Taxation Law Report: Analysis of Fringe Benefit Tax and Capital Gains

VerifiedAdded on 2021/02/21

|9

|2510

|128

Report

AI Summary

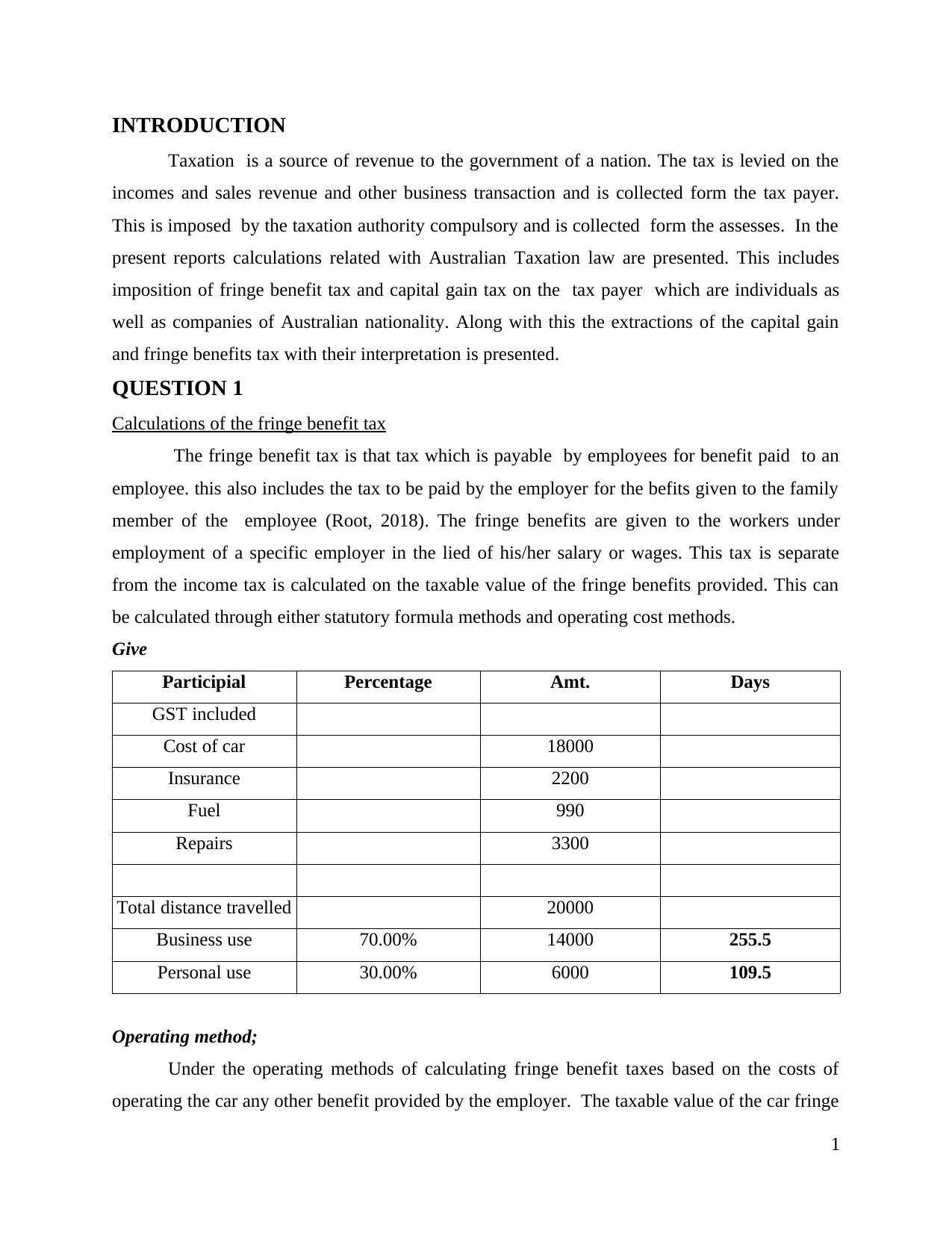

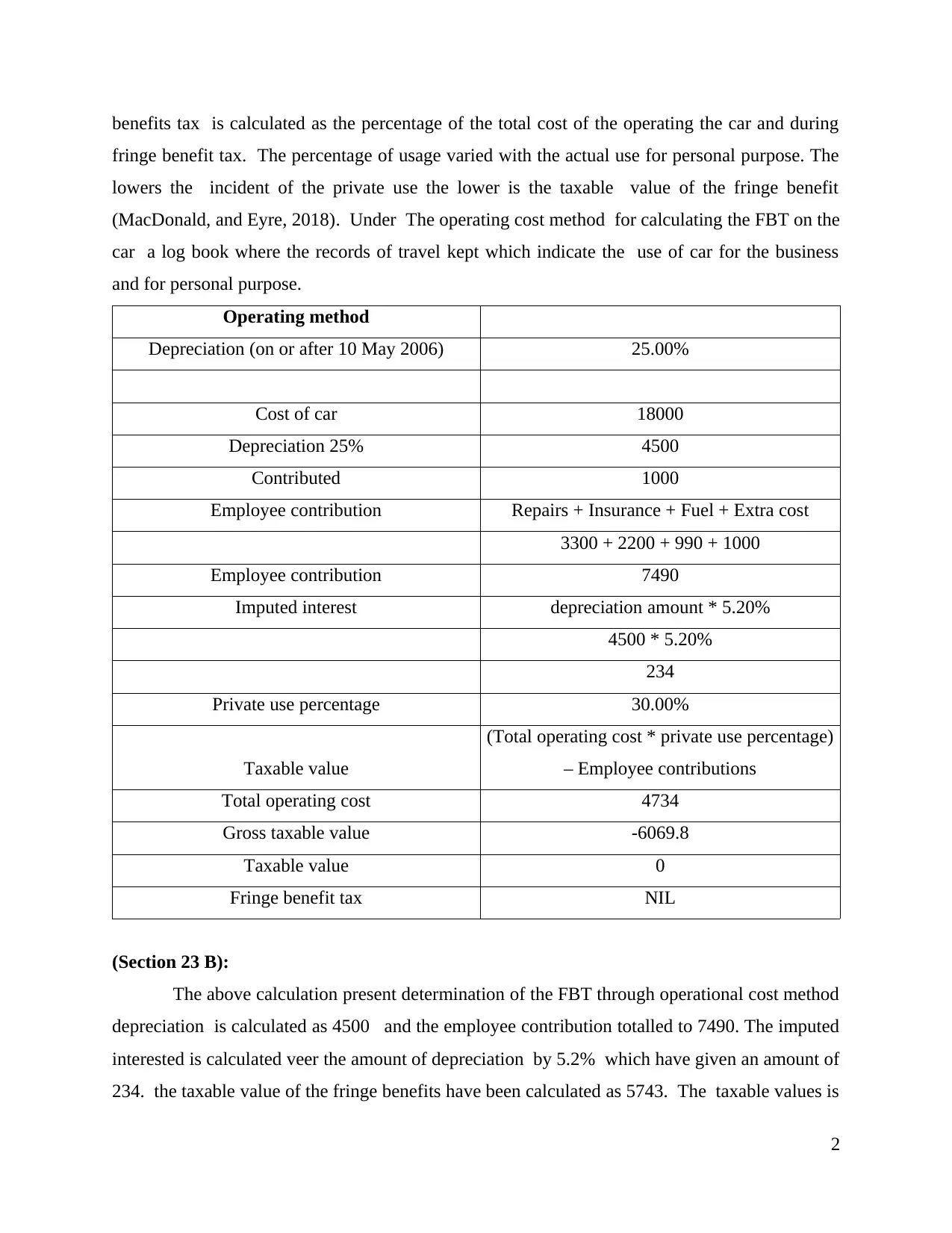

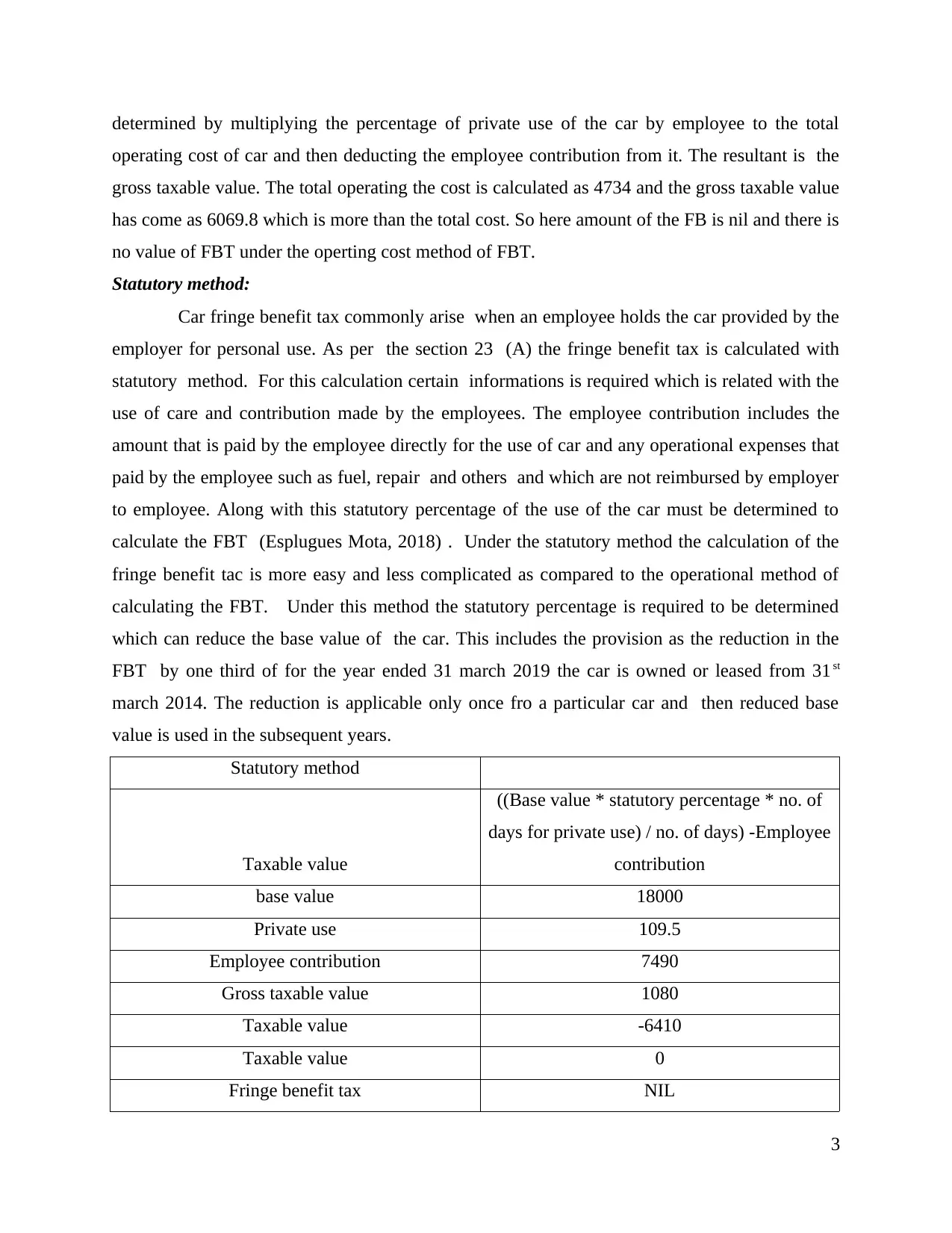

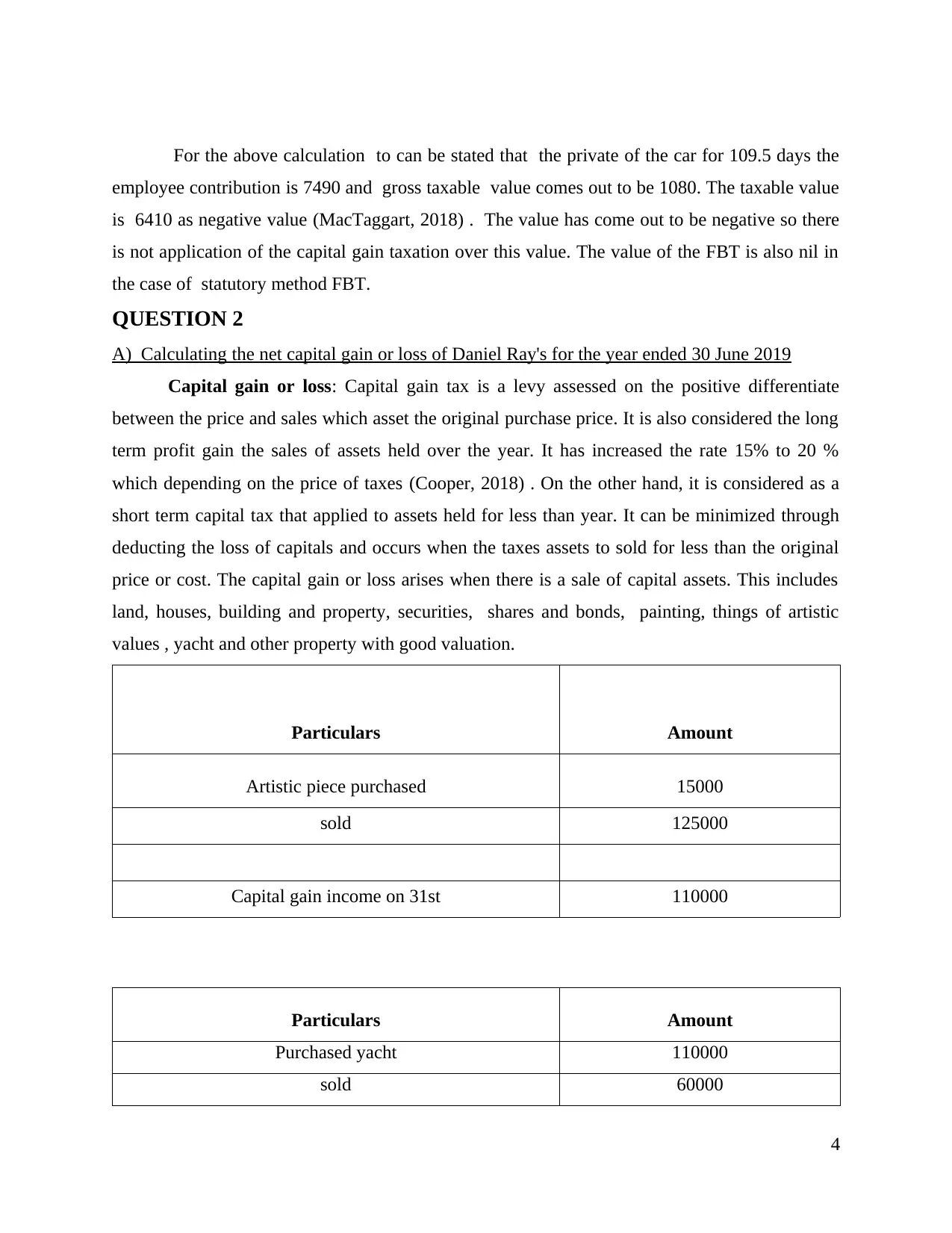

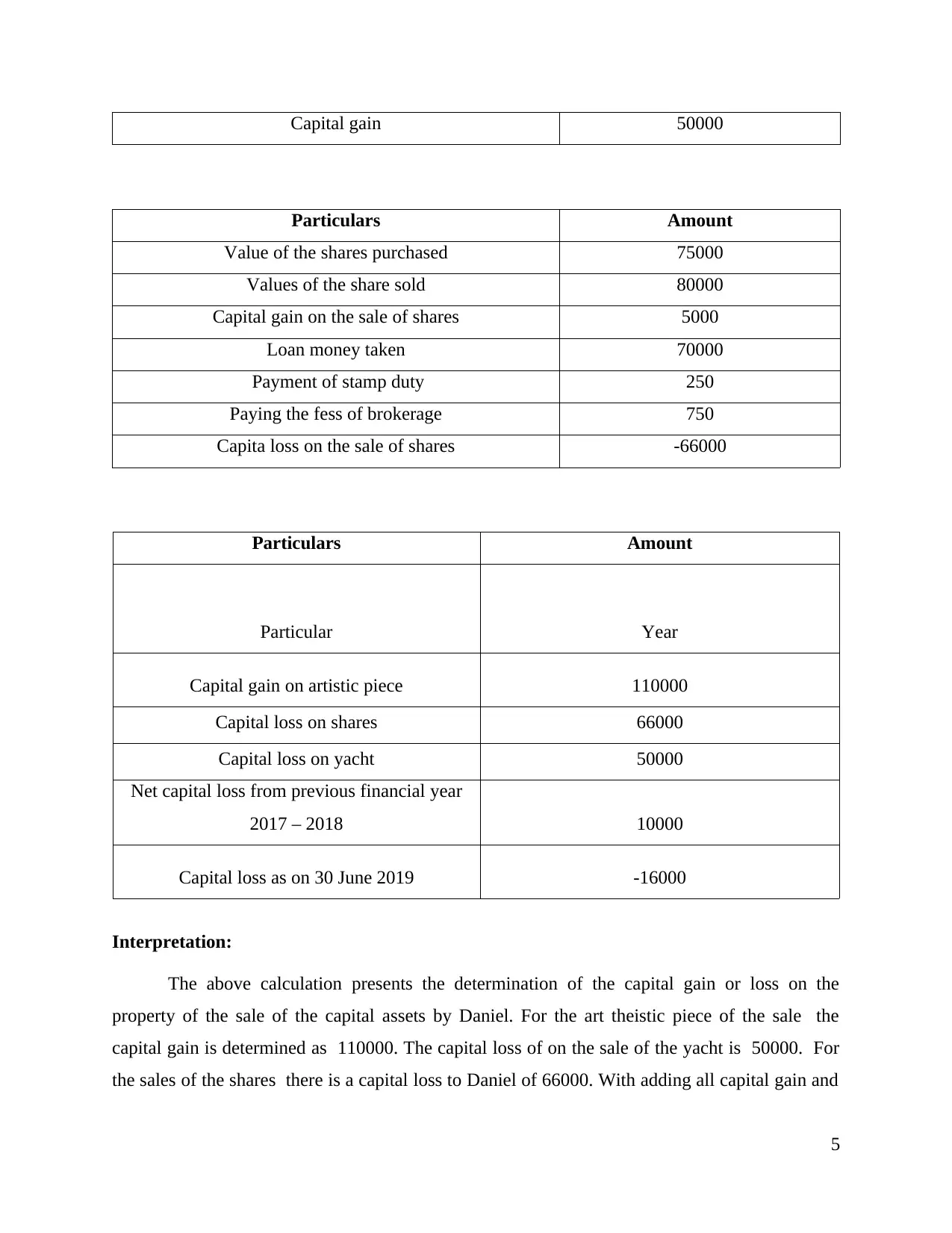

This report delves into the intricacies of Australian taxation law, providing a comprehensive analysis of fringe benefit tax (FBT) and capital gains tax (CGT). The report begins with an introduction to taxation as a revenue source for the government, setting the stage for detailed calculations and interpretations. Question 1 focuses on FBT, explaining its application to employee benefits and detailing calculations using both operating cost and statutory methods. The report then moves on to Question 2, which analyzes capital gains and losses for an individual named Daniel Ray. It calculates capital gains and losses from various assets, including artistic pieces, yachts, and shares. The report further examines Daniel's treatment of net capital gains and losses, differentiating between short-term and long-term perspectives and highlighting how capital losses can be carried forward to reduce future tax liabilities. The report concludes by summarizing the key takeaways from the analysis of FBT and CGT, providing a clear understanding of the tax implications in the Australian context.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.