Fringe Benefits Tax and Shine Homes

VerifiedAdded on 2020/03/23

|9

|1661

|41

AI Summary

This assignment delves into the complexities of Fringe Benefits Tax (FBT) as applied to Shine Homes Pty Ltd. It examines a scenario where the company provides various benefits to their employee, Charlie, including car parking, honeymoon accommodation, and car hire costs. The analysis explores whether these benefits constitute FBT liabilities for Shine Homes and tax implications for Charlie. It references relevant Australian legislation like the Fringe Benefit Tax Act 1986 and Income Tax Assessment Act 1936 to provide a comprehensive understanding of the FBT obligations in this case.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAXATION

Taxation

Name of Student:

Name of University:

Author’s Note:

Taxation

Name of Student:

Name of University:

Author’s Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1TAXATION

Table of Contents

Issue:................................................................................................................................................2

Laws:................................................................................................................................................2

Application:.....................................................................................................................................2

Conclusion:......................................................................................................................................7

Reference List:.................................................................................................................................8

Table of Contents

Issue:................................................................................................................................................2

Laws:................................................................................................................................................2

Application:.....................................................................................................................................2

Conclusion:......................................................................................................................................7

Reference List:.................................................................................................................................8

2TAXATION

Issue:

The given case study shows that Charlie worked as the agent of the real estate for Shine

Homes Private Limited. He was given a sedan. The issue at present is dependent on the

determination of the fringe benefit consequences of Charlie and Shine Homes. Based on the

Section 6 of the Miscellaneous Taxation Rulings and Fringe Benefit Tax Assessment Act 1986

there are some cases in which the tax on fringe benefits is levied on the cars (Barkoczy, 2016).

Laws:

a. Section 6 of the Miscellaneous Taxation Rulings

b. Fringe Benefit Tax Assessment Act 1986

c. taxation rulings of MT 2027

d. sub-section 136 (1) of the Miscellaneous Taxation Rulings of 2027

e. section 51 of the Income Tax Assessment Act 1997

f. Lunney and Hayley v FCT (1958)

g. Newsom v Robertson (1952) 2 All ER 728; (1952)

h. Simon in Taylor v Provan (1975) AC 194

i. Tubemakers of Australia Ltd v. FC of T 93

Application:

The paragraph 3 of the Miscellaneous Taxation Ruling states that details of any type of

the business utilities of cars need to be incorporated in the log book or any sort of file due to the

business kilometres which have been travelled using the operating cost method. Any kind of

utility made by the employees which is not entirely connected to the course of producing taxable

Issue:

The given case study shows that Charlie worked as the agent of the real estate for Shine

Homes Private Limited. He was given a sedan. The issue at present is dependent on the

determination of the fringe benefit consequences of Charlie and Shine Homes. Based on the

Section 6 of the Miscellaneous Taxation Rulings and Fringe Benefit Tax Assessment Act 1986

there are some cases in which the tax on fringe benefits is levied on the cars (Barkoczy, 2016).

Laws:

a. Section 6 of the Miscellaneous Taxation Rulings

b. Fringe Benefit Tax Assessment Act 1986

c. taxation rulings of MT 2027

d. sub-section 136 (1) of the Miscellaneous Taxation Rulings of 2027

e. section 51 of the Income Tax Assessment Act 1997

f. Lunney and Hayley v FCT (1958)

g. Newsom v Robertson (1952) 2 All ER 728; (1952)

h. Simon in Taylor v Provan (1975) AC 194

i. Tubemakers of Australia Ltd v. FC of T 93

Application:

The paragraph 3 of the Miscellaneous Taxation Ruling states that details of any type of

the business utilities of cars need to be incorporated in the log book or any sort of file due to the

business kilometres which have been travelled using the operating cost method. Any kind of

utility made by the employees which is not entirely connected to the course of producing taxable

3TAXATION

income by that employee can be considered as personal use according to the taxation rulings of

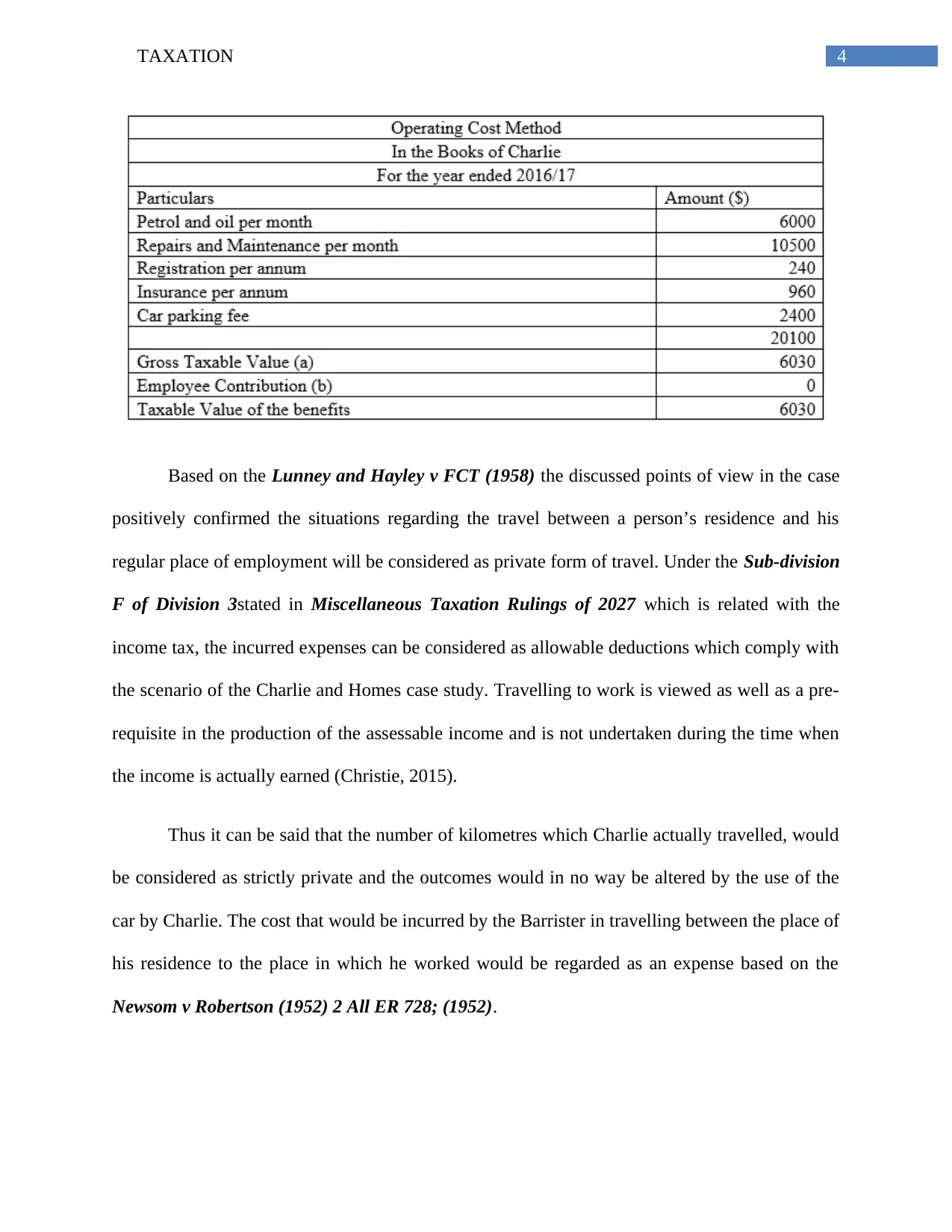

MT 2027 with reference to sub-section 136 (1). The given case study clearly shows that the car

was used by Charlie for functions related to work for 50 kilometres distance. In order to

determine the fringe benefits of the cars which were used by Charlie, the operational cost

valuation will be used in agreement with the sub-section 136 (1) of the Miscellaneous Taxation

Rulings of 2027.

The significant question is whether the car was utilised by the employee or the associate

wanted to exclusively attain the assessable income of the employee. Based on the rules, the

private as well as the business uses of the cars need to be determined. Depending on the sub

section 136 (1) it can clearly be stated that the use of the car by the employee which was

provided by his employer and used during the course of employment for the employment activity

purpose might be considered as the business use of the car for the Fringe benefit Tax. Hence the

levying of the tax is applicable (Woellner et al., 2016).

That Charlie has used the car is representative of the business use in relation to the

generation of the income of the employee which is taxable and is bound to result in Fringe

Benefit Tax. It is clearly seen from the case study that, the car was used by Charlie during his

tenure as an employee of Homes Pty Ltd and this was due to business purposes (Saad, 2014).

In ascertaining whether the car expenses can be allowable to be deducted under the

section 51 of the Income Tax Assessment Act 1997, certain facts have been obtained from the

case study that can be regarded as the allowable deductions for the purpose of the Income tax.

income by that employee can be considered as personal use according to the taxation rulings of

MT 2027 with reference to sub-section 136 (1). The given case study clearly shows that the car

was used by Charlie for functions related to work for 50 kilometres distance. In order to

determine the fringe benefits of the cars which were used by Charlie, the operational cost

valuation will be used in agreement with the sub-section 136 (1) of the Miscellaneous Taxation

Rulings of 2027.

The significant question is whether the car was utilised by the employee or the associate

wanted to exclusively attain the assessable income of the employee. Based on the rules, the

private as well as the business uses of the cars need to be determined. Depending on the sub

section 136 (1) it can clearly be stated that the use of the car by the employee which was

provided by his employer and used during the course of employment for the employment activity

purpose might be considered as the business use of the car for the Fringe benefit Tax. Hence the

levying of the tax is applicable (Woellner et al., 2016).

That Charlie has used the car is representative of the business use in relation to the

generation of the income of the employee which is taxable and is bound to result in Fringe

Benefit Tax. It is clearly seen from the case study that, the car was used by Charlie during his

tenure as an employee of Homes Pty Ltd and this was due to business purposes (Saad, 2014).

In ascertaining whether the car expenses can be allowable to be deducted under the

section 51 of the Income Tax Assessment Act 1997, certain facts have been obtained from the

case study that can be regarded as the allowable deductions for the purpose of the Income tax.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4TAXATION

Based on the Lunney and Hayley v FCT (1958) the discussed points of view in the case

positively confirmed the situations regarding the travel between a person’s residence and his

regular place of employment will be considered as private form of travel. Under the Sub-division

F of Division 3stated in Miscellaneous Taxation Rulings of 2027 which is related with the

income tax, the incurred expenses can be considered as allowable deductions which comply with

the scenario of the Charlie and Homes case study. Travelling to work is viewed as well as a pre-

requisite in the production of the assessable income and is not undertaken during the time when

the income is actually earned (Christie, 2015).

Thus it can be said that the number of kilometres which Charlie actually travelled, would

be considered as strictly private and the outcomes would in no way be altered by the use of the

car by Charlie. The cost that would be incurred by the Barrister in travelling between the place of

his residence to the place in which he worked would be regarded as an expense based on the

Newsom v Robertson (1952) 2 All ER 728; (1952).

Based on the Lunney and Hayley v FCT (1958) the discussed points of view in the case

positively confirmed the situations regarding the travel between a person’s residence and his

regular place of employment will be considered as private form of travel. Under the Sub-division

F of Division 3stated in Miscellaneous Taxation Rulings of 2027 which is related with the

income tax, the incurred expenses can be considered as allowable deductions which comply with

the scenario of the Charlie and Homes case study. Travelling to work is viewed as well as a pre-

requisite in the production of the assessable income and is not undertaken during the time when

the income is actually earned (Christie, 2015).

Thus it can be said that the number of kilometres which Charlie actually travelled, would

be considered as strictly private and the outcomes would in no way be altered by the use of the

car by Charlie. The cost that would be incurred by the Barrister in travelling between the place of

his residence to the place in which he worked would be regarded as an expense based on the

Newsom v Robertson (1952) 2 All ER 728; (1952).

5TAXATION

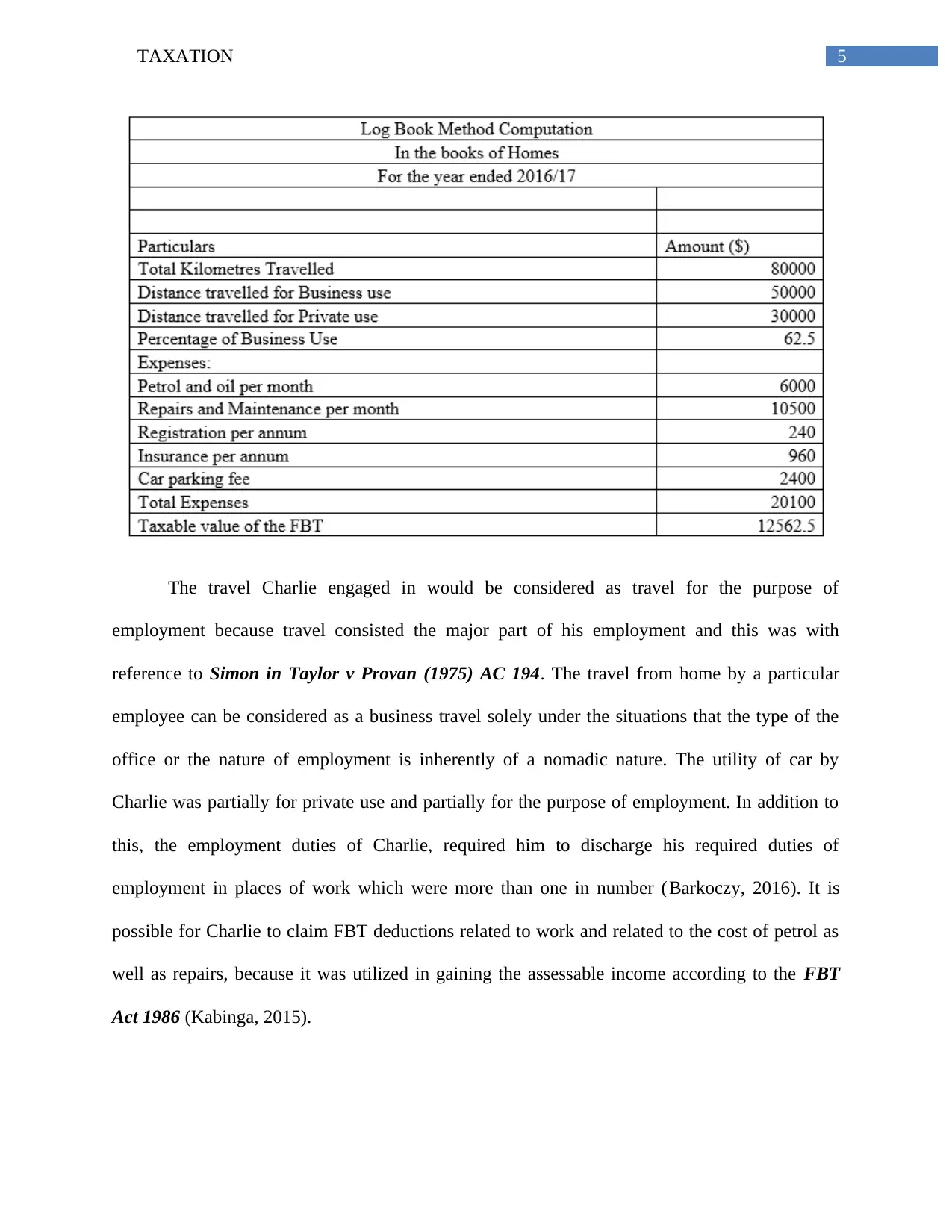

The travel Charlie engaged in would be considered as travel for the purpose of

employment because travel consisted the major part of his employment and this was with

reference to Simon in Taylor v Provan (1975) AC 194. The travel from home by a particular

employee can be considered as a business travel solely under the situations that the type of the

office or the nature of employment is inherently of a nomadic nature. The utility of car by

Charlie was partially for private use and partially for the purpose of employment. In addition to

this, the employment duties of Charlie, required him to discharge his required duties of

employment in places of work which were more than one in number (Barkoczy, 2016). It is

possible for Charlie to claim FBT deductions related to work and related to the cost of petrol as

well as repairs, because it was utilized in gaining the assessable income according to the FBT

Act 1986 (Kabinga, 2015).

The travel Charlie engaged in would be considered as travel for the purpose of

employment because travel consisted the major part of his employment and this was with

reference to Simon in Taylor v Provan (1975) AC 194. The travel from home by a particular

employee can be considered as a business travel solely under the situations that the type of the

office or the nature of employment is inherently of a nomadic nature. The utility of car by

Charlie was partially for private use and partially for the purpose of employment. In addition to

this, the employment duties of Charlie, required him to discharge his required duties of

employment in places of work which were more than one in number (Barkoczy, 2016). It is

possible for Charlie to claim FBT deductions related to work and related to the cost of petrol as

well as repairs, because it was utilized in gaining the assessable income according to the FBT

Act 1986 (Kabinga, 2015).

6TAXATION

There is the possibility of a car parking Fringe Benefit arising in case the employer

provides the employee with the car parking facility and the listed criteria below are met:

a. The car has been parked for more than four hours

b. The employee controls or hires the car

c. The car is provided for the discharge of the employment duties

d. There is the existence of a commercial parking space which charges fees for the car that

is parked for the whole day within a one kilometre range.

e. The employee utilizes the car for travelling purposes from work to home or from home to

work for least once in a day.

From the case study it is observed that Charlie parked the car in his self controlled

garage. He basically parked the car in a secure place for which the employer paid him $200

every week. The car was used by Charlie for the purpose of travelling between the place of

his employment and his home every day. Thus this results in the fringe benefits for Charlie

and Homes can also claim the deductions for the parking fees on behalf of the employee on

the other hand (Miller & Oats, 2016).

Based on the Fringe Benefit Tax Act 1986, resulting in the tax liability it can be clearly

said from the case study that the Shine Homes Pty Ltd provided Charlie with the honeymoon

accommodation as it was falling within the said act. It is quite evident that the Shine Homes

paid the cost of the accommodations which they claim as the allowable deductions. Charlie

however, shall be under the obligation of declaring the nature of these types of allowance in

the income tax return.

There is the possibility of a car parking Fringe Benefit arising in case the employer

provides the employee with the car parking facility and the listed criteria below are met:

a. The car has been parked for more than four hours

b. The employee controls or hires the car

c. The car is provided for the discharge of the employment duties

d. There is the existence of a commercial parking space which charges fees for the car that

is parked for the whole day within a one kilometre range.

e. The employee utilizes the car for travelling purposes from work to home or from home to

work for least once in a day.

From the case study it is observed that Charlie parked the car in his self controlled

garage. He basically parked the car in a secure place for which the employer paid him $200

every week. The car was used by Charlie for the purpose of travelling between the place of

his employment and his home every day. Thus this results in the fringe benefits for Charlie

and Homes can also claim the deductions for the parking fees on behalf of the employee on

the other hand (Miller & Oats, 2016).

Based on the Fringe Benefit Tax Act 1986, resulting in the tax liability it can be clearly

said from the case study that the Shine Homes Pty Ltd provided Charlie with the honeymoon

accommodation as it was falling within the said act. It is quite evident that the Shine Homes

paid the cost of the accommodations which they claim as the allowable deductions. Charlie

however, shall be under the obligation of declaring the nature of these types of allowance in

the income tax return.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION

The liability concerned with the Fringe Benefit Tax for the Shine Homes comes under the

legislation of the Commonwealth. In order to claim benefit for the taxpayers who are actually

employees the Subsection 51 (1) of the Income Tax Assessment Act 1936 is applied. Based on

Tubemakers of Australia Ltd v. FC of T 93 the FBT includes that particular sum which occurs

in the ordinary case that reflects the amount of value which is allocated to the several FBTs. This

are given by the Shine Homes to the employee Charlie. According to the case study, the Shines

homes had incurred numerous FBT expenditures in the form of car hire cost, parking fees,

honeymoon accommodation and so on. The expenses incurred by the Shine Homes in gaining

the assessable income would be regarded as deductable expenditure based on the subsection 51

(1) of the ITAA 1997.

Conclusion:

Conclusively it can be stated that the fringe benefit expenditures will be considered for

tax purposes under the FBT Act 1986. The particular study considers the different aspects of

fringe benefit tax incurred in respect of the Charlie and Homes Pty Ltd. The car used by Charlie

will be regarded as use of business in gaining the income that is taxable which attracts the FBT.

The liability concerned with the Fringe Benefit Tax for the Shine Homes comes under the

legislation of the Commonwealth. In order to claim benefit for the taxpayers who are actually

employees the Subsection 51 (1) of the Income Tax Assessment Act 1936 is applied. Based on

Tubemakers of Australia Ltd v. FC of T 93 the FBT includes that particular sum which occurs

in the ordinary case that reflects the amount of value which is allocated to the several FBTs. This

are given by the Shine Homes to the employee Charlie. According to the case study, the Shines

homes had incurred numerous FBT expenditures in the form of car hire cost, parking fees,

honeymoon accommodation and so on. The expenses incurred by the Shine Homes in gaining

the assessable income would be regarded as deductable expenditure based on the subsection 51

(1) of the ITAA 1997.

Conclusion:

Conclusively it can be stated that the fringe benefit expenditures will be considered for

tax purposes under the FBT Act 1986. The particular study considers the different aspects of

fringe benefit tax incurred in respect of the Charlie and Homes Pty Ltd. The car used by Charlie

will be regarded as use of business in gaining the income that is taxable which attracts the FBT.

8TAXATION

Reference List:

Barkoczy, S. (2016). Foundations of Taxation Law 2016. OUP Catalogue.

Christie, M. (2015). Principles of Taxation Law 2015.

Kabinga, M. (2015). Established principles of taxation. Tax justice & poverty.

Miller, A., & Oats, L. (2016). Principles of international taxation. Bloomsbury Publishing.

Saad, N. (2014). Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, 1069-1075.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C., & Pinto, D. (2016). Australian Taxation Law

2016. OUP Catalogue.

Reference List:

Barkoczy, S. (2016). Foundations of Taxation Law 2016. OUP Catalogue.

Christie, M. (2015). Principles of Taxation Law 2015.

Kabinga, M. (2015). Established principles of taxation. Tax justice & poverty.

Miller, A., & Oats, L. (2016). Principles of international taxation. Bloomsbury Publishing.

Saad, N. (2014). Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, 1069-1075.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C., & Pinto, D. (2016). Australian Taxation Law

2016. OUP Catalogue.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.