Stakeholder Engagement in Sustainability

VerifiedAdded on 2020/02/24

|20

|5015

|219

AI Summary

This assignment delves into the concept of stakeholder engagement within the context of sustainability reporting. It examines various theoretical perspectives on stakeholder engagement, including normative stakeholder theory and its implications for ethical decision-making. The assignment also discusses practical challenges associated with engaging stakeholders effectively, emphasizing the importance of transparency, communication, and collaboration in fostering sustainable practices.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

ACCOUNTING THEORY

1

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

Introduction................................................................................................................................3

Requirement 1............................................................................................................................4

Discussion of terms................................................................................................................4

Requirement 2............................................................................................................................5

Concept of Stakeholder Engagement.....................................................................................5

Stakeholders of the firm.........................................................................................................5

Requirement 3............................................................................................................................7

Accounting theories................................................................................................................7

Requirement 4............................................................................................................................9

Adequacy of Data...................................................................................................................9

Requirement 5..........................................................................................................................10

Research Proposal................................................................................................................10

Conclusion................................................................................................................................14

References................................................................................................................................15

2

Introduction................................................................................................................................3

Requirement 1............................................................................................................................4

Discussion of terms................................................................................................................4

Requirement 2............................................................................................................................5

Concept of Stakeholder Engagement.....................................................................................5

Stakeholders of the firm.........................................................................................................5

Requirement 3............................................................................................................................7

Accounting theories................................................................................................................7

Requirement 4............................................................................................................................9

Adequacy of Data...................................................................................................................9

Requirement 5..........................................................................................................................10

Research Proposal................................................................................................................10

Conclusion................................................................................................................................14

References................................................................................................................................15

2

Introduction

This report embarks on the stakeholder’s engagement. As the stakeholders are related to the

business and organization. There are five important parts of the report. The first requirement

of the report includes the description of some important terms used in the report. The second

requirement of the project describes the concept of the stakeholder’s management and the

different stakeholders of the firm. The third requirement of the report includes the different

accounting theories in perspective to the stakeholder’s engagement. The requirement

critically reflects the adequacy of different data i.e. primary and secondary to support the

study. In the fifth requirement of the report is related to the research. A proposal for the

research is being made which includes the research question, objective, importance, literature

review, methodology and the steps for ethical approval to undertake the research project.

3

This report embarks on the stakeholder’s engagement. As the stakeholders are related to the

business and organization. There are five important parts of the report. The first requirement

of the report includes the description of some important terms used in the report. The second

requirement of the project describes the concept of the stakeholder’s management and the

different stakeholders of the firm. The third requirement of the report includes the different

accounting theories in perspective to the stakeholder’s engagement. The requirement

critically reflects the adequacy of different data i.e. primary and secondary to support the

study. In the fifth requirement of the report is related to the research. A proposal for the

research is being made which includes the research question, objective, importance, literature

review, methodology and the steps for ethical approval to undertake the research project.

3

Requirement 1

Discussion of terms

Some of the important terms are discussed below:

Stakeholder- The term stakeholder means a person or group of person or any organization

has an interest in investing in an organization or have a stake in the company for earning a

profit or we can say a person or an organization having an interest in a start-up of a new

project in the organization (Manetti, 2013).

Internal stakeholder- Internal stakeholder is the owner's managers and employees of the

organization these are responsible for the organization growth, owners, managers, and

employees perform the operation by helping them in making the strategy and plans and also

make the decision for the success of the organization (Lorne & Dilling, 2012).

External stakeholder- External stakeholders are those such as customers, suppliers and

creditors these are the outside persons who take the interest in company for investment

(Lorne & Dilling, 2012). Customers are those which purchase the products of the company

and the suppliers are those which purchase the product form the company for the society and

the creditors are those such as banks, government from which company takes the money for

the business these all are the external stakeholders.

Stakeholder Engagement- Stakeholder engagement is the process in which people are

involved from the outside in the organization in the decision-making process, as the

stakeholder's activities can affect the decision of the organization or the decision taken by the

organization can affect the stakeholder's interests. Stakeholders are the most important part of

the company which helps in the organization to find out the social and environmental issue of

the company which is going on outside (Kaur, 2014). The responsibility of stakeholder

engagement is to find out the solution for these issues and help the company for improving

their performance and help in achieving the objectives of the company.

Accounting theory- Accounting theory can be described as a process, which examines the

methodologies of the accounting, it is a set of accounting rules and the principle of the

financial accounting. Accounting theory is set of principle by which company accounts can

be properly managed by the company.

4

Discussion of terms

Some of the important terms are discussed below:

Stakeholder- The term stakeholder means a person or group of person or any organization

has an interest in investing in an organization or have a stake in the company for earning a

profit or we can say a person or an organization having an interest in a start-up of a new

project in the organization (Manetti, 2013).

Internal stakeholder- Internal stakeholder is the owner's managers and employees of the

organization these are responsible for the organization growth, owners, managers, and

employees perform the operation by helping them in making the strategy and plans and also

make the decision for the success of the organization (Lorne & Dilling, 2012).

External stakeholder- External stakeholders are those such as customers, suppliers and

creditors these are the outside persons who take the interest in company for investment

(Lorne & Dilling, 2012). Customers are those which purchase the products of the company

and the suppliers are those which purchase the product form the company for the society and

the creditors are those such as banks, government from which company takes the money for

the business these all are the external stakeholders.

Stakeholder Engagement- Stakeholder engagement is the process in which people are

involved from the outside in the organization in the decision-making process, as the

stakeholder's activities can affect the decision of the organization or the decision taken by the

organization can affect the stakeholder's interests. Stakeholders are the most important part of

the company which helps in the organization to find out the social and environmental issue of

the company which is going on outside (Kaur, 2014). The responsibility of stakeholder

engagement is to find out the solution for these issues and help the company for improving

their performance and help in achieving the objectives of the company.

Accounting theory- Accounting theory can be described as a process, which examines the

methodologies of the accounting, it is a set of accounting rules and the principle of the

financial accounting. Accounting theory is set of principle by which company accounts can

be properly managed by the company.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sustainability reporting- The term sustainability reporting can be defined as a report that is

used to be published by an organization or a company about social, environmental and

economic impacts caused by their activities (Bal & Bryde, 2013).

Integrated reporting- A report created by an organization in order to communicate its

prospects, performance, governance, and strategies that will result in creating value over the

short, medium and long-term (Zakhem, 2017).

Corporate social reporting- It is a concept of corporate social responsibilities that consist of

a process of communicating the environmental and social possessions of organizations

profitable engagements to specific interest groups within the society (Belal, 2016).

5

used to be published by an organization or a company about social, environmental and

economic impacts caused by their activities (Bal & Bryde, 2013).

Integrated reporting- A report created by an organization in order to communicate its

prospects, performance, governance, and strategies that will result in creating value over the

short, medium and long-term (Zakhem, 2017).

Corporate social reporting- It is a concept of corporate social responsibilities that consist of

a process of communicating the environmental and social possessions of organizations

profitable engagements to specific interest groups within the society (Belal, 2016).

5

Requirement 2

Concept of Stakeholder Engagement

Stakeholder Engagement plays an important role in an organization by the help of

engagement of stakeholders in several business aspects, an organization can make provisions

for its activities and it can also evade the social reaction (Kaur, 2014). In an organization, the

involvement of the stakeholders enables the organization to ascertain and address the

apprehensions, that decrease the threats and deadlocks which are used to arise from confusion

or misunderstandings (Lemke, 2015). As through the involvement of stakeholders, potential

problems could be identified and plan can be developed to mitigate those problems before

they arise; it helps the organization to function in a more constant socio-political

environment.

Stakeholder engagement can be elucidated as the initiation of collaborative activities

instigated by the business with its stakeholders. There are lots of opportunities to embark on

the engagement of stakeholders and a number of way for instigating a dialogue. An

organization has to pay the attention while building the relationships and also make

consideration in recognizing the stakeholder that can be affected by the different projects

(Glover, 2015). In addition to this engagement of stakeholders helps in solving the issue not

only related to the organization but also related to the stakeholders In both of the aspects,

stakeholder engagement involves two essential points:- Identification of the Stakeholder and

Dialogue with the stakeholders.

Stakeholders of the firm

The term stakeholder can be defined as a group or individual which may be affected through

or may affect the achievement of the organization`s goals. In this these traditionally has been

such as:

Internal stakeholder- The internal stakeholders of the firm are employees and

shareholder

Coordinate authorities- The external shareholders of the firm are- customers and

suppliers

External stakeholder- Some other stakeholders of the firm are professional

associations and government.

It is crucial for the organization to ascertain all the important stakeholders including those

who have been forgotten frequently, but then again they could make a major impression on

reputation and activities or functions of the organization, such as aboriginal communities or

6

Concept of Stakeholder Engagement

Stakeholder Engagement plays an important role in an organization by the help of

engagement of stakeholders in several business aspects, an organization can make provisions

for its activities and it can also evade the social reaction (Kaur, 2014). In an organization, the

involvement of the stakeholders enables the organization to ascertain and address the

apprehensions, that decrease the threats and deadlocks which are used to arise from confusion

or misunderstandings (Lemke, 2015). As through the involvement of stakeholders, potential

problems could be identified and plan can be developed to mitigate those problems before

they arise; it helps the organization to function in a more constant socio-political

environment.

Stakeholder engagement can be elucidated as the initiation of collaborative activities

instigated by the business with its stakeholders. There are lots of opportunities to embark on

the engagement of stakeholders and a number of way for instigating a dialogue. An

organization has to pay the attention while building the relationships and also make

consideration in recognizing the stakeholder that can be affected by the different projects

(Glover, 2015). In addition to this engagement of stakeholders helps in solving the issue not

only related to the organization but also related to the stakeholders In both of the aspects,

stakeholder engagement involves two essential points:- Identification of the Stakeholder and

Dialogue with the stakeholders.

Stakeholders of the firm

The term stakeholder can be defined as a group or individual which may be affected through

or may affect the achievement of the organization`s goals. In this these traditionally has been

such as:

Internal stakeholder- The internal stakeholders of the firm are employees and

shareholder

Coordinate authorities- The external shareholders of the firm are- customers and

suppliers

External stakeholder- Some other stakeholders of the firm are professional

associations and government.

It is crucial for the organization to ascertain all the important stakeholders including those

who have been forgotten frequently, but then again they could make a major impression on

reputation and activities or functions of the organization, such as aboriginal communities or

6

activities group (Bal, et al., 2013). In addition to this, the responsible organization has to

identify and work together with the stakeholders who are going to be influenced by its

activities; on the whole, if the influence is expected to be negative. One of the other measures

for recognizing and listing stakeholders consist of the attributes of urgency, legitimacy,

power as well as the ability of the stakeholders that may affect or could be affected by the

actions perceived by the organization (Manetti, 2013).

7

identify and work together with the stakeholders who are going to be influenced by its

activities; on the whole, if the influence is expected to be negative. One of the other measures

for recognizing and listing stakeholders consist of the attributes of urgency, legitimacy,

power as well as the ability of the stakeholders that may affect or could be affected by the

actions perceived by the organization (Manetti, 2013).

7

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Requirement 3

Accounting theories

In this case study, the organization needs the support from stakeholders to find out issues

related to environmental and social aspects professed by the stakeholders. Corporate social

reporting is useful for the organizations in order to represent itself as socially responsible. In

this by the help of accounting and integrated reporting, stakeholders relation can be

maintained and move towards the operations (Manetti, 2013). Sustainability reporting and

accounting can build a base for dealing with complex stakeholder’s relationships and moving

towards other viable processes. According to the accountability theory, the success of the

engagement is based on the understanding the following aspects-

Who are the stakeholders that could be engaged,

Why these stakeholders shall be engaged (purpose of stakeholder engagement)

What is the scope of stakeholder engagement

How the engagement of stakeholders could be done (technique for stakeholder

engagement)

This accounting theory determines that the involvement of stakeholders supports

organizations to develop and improve strategy as well as to identify and address operational

issues.

Normative stakeholder theory lays emphasis on the activities of the organization that what

the organizations shall do in context to the stakeholders. This theory is based upon treatments

of some aspects such as- corporate legitimacy principle, fiduciary principle, and corporate

social responsibility (Kaur, 2014). These two aspects are different from each other, as the

first aspects embark on the stakeholders that can retain the ability to influence the

organization is legitimate; on the other hand, the second aspects state that such legitimacy is

consequential from ethical responsibility outstanding to other stakeholders.

Instrumental theory, in contrast to this, the instrumental theory lays emphasis on the

concept that whether the activities carried out by the organization is beneficial for the

business or not, however, the interest of the stakeholders should be considered. This theory is

regarded as a part of instrumental version and depicts shareholders as crucial factors which

support the organization to accomplish its goals and objectives as well as empowers the

leaders to come across their fiduciary responsibilities to the shareholders (Doherty, et al.,

2009). As per this theory, organizations deal with its stakeholders on the basis of

collaboration; in addition to this, the mutual trust facilitates competitive advantage to the

8

Accounting theories

In this case study, the organization needs the support from stakeholders to find out issues

related to environmental and social aspects professed by the stakeholders. Corporate social

reporting is useful for the organizations in order to represent itself as socially responsible. In

this by the help of accounting and integrated reporting, stakeholders relation can be

maintained and move towards the operations (Manetti, 2013). Sustainability reporting and

accounting can build a base for dealing with complex stakeholder’s relationships and moving

towards other viable processes. According to the accountability theory, the success of the

engagement is based on the understanding the following aspects-

Who are the stakeholders that could be engaged,

Why these stakeholders shall be engaged (purpose of stakeholder engagement)

What is the scope of stakeholder engagement

How the engagement of stakeholders could be done (technique for stakeholder

engagement)

This accounting theory determines that the involvement of stakeholders supports

organizations to develop and improve strategy as well as to identify and address operational

issues.

Normative stakeholder theory lays emphasis on the activities of the organization that what

the organizations shall do in context to the stakeholders. This theory is based upon treatments

of some aspects such as- corporate legitimacy principle, fiduciary principle, and corporate

social responsibility (Kaur, 2014). These two aspects are different from each other, as the

first aspects embark on the stakeholders that can retain the ability to influence the

organization is legitimate; on the other hand, the second aspects state that such legitimacy is

consequential from ethical responsibility outstanding to other stakeholders.

Instrumental theory, in contrast to this, the instrumental theory lays emphasis on the

concept that whether the activities carried out by the organization is beneficial for the

business or not, however, the interest of the stakeholders should be considered. This theory is

regarded as a part of instrumental version and depicts shareholders as crucial factors which

support the organization to accomplish its goals and objectives as well as empowers the

leaders to come across their fiduciary responsibilities to the shareholders (Doherty, et al.,

2009). As per this theory, organizations deal with its stakeholders on the basis of

collaboration; in addition to this, the mutual trust facilitates competitive advantage to the

8

organization (as in case the competitors are not considering the stakeholder`s engagement).

The instrumental stakeholder’s theory is based upon the underlying principle that

stakeholders can be grouped as shareholders, customers, and labors. These groups operate as

structural units in which common ideas could be shared by the members.

Sustainability theory specifies the identification of the stakeholder states that, the important

stakeholders for the business shall be identified. After identifying the stakeholders of the

organization. They shall be engaged in various processes of the organization.

Descriptive stakeholder’s theory, general outline and elucidate the organization`s specific

behaviors and characteristics, for instance, nature of the organization. This theory embraces

that the firm is at the center of competition and cooperation, both of their inherent value. In

addition to this, the descriptive theory in relation to stakeholder`s aspects describe such

factors- organization`s nature, managers way of thinking in context to the management

aspects, how the management of corporations can be done in reality, thinking of board

members in regards to corporate constituencies` interests and identification of stakeholders

(Bal, et al., 2013).

The accounting theories which also support the aspects of engagement of stakeholders is one

of the essential parts of sustainability accounting process; for instance, it can provide various

benefits to the organization such as-

1. To ascertain stakeholder concerns concerning to its activities and economic, social as

well as environmental performance (Ali & Abdelfettah, 2016).

2. To define the scope of the present process in context to the stakeholders, accounting

framework, operating issues and units and geographical locations as well as centered

on engagement consequences.

3. To recognize social, economic and environmental indicators over and done with

stakeholder engagement (Glover, 2015). To gather information in context to the

performance of the organization in perspective to the recognized indicators.

Moral accounting theory outlines the responsibility of the managers for internal

stakeholders such as employees. Managers are responsible to take account of employee`s

legitimate rights (Glover, 2015).

9

The instrumental stakeholder’s theory is based upon the underlying principle that

stakeholders can be grouped as shareholders, customers, and labors. These groups operate as

structural units in which common ideas could be shared by the members.

Sustainability theory specifies the identification of the stakeholder states that, the important

stakeholders for the business shall be identified. After identifying the stakeholders of the

organization. They shall be engaged in various processes of the organization.

Descriptive stakeholder’s theory, general outline and elucidate the organization`s specific

behaviors and characteristics, for instance, nature of the organization. This theory embraces

that the firm is at the center of competition and cooperation, both of their inherent value. In

addition to this, the descriptive theory in relation to stakeholder`s aspects describe such

factors- organization`s nature, managers way of thinking in context to the management

aspects, how the management of corporations can be done in reality, thinking of board

members in regards to corporate constituencies` interests and identification of stakeholders

(Bal, et al., 2013).

The accounting theories which also support the aspects of engagement of stakeholders is one

of the essential parts of sustainability accounting process; for instance, it can provide various

benefits to the organization such as-

1. To ascertain stakeholder concerns concerning to its activities and economic, social as

well as environmental performance (Ali & Abdelfettah, 2016).

2. To define the scope of the present process in context to the stakeholders, accounting

framework, operating issues and units and geographical locations as well as centered

on engagement consequences.

3. To recognize social, economic and environmental indicators over and done with

stakeholder engagement (Glover, 2015). To gather information in context to the

performance of the organization in perspective to the recognized indicators.

Moral accounting theory outlines the responsibility of the managers for internal

stakeholders such as employees. Managers are responsible to take account of employee`s

legitimate rights (Glover, 2015).

9

Requirement 4

Adequacy of Data

According to Professor Shallow, the secondary data is adequate in context to the study

purpose. As the secondary data is used to be gathered in an easy manner in comparison to the

primary data. Both of the data sources i.e. primary data and secondary data sources have their

own adequacies in relation to the study.

Primary data and its sources- Primary data are the first-hand data which is gathered by the

researcher for the first time when he or she has pursued the research (C & C, 2012). There are

a number of techniques through which the primary or first-hand data could be gathered. Some

of the primary data sources are- surveys, interviews, observation technique etc.

Secondary Data and its sources- It is also known as second-hand data, as the data is

gathered through some other researcher or individual for his or her own purpose (Olsen,

2011). This data can be easily used as the secondary data can be gathered from a number of

resources such as- internet, official reports, business reports and magazines, books, journals,

newspapers and many other sources.

Both of the sources to gather data for the research study are important in their own way. As

the primary data source could be approached by the researcher when more valid data is

required for the research as sometimes the secondary data could be less valid in comparison

to the primary data (C & C, 2012). In contrast to this, the secondary data could be approached

by the researcher for his or her study, when there is less time to complete the study, as to

collect the primary data it consumes more time. Whereas secondary data could be gathered in

less time as it is already available and could be approached through various sources and do

not consume more cost (Olsen, 2011). Hence, the data for the study could be approached by

considering following aspects- convenience, relevance, suitability, and requirement of the

study.

10

Adequacy of Data

According to Professor Shallow, the secondary data is adequate in context to the study

purpose. As the secondary data is used to be gathered in an easy manner in comparison to the

primary data. Both of the data sources i.e. primary data and secondary data sources have their

own adequacies in relation to the study.

Primary data and its sources- Primary data are the first-hand data which is gathered by the

researcher for the first time when he or she has pursued the research (C & C, 2012). There are

a number of techniques through which the primary or first-hand data could be gathered. Some

of the primary data sources are- surveys, interviews, observation technique etc.

Secondary Data and its sources- It is also known as second-hand data, as the data is

gathered through some other researcher or individual for his or her own purpose (Olsen,

2011). This data can be easily used as the secondary data can be gathered from a number of

resources such as- internet, official reports, business reports and magazines, books, journals,

newspapers and many other sources.

Both of the sources to gather data for the research study are important in their own way. As

the primary data source could be approached by the researcher when more valid data is

required for the research as sometimes the secondary data could be less valid in comparison

to the primary data (C & C, 2012). In contrast to this, the secondary data could be approached

by the researcher for his or her study, when there is less time to complete the study, as to

collect the primary data it consumes more time. Whereas secondary data could be gathered in

less time as it is already available and could be approached through various sources and do

not consume more cost (Olsen, 2011). Hence, the data for the study could be approached by

considering following aspects- convenience, relevance, suitability, and requirement of the

study.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Requirement 5

Research Proposal

Title of Research Project- A study on importance of stakeholder’s engagement

Importance of Research

This research is important to be pursued, as through the study it could be concluded that what

is the importance of the stakeholder’s engagement for an organization. As the stakeholders

are considered as the integral and essential part of the organizations (Bates, 2014). Each and

every organization have stakeholders and some of the important stakeholders of the

organization are- management, owner, employee, shareholders and investors, government,

customers etc. Through the research, the importance of the stakeholders and their engagement

will be ascertained and this will facilitate in the accomplishment of the objectives in a better

manner. Another importance of the research is that the importance of stakeholder’s

engagement in developing the guidelines and policies of the organization will also be

determined. As it is important to ascertain the importance of engaging with the stakeholders

in order to run the business successful (Denscombe, 2012). Besides this, the techniques which

could be used by the organization for motivating the stakeholder's engagement could also be

ascertained and such techniques may be used further.

The Research Question

The major question of the research is to ascertain- “What is the importance of

stakeholder’s engagement for an organization?”

In addition to this, there are some other important questions are also there which will be

answered through the research, some of the secondary questions that will support in ascertain

the answer for the major research questions are-

How can the stakeholders be engaged without affecting the organization`s business

aspects?

What are the techniques that could be practiced for stakeholder’s engagement?

What are the areas which require stakeholder’s engagement?

Literature Review

11

Research Proposal

Title of Research Project- A study on importance of stakeholder’s engagement

Importance of Research

This research is important to be pursued, as through the study it could be concluded that what

is the importance of the stakeholder’s engagement for an organization. As the stakeholders

are considered as the integral and essential part of the organizations (Bates, 2014). Each and

every organization have stakeholders and some of the important stakeholders of the

organization are- management, owner, employee, shareholders and investors, government,

customers etc. Through the research, the importance of the stakeholders and their engagement

will be ascertained and this will facilitate in the accomplishment of the objectives in a better

manner. Another importance of the research is that the importance of stakeholder’s

engagement in developing the guidelines and policies of the organization will also be

determined. As it is important to ascertain the importance of engaging with the stakeholders

in order to run the business successful (Denscombe, 2012). Besides this, the techniques which

could be used by the organization for motivating the stakeholder's engagement could also be

ascertained and such techniques may be used further.

The Research Question

The major question of the research is to ascertain- “What is the importance of

stakeholder’s engagement for an organization?”

In addition to this, there are some other important questions are also there which will be

answered through the research, some of the secondary questions that will support in ascertain

the answer for the major research questions are-

How can the stakeholders be engaged without affecting the organization`s business

aspects?

What are the techniques that could be practiced for stakeholder’s engagement?

What are the areas which require stakeholder’s engagement?

Literature Review

11

Engagement of stakeholders cannot be done in deprived of any difficulties that may consist

of- conflict with those outside the process, huge extent of staff time and extraordinary cost

(Belal, 2016). Irrespective of such encounters, it proves that stakeholder’s engagement is

beneficial in turning out useful and supported plans of the management and it also helps in

building long-stand and solid relationships.

Normative stakeholder theory lays consideration on the doings or undertakings of the

organization that what actions shall be undertaken by the organizations in regards to the

stakeholders (Kaur, 2014). This theory determines the aspects related to the treatment of a

number of aspects for instance- corporate legitimacy principle, corporate social responsibility

and fiduciary principle (Oruc, 2011).

On the other hand, the instrumental theory lays concentration on the perception that,

whether the actions were undertaken by the firm is constructive for the business or not;

though the stakeholder’s interest should be considered. So that interest of the stakeholders

shall not be influenced in a negative manner (Bal, et al., 2013). The instrumental

stakeholder’s theory is grounded upon the fundamental principle that stakeholders can come

together as labors, shareholders, and consumers. These groups work as essential units in

which common ideas, suggestions, and feedbacks could be shared by any of the members

(Manetti, 2013).

The descriptive theory, in context to stakeholder`s aspects, elucidate the factors related to

the stakeholders and the organizations. How the manager thinks about the engagement of

employees in the decision-making process, the way by which organization`s management can

be done, deliberation of top management about stakeholder`s identification and other aspects.

Moral accounting theory, states that managers shall take account of legitimate rights of the

employees (Williams & Adams, 2014). Moral stakeholder perspective shall be considered in

context to disclosure of employees issues in order to expand accountability and transparency

to society and employees.

Vilma Luoma-who in the year 2015, stated in his article that there are three different type of

stakeholder relationships. The first one has certainly engaged faith holders, the destructively

engaged holders and the last one is fake holders (Luoma-aho, 2015). For an effective public

relations; it is important to support the faith holders, engage the hate holders and reveal the

fake holders.

12

of- conflict with those outside the process, huge extent of staff time and extraordinary cost

(Belal, 2016). Irrespective of such encounters, it proves that stakeholder’s engagement is

beneficial in turning out useful and supported plans of the management and it also helps in

building long-stand and solid relationships.

Normative stakeholder theory lays consideration on the doings or undertakings of the

organization that what actions shall be undertaken by the organizations in regards to the

stakeholders (Kaur, 2014). This theory determines the aspects related to the treatment of a

number of aspects for instance- corporate legitimacy principle, corporate social responsibility

and fiduciary principle (Oruc, 2011).

On the other hand, the instrumental theory lays concentration on the perception that,

whether the actions were undertaken by the firm is constructive for the business or not;

though the stakeholder’s interest should be considered. So that interest of the stakeholders

shall not be influenced in a negative manner (Bal, et al., 2013). The instrumental

stakeholder’s theory is grounded upon the fundamental principle that stakeholders can come

together as labors, shareholders, and consumers. These groups work as essential units in

which common ideas, suggestions, and feedbacks could be shared by any of the members

(Manetti, 2013).

The descriptive theory, in context to stakeholder`s aspects, elucidate the factors related to

the stakeholders and the organizations. How the manager thinks about the engagement of

employees in the decision-making process, the way by which organization`s management can

be done, deliberation of top management about stakeholder`s identification and other aspects.

Moral accounting theory, states that managers shall take account of legitimate rights of the

employees (Williams & Adams, 2014). Moral stakeholder perspective shall be considered in

context to disclosure of employees issues in order to expand accountability and transparency

to society and employees.

Vilma Luoma-who in the year 2015, stated in his article that there are three different type of

stakeholder relationships. The first one has certainly engaged faith holders, the destructively

engaged holders and the last one is fake holders (Luoma-aho, 2015). For an effective public

relations; it is important to support the faith holders, engage the hate holders and reveal the

fake holders.

12

Menoka Bal and David Bryde in the year 2013, published their article in context to the

engagement of the stakeholders for achieving sustainability in the construction business. This

sustainability theory states that the important stakeholders for the business shall be identified.

The engagement of stakeholder can be done through a process which includes six different

steps i.e. identification of the stakeholders; relating stakeholders to different targets related to

sustainability; prioritization; managing; evaluating performance; carrying out targets into

action (Bal & Bryde, 2013).

Methodology

Type of research- It is a descriptive research, therefore qualitative research methodology will

be followed for the study.

Sample technique- Convenient sample technique is going to be approached for the research

as through such technique, the sampling of the respondent could be done as per the

researcher’s convenience (Becker, & Denicolo, 2012).

A number of the sample- The number of sample for the study will be four different managers

if different organization.

Data collection- Primary data will be approached for the study, as the research requires fresh

data to be studied to reach a conclusion ( Leavy, 2017). Data will be collected through a

survey. As this technique will be suitable for the research.

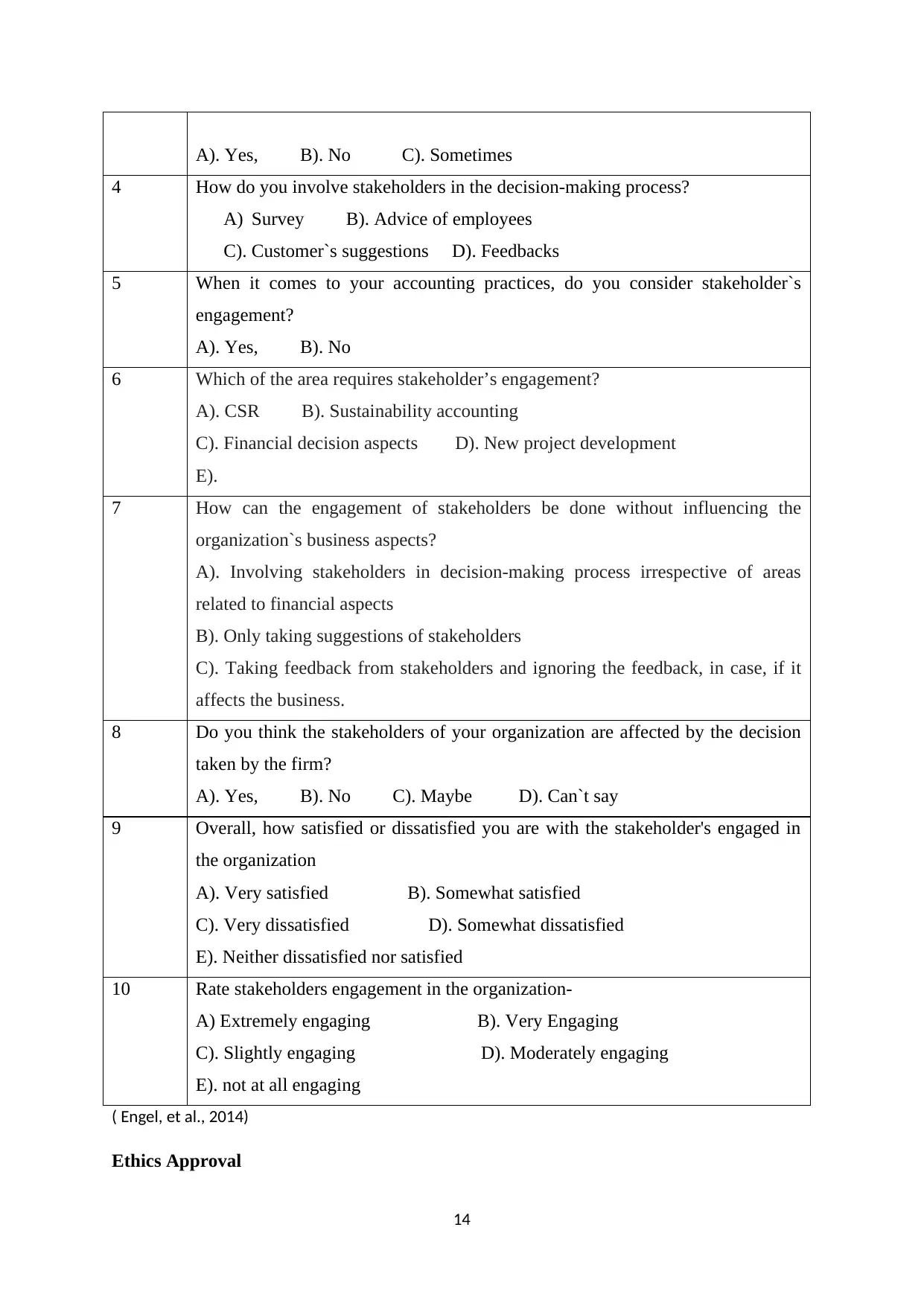

Survey Questions

The questions which will be asked to the respondent samples are given below:

Questio

n No.

Questions

1 Do you consider stakeholders as an important part of your organization?

A). Yes, B). No C). Sometimes

2 Do you think stakeholder’s engagement is an important perspective for the

business and stakeholders benefits?

A). Yes, B). No C). Maybe

3 Do you let your stakeholders participate in the decision-making process?

13

engagement of the stakeholders for achieving sustainability in the construction business. This

sustainability theory states that the important stakeholders for the business shall be identified.

The engagement of stakeholder can be done through a process which includes six different

steps i.e. identification of the stakeholders; relating stakeholders to different targets related to

sustainability; prioritization; managing; evaluating performance; carrying out targets into

action (Bal & Bryde, 2013).

Methodology

Type of research- It is a descriptive research, therefore qualitative research methodology will

be followed for the study.

Sample technique- Convenient sample technique is going to be approached for the research

as through such technique, the sampling of the respondent could be done as per the

researcher’s convenience (Becker, & Denicolo, 2012).

A number of the sample- The number of sample for the study will be four different managers

if different organization.

Data collection- Primary data will be approached for the study, as the research requires fresh

data to be studied to reach a conclusion ( Leavy, 2017). Data will be collected through a

survey. As this technique will be suitable for the research.

Survey Questions

The questions which will be asked to the respondent samples are given below:

Questio

n No.

Questions

1 Do you consider stakeholders as an important part of your organization?

A). Yes, B). No C). Sometimes

2 Do you think stakeholder’s engagement is an important perspective for the

business and stakeholders benefits?

A). Yes, B). No C). Maybe

3 Do you let your stakeholders participate in the decision-making process?

13

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

A). Yes, B). No C). Sometimes

4 How do you involve stakeholders in the decision-making process?

A) Survey B). Advice of employees

C). Customer`s suggestions D). Feedbacks

5 When it comes to your accounting practices, do you consider stakeholder`s

engagement?

A). Yes, B). No

6 Which of the area requires stakeholder’s engagement?

A). CSR B). Sustainability accounting

C). Financial decision aspects D). New project development

E).

7 How can the engagement of stakeholders be done without influencing the

organization`s business aspects?

A). Involving stakeholders in decision-making process irrespective of areas

related to financial aspects

B). Only taking suggestions of stakeholders

C). Taking feedback from stakeholders and ignoring the feedback, in case, if it

affects the business.

8 Do you think the stakeholders of your organization are affected by the decision

taken by the firm?

A). Yes, B). No C). Maybe D). Can`t say

9 Overall, how satisfied or dissatisfied you are with the stakeholder's engaged in

the organization

A). Very satisfied B). Somewhat satisfied

C). Very dissatisfied D). Somewhat dissatisfied

E). Neither dissatisfied nor satisfied

10 Rate stakeholders engagement in the organization-

A) Extremely engaging B). Very Engaging

C). Slightly engaging D). Moderately engaging

E). not at all engaging

( Engel, et al., 2014)

Ethics Approval

14

4 How do you involve stakeholders in the decision-making process?

A) Survey B). Advice of employees

C). Customer`s suggestions D). Feedbacks

5 When it comes to your accounting practices, do you consider stakeholder`s

engagement?

A). Yes, B). No

6 Which of the area requires stakeholder’s engagement?

A). CSR B). Sustainability accounting

C). Financial decision aspects D). New project development

E).

7 How can the engagement of stakeholders be done without influencing the

organization`s business aspects?

A). Involving stakeholders in decision-making process irrespective of areas

related to financial aspects

B). Only taking suggestions of stakeholders

C). Taking feedback from stakeholders and ignoring the feedback, in case, if it

affects the business.

8 Do you think the stakeholders of your organization are affected by the decision

taken by the firm?

A). Yes, B). No C). Maybe D). Can`t say

9 Overall, how satisfied or dissatisfied you are with the stakeholder's engaged in

the organization

A). Very satisfied B). Somewhat satisfied

C). Very dissatisfied D). Somewhat dissatisfied

E). Neither dissatisfied nor satisfied

10 Rate stakeholders engagement in the organization-

A) Extremely engaging B). Very Engaging

C). Slightly engaging D). Moderately engaging

E). not at all engaging

( Engel, et al., 2014)

Ethics Approval

14

The steps which are required to be taken in order to gain ethical approval to undertake this

project are given below:

Step 1. The very first step will be to assemble all the application documents such as-

supporting documents and application forms (survey instrument).

Step 2. The application package will be signed off by the Head of School, afterward,

the signed application will be sent to the Human Ethics office (Hammond, 2016).

Step 3. The office if Human Ethics will evaluate the application`s level of risk and

this application will be assigned to the potential review pathways.

Step 4. The ethics application will be reviewed ( Frankena, 2015) by the RERC or

HREC. In case any changes are there then it will be requested by the review body.

After making the requested changes application will be accepted by the body.

Step 5. Notification of the ethics approval for the project will be granted by the

Human Ethics office, after then the research project could begin.

15

project are given below:

Step 1. The very first step will be to assemble all the application documents such as-

supporting documents and application forms (survey instrument).

Step 2. The application package will be signed off by the Head of School, afterward,

the signed application will be sent to the Human Ethics office (Hammond, 2016).

Step 3. The office if Human Ethics will evaluate the application`s level of risk and

this application will be assigned to the potential review pathways.

Step 4. The ethics application will be reviewed ( Frankena, 2015) by the RERC or

HREC. In case any changes are there then it will be requested by the review body.

After making the requested changes application will be accepted by the body.

Step 5. Notification of the ethics approval for the project will be granted by the

Human Ethics office, after then the research project could begin.

15

Conclusion

This could be concluded from the report that there are different thoughts about stakeholder’s

engagement. As the stakeholders are the inseparable part of the organization, therefore it is

must for the firm to consider about the stakeholders while initiating a plan, or change in the

process. As the organization`s activities may influence the interests of the stakeholders in the

positive or negative way. Beside this, it is also not wrong to say, that the activities of the

stakeholders as well can influence the business of the firm. Therefore it is concluded from the

study that stakeholders shall be considered in context to the sustainability reporting and

accounting.

16

This could be concluded from the report that there are different thoughts about stakeholder’s

engagement. As the stakeholders are the inseparable part of the organization, therefore it is

must for the firm to consider about the stakeholders while initiating a plan, or change in the

process. As the organization`s activities may influence the interests of the stakeholders in the

positive or negative way. Beside this, it is also not wrong to say, that the activities of the

stakeholders as well can influence the business of the firm. Therefore it is concluded from the

study that stakeholders shall be considered in context to the sustainability reporting and

accounting.

16

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Creswell, J. W., 2014. Research Design: Qualitative, Quantitative, and Mixed Methods

Approaches. s.l.:SAGE.

Engel, U., Jann, B. & Lynn, ., 2014. Improving Survey Methods: Lessons from Recent

Research. s.l.:Routledge. .

Israel, D., 2009. Data Analysis in Business Research. s.l.: SAGE Publications.

Kuada, J., 2012. Research Methodology. s.l.:Samfundslitteratur.

Leavy, P., 2017. Research Design. s.l.:Guilford Publications.

Marsden, P. V. & Wright, . D., 2010. Handbook of Survey Research. s.l.:Emerald Group

Publishing.

Saris, W. E. & Gallhofer, . N., 2014. Design, Evaluation, and Analysis of Questionnaires for

Survey Research. s.l.: John Wiley & Sons..

Troidl, H., Spitzer, . & McPeek, . ., 2012. Principles and Practice of Research. s.l.:Springer

Science & Business Media.

Wetcher, D., 2011. Analyzing Quantitative Data. s.l.: John Wiley & Sons.

Ali, A. & Abdelfettah, B., 2016. An overview on stakeholder theory perspective:

towardsmanaging stakeholder expectation. International Academic Journal of Accounting

and Financial, 3(3), pp. 40-53.

Andres, L., 2012. Designing and Doing Survey Research. s.l.:SAGE.

Bal, M. & Bryde, D., 2013. Stakeholder Engagement: Achieving Sustainability in the

Construction Sector. [Online]

Available at: www.mdpi.com/2071-1050/5/2/695/pdf

[Accessed 20 10 2017].

Banfield, T., 2014. Why Customer Satisfaction is Important (and How to Focus on It).

[Online]

Available at: https://www.surveymonkey.com/blog/2015/02/06/customer-satisfaction-

important-focus/

Bates, S., 2014. Understanding and Doing Successful Research. s.l.:Routledge.

17

Creswell, J. W., 2014. Research Design: Qualitative, Quantitative, and Mixed Methods

Approaches. s.l.:SAGE.

Engel, U., Jann, B. & Lynn, ., 2014. Improving Survey Methods: Lessons from Recent

Research. s.l.:Routledge. .

Israel, D., 2009. Data Analysis in Business Research. s.l.: SAGE Publications.

Kuada, J., 2012. Research Methodology. s.l.:Samfundslitteratur.

Leavy, P., 2017. Research Design. s.l.:Guilford Publications.

Marsden, P. V. & Wright, . D., 2010. Handbook of Survey Research. s.l.:Emerald Group

Publishing.

Saris, W. E. & Gallhofer, . N., 2014. Design, Evaluation, and Analysis of Questionnaires for

Survey Research. s.l.: John Wiley & Sons..

Troidl, H., Spitzer, . & McPeek, . ., 2012. Principles and Practice of Research. s.l.:Springer

Science & Business Media.

Wetcher, D., 2011. Analyzing Quantitative Data. s.l.: John Wiley & Sons.

Ali, A. & Abdelfettah, B., 2016. An overview on stakeholder theory perspective:

towardsmanaging stakeholder expectation. International Academic Journal of Accounting

and Financial, 3(3), pp. 40-53.

Andres, L., 2012. Designing and Doing Survey Research. s.l.:SAGE.

Bal, M. & Bryde, D., 2013. Stakeholder Engagement: Achieving Sustainability in the

Construction Sector. [Online]

Available at: www.mdpi.com/2071-1050/5/2/695/pdf

[Accessed 20 10 2017].

Banfield, T., 2014. Why Customer Satisfaction is Important (and How to Focus on It).

[Online]

Available at: https://www.surveymonkey.com/blog/2015/02/06/customer-satisfaction-

important-focus/

Bates, S., 2014. Understanding and Doing Successful Research. s.l.:Routledge.

17

B. & C, M., 2012. Online Instruments, Data Collection, and Electronic Measurements. s.l.:

IGI Global.

Becker,, . L. & Denicolo, . P., 2012. Developing Research Proposals. s.l.:SAGE.

Belal, A. R., 2016. Corporate Social Responsibility Reporting in Developing Countries.

s.l.:Pages displayed by permission of Routledge.

Boeije, H. R., 2009. Analysis in Qualitative Research. s.l.:Sage.

Brown, M., 2012. Data mining techniques, s.l.: s.n.

Crowther, D. & Lancaster, G., 2012. Research Methods. s.l.: Routledge.

Denscombe, M., 2012. Research Proposals: A Practical Guide. s.l.:McGraw-Hill Education.

Doherty, B., Foster, G., Mason, C. & Meehan, J., 2009. Management for Social Enterprise.

s.l.:SAGE.

. F., 2015. Ethics. s.l.:Pearson Education.

Fowler, F. J., 2013. Survey Research Methods. s.l.: SAGE Publications.

Glover, J., 2015. Why stakeholder management is an important part of project management.

[Online]

Available at: http://cloud-collaboration.kahootz.com/why-stakeholder-management-is-an-

important-part-of-project-management

Hammond, W., 2016. Informed Consent: Procedures, Ethics and Best Practices. s.l.:Nova

Science Publishers.

Harrin, E., 2017. 4 UNUSUAL REASONS WHY STAKEHOLDER MANAGEMENT IS

IMPORTANT. [Online]

Available at: https://www.girlsguidetopm.com/4-unusual-reasons-why-stakeholder-

management-is-important/

Kaur, A., 2014. Stakeholder engagement in sustainability accounting and reporting: A study

of Australian local councils. [Online]

Available at:

http://search.ror.unisa.edu.au/media/researcharchive/open/9915866601701831/53111868410

001831

[Accessed 5 9 2017].

18

IGI Global.

Becker,, . L. & Denicolo, . P., 2012. Developing Research Proposals. s.l.:SAGE.

Belal, A. R., 2016. Corporate Social Responsibility Reporting in Developing Countries.

s.l.:Pages displayed by permission of Routledge.

Boeije, H. R., 2009. Analysis in Qualitative Research. s.l.:Sage.

Brown, M., 2012. Data mining techniques, s.l.: s.n.

Crowther, D. & Lancaster, G., 2012. Research Methods. s.l.: Routledge.

Denscombe, M., 2012. Research Proposals: A Practical Guide. s.l.:McGraw-Hill Education.

Doherty, B., Foster, G., Mason, C. & Meehan, J., 2009. Management for Social Enterprise.

s.l.:SAGE.

. F., 2015. Ethics. s.l.:Pearson Education.

Fowler, F. J., 2013. Survey Research Methods. s.l.: SAGE Publications.

Glover, J., 2015. Why stakeholder management is an important part of project management.

[Online]

Available at: http://cloud-collaboration.kahootz.com/why-stakeholder-management-is-an-

important-part-of-project-management

Hammond, W., 2016. Informed Consent: Procedures, Ethics and Best Practices. s.l.:Nova

Science Publishers.

Harrin, E., 2017. 4 UNUSUAL REASONS WHY STAKEHOLDER MANAGEMENT IS

IMPORTANT. [Online]

Available at: https://www.girlsguidetopm.com/4-unusual-reasons-why-stakeholder-

management-is-important/

Kaur, A., 2014. Stakeholder engagement in sustainability accounting and reporting: A study

of Australian local councils. [Online]

Available at:

http://search.ror.unisa.edu.au/media/researcharchive/open/9915866601701831/53111868410

001831

[Accessed 5 9 2017].

18

Khan, 2011. Research Methodology. s.l.:APH Publishing.

Lemke, A. A., 2015. Stakeholder engagement in policy development: challenges and

opportunities for human genomics. [Online]

Available at: https://www.ncbi.nlm.nih.gov/pmc/articles/PMC4567945/

[Accessed 10 9 2017].

Lorne, F. T. & Dilling, P., 2012. Creating Values for Sustainability: Stakeholders

Engagement, Incentive Alignment, and Value Currency. [Online]

Available at: https://www.hindawi.com/journals/ecri/2012/142910/

[Accessed 8 9 2017].

Luoma-aho, V., 2015. Understanding Stakeholder Engagement: Faith-holders, Hateholders &

Fakeholders. Research Journal of the Institute for Public Relations, 2(1), pp. 1-21.

Manetti, G., 2013. The Quality of Stakeholder Engagement in Sustainability Reporting:

Empirical Evidence and Critical Points. [Online]

Available at: http://citeseerx.ist.psu.edu/viewdoc/download?

doi=10.1.1.477.872&rep=rep1&type=pdf

[Accessed 6 9 2017].

Olsen, W., 2011. Data Collection. s.l.:SAGE..

Olsen, W., 2011. Data Collection: Key Debates and Methods in Social Research. s.l.:Sage.

Oruc, I., 2011. Normative stakeholder theory in relation to ethics of care. [Online]

Available at: http://www.emeraldinsight.com/doi/abs/10.1108/17471111111154527

[Accessed 10 9 2017].

Rinaldi, L., 2013. Stakeholder Engagement. [Online]

Available at: https://link.springer.com/chapter/10.1007/978-3-319-02168-3_6

[Accessed 4 9 2017].

Sawshilya, A., 2012. Ethics and Governance. s.l.:ICFAI.

Williams , S. & Adams, C. A., 2014. Moral accounting? Employee disclosures from a

stakeholder accountability perspective. [Online]

Available at: https://drcaroladams.net/moral-accounting-employee-disclosures-from-a-

stakeholder-accountability-perspective/

[Accessed 20 10 2017].

19

Lemke, A. A., 2015. Stakeholder engagement in policy development: challenges and

opportunities for human genomics. [Online]

Available at: https://www.ncbi.nlm.nih.gov/pmc/articles/PMC4567945/

[Accessed 10 9 2017].

Lorne, F. T. & Dilling, P., 2012. Creating Values for Sustainability: Stakeholders

Engagement, Incentive Alignment, and Value Currency. [Online]

Available at: https://www.hindawi.com/journals/ecri/2012/142910/

[Accessed 8 9 2017].

Luoma-aho, V., 2015. Understanding Stakeholder Engagement: Faith-holders, Hateholders &

Fakeholders. Research Journal of the Institute for Public Relations, 2(1), pp. 1-21.

Manetti, G., 2013. The Quality of Stakeholder Engagement in Sustainability Reporting:

Empirical Evidence and Critical Points. [Online]

Available at: http://citeseerx.ist.psu.edu/viewdoc/download?

doi=10.1.1.477.872&rep=rep1&type=pdf

[Accessed 6 9 2017].

Olsen, W., 2011. Data Collection. s.l.:SAGE..

Olsen, W., 2011. Data Collection: Key Debates and Methods in Social Research. s.l.:Sage.

Oruc, I., 2011. Normative stakeholder theory in relation to ethics of care. [Online]

Available at: http://www.emeraldinsight.com/doi/abs/10.1108/17471111111154527

[Accessed 10 9 2017].

Rinaldi, L., 2013. Stakeholder Engagement. [Online]

Available at: https://link.springer.com/chapter/10.1007/978-3-319-02168-3_6

[Accessed 4 9 2017].

Sawshilya, A., 2012. Ethics and Governance. s.l.:ICFAI.

Williams , S. & Adams, C. A., 2014. Moral accounting? Employee disclosures from a

stakeholder accountability perspective. [Online]

Available at: https://drcaroladams.net/moral-accounting-employee-disclosures-from-a-

stakeholder-accountability-perspective/

[Accessed 20 10 2017].

19

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Zakhem, A., 2017. Normative Stakeholder Theory. [Online]

Available at: http://www.emeraldinsight.com/doi/abs/10.1108/S2514-175920170000003

[Accessed 11 9 2017].

20

Available at: http://www.emeraldinsight.com/doi/abs/10.1108/S2514-175920170000003

[Accessed 11 9 2017].

20

1 out of 20

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.