The Effect of Tax Avoidance on Firm Risk in the UK

19 Pages5289 Words50 Views

Added on 2023-06-07

About This Document

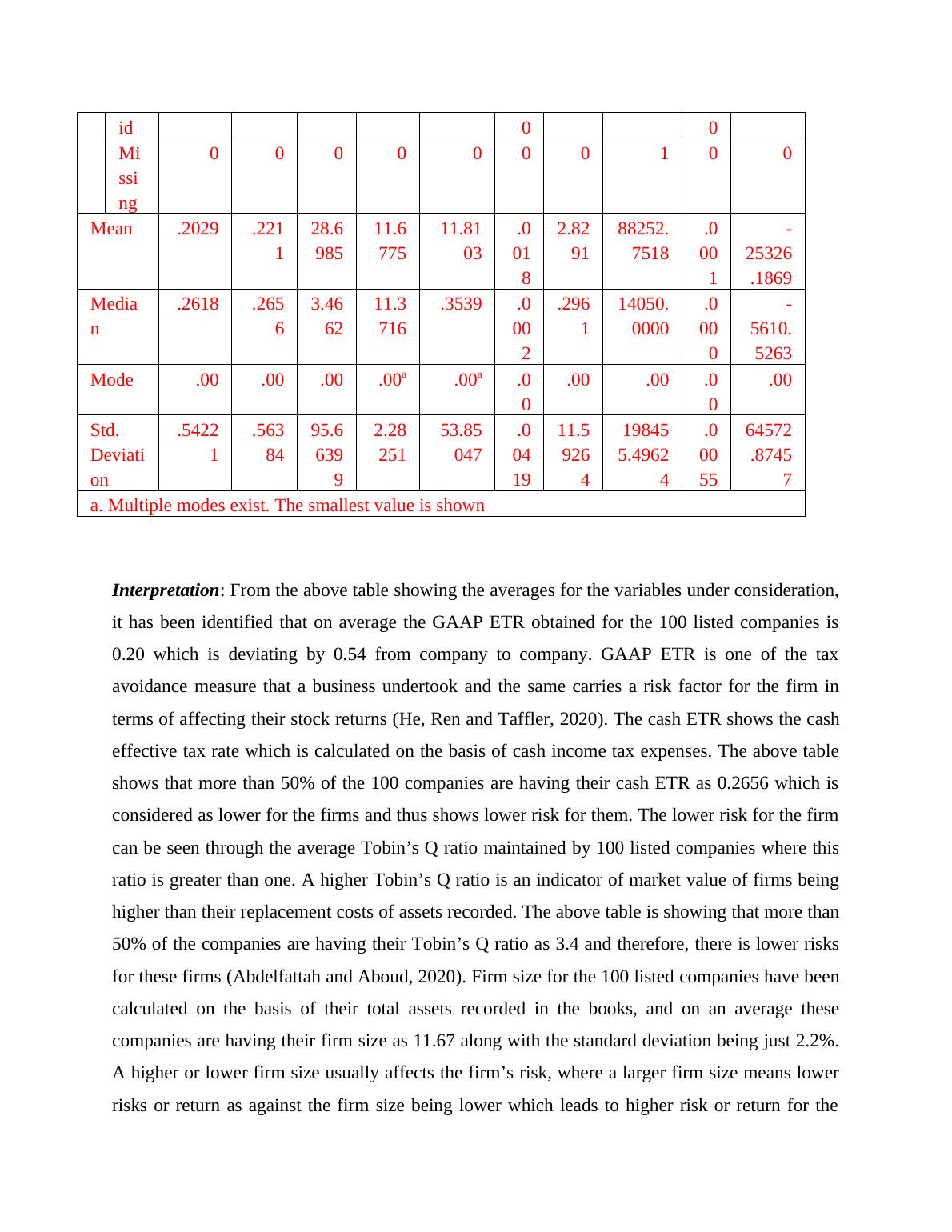

This study analyzes the impact of tax avoidance on firm risk in the UK through statistical analysis of data from 100 listed companies. The findings reveal correlations between GAAP ETR, Cash ETR, BTD, Tobin’s Q ratio, firm size, fixed assets, ROA, Debt, Leverage and NOL. Descriptive statistics, correlation, regression, ANOVA test and frequencies have been used to determine the degree of relationship among the variables of interest. The study concludes that tax avoidance measures such as GAAP ETR and BTD carry a risk factor for the firm in terms of affecting their stock returns.

The Effect of Tax Avoidance on Firm Risk in the UK

Added on 2023-06-07

ShareRelated Documents

End of preview

Want to access all the pages? Upload your documents or become a member.

SPSS Data Collection - Assignment

|11

|1734

|19

Regression Analysis in SPSS

|16

|1866

|25

Steps to Perform Regression Analysis

|4

|717

|426

Statistical Analysis of Room Prices in UK Hotels

|7

|530

|140

Analytical Methods for Monthly Prices of Index and Stock

|8

|660

|98

Statistics | ANOVA | Assignment

|11

|724

|26