Analysis of System Flow Charts: Purchases, Cash Disbursement, Payroll

VerifiedAdded on 2022/12/15

|13

|2842

|360

Report

AI Summary

This report provides a comprehensive analysis of system flow charts for purchases, cash disbursement, and payroll systems. It begins with an executive summary and table of contents, followed by detailed flow charts for each system, including explanations of the processes involved. The report identifies internal control weaknesses within each system, such as manual processes and potential for errors, and discusses the associated risks. Recommendations are made for improvement, emphasizing the implementation of an Accounting Information System (AIS). The report explores the benefits of AIS, including its ability to streamline transactions, improve accuracy, and provide detailed financial information. It differentiates between manual and legacy AIS, and explores the benefits of transitioning to a modern AIS, ultimately suggesting improvements in efficiency and accuracy through the use of technology. The report highlights the advantages of an accounting information system in enhancing business transactions, accounts payable and receivable, financial statements, and year-end closing processes.

Running head: SYSTEM FLOW CHART

SYSTEM FLOW CHART

Name of the Student

Name of the University

Author note

SYSTEM FLOW CHART

Name of the Student

Name of the University

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

SYSTEM FLOW CHART

Executive Summary

This report provides a brief explanation regarding the system flowchart of the purchases

system. This report also discusses about the system flowchart of the cash disbursement

system. Proper discussion regarding system flowchart of the payroll system is also provided.

Proper discussion regarding the internal management issues present will also be stated.

Proper discussion regarding the Accounting Information system is also provided in the report.

Importance of accounting information system is also provided along with the different kind of

systems that are in use.

SYSTEM FLOW CHART

Executive Summary

This report provides a brief explanation regarding the system flowchart of the purchases

system. This report also discusses about the system flowchart of the cash disbursement

system. Proper discussion regarding system flowchart of the payroll system is also provided.

Proper discussion regarding the internal management issues present will also be stated.

Proper discussion regarding the Accounting Information system is also provided in the report.

Importance of accounting information system is also provided along with the different kind of

systems that are in use.

2

SYSTEM FLOW CHART

Table of Contents

Introduction........................................................................................................................2

System flowchart of purchases system.............................................................................2

System flowchart of cash disbursement system...............................................................4

System flowchart of payroll system...................................................................................5

Description of internal control weakness in the following systems...................................6

Conclusion.......................................................................................................................10

References.......................................................................................................................11

SYSTEM FLOW CHART

Table of Contents

Introduction........................................................................................................................2

System flowchart of purchases system.............................................................................2

System flowchart of cash disbursement system...............................................................4

System flowchart of payroll system...................................................................................5

Description of internal control weakness in the following systems...................................6

Conclusion.......................................................................................................................10

References.......................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

SYSTEM FLOW CHART

Introduction

This report will be discussing about the system flow chart of the purchases system.

Proper discussion regarding the cash disbursement system is also made in this report.

Discussion regarding the system flowchart of payroll system is also stated. Description of the

internal management issues are also well discussed in this report.

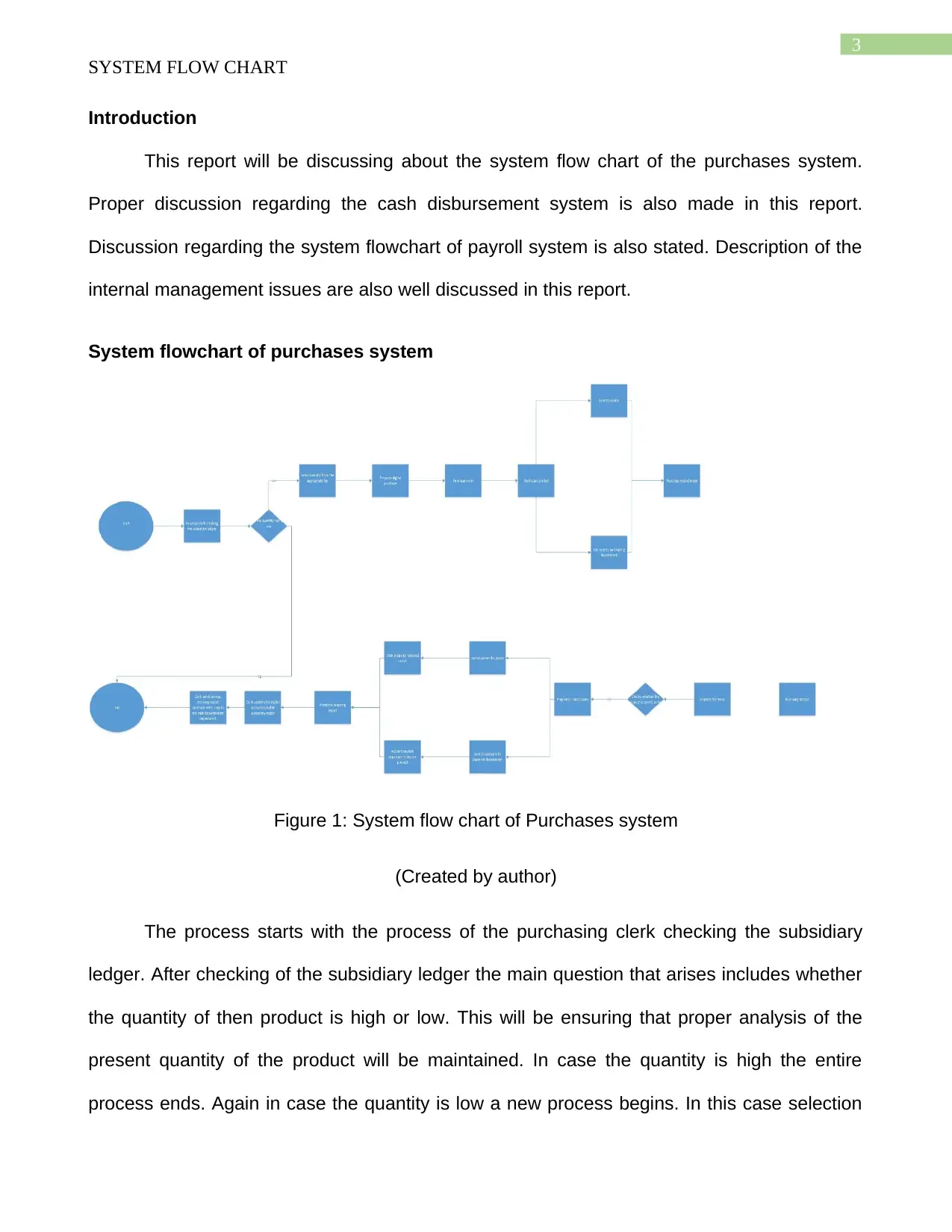

System flowchart of purchases system

Figure 1: System flow chart of Purchases system

(Created by author)

The process starts with the process of the purchasing clerk checking the subsidiary

ledger. After checking of the subsidiary ledger the main question that arises includes whether

the quantity of then product is high or low. This will be ensuring that proper analysis of the

present quantity of the product will be maintained. In case the quantity is high the entire

process ends. Again in case the quantity is low a new process begins. In this case selection

SYSTEM FLOW CHART

Introduction

This report will be discussing about the system flow chart of the purchases system.

Proper discussion regarding the cash disbursement system is also made in this report.

Discussion regarding the system flowchart of payroll system is also stated. Description of the

internal management issues are also well discussed in this report.

System flowchart of purchases system

Figure 1: System flow chart of Purchases system

(Created by author)

The process starts with the process of the purchasing clerk checking the subsidiary

ledger. After checking of the subsidiary ledger the main question that arises includes whether

the quantity of then product is high or low. This will be ensuring that proper analysis of the

present quantity of the product will be maintained. In case the quantity is high the entire

process ends. Again in case the quantity is low a new process begins. In this case selection

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

SYSTEM FLOW CHART

of the vendor from the catalogue. After performing proper selection of the vendor, digital

purchase process is prepared. This acts as a major step and hence wise order is placed after

this section. After this process 2 hard copies of the purchase order is printed. The 2 files are

sent to 2 different sections. One copy is sent to the vendor and the other copy is sent to the

purchasing department. After this process the purchase record is made.

After this stage the receiving stage starts. The first stage is bothered with the

inspection of the items. After inspection of the items, proper checking of the product is

performed. Whether the product that is chosen is correct or not is decided. If the answer is no

the phase shifts backwards and the process starts from the beginning. In case the product

that is selected is correct, preparation of 2 hard copies are made. In this case one hard copy

accompanies with the goods and the other copy is sent to the account department or the

payment department. For the hard copy that is sent with the goods, the clerk prepares a

received report after receiving the same. The stage in which another hard copy is sent to the

payment department, the account payable department files the product. After this stage

printing of the receiving report is performed. After this stage, the clerk updates the digital

account that is payable in the subsidiary ledger. After this section the clerk sends the invoice

to the receiving report and hence wise purchase order copy as per the cash disbursement

department is also done. After completion of all these steps the project ends.

SYSTEM FLOW CHART

of the vendor from the catalogue. After performing proper selection of the vendor, digital

purchase process is prepared. This acts as a major step and hence wise order is placed after

this section. After this process 2 hard copies of the purchase order is printed. The 2 files are

sent to 2 different sections. One copy is sent to the vendor and the other copy is sent to the

purchasing department. After this process the purchase record is made.

After this stage the receiving stage starts. The first stage is bothered with the

inspection of the items. After inspection of the items, proper checking of the product is

performed. Whether the product that is chosen is correct or not is decided. If the answer is no

the phase shifts backwards and the process starts from the beginning. In case the product

that is selected is correct, preparation of 2 hard copies are made. In this case one hard copy

accompanies with the goods and the other copy is sent to the account department or the

payment department. For the hard copy that is sent with the goods, the clerk prepares a

received report after receiving the same. The stage in which another hard copy is sent to the

payment department, the account payable department files the product. After this stage

printing of the receiving report is performed. After this stage, the clerk updates the digital

account that is payable in the subsidiary ledger. After this section the clerk sends the invoice

to the receiving report and hence wise purchase order copy as per the cash disbursement

department is also done. After completion of all these steps the project ends.

5

SYSTEM FLOW CHART

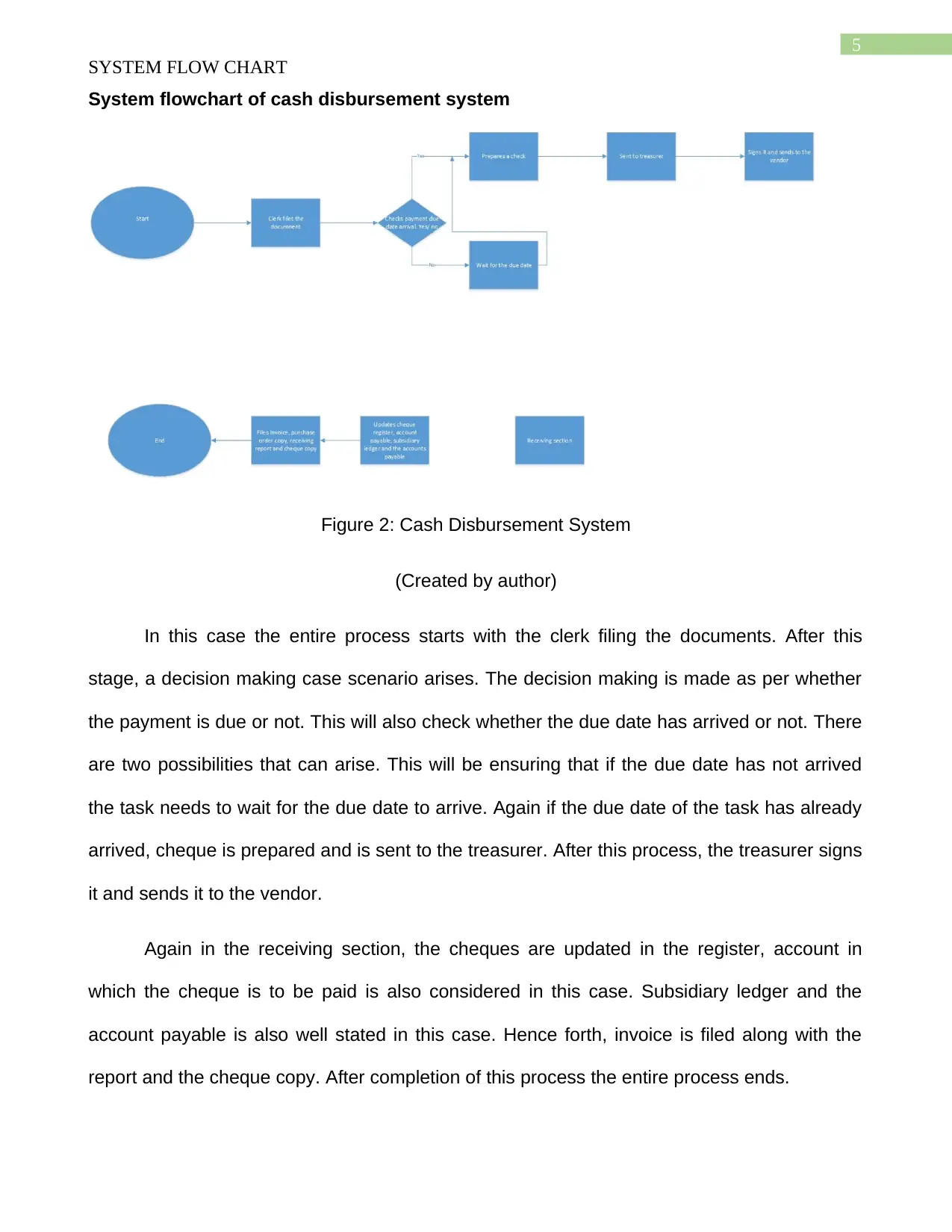

System flowchart of cash disbursement system

Figure 2: Cash Disbursement System

(Created by author)

In this case the entire process starts with the clerk filing the documents. After this

stage, a decision making case scenario arises. The decision making is made as per whether

the payment is due or not. This will also check whether the due date has arrived or not. There

are two possibilities that can arise. This will be ensuring that if the due date has not arrived

the task needs to wait for the due date to arrive. Again if the due date of the task has already

arrived, cheque is prepared and is sent to the treasurer. After this process, the treasurer signs

it and sends it to the vendor.

Again in the receiving section, the cheques are updated in the register, account in

which the cheque is to be paid is also considered in this case. Subsidiary ledger and the

account payable is also well stated in this case. Hence forth, invoice is filed along with the

report and the cheque copy. After completion of this process the entire process ends.

SYSTEM FLOW CHART

System flowchart of cash disbursement system

Figure 2: Cash Disbursement System

(Created by author)

In this case the entire process starts with the clerk filing the documents. After this

stage, a decision making case scenario arises. The decision making is made as per whether

the payment is due or not. This will also check whether the due date has arrived or not. There

are two possibilities that can arise. This will be ensuring that if the due date has not arrived

the task needs to wait for the due date to arrive. Again if the due date of the task has already

arrived, cheque is prepared and is sent to the treasurer. After this process, the treasurer signs

it and sends it to the vendor.

Again in the receiving section, the cheques are updated in the register, account in

which the cheque is to be paid is also considered in this case. Subsidiary ledger and the

account payable is also well stated in this case. Hence forth, invoice is filed along with the

report and the cheque copy. After completion of this process the entire process ends.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

SYSTEM FLOW CHART

System flowchart of payroll system

Figure 3: System flowchart of payroll system

(Author note)

The entire project starts with Adam & Co employees records the time card and the

work time on daily basis. After this process, the supervisor will be checking the time card and

the correctness of the entry. After checking the correctness of the data, the same is submitted

to the payroll.

There is a separate work function that will be going in in the payroll company. In this

process, the payroll checks the input of data in the very initial stage. The payroll clerk checks

the input of the data. After this section, the hard copy will be printed as well. After this

process, 2 copies of the payroll register is made. After making of 2 copies of payroll register,

the copies are sent to the digital employee record. After this section the payroll clerk collects

the files. After collecting the file, 2 copies of the employee pay cheques to various supervisors

are made. After this a decision making stage arises. In this case, if the data is collected, it

gets distributed to the respective department. Hence forth the entire process will be ensuring

that the payroll clerk sends the data and 2 copies are made. The 1st copy is sent to the

SYSTEM FLOW CHART

System flowchart of payroll system

Figure 3: System flowchart of payroll system

(Author note)

The entire project starts with Adam & Co employees records the time card and the

work time on daily basis. After this process, the supervisor will be checking the time card and

the correctness of the entry. After checking the correctness of the data, the same is submitted

to the payroll.

There is a separate work function that will be going in in the payroll company. In this

process, the payroll checks the input of data in the very initial stage. The payroll clerk checks

the input of the data. After this section, the hard copy will be printed as well. After this

process, 2 copies of the payroll register is made. After making of 2 copies of payroll register,

the copies are sent to the digital employee record. After this section the payroll clerk collects

the files. After collecting the file, 2 copies of the employee pay cheques to various supervisors

are made. After this a decision making stage arises. In this case, if the data is collected, it

gets distributed to the respective department. Hence forth the entire process will be ensuring

that the payroll clerk sends the data and 2 copies are made. The 1st copy is sent to the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

SYSTEM FLOW CHART

account payable department and the 2nd copy of the data is sent to the payroll department.

After this stage, the clerk posts general ledger and hence wise files voucher. After this phase

the task ends.

Description of internal control weakness in the following systems

In case of the purchases system, the main internal control weakness that was present

is that the clerk was excessively pressurized regarding the functional process. The entire

process was performed by him in manual manner. Analyzing of the quantity of the product left

and hence wise decision making process is performed manually in this case. The internal

management issues that might arise due to this problems include inaccuracy in decision

making and hence wise proper execution of the task might be at stake. Another major issue

that can be stated is that the transaction process is highly complex and in case of missing of a

single step might be creating a major problem in the project execution process. Again manual

interference is also very high, leading to increase in chances of mistakes.

In case of the cash disbursements system, the main issue that is present is that the clerk

checks if the due date has arrived or not. In this case, the main aspect that is considered is

that the clerk might be missing the due date and forget the due date, the entire process will be

lagging.

In case of the Payroll system, the main issue that is present is that there is manual

filling of the data. This manual filling of the data might be decreasing the accuracy of the

system. In case the data that are entered by the workers might be wrong. In case the data

that are provided are wrong in nature the entire functioning of the payroll system will be

getting wrong. Again the main issue in this case is that the entire process is performed

manually. This manual treatment will be reducing the accuracy of the system.

SYSTEM FLOW CHART

account payable department and the 2nd copy of the data is sent to the payroll department.

After this stage, the clerk posts general ledger and hence wise files voucher. After this phase

the task ends.

Description of internal control weakness in the following systems

In case of the purchases system, the main internal control weakness that was present

is that the clerk was excessively pressurized regarding the functional process. The entire

process was performed by him in manual manner. Analyzing of the quantity of the product left

and hence wise decision making process is performed manually in this case. The internal

management issues that might arise due to this problems include inaccuracy in decision

making and hence wise proper execution of the task might be at stake. Another major issue

that can be stated is that the transaction process is highly complex and in case of missing of a

single step might be creating a major problem in the project execution process. Again manual

interference is also very high, leading to increase in chances of mistakes.

In case of the cash disbursements system, the main issue that is present is that the clerk

checks if the due date has arrived or not. In this case, the main aspect that is considered is

that the clerk might be missing the due date and forget the due date, the entire process will be

lagging.

In case of the Payroll system, the main issue that is present is that there is manual

filling of the data. This manual filling of the data might be decreasing the accuracy of the

system. In case the data that are entered by the workers might be wrong. In case the data

that are provided are wrong in nature the entire functioning of the payroll system will be

getting wrong. Again the main issue in this case is that the entire process is performed

manually. This manual treatment will be reducing the accuracy of the system.

8

SYSTEM FLOW CHART

Risks associated with the above system

The major risks associated with the above scenarios are as follows: -

The time that will be taken for completion of the stated case will be very high

The complexity in the functioning process is high as well.

Accuracy of the functional process can also be questioned at times.

Recommendation for the above problem

The best way to mitigate these issues is by implementing Accounting information system.

There are 2 major types of Accounting Information System. The types includes the

likes of Manual Account Information System and Legacy Account Information System.

Manual accounting system is mainly concerned with the small businesses. These

businesses includes the fact that gathering of source data along with general ledger

and general journal is performed. This leads to the fact that better assessment of the

subsidiary journals are also included. This is the main reason that this type of Account

Information system is generally used in the small scale businesses. In case of the

manual account information system, the main aspect that is considered is that the

transactions are properly maintained (Schaltegger and Burritt 2017). This leads to the

fact that proper assessment of the error rate can also be provided. This is the main

reason that manual rolled up system is well provided as the journals and the

transaction process gets performed in a proper manner. This is the main reason that

the financial statements are provided. This provisioning of the financial statement will

ensure that reduction in error rate can be performed. But the major issue that is seen in

this case is that despite reduction in the errors in the financial statement, there are

errors present in the functional process. The speed of functioning is also much slower

SYSTEM FLOW CHART

Risks associated with the above system

The major risks associated with the above scenarios are as follows: -

The time that will be taken for completion of the stated case will be very high

The complexity in the functioning process is high as well.

Accuracy of the functional process can also be questioned at times.

Recommendation for the above problem

The best way to mitigate these issues is by implementing Accounting information system.

There are 2 major types of Accounting Information System. The types includes the

likes of Manual Account Information System and Legacy Account Information System.

Manual accounting system is mainly concerned with the small businesses. These

businesses includes the fact that gathering of source data along with general ledger

and general journal is performed. This leads to the fact that better assessment of the

subsidiary journals are also included. This is the main reason that this type of Account

Information system is generally used in the small scale businesses. In case of the

manual account information system, the main aspect that is considered is that the

transactions are properly maintained (Schaltegger and Burritt 2017). This leads to the

fact that proper assessment of the error rate can also be provided. This is the main

reason that manual rolled up system is well provided as the journals and the

transaction process gets performed in a proper manner. This is the main reason that

the financial statements are provided. This provisioning of the financial statement will

ensure that reduction in error rate can be performed. But the major issue that is seen in

this case is that despite reduction in the errors in the financial statement, there are

errors present in the functional process. The speed of functioning is also much slower

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

SYSTEM FLOW CHART

than the expected rate (Susanto 2016). This leads to the fact that usage of this

technology has not been very high.

Usage of the legacy system accounting information system will also be beneficial in

nature. These are the systems that are in use by the existing business organization.

These information system was mainly focused with old fashioned accounting

information system (Alewine, Allport and Shen 2016). It has been seen that the legacy

accounting information system has the potentiality of constant evolvement as per the

requirement of the business and hence wise customization gets easier. The major

disadvantage that this process has is that no proper documentation is present in the

system.

There is a proper replacement of legacy system. This system is mainly concerned with

removing the legacy system and updating the same with the up to date system. In this

case the major aspect that is considered is performing screen scraping ( Collier 2015).

Despite the fact that this system is highly expensive in nature, this alteration can be

made at any point of time. With the help of screen scraping the major advantage that

will be enjoyed is that the data that is displayed on the screen gets translated in a form

that the newer application reads it. Setting up of the enterprise application is also an

important act of the replacement of legacy system (Libby 2017). Activities namely

inventory and payroll will also be acting as the major advantage of implementing these

technique.

The benefits that will be enjoyed after implementation of the accounting information system

are as follows: -

Accounting Information system is a computerized accounting program that takes into

consideration the need of records handling and transaction process. The information

SYSTEM FLOW CHART

than the expected rate (Susanto 2016). This leads to the fact that usage of this

technology has not been very high.

Usage of the legacy system accounting information system will also be beneficial in

nature. These are the systems that are in use by the existing business organization.

These information system was mainly focused with old fashioned accounting

information system (Alewine, Allport and Shen 2016). It has been seen that the legacy

accounting information system has the potentiality of constant evolvement as per the

requirement of the business and hence wise customization gets easier. The major

disadvantage that this process has is that no proper documentation is present in the

system.

There is a proper replacement of legacy system. This system is mainly concerned with

removing the legacy system and updating the same with the up to date system. In this

case the major aspect that is considered is performing screen scraping ( Collier 2015).

Despite the fact that this system is highly expensive in nature, this alteration can be

made at any point of time. With the help of screen scraping the major advantage that

will be enjoyed is that the data that is displayed on the screen gets translated in a form

that the newer application reads it. Setting up of the enterprise application is also an

important act of the replacement of legacy system (Libby 2017). Activities namely

inventory and payroll will also be acting as the major advantage of implementing these

technique.

The benefits that will be enjoyed after implementation of the accounting information system

are as follows: -

Accounting Information system is a computerized accounting program that takes into

consideration the need of records handling and transaction process. The information

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

SYSTEM FLOW CHART

that are entered in the system are structured by the account information system. These

technology can be used for performing proper detailed information about the financial

statements and the financial transaction. There are few sections that gets benefitted in

the functional process. The sectors include Business Transactions, Account Payable,

Account Receivable, Financial statements and provide proper analysis of data

regarding the Year End Closing (Budiarto et al, 2018).

It is considered that Accounting Information System provides its maximum utility in the

business transaction section. The Accounting information system is mainly concerned

with the record all the data that are being transacted. This insists the fact that the data

that are entered in the system stays in the system and can be re used. The transaction

process also performs in a manner that the sectioning of the data that are collected are

done (Susanto 2015). This ensures that structuring of the data gets easier.

Transactions are hence wise posted in the respective departments correspondingly.

Proper gathering of the accounting information system is also provided. This ensures

that the payment process gets easier. This ensures that proper assessment of the

business management regarding account related data are made. Another benefit that

is received is that the data regarding the accounting details are provided in a precise

manner and hence wise gaining access to the data as per the entry date gets easier

and this increases the efficiency of the entire process.

Proper allocation of the accounts payable is also well stated. This process also helps in

proper generation of the bills and hence wise proper allocation of bills is also

performed. Generation of bills gets easier and hence wise the entire functioning

process of the clerk. This will be increasing the efficiency of the entire project ( Prasad

and Green 2015).

SYSTEM FLOW CHART

that are entered in the system are structured by the account information system. These

technology can be used for performing proper detailed information about the financial

statements and the financial transaction. There are few sections that gets benefitted in

the functional process. The sectors include Business Transactions, Account Payable,

Account Receivable, Financial statements and provide proper analysis of data

regarding the Year End Closing (Budiarto et al, 2018).

It is considered that Accounting Information System provides its maximum utility in the

business transaction section. The Accounting information system is mainly concerned

with the record all the data that are being transacted. This insists the fact that the data

that are entered in the system stays in the system and can be re used. The transaction

process also performs in a manner that the sectioning of the data that are collected are

done (Susanto 2015). This ensures that structuring of the data gets easier.

Transactions are hence wise posted in the respective departments correspondingly.

Proper gathering of the accounting information system is also provided. This ensures

that the payment process gets easier. This ensures that proper assessment of the

business management regarding account related data are made. Another benefit that

is received is that the data regarding the accounting details are provided in a precise

manner and hence wise gaining access to the data as per the entry date gets easier

and this increases the efficiency of the entire process.

Proper allocation of the accounts payable is also well stated. This process also helps in

proper generation of the bills and hence wise proper allocation of bills is also

performed. Generation of bills gets easier and hence wise the entire functioning

process of the clerk. This will be increasing the efficiency of the entire project ( Prasad

and Green 2015).

11

SYSTEM FLOW CHART

Creation of financial statements is also another benefit that is performed by the

Accounting information system. In this case the dates are entered in the system and

the entire data sets that are present are provided. The system has the capability of

producing reports regarding the client. This will also provide data regarding the data of

different periods. This is the main reason that gaining annual data gets easier and the

accuracy of the data transacted gets higher.

Conclusion

From the above discussion it can be stated that the accounting information system is

one of the major technology that can be implemented for mitigation of the issues that are

detected in the process. With proper implementation of the accounting information system

issues that might arise due to complexity in framework can be mitigated as well.

SYSTEM FLOW CHART

Creation of financial statements is also another benefit that is performed by the

Accounting information system. In this case the dates are entered in the system and

the entire data sets that are present are provided. The system has the capability of

producing reports regarding the client. This will also provide data regarding the data of

different periods. This is the main reason that gaining annual data gets easier and the

accuracy of the data transacted gets higher.

Conclusion

From the above discussion it can be stated that the accounting information system is

one of the major technology that can be implemented for mitigation of the issues that are

detected in the process. With proper implementation of the accounting information system

issues that might arise due to complexity in framework can be mitigated as well.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.