Taxation: Ruby Pty Ltd - Expense Deductibility and CGT Implications

VerifiedAdded on 2023/06/04

|6

|1558

|168

Homework Assignment

AI Summary

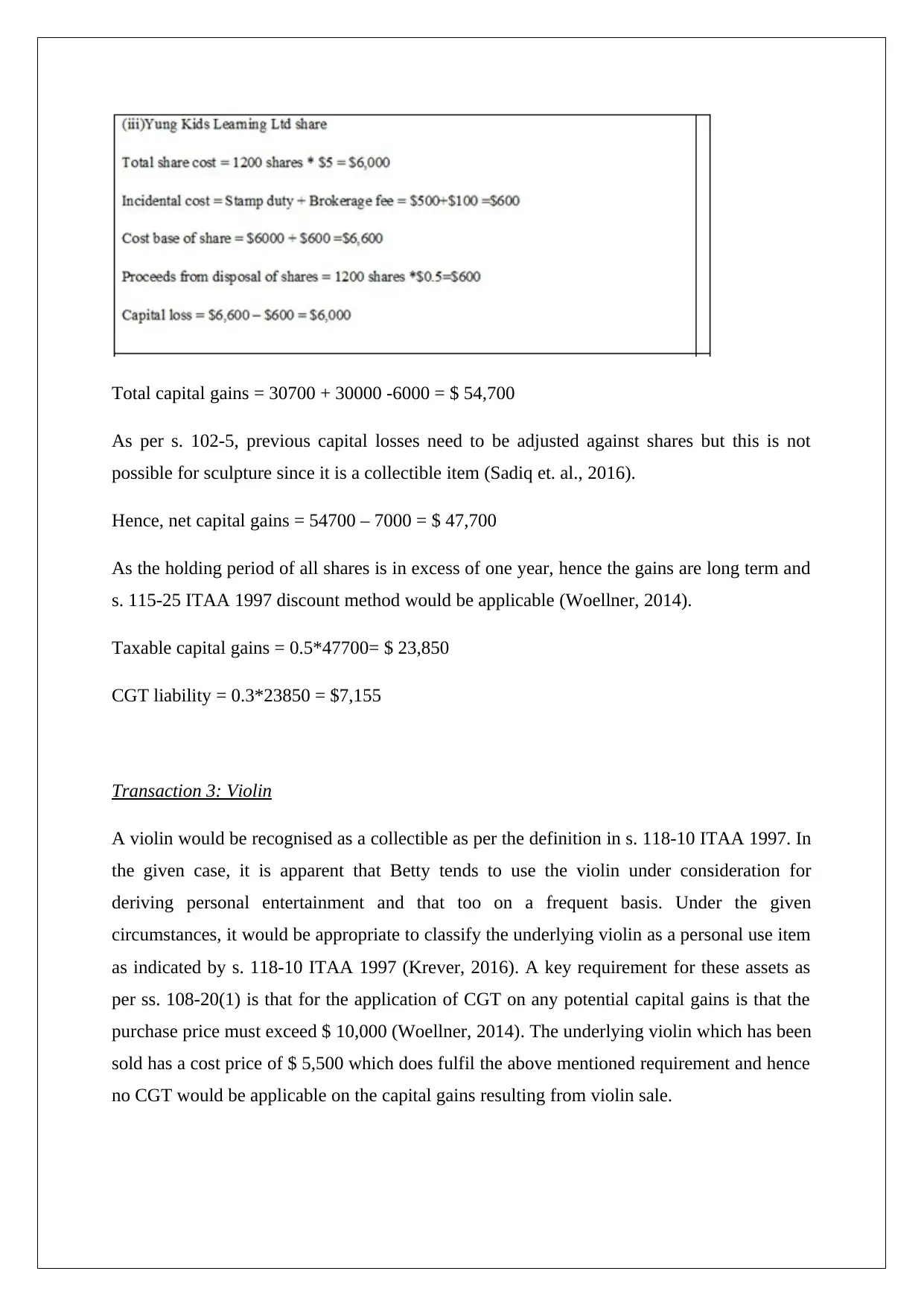

This assignment provides a detailed analysis of the tax deductibility of various transactions for Ruby Pty Ltd, focusing on expenses related to kitchen fitting replacements, legal expenses, and claims. It references relevant sections of the ITAA 1997 and tax rulings to determine whether these expenses are capital or revenue in nature, impacting their deductibility. The assignment also examines the CGT implications for Betty, an individual taxpayer, concerning the sale of a painting, shares, and a violin. It considers pre-CGT assets, A1 CGT events, cost base calculations, and the treatment of collectibles and personal use items under taxation law, providing a comprehensive overview of the tax consequences for each transaction. Desklib offers a range of solved assignments and study tools for students.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.