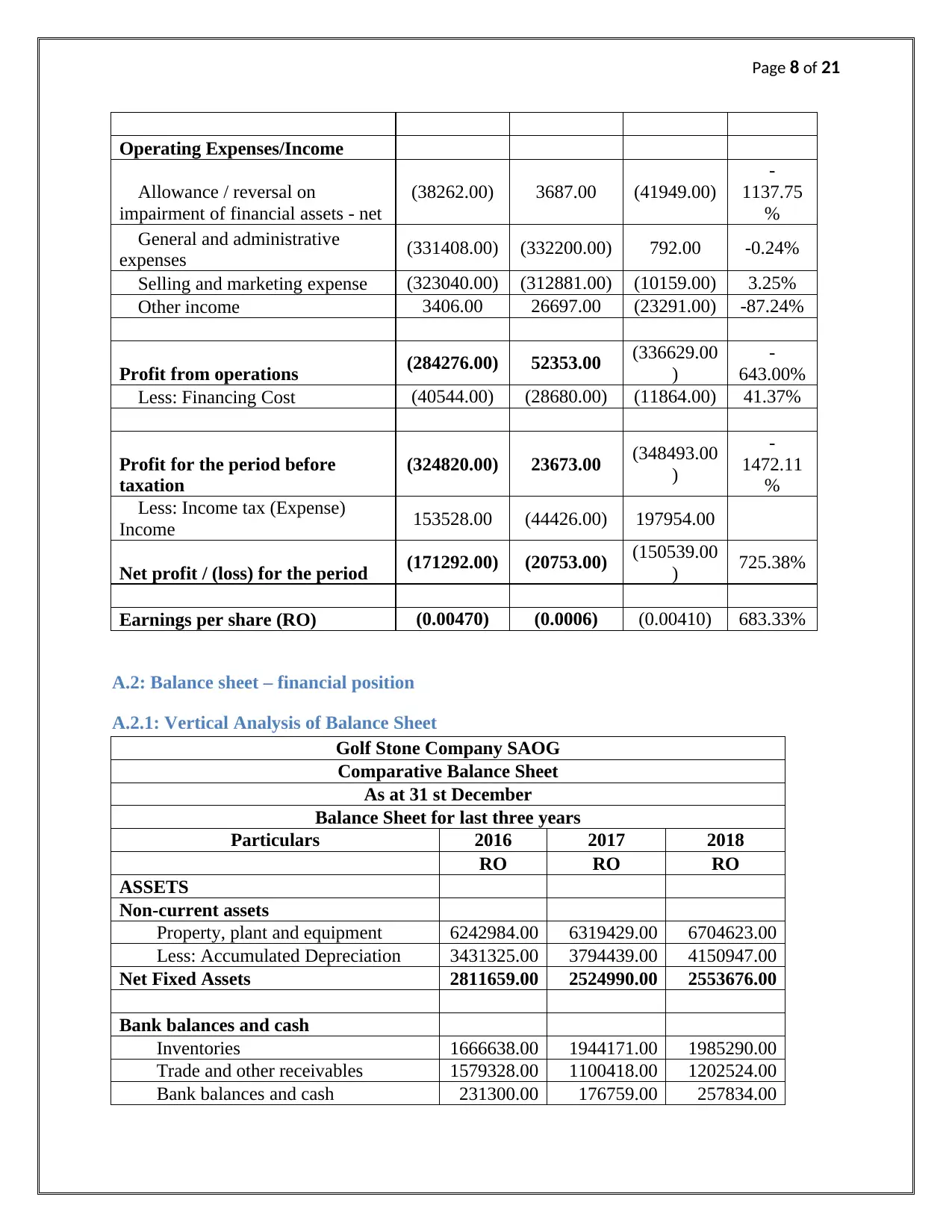

Operating Expenses/Income

Allowance / reversal on

impairment of financial assets - net

(38262.00) 3687.00 (41949.00)

-

1137.75

%

General and administrative

expenses (331408.00) (332200.00) 792.00 -0.24%

Selling and marketing expense (323040.00) (312881.00) (10159.00) 3.25%

Other income 3406.00 26697.00 (23291.00) -87.24%

Profit from operations (284276.00) 52353.00 (336629.00

)

-

643.00%

Less: Financing Cost (40544.00) (28680.00) (11864.00) 41.37%

Profit for the period before

taxation

(324820.00) 23673.00 (348493.00

)

-

1472.11

%

Less: Income tax (Expense)

Income 153528.00 (44426.00) 197954.00

Net profit / (loss) for the period (171292.00) (20753.00) (150539.00

) 725.38%

Earnings per share (RO) (0.00470) (0.0006) (0.00410) 683.33%

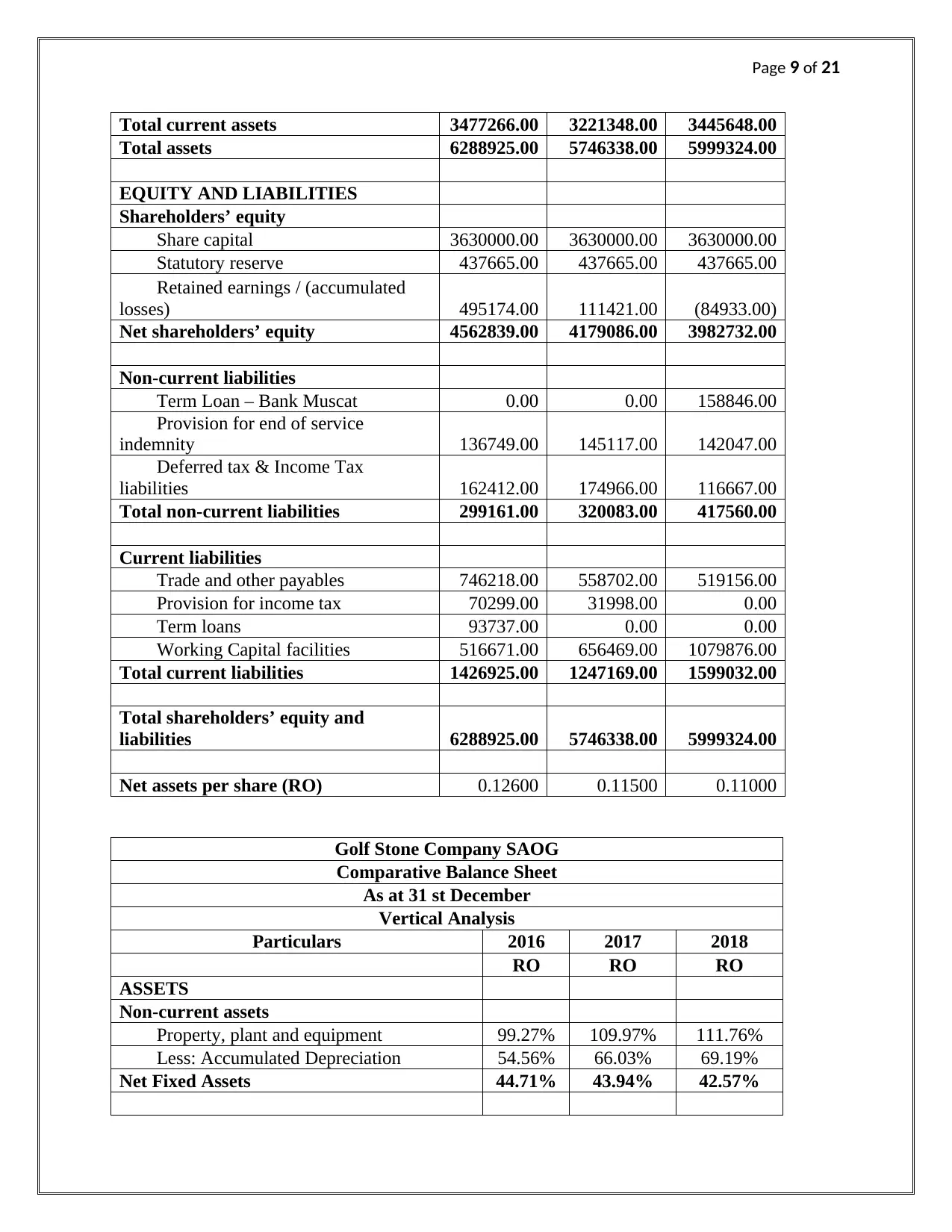

A.2: Balance sheet – financial position

A.2.1: Vertical Analysis of Balance Sheet

Golf Stone Company SAOG

Comparative Balance Sheet

As at 31 st December

Balance Sheet for last three years

Particulars 2016 2017 2018

RO RO RO

ASSETS

Non-current assets

Property, plant and equipment 6242984.00 6319429.00 6704623.00

Less: Accumulated Depreciation 3431325.00 3794439.00 4150947.00

Net Fixed Assets 2811659.00 2524990.00 2553676.00

Bank balances and cash

Inventories 1666638.00 1944171.00 1985290.00

Trade and other receivables 1579328.00 1100418.00 1202524.00

Bank balances and cash 231300.00 176759.00 257834.00

Operating Expenses/Income

Allowance / reversal on

impairment of financial assets - net

(38262.00) 3687.00 (41949.00)

-

1137.75

%

General and administrative

expenses (331408.00) (332200.00) 792.00 -0.24%

Selling and marketing expense (323040.00) (312881.00) (10159.00) 3.25%

Other income 3406.00 26697.00 (23291.00) -87.24%

Profit from operations (284276.00) 52353.00 (336629.00

)

-

643.00%

Less: Financing Cost (40544.00) (28680.00) (11864.00) 41.37%

Profit for the period before

taxation

(324820.00) 23673.00 (348493.00

)

-

1472.11

%

Less: Income tax (Expense)

Income 153528.00 (44426.00) 197954.00

Net profit / (loss) for the period (171292.00) (20753.00) (150539.00

) 725.38%

Earnings per share (RO) (0.00470) (0.0006) (0.00410) 683.33%

A.2: Balance sheet – financial position

A.2.1: Vertical Analysis of Balance Sheet

Golf Stone Company SAOG

Comparative Balance Sheet

As at 31 st December

Balance Sheet for last three years

Particulars 2016 2017 2018

RO RO RO

ASSETS

Non-current assets

Property, plant and equipment 6242984.00 6319429.00 6704623.00

Less: Accumulated Depreciation 3431325.00 3794439.00 4150947.00

Net Fixed Assets 2811659.00 2524990.00 2553676.00

Bank balances and cash

Inventories 1666638.00 1944171.00 1985290.00

Trade and other receivables 1579328.00 1100418.00 1202524.00

Bank balances and cash 231300.00 176759.00 257834.00

Page 9 of 21

Total current assets 3477266.00 3221348.00 3445648.00

Total assets 6288925.00 5746338.00 5999324.00

EQUITY AND LIABILITIES

Shareholders’ equity

Share capital 3630000.00 3630000.00 3630000.00

Statutory reserve 437665.00 437665.00 437665.00

Retained earnings / (accumulated

losses) 495174.00 111421.00 (84933.00)

Net shareholders’ equity 4562839.00 4179086.00 3982732.00

Non-current liabilities

Term Loan – Bank Muscat 0.00 0.00 158846.00

Provision for end of service

indemnity 136749.00 145117.00 142047.00

Deferred tax & Income Tax

liabilities 162412.00 174966.00 116667.00

Total non-current liabilities 299161.00 320083.00 417560.00

Current liabilities

Trade and other payables 746218.00 558702.00 519156.00

Provision for income tax 70299.00 31998.00 0.00

Term loans 93737.00 0.00 0.00

Working Capital facilities 516671.00 656469.00 1079876.00

Total current liabilities 1426925.00 1247169.00 1599032.00

Total shareholders’ equity and

liabilities 6288925.00 5746338.00 5999324.00

Net assets per share (RO) 0.12600 0.11500 0.11000

Golf Stone Company SAOG

Comparative Balance Sheet

As at 31 st December

Vertical Analysis

Particulars 2016 2017 2018

RO RO RO

ASSETS

Non-current assets

Property, plant and equipment 99.27% 109.97% 111.76%

Less: Accumulated Depreciation 54.56% 66.03% 69.19%

Net Fixed Assets 44.71% 43.94% 42.57%

Total current assets 3477266.00 3221348.00 3445648.00

Total assets 6288925.00 5746338.00 5999324.00

EQUITY AND LIABILITIES

Shareholders’ equity

Share capital 3630000.00 3630000.00 3630000.00

Statutory reserve 437665.00 437665.00 437665.00

Retained earnings / (accumulated

losses) 495174.00 111421.00 (84933.00)

Net shareholders’ equity 4562839.00 4179086.00 3982732.00

Non-current liabilities

Term Loan – Bank Muscat 0.00 0.00 158846.00

Provision for end of service

indemnity 136749.00 145117.00 142047.00

Deferred tax & Income Tax

liabilities 162412.00 174966.00 116667.00

Total non-current liabilities 299161.00 320083.00 417560.00

Current liabilities

Trade and other payables 746218.00 558702.00 519156.00

Provision for income tax 70299.00 31998.00 0.00

Term loans 93737.00 0.00 0.00

Working Capital facilities 516671.00 656469.00 1079876.00

Total current liabilities 1426925.00 1247169.00 1599032.00

Total shareholders’ equity and

liabilities 6288925.00 5746338.00 5999324.00

Net assets per share (RO) 0.12600 0.11500 0.11000

Golf Stone Company SAOG

Comparative Balance Sheet

As at 31 st December

Vertical Analysis

Particulars 2016 2017 2018

RO RO RO

ASSETS

Non-current assets

Property, plant and equipment 99.27% 109.97% 111.76%

Less: Accumulated Depreciation 54.56% 66.03% 69.19%

Net Fixed Assets 44.71% 43.94% 42.57%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Page 10 of 21

Bank balances and cash

Inventories 26.50% 33.83% 33.09%

Trade and other receivables 25.11% 19.15% 20.04%

Bank balances and cash 3.68% 3.08% 4.30%

Total current assets 55.29% 56.06% 57.43%

Total assets

100.00

% 100.00% 100.00%

EQUITY AND LIABILITIES

Shareholders’ equity

Share capital 57.72% 63.17% 60.51%

Statutory reserve 6.96% 7.62% 7.30%

Retained earnings / (accumulated losses) 7.87% 1.94% -1.42%

Net shareholders’ equity 72.55% 72.73% 66.39%

Non-current liabilities

Term Loan – Bank Muscat 0.00% 0.00% 2.65%

Provision for end of service indemnity 2.17% 2.53% 2.37%

Deferred tax & Income Tax liabilities 2.58% 3.04% 1.94%

Total non-current liabilities 4.76% 5.57% 6.96%

Current liabilities

Trade and other payables 11.87% 9.72% 8.65%

Provision for income tax 1.12% 0.56% 0.00%

Term loans 1.49% 0.00% 0.00%

Working Capital facilities 8.22% 11.42% 18.00%

Total current liabilities 22.69% 21.70% 26.65%

Total shareholders’ equity and liabilities

100.00

% 100.00% 100.00%

Net assets per share (RO) 0.12600 0.11500 0.11000

A.2.2: Horizontal Analysis of Balance Sheet

Golf Stone Company SAOG

Comparative Balance Sheet

As at 31 st December

Horizontal Analysis

Increase or Decrease

Particulars 2018 2017 Amount Percent

RO RO

Bank balances and cash

Inventories 26.50% 33.83% 33.09%

Trade and other receivables 25.11% 19.15% 20.04%

Bank balances and cash 3.68% 3.08% 4.30%

Total current assets 55.29% 56.06% 57.43%

Total assets

100.00

% 100.00% 100.00%

EQUITY AND LIABILITIES

Shareholders’ equity

Share capital 57.72% 63.17% 60.51%

Statutory reserve 6.96% 7.62% 7.30%

Retained earnings / (accumulated losses) 7.87% 1.94% -1.42%

Net shareholders’ equity 72.55% 72.73% 66.39%

Non-current liabilities

Term Loan – Bank Muscat 0.00% 0.00% 2.65%

Provision for end of service indemnity 2.17% 2.53% 2.37%

Deferred tax & Income Tax liabilities 2.58% 3.04% 1.94%

Total non-current liabilities 4.76% 5.57% 6.96%

Current liabilities

Trade and other payables 11.87% 9.72% 8.65%

Provision for income tax 1.12% 0.56% 0.00%

Term loans 1.49% 0.00% 0.00%

Working Capital facilities 8.22% 11.42% 18.00%

Total current liabilities 22.69% 21.70% 26.65%

Total shareholders’ equity and liabilities

100.00

% 100.00% 100.00%

Net assets per share (RO) 0.12600 0.11500 0.11000

A.2.2: Horizontal Analysis of Balance Sheet

Golf Stone Company SAOG

Comparative Balance Sheet

As at 31 st December

Horizontal Analysis

Increase or Decrease

Particulars 2018 2017 Amount Percent

RO RO

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Page 11 of 21

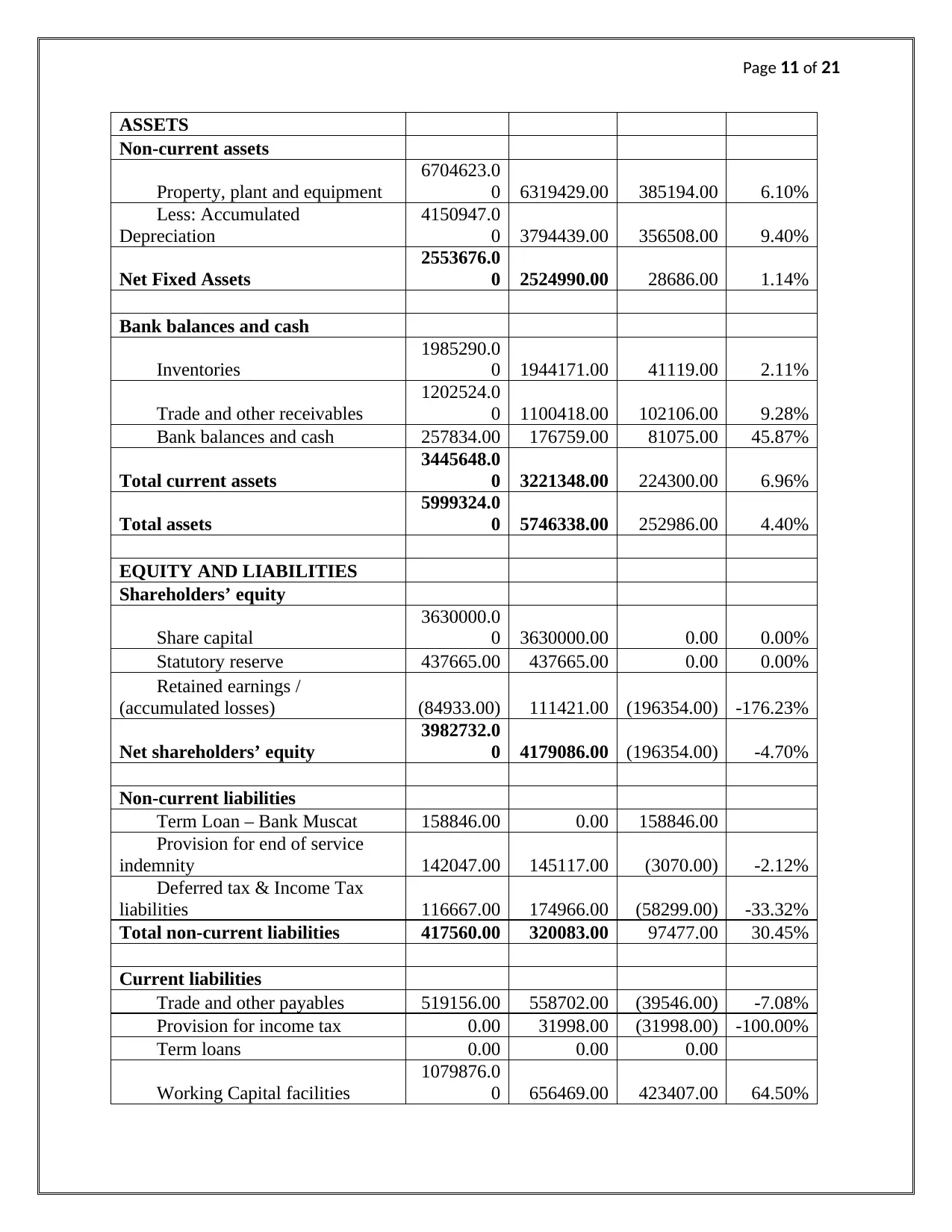

ASSETS

Non-current assets

Property, plant and equipment

6704623.0

0 6319429.00 385194.00 6.10%

Less: Accumulated

Depreciation

4150947.0

0 3794439.00 356508.00 9.40%

Net Fixed Assets

2553676.0

0 2524990.00 28686.00 1.14%

Bank balances and cash

Inventories

1985290.0

0 1944171.00 41119.00 2.11%

Trade and other receivables

1202524.0

0 1100418.00 102106.00 9.28%

Bank balances and cash 257834.00 176759.00 81075.00 45.87%

Total current assets

3445648.0

0 3221348.00 224300.00 6.96%

Total assets

5999324.0

0 5746338.00 252986.00 4.40%

EQUITY AND LIABILITIES

Shareholders’ equity

Share capital

3630000.0

0 3630000.00 0.00 0.00%

Statutory reserve 437665.00 437665.00 0.00 0.00%

Retained earnings /

(accumulated losses) (84933.00) 111421.00 (196354.00) -176.23%

Net shareholders’ equity

3982732.0

0 4179086.00 (196354.00) -4.70%

Non-current liabilities

Term Loan – Bank Muscat 158846.00 0.00 158846.00

Provision for end of service

indemnity 142047.00 145117.00 (3070.00) -2.12%

Deferred tax & Income Tax

liabilities 116667.00 174966.00 (58299.00) -33.32%

Total non-current liabilities 417560.00 320083.00 97477.00 30.45%

Current liabilities

Trade and other payables 519156.00 558702.00 (39546.00) -7.08%

Provision for income tax 0.00 31998.00 (31998.00) -100.00%

Term loans 0.00 0.00 0.00

Working Capital facilities

1079876.0

0 656469.00 423407.00 64.50%

ASSETS

Non-current assets

Property, plant and equipment

6704623.0

0 6319429.00 385194.00 6.10%

Less: Accumulated

Depreciation

4150947.0

0 3794439.00 356508.00 9.40%

Net Fixed Assets

2553676.0

0 2524990.00 28686.00 1.14%

Bank balances and cash

Inventories

1985290.0

0 1944171.00 41119.00 2.11%

Trade and other receivables

1202524.0

0 1100418.00 102106.00 9.28%

Bank balances and cash 257834.00 176759.00 81075.00 45.87%

Total current assets

3445648.0

0 3221348.00 224300.00 6.96%

Total assets

5999324.0

0 5746338.00 252986.00 4.40%

EQUITY AND LIABILITIES

Shareholders’ equity

Share capital

3630000.0

0 3630000.00 0.00 0.00%

Statutory reserve 437665.00 437665.00 0.00 0.00%

Retained earnings /

(accumulated losses) (84933.00) 111421.00 (196354.00) -176.23%

Net shareholders’ equity

3982732.0

0 4179086.00 (196354.00) -4.70%

Non-current liabilities

Term Loan – Bank Muscat 158846.00 0.00 158846.00

Provision for end of service

indemnity 142047.00 145117.00 (3070.00) -2.12%

Deferred tax & Income Tax

liabilities 116667.00 174966.00 (58299.00) -33.32%

Total non-current liabilities 417560.00 320083.00 97477.00 30.45%

Current liabilities

Trade and other payables 519156.00 558702.00 (39546.00) -7.08%

Provision for income tax 0.00 31998.00 (31998.00) -100.00%

Term loans 0.00 0.00 0.00

Working Capital facilities

1079876.0

0 656469.00 423407.00 64.50%

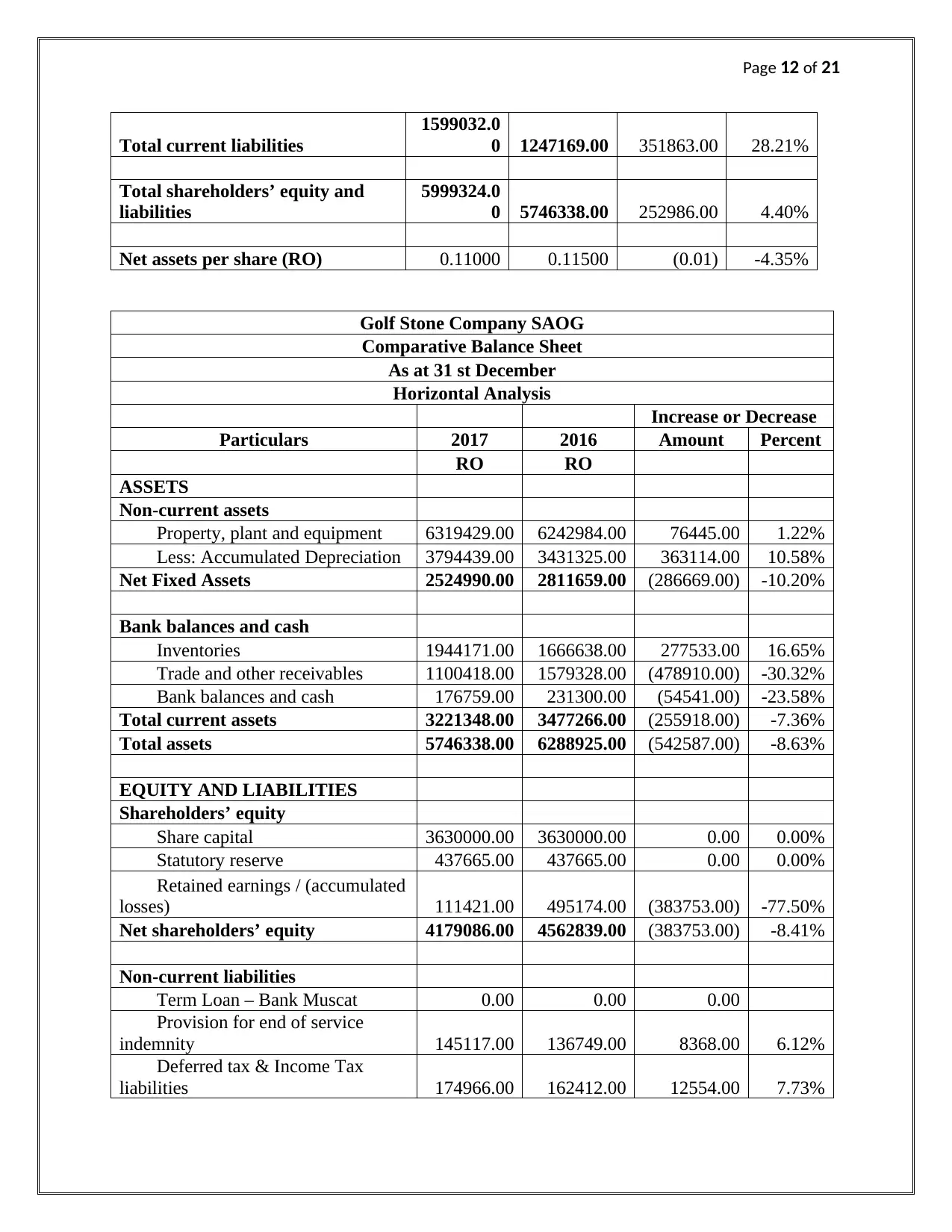

Page 12 of 21

Total current liabilities

1599032.0

0 1247169.00 351863.00 28.21%

Total shareholders’ equity and

liabilities

5999324.0

0 5746338.00 252986.00 4.40%

Net assets per share (RO) 0.11000 0.11500 (0.01) -4.35%

Golf Stone Company SAOG

Comparative Balance Sheet

As at 31 st December

Horizontal Analysis

Increase or Decrease

Particulars 2017 2016 Amount Percent

RO RO

ASSETS

Non-current assets

Property, plant and equipment 6319429.00 6242984.00 76445.00 1.22%

Less: Accumulated Depreciation 3794439.00 3431325.00 363114.00 10.58%

Net Fixed Assets 2524990.00 2811659.00 (286669.00) -10.20%

Bank balances and cash

Inventories 1944171.00 1666638.00 277533.00 16.65%

Trade and other receivables 1100418.00 1579328.00 (478910.00) -30.32%

Bank balances and cash 176759.00 231300.00 (54541.00) -23.58%

Total current assets 3221348.00 3477266.00 (255918.00) -7.36%

Total assets 5746338.00 6288925.00 (542587.00) -8.63%

EQUITY AND LIABILITIES

Shareholders’ equity

Share capital 3630000.00 3630000.00 0.00 0.00%

Statutory reserve 437665.00 437665.00 0.00 0.00%

Retained earnings / (accumulated

losses) 111421.00 495174.00 (383753.00) -77.50%

Net shareholders’ equity 4179086.00 4562839.00 (383753.00) -8.41%

Non-current liabilities

Term Loan – Bank Muscat 0.00 0.00 0.00

Provision for end of service

indemnity 145117.00 136749.00 8368.00 6.12%

Deferred tax & Income Tax

liabilities 174966.00 162412.00 12554.00 7.73%

Total current liabilities

1599032.0

0 1247169.00 351863.00 28.21%

Total shareholders’ equity and

liabilities

5999324.0

0 5746338.00 252986.00 4.40%

Net assets per share (RO) 0.11000 0.11500 (0.01) -4.35%

Golf Stone Company SAOG

Comparative Balance Sheet

As at 31 st December

Horizontal Analysis

Increase or Decrease

Particulars 2017 2016 Amount Percent

RO RO

ASSETS

Non-current assets

Property, plant and equipment 6319429.00 6242984.00 76445.00 1.22%

Less: Accumulated Depreciation 3794439.00 3431325.00 363114.00 10.58%

Net Fixed Assets 2524990.00 2811659.00 (286669.00) -10.20%

Bank balances and cash

Inventories 1944171.00 1666638.00 277533.00 16.65%

Trade and other receivables 1100418.00 1579328.00 (478910.00) -30.32%

Bank balances and cash 176759.00 231300.00 (54541.00) -23.58%

Total current assets 3221348.00 3477266.00 (255918.00) -7.36%

Total assets 5746338.00 6288925.00 (542587.00) -8.63%

EQUITY AND LIABILITIES

Shareholders’ equity

Share capital 3630000.00 3630000.00 0.00 0.00%

Statutory reserve 437665.00 437665.00 0.00 0.00%

Retained earnings / (accumulated

losses) 111421.00 495174.00 (383753.00) -77.50%

Net shareholders’ equity 4179086.00 4562839.00 (383753.00) -8.41%

Non-current liabilities

Term Loan – Bank Muscat 0.00 0.00 0.00

Provision for end of service

indemnity 145117.00 136749.00 8368.00 6.12%

Deferred tax & Income Tax

liabilities 174966.00 162412.00 12554.00 7.73%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.