Financial Performance Analysis: Tesco vs. Morrison

VerifiedAdded on 2020/02/05

|15

|4108

|36

AI Summary

This assignment requires a comparative analysis of the financial performance of two major UK supermarket chains, Tesco and Morrison. Students must calculate and interpret various financial ratios, such as gross profit margin, net profit margin, current ratio, quick ratio, debt-equity ratio, earnings per share, and price-earnings ratio. The aim is to assess and compare the profitability, liquidity, solvency, and efficiency of both companies using these key performance indicators.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

FINANCIAL MANAGEMENT

AND ANALYSIS

AND ANALYSIS

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

Choice of company and justification for its inclusion................................................................3

Ratio analysis of Tesco and Morison..........................................................................................3

Weakness of ratio analysis........................................................................................................12

Recommendation...........................................................................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES .............................................................................................................................15

INDEX OF TABLES

Table 1: Ratio analysis of Tesco and Morison ................................................................................3

ILLUSTRATION INDEX

Illustration 1: Gross profit ratio of the Tesco and Morison.............................................................5

Illustration 2: Net profit ratio of the Tesco and Morison.................................................................6

Illustration 3: Current ratio of the Tesco and Morison...................................................................7

Illustration 4: Quick ratio of the Tesco and Morison......................................................................8

Illustration 5: Working capital turnover ratio..................................................................................9

Illustration 6: Debt equity ratio of Tesco and Morison..................................................................10

Illustration 7: Earning per share of Tesco and Morison................................................................11

Illustration 8: Price earning ratio of Tesco and Morison...............................................................12

INTRODUCTION...........................................................................................................................3

Choice of company and justification for its inclusion................................................................3

Ratio analysis of Tesco and Morison..........................................................................................3

Weakness of ratio analysis........................................................................................................12

Recommendation...........................................................................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES .............................................................................................................................15

INDEX OF TABLES

Table 1: Ratio analysis of Tesco and Morison ................................................................................3

ILLUSTRATION INDEX

Illustration 1: Gross profit ratio of the Tesco and Morison.............................................................5

Illustration 2: Net profit ratio of the Tesco and Morison.................................................................6

Illustration 3: Current ratio of the Tesco and Morison...................................................................7

Illustration 4: Quick ratio of the Tesco and Morison......................................................................8

Illustration 5: Working capital turnover ratio..................................................................................9

Illustration 6: Debt equity ratio of Tesco and Morison..................................................................10

Illustration 7: Earning per share of Tesco and Morison................................................................11

Illustration 8: Price earning ratio of Tesco and Morison...............................................................12

INTRODUCTION

Ratio analysis is one of the most important techniques which is used to measure the firm

performance. By using this method, company’s performance is evaluated on the basis of various

parameters. The technique is commonly used to compare two or more companies on the basis of

various criteria that are operating in the same industry. Financial analysts and equity research

analysts commonly use this method to do fundamental analysis. Hence, it can be assumed that

this method has great importance for the firms. In this report, two retail firms will be taken into

consideration and ratio analysis will be done by taking facts as well as figures of these firms. By

comparing firms on the basis of some of financial ratios, it will be identified that in which firm,

investors must make an investment. In the report, various categories of ratios will be computed

like profitability, liquidity, working capital management, capital structure and stock market

performance. On the basis of ratio analysis, weak points of the firm will be identified and on that

basis, recommendations will be made that can be used by the business firms to convert their

weakness into strength. It can be said that in this report, companies will be systematically

compared with each other.

Choice of company and justification for its inclusion

In the present study, two retail companies which are Tesco and Morison are chosen for

making comparison and finding out the best company for the investment purpose. Tesco is one

of the largest players in the retail industry of the UK. Currently, it has the largest market share in

the UK retail industry but even though, its profitability is shrinking on the yearly basis (Tesco plc

ADR, 2016). Hence, by doing ratio analysis of Tesco, reasons will be identified due to which

firm performance is poor. In the report, other firm that is chosen for comparing with Tesco is

Morison. WM Morison is also one of the largest retail firms in the UK and one of the main

competitors of Tesco (Morrison supermarket plc ADR. 2016). Both companies come in the

ranking of top five and due to this reason, in order to identify the best investment opportunity in

the UK retail industry, Morison is chosen for making comparison with Tesco.

Ratio analysis of Tesco and Morison

Table 1: Ratio analysis of Tesco and Morison

TESCO Morison

Ratio analysis is one of the most important techniques which is used to measure the firm

performance. By using this method, company’s performance is evaluated on the basis of various

parameters. The technique is commonly used to compare two or more companies on the basis of

various criteria that are operating in the same industry. Financial analysts and equity research

analysts commonly use this method to do fundamental analysis. Hence, it can be assumed that

this method has great importance for the firms. In this report, two retail firms will be taken into

consideration and ratio analysis will be done by taking facts as well as figures of these firms. By

comparing firms on the basis of some of financial ratios, it will be identified that in which firm,

investors must make an investment. In the report, various categories of ratios will be computed

like profitability, liquidity, working capital management, capital structure and stock market

performance. On the basis of ratio analysis, weak points of the firm will be identified and on that

basis, recommendations will be made that can be used by the business firms to convert their

weakness into strength. It can be said that in this report, companies will be systematically

compared with each other.

Choice of company and justification for its inclusion

In the present study, two retail companies which are Tesco and Morison are chosen for

making comparison and finding out the best company for the investment purpose. Tesco is one

of the largest players in the retail industry of the UK. Currently, it has the largest market share in

the UK retail industry but even though, its profitability is shrinking on the yearly basis (Tesco plc

ADR, 2016). Hence, by doing ratio analysis of Tesco, reasons will be identified due to which

firm performance is poor. In the report, other firm that is chosen for comparing with Tesco is

Morison. WM Morison is also one of the largest retail firms in the UK and one of the main

competitors of Tesco (Morrison supermarket plc ADR. 2016). Both companies come in the

ranking of top five and due to this reason, in order to identify the best investment opportunity in

the UK retail industry, Morison is chosen for making comparison with Tesco.

Ratio analysis of Tesco and Morison

Table 1: Ratio analysis of Tesco and Morison

TESCO Morison

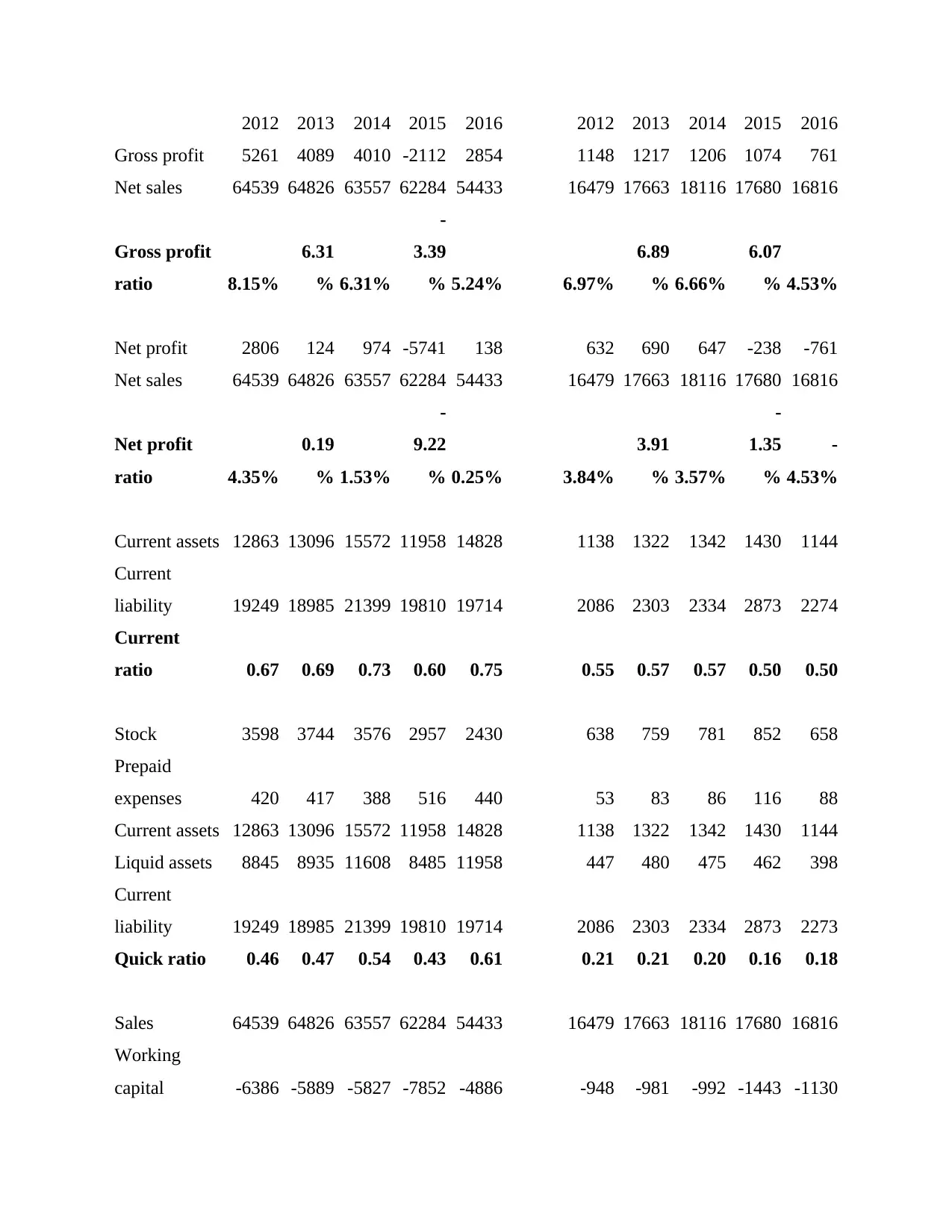

2012 2013 2014 2015 2016 2012 2013 2014 2015 2016

Gross profit 5261 4089 4010 -2112 2854 1148 1217 1206 1074 761

Net sales 64539 64826 63557 62284 54433 16479 17663 18116 17680 16816

Gross profit

ratio 8.15%

6.31

% 6.31%

-

3.39

% 5.24% 6.97%

6.89

% 6.66%

6.07

% 4.53%

Net profit 2806 124 974 -5741 138 632 690 647 -238 -761

Net sales 64539 64826 63557 62284 54433 16479 17663 18116 17680 16816

Net profit

ratio 4.35%

0.19

% 1.53%

-

9.22

% 0.25% 3.84%

3.91

% 3.57%

-

1.35

%

-

4.53%

Current assets 12863 13096 15572 11958 14828 1138 1322 1342 1430 1144

Current

liability 19249 18985 21399 19810 19714 2086 2303 2334 2873 2274

Current

ratio 0.67 0.69 0.73 0.60 0.75 0.55 0.57 0.57 0.50 0.50

Stock 3598 3744 3576 2957 2430 638 759 781 852 658

Prepaid

expenses 420 417 388 516 440 53 83 86 116 88

Current assets 12863 13096 15572 11958 14828 1138 1322 1342 1430 1144

Liquid assets 8845 8935 11608 8485 11958 447 480 475 462 398

Current

liability 19249 18985 21399 19810 19714 2086 2303 2334 2873 2273

Quick ratio 0.46 0.47 0.54 0.43 0.61 0.21 0.21 0.20 0.16 0.18

Sales 64539 64826 63557 62284 54433 16479 17663 18116 17680 16816

Working

capital -6386 -5889 -5827 -7852 -4886 -948 -981 -992 -1443 -1130

Gross profit 5261 4089 4010 -2112 2854 1148 1217 1206 1074 761

Net sales 64539 64826 63557 62284 54433 16479 17663 18116 17680 16816

Gross profit

ratio 8.15%

6.31

% 6.31%

-

3.39

% 5.24% 6.97%

6.89

% 6.66%

6.07

% 4.53%

Net profit 2806 124 974 -5741 138 632 690 647 -238 -761

Net sales 64539 64826 63557 62284 54433 16479 17663 18116 17680 16816

Net profit

ratio 4.35%

0.19

% 1.53%

-

9.22

% 0.25% 3.84%

3.91

% 3.57%

-

1.35

%

-

4.53%

Current assets 12863 13096 15572 11958 14828 1138 1322 1342 1430 1144

Current

liability 19249 18985 21399 19810 19714 2086 2303 2334 2873 2274

Current

ratio 0.67 0.69 0.73 0.60 0.75 0.55 0.57 0.57 0.50 0.50

Stock 3598 3744 3576 2957 2430 638 759 781 852 658

Prepaid

expenses 420 417 388 516 440 53 83 86 116 88

Current assets 12863 13096 15572 11958 14828 1138 1322 1342 1430 1144

Liquid assets 8845 8935 11608 8485 11958 447 480 475 462 398

Current

liability 19249 18985 21399 19810 19714 2086 2303 2334 2873 2273

Quick ratio 0.46 0.47 0.54 0.43 0.61 0.21 0.21 0.20 0.16 0.18

Sales 64539 64826 63557 62284 54433 16479 17663 18116 17680 16816

Working

capital -6386 -5889 -5827 -7852 -4886 -948 -981 -992 -1443 -1130

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

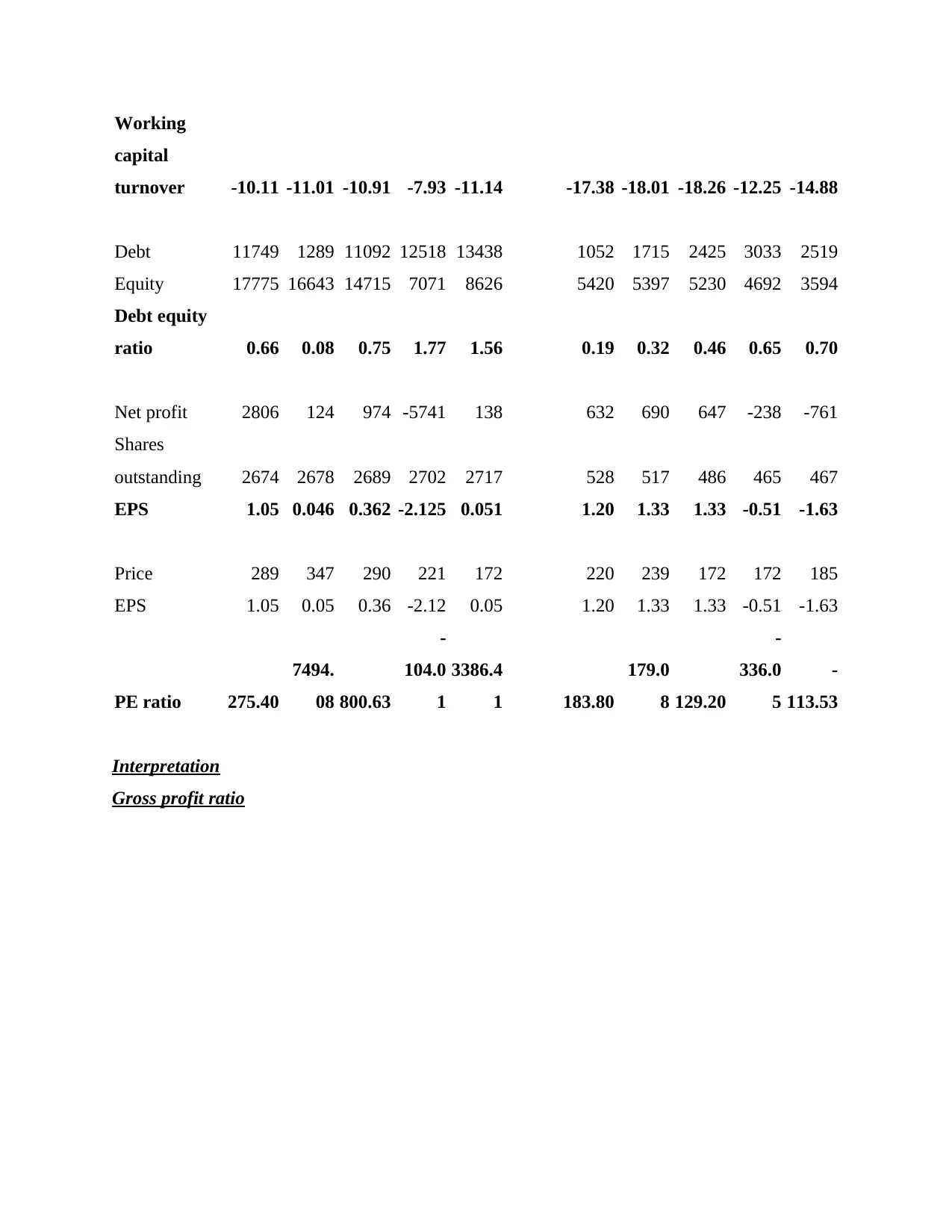

Working

capital

turnover -10.11 -11.01 -10.91 -7.93 -11.14 -17.38 -18.01 -18.26 -12.25 -14.88

Debt 11749 1289 11092 12518 13438 1052 1715 2425 3033 2519

Equity 17775 16643 14715 7071 8626 5420 5397 5230 4692 3594

Debt equity

ratio 0.66 0.08 0.75 1.77 1.56 0.19 0.32 0.46 0.65 0.70

Net profit 2806 124 974 -5741 138 632 690 647 -238 -761

Shares

outstanding 2674 2678 2689 2702 2717 528 517 486 465 467

EPS 1.05 0.046 0.362 -2.125 0.051 1.20 1.33 1.33 -0.51 -1.63

Price 289 347 290 221 172 220 239 172 172 185

EPS 1.05 0.05 0.36 -2.12 0.05 1.20 1.33 1.33 -0.51 -1.63

PE ratio 275.40

7494.

08 800.63

-

104.0

1

3386.4

1 183.80

179.0

8 129.20

-

336.0

5

-

113.53

Interpretation

Gross profit ratio

capital

turnover -10.11 -11.01 -10.91 -7.93 -11.14 -17.38 -18.01 -18.26 -12.25 -14.88

Debt 11749 1289 11092 12518 13438 1052 1715 2425 3033 2519

Equity 17775 16643 14715 7071 8626 5420 5397 5230 4692 3594

Debt equity

ratio 0.66 0.08 0.75 1.77 1.56 0.19 0.32 0.46 0.65 0.70

Net profit 2806 124 974 -5741 138 632 690 647 -238 -761

Shares

outstanding 2674 2678 2689 2702 2717 528 517 486 465 467

EPS 1.05 0.046 0.362 -2.125 0.051 1.20 1.33 1.33 -0.51 -1.63

Price 289 347 290 221 172 220 239 172 172 185

EPS 1.05 0.05 0.36 -2.12 0.05 1.20 1.33 1.33 -0.51 -1.63

PE ratio 275.40

7494.

08 800.63

-

104.0

1

3386.4

1 183.80

179.0

8 129.20

-

336.0

5

-

113.53

Interpretation

Gross profit ratio

Interpretation

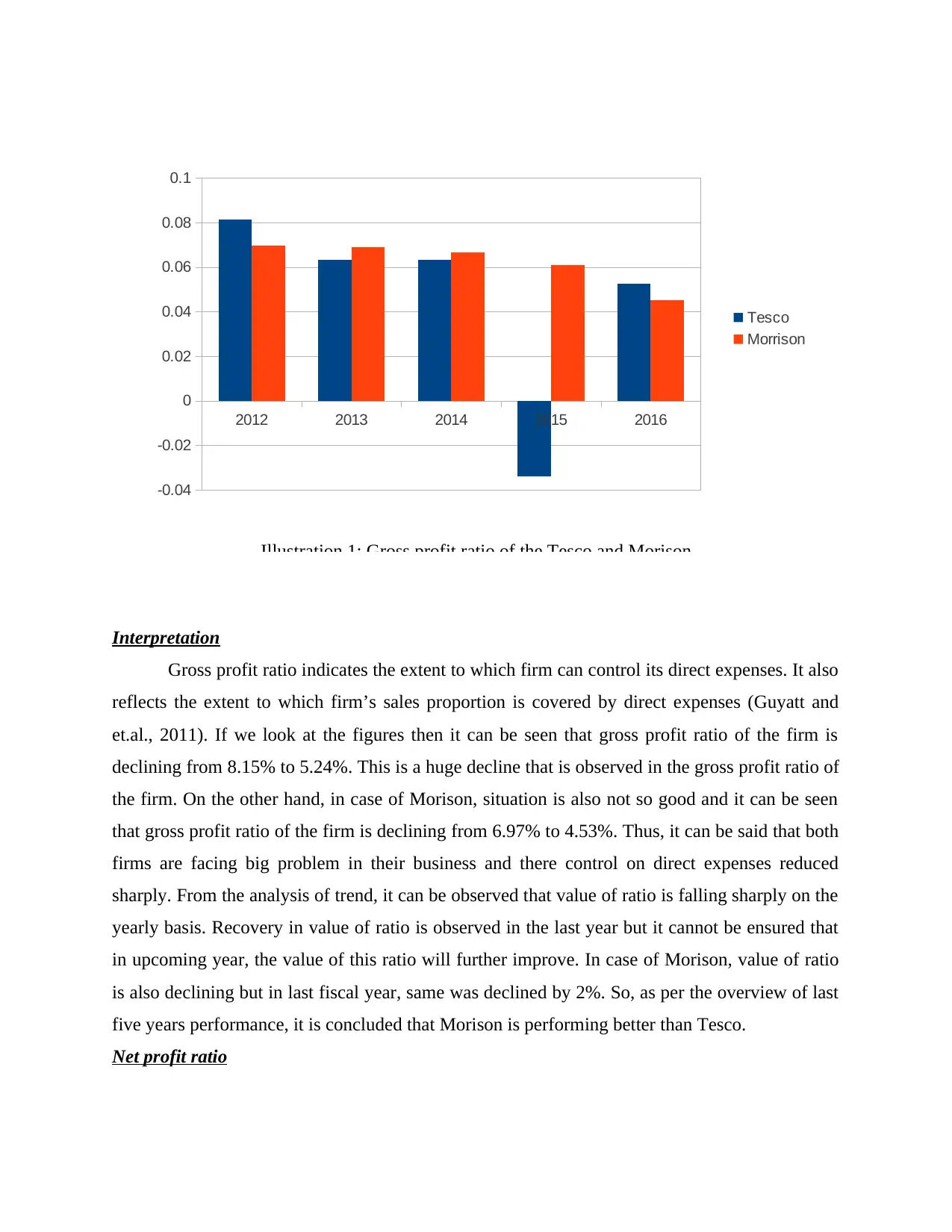

Gross profit ratio indicates the extent to which firm can control its direct expenses. It also

reflects the extent to which firm’s sales proportion is covered by direct expenses (Guyatt and

et.al., 2011). If we look at the figures then it can be seen that gross profit ratio of the firm is

declining from 8.15% to 5.24%. This is a huge decline that is observed in the gross profit ratio of

the firm. On the other hand, in case of Morison, situation is also not so good and it can be seen

that gross profit ratio of the firm is declining from 6.97% to 4.53%. Thus, it can be said that both

firms are facing big problem in their business and there control on direct expenses reduced

sharply. From the analysis of trend, it can be observed that value of ratio is falling sharply on the

yearly basis. Recovery in value of ratio is observed in the last year but it cannot be ensured that

in upcoming year, the value of this ratio will further improve. In case of Morison, value of ratio

is also declining but in last fiscal year, same was declined by 2%. So, as per the overview of last

five years performance, it is concluded that Morison is performing better than Tesco.

Net profit ratio

2012 2013 2014 2015 2016

-0.04

-0.02

0

0.02

0.04

0.06

0.08

0.1

Tesco

Morrison

Illustration 1: Gross profit ratio of the Tesco and Morison

Gross profit ratio indicates the extent to which firm can control its direct expenses. It also

reflects the extent to which firm’s sales proportion is covered by direct expenses (Guyatt and

et.al., 2011). If we look at the figures then it can be seen that gross profit ratio of the firm is

declining from 8.15% to 5.24%. This is a huge decline that is observed in the gross profit ratio of

the firm. On the other hand, in case of Morison, situation is also not so good and it can be seen

that gross profit ratio of the firm is declining from 6.97% to 4.53%. Thus, it can be said that both

firms are facing big problem in their business and there control on direct expenses reduced

sharply. From the analysis of trend, it can be observed that value of ratio is falling sharply on the

yearly basis. Recovery in value of ratio is observed in the last year but it cannot be ensured that

in upcoming year, the value of this ratio will further improve. In case of Morison, value of ratio

is also declining but in last fiscal year, same was declined by 2%. So, as per the overview of last

five years performance, it is concluded that Morison is performing better than Tesco.

Net profit ratio

2012 2013 2014 2015 2016

-0.04

-0.02

0

0.02

0.04

0.06

0.08

0.1

Tesco

Morrison

Illustration 1: Gross profit ratio of the Tesco and Morison

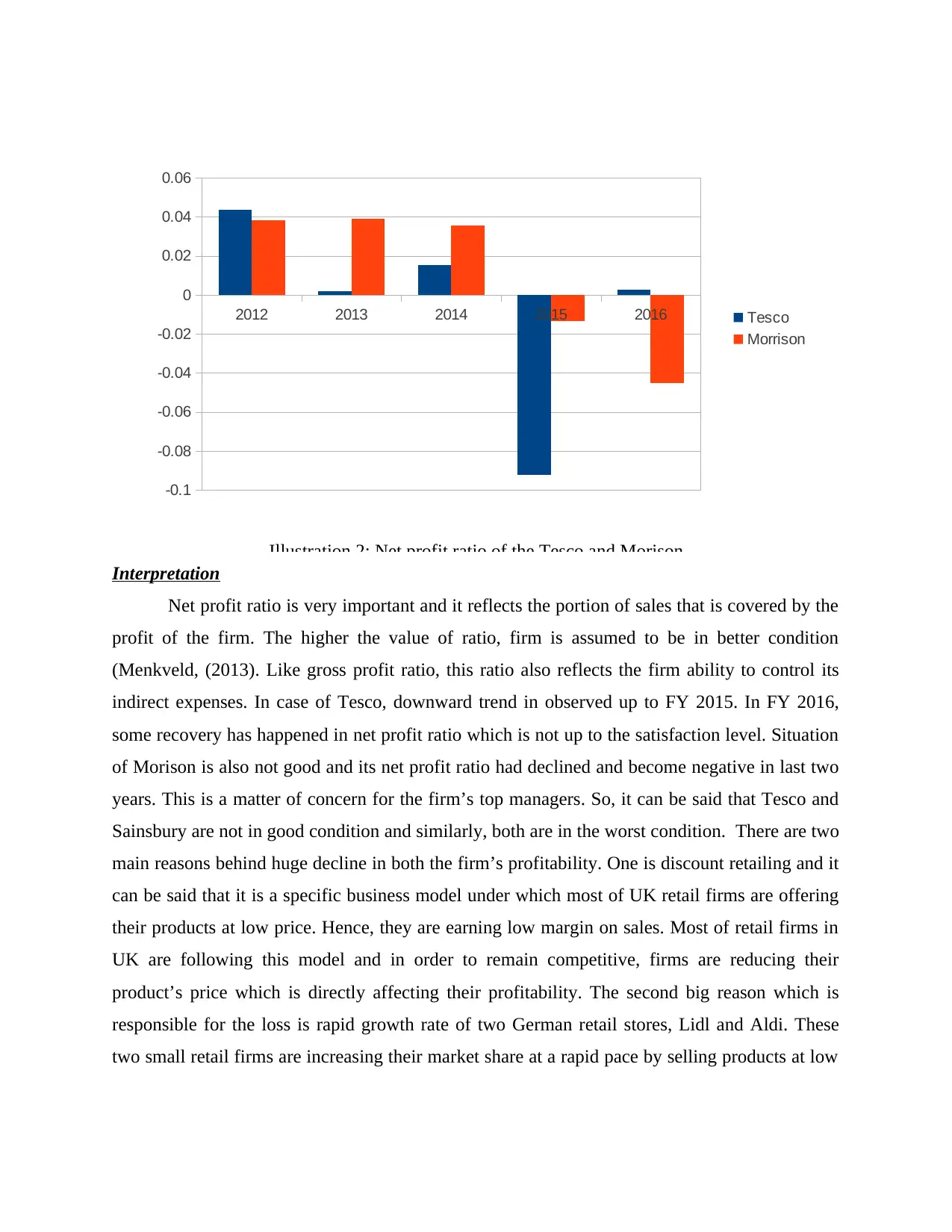

Interpretation

Net profit ratio is very important and it reflects the portion of sales that is covered by the

profit of the firm. The higher the value of ratio, firm is assumed to be in better condition

(Menkveld, (2013). Like gross profit ratio, this ratio also reflects the firm ability to control its

indirect expenses. In case of Tesco, downward trend in observed up to FY 2015. In FY 2016,

some recovery has happened in net profit ratio which is not up to the satisfaction level. Situation

of Morison is also not good and its net profit ratio had declined and become negative in last two

years. This is a matter of concern for the firm’s top managers. So, it can be said that Tesco and

Sainsbury are not in good condition and similarly, both are in the worst condition. There are two

main reasons behind huge decline in both the firm’s profitability. One is discount retailing and it

can be said that it is a specific business model under which most of UK retail firms are offering

their products at low price. Hence, they are earning low margin on sales. Most of retail firms in

UK are following this model and in order to remain competitive, firms are reducing their

product’s price which is directly affecting their profitability. The second big reason which is

responsible for the loss is rapid growth rate of two German retail stores, Lidl and Aldi. These

two small retail firms are increasing their market share at a rapid pace by selling products at low

2012 2013 2014 2015 2016

-0.1

-0.08

-0.06

-0.04

-0.02

0

0.02

0.04

0.06

Tesco

Morrison

Illustration 2: Net profit ratio of the Tesco and Morison

Net profit ratio is very important and it reflects the portion of sales that is covered by the

profit of the firm. The higher the value of ratio, firm is assumed to be in better condition

(Menkveld, (2013). Like gross profit ratio, this ratio also reflects the firm ability to control its

indirect expenses. In case of Tesco, downward trend in observed up to FY 2015. In FY 2016,

some recovery has happened in net profit ratio which is not up to the satisfaction level. Situation

of Morison is also not good and its net profit ratio had declined and become negative in last two

years. This is a matter of concern for the firm’s top managers. So, it can be said that Tesco and

Sainsbury are not in good condition and similarly, both are in the worst condition. There are two

main reasons behind huge decline in both the firm’s profitability. One is discount retailing and it

can be said that it is a specific business model under which most of UK retail firms are offering

their products at low price. Hence, they are earning low margin on sales. Most of retail firms in

UK are following this model and in order to remain competitive, firms are reducing their

product’s price which is directly affecting their profitability. The second big reason which is

responsible for the loss is rapid growth rate of two German retail stores, Lidl and Aldi. These

two small retail firms are increasing their market share at a rapid pace by selling products at low

2012 2013 2014 2015 2016

-0.1

-0.08

-0.06

-0.04

-0.02

0

0.02

0.04

0.06

Tesco

Morrison

Illustration 2: Net profit ratio of the Tesco and Morison

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

price and generating economies of scale in their business. Hence, firms need to find out the

solution of these two problems as fast as possible.

Current ratio

Interpretation

Current ratio reflects liquidity position of the firm. It also defines firm capacity to pay

current liabilities by using current assets. Standard current ratio for the firm is 2:1 which means

that for every one pound of current liabilities, there must have two pound of current assets (Gill,,

Biger. and Mathur, N. (2010). From the figures, it is clear that liquidity position of both the firms

is not good and both of them are not able to pay their current liabilities completely by making

use of current assets. However, Tesco is in the better condition than Morison because its ratio

values are increasing consistently. On the other hand, in case of Morison, scene is different and

value of current ratio is declining. On the basis of this analysis, Tesco is assumed to be in much

better condition than Morrison. The main reason due to which value of this ratio is low in case

of both firms is that they are earning no or less profit in there business. Due to this reason they

have less current assets in there business. In order to meet the working capital needs, these firms

are taking short term loans from bank on the regular basis. Hence, value of ratio is decreasing

very sharply in case of both the firms.

2012 2013 2014 2015 2016

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

Tesco

Morrison

Illustration 3: Current ratio of the Tesco and Morison

solution of these two problems as fast as possible.

Current ratio

Interpretation

Current ratio reflects liquidity position of the firm. It also defines firm capacity to pay

current liabilities by using current assets. Standard current ratio for the firm is 2:1 which means

that for every one pound of current liabilities, there must have two pound of current assets (Gill,,

Biger. and Mathur, N. (2010). From the figures, it is clear that liquidity position of both the firms

is not good and both of them are not able to pay their current liabilities completely by making

use of current assets. However, Tesco is in the better condition than Morison because its ratio

values are increasing consistently. On the other hand, in case of Morison, scene is different and

value of current ratio is declining. On the basis of this analysis, Tesco is assumed to be in much

better condition than Morrison. The main reason due to which value of this ratio is low in case

of both firms is that they are earning no or less profit in there business. Due to this reason they

have less current assets in there business. In order to meet the working capital needs, these firms

are taking short term loans from bank on the regular basis. Hence, value of ratio is decreasing

very sharply in case of both the firms.

2012 2013 2014 2015 2016

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

Tesco

Morrison

Illustration 3: Current ratio of the Tesco and Morison

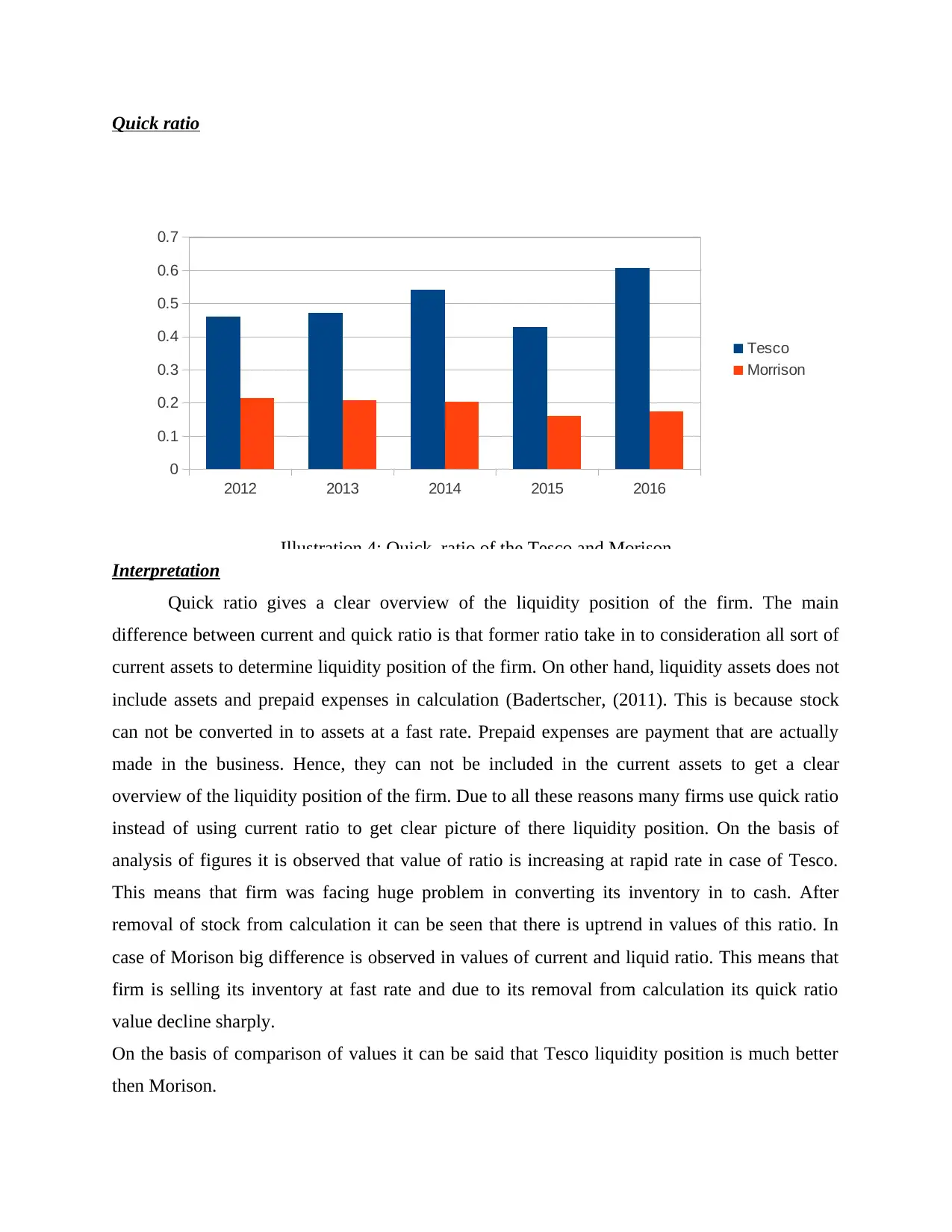

Quick ratio

Interpretation

Quick ratio gives a clear overview of the liquidity position of the firm. The main

difference between current and quick ratio is that former ratio take in to consideration all sort of

current assets to determine liquidity position of the firm. On other hand, liquidity assets does not

include assets and prepaid expenses in calculation (Badertscher, (2011). This is because stock

can not be converted in to assets at a fast rate. Prepaid expenses are payment that are actually

made in the business. Hence, they can not be included in the current assets to get a clear

overview of the liquidity position of the firm. Due to all these reasons many firms use quick ratio

instead of using current ratio to get clear picture of there liquidity position. On the basis of

analysis of figures it is observed that value of ratio is increasing at rapid rate in case of Tesco.

This means that firm was facing huge problem in converting its inventory in to cash. After

removal of stock from calculation it can be seen that there is uptrend in values of this ratio. In

case of Morison big difference is observed in values of current and liquid ratio. This means that

firm is selling its inventory at fast rate and due to its removal from calculation its quick ratio

value decline sharply.

On the basis of comparison of values it can be said that Tesco liquidity position is much better

then Morison.

2012 2013 2014 2015 2016

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

Tesco

Morrison

Illustration 4: Quick ratio of the Tesco and Morison

Interpretation

Quick ratio gives a clear overview of the liquidity position of the firm. The main

difference between current and quick ratio is that former ratio take in to consideration all sort of

current assets to determine liquidity position of the firm. On other hand, liquidity assets does not

include assets and prepaid expenses in calculation (Badertscher, (2011). This is because stock

can not be converted in to assets at a fast rate. Prepaid expenses are payment that are actually

made in the business. Hence, they can not be included in the current assets to get a clear

overview of the liquidity position of the firm. Due to all these reasons many firms use quick ratio

instead of using current ratio to get clear picture of there liquidity position. On the basis of

analysis of figures it is observed that value of ratio is increasing at rapid rate in case of Tesco.

This means that firm was facing huge problem in converting its inventory in to cash. After

removal of stock from calculation it can be seen that there is uptrend in values of this ratio. In

case of Morison big difference is observed in values of current and liquid ratio. This means that

firm is selling its inventory at fast rate and due to its removal from calculation its quick ratio

value decline sharply.

On the basis of comparison of values it can be said that Tesco liquidity position is much better

then Morison.

2012 2013 2014 2015 2016

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

Tesco

Morrison

Illustration 4: Quick ratio of the Tesco and Morison

Working capital turnover ratio

Interpretation

Working capital turnover ratio indicate the extent to which firm generate sales using

working capital. Higher working capital ratio is assumed better for the firm because higher value

of the ratio means that firm is generating heavy amount of sales by using working capital

(Cooper and et.al., (2011)). If working capital ratio of the firm is negative then it means that firm

is not able to fund its operations because its entire current assets are used in paying current

liabilities of the business. In case of both firms it can be seen that working capital turnover ratio

is negative and it means that working capital is used by the firms in order to pay its current

liability. Nothing remaining from amount of current assets that can be used to finance business

operations.

Debt equity ratio

2012 2013 2014 2015 2016

-20

-18

-16

-14

-12

-10

-8

-6

-4

-2

0

Tesco

Morrison

Illustration 5: Working capital turnover ratio

Interpretation

Working capital turnover ratio indicate the extent to which firm generate sales using

working capital. Higher working capital ratio is assumed better for the firm because higher value

of the ratio means that firm is generating heavy amount of sales by using working capital

(Cooper and et.al., (2011)). If working capital ratio of the firm is negative then it means that firm

is not able to fund its operations because its entire current assets are used in paying current

liabilities of the business. In case of both firms it can be seen that working capital turnover ratio

is negative and it means that working capital is used by the firms in order to pay its current

liability. Nothing remaining from amount of current assets that can be used to finance business

operations.

Debt equity ratio

2012 2013 2014 2015 2016

-20

-18

-16

-14

-12

-10

-8

-6

-4

-2

0

Tesco

Morrison

Illustration 5: Working capital turnover ratio

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

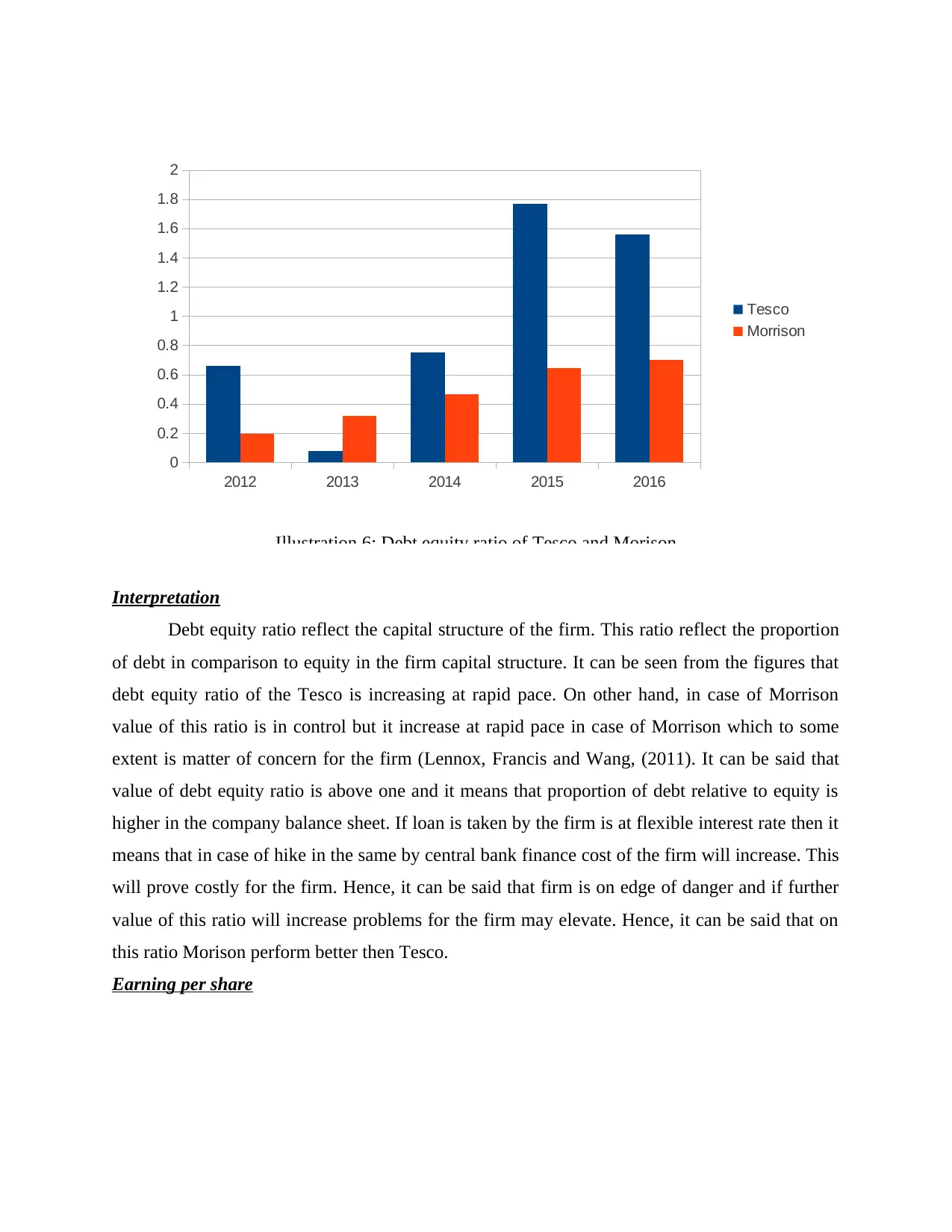

Interpretation

Debt equity ratio reflect the capital structure of the firm. This ratio reflect the proportion

of debt in comparison to equity in the firm capital structure. It can be seen from the figures that

debt equity ratio of the Tesco is increasing at rapid pace. On other hand, in case of Morrison

value of this ratio is in control but it increase at rapid pace in case of Morrison which to some

extent is matter of concern for the firm (Lennox, Francis and Wang, (2011). It can be said that

value of debt equity ratio is above one and it means that proportion of debt relative to equity is

higher in the company balance sheet. If loan is taken by the firm is at flexible interest rate then it

means that in case of hike in the same by central bank finance cost of the firm will increase. This

will prove costly for the firm. Hence, it can be said that firm is on edge of danger and if further

value of this ratio will increase problems for the firm may elevate. Hence, it can be said that on

this ratio Morison perform better then Tesco.

Earning per share

2012 2013 2014 2015 2016

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2

Tesco

Morrison

Illustration 6: Debt equity ratio of Tesco and Morison

Debt equity ratio reflect the capital structure of the firm. This ratio reflect the proportion

of debt in comparison to equity in the firm capital structure. It can be seen from the figures that

debt equity ratio of the Tesco is increasing at rapid pace. On other hand, in case of Morrison

value of this ratio is in control but it increase at rapid pace in case of Morrison which to some

extent is matter of concern for the firm (Lennox, Francis and Wang, (2011). It can be said that

value of debt equity ratio is above one and it means that proportion of debt relative to equity is

higher in the company balance sheet. If loan is taken by the firm is at flexible interest rate then it

means that in case of hike in the same by central bank finance cost of the firm will increase. This

will prove costly for the firm. Hence, it can be said that firm is on edge of danger and if further

value of this ratio will increase problems for the firm may elevate. Hence, it can be said that on

this ratio Morison perform better then Tesco.

Earning per share

2012 2013 2014 2015 2016

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2

Tesco

Morrison

Illustration 6: Debt equity ratio of Tesco and Morison

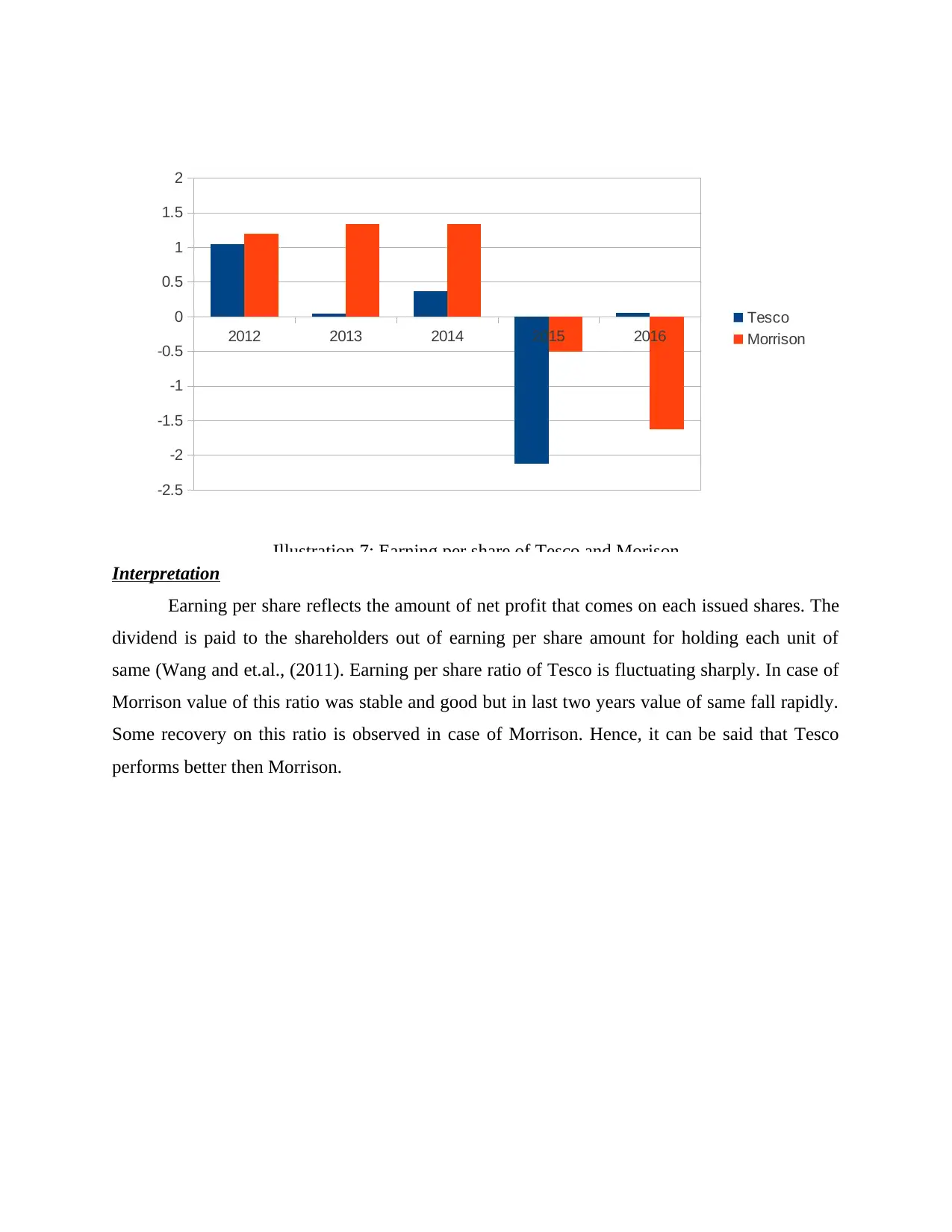

Interpretation

Earning per share reflects the amount of net profit that comes on each issued shares. The

dividend is paid to the shareholders out of earning per share amount for holding each unit of

same (Wang and et.al., (2011). Earning per share ratio of Tesco is fluctuating sharply. In case of

Morrison value of this ratio was stable and good but in last two years value of same fall rapidly.

Some recovery on this ratio is observed in case of Morrison. Hence, it can be said that Tesco

performs better then Morrison.

2012 2013 2014 2015 2016

-2.5

-2

-1.5

-1

-0.5

0

0.5

1

1.5

2

Tesco

Morrison

Illustration 7: Earning per share of Tesco and Morison

Earning per share reflects the amount of net profit that comes on each issued shares. The

dividend is paid to the shareholders out of earning per share amount for holding each unit of

same (Wang and et.al., (2011). Earning per share ratio of Tesco is fluctuating sharply. In case of

Morrison value of this ratio was stable and good but in last two years value of same fall rapidly.

Some recovery on this ratio is observed in case of Morrison. Hence, it can be said that Tesco

performs better then Morrison.

2012 2013 2014 2015 2016

-2.5

-2

-1.5

-1

-0.5

0

0.5

1

1.5

2

Tesco

Morrison

Illustration 7: Earning per share of Tesco and Morison

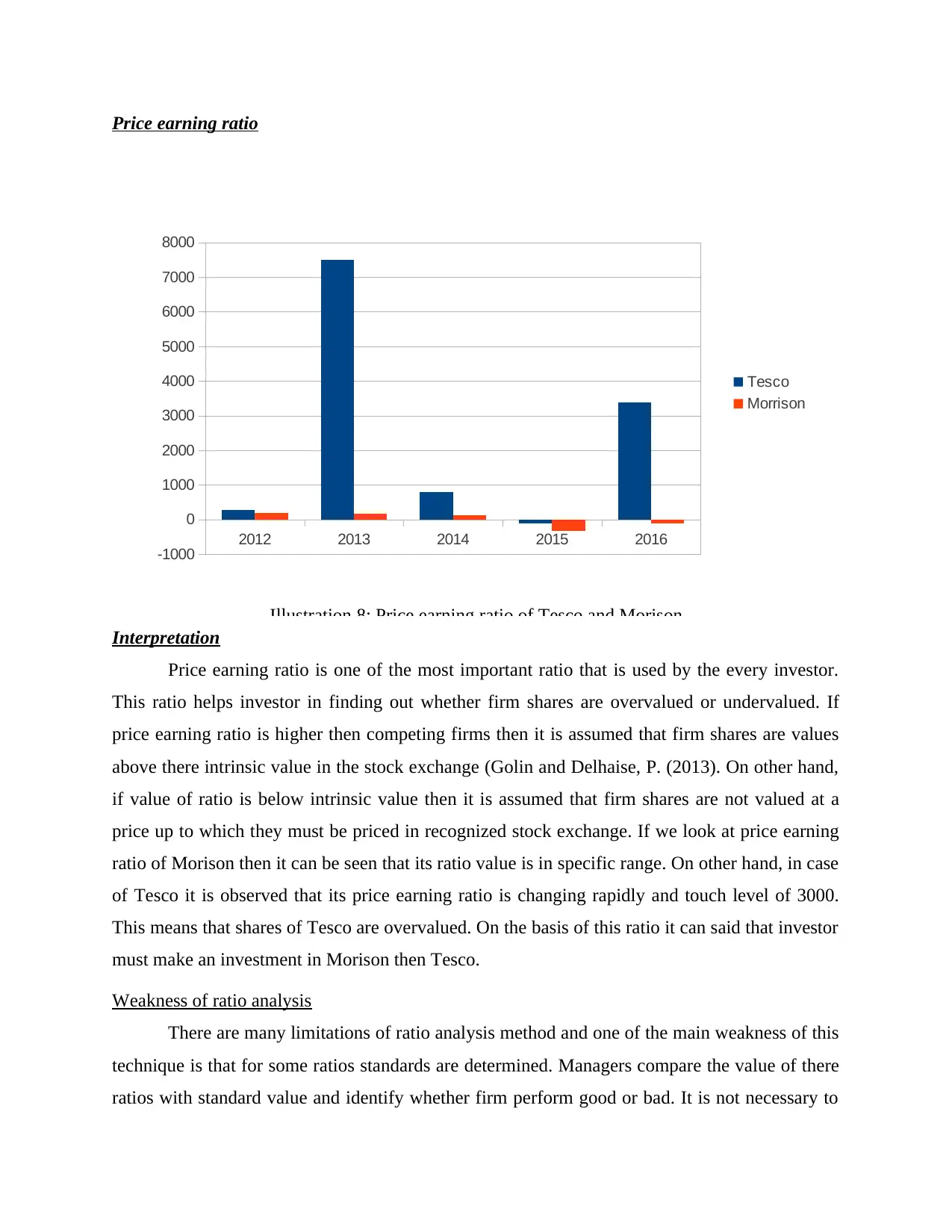

Price earning ratio

Interpretation

Price earning ratio is one of the most important ratio that is used by the every investor.

This ratio helps investor in finding out whether firm shares are overvalued or undervalued. If

price earning ratio is higher then competing firms then it is assumed that firm shares are values

above there intrinsic value in the stock exchange (Golin and Delhaise, P. (2013). On other hand,

if value of ratio is below intrinsic value then it is assumed that firm shares are not valued at a

price up to which they must be priced in recognized stock exchange. If we look at price earning

ratio of Morison then it can be seen that its ratio value is in specific range. On other hand, in case

of Tesco it is observed that its price earning ratio is changing rapidly and touch level of 3000.

This means that shares of Tesco are overvalued. On the basis of this ratio it can said that investor

must make an investment in Morison then Tesco.

Weakness of ratio analysis

There are many limitations of ratio analysis method and one of the main weakness of this

technique is that for some ratios standards are determined. Managers compare the value of there

ratios with standard value and identify whether firm perform good or bad. It is not necessary to

2012 2013 2014 2015 2016

-1000

0

1000

2000

3000

4000

5000

6000

7000

8000

Tesco

Morrison

Illustration 8: Price earning ratio of Tesco and Morison

Interpretation

Price earning ratio is one of the most important ratio that is used by the every investor.

This ratio helps investor in finding out whether firm shares are overvalued or undervalued. If

price earning ratio is higher then competing firms then it is assumed that firm shares are values

above there intrinsic value in the stock exchange (Golin and Delhaise, P. (2013). On other hand,

if value of ratio is below intrinsic value then it is assumed that firm shares are not valued at a

price up to which they must be priced in recognized stock exchange. If we look at price earning

ratio of Morison then it can be seen that its ratio value is in specific range. On other hand, in case

of Tesco it is observed that its price earning ratio is changing rapidly and touch level of 3000.

This means that shares of Tesco are overvalued. On the basis of this ratio it can said that investor

must make an investment in Morison then Tesco.

Weakness of ratio analysis

There are many limitations of ratio analysis method and one of the main weakness of this

technique is that for some ratios standards are determined. Managers compare the value of there

ratios with standard value and identify whether firm perform good or bad. It is not necessary to

2012 2013 2014 2015 2016

-1000

0

1000

2000

3000

4000

5000

6000

7000

8000

Tesco

Morrison

Illustration 8: Price earning ratio of Tesco and Morison

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

use same standard again and again even situation gets changed. In case of current ratio standard

value is 2:1 means current assets must be double of current liability (Kalbfleisch and Prentice,

(2011). If we look a retail industry of UK due to sale of product at low price it is no longer

possible for firms to earn sufficient amount of profit in the business. On other hand, Lidl and

Aldi are increasing there market share rapidly. This also affects profitability of Tesco and

Morrison. Hence, it is not possible for them to achieve standard value of the ratio. In such a

situation if firm liquidity position will be accessed by comparing current value with standard

value then firm managers will not be able to measure actual performance of the firm. So, it is

major limitation of ratio analysis. Thus, managers must make sure that they according to change

in situation are setting reasonable standards for the research.

Recommendation

It is recommended that investor must makes an investment in Tesco instead of Morrison.

This is because in most of ratios in last two year selected firm perform better then Morrison. In

most of ratios performance of Morison fall suddenly in last two years which is matter of concern

for investment purpose. On other hand, in case of Tesco recovery in its performance is observed.

Shares of Tesco are overvalued which reflects that investors have confidence that price of same

will increase in future. Sign of recovery is observed in case of Tesco and investors have

confidence in the firm. Hence, it is recommended that investment must be made in Tesco instead

of Morison. It is recommended that Morison must try to improve its liquidity position. In this

regard it must adopt cash management technique (Protani, Coory. and Martin, (2010). In this

regard, it must try to decentralize its payment receipt system and must centralize payment

making system. By doing so firm can reduce its cash outflow to some extent and can boost cash

inflow in the business. Result will be that firm will have abundant amount of cash in its business.

By doing this value of current ratio can be increased (Ayyub, (2014). If current assets will be

more then current liability then firm working capital turnover ratio will increase. Morrison net

profit ratio decline by good percentage and it is recommended that it must try to find out ways

by using which economics of scale can be generated in the business. Debt equity ratio is higher

in case of Tesco which means that its debt is higher in amount relative to equity. Here firm needs

to improve its performance and in this regard it mus abstain further from taking higher amount of

loan. It must invite investment from institutional investors will be invested in the business in

value is 2:1 means current assets must be double of current liability (Kalbfleisch and Prentice,

(2011). If we look a retail industry of UK due to sale of product at low price it is no longer

possible for firms to earn sufficient amount of profit in the business. On other hand, Lidl and

Aldi are increasing there market share rapidly. This also affects profitability of Tesco and

Morrison. Hence, it is not possible for them to achieve standard value of the ratio. In such a

situation if firm liquidity position will be accessed by comparing current value with standard

value then firm managers will not be able to measure actual performance of the firm. So, it is

major limitation of ratio analysis. Thus, managers must make sure that they according to change

in situation are setting reasonable standards for the research.

Recommendation

It is recommended that investor must makes an investment in Tesco instead of Morrison.

This is because in most of ratios in last two year selected firm perform better then Morrison. In

most of ratios performance of Morison fall suddenly in last two years which is matter of concern

for investment purpose. On other hand, in case of Tesco recovery in its performance is observed.

Shares of Tesco are overvalued which reflects that investors have confidence that price of same

will increase in future. Sign of recovery is observed in case of Tesco and investors have

confidence in the firm. Hence, it is recommended that investment must be made in Tesco instead

of Morison. It is recommended that Morison must try to improve its liquidity position. In this

regard it must adopt cash management technique (Protani, Coory. and Martin, (2010). In this

regard, it must try to decentralize its payment receipt system and must centralize payment

making system. By doing so firm can reduce its cash outflow to some extent and can boost cash

inflow in the business. Result will be that firm will have abundant amount of cash in its business.

By doing this value of current ratio can be increased (Ayyub, (2014). If current assets will be

more then current liability then firm working capital turnover ratio will increase. Morrison net

profit ratio decline by good percentage and it is recommended that it must try to find out ways

by using which economics of scale can be generated in the business. Debt equity ratio is higher

in case of Tesco which means that its debt is higher in amount relative to equity. Here firm needs

to improve its performance and in this regard it mus abstain further from taking higher amount of

loan. It must invite investment from institutional investors will be invested in the business in

order to earn profit. If revenue and profit of the firm will increase then earning per share will

increase automatically.

CONCLUSION

On the basis of above discussion it is concluded that ratio analysis is one of the most

important technique which is used by analysts to evaluate business firm from various angels. It is

also concluded that managers needs to use standards of the ratios very cautiously in order to

evaluate firm performance. It is concluded that there is very close relation between gross profit,

net profit and current ratio. If there will be low value of profitability ratios then value of liquidity

ratios will be below standards. Hence, firm must lay down main emphasis on improving its

profitability ratios. Firms must time to time use this method to measure there standing in the

industry in comparison to peer firm. By using this method firm can identify its weak points and

by taking steps on time it can remain ahead of its competitors.

increase automatically.

CONCLUSION

On the basis of above discussion it is concluded that ratio analysis is one of the most

important technique which is used by analysts to evaluate business firm from various angels. It is

also concluded that managers needs to use standards of the ratios very cautiously in order to

evaluate firm performance. It is concluded that there is very close relation between gross profit,

net profit and current ratio. If there will be low value of profitability ratios then value of liquidity

ratios will be below standards. Hence, firm must lay down main emphasis on improving its

profitability ratios. Firms must time to time use this method to measure there standing in the

industry in comparison to peer firm. By using this method firm can identify its weak points and

by taking steps on time it can remain ahead of its competitors.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.