Pharmaceutical Industry Analysis

VerifiedAdded on 2020/02/05

|49

|11109

|278

Report

AI Summary

This assignment delves into a comparative analysis of GlaxoSmithKline (GSK) and AstraZeneca (AZN), two prominent players in the UK pharmaceutical industry. Students are tasked with evaluating their financial statements – balance sheets, income statements, and cash flow statements – to assess their performance, profitability, and financial health. The assignment encourages an exploration of key financial ratios and metrics, drawing connections between their financial strategies and the broader context of the UK pharmaceutical market.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Accounting & Financial

Management

This is a financial analysis of Glaxo Smith Kline and a comparison with Astra Zeneca, with the

industry benchmarks.

1

Management

This is a financial analysis of Glaxo Smith Kline and a comparison with Astra Zeneca, with the

industry benchmarks.

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

Executive Summary..............................................................................................................................3

INTRODUCTION................................................................................................................................4

PROFILE OF Glaxo Smith Kline (GSK).............................................................................................5

PROFILE OF Astra Zeneca (AZN)....................................................................................................11

SWOT analysis of GSK vs AZN........................................................................................................17

Industry analysis.................................................................................................................................18

Conclusion.....................................................................................................................................20

Ratio analysis and financial performance......................................................................................20

Financing............................................................................................................................................30

External sources of financing...................................................................................................31

Internal sources of financing..........................................................................................................34

Budgeting...........................................................................................................................................35

Conclusion..........................................................................................................................................43

RECOMMENDATIONS....................................................................................................................43

REFERENCES...................................................................................................................................44

APPENDIX........................................................................................................................................46

2

Executive Summary..............................................................................................................................3

INTRODUCTION................................................................................................................................4

PROFILE OF Glaxo Smith Kline (GSK).............................................................................................5

PROFILE OF Astra Zeneca (AZN)....................................................................................................11

SWOT analysis of GSK vs AZN........................................................................................................17

Industry analysis.................................................................................................................................18

Conclusion.....................................................................................................................................20

Ratio analysis and financial performance......................................................................................20

Financing............................................................................................................................................30

External sources of financing...................................................................................................31

Internal sources of financing..........................................................................................................34

Budgeting...........................................................................................................................................35

Conclusion..........................................................................................................................................43

RECOMMENDATIONS....................................................................................................................43

REFERENCES...................................................................................................................................44

APPENDIX........................................................................................................................................46

2

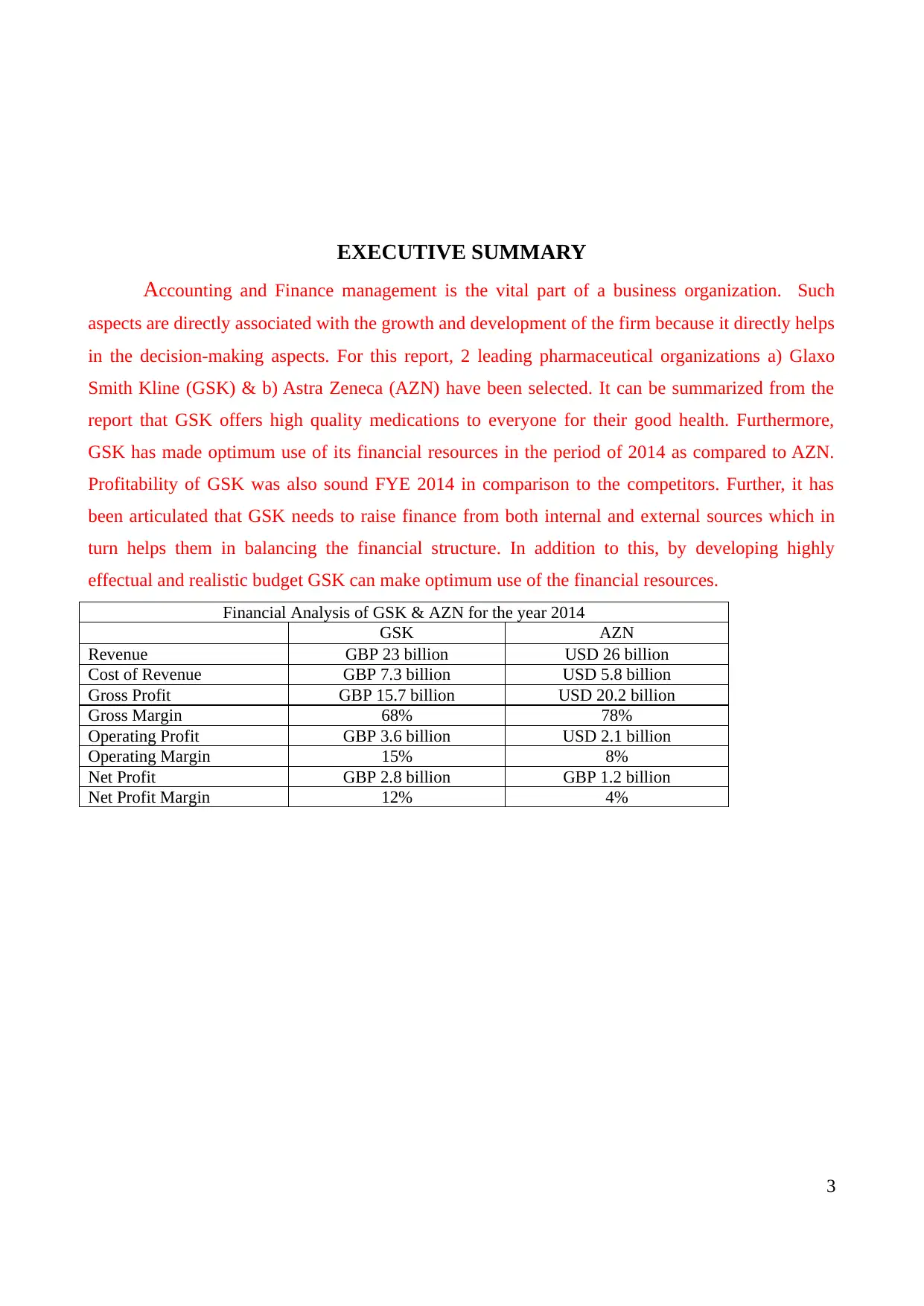

EXECUTIVE SUMMARY

Accounting and Finance management is the vital part of a business organization. Such

aspects are directly associated with the growth and development of the firm because it directly helps

in the decision-making aspects. For this report, 2 leading pharmaceutical organizations a) Glaxo

Smith Kline (GSK) & b) Astra Zeneca (AZN) have been selected. It can be summarized from the

report that GSK offers high quality medications to everyone for their good health. Furthermore,

GSK has made optimum use of its financial resources in the period of 2014 as compared to AZN.

Profitability of GSK was also sound FYE 2014 in comparison to the competitors. Further, it has

been articulated that GSK needs to raise finance from both internal and external sources which in

turn helps them in balancing the financial structure. In addition to this, by developing highly

effectual and realistic budget GSK can make optimum use of the financial resources.

Financial Analysis of GSK & AZN for the year 2014

GSK AZN

Revenue GBP 23 billion USD 26 billion

Cost of Revenue GBP 7.3 billion USD 5.8 billion

Gross Profit GBP 15.7 billion USD 20.2 billion

Gross Margin 68% 78%

Operating Profit GBP 3.6 billion USD 2.1 billion

Operating Margin 15% 8%

Net Profit GBP 2.8 billion GBP 1.2 billion

Net Profit Margin 12% 4%

3

Accounting and Finance management is the vital part of a business organization. Such

aspects are directly associated with the growth and development of the firm because it directly helps

in the decision-making aspects. For this report, 2 leading pharmaceutical organizations a) Glaxo

Smith Kline (GSK) & b) Astra Zeneca (AZN) have been selected. It can be summarized from the

report that GSK offers high quality medications to everyone for their good health. Furthermore,

GSK has made optimum use of its financial resources in the period of 2014 as compared to AZN.

Profitability of GSK was also sound FYE 2014 in comparison to the competitors. Further, it has

been articulated that GSK needs to raise finance from both internal and external sources which in

turn helps them in balancing the financial structure. In addition to this, by developing highly

effectual and realistic budget GSK can make optimum use of the financial resources.

Financial Analysis of GSK & AZN for the year 2014

GSK AZN

Revenue GBP 23 billion USD 26 billion

Cost of Revenue GBP 7.3 billion USD 5.8 billion

Gross Profit GBP 15.7 billion USD 20.2 billion

Gross Margin 68% 78%

Operating Profit GBP 3.6 billion USD 2.1 billion

Operating Margin 15% 8%

Net Profit GBP 2.8 billion GBP 1.2 billion

Net Profit Margin 12% 4%

3

INTRODUCTION

Accounting management may be defined as a technique which helps in controlling and

providing the report about the financial position as well as performance. In the present era, each

business organisation place high level of emphasis on maintaining records regarding financial

aspects (Schroeder, Clark and Cathey, 2013). This, in turn, provides deeper insight into the business

organisation about the changes which they need to make in the existing strategic and policy

framework. Moreover, by making a comparison of their own financial performance against

competitors, business unit can assess its position within the marketplace. The company can attain

success only when it manages the financial resources more effectively and efficiently (Hussainey,

Oscar Mgbame and Chijoke-Mgbame, 2011). Moreover, for the execution of business plan business

unit is highly required to make optimum use of resources by preparing the budgeting framework.

This project report is based on the pharmaceutical sector which is one of the leading and growing

industries in UK. For this project, Glaxo Smith Kline GSK) has been selected which is the world's

sixth largest pharmaceutical company. It offers high-quality drugs and vaccines to the customers. It

is the main constituent of the FTSE 100 indices and listed on London Stock Exchange. The

company has made vital contributions in the economic growth and development by offering

employment opportunities to many people. Another multinational pharmaceutical company - Astra

Zeneca (AZN) has been selected for this report as the major competitor of GSK. AZN’s

headquarters is also situated in London, just like GSK.

This report will shed light on financial health and performance of GSK against its competitors such

as AZN, through the means of ratio analysis technique. Further, it will describe the company's and

its competitor's profile in depth. The report will also develop understanding of the sources of

finance which GSK can undertake for fulfilling the financial requirements about the acquisition of

land and building. In addition to this, project report also depicts how budgeting technique assists the

company in making effective utilisation of the financial resources. Moreover, now the company can

get the desired level of outcome or success if it has effective control on financial spending. The

rationale behind this finance is one of the essential and crucial elements that have the high level of

impact on the growth aspect of the firm.

4

Accounting management may be defined as a technique which helps in controlling and

providing the report about the financial position as well as performance. In the present era, each

business organisation place high level of emphasis on maintaining records regarding financial

aspects (Schroeder, Clark and Cathey, 2013). This, in turn, provides deeper insight into the business

organisation about the changes which they need to make in the existing strategic and policy

framework. Moreover, by making a comparison of their own financial performance against

competitors, business unit can assess its position within the marketplace. The company can attain

success only when it manages the financial resources more effectively and efficiently (Hussainey,

Oscar Mgbame and Chijoke-Mgbame, 2011). Moreover, for the execution of business plan business

unit is highly required to make optimum use of resources by preparing the budgeting framework.

This project report is based on the pharmaceutical sector which is one of the leading and growing

industries in UK. For this project, Glaxo Smith Kline GSK) has been selected which is the world's

sixth largest pharmaceutical company. It offers high-quality drugs and vaccines to the customers. It

is the main constituent of the FTSE 100 indices and listed on London Stock Exchange. The

company has made vital contributions in the economic growth and development by offering

employment opportunities to many people. Another multinational pharmaceutical company - Astra

Zeneca (AZN) has been selected for this report as the major competitor of GSK. AZN’s

headquarters is also situated in London, just like GSK.

This report will shed light on financial health and performance of GSK against its competitors such

as AZN, through the means of ratio analysis technique. Further, it will describe the company's and

its competitor's profile in depth. The report will also develop understanding of the sources of

finance which GSK can undertake for fulfilling the financial requirements about the acquisition of

land and building. In addition to this, project report also depicts how budgeting technique assists the

company in making effective utilisation of the financial resources. Moreover, now the company can

get the desired level of outcome or success if it has effective control on financial spending. The

rationale behind this finance is one of the essential and crucial elements that have the high level of

impact on the growth aspect of the firm.

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

PROFILE OF Glaxo Smith Kline (GSK)

Established in December 2000

Founders It established through the means of merger

strategy such as Glaxo Wellcome and Smith

Kline Beecham. Hence, both the organisation

merged their business operations and function

and started with the new name such as GSK.

Website www.gsk.com

Leading brands & product line Top selling products of GSK includes Advair,

Avodart, Flovent, Augmentin, Lovaza and

Lamictal. Along with this, consumer products

which are offered by GSK has earned £5.2

billion in the accounting year 2013.

Geographical presence GSK has extensive network of manufacturing

sites as well as research and development

centres in US, UK, Spain, Belgium and China.

Along with this, business unit offers

pharmaceutical; products to the customers

worldwide.

World headquarters Headquartered in Isleworth, London

Chief executive officer Andrew Witty

Worldwide employees 100000 people across 150 countries

5

Established in December 2000

Founders It established through the means of merger

strategy such as Glaxo Wellcome and Smith

Kline Beecham. Hence, both the organisation

merged their business operations and function

and started with the new name such as GSK.

Website www.gsk.com

Leading brands & product line Top selling products of GSK includes Advair,

Avodart, Flovent, Augmentin, Lovaza and

Lamictal. Along with this, consumer products

which are offered by GSK has earned £5.2

billion in the accounting year 2013.

Geographical presence GSK has extensive network of manufacturing

sites as well as research and development

centres in US, UK, Spain, Belgium and China.

Along with this, business unit offers

pharmaceutical; products to the customers

worldwide.

World headquarters Headquartered in Isleworth, London

Chief executive officer Andrew Witty

Worldwide employees 100000 people across 150 countries

5

Initial public offering On initial level, company has listed on London

stock exchange and now it becomes the most

important constituent of FTSE 100 index. In

August 2016, the market capitalization of the

firm is around £81 billion. Further, another

achievement is that company has got the fourth

position in London stock exchange. Now, it is

also listing on the New York stock exchange.

The company is well known for the high-quality

products which are offered by it.

Worldwide revenue 2014 / 2015 £23 billion / £23.923 billion

Mission GSK mission is to provide the high level of

assistance to the people to do more, feel better

and live longer (Mission, vision and strategies of

GSK, 2016).

Vision Long term vision has been setting down by the

firm for their value chain about being carbon

neutral by 2050. Further, vision statement of the

company is to become a leading firm in the

pharmaceutical sector.

Value Key values of GSK include integrity, respect for

people, ensuring transparency and offering

patient focused products or services.

Key competitors Pfizer

6

stock exchange and now it becomes the most

important constituent of FTSE 100 index. In

August 2016, the market capitalization of the

firm is around £81 billion. Further, another

achievement is that company has got the fourth

position in London stock exchange. Now, it is

also listing on the New York stock exchange.

The company is well known for the high-quality

products which are offered by it.

Worldwide revenue 2014 / 2015 £23 billion / £23.923 billion

Mission GSK mission is to provide the high level of

assistance to the people to do more, feel better

and live longer (Mission, vision and strategies of

GSK, 2016).

Vision Long term vision has been setting down by the

firm for their value chain about being carbon

neutral by 2050. Further, vision statement of the

company is to become a leading firm in the

pharmaceutical sector.

Value Key values of GSK include integrity, respect for

people, ensuring transparency and offering

patient focused products or services.

Key competitors Pfizer

6

AZN

Xeno Port

Merck

Colgate-Palmolive

Research and development investments Business unit has invested £300000 in

researching new medicines, vaccines and other

products.

Firm level strategies Company primarily focuses on increasing

growth, reducing the risk level and improving

the long-term financial performance. Hence, the

company has developed competent strategic and

policy framework to attain all such aspects. This,

in turn, enables a firm to enhance the sales

revenue and thereby offered improved return to

the shareholders. Along with this, the major

focus of GSK is on three areas such as

pharmaceutical, vaccines and consumer

healthcare.

Mergers & acquisition It acquired GlycoVaxyn in the year 2015.

However, GSK Cancer division has been

sold to Novartis. Despite this, Novartis

Vaccine Division was acquired in 2014

by GSK.

In the year 2013, it acquired Human

Genome Sciences and CellZome in 2011.

During 2010, it acquired Maxinutrition

and Laboratories Phoenix.

7

Xeno Port

Merck

Colgate-Palmolive

Research and development investments Business unit has invested £300000 in

researching new medicines, vaccines and other

products.

Firm level strategies Company primarily focuses on increasing

growth, reducing the risk level and improving

the long-term financial performance. Hence, the

company has developed competent strategic and

policy framework to attain all such aspects. This,

in turn, enables a firm to enhance the sales

revenue and thereby offered improved return to

the shareholders. Along with this, the major

focus of GSK is on three areas such as

pharmaceutical, vaccines and consumer

healthcare.

Mergers & acquisition It acquired GlycoVaxyn in the year 2015.

However, GSK Cancer division has been

sold to Novartis. Despite this, Novartis

Vaccine Division was acquired in 2014

by GSK.

In the year 2013, it acquired Human

Genome Sciences and CellZome in 2011.

During 2010, it acquired Maxinutrition

and Laboratories Phoenix.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate credit rating Sound

Award and recognitions GSK is awarded by ‘Royal society of London’

for the contribution made by it in the medical

and veterinary sciences.

Corporate social responsibility initiatives GSK has organised several campaigns

with the aim to develop awareness

among the people regarding the health

aspect.

Besides this, the company is not setting

the fixed amount for this purpose. It

takes more initiatives and prefers to

invest more on charities, NGO's, etc.

Further, health and education programs

about AIDS, HIV, malaria and diarrhoeal

diseases. Through this, GSK persuades

people to take quick treatment while

suffering from malaria.

Moreover, this disease creates the high

level of the health issues so, prompt

prevention of it is highly required.

In the accounting year 2008, business

unit has donated medicines

approximately £5.3 million for

humanitarian aid.

Thus, it can be said that business unit has

offered support to 118 countries which

suffered from war and natural disaster.

8

Award and recognitions GSK is awarded by ‘Royal society of London’

for the contribution made by it in the medical

and veterinary sciences.

Corporate social responsibility initiatives GSK has organised several campaigns

with the aim to develop awareness

among the people regarding the health

aspect.

Besides this, the company is not setting

the fixed amount for this purpose. It

takes more initiatives and prefers to

invest more on charities, NGO's, etc.

Further, health and education programs

about AIDS, HIV, malaria and diarrhoeal

diseases. Through this, GSK persuades

people to take quick treatment while

suffering from malaria.

Moreover, this disease creates the high

level of the health issues so, prompt

prevention of it is highly required.

In the accounting year 2008, business

unit has donated medicines

approximately £5.3 million for

humanitarian aid.

Thus, it can be said that business unit has

offered support to 118 countries which

suffered from war and natural disaster.

8

Business enterprise was also donated

medicines, vaccines and consumer health

products to the people who affected from

an earthquake.

Taxes and fines Fine of £37m has been imposed by the

Competition and market authority on GSK for

its illegal behaviour.

Penalties imposed by the government UK government has imposed penalties of

£44.99m on GSK due to making supply of

paroxetine.

Legal suits filed for and against the organization Approximately 5000 filed suit in against to GSK

due to the side effects of its antidepressant Paxil

and anti-nausea drugs.

Management and leadership team Chairman – Sir Philip Hampton

Chief Executive Officer – Sir Andrew

Witty

Chief Financial Officer = Simon

Dingemans

Global Vaccines Chairman – Dr Moncef

Slaoui

Independent Non-Executive Directors –

Manvinder Singh and Stacey Cartwright

Dividend paid In 2015, GSK paid a dividend of 80p on each

equity holding, however, on the other hand, a

special dividend paid of 20p per share.

9

medicines, vaccines and consumer health

products to the people who affected from

an earthquake.

Taxes and fines Fine of £37m has been imposed by the

Competition and market authority on GSK for

its illegal behaviour.

Penalties imposed by the government UK government has imposed penalties of

£44.99m on GSK due to making supply of

paroxetine.

Legal suits filed for and against the organization Approximately 5000 filed suit in against to GSK

due to the side effects of its antidepressant Paxil

and anti-nausea drugs.

Management and leadership team Chairman – Sir Philip Hampton

Chief Executive Officer – Sir Andrew

Witty

Chief Financial Officer = Simon

Dingemans

Global Vaccines Chairman – Dr Moncef

Slaoui

Independent Non-Executive Directors –

Manvinder Singh and Stacey Cartwright

Dividend paid In 2015, GSK paid a dividend of 80p on each

equity holding, however, on the other hand, a

special dividend paid of 20p per share.

9

Vision 2020 GSK's vision is to file up to 20 new drugs by

2020.

PROFILE OF ASTRA ZENECA (AZN)

Established in AstraZeneca Plc is one of the largest pharmaceutical public

limited company that was established in the year 1999.

Founders It has been established through the merger of both the Astra

AB and Zeneca Group Plc.

Website Headquarter of the company is located in Cambridge,

England.

Leading brands & product line Its product portfolio mainly consists of cardiovascular and

metabolic diseases (CVMD), anaesthetics, infectious

disease, neuroscience, respiratory, gastrointestinal and

inflammation.

Geographical presence It operates across the globe as AZN carries out its daily

operations in Angola, Africa, Europe, Ghana, Australian,

China, Hong Kong, India, Argentina, United States,

Mexico, Mauritius, Nigeria, Zambia and others. Its

worldwide operations are divided into four parts that are

US, Europe, Established ROW and Emerging Markets as

10

2020.

PROFILE OF ASTRA ZENECA (AZN)

Established in AstraZeneca Plc is one of the largest pharmaceutical public

limited company that was established in the year 1999.

Founders It has been established through the merger of both the Astra

AB and Zeneca Group Plc.

Website Headquarter of the company is located in Cambridge,

England.

Leading brands & product line Its product portfolio mainly consists of cardiovascular and

metabolic diseases (CVMD), anaesthetics, infectious

disease, neuroscience, respiratory, gastrointestinal and

inflammation.

Geographical presence It operates across the globe as AZN carries out its daily

operations in Angola, Africa, Europe, Ghana, Australian,

China, Hong Kong, India, Argentina, United States,

Mexico, Mauritius, Nigeria, Zambia and others. Its

worldwide operations are divided into four parts that are

US, Europe, Established ROW and Emerging Markets as

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

well.

World headquarters Cambridge, England

Chief executive officer Ward-Lilley

Worldwide employees 50000

Initial public offering AZN is primarily listed on London Stock Exchange ad

constituent of FTSE 100 Index. However, secondarily it is

listed on NYSE (New York Stock Exchange) and OMX

exchange.

Worldwide revenue 24.708 US dollar billion

Mission The target of the company is to improve people’s health by

rendering exceptional medical treatment.

Vision The vision statement of AZN is to deliver improved value

to all the stakeholders and society through best practices

and services.

Value To deliver best vaccination and cure treatment

To improve workers talent and capabilities and value their

efforts

To maximize business performance and competitive

strength

To use advanced and upgraded technologies through R&D

operations

Key competitors Amgen, GSK, Teva Pharmaceuticals

11

World headquarters Cambridge, England

Chief executive officer Ward-Lilley

Worldwide employees 50000

Initial public offering AZN is primarily listed on London Stock Exchange ad

constituent of FTSE 100 Index. However, secondarily it is

listed on NYSE (New York Stock Exchange) and OMX

exchange.

Worldwide revenue 24.708 US dollar billion

Mission The target of the company is to improve people’s health by

rendering exceptional medical treatment.

Vision The vision statement of AZN is to deliver improved value

to all the stakeholders and society through best practices

and services.

Value To deliver best vaccination and cure treatment

To improve workers talent and capabilities and value their

efforts

To maximize business performance and competitive

strength

To use advanced and upgraded technologies through R&D

operations

Key competitors Amgen, GSK, Teva Pharmaceuticals

11

Research and development

investments

AZN regulatory focused on innovations by

collaboration with many research institutions and strategic

R&D centres at different locations such as Maryland,

Gaithersburg and Cambridge, UK. In 2015, AZN spent

$140 billion on R&D operations which clearly demonstrate

that company pay focused on bringing innovations and

uniqueness in their practices so as to deliver the best

treatment and medical services to the patients to cure their

diseases. IMED technology, Global Medicine Development

(GMD) and other innovations to provide the best therapy

are the results of R&D operations.

Firm level strategies The corporate strategy of AZN is to focus on moving

towards innovative science-led practices it is highly focused

on delivering sustainable delivery and put best efforts to

give better value to the patients and shareholders. The

company also pay its focus to accelerate its pipeline

business model, maximise growth and build a strong culture

to retain a talented workforce.

Mergers & acquisition n December 2015, AZN acquired ZS Pharma

company and Entasis Therapeutics which proves as

an improvement to its pipeline and CVMD

technology.

In the year 2014, it acquired Bristol-Myers Squibb

(BMS) to share its global diabetes alliances.

In the year 2013, it acquired Omthera

12

investments

AZN regulatory focused on innovations by

collaboration with many research institutions and strategic

R&D centres at different locations such as Maryland,

Gaithersburg and Cambridge, UK. In 2015, AZN spent

$140 billion on R&D operations which clearly demonstrate

that company pay focused on bringing innovations and

uniqueness in their practices so as to deliver the best

treatment and medical services to the patients to cure their

diseases. IMED technology, Global Medicine Development

(GMD) and other innovations to provide the best therapy

are the results of R&D operations.

Firm level strategies The corporate strategy of AZN is to focus on moving

towards innovative science-led practices it is highly focused

on delivering sustainable delivery and put best efforts to

give better value to the patients and shareholders. The

company also pay its focus to accelerate its pipeline

business model, maximise growth and build a strong culture

to retain a talented workforce.

Mergers & acquisition n December 2015, AZN acquired ZS Pharma

company and Entasis Therapeutics which proves as

an improvement to its pipeline and CVMD

technology.

In the year 2014, it acquired Bristol-Myers Squibb

(BMS) to share its global diabetes alliances.

In the year 2013, it acquired Omthera

12

Pharmaceuticals, Pearl Therapeutics and Spirogen.

In 2012, Amylin Pharmaceuticals, Ardea Bioscience

and Guangdong BeiKang Pharmaceutical Company

were acquired.

Corporate credit rating Good

Award and recognitions AZN won a number of awards and recognition as it won

Best Partnership Alliance, Best Management Team of the

year to Business Development Operations (BDO) and Best

Licensing Deal of the year.

Corporate social responsibility

initiatives

AZN follows environmental sustainability so as to

effectively and optimal utilise their natural resources

and minimise carbon footprint and wastage to

maintain ecological integrity.

Eradication of poverty, hunger and malnutrition

Promoting education among society

Promoting and improving public health

Reduction in infant mortality rate

Protecting natural heritage, historical buildings and

culture

Encourage sport activities

13

In 2012, Amylin Pharmaceuticals, Ardea Bioscience

and Guangdong BeiKang Pharmaceutical Company

were acquired.

Corporate credit rating Good

Award and recognitions AZN won a number of awards and recognition as it won

Best Partnership Alliance, Best Management Team of the

year to Business Development Operations (BDO) and Best

Licensing Deal of the year.

Corporate social responsibility

initiatives

AZN follows environmental sustainability so as to

effectively and optimal utilise their natural resources

and minimise carbon footprint and wastage to

maintain ecological integrity.

Eradication of poverty, hunger and malnutrition

Promoting education among society

Promoting and improving public health

Reduction in infant mortality rate

Protecting natural heritage, historical buildings and

culture

Encourage sport activities

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Rural development projects

Taxes and fines In the year 2015, AZN paid the $243m amount as their

taxation obligation. Government and taxation authority

have the right to put lawsuits against the business in case of

non-compliance with the tax laws.

Penalties imposed by the

government

AZN's failure to comply with laws, rules and regulations

may give rise to criminal or civil offences against which

government charge lawsuits. Disruption of anti-bribery act,

data protection legislation and non-compliance with laws

and regulatory principles imposed penalties or fines towards

AZN. In the year 2010, a court ordered AZN to pay the fine

of 52.5 pounds million because of its illegal business

practice to gain a dominant market position.

Legal suits filed for and against the

organization

In the year 2016, the company was charged at the amount of

5.5 dollars million because of breaching and violating

Foreign Corruption Practice Act.

Management and leadership team Its management and leadership team is responsible for

carrying out responsible and ethical business practice to

drive long-term success. Main leaders and managers of

AZN are given below:

14

Taxes and fines In the year 2015, AZN paid the $243m amount as their

taxation obligation. Government and taxation authority

have the right to put lawsuits against the business in case of

non-compliance with the tax laws.

Penalties imposed by the

government

AZN's failure to comply with laws, rules and regulations

may give rise to criminal or civil offences against which

government charge lawsuits. Disruption of anti-bribery act,

data protection legislation and non-compliance with laws

and regulatory principles imposed penalties or fines towards

AZN. In the year 2010, a court ordered AZN to pay the fine

of 52.5 pounds million because of its illegal business

practice to gain a dominant market position.

Legal suits filed for and against the

organization

In the year 2016, the company was charged at the amount of

5.5 dollars million because of breaching and violating

Foreign Corruption Practice Act.

Management and leadership team Its management and leadership team is responsible for

carrying out responsible and ethical business practice to

drive long-term success. Main leaders and managers of

AZN are given below:

14

Chief – Executive Officer (CEO) – Ward-Lilley

Chief Compliance Officer (CCO) – Katarina Ageborg

Non-Executive Chairman – Leif Johansson

Certified Financial Officer (CFO) Marc Dunoyer

Chief Medical Officer – Sean Bohen

Dividend paid It follows progressive dividend policy which aims at

maintaining or increasing shareholder’s dividend each year.

During the year 2015, its paid dividend of $3539 million to

their shareholders, however, dividend per ordinary share

(DPS) is $2.80 means 188.5 pence.

Vision 2020 Its vision is to become a leader in the pharmaceutical

industry by delivering high-quality and innovative medical

treatment and cure services.

SWOT ANALYSIS OF GSK VS AZN

SWOT analysis helps to identify internal strength and weakness while external market analysis

helps to assess its opportunities and threats as well. Concerning GSK and AZN, SWOT analysis is

conducted below:

GSK’s SWOT analysis

Strengths Weakness

Strong product portfolio

Excellent market position

Expiry of Patent

Declined turnover

15

Chief Compliance Officer (CCO) – Katarina Ageborg

Non-Executive Chairman – Leif Johansson

Certified Financial Officer (CFO) Marc Dunoyer

Chief Medical Officer – Sean Bohen

Dividend paid It follows progressive dividend policy which aims at

maintaining or increasing shareholder’s dividend each year.

During the year 2015, its paid dividend of $3539 million to

their shareholders, however, dividend per ordinary share

(DPS) is $2.80 means 188.5 pence.

Vision 2020 Its vision is to become a leader in the pharmaceutical

industry by delivering high-quality and innovative medical

treatment and cure services.

SWOT ANALYSIS OF GSK VS AZN

SWOT analysis helps to identify internal strength and weakness while external market analysis

helps to assess its opportunities and threats as well. Concerning GSK and AZN, SWOT analysis is

conducted below:

GSK’s SWOT analysis

Strengths Weakness

Strong product portfolio

Excellent market position

Expiry of Patent

Declined turnover

15

Worldwide presence

Extensive Research and Development

High market turnover

Chemical industry and resource

efficiency rewards

Requirement of invention of new drug

and medicines

Needs to enter into new markets

Controversies regards to drug safety

negatively impact its corporate image

Opportunity Threats

Ageing UK population

Expansion into emerging economies i.e.

BRIC

Rising consumer awareness

Mergers and acquisition

Invention of new drug and medicines

Innovative technology

Tough competition from Amgen, AZN,

Abbott Laboratories

End of Intellectual Property Rights like

patent

Expensive research

High regulations

Economic downturn in Europe

AZN’s SWOT analysis

Strengths Weakness

Rapid and instant decision-making

Presence in emerging markets

Worldwide operations

Strong and dedicated R&D team

Strong brand and product portfolio

Global sales

Negative effect on business operations

due to drug shortage in Cefotan

Pricing issues adversely effected its

corporate reputation

Product discontinuation due to late-

stage development of its business

model Pipeline

Legal controversies and proceedings

regards to patent

Dependencies upon small molecules

Opportunity Threats

Leverage presence through expansion

in emerging economies

Copycat generic drug and medicines

Exposure to high level of competition

16

Extensive Research and Development

High market turnover

Chemical industry and resource

efficiency rewards

Requirement of invention of new drug

and medicines

Needs to enter into new markets

Controversies regards to drug safety

negatively impact its corporate image

Opportunity Threats

Ageing UK population

Expansion into emerging economies i.e.

BRIC

Rising consumer awareness

Mergers and acquisition

Invention of new drug and medicines

Innovative technology

Tough competition from Amgen, AZN,

Abbott Laboratories

End of Intellectual Property Rights like

patent

Expensive research

High regulations

Economic downturn in Europe

AZN’s SWOT analysis

Strengths Weakness

Rapid and instant decision-making

Presence in emerging markets

Worldwide operations

Strong and dedicated R&D team

Strong brand and product portfolio

Global sales

Negative effect on business operations

due to drug shortage in Cefotan

Pricing issues adversely effected its

corporate reputation

Product discontinuation due to late-

stage development of its business

model Pipeline

Legal controversies and proceedings

regards to patent

Dependencies upon small molecules

Opportunity Threats

Leverage presence through expansion

in emerging economies

Copycat generic drug and medicines

Exposure to high level of competition

16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Cost-restructuring

Global strategic alliances through

M&A

Moving into other biosimilars markets

Rise in market demand due to ageing

population across globe

with Amgen, GSK, Teva

Pharmaceuticals

Changes in regulations and legislations

Pricing pressure

INDUSTRY ANALYSIS

Pharmaceutical industry of UK is continuously increasing and has offered high level of

employment opportunity to people. It is a major industry of UK which makes vital contribution in

GDP and exports level. Along with this, companies operated in pharma sector made high level of

investment in R&D activities with the aim to provides customers with high-quality drugs and

services (Bowen, 2011). Major pharma companies of UK include GSK and AZN which has attained

higher fifth & sixth position regarding market share. From the period of 1994 to 2014,

pharmaceutical sector has generated high trade surplus such as 1.1 billion per annum. This aspect

entails the success story of the pharma industry.

17

Global strategic alliances through

M&A

Moving into other biosimilars markets

Rise in market demand due to ageing

population across globe

with Amgen, GSK, Teva

Pharmaceuticals

Changes in regulations and legislations

Pricing pressure

INDUSTRY ANALYSIS

Pharmaceutical industry of UK is continuously increasing and has offered high level of

employment opportunity to people. It is a major industry of UK which makes vital contribution in

GDP and exports level. Along with this, companies operated in pharma sector made high level of

investment in R&D activities with the aim to provides customers with high-quality drugs and

services (Bowen, 2011). Major pharma companies of UK include GSK and AZN which has attained

higher fifth & sixth position regarding market share. From the period of 1994 to 2014,

pharmaceutical sector has generated high trade surplus such as 1.1 billion per annum. This aspect

entails the success story of the pharma industry.

17

According to the presented graph, it can be seen that in the pharmaceutical industry, AZN

stood at 10th position as its total revenue is $23,641m, however, GSK ranked at 7th position by

generating annual revenue of $36,566m.

Also, the pharmaceutical sector of UK is facing stiff competition due to the presence of highly

strong companies. Although there’s only a small number of firms that exist, they are competing in

an intense way. Moreover, large companies like GSK and AZN carry out several research projects at

one time with the aim to build or sustain leading position. In addition to this, customers need and

preferences are also changing constantly. Moreover, once the duration of the patent has been

completed, the company introduces generic medicines. Hence, the cost of generic medicines is

lower than the original one (Gaskill, Van Auken and Kim, 2015). Hence, by offering generic

medicines, business organisation can satisfy the needs of customers. Along with this, a profit margin

of the companies operated in pharma sector is continuously increasing. Moreover, the government

also takes the initiative in offering medicines at affordable prices. In this way, revenue and profit

margin of such sector is continuously rising.

18

stood at 10th position as its total revenue is $23,641m, however, GSK ranked at 7th position by

generating annual revenue of $36,566m.

Also, the pharmaceutical sector of UK is facing stiff competition due to the presence of highly

strong companies. Although there’s only a small number of firms that exist, they are competing in

an intense way. Moreover, large companies like GSK and AZN carry out several research projects at

one time with the aim to build or sustain leading position. In addition to this, customers need and

preferences are also changing constantly. Moreover, once the duration of the patent has been

completed, the company introduces generic medicines. Hence, the cost of generic medicines is

lower than the original one (Gaskill, Van Auken and Kim, 2015). Hence, by offering generic

medicines, business organisation can satisfy the needs of customers. Along with this, a profit margin

of the companies operated in pharma sector is continuously increasing. Moreover, the government

also takes the initiative in offering medicines at affordable prices. In this way, revenue and profit

margin of such sector is continuously rising.

18

However, in the accounting year 2013 and 2014 sales revenue as well as the profit margin of GSK

and AZN decreased to a large extent. The reason behind this high level of unemployment situation

exists in the UK. Hence, due to this, business organisations performed in pharma sector faced

difficulty about the generation of enough amount of sales (Hung and Subramanyam, 2007). In

addition to this, UK has many pharma companies which are listed on London stock exchange.

Further, UK has top 25 companies which make the investment in the R&D to the large extent ion

which GSK and AZN has captured top positions as compared to other firms. Hence, in such

research-intensive industry companies of UK have made their best efforts and thereby contributed

to the economic growth and development.

Conclusion

From the above analysis, it has been concluded that GSK is one of the largest and leading

pharmaceutical companies in UK, as compared to rival firms. Besides this, it has been concluded

that strategies and policies developed by GSK is sound in comparison to AZN. Further, it can be

stated that GSK has several strengths regarding skilled personnel, high R&D investment compared

to AZN. It can be seen in the report that both companies have the opportunity to attain success by

introducing highly effectual and innovative medicines.

Ratio analysis and financial performance

Ratio analysis may be defined as a tool which assists a business organisation in evaluating their

financial performance and position against rival firms. It also offers an opportunity to the business

enterprise to compare their financials against previous years. Along with this, such financial

statement analysis tool provides stakeholders with huge amount of information that aids in the

effective and profitable decision making.

Current Ratio:

Current Ratio = Current Assets / Current Liabilities

This ratio furnishes information about the company's ability about fulfilling the current obligations

over the current assets (Brealey, 2012). By using such ratios companies and their stakeholders can

evaluate the liquidity position and performance of the firm.

Company 2013 2014

19

and AZN decreased to a large extent. The reason behind this high level of unemployment situation

exists in the UK. Hence, due to this, business organisations performed in pharma sector faced

difficulty about the generation of enough amount of sales (Hung and Subramanyam, 2007). In

addition to this, UK has many pharma companies which are listed on London stock exchange.

Further, UK has top 25 companies which make the investment in the R&D to the large extent ion

which GSK and AZN has captured top positions as compared to other firms. Hence, in such

research-intensive industry companies of UK have made their best efforts and thereby contributed

to the economic growth and development.

Conclusion

From the above analysis, it has been concluded that GSK is one of the largest and leading

pharmaceutical companies in UK, as compared to rival firms. Besides this, it has been concluded

that strategies and policies developed by GSK is sound in comparison to AZN. Further, it can be

stated that GSK has several strengths regarding skilled personnel, high R&D investment compared

to AZN. It can be seen in the report that both companies have the opportunity to attain success by

introducing highly effectual and innovative medicines.

Ratio analysis and financial performance

Ratio analysis may be defined as a tool which assists a business organisation in evaluating their

financial performance and position against rival firms. It also offers an opportunity to the business

enterprise to compare their financials against previous years. Along with this, such financial

statement analysis tool provides stakeholders with huge amount of information that aids in the

effective and profitable decision making.

Current Ratio:

Current Ratio = Current Assets / Current Liabilities

This ratio furnishes information about the company's ability about fulfilling the current obligations

over the current assets (Brealey, 2012). By using such ratios companies and their stakeholders can

evaluate the liquidity position and performance of the firm.

Company 2013 2014

19

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

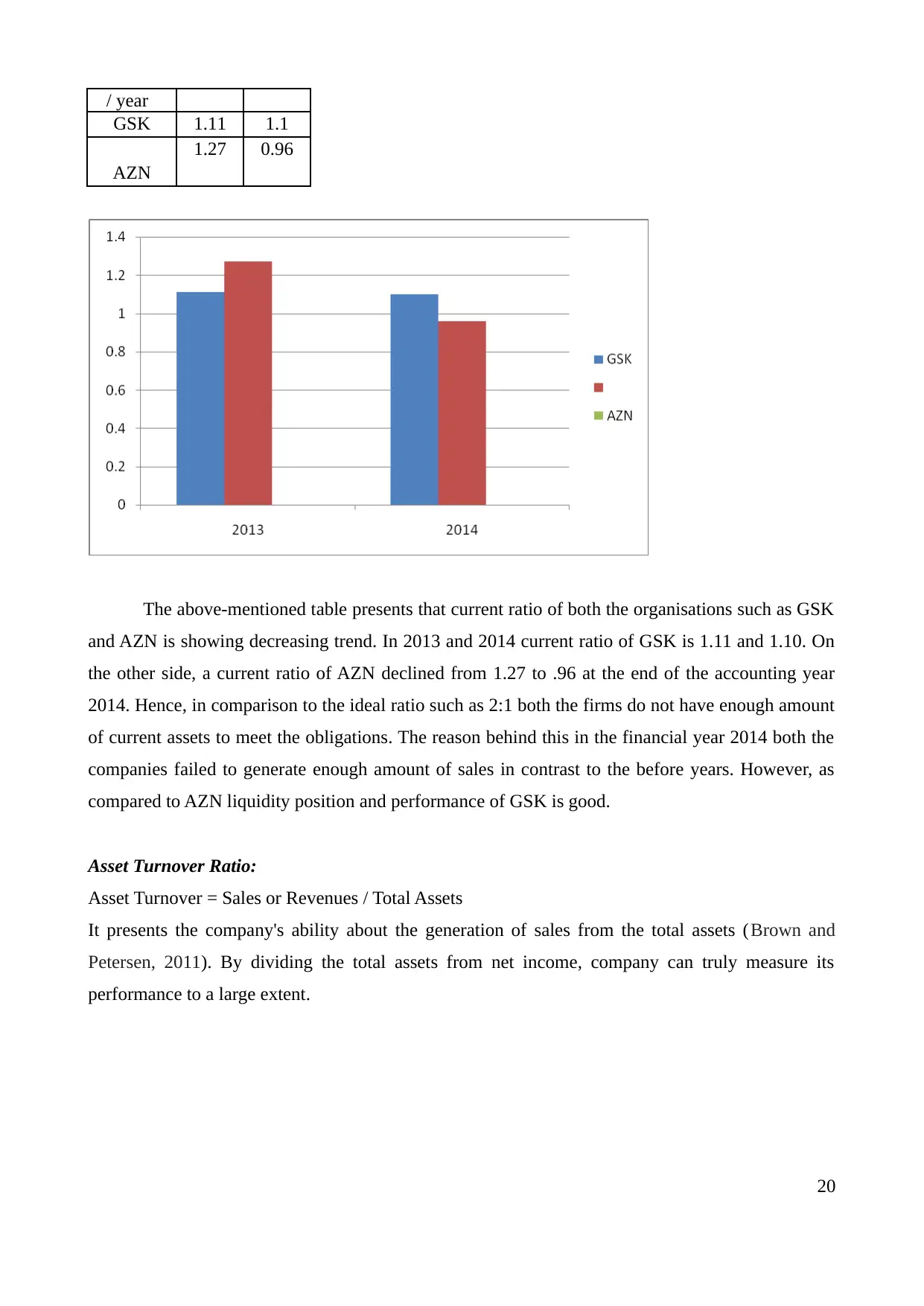

/ year

GSK 1.11 1.1

1.27 0.96

AZN

The above-mentioned table presents that current ratio of both the organisations such as GSK

and AZN is showing decreasing trend. In 2013 and 2014 current ratio of GSK is 1.11 and 1.10. On

the other side, a current ratio of AZN declined from 1.27 to .96 at the end of the accounting year

2014. Hence, in comparison to the ideal ratio such as 2:1 both the firms do not have enough amount

of current assets to meet the obligations. The reason behind this in the financial year 2014 both the

companies failed to generate enough amount of sales in contrast to the before years. However, as

compared to AZN liquidity position and performance of GSK is good.

Asset Turnover Ratio:

Asset Turnover = Sales or Revenues / Total Assets

It presents the company's ability about the generation of sales from the total assets (Brown and

Petersen, 2011). By dividing the total assets from net income, company can truly measure its

performance to a large extent.

20

GSK 1.11 1.1

1.27 0.96

AZN

The above-mentioned table presents that current ratio of both the organisations such as GSK

and AZN is showing decreasing trend. In 2013 and 2014 current ratio of GSK is 1.11 and 1.10. On

the other side, a current ratio of AZN declined from 1.27 to .96 at the end of the accounting year

2014. Hence, in comparison to the ideal ratio such as 2:1 both the firms do not have enough amount

of current assets to meet the obligations. The reason behind this in the financial year 2014 both the

companies failed to generate enough amount of sales in contrast to the before years. However, as

compared to AZN liquidity position and performance of GSK is good.

Asset Turnover Ratio:

Asset Turnover = Sales or Revenues / Total Assets

It presents the company's ability about the generation of sales from the total assets (Brown and

Petersen, 2011). By dividing the total assets from net income, company can truly measure its

performance to a large extent.

20

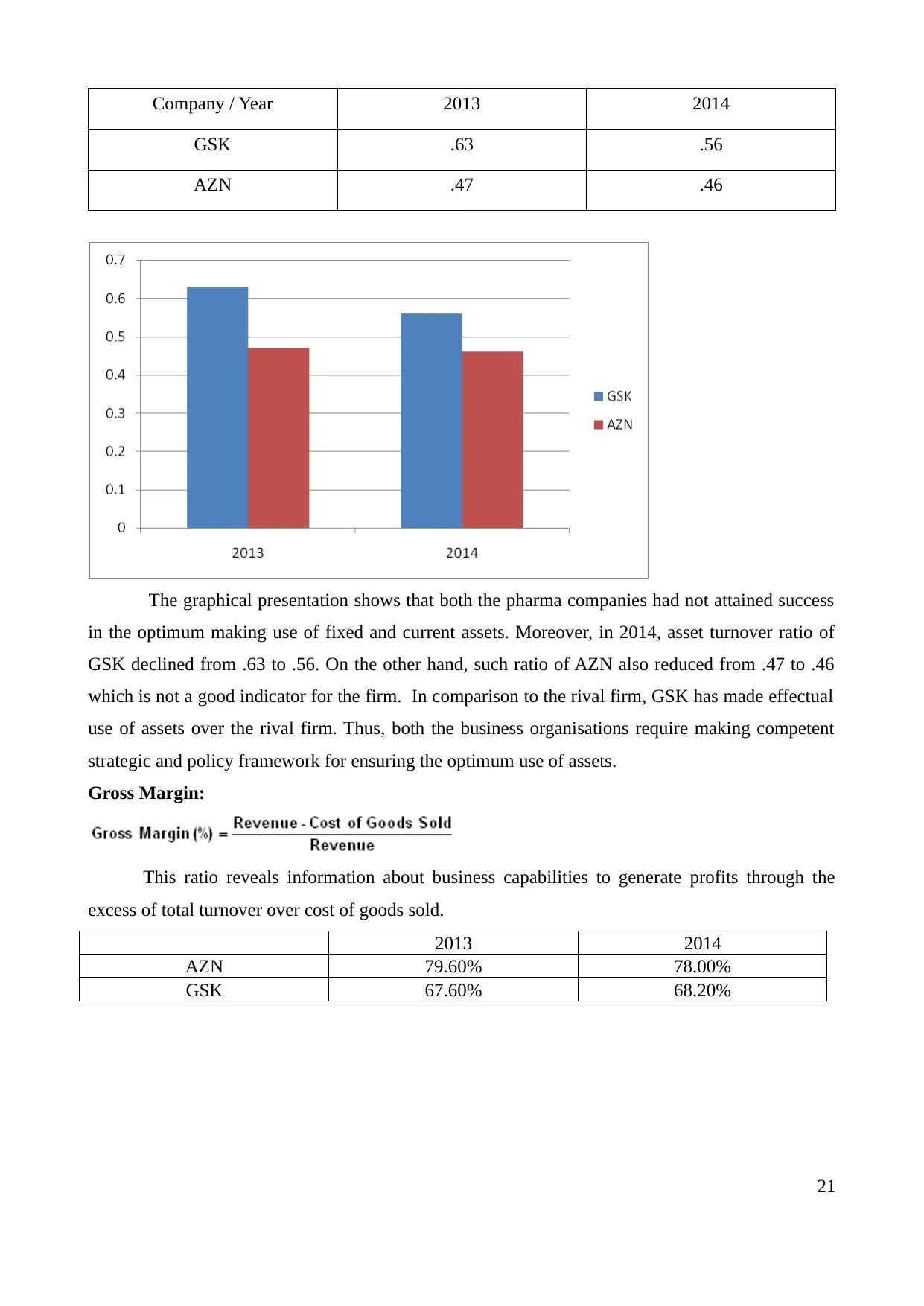

Company / Year 2013 2014

GSK .63 .56

AZN .47 .46

The graphical presentation shows that both the pharma companies had not attained success

in the optimum making use of fixed and current assets. Moreover, in 2014, asset turnover ratio of

GSK declined from .63 to .56. On the other hand, such ratio of AZN also reduced from .47 to .46

which is not a good indicator for the firm. In comparison to the rival firm, GSK has made effectual

use of assets over the rival firm. Thus, both the business organisations require making competent

strategic and policy framework for ensuring the optimum use of assets.

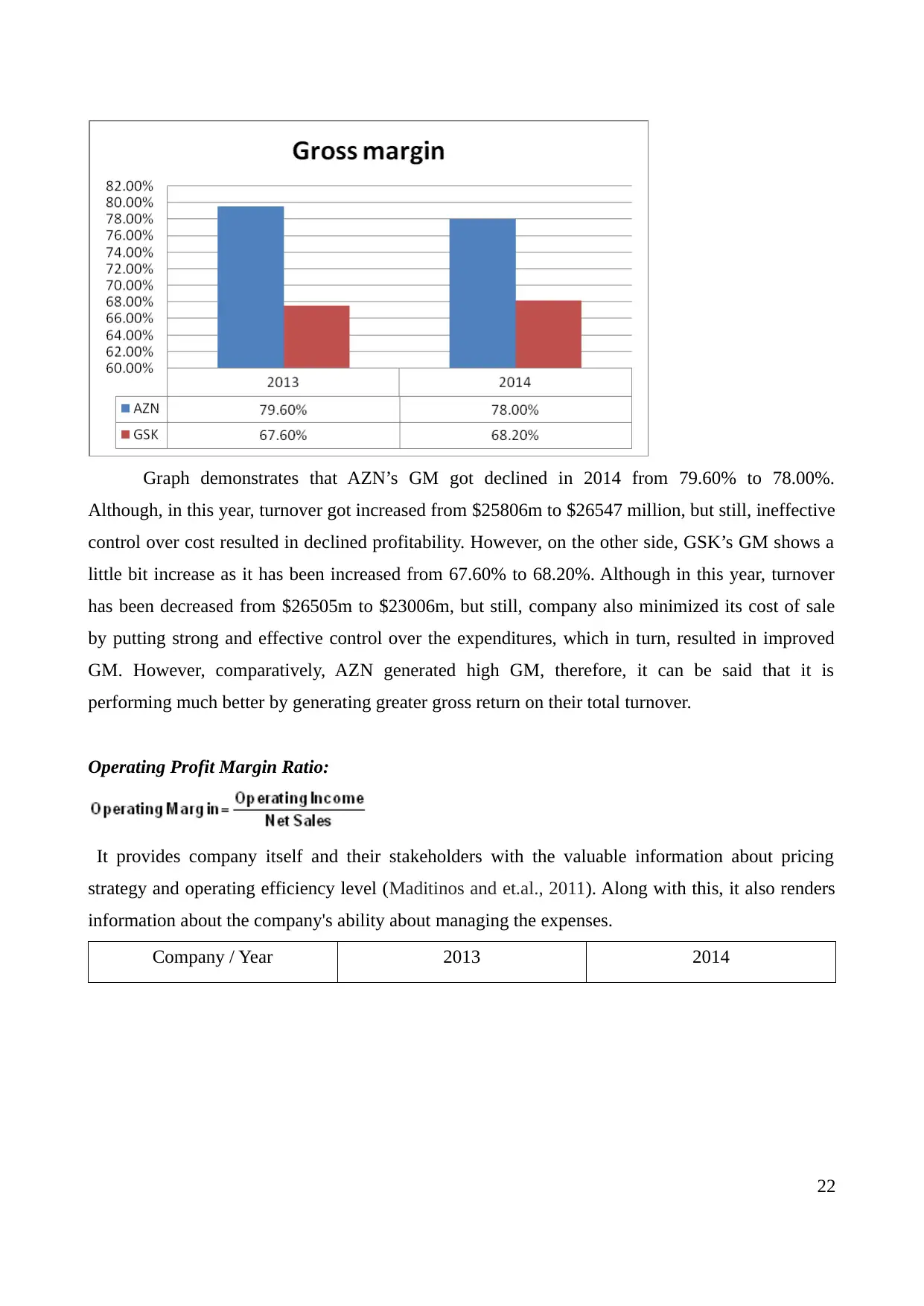

Gross Margin:

This ratio reveals information about business capabilities to generate profits through the

excess of total turnover over cost of goods sold.

2013 2014

AZN 79.60% 78.00%

GSK 67.60% 68.20%

21

GSK .63 .56

AZN .47 .46

The graphical presentation shows that both the pharma companies had not attained success

in the optimum making use of fixed and current assets. Moreover, in 2014, asset turnover ratio of

GSK declined from .63 to .56. On the other hand, such ratio of AZN also reduced from .47 to .46

which is not a good indicator for the firm. In comparison to the rival firm, GSK has made effectual

use of assets over the rival firm. Thus, both the business organisations require making competent

strategic and policy framework for ensuring the optimum use of assets.

Gross Margin:

This ratio reveals information about business capabilities to generate profits through the

excess of total turnover over cost of goods sold.

2013 2014

AZN 79.60% 78.00%

GSK 67.60% 68.20%

21

Graph demonstrates that AZN’s GM got declined in 2014 from 79.60% to 78.00%.

Although, in this year, turnover got increased from $25806m to $26547 million, but still, ineffective

control over cost resulted in declined profitability. However, on the other side, GSK’s GM shows a

little bit increase as it has been increased from 67.60% to 68.20%. Although in this year, turnover

has been decreased from $26505m to $23006m, but still, company also minimized its cost of sale

by putting strong and effective control over the expenditures, which in turn, resulted in improved

GM. However, comparatively, AZN generated high GM, therefore, it can be said that it is

performing much better by generating greater gross return on their total turnover.

Operating Profit Margin Ratio:

It provides company itself and their stakeholders with the valuable information about pricing

strategy and operating efficiency level (Maditinos and et.al., 2011). Along with this, it also renders

information about the company's ability about managing the expenses.

Company / Year 2013 2014

22

Although, in this year, turnover got increased from $25806m to $26547 million, but still, ineffective

control over cost resulted in declined profitability. However, on the other side, GSK’s GM shows a

little bit increase as it has been increased from 67.60% to 68.20%. Although in this year, turnover

has been decreased from $26505m to $23006m, but still, company also minimized its cost of sale

by putting strong and effective control over the expenditures, which in turn, resulted in improved

GM. However, comparatively, AZN generated high GM, therefore, it can be said that it is

performing much better by generating greater gross return on their total turnover.

Operating Profit Margin Ratio:

It provides company itself and their stakeholders with the valuable information about pricing

strategy and operating efficiency level (Maditinos and et.al., 2011). Along with this, it also renders

information about the company's ability about managing the expenses.

Company / Year 2013 2014

22

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

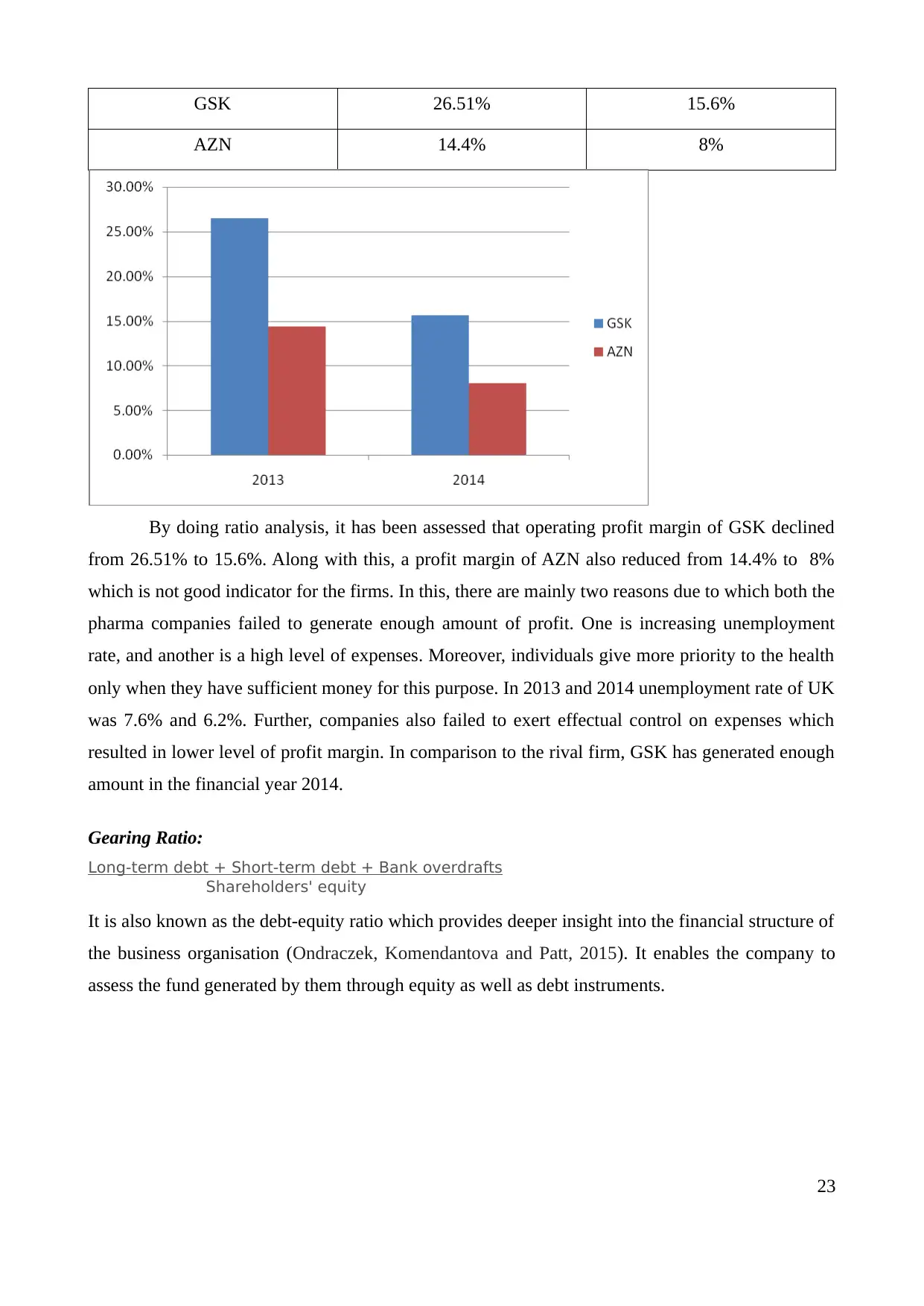

GSK 26.51% 15.6%

AZN 14.4% 8%

By doing ratio analysis, it has been assessed that operating profit margin of GSK declined

from 26.51% to 15.6%. Along with this, a profit margin of AZN also reduced from 14.4% to 8%

which is not good indicator for the firms. In this, there are mainly two reasons due to which both the

pharma companies failed to generate enough amount of profit. One is increasing unemployment

rate, and another is a high level of expenses. Moreover, individuals give more priority to the health

only when they have sufficient money for this purpose. In 2013 and 2014 unemployment rate of UK

was 7.6% and 6.2%. Further, companies also failed to exert effectual control on expenses which

resulted in lower level of profit margin. In comparison to the rival firm, GSK has generated enough

amount in the financial year 2014.

Gearing Ratio:

Long-term debt + Short-term debt + Bank overdrafts

Shareholders' equity

It is also known as the debt-equity ratio which provides deeper insight into the financial structure of

the business organisation (Ondraczek, Komendantova and Patt, 2015). It enables the company to

assess the fund generated by them through equity as well as debt instruments.

23

AZN 14.4% 8%

By doing ratio analysis, it has been assessed that operating profit margin of GSK declined

from 26.51% to 15.6%. Along with this, a profit margin of AZN also reduced from 14.4% to 8%

which is not good indicator for the firms. In this, there are mainly two reasons due to which both the

pharma companies failed to generate enough amount of profit. One is increasing unemployment

rate, and another is a high level of expenses. Moreover, individuals give more priority to the health

only when they have sufficient money for this purpose. In 2013 and 2014 unemployment rate of UK

was 7.6% and 6.2%. Further, companies also failed to exert effectual control on expenses which

resulted in lower level of profit margin. In comparison to the rival firm, GSK has generated enough

amount in the financial year 2014.

Gearing Ratio:

Long-term debt + Short-term debt + Bank overdrafts

Shareholders' equity

It is also known as the debt-equity ratio which provides deeper insight into the financial structure of

the business organisation (Ondraczek, Komendantova and Patt, 2015). It enables the company to

assess the fund generated by them through equity as well as debt instruments.

23

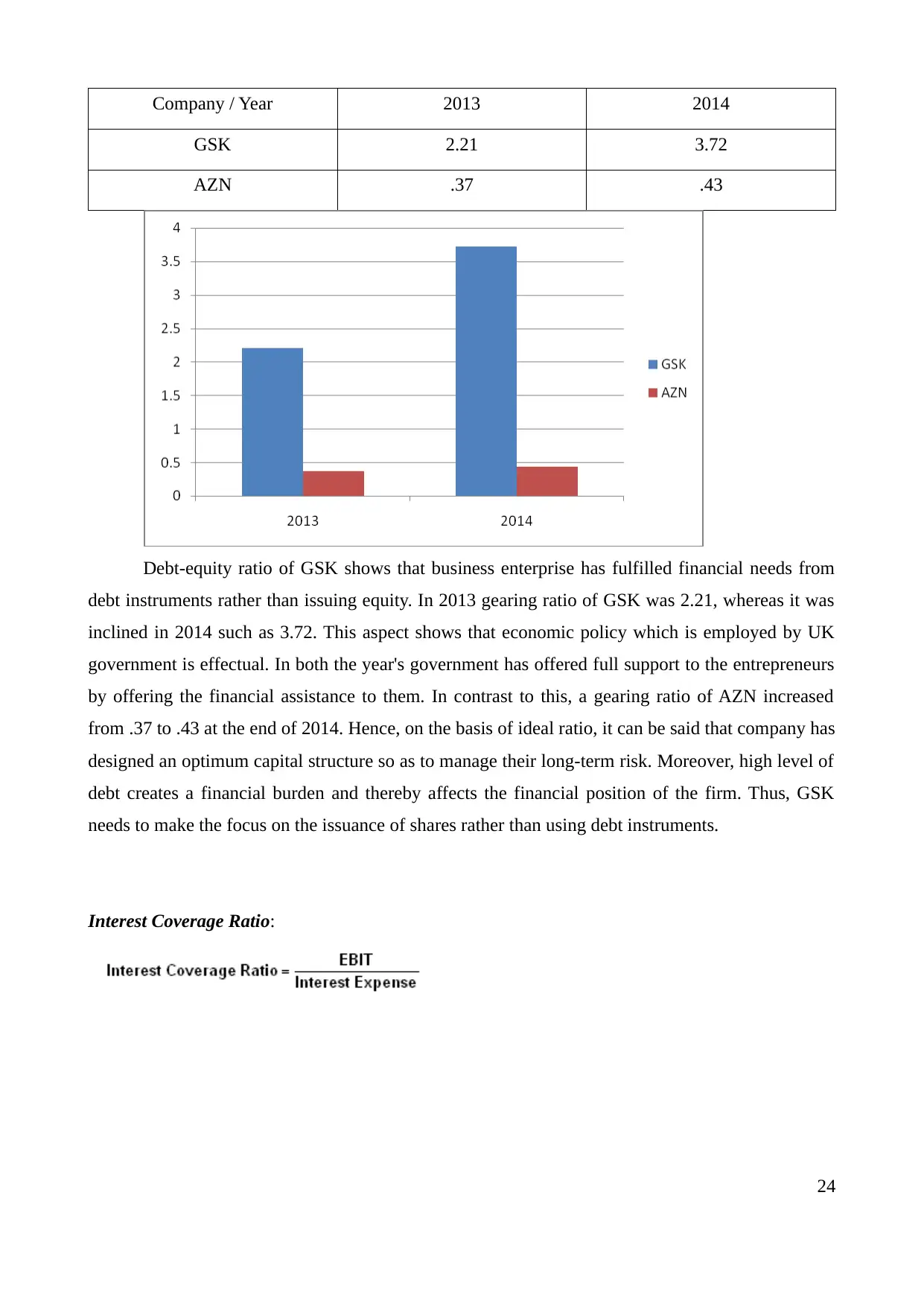

Company / Year 2013 2014

GSK 2.21 3.72

AZN .37 .43

Debt-equity ratio of GSK shows that business enterprise has fulfilled financial needs from

debt instruments rather than issuing equity. In 2013 gearing ratio of GSK was 2.21, whereas it was

inclined in 2014 such as 3.72. This aspect shows that economic policy which is employed by UK

government is effectual. In both the year's government has offered full support to the entrepreneurs

by offering the financial assistance to them. In contrast to this, a gearing ratio of AZN increased

from .37 to .43 at the end of 2014. Hence, on the basis of ideal ratio, it can be said that company has

designed an optimum capital structure so as to manage their long-term risk. Moreover, high level of

debt creates a financial burden and thereby affects the financial position of the firm. Thus, GSK

needs to make the focus on the issuance of shares rather than using debt instruments.

Interest Coverage Ratio:

24

GSK 2.21 3.72

AZN .37 .43

Debt-equity ratio of GSK shows that business enterprise has fulfilled financial needs from

debt instruments rather than issuing equity. In 2013 gearing ratio of GSK was 2.21, whereas it was

inclined in 2014 such as 3.72. This aspect shows that economic policy which is employed by UK

government is effectual. In both the year's government has offered full support to the entrepreneurs

by offering the financial assistance to them. In contrast to this, a gearing ratio of AZN increased

from .37 to .43 at the end of 2014. Hence, on the basis of ideal ratio, it can be said that company has

designed an optimum capital structure so as to manage their long-term risk. Moreover, high level of

debt creates a financial burden and thereby affects the financial position of the firm. Thus, GSK

needs to make the focus on the issuance of shares rather than using debt instruments.

Interest Coverage Ratio:

24

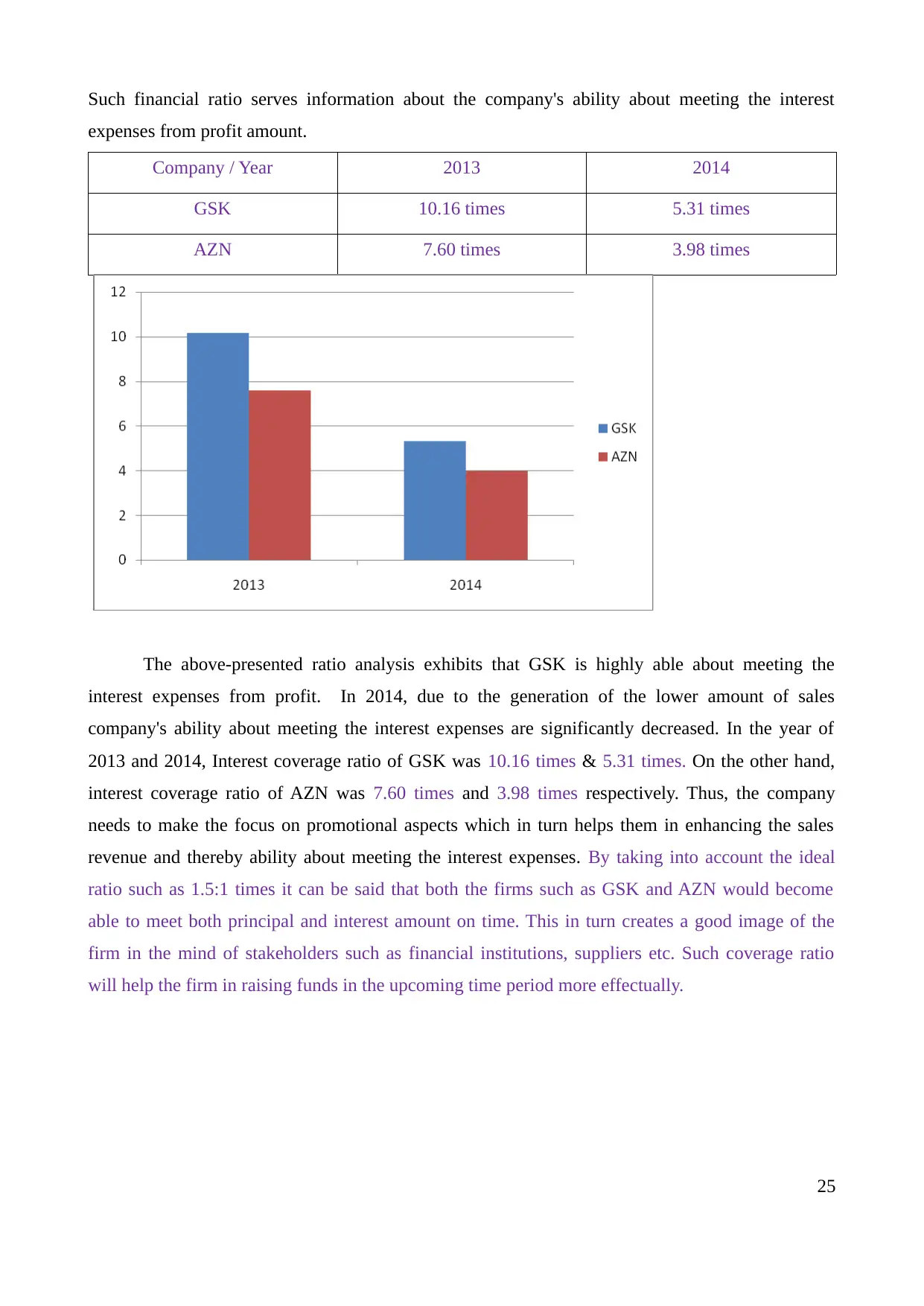

Such financial ratio serves information about the company's ability about meeting the interest

expenses from profit amount.

Company / Year 2013 2014

GSK 10.16 times 5.31 times

AZN 7.60 times 3.98 times

The above-presented ratio analysis exhibits that GSK is highly able about meeting the

interest expenses from profit. In 2014, due to the generation of the lower amount of sales

company's ability about meeting the interest expenses are significantly decreased. In the year of

2013 and 2014, Interest coverage ratio of GSK was 10.16 times & 5.31 times. On the other hand,

interest coverage ratio of AZN was 7.60 times and 3.98 times respectively. Thus, the company

needs to make the focus on promotional aspects which in turn helps them in enhancing the sales

revenue and thereby ability about meeting the interest expenses. By taking into account the ideal

ratio such as 1.5:1 times it can be said that both the firms such as GSK and AZN would become

able to meet both principal and interest amount on time. This in turn creates a good image of the

firm in the mind of stakeholders such as financial institutions, suppliers etc. Such coverage ratio

will help the firm in raising funds in the upcoming time period more effectually.

25

expenses from profit amount.

Company / Year 2013 2014

GSK 10.16 times 5.31 times

AZN 7.60 times 3.98 times

The above-presented ratio analysis exhibits that GSK is highly able about meeting the

interest expenses from profit. In 2014, due to the generation of the lower amount of sales

company's ability about meeting the interest expenses are significantly decreased. In the year of

2013 and 2014, Interest coverage ratio of GSK was 10.16 times & 5.31 times. On the other hand,

interest coverage ratio of AZN was 7.60 times and 3.98 times respectively. Thus, the company

needs to make the focus on promotional aspects which in turn helps them in enhancing the sales

revenue and thereby ability about meeting the interest expenses. By taking into account the ideal

ratio such as 1.5:1 times it can be said that both the firms such as GSK and AZN would become

able to meet both principal and interest amount on time. This in turn creates a good image of the

firm in the mind of stakeholders such as financial institutions, suppliers etc. Such coverage ratio

will help the firm in raising funds in the upcoming time period more effectually.

25

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

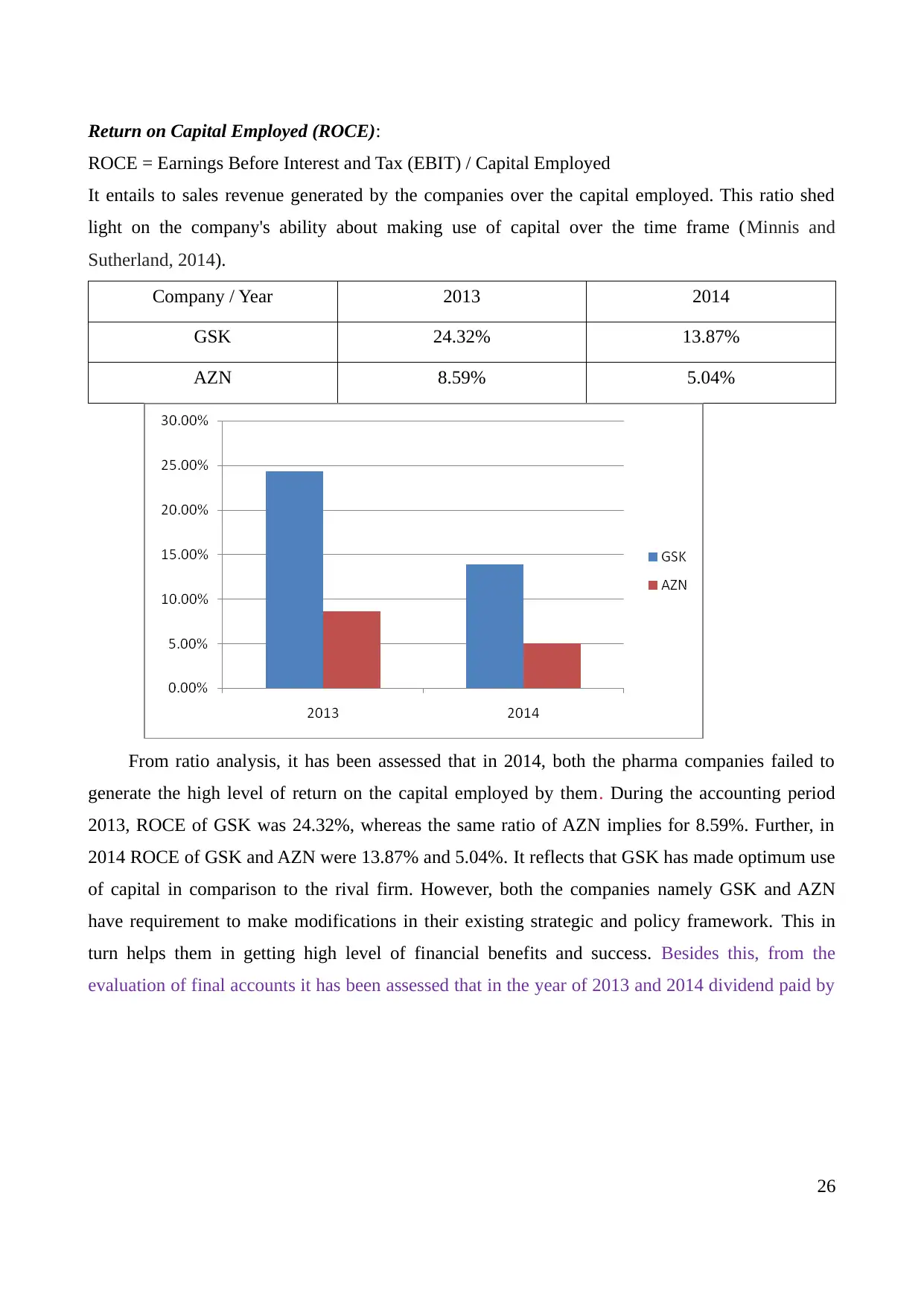

Return on Capital Employed (ROCE):

ROCE = Earnings Before Interest and Tax (EBIT) / Capital Employed

It entails to sales revenue generated by the companies over the capital employed. This ratio shed

light on the company's ability about making use of capital over the time frame (Minnis and

Sutherland, 2014).

Company / Year 2013 2014

GSK 24.32% 13.87%

AZN 8.59% 5.04%

From ratio analysis, it has been assessed that in 2014, both the pharma companies failed to

generate the high level of return on the capital employed by them. During the accounting period

2013, ROCE of GSK was 24.32%, whereas the same ratio of AZN implies for 8.59%. Further, in

2014 ROCE of GSK and AZN were 13.87% and 5.04%. It reflects that GSK has made optimum use

of capital in comparison to the rival firm. However, both the companies namely GSK and AZN

have requirement to make modifications in their existing strategic and policy framework. This in

turn helps them in getting high level of financial benefits and success. Besides this, from the

evaluation of final accounts it has been assessed that in the year of 2013 and 2014 dividend paid by

26

ROCE = Earnings Before Interest and Tax (EBIT) / Capital Employed

It entails to sales revenue generated by the companies over the capital employed. This ratio shed

light on the company's ability about making use of capital over the time frame (Minnis and

Sutherland, 2014).

Company / Year 2013 2014

GSK 24.32% 13.87%

AZN 8.59% 5.04%

From ratio analysis, it has been assessed that in 2014, both the pharma companies failed to

generate the high level of return on the capital employed by them. During the accounting period

2013, ROCE of GSK was 24.32%, whereas the same ratio of AZN implies for 8.59%. Further, in

2014 ROCE of GSK and AZN were 13.87% and 5.04%. It reflects that GSK has made optimum use

of capital in comparison to the rival firm. However, both the companies namely GSK and AZN

have requirement to make modifications in their existing strategic and policy framework. This in

turn helps them in getting high level of financial benefits and success. Besides this, from the

evaluation of final accounts it has been assessed that in the year of 2013 and 2014 dividend paid by

26

GSK accounts for £1.56 and £1.60 GBP respectively. On the other hand, during the similar time

period, dividend paid by AZN was constant such as £1.40 GBP. By taking into account such aspect

it can be stated that higher returns were offered by GSK to investors in the form of dividend as

compared to AZN. However, dividend amount provided by GSK to investors were not high. Thus,

both the firms require to undertake sound strategic framework which in turn facilitate effectual as of

shareholder’s equity.

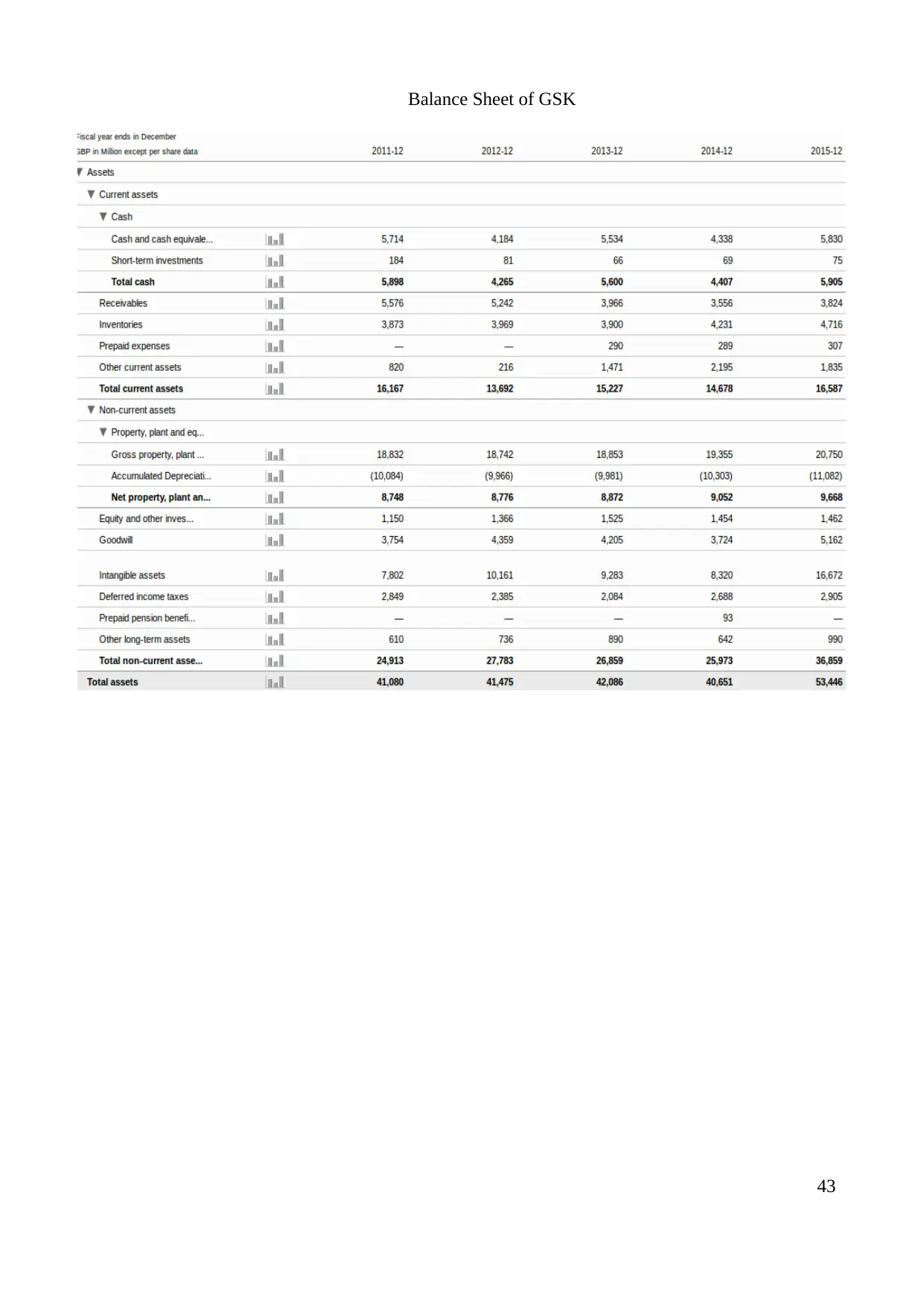

FINANCING

In the present era, to cope with the dynamic business aspects, it is highly required for the company

to invest money in fixed assets. Hence, with the aim to fulfil the goals and objectives business unit

has to make the investment in the land & building, machinery, etc. (Picker, 2016). On the basis of

the cited case situation, GSK requires 20% of the net assets for making the investment in the land &

building. From this aspect, the business unit needs the fund of £852.6 million for the investment

purpose. In this regard, by taking into account the several internal and external sources, GSK can

fulfil the financial requirements to a large extent.

Amount required = [Total assets – total liabilities] * 20%

Particulars Amount (in £ Mio)

Total assets 40,651

Total liabilities 36,388

Net assets 4,263

Amount required (4263*20%) 852.6

Sources of finance

Internal sources External sources

Retained profit

Sales of non-productive assets

Issue share capital

Leasing

Loans

27

period, dividend paid by AZN was constant such as £1.40 GBP. By taking into account such aspect

it can be stated that higher returns were offered by GSK to investors in the form of dividend as

compared to AZN. However, dividend amount provided by GSK to investors were not high. Thus,

both the firms require to undertake sound strategic framework which in turn facilitate effectual as of

shareholder’s equity.

FINANCING

In the present era, to cope with the dynamic business aspects, it is highly required for the company

to invest money in fixed assets. Hence, with the aim to fulfil the goals and objectives business unit

has to make the investment in the land & building, machinery, etc. (Picker, 2016). On the basis of

the cited case situation, GSK requires 20% of the net assets for making the investment in the land &

building. From this aspect, the business unit needs the fund of £852.6 million for the investment

purpose. In this regard, by taking into account the several internal and external sources, GSK can

fulfil the financial requirements to a large extent.

Amount required = [Total assets – total liabilities] * 20%

Particulars Amount (in £ Mio)

Total assets 40,651

Total liabilities 36,388

Net assets 4,263

Amount required (4263*20%) 852.6

Sources of finance

Internal sources External sources

Retained profit

Sales of non-productive assets

Issue share capital

Leasing

Loans

27

Discounts receivables

External sources of financing

External sources refer to those which are available outside the business organization. In this,

external sources which GSK can undertake for raising capital are enumerated below:

Issue of equity shares: It is one of most effectual sources which can be undertaken by GSK

to meet the financial needs. According to the outcome of ratio analysis in the financial year, 2014

business enterprise has fulfilled more of its needs from debt sources as compared to equity. In this,

GSK can develop sound financial structure by issuing shares to the general public at large. Thus, by

attracting both existing and potential shareholders business unit can generate enough amount of

fund for purchasing the land and building (Uechi and et.al., 2015). Usually, shareholders are ready

to invest money in the firm's operations which is growing and offer the high dividend to the

shareholders. In this, by offering shares to people business enterprise can raise finance.

The major benefits of this method is that it reduces the fixed financial burden of the company.

Moreover, in shares company offers a dividend to the shareholders only when it earns enough

amount of profit margin. In this way, by issuing the shares company can enjoy the financial benefits

(Robinson and et.al., 2015). However, on the critical note, such source of finance increases the

interference of the shareholders in the decision-making aspect. The reason behind this shareholder

has the legal right to take part in the decision-making by voting rights provided to them. In the year

2013, GSK’s total share capital was reported to £42,086m that has been decreased to £40,651m,

whilst in the next year, 2015, it got improved to £53,446m indicates that this year, company

gathered more capital through issuing additional shares in order to fulfil corporation’s long-term

capital requirement.

Loan capital: GSK can also obtain required capital through acquiring bank loan, but at the

28

External sources of financing

External sources refer to those which are available outside the business organization. In this,

external sources which GSK can undertake for raising capital are enumerated below:

Issue of equity shares: It is one of most effectual sources which can be undertaken by GSK

to meet the financial needs. According to the outcome of ratio analysis in the financial year, 2014

business enterprise has fulfilled more of its needs from debt sources as compared to equity. In this,

GSK can develop sound financial structure by issuing shares to the general public at large. Thus, by

attracting both existing and potential shareholders business unit can generate enough amount of

fund for purchasing the land and building (Uechi and et.al., 2015). Usually, shareholders are ready

to invest money in the firm's operations which is growing and offer the high dividend to the

shareholders. In this, by offering shares to people business enterprise can raise finance.

The major benefits of this method is that it reduces the fixed financial burden of the company.

Moreover, in shares company offers a dividend to the shareholders only when it earns enough

amount of profit margin. In this way, by issuing the shares company can enjoy the financial benefits

(Robinson and et.al., 2015). However, on the critical note, such source of finance increases the

interference of the shareholders in the decision-making aspect. The reason behind this shareholder

has the legal right to take part in the decision-making by voting rights provided to them. In the year

2013, GSK’s total share capital was reported to £42,086m that has been decreased to £40,651m,

whilst in the next year, 2015, it got improved to £53,446m indicates that this year, company

gathered more capital through issuing additional shares in order to fulfil corporation’s long-term

capital requirement.

Loan capital: GSK can also obtain required capital through acquiring bank loan, but at the

28

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

same time, it is also necessary for the firm to make sure that it is able to bear the fixed burden

charged on the loans. In the year 2013, GSK’s long-term debt has been reported to £15456m got

inclined to £15,841m, thus, it indicates that this year, GSK meet-out their long-term debt capital

requirement through more debt resources. While, in 2015, company repaid the capital worth £517m

and as a result, in the annual financial statement, company reported their debt capital to £15324m.

Excessive loan brings financial burden to the organizations but at the same time, it also drive

taxation benefits to the organizations because taxation authorities grant deductions to the extent of

interest payment, which in turn, increase net yield. Moreover, debt-holders do not have right to take

part in GSK’s corporate decisions, thus, it provides full freedom to the managers to take business

decisions.

Leasing: GSK can also fulfil the need about making an investment in the land and building

by taking it on the lease. This source of finance offers the tax benefit to the firm and thereby

enhances the profit margin of the firm. Along with this, leasing also offers the opportunity to the

business enterprise to make use of land and building for the expansion purpose without making any

huge investment on it (Upton and et.al., 2015). Moreover, in lease GSK will only be obliged to

make payment of rent in return for making use of the asset. In this way, by acquiring the land and

building GSK can execute the business plan more effectually and efficiently. However, in leasing

business enterprise is obliged to make use of assets according to the contractual aspects. This aspect

acts as a barrier and thereby creates difficulty in front of the firm about the execution of a plan.

Discounting receivables: Business enterprise can meet the financial requirements of £852.6

million by discounting the receivables from the financial institution. Now, financial institutions

offer early payment facility to the business customers by charging some discounting cost. It is

another effective source which help company in generating fund. Moreover, discounting cost which

is charged by the banks lower than the other cost of financing. However, this aspect closely

influences the working capital of the firm (Valentin and Mihaela–Andreea, 2015). Moreover,

working capital reflects the balance of current assets and liabilities. Along with this, it will also

influence the current ratio of the firm. In 2014, the current ratio of GSK was only 1.10 so, if the

29

charged on the loans. In the year 2013, GSK’s long-term debt has been reported to £15456m got

inclined to £15,841m, thus, it indicates that this year, GSK meet-out their long-term debt capital

requirement through more debt resources. While, in 2015, company repaid the capital worth £517m

and as a result, in the annual financial statement, company reported their debt capital to £15324m.

Excessive loan brings financial burden to the organizations but at the same time, it also drive

taxation benefits to the organizations because taxation authorities grant deductions to the extent of

interest payment, which in turn, increase net yield. Moreover, debt-holders do not have right to take

part in GSK’s corporate decisions, thus, it provides full freedom to the managers to take business

decisions.

Leasing: GSK can also fulfil the need about making an investment in the land and building