Evaluating Capital Investment Options with Quantitative Methods

VerifiedAdded on 2020/05/16

|14

|1960

|234

AI Summary

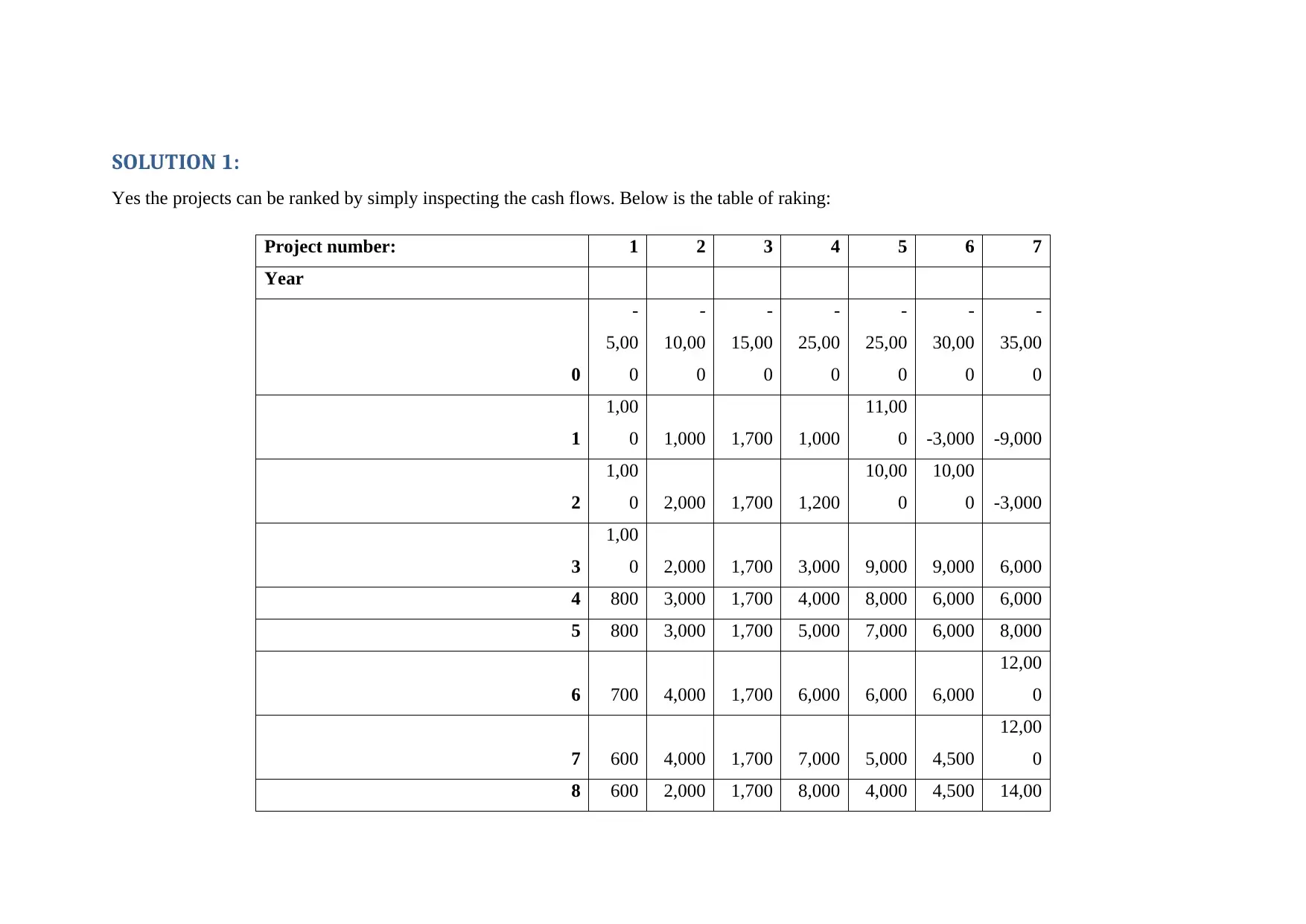

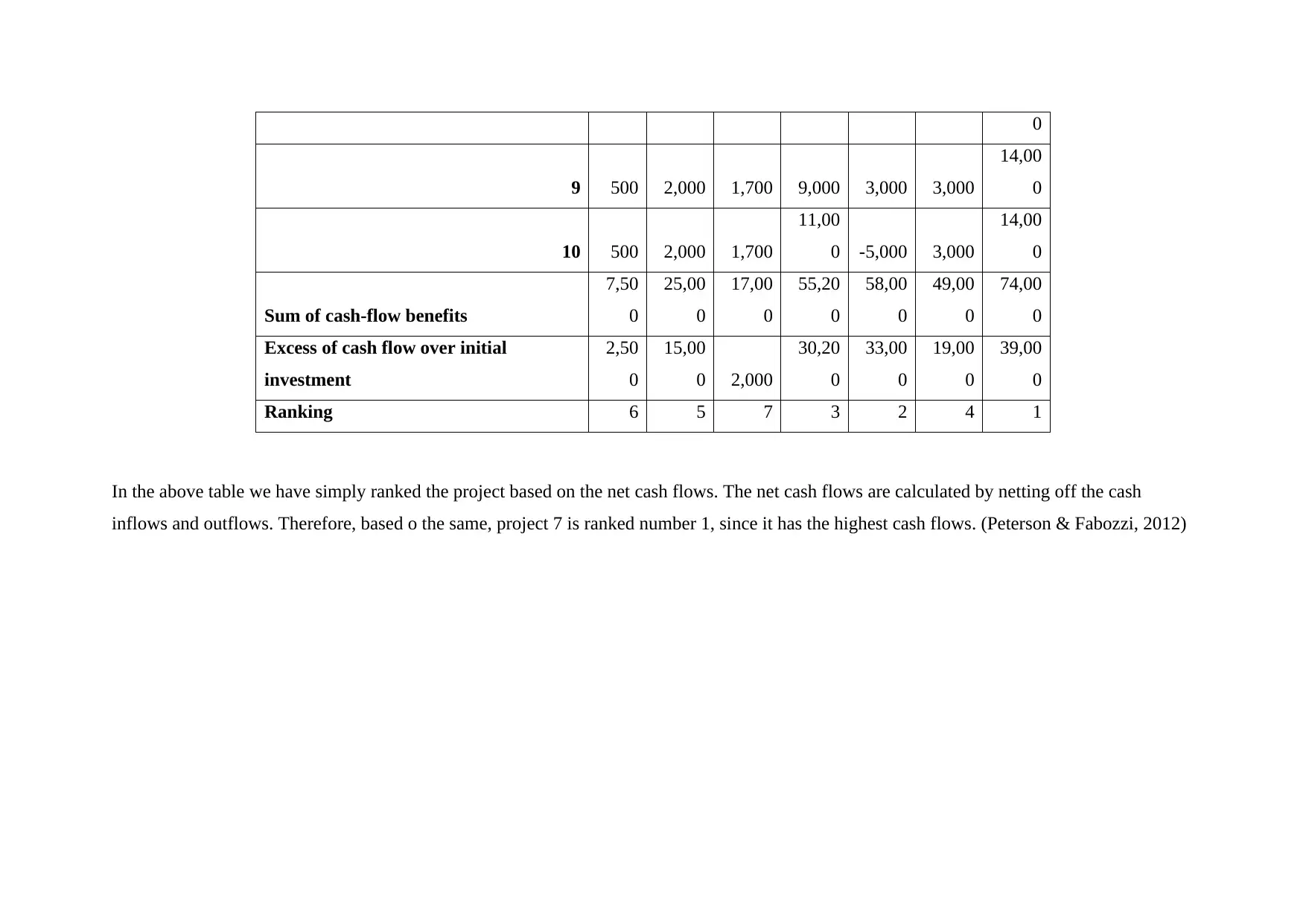

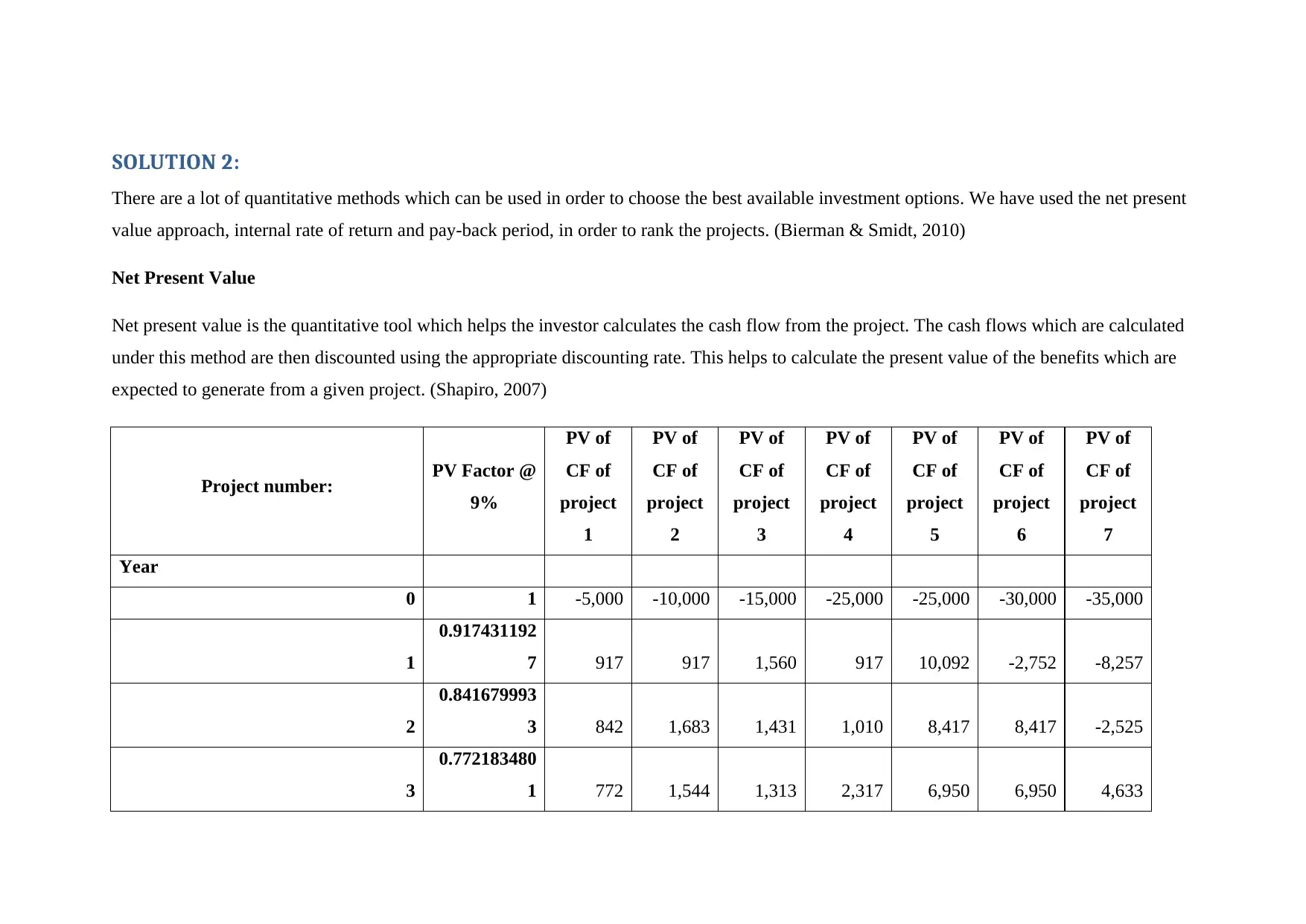

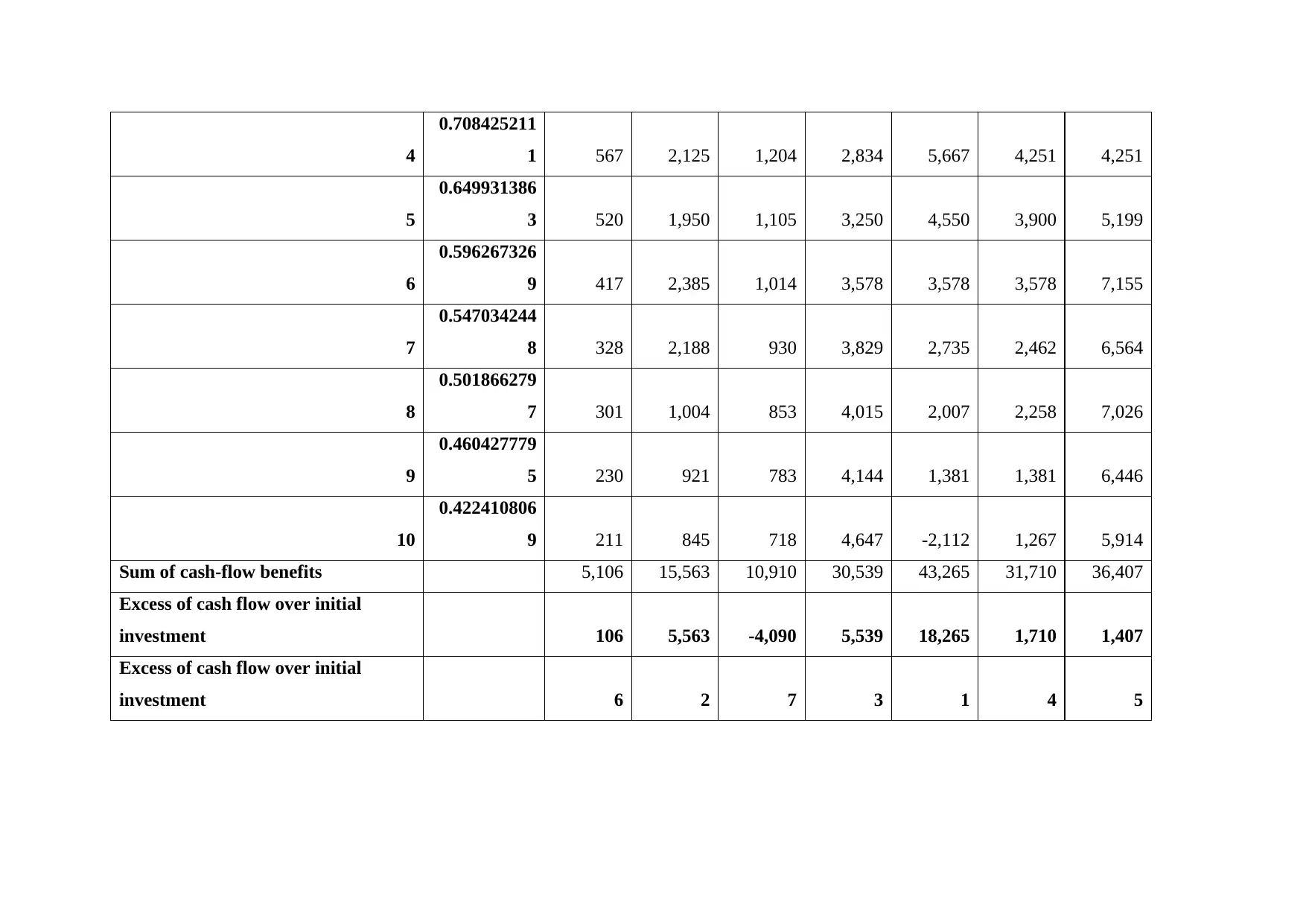

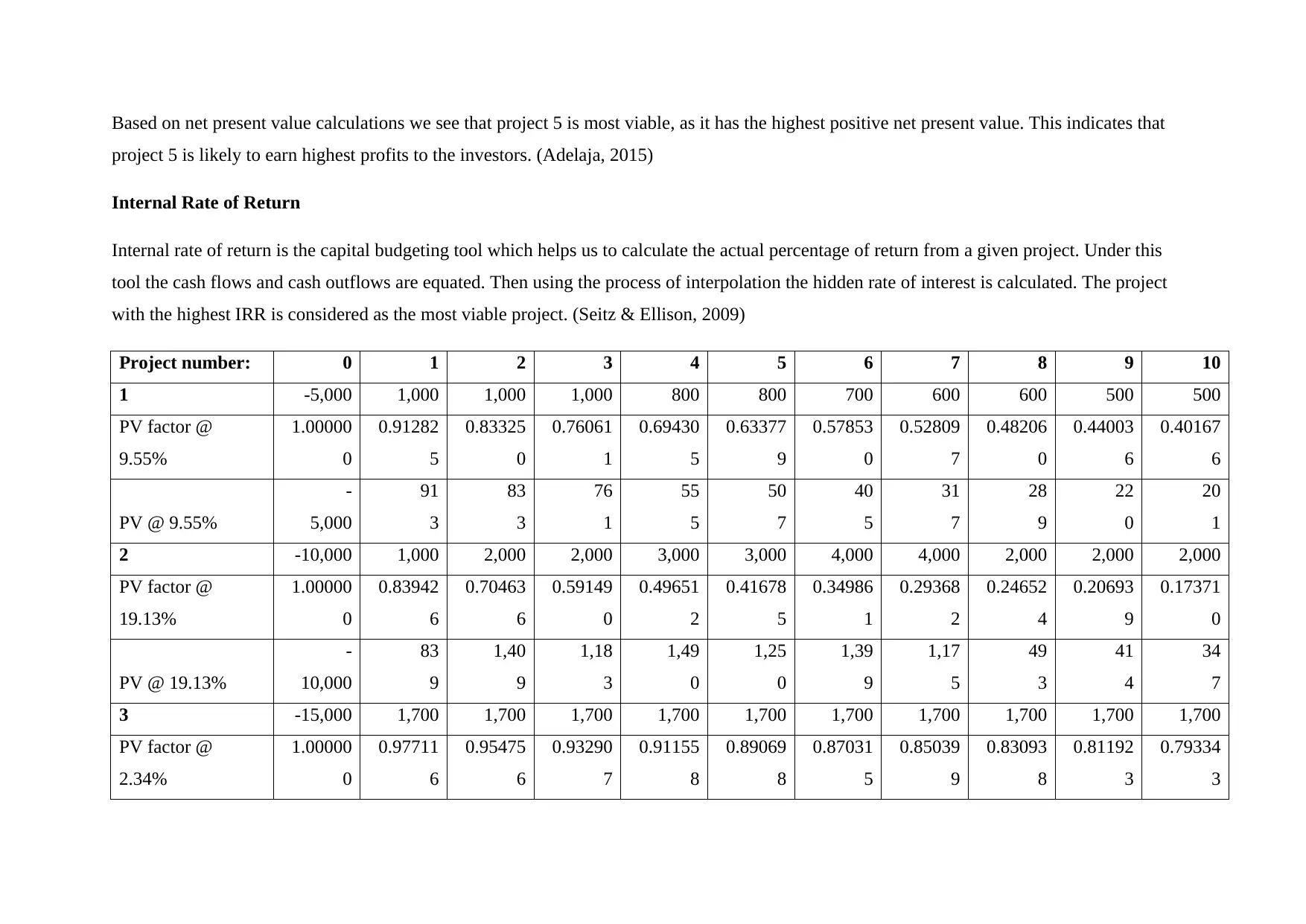

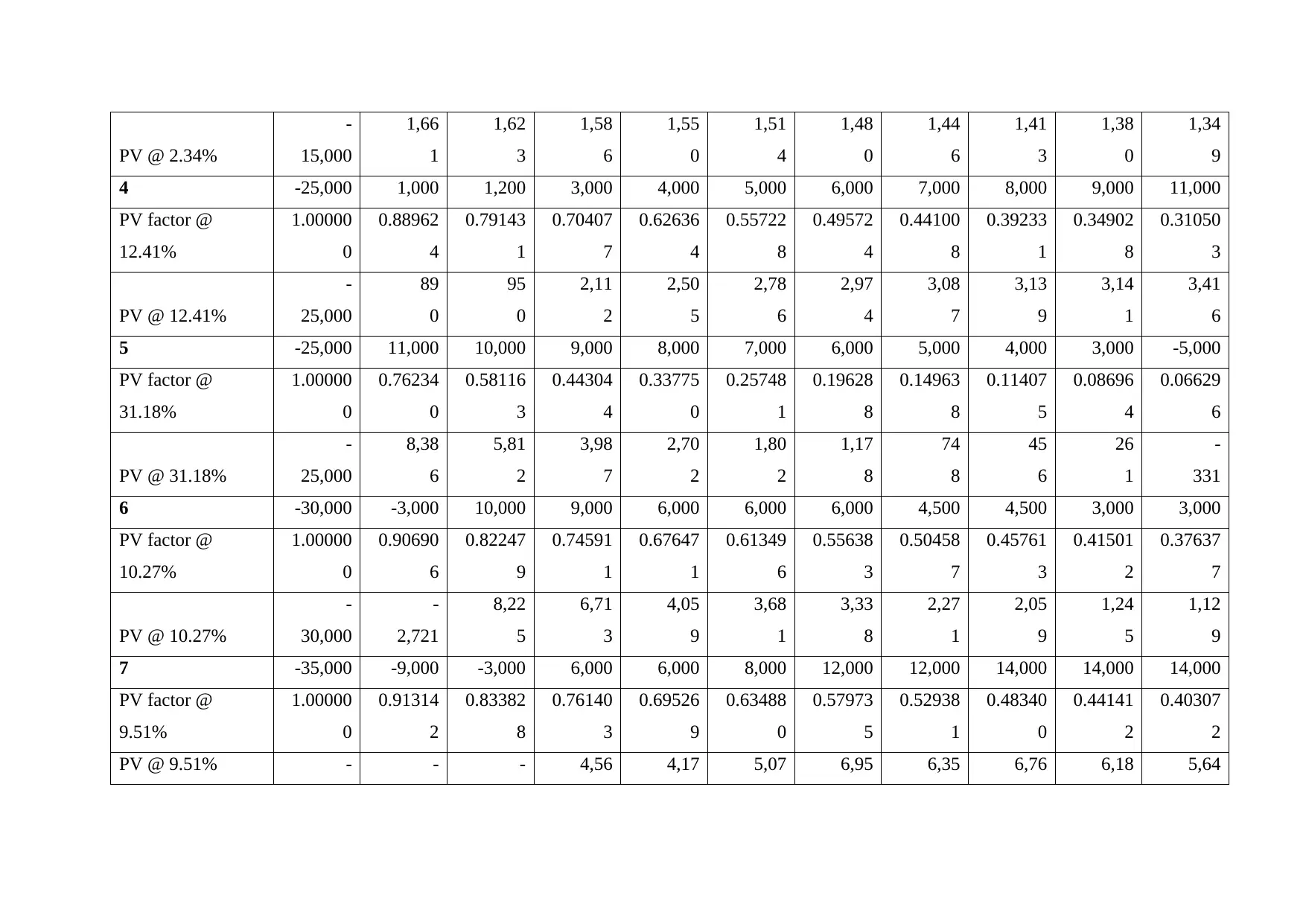

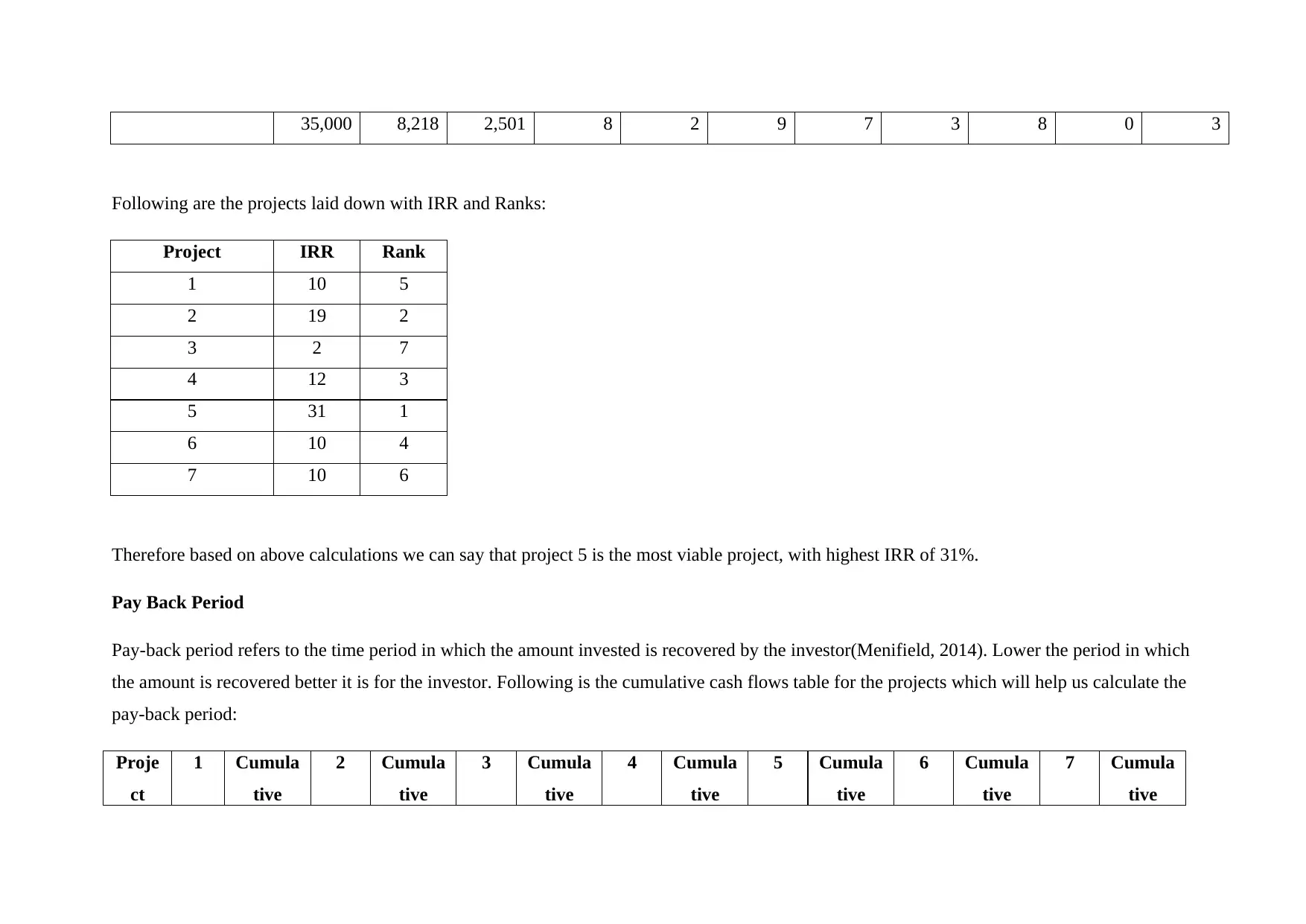

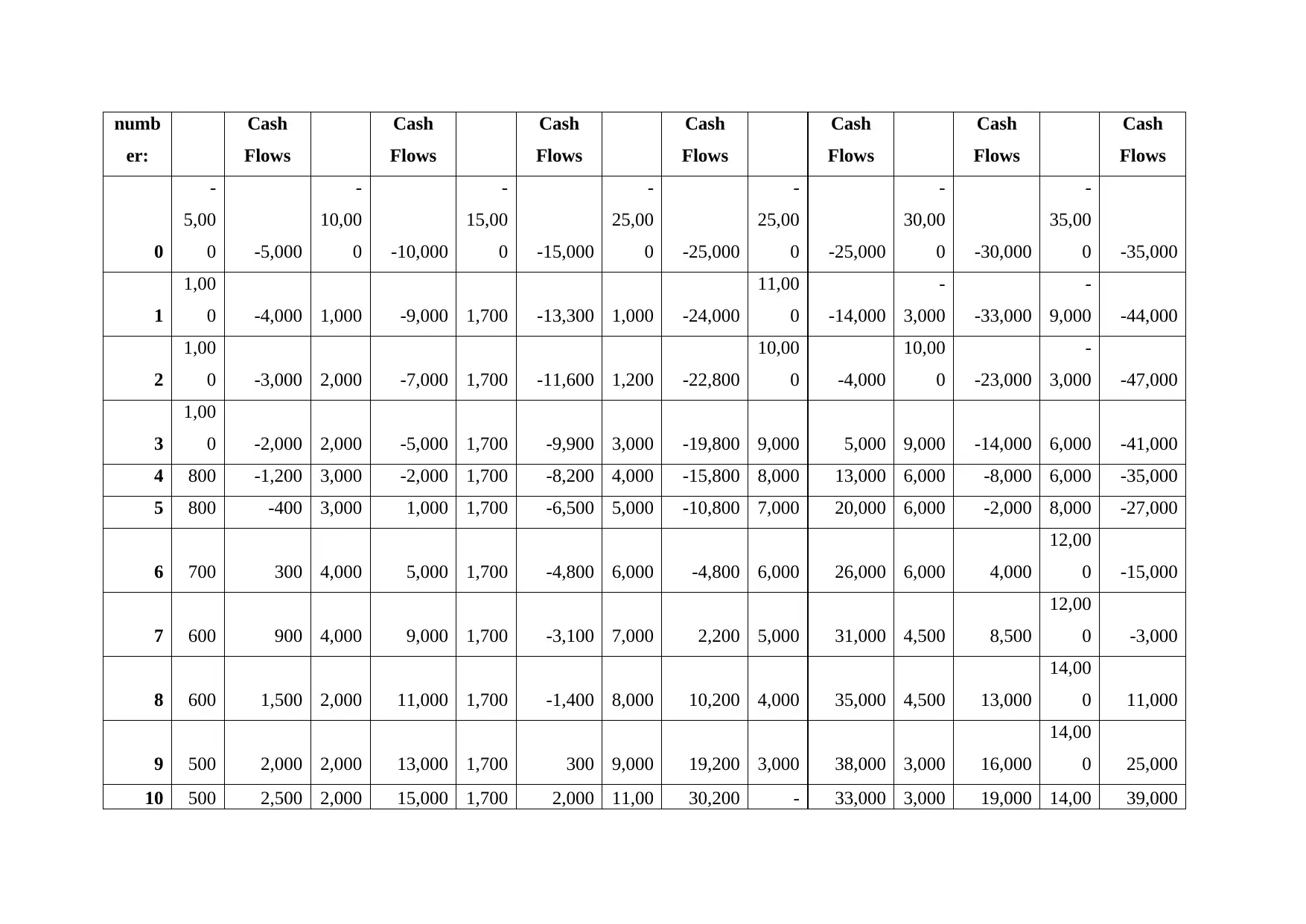

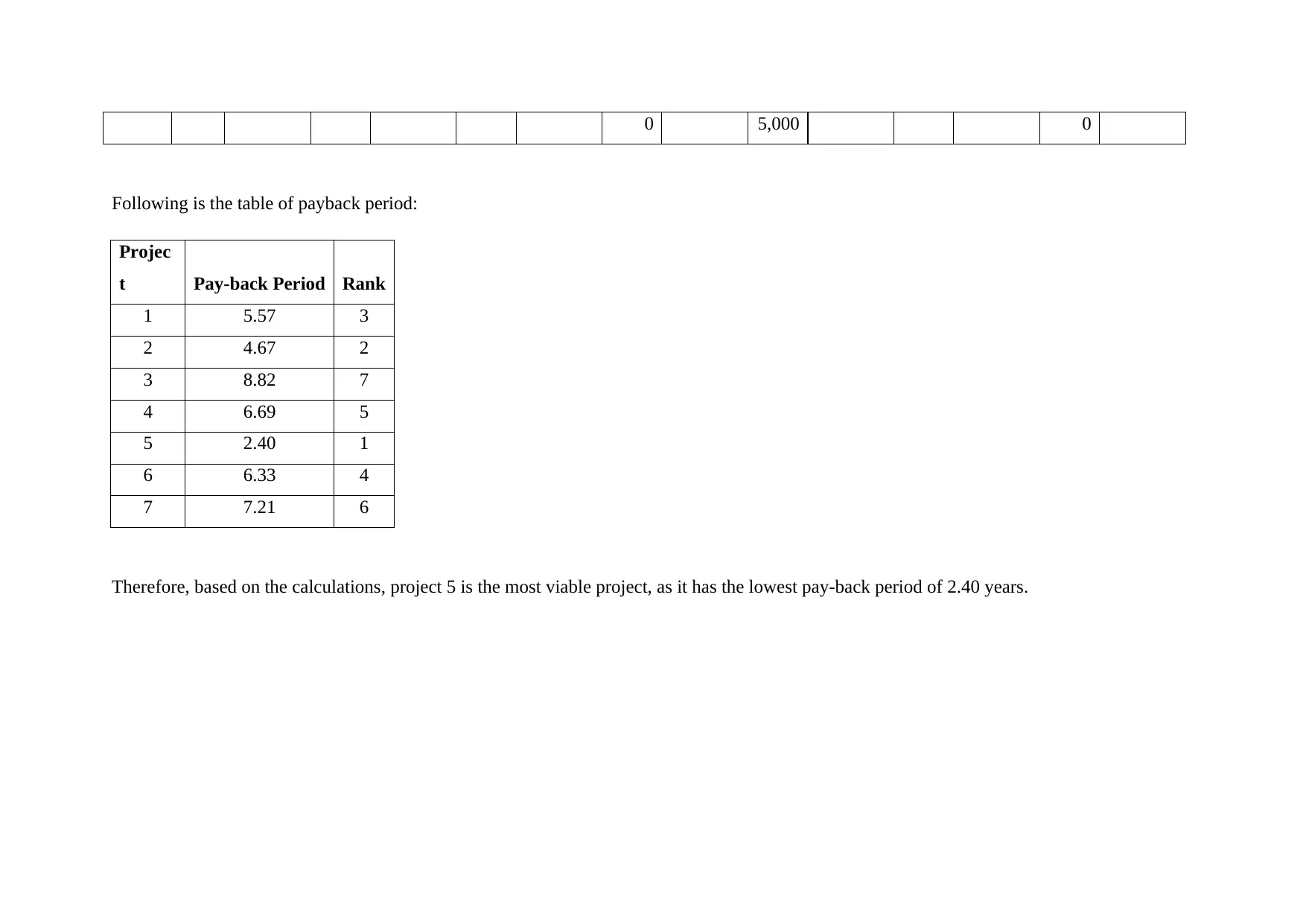

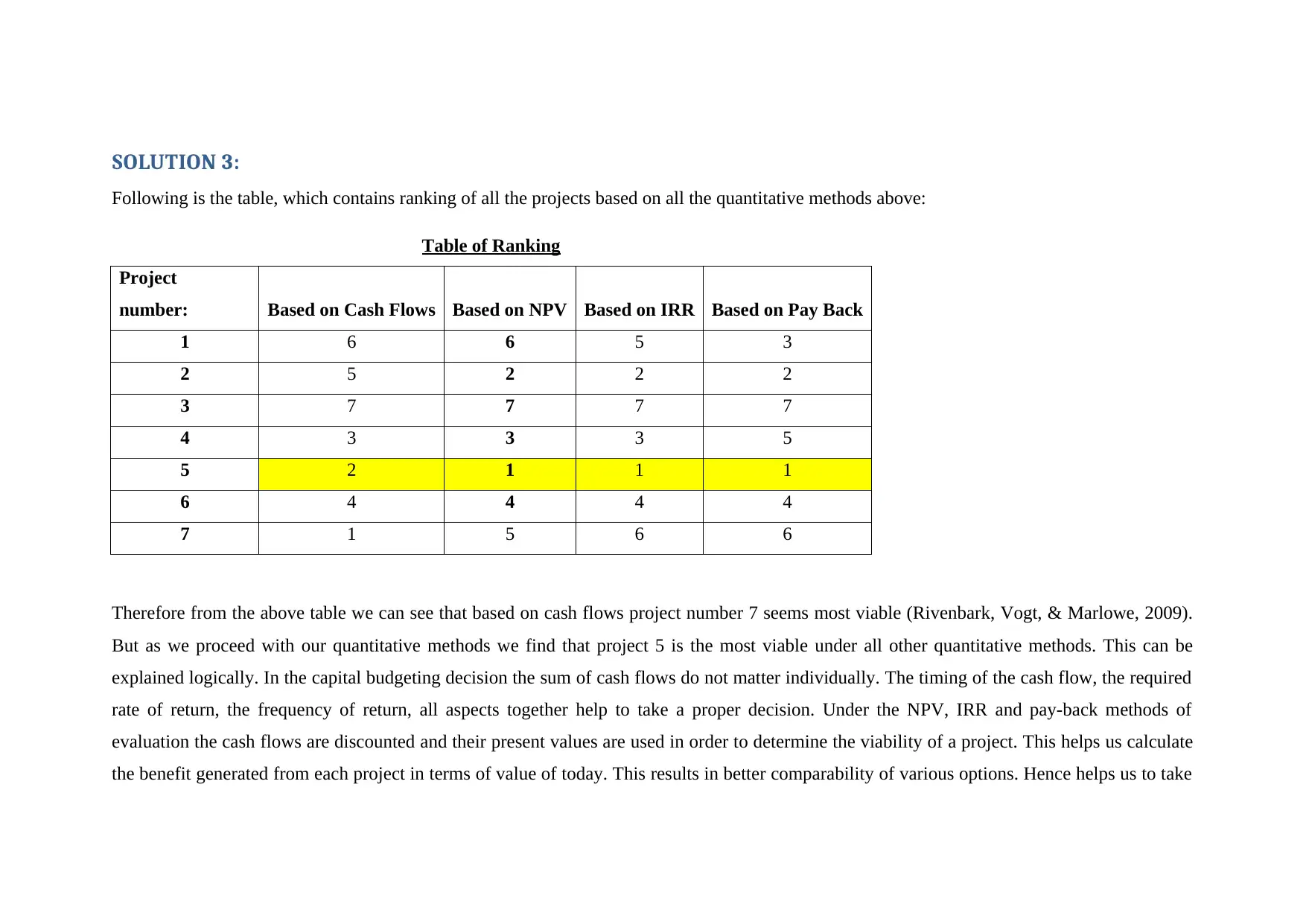

In this analysis, we examine seven capital investment options using various quantitative methods: cash flows, net present value (NPV), internal rate of return (IRR), and payback periods, in order to determine the best investments for a resource-constrained company. Initially, each project's total cash flow is assessed over its life span, with Project 5 showing the highest cumulative cash inflow at $6,500,000. Following this, we compute the NPV for each project using a required rate of return of 12% and determine their respective IRRs by equating them to zero in the NPV equation. The projects are then ranked based on these criteria, revealing Project 5 as the top choice with an NPV of $1,357,500 and an IRR of 14.9%. Subsequently, we calculate the payback period for each project to identify how quickly investments can be recouped, finding Project 5 again has the shortest duration at approximately 2.40 years. A comprehensive ranking table consolidates these findings across all methods, indicating that while Project 7 initially appears most viable based on cash flows alone, Projects 5 and 6 perform best under NPV, IRR, and payback criteria. Since Projects 4 and 5 are mutually exclusive, we select Project 5 due to its superior performance over Project 4. Ultimately, the analysis recommends accepting Projects 5, 6, and 2 as the top investment choices for the company.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.