Taxation Law Assignment: Deductions, Capital Gains Tax, and Cases

VerifiedAdded on 2023/06/03

|10

|2240

|138

Homework Assignment

AI Summary

This taxation law assignment addresses two main questions. Question 1 examines the deductibility of expenses incurred by Ruby Engineering Pty Ltd, including repair costs for a rental property, legal expenses from a visitor's injury, and compensation paid due to defective parts. It analyzes these expenses under the Income Tax Assessment Act 1997 (ITAA 1997) and relevant case law. Question 2 delves into capital gains tax (CGT), discussing the treatment of pre-CGT assets (a painting), shares, and personal use assets (a violin). It includes calculations for capital gains and losses from share transactions and provides a detailed analysis of the CGT implications, referencing the relevant sections of the ITAA 1997, such as sections 108-5, 104-10(1), 118-10 (3), and 26-5. The assignment provides detailed answers and calculations, along with a list of references to support the analysis.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to A:..........................................................................................................................2

Answer to B:..........................................................................................................................2

Answer to C:..........................................................................................................................3

Answer to question 2:.................................................................................................................4

Answer to A:..........................................................................................................................4

Answer to B:..........................................................................................................................5

Answer to C:..........................................................................................................................5

References..................................................................................................................................8

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to A:..........................................................................................................................2

Answer to B:..........................................................................................................................2

Answer to C:..........................................................................................................................3

Answer to question 2:.................................................................................................................4

Answer to A:..........................................................................................................................4

Answer to B:..........................................................................................................................5

Answer to C:..........................................................................................................................5

References..................................................................................................................................8

2TAXATION LAW

Answer to question 1:

Answer to A:

The “taxation ruling of TR 97/23” clarifies the conditions where the outgoings

associated to repairs is treated as the permissible deductions under “section 25-10 of the

ITAA 1997”. In context of “section 25-10” repairs are denoted as work performed on the

premises to remedy the defects, damage or deterioration that contemplates the continuous

presence of property (Barkoczy, 2014). Repairs for majority of part is partial or occasional.

Works can be fairly termed as repair if it carried out to make the deterioration good arisen by

wear and tear, by accidental or deliberate damage or due to the natural causes. The judicial

decision made in “BP Oil Refinary Ltd v FC of T (1992)” stated that the work would not be

treated as repair until it comprises restoration of something that is damaged or lost whether

function or substances or certain other characteristics or quality (Grange et al., 2014).

Ruby Engineering Pty Ltd held the rental property since 2008. The company replaced

the kitchen fittings and cupboard that was deteriorated by wear and tear. The company

replaced the cupboard with the similar type without causing any substantial change. In

context of the “section 25-10 of the ITAA 1997”, the repairs expense of $8,500 performed by

company on the kitchen will quality for deduction since the work was performed to remedy

the defects caused by wear and tear in order to contemplate the continuous presence of

property (James, 2015). The works can be fairly termed as repair which was carried out to

make the deterioration good arisen by wear and tear.

Answer to B:

As per “section 8-1 of the ITAA 1997” the taxpayer is permitted to obtain the

deduction for the legal outgoings that is occurred in defending the damages claims in context

of the injuries that is allegedly sustained by the person who was visiting the tenant at the

Answer to question 1:

Answer to A:

The “taxation ruling of TR 97/23” clarifies the conditions where the outgoings

associated to repairs is treated as the permissible deductions under “section 25-10 of the

ITAA 1997”. In context of “section 25-10” repairs are denoted as work performed on the

premises to remedy the defects, damage or deterioration that contemplates the continuous

presence of property (Barkoczy, 2014). Repairs for majority of part is partial or occasional.

Works can be fairly termed as repair if it carried out to make the deterioration good arisen by

wear and tear, by accidental or deliberate damage or due to the natural causes. The judicial

decision made in “BP Oil Refinary Ltd v FC of T (1992)” stated that the work would not be

treated as repair until it comprises restoration of something that is damaged or lost whether

function or substances or certain other characteristics or quality (Grange et al., 2014).

Ruby Engineering Pty Ltd held the rental property since 2008. The company replaced

the kitchen fittings and cupboard that was deteriorated by wear and tear. The company

replaced the cupboard with the similar type without causing any substantial change. In

context of the “section 25-10 of the ITAA 1997”, the repairs expense of $8,500 performed by

company on the kitchen will quality for deduction since the work was performed to remedy

the defects caused by wear and tear in order to contemplate the continuous presence of

property (James, 2015). The works can be fairly termed as repair which was carried out to

make the deterioration good arisen by wear and tear.

Answer to B:

As per “section 8-1 of the ITAA 1997” the taxpayer is permitted to obtain the

deduction for the legal outgoings that is occurred in defending the damages claims in context

of the injuries that is allegedly sustained by the person who was visiting the tenant at the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

rental property (Jover-Ledesma, 2015). The general provision of “section 8-1” permits the

deduction for the outgoings when the outlays has been incurred in gaining or generating the

assessable earnings unless the expenditure are private or capital or related in the derivation of

the exempted income.

The opinion expressed in “Herald & Weekly Times Ltd v FC of T (1991)” held that

lawful expenses are treated deductible given the expenses have originated based on the

consequences of the taxpayer revenue deriving activities given legal outlays are not private or

domestic in nature (Sadiq, 2015). As understood in the current situation of Ruby Engineering

Pty Ltd the company incurred legal expenses when the visitor to tenants slipped on the steps

and suffered injuries that needed the medical attention. The visitor initiated legal proceedings

which resulted Ruby to incur legal expense of $7,000.

The legal expenses incurred by Ruby Engineering Pty Ltd is a permissible deductible

outgoing. Ruby Engineering incurred the legal expenses in capacity of land lord resulting

from the risk that is ever present to the land lord. The outgoings are a permissible deductible

expenses since it was incurred because the property was let out for generating assessable

income. The expenses were incurred by Ruby Engineering during the course of generating

assessable income. Furthermore, there is a clear connection amid the legal expenses and

Ruby engineering rental income such that the outgoings were relevant and incidental in the

derivation of the taxable rental income (Woellner et al., 2016). Therefore, the taxpayer here

Ruby Engineering is entitled to obtain the deduction under “section 8-1” relating to the legal

outgoings that it has occurred in the defending the claims for damages.

Answer to C:

According to the “section 26-5 of the ITAA 1997”, a person is denied income tax

deduction through the penalty under the Australian law (Blakelock & King, 2017). The

rental property (Jover-Ledesma, 2015). The general provision of “section 8-1” permits the

deduction for the outgoings when the outlays has been incurred in gaining or generating the

assessable earnings unless the expenditure are private or capital or related in the derivation of

the exempted income.

The opinion expressed in “Herald & Weekly Times Ltd v FC of T (1991)” held that

lawful expenses are treated deductible given the expenses have originated based on the

consequences of the taxpayer revenue deriving activities given legal outlays are not private or

domestic in nature (Sadiq, 2015). As understood in the current situation of Ruby Engineering

Pty Ltd the company incurred legal expenses when the visitor to tenants slipped on the steps

and suffered injuries that needed the medical attention. The visitor initiated legal proceedings

which resulted Ruby to incur legal expense of $7,000.

The legal expenses incurred by Ruby Engineering Pty Ltd is a permissible deductible

outgoing. Ruby Engineering incurred the legal expenses in capacity of land lord resulting

from the risk that is ever present to the land lord. The outgoings are a permissible deductible

expenses since it was incurred because the property was let out for generating assessable

income. The expenses were incurred by Ruby Engineering during the course of generating

assessable income. Furthermore, there is a clear connection amid the legal expenses and

Ruby engineering rental income such that the outgoings were relevant and incidental in the

derivation of the taxable rental income (Woellner et al., 2016). Therefore, the taxpayer here

Ruby Engineering is entitled to obtain the deduction under “section 8-1” relating to the legal

outgoings that it has occurred in the defending the claims for damages.

Answer to C:

According to the “section 26-5 of the ITAA 1997”, a person is denied income tax

deduction through the penalty under the Australian law (Blakelock & King, 2017). The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

taxpayers are denied deduction for any amount that is ordered by the law court to be paid as

the conviction to a business for the offence against the Australian law or the overseas law.

“Section 26-5 of the ITAA 1997” provides instances where the fines imposed on business for

indulging in the misleading or deceptive conduct is not allowed as deduction (Burton, 2017).

As understood from the circumstances of Ruby Engineering the company sold a batch

of defective parts to an Australian car producer. The car producer lodged the claim for

damages against Ruby Engineering that resulted the company to pay compensation of

$750,000. The amount paid as compensation by Ruby Engineering Pty Ltd is non-deductible

under the “section 26-5 of the ITAA 1997” since it constituted a business fines that is

imposed for indulging in the deceptive business conduct.

Answer to question 2:

Answer to A:

Capital gains tax is not treated as the separate tax. Capital gains is only applied on the

assets that is purchased on or after the 20th September 1985. Consequently, the term pre-CGT

and post CGT that is generally used to refer to the assets that is purchased or events that takes

place before or after the that date (Chardon et al., 2017). Usually, CGT functions

prospectively and it is applicable when the CGT event takes place for the assets that are

acquired on or after the 20/9/1985. A capital gains or capital loss only happens if the CGT

event occurs relating to the CGT asset. The gains or loss is only derived at the time when the

CGT event takes place.

As understood here Betty bought a painting on 2nd May 1985 which was later sold for

$125,000. The painting will be classified as the Pre-CGT asset since the painting was bought

by Betty before the introduction of the capital gains tax (Miller & Oats, 2016). In other

words, the painting will be treated as the pre-CGT asset because it was purchased by Betty

taxpayers are denied deduction for any amount that is ordered by the law court to be paid as

the conviction to a business for the offence against the Australian law or the overseas law.

“Section 26-5 of the ITAA 1997” provides instances where the fines imposed on business for

indulging in the misleading or deceptive conduct is not allowed as deduction (Burton, 2017).

As understood from the circumstances of Ruby Engineering the company sold a batch

of defective parts to an Australian car producer. The car producer lodged the claim for

damages against Ruby Engineering that resulted the company to pay compensation of

$750,000. The amount paid as compensation by Ruby Engineering Pty Ltd is non-deductible

under the “section 26-5 of the ITAA 1997” since it constituted a business fines that is

imposed for indulging in the deceptive business conduct.

Answer to question 2:

Answer to A:

Capital gains tax is not treated as the separate tax. Capital gains is only applied on the

assets that is purchased on or after the 20th September 1985. Consequently, the term pre-CGT

and post CGT that is generally used to refer to the assets that is purchased or events that takes

place before or after the that date (Chardon et al., 2017). Usually, CGT functions

prospectively and it is applicable when the CGT event takes place for the assets that are

acquired on or after the 20/9/1985. A capital gains or capital loss only happens if the CGT

event occurs relating to the CGT asset. The gains or loss is only derived at the time when the

CGT event takes place.

As understood here Betty bought a painting on 2nd May 1985 which was later sold for

$125,000. The painting will be classified as the Pre-CGT asset since the painting was bought

by Betty before the introduction of the capital gains tax (Miller & Oats, 2016). In other

words, the painting will be treated as the pre-CGT asset because it was purchased by Betty

5TAXATION LAW

before 20 September 1985 (Blakelock & King, 2017). The capital gains that is derived from

the disposal of painting shall be excluded from the provision of capital gains and would not

attract tax liability.

Answer to B:

According to the “section 108-5 of the ITAA 1997” shares in the corporation and

units in the trust are viewed as the CGT asset. A CGT event A1 happens under “section 104-

10 (1)” when the CGT asset is sold or disposed that is owned by the taxpayer (James &

Nobes, 2016). For an investor, the capital gains tax is applied on the shares or units when the

CGT event takes place, such as when the shares held are sold.

As evident here Betty obtained profits from selling the shares of Common Bank Ltd

and PHB Iron Ore Ltd. However, Betty suffered loss from the Young Kids Learning Ltd

shares.

Answer to C:

Conferring to the “subdivision 108-C” a personal use assets are viewed as non-

collectable asset that is kept mostly by the taxpayers for their individual enjoyment and usage

(Fleurbaey & Maniquet, 2015). These possessions comprise the boats, furniture, electrical

goods and items of household. The private use assets however do not contain of the land and

building. As per the “section 108-30 of the ITAA 1997” the price base of the private use

asset is not included under the third element.

As stated under the “section 118-10 (3) of the ITAA 1997” any type of capital gains

that is derived by the assesse from the personal use asset purchased or acquired for the

$10,000 or less should be disregarded by the taxpayer (Miller & Oats, 2016). This indicates

that the assesse is under the requirement of keeping the records of the acquisition of the

individual use assets given the assets are purchase or purchased for $10,000 or more.

before 20 September 1985 (Blakelock & King, 2017). The capital gains that is derived from

the disposal of painting shall be excluded from the provision of capital gains and would not

attract tax liability.

Answer to B:

According to the “section 108-5 of the ITAA 1997” shares in the corporation and

units in the trust are viewed as the CGT asset. A CGT event A1 happens under “section 104-

10 (1)” when the CGT asset is sold or disposed that is owned by the taxpayer (James &

Nobes, 2016). For an investor, the capital gains tax is applied on the shares or units when the

CGT event takes place, such as when the shares held are sold.

As evident here Betty obtained profits from selling the shares of Common Bank Ltd

and PHB Iron Ore Ltd. However, Betty suffered loss from the Young Kids Learning Ltd

shares.

Answer to C:

Conferring to the “subdivision 108-C” a personal use assets are viewed as non-

collectable asset that is kept mostly by the taxpayers for their individual enjoyment and usage

(Fleurbaey & Maniquet, 2015). These possessions comprise the boats, furniture, electrical

goods and items of household. The private use assets however do not contain of the land and

building. As per the “section 108-30 of the ITAA 1997” the price base of the private use

asset is not included under the third element.

As stated under the “section 118-10 (3) of the ITAA 1997” any type of capital gains

that is derived by the assesse from the personal use asset purchased or acquired for the

$10,000 or less should be disregarded by the taxpayer (Miller & Oats, 2016). This indicates

that the assesse is under the requirement of keeping the records of the acquisition of the

individual use assets given the assets are purchase or purchased for $10,000 or more.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Alternatively, if the private use asset is sold by the taxpayer for a loss the taxpayer is not

permitted to offset the loss contrary to the capital gains.

As understood here that Betty was interested in collecting the musical instrument.

Betty sold the violin for $12,000 that was purchased by her for a cost of $5,500. The violin

can be categorized as the personal use asset because Betty used the violin for her own

enjoyment and use. With respect to the “section 118-10 (3), ITAA 1997” the capital gains

that is made by Betty from the violin should be disregarded because the cost of painting was

less than $10,000 and hence capital gains made from the disposal should be disregarded.

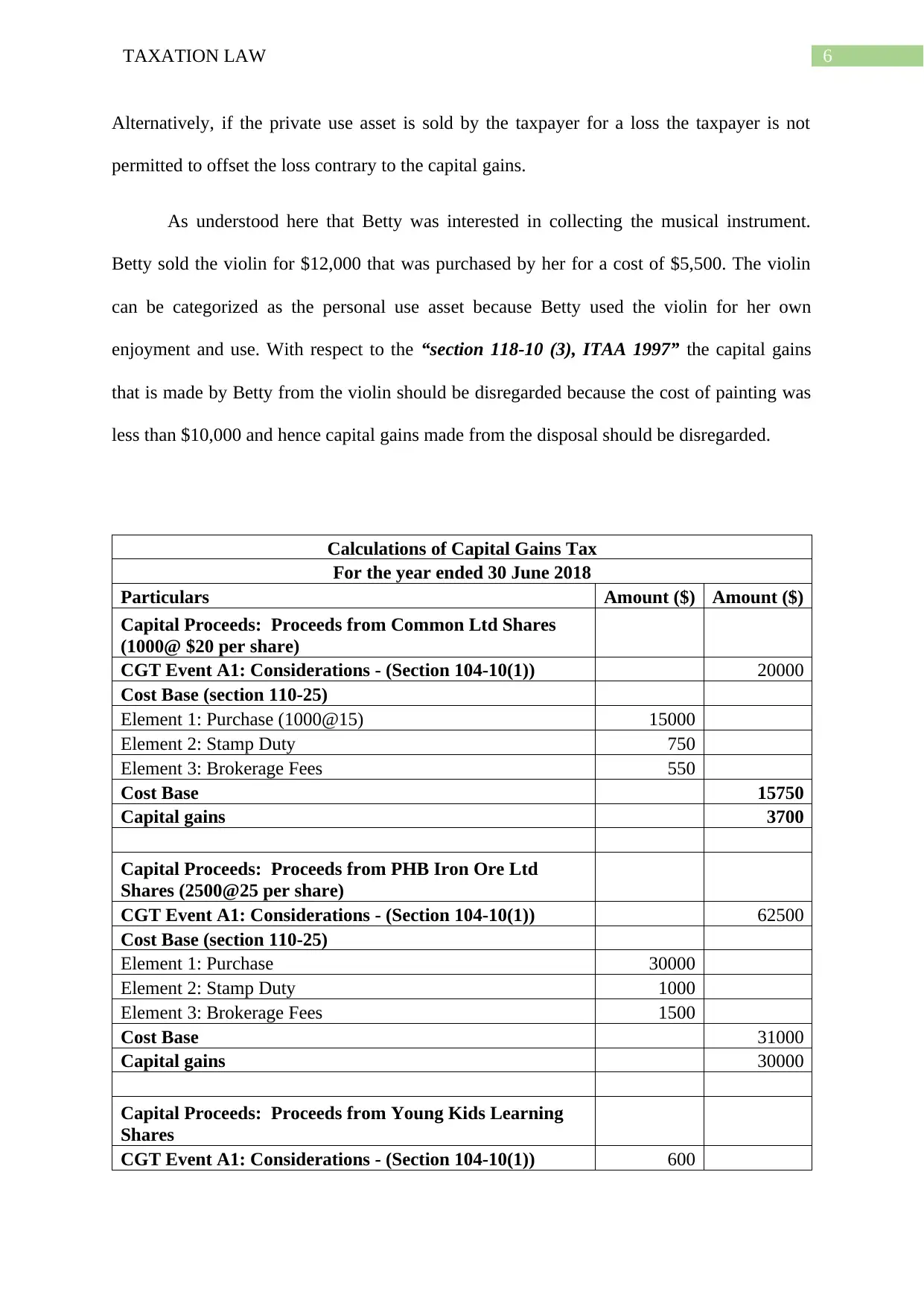

Calculations of Capital Gains Tax

For the year ended 30 June 2018

Particulars Amount ($) Amount ($)

Capital Proceeds: Proceeds from Common Ltd Shares

(1000@ $20 per share)

CGT Event A1: Considerations - (Section 104-10(1)) 20000

Cost Base (section 110-25)

Element 1: Purchase (1000@15) 15000

Element 2: Stamp Duty 750

Element 3: Brokerage Fees 550

Cost Base 15750

Capital gains 3700

Capital Proceeds: Proceeds from PHB Iron Ore Ltd

Shares (2500@25 per share)

CGT Event A1: Considerations - (Section 104-10(1)) 62500

Cost Base (section 110-25)

Element 1: Purchase 30000

Element 2: Stamp Duty 1000

Element 3: Brokerage Fees 1500

Cost Base 31000

Capital gains 30000

Capital Proceeds: Proceeds from Young Kids Learning

Shares

CGT Event A1: Considerations - (Section 104-10(1)) 600

Alternatively, if the private use asset is sold by the taxpayer for a loss the taxpayer is not

permitted to offset the loss contrary to the capital gains.

As understood here that Betty was interested in collecting the musical instrument.

Betty sold the violin for $12,000 that was purchased by her for a cost of $5,500. The violin

can be categorized as the personal use asset because Betty used the violin for her own

enjoyment and use. With respect to the “section 118-10 (3), ITAA 1997” the capital gains

that is made by Betty from the violin should be disregarded because the cost of painting was

less than $10,000 and hence capital gains made from the disposal should be disregarded.

Calculations of Capital Gains Tax

For the year ended 30 June 2018

Particulars Amount ($) Amount ($)

Capital Proceeds: Proceeds from Common Ltd Shares

(1000@ $20 per share)

CGT Event A1: Considerations - (Section 104-10(1)) 20000

Cost Base (section 110-25)

Element 1: Purchase (1000@15) 15000

Element 2: Stamp Duty 750

Element 3: Brokerage Fees 550

Cost Base 15750

Capital gains 3700

Capital Proceeds: Proceeds from PHB Iron Ore Ltd

Shares (2500@25 per share)

CGT Event A1: Considerations - (Section 104-10(1)) 62500

Cost Base (section 110-25)

Element 1: Purchase 30000

Element 2: Stamp Duty 1000

Element 3: Brokerage Fees 1500

Cost Base 31000

Capital gains 30000

Capital Proceeds: Proceeds from Young Kids Learning

Shares

CGT Event A1: Considerations - (Section 104-10(1)) 600

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

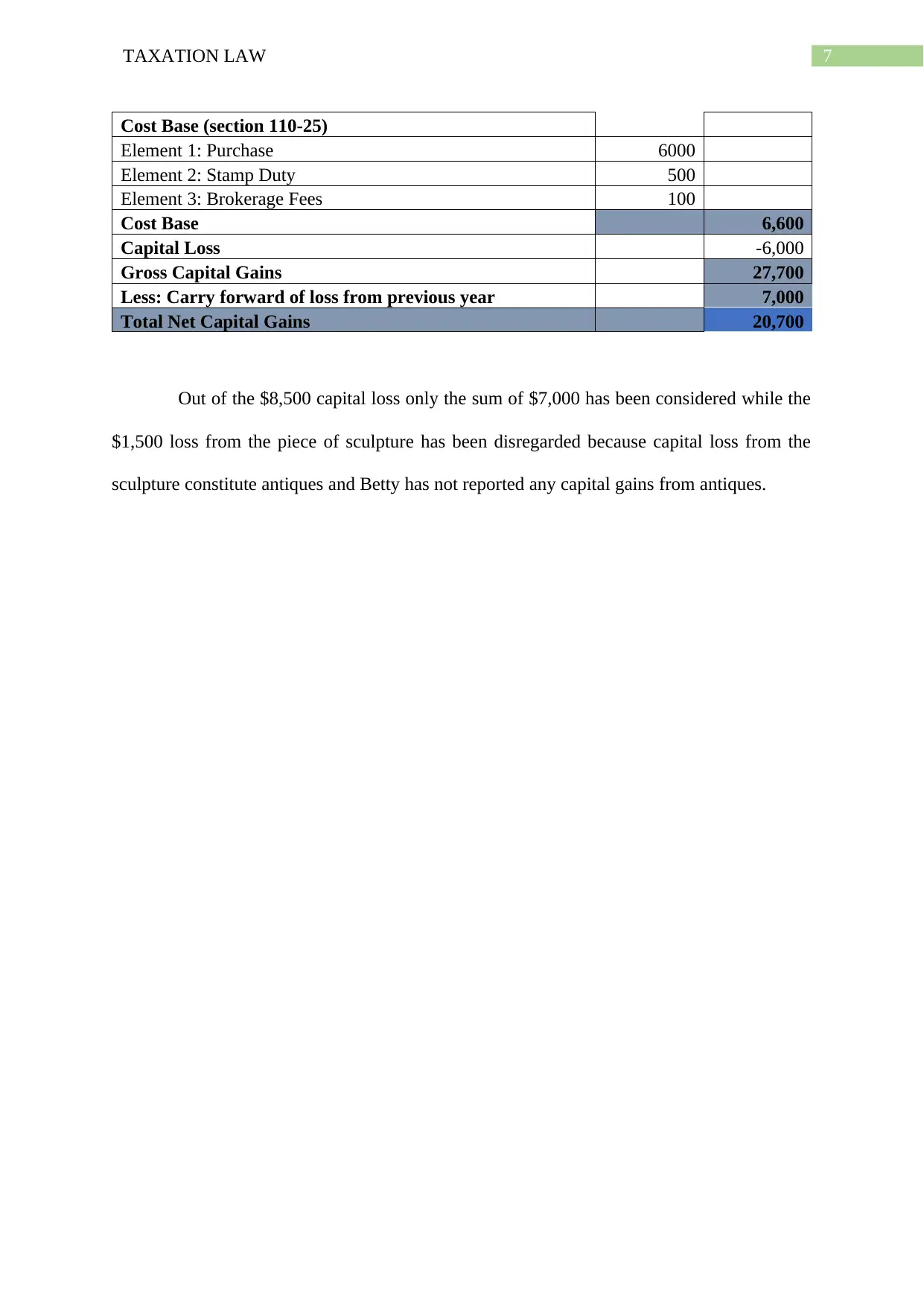

Cost Base (section 110-25)

Element 1: Purchase 6000

Element 2: Stamp Duty 500

Element 3: Brokerage Fees 100

Cost Base 6,600

Capital Loss -6,000

Gross Capital Gains 27,700

Less: Carry forward of loss from previous year 7,000

Total Net Capital Gains 20,700

Out of the $8,500 capital loss only the sum of $7,000 has been considered while the

$1,500 loss from the piece of sculpture has been disregarded because capital loss from the

sculpture constitute antiques and Betty has not reported any capital gains from antiques.

Cost Base (section 110-25)

Element 1: Purchase 6000

Element 2: Stamp Duty 500

Element 3: Brokerage Fees 100

Cost Base 6,600

Capital Loss -6,000

Gross Capital Gains 27,700

Less: Carry forward of loss from previous year 7,000

Total Net Capital Gains 20,700

Out of the $8,500 capital loss only the sum of $7,000 has been considered while the

$1,500 loss from the piece of sculpture has been disregarded because capital loss from the

sculpture constitute antiques and Betty has not reported any capital gains from antiques.

8TAXATION LAW

References

Barkoczy, S. (2014). Foundations of taxation law 2014.

Blakelock, S., & King, P. (2017). Taxation law: The advance of ATO data

matching. Proctor, The, 37(6), 18.

Burton, M. (2017). A Review of Judicial References to the Dictum of Jordan CJ, Expressed

in Scott v. Commissioner of Taxation, in Elaborating the Meaning of Income for the

Purposes of the Australian Income Tax. J. Austl. Tax'n, 19, 50.

Chardon, T., Brimble, M., & Freudenberg, B. (2017). Tax and superannuation literacy:

Australian and New Zealand perspectives [Part 1]. Taxation Today, (102), 17-25.

Fleurbaey, M., & Maniquet, F. (2015). Optimal taxation theory and principles of

fairness (No. 2015005). Université catholique de Louvain, Center for Operations

Research and Econometrics (CORE).

Grange, J., Jover-Ledesma, G. and Maydew, G. (2014). Principles of business taxation.

James, S. (2015). The economics of taxation.

James, S. R., & Nobes, C. (2016). Economics of Taxation: Principles, Policy and Practice.

Fiscal Publications.

Jover-Ledesma, G. (2015). Principles of business taxation: Cch Incorporated.

Miller, A., & Oats, L. (2016). Principles of international taxation. Bloomsbury Publishing.

Sadiq, K. (2015). Principles of taxation law 2014.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C., & Pinto, D. (2016). Australian Taxation

Law. OUP Catalogue.

References

Barkoczy, S. (2014). Foundations of taxation law 2014.

Blakelock, S., & King, P. (2017). Taxation law: The advance of ATO data

matching. Proctor, The, 37(6), 18.

Burton, M. (2017). A Review of Judicial References to the Dictum of Jordan CJ, Expressed

in Scott v. Commissioner of Taxation, in Elaborating the Meaning of Income for the

Purposes of the Australian Income Tax. J. Austl. Tax'n, 19, 50.

Chardon, T., Brimble, M., & Freudenberg, B. (2017). Tax and superannuation literacy:

Australian and New Zealand perspectives [Part 1]. Taxation Today, (102), 17-25.

Fleurbaey, M., & Maniquet, F. (2015). Optimal taxation theory and principles of

fairness (No. 2015005). Université catholique de Louvain, Center for Operations

Research and Econometrics (CORE).

Grange, J., Jover-Ledesma, G. and Maydew, G. (2014). Principles of business taxation.

James, S. (2015). The economics of taxation.

James, S. R., & Nobes, C. (2016). Economics of Taxation: Principles, Policy and Practice.

Fiscal Publications.

Jover-Ledesma, G. (2015). Principles of business taxation: Cch Incorporated.

Miller, A., & Oats, L. (2016). Principles of international taxation. Bloomsbury Publishing.

Sadiq, K. (2015). Principles of taxation law 2014.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C., & Pinto, D. (2016). Australian Taxation

Law. OUP Catalogue.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.