Tax Deductibility Analysis: Ruby Pty Ltd Taxation Assignment

VerifiedAdded on 2023/06/03

|7

|1510

|205

Homework Assignment

AI Summary

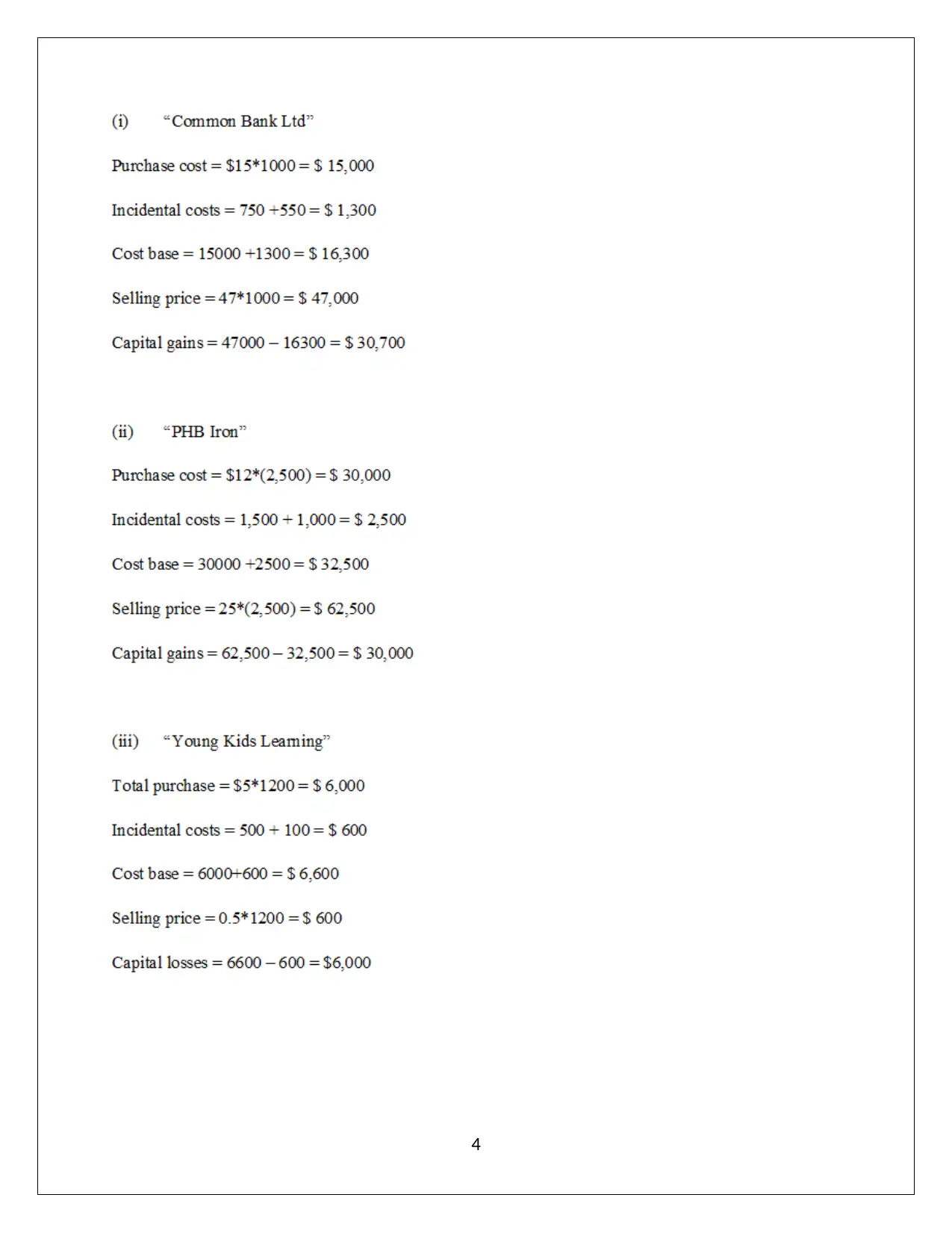

This assignment solution addresses the tax deductibility of expenses incurred by Ruby Pty Ltd. It analyzes the deductibility of expenses related to the replacement of kitchen fittings, considering whether the expenditure constitutes repairs or capital improvements. The solution references relevant tax legislation, including sections 8-1 and 25-10 of the ITAA 1997, and case law such as TR 97/23. The assignment also examines the deductibility of legal expenses incurred due to a visitor's injury, differentiating between revenue and capital expenditure based on the advantage derived from the expense. Furthermore, the solution covers the capital gains tax (CGT) implications for Betty, an investor and collector, analyzing the disposal of shares, a painting (pre-CGT asset), and a violin (collectible), considering relevant sections of the ITAA 1997, including s. 149(10), s. 104(5), s. 110-25(1), s. 115-25, and s. 118(10) to determine the CGT liability. The solution concludes that no CGT implications would be raised on taxpayer on the account of selling of the violin.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.