Regression Analysis | Assignment-1

VerifiedAdded on 2022/09/12

|7

|872

|19

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Question 4

(a) Estimation of regression coefficients by least squares.

(i) Using R we obtainer estimates shown in table 1.

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 11.8563752 1.1049463 10.730 1.34e-05 ***

x1 -0.8790123 0.1846072 -4.762 0.00206 **

x2 -0.0001172 0.0423181 -0.003 0.99787

---

Therefore,

β0=11.8564, β1=−0.8790 and β2=−0.0001

(ii) The estimated 95% confidence interval is

−1.315539 ≤ β1 ≤−0.4424856

(iii) Given ( n−p ) ^σ 2

σ 2 χn− p

2

P ( χ(n− p ,0.975)

2 < ( n− p ) ^σ2

σ2 < χ(n− p ,0.025)

2

)=0.95

P ( χ(n −p , 0.975)

2

( n−p ) ^σ2 < 1

σ 2 < χ(n− p , 0.025)

2

( n− p ) ^σ 2 )=0.95

P ( ( n−p ) ^σ2

χ(n −p , 0.025)

2 < σ2 < ( n− p ) ^σ 2

χ(n− p , 0.97 5)

2 )=0.95

Therefore, the 95% confidence interval is

( n− p ) ^σ 2

χ(n− p , 0.025)

2 < σ2< ( n− p ) ^σ2

χ(n− p ,0. 975 )

2

(iv) Test the null hypothesis that β2=0.

H0 : β2=0

Ha : β2 ≠ 0

The test statistic is a t statistic (t) defined by

t= β2

SE with df = 10-2 = 8.

α=0.05

Decision, reject null hypothesis if |t | is greater than t8 ,0.025=2.306

t=−0.0001

0.0423 =−0.00236

Since, |t |=0.00236 is less than t8 ,0.025=2.306, fail to reject the null hypothesis

and conclude that β2=0.

(v) Test the null hypothesis that β1+10 β2=0

H0 : β1+10 β2=0

Ha : β1+10 β2 ≠ 0

The test statistic is a t statistic (t) defined by

(a) Estimation of regression coefficients by least squares.

(i) Using R we obtainer estimates shown in table 1.

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 11.8563752 1.1049463 10.730 1.34e-05 ***

x1 -0.8790123 0.1846072 -4.762 0.00206 **

x2 -0.0001172 0.0423181 -0.003 0.99787

---

Therefore,

β0=11.8564, β1=−0.8790 and β2=−0.0001

(ii) The estimated 95% confidence interval is

−1.315539 ≤ β1 ≤−0.4424856

(iii) Given ( n−p ) ^σ 2

σ 2 χn− p

2

P ( χ(n− p ,0.975)

2 < ( n− p ) ^σ2

σ2 < χ(n− p ,0.025)

2

)=0.95

P ( χ(n −p , 0.975)

2

( n−p ) ^σ2 < 1

σ 2 < χ(n− p , 0.025)

2

( n− p ) ^σ 2 )=0.95

P ( ( n−p ) ^σ2

χ(n −p , 0.025)

2 < σ2 < ( n− p ) ^σ 2

χ(n− p , 0.97 5)

2 )=0.95

Therefore, the 95% confidence interval is

( n− p ) ^σ 2

χ(n− p , 0.025)

2 < σ2< ( n− p ) ^σ2

χ(n− p ,0. 975 )

2

(iv) Test the null hypothesis that β2=0.

H0 : β2=0

Ha : β2 ≠ 0

The test statistic is a t statistic (t) defined by

t= β2

SE with df = 10-2 = 8.

α=0.05

Decision, reject null hypothesis if |t | is greater than t8 ,0.025=2.306

t=−0.0001

0.0423 =−0.00236

Since, |t |=0.00236 is less than t8 ,0.025=2.306, fail to reject the null hypothesis

and conclude that β2=0.

(v) Test the null hypothesis that β1+10 β2=0

H0 : β1+10 β2=0

Ha : β1+10 β2 ≠ 0

The test statistic is a t statistic (t) defined by

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

t= β1+10 β2

SE1+10 SE2

with df = 10-2 = 8.

α=0.05

Decision, reject null hypothesis if |t | is greater than t8 ,0.025=2.306

t= 11.8564−0.001

0.1846+0.423 =19.512

Since, |t |=19.512 is greater than t8 ,0.025=2.306, reject the null hypothesis and

conclude that β1+ 10 β2 ≠0.

(vi) x1 i is the best linear predictor of y, because the estimated slope coefficient is

statistically significant at 95% confidence level.

(b) Given the following

y1 j =β1 +e1 j

y2 j =β1 + β2 +e2 j

y3 j =β1+ β2 + β3+ e3 j

(i) Express this model in the form y=Zβ+e ,

Z=

(1 0 0

1 1 0

1 1 1)

(ii) Show that

^β1= y1 , ^β2= y2− y1, and ^β3= y3− y1

Let’s start with

y1 j =β1 +e1 j make e1 j the subject

e1 j= y1 j−β1 square both sides and sum

∑

j=1

5

e1 j

2 =∑

j =1

5

( y1 j− β1 )2

∑

j=1

5

e1 j

2 =∑

j =1

5

( y1 j

2−2 β1 y1 j+ β1

2 )

Let L=∑

j=1

5

e1 j

2

L=∑

j=1

5

( y1 j

2−2 β1 y1 j + β1

2 )

L=∑

j=1

5

y1 j

2−2 β1 ∑

j=1

5

y1 j +5 β1

2 differentiate with respect to β1 and equate to

zero.

∂ L

∂ β1

=−2 ∑

j=1

5

y1 j +10 β1=0

^β1=

∑

j =1

5

y1 j

5 = y1

Next,

SE1+10 SE2

with df = 10-2 = 8.

α=0.05

Decision, reject null hypothesis if |t | is greater than t8 ,0.025=2.306

t= 11.8564−0.001

0.1846+0.423 =19.512

Since, |t |=19.512 is greater than t8 ,0.025=2.306, reject the null hypothesis and

conclude that β1+ 10 β2 ≠0.

(vi) x1 i is the best linear predictor of y, because the estimated slope coefficient is

statistically significant at 95% confidence level.

(b) Given the following

y1 j =β1 +e1 j

y2 j =β1 + β2 +e2 j

y3 j =β1+ β2 + β3+ e3 j

(i) Express this model in the form y=Zβ+e ,

Z=

(1 0 0

1 1 0

1 1 1)

(ii) Show that

^β1= y1 , ^β2= y2− y1, and ^β3= y3− y1

Let’s start with

y1 j =β1 +e1 j make e1 j the subject

e1 j= y1 j−β1 square both sides and sum

∑

j=1

5

e1 j

2 =∑

j =1

5

( y1 j− β1 )2

∑

j=1

5

e1 j

2 =∑

j =1

5

( y1 j

2−2 β1 y1 j+ β1

2 )

Let L=∑

j=1

5

e1 j

2

L=∑

j=1

5

( y1 j

2−2 β1 y1 j + β1

2 )

L=∑

j=1

5

y1 j

2−2 β1 ∑

j=1

5

y1 j +5 β1

2 differentiate with respect to β1 and equate to

zero.

∂ L

∂ β1

=−2 ∑

j=1

5

y1 j +10 β1=0

^β1=

∑

j =1

5

y1 j

5 = y1

Next,

y2 j =β1 + β2 +e2 j make e1 j the subject

e2 j= y2 j− y1−β2 square both sides and sum

∑

j=1

5

e2 j

2 =∑

j =1

5

( y2 j− y1−β2 )2

∑

j=1

5

e2 j

2 =∑

j =1

5

( y2 j

2−2 ( y1−β2 ) y2 j+ ( y1−β2 )2

)

Let L=∑

j=1

5

e2 j

2

L=∑

j=1

5

( y2 j

2−2 ( y1− β2 ) y2 j + ( y1− β2 ) 2

)

L=∑

j=1

5

y2 j

2−2 ( y1−β2 )∑

j=1

5

y2 j +5 ( y1

2−2 β2 y1 + β2

2 ) differentiate with respect to

β2 and equate to zero.

∂ L

∂ β1

=2∑

j=1

5

y2 j−10 y1 +10 β2=0

^β2=

∑

j =1

5

y2 j

5 − y1= y2− y1

Finally,

y3 j =β1+ β2 + β3+ e3 j make e1 j the subject

e3 j= y3 j− y2− β3 square both sides and sum

∑

j=1

5

e3 j

2=∑

j=1

5

( y3 j − y2−β3 )2

∑

j=1

5

e3 j

2=∑

j=1

5

( y3 j

2−2 ( y2−β3 ) y3 j + ( y2−β3 )2

)

Let L=∑

j=1

5

e3 j

2

L=∑

j=1

5

( y3 j

2−2 ( y2 −β3 ) y3 j + ( y2−β3 )2

)

L=∑

j=1

5

y3 j

2−2 ( y2−β3 ) ∑

j =1

5

y3 j +5 ( y2

2−2 β3 y2 +β3

2 ) differentiate with respect to

β3 and equate to zero.

∂ L

∂ β1

=2∑

j=1

5

y3 j−10 y2 +10 β3=0

^β2=

∑

j =1

5

y3 j

5 − y2= y3 − y2

(iii) Using R we obtain the column means for the data and thus we have the

estimates as follows:

e2 j= y2 j− y1−β2 square both sides and sum

∑

j=1

5

e2 j

2 =∑

j =1

5

( y2 j− y1−β2 )2

∑

j=1

5

e2 j

2 =∑

j =1

5

( y2 j

2−2 ( y1−β2 ) y2 j+ ( y1−β2 )2

)

Let L=∑

j=1

5

e2 j

2

L=∑

j=1

5

( y2 j

2−2 ( y1− β2 ) y2 j + ( y1− β2 ) 2

)

L=∑

j=1

5

y2 j

2−2 ( y1−β2 )∑

j=1

5

y2 j +5 ( y1

2−2 β2 y1 + β2

2 ) differentiate with respect to

β2 and equate to zero.

∂ L

∂ β1

=2∑

j=1

5

y2 j−10 y1 +10 β2=0

^β2=

∑

j =1

5

y2 j

5 − y1= y2− y1

Finally,

y3 j =β1+ β2 + β3+ e3 j make e1 j the subject

e3 j= y3 j− y2− β3 square both sides and sum

∑

j=1

5

e3 j

2=∑

j=1

5

( y3 j − y2−β3 )2

∑

j=1

5

e3 j

2=∑

j=1

5

( y3 j

2−2 ( y2−β3 ) y3 j + ( y2−β3 )2

)

Let L=∑

j=1

5

e3 j

2

L=∑

j=1

5

( y3 j

2−2 ( y2 −β3 ) y3 j + ( y2−β3 )2

)

L=∑

j=1

5

y3 j

2−2 ( y2−β3 ) ∑

j =1

5

y3 j +5 ( y2

2−2 β3 y2 +β3

2 ) differentiate with respect to

β3 and equate to zero.

∂ L

∂ β1

=2∑

j=1

5

y3 j−10 y2 +10 β3=0

^β2=

∑

j =1

5

y3 j

5 − y2= y3 − y2

(iii) Using R we obtain the column means for the data and thus we have the

estimates as follows:

y1=18.874 , y2=20.448, and y3=25.064

Then, the OLS estimates are

^β1= y1=18.874 , ^β2= y2− y1 =1.574, and ^β3= y3− y2=4.616

(iv) Test the hypothesis.

H0 : β2=0

Ha : β2> 0

The test statistic is a t statistic (t) defined by

t= y1− y3

SE with df = 5-2 = 3.

α=0.05 one tailed test

Decision, reject null hypothesis if |t | is greater than t3 ,0.05=2.353

SE= s

√n

SE= 0.3708

√5 =0.1658

t= 18.874

0.1658 =113.836

Since, |t |=113.836 is greater than t3 ,0.05=2.353, reject the null hypothesis and

conclude that β2> 0.

(v) Test the hypothesis.

H0 : β2=β3

Ha : β2> β3

The test statistic is a t statistic (t) defined by

t= β2

SE with df = 5-2 = 3.

α=0.05 one tailed test

Decision, reject null hypothesis if |t | is greater than t3 ,0.05=2.353

SE= S( y1− y3)

√n

SE= 2.1614

√5 =0.9666

t= 18.874−4.616

0. 9666 =14.7507

Since, |t |=14.7507 is greater than t3 ,0.05=2.353 , reject the null hypothesis and

conclude that β2> β3

Then, the OLS estimates are

^β1= y1=18.874 , ^β2= y2− y1 =1.574, and ^β3= y3− y2=4.616

(iv) Test the hypothesis.

H0 : β2=0

Ha : β2> 0

The test statistic is a t statistic (t) defined by

t= y1− y3

SE with df = 5-2 = 3.

α=0.05 one tailed test

Decision, reject null hypothesis if |t | is greater than t3 ,0.05=2.353

SE= s

√n

SE= 0.3708

√5 =0.1658

t= 18.874

0.1658 =113.836

Since, |t |=113.836 is greater than t3 ,0.05=2.353, reject the null hypothesis and

conclude that β2> 0.

(v) Test the hypothesis.

H0 : β2=β3

Ha : β2> β3

The test statistic is a t statistic (t) defined by

t= β2

SE with df = 5-2 = 3.

α=0.05 one tailed test

Decision, reject null hypothesis if |t | is greater than t3 ,0.05=2.353

SE= S( y1− y3)

√n

SE= 2.1614

√5 =0.9666

t= 18.874−4.616

0. 9666 =14.7507

Since, |t |=14.7507 is greater than t3 ,0.05=2.353 , reject the null hypothesis and

conclude that β2> β3

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Question 5

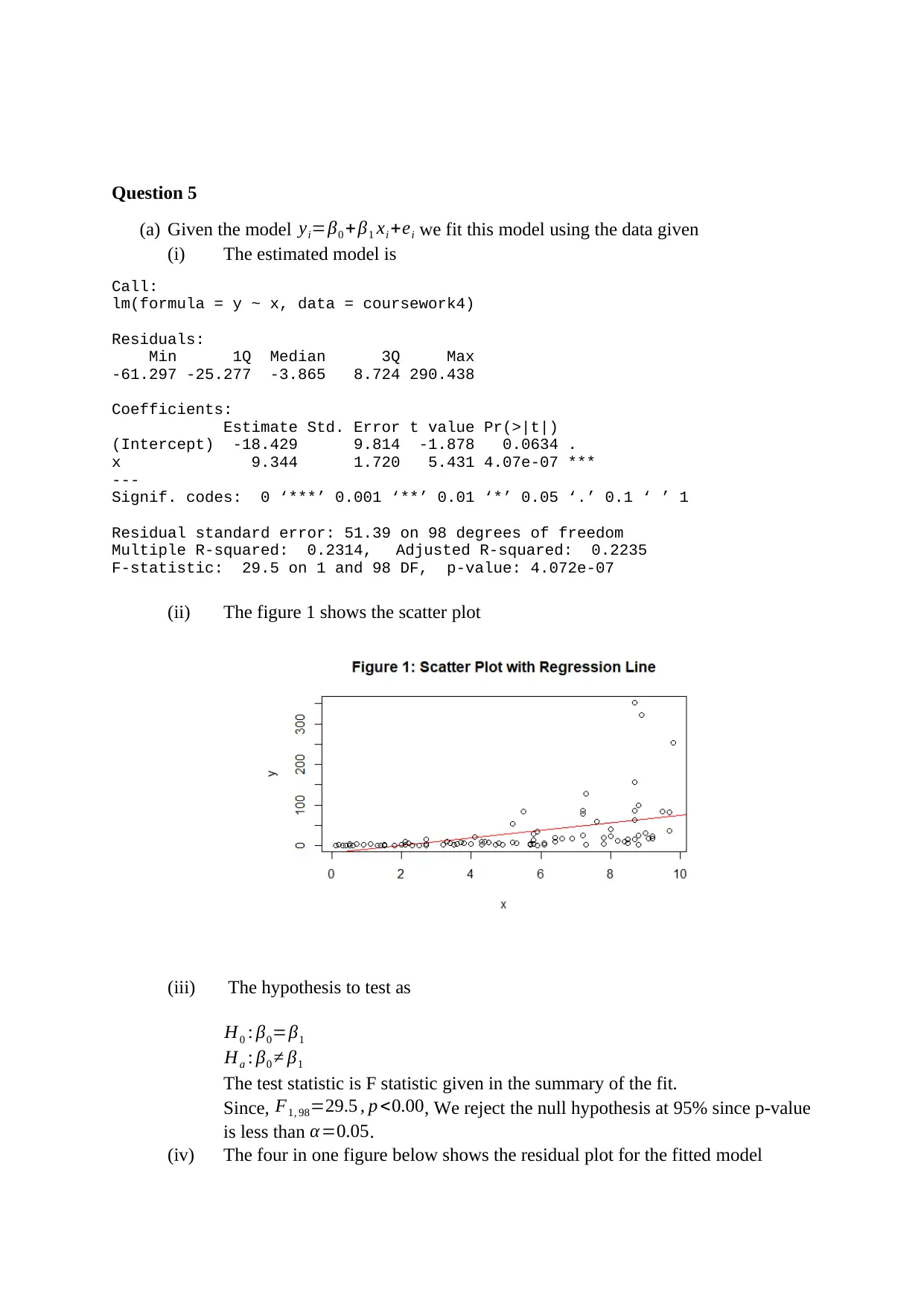

(a) Given the model yi=β0 + β1 xi +ei we fit this model using the data given

(i) The estimated model is

Call:

lm(formula = y ~ x, data = coursework4)

Residuals:

Min 1Q Median 3Q Max

-61.297 -25.277 -3.865 8.724 290.438

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -18.429 9.814 -1.878 0.0634 .

x 9.344 1.720 5.431 4.07e-07 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 51.39 on 98 degrees of freedom

Multiple R-squared: 0.2314, Adjusted R-squared: 0.2235

F-statistic: 29.5 on 1 and 98 DF, p-value: 4.072e-07

(ii) The figure 1 shows the scatter plot

(iii) The hypothesis to test as

H0 : β0=β1

Ha : β0 ≠ β1

The test statistic is F statistic given in the summary of the fit.

Since, F1, 98=29.5 , p <0.00, We reject the null hypothesis at 95% since p-value

is less than α =0.05.

(iv) The four in one figure below shows the residual plot for the fitted model

(a) Given the model yi=β0 + β1 xi +ei we fit this model using the data given

(i) The estimated model is

Call:

lm(formula = y ~ x, data = coursework4)

Residuals:

Min 1Q Median 3Q Max

-61.297 -25.277 -3.865 8.724 290.438

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -18.429 9.814 -1.878 0.0634 .

x 9.344 1.720 5.431 4.07e-07 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 51.39 on 98 degrees of freedom

Multiple R-squared: 0.2314, Adjusted R-squared: 0.2235

F-statistic: 29.5 on 1 and 98 DF, p-value: 4.072e-07

(ii) The figure 1 shows the scatter plot

(iii) The hypothesis to test as

H0 : β0=β1

Ha : β0 ≠ β1

The test statistic is F statistic given in the summary of the fit.

Since, F1, 98=29.5 , p <0.00, We reject the null hypothesis at 95% since p-value

is less than α =0.05.

(iv) The four in one figure below shows the residual plot for the fitted model

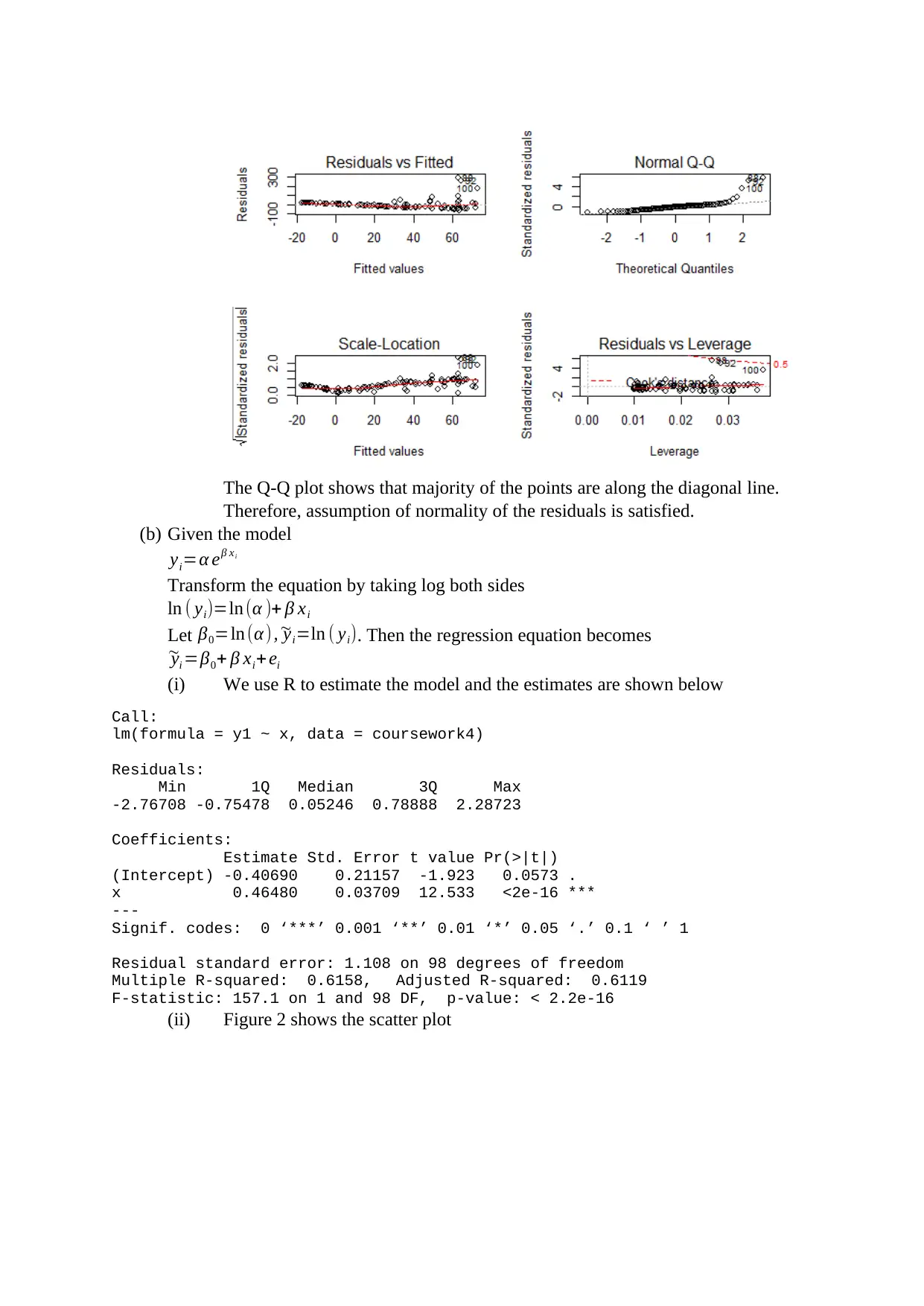

The Q-Q plot shows that majority of the points are along the diagonal line.

Therefore, assumption of normality of the residuals is satisfied.

(b) Given the model

yi=α eβ xi

Transform the equation by taking log both sides

ln ( yi)=ln (α )+ β xi

Let β0=ln (α ) , ~yi=ln ( yi). Then the regression equation becomes

~yi =β0+ β xi+ ei

(i) We use R to estimate the model and the estimates are shown below

Call:

lm(formula = y1 ~ x, data = coursework4)

Residuals:

Min 1Q Median 3Q Max

-2.76708 -0.75478 0.05246 0.78888 2.28723

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -0.40690 0.21157 -1.923 0.0573 .

x 0.46480 0.03709 12.533 <2e-16 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 1.108 on 98 degrees of freedom

Multiple R-squared: 0.6158, Adjusted R-squared: 0.6119

F-statistic: 157.1 on 1 and 98 DF, p-value: < 2.2e-16

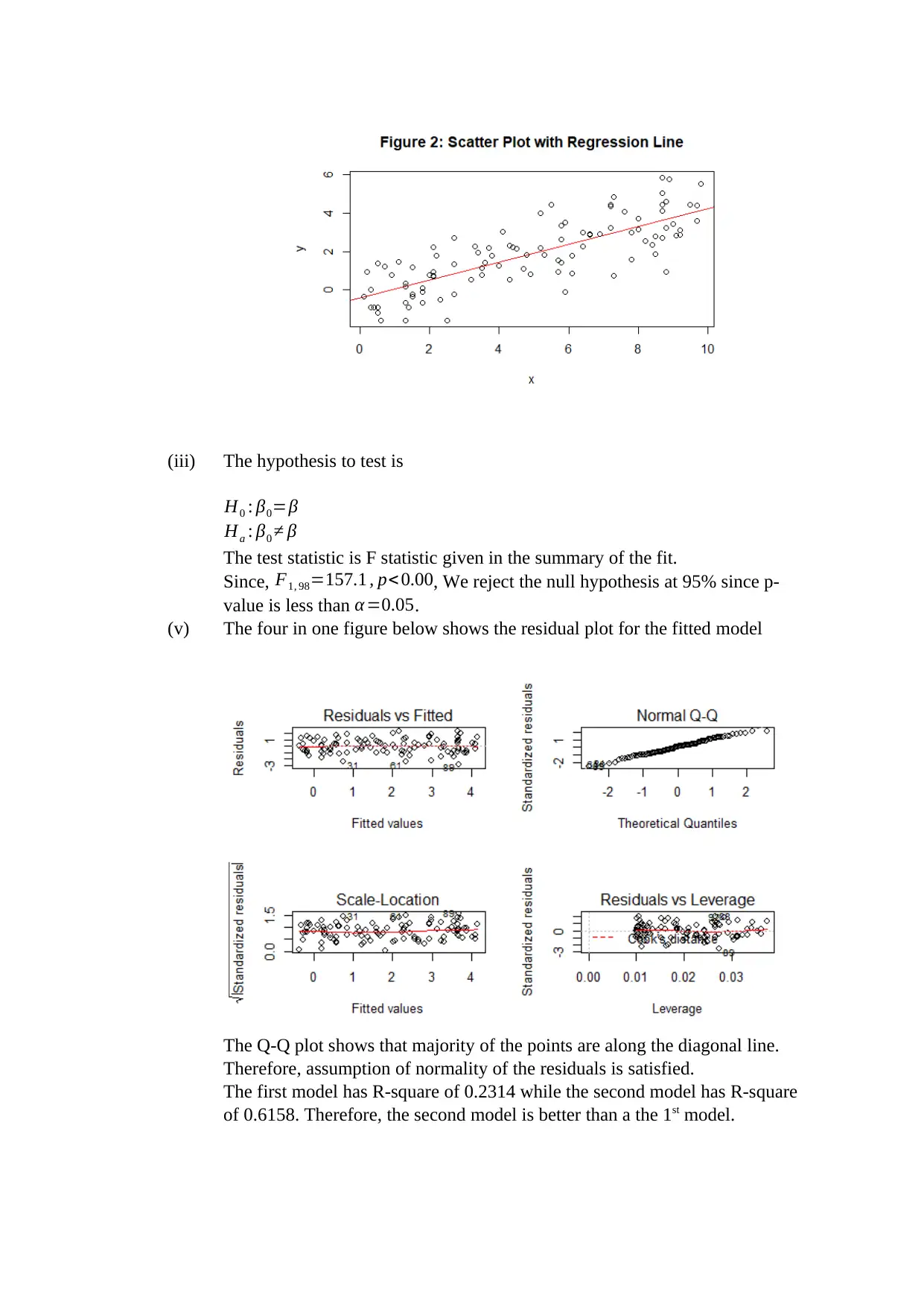

(ii) Figure 2 shows the scatter plot

Therefore, assumption of normality of the residuals is satisfied.

(b) Given the model

yi=α eβ xi

Transform the equation by taking log both sides

ln ( yi)=ln (α )+ β xi

Let β0=ln (α ) , ~yi=ln ( yi). Then the regression equation becomes

~yi =β0+ β xi+ ei

(i) We use R to estimate the model and the estimates are shown below

Call:

lm(formula = y1 ~ x, data = coursework4)

Residuals:

Min 1Q Median 3Q Max

-2.76708 -0.75478 0.05246 0.78888 2.28723

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -0.40690 0.21157 -1.923 0.0573 .

x 0.46480 0.03709 12.533 <2e-16 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 1.108 on 98 degrees of freedom

Multiple R-squared: 0.6158, Adjusted R-squared: 0.6119

F-statistic: 157.1 on 1 and 98 DF, p-value: < 2.2e-16

(ii) Figure 2 shows the scatter plot

(iii) The hypothesis to test is

H0 : β0=β

Ha : β0 ≠ β

The test statistic is F statistic given in the summary of the fit.

Since, F1, 98=157.1 , p< 0.00, We reject the null hypothesis at 95% since p-

value is less than α =0.05.

(v) The four in one figure below shows the residual plot for the fitted model

The Q-Q plot shows that majority of the points are along the diagonal line.

Therefore, assumption of normality of the residuals is satisfied.

The first model has R-square of 0.2314 while the second model has R-square

of 0.6158. Therefore, the second model is better than a the 1st model.

H0 : β0=β

Ha : β0 ≠ β

The test statistic is F statistic given in the summary of the fit.

Since, F1, 98=157.1 , p< 0.00, We reject the null hypothesis at 95% since p-

value is less than α =0.05.

(v) The four in one figure below shows the residual plot for the fitted model

The Q-Q plot shows that majority of the points are along the diagonal line.

Therefore, assumption of normality of the residuals is satisfied.

The first model has R-square of 0.2314 while the second model has R-square

of 0.6158. Therefore, the second model is better than a the 1st model.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.