Fringe Benefits Tax in Australia

VerifiedAdded on 2020/04/01

|13

|2560

|39

AI Summary

This assignment delves into the complexities of Australian Fringe Benefits Tax (FBT) legislation. It examines various aspects of FBT, including its application to fringe benefits like car usage and travel expenses. The analysis incorporates relevant case laws and legal interpretations to illustrate how FBT operates in real-world scenarios.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Author’s Note

Taxation Law

Name of the Student

Name of the University

Author’s Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1TAXATION LAW

Table of Contents

Issue.................................................................................................................................................2

Legislation.......................................................................................................................................2

Application......................................................................................................................................3

Car FBT Determination...............................................................................................................3

Employment Duties of an Itinerant Nature..................................................................................6

Fringe Benefit Tax for Car Parking.............................................................................................7

Fringe Benefit Tax on Accommodation......................................................................................7

Charlie and Shiny Homes Fringe Benefit Tax Consequences.....................................................8

Conclusion.......................................................................................................................................9

References......................................................................................................................................10

Table of Contents

Issue.................................................................................................................................................2

Legislation.......................................................................................................................................2

Application......................................................................................................................................3

Car FBT Determination...............................................................................................................3

Employment Duties of an Itinerant Nature..................................................................................6

Fringe Benefit Tax for Car Parking.............................................................................................7

Fringe Benefit Tax on Accommodation......................................................................................7

Charlie and Shiny Homes Fringe Benefit Tax Consequences.....................................................8

Conclusion.......................................................................................................................................9

References......................................................................................................................................10

2TAXATION LAW

Issue

In this report, the main issue is to determine the consequences of fringe benefits of Shiny

Homes and Charlie. The provided case states that Charlie works as a real estate agent and is

employed in Shiny Homes Pty Ltd. Shiny Homes is involved in the landscaping business and the

company has provided Charlie with a 4-wheel drive sedan. According to Section 6 of the

Miscellaneous Taxation Rulings and Fringe Benefit Tax Assessment Act 1986, there are

certain circumstances where fringe benefits tax will be levied on car.

Legislation

The relevant legislation in this case is mentioned below:

Section 6 of the Miscellaneous Taxation Rulings and Fringe Benefit Tax Assessment Act

1986

Taxation rulings of MT 2027

Sub-section 136

Sub-section 136 (1)

Section 51 of the Income Tax Assessment Act 1997

Sub-division F of Division 3

Lunney and Hayley v FCT (1958)

Newsom v Robertson (1952) 2 All ER 728; (1952)

Simon in Taylor v Provan (1975) AC 194

Section 5 of the Fringe Benefit Tax Act 1986

Tubemakers of Australia Ltd v. FC of T 93

Issue

In this report, the main issue is to determine the consequences of fringe benefits of Shiny

Homes and Charlie. The provided case states that Charlie works as a real estate agent and is

employed in Shiny Homes Pty Ltd. Shiny Homes is involved in the landscaping business and the

company has provided Charlie with a 4-wheel drive sedan. According to Section 6 of the

Miscellaneous Taxation Rulings and Fringe Benefit Tax Assessment Act 1986, there are

certain circumstances where fringe benefits tax will be levied on car.

Legislation

The relevant legislation in this case is mentioned below:

Section 6 of the Miscellaneous Taxation Rulings and Fringe Benefit Tax Assessment Act

1986

Taxation rulings of MT 2027

Sub-section 136

Sub-section 136 (1)

Section 51 of the Income Tax Assessment Act 1997

Sub-division F of Division 3

Lunney and Hayley v FCT (1958)

Newsom v Robertson (1952) 2 All ER 728; (1952)

Simon in Taylor v Provan (1975) AC 194

Section 5 of the Fringe Benefit Tax Act 1986

Tubemakers of Australia Ltd v. FC of T 93

3TAXATION LAW

Application

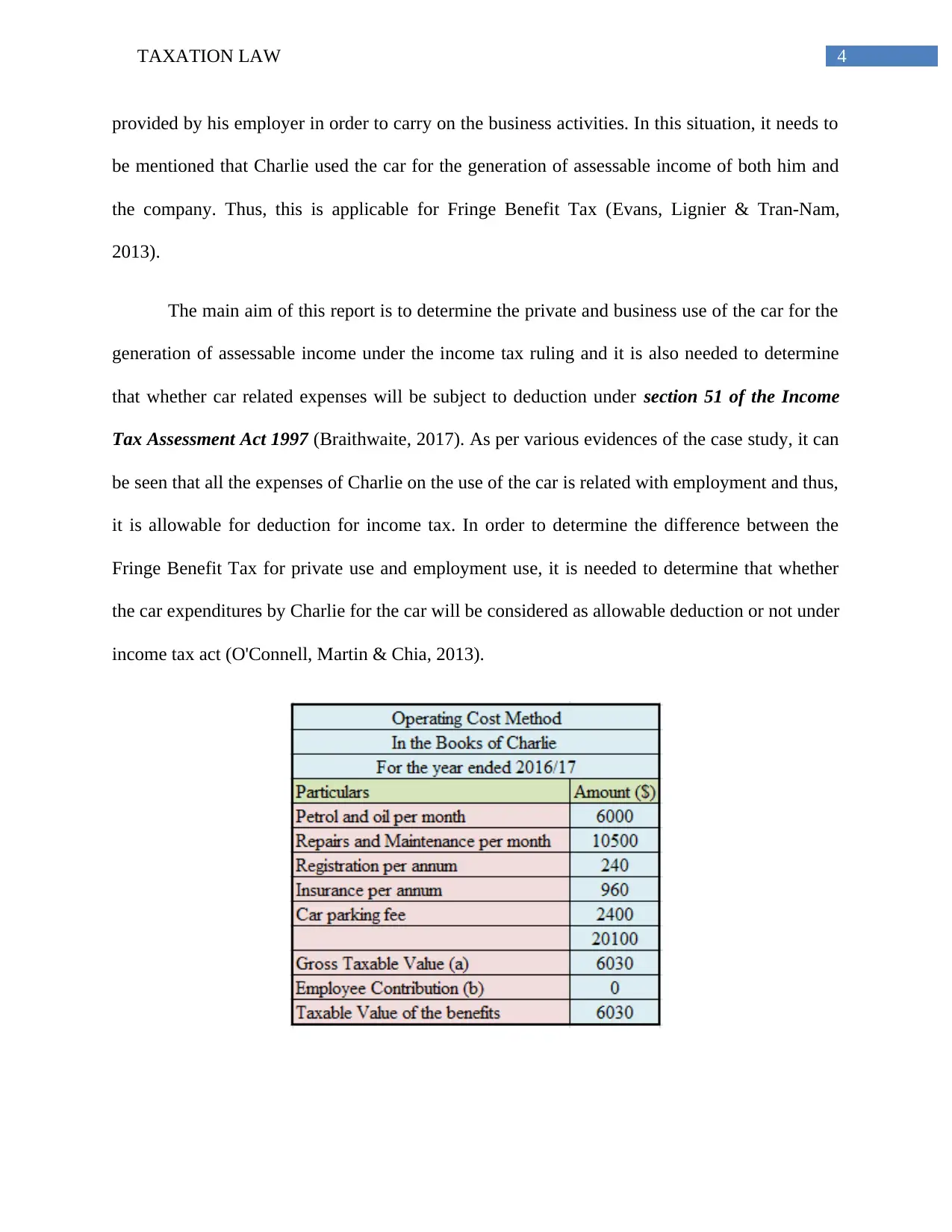

Car FBT Determination

It is stated in taxation rulings of MT 2027 private use under sub-section 136 (1) that any

kind of use by the employees that is not for the purpose of generating assessable income will be

considered as Private Use. Sub-section 136 (1) includes valuation method of operating cost of

the business journey of the cars that is not associated with the private use. It is defined under

Paragraph 3 of the Miscellaneous Taxation Ruling that in order to determine the operating cost

of the cars, it is required to write down the kilometer travelled by the car for the personal use of

the employees in a particular logbook or any kind of similar documents (Lowe, 2014). It can be

seen in the provided case study that Charlie travelled a total of 50000 kilometer for his work

purpose. In order to determine the fringe benefit of the car used by Charlie, there will be

application of operational cost valuation method as per Sub-section 136 (1) of the

Miscellaneous Taxation Rulings of 2027 (Lignier & Evans, 2012).

There is a criticality in determining the business and private use. Thus, it is needed to

determine whether the employee uses the car or the associates for the generation of the

employee’s assessable income (Evans & Kerr, 2012). In this situation, as per Sub section 136

(1), this process includes the use of the car by the employee in order to generate assessable

income or to perform the business activities in order to generate the assessable income of the

business organization (Mountain & Szuster, 2014). This process also includes the use of the car

by the employee that the employer has provided to him in order to carry on the business

activities and this is eligible under Fringe Benefit Tax. In addition, the use of the car by the

associate of the employee and is carried out by the employee will also be considered for the use

of business purpose. As per the provided scenario, it can be seen that Charlie used the car

Application

Car FBT Determination

It is stated in taxation rulings of MT 2027 private use under sub-section 136 (1) that any

kind of use by the employees that is not for the purpose of generating assessable income will be

considered as Private Use. Sub-section 136 (1) includes valuation method of operating cost of

the business journey of the cars that is not associated with the private use. It is defined under

Paragraph 3 of the Miscellaneous Taxation Ruling that in order to determine the operating cost

of the cars, it is required to write down the kilometer travelled by the car for the personal use of

the employees in a particular logbook or any kind of similar documents (Lowe, 2014). It can be

seen in the provided case study that Charlie travelled a total of 50000 kilometer for his work

purpose. In order to determine the fringe benefit of the car used by Charlie, there will be

application of operational cost valuation method as per Sub-section 136 (1) of the

Miscellaneous Taxation Rulings of 2027 (Lignier & Evans, 2012).

There is a criticality in determining the business and private use. Thus, it is needed to

determine whether the employee uses the car or the associates for the generation of the

employee’s assessable income (Evans & Kerr, 2012). In this situation, as per Sub section 136

(1), this process includes the use of the car by the employee in order to generate assessable

income or to perform the business activities in order to generate the assessable income of the

business organization (Mountain & Szuster, 2014). This process also includes the use of the car

by the employee that the employer has provided to him in order to carry on the business

activities and this is eligible under Fringe Benefit Tax. In addition, the use of the car by the

associate of the employee and is carried out by the employee will also be considered for the use

of business purpose. As per the provided scenario, it can be seen that Charlie used the car

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4TAXATION LAW

provided by his employer in order to carry on the business activities. In this situation, it needs to

be mentioned that Charlie used the car for the generation of assessable income of both him and

the company. Thus, this is applicable for Fringe Benefit Tax (Evans, Lignier & Tran-Nam,

2013).

The main aim of this report is to determine the private and business use of the car for the

generation of assessable income under the income tax ruling and it is also needed to determine

that whether car related expenses will be subject to deduction under section 51 of the Income

Tax Assessment Act 1997 (Braithwaite, 2017). As per various evidences of the case study, it can

be seen that all the expenses of Charlie on the use of the car is related with employment and thus,

it is allowable for deduction for income tax. In order to determine the difference between the

Fringe Benefit Tax for private use and employment use, it is needed to determine that whether

the car expenditures by Charlie for the car will be considered as allowable deduction or not under

income tax act (O'Connell, Martin & Chia, 2013).

provided by his employer in order to carry on the business activities. In this situation, it needs to

be mentioned that Charlie used the car for the generation of assessable income of both him and

the company. Thus, this is applicable for Fringe Benefit Tax (Evans, Lignier & Tran-Nam,

2013).

The main aim of this report is to determine the private and business use of the car for the

generation of assessable income under the income tax ruling and it is also needed to determine

that whether car related expenses will be subject to deduction under section 51 of the Income

Tax Assessment Act 1997 (Braithwaite, 2017). As per various evidences of the case study, it can

be seen that all the expenses of Charlie on the use of the car is related with employment and thus,

it is allowable for deduction for income tax. In order to determine the difference between the

Fringe Benefit Tax for private use and employment use, it is needed to determine that whether

the car expenditures by Charlie for the car will be considered as allowable deduction or not under

income tax act (O'Connell, Martin & Chia, 2013).

5TAXATION LAW

In consideration with the provided case study of Charlie and Shiny Homes, the principles

and guidelines of Miscellaneous Taxation Rulings of 2027 are most relevant under Income Tax.

In this situation, it needs to be mentioned that as per the rulings of Sub-division F of Division 3,

the incurred car expenses of Charlie and Shiny Homes is subject to income tax deduction.

The Taxation rulings of IT 112 and the verdict in the case of Lunney and Hayley v FCT

(1958) state that the travel between the workplace and the home of the employees will be

considered as ordinary private travel (Cornish & Lock, 2015). For the generation of assessable

income, travelling to work is necessary pre-requisite and it is essential for earning of income. For

this reason, the kilometer travelled by Charlie from his home to the workplace will be considered

as private travel and the various course of employment will not change the course of the result.

Hence, the workplace and employment is essential for this purpose. As per the verdict in

Newsom v Robertson (1952) 2 All ER 728; (1952), the barrister’s cost while travelling from

home to office would be considered as office expenses (Samuel, 2013). As per the court’s

verdict, the travelling of the barrister from home to chamber or to other courts would not be

considered as expenses.

In consideration with the provided case study of Charlie and Shiny Homes, the principles

and guidelines of Miscellaneous Taxation Rulings of 2027 are most relevant under Income Tax.

In this situation, it needs to be mentioned that as per the rulings of Sub-division F of Division 3,

the incurred car expenses of Charlie and Shiny Homes is subject to income tax deduction.

The Taxation rulings of IT 112 and the verdict in the case of Lunney and Hayley v FCT

(1958) state that the travel between the workplace and the home of the employees will be

considered as ordinary private travel (Cornish & Lock, 2015). For the generation of assessable

income, travelling to work is necessary pre-requisite and it is essential for earning of income. For

this reason, the kilometer travelled by Charlie from his home to the workplace will be considered

as private travel and the various course of employment will not change the course of the result.

Hence, the workplace and employment is essential for this purpose. As per the verdict in

Newsom v Robertson (1952) 2 All ER 728; (1952), the barrister’s cost while travelling from

home to office would be considered as office expenses (Samuel, 2013). As per the court’s

verdict, the travelling of the barrister from home to chamber or to other courts would not be

considered as expenses.

6TAXATION LAW

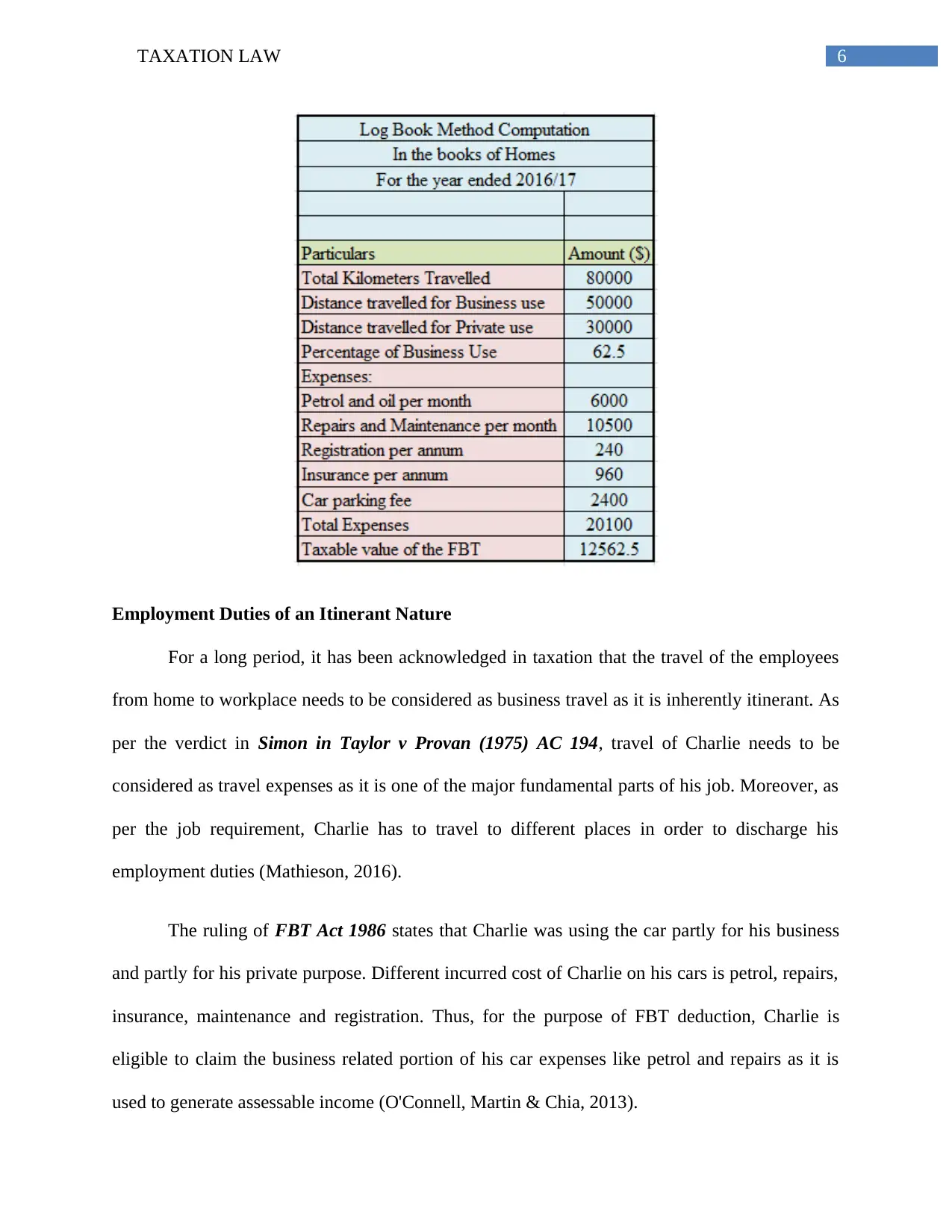

Employment Duties of an Itinerant Nature

For a long period, it has been acknowledged in taxation that the travel of the employees

from home to workplace needs to be considered as business travel as it is inherently itinerant. As

per the verdict in Simon in Taylor v Provan (1975) AC 194, travel of Charlie needs to be

considered as travel expenses as it is one of the major fundamental parts of his job. Moreover, as

per the job requirement, Charlie has to travel to different places in order to discharge his

employment duties (Mathieson, 2016).

The ruling of FBT Act 1986 states that Charlie was using the car partly for his business

and partly for his private purpose. Different incurred cost of Charlie on his cars is petrol, repairs,

insurance, maintenance and registration. Thus, for the purpose of FBT deduction, Charlie is

eligible to claim the business related portion of his car expenses like petrol and repairs as it is

used to generate assessable income (O'Connell, Martin & Chia, 2013).

Employment Duties of an Itinerant Nature

For a long period, it has been acknowledged in taxation that the travel of the employees

from home to workplace needs to be considered as business travel as it is inherently itinerant. As

per the verdict in Simon in Taylor v Provan (1975) AC 194, travel of Charlie needs to be

considered as travel expenses as it is one of the major fundamental parts of his job. Moreover, as

per the job requirement, Charlie has to travel to different places in order to discharge his

employment duties (Mathieson, 2016).

The ruling of FBT Act 1986 states that Charlie was using the car partly for his business

and partly for his private purpose. Different incurred cost of Charlie on his cars is petrol, repairs,

insurance, maintenance and registration. Thus, for the purpose of FBT deduction, Charlie is

eligible to claim the business related portion of his car expenses like petrol and repairs as it is

used to generate assessable income (O'Connell, Martin & Chia, 2013).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Fringe Benefit Tax for Car Parking

Car parking fringe benefit can be applied in case the employee gets car parking facility

from the employer and the following factors are satisfied:

The employee parks the car in the premise that is owned or leased by the employer or the

provider of the car.

The employee parks the car for more than four hours.

Employer owns the car under the control of the employees.

The car is giver for the employment of the employee.

For a minimum of one day, the employee uses the car to go from home to office and

office to home.

The employee parks the car in a commercial parking station for a charge or fee and the

place is within one kilometer of the premise radius.

Based on the above discussion, it needs to be mentioned that the car of Charlie was parked in

a secure parking station for which he gets $200 each week from Shiny Homes. It can be seen

that was parked in Charlie’s garage that is under the control of the provider. In addition, the car

was given to Charlie for employment purpose and he used the car for home to work and work to

home for daily basis. For all these reasons, Charlie is eligible to claim the Fringe Benefits and

Shiny Homes is eligible to claim deduction for car parking fees under on the behalf of the

employee (Hodgson & Pearce, 2015).

Fringe Benefit Tax on Accommodation

As per Fringe Benefit Tax Act 1986, there are certain forms of entertainment under the

provision of entertainment that are in the form of drink or recession, travel or accommodation

Fringe Benefit Tax for Car Parking

Car parking fringe benefit can be applied in case the employee gets car parking facility

from the employer and the following factors are satisfied:

The employee parks the car in the premise that is owned or leased by the employer or the

provider of the car.

The employee parks the car for more than four hours.

Employer owns the car under the control of the employees.

The car is giver for the employment of the employee.

For a minimum of one day, the employee uses the car to go from home to office and

office to home.

The employee parks the car in a commercial parking station for a charge or fee and the

place is within one kilometer of the premise radius.

Based on the above discussion, it needs to be mentioned that the car of Charlie was parked in

a secure parking station for which he gets $200 each week from Shiny Homes. It can be seen

that was parked in Charlie’s garage that is under the control of the provider. In addition, the car

was given to Charlie for employment purpose and he used the car for home to work and work to

home for daily basis. For all these reasons, Charlie is eligible to claim the Fringe Benefits and

Shiny Homes is eligible to claim deduction for car parking fees under on the behalf of the

employee (Hodgson & Pearce, 2015).

Fringe Benefit Tax on Accommodation

As per Fringe Benefit Tax Act 1986, there are certain forms of entertainment under the

provision of entertainment that are in the form of drink or recession, travel or accommodation

8TAXATION LAW

with entertainment and others (Jeremenko, 2014). As per the provided case, Charlie was unable

to use the car for two weeks as he had a minor accident. This happened prior to Charlie’s

wedding and the company decided to hire the car for allowing him to go for honeymoon. In

addition, Shiny Home paid for the accommodation of Charlie’s honeymoon. This is related with

the fringe benefits tax and occurs tax liability for the provision of entertainment. Thus, based on

the above discussion, it can be said that Shiny Homes is eligible to claim deduction and Charlie

has to show this allowance in his tax return as income.

Charlie and Shiny Homes Fringe Benefit Tax Consequences

The tax regulation of TR 94/25 is applicable for the employer and the employer is liable

under section 5 of the Fringe Benefit Tax Act 1986. Thus, under subsection 51 (1) of the

Income Tax Assessment Act 1936, the employer is eligible for claiming fringe benefits tax. In

this regard, subsection 51 (1) is concerned with the fringe benefits installment and timings. As

per TR 94/25, fringe benefits are incurred for the gaining of assessable income and it is subject to

tax deduction under subsection 51 (1) of the ITAA (Tang & Wan, 2015).

The Fringe Benefits tax liability for Shiny Homes generates under the commonwealth

legislation. As per section 5 of the Fringe Benefit Tax Act 1986, based on the fringe benefits

taxable sums, the taxes are generally imposed. According to the verdict of Tubemakers of

Australia Ltd v. FC of T 93, Fringe Benefits Taxable sums includes various fringe benefits

provided by Shiny Homes to Charlie (Barnett & Harder, 2014).

Thus, it can be seen that Shiny Homes has incurred different expenses like honeymoon

accommodation, cost to hire the car and others in order to generate assessable income. Hence, as

per subsection 51 (1) of the ITAA 1997, all the expenses incurred by Shiny Homes is for the

with entertainment and others (Jeremenko, 2014). As per the provided case, Charlie was unable

to use the car for two weeks as he had a minor accident. This happened prior to Charlie’s

wedding and the company decided to hire the car for allowing him to go for honeymoon. In

addition, Shiny Home paid for the accommodation of Charlie’s honeymoon. This is related with

the fringe benefits tax and occurs tax liability for the provision of entertainment. Thus, based on

the above discussion, it can be said that Shiny Homes is eligible to claim deduction and Charlie

has to show this allowance in his tax return as income.

Charlie and Shiny Homes Fringe Benefit Tax Consequences

The tax regulation of TR 94/25 is applicable for the employer and the employer is liable

under section 5 of the Fringe Benefit Tax Act 1986. Thus, under subsection 51 (1) of the

Income Tax Assessment Act 1936, the employer is eligible for claiming fringe benefits tax. In

this regard, subsection 51 (1) is concerned with the fringe benefits installment and timings. As

per TR 94/25, fringe benefits are incurred for the gaining of assessable income and it is subject to

tax deduction under subsection 51 (1) of the ITAA (Tang & Wan, 2015).

The Fringe Benefits tax liability for Shiny Homes generates under the commonwealth

legislation. As per section 5 of the Fringe Benefit Tax Act 1986, based on the fringe benefits

taxable sums, the taxes are generally imposed. According to the verdict of Tubemakers of

Australia Ltd v. FC of T 93, Fringe Benefits Taxable sums includes various fringe benefits

provided by Shiny Homes to Charlie (Barnett & Harder, 2014).

Thus, it can be seen that Shiny Homes has incurred different expenses like honeymoon

accommodation, cost to hire the car and others in order to generate assessable income. Hence, as

per subsection 51 (1) of the ITAA 1997, all the expenses incurred by Shiny Homes is for the

9TAXATION LAW

purpose to generate the assessable income and for this reason, Shiny Home is eligible to claim

allowable deduction for expenses (Martin, 2015).

Conclusion

Based on the above discussion, it can be concluded that all the fringe benefits related

events are taxable under FBT Act 1986. Various parts of this report take into account the

application of different case laws in order to arrive to the decision regarding the car fringe

benefits.

purpose to generate the assessable income and for this reason, Shiny Home is eligible to claim

allowable deduction for expenses (Martin, 2015).

Conclusion

Based on the above discussion, it can be concluded that all the fringe benefits related

events are taxable under FBT Act 1986. Various parts of this report take into account the

application of different case laws in order to arrive to the decision regarding the car fringe

benefits.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10TAXATION LAW

References

Barnett, K., & Harder, S. (2014). Remedies in Australian private law. Cambridge University

Press.

Braithwaite, V. (Ed.). (2017). Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Cornish, A., & Lock, H. (2015). Transport, accommodation and meals: FBT tricks and traps. Tax

Specialist, 19(2), 58.

Evans, C., & Kerr, J. (2012). Tax Reform and'Rough Justice’: Is it Time for Simplicity to Shine?.

Evans, C., Lignier, P., & Tran-Nam, B. (2013). Tax compliance costs for the small and medium

enterprise business sector: Recent evidence from Australia. Tax Administration Research

Centre University of EXETER Discussion Paper, 003-13.

Hodgson, H., & Pearce, P. (2015). TravelSmart or travel tax breaks: is the fringe benefits tax a

barrier to active commuting in Australia? 1. eJournal of Tax Research, 13(3), 819.

Jeremenko, R. (2014). Temporary budget repair levy: Adding complexity. Taxation in

Australia, 49(1), 5.

Lignier, P., & Evans, C. (2012). The rise and rise of tax compliance costs for the small business

sector in Australia.

Lowe, M. (2014). Obesity and climate change mitigation in Australia: overview and analysis of

policies with co‐benefits. Australian and New Zealand journal of public health, 38(1),

19-24.

References

Barnett, K., & Harder, S. (2014). Remedies in Australian private law. Cambridge University

Press.

Braithwaite, V. (Ed.). (2017). Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Cornish, A., & Lock, H. (2015). Transport, accommodation and meals: FBT tricks and traps. Tax

Specialist, 19(2), 58.

Evans, C., & Kerr, J. (2012). Tax Reform and'Rough Justice’: Is it Time for Simplicity to Shine?.

Evans, C., Lignier, P., & Tran-Nam, B. (2013). Tax compliance costs for the small and medium

enterprise business sector: Recent evidence from Australia. Tax Administration Research

Centre University of EXETER Discussion Paper, 003-13.

Hodgson, H., & Pearce, P. (2015). TravelSmart or travel tax breaks: is the fringe benefits tax a

barrier to active commuting in Australia? 1. eJournal of Tax Research, 13(3), 819.

Jeremenko, R. (2014). Temporary budget repair levy: Adding complexity. Taxation in

Australia, 49(1), 5.

Lignier, P., & Evans, C. (2012). The rise and rise of tax compliance costs for the small business

sector in Australia.

Lowe, M. (2014). Obesity and climate change mitigation in Australia: overview and analysis of

policies with co‐benefits. Australian and New Zealand journal of public health, 38(1),

19-24.

11TAXATION LAW

Martin, F. (2015). Overseas travel by employees: When does FBT apply?. Taxation in

Australia, 49(7), 382.

Mathieson, A. C. (2016). Rapid assessment survey of fouling and introduced seaweeds from

southern Maine to Rhode Island. Rhodora, 118(974), 113-147.

Mountain, B., & Szuster, P. (2014). Australia's million solar roofs; disruption on the fringes or

the beginning of a new order?'. Distributed Generation and its Implications for the Utility

Industry, 1.

O'Connell, A., Martin, F., & Chia, J. (2013). Law, policy and politics in Australia's recent not-

for-profit sector reforms. Austl. Tax F., 28, 289.

Samuel, G. (2013). Law of Obligations & Legal Remedies. Routledge.

Tang, R., & Wan, J. (2015). Fringe benefits tax and fly-in fly-out arrangements: John Holland

Group Pty Ltd v Commissioner of Taxation. Australian Resources and Energy Law

Journal, 34(1), 17.

Martin, F. (2015). Overseas travel by employees: When does FBT apply?. Taxation in

Australia, 49(7), 382.

Mathieson, A. C. (2016). Rapid assessment survey of fouling and introduced seaweeds from

southern Maine to Rhode Island. Rhodora, 118(974), 113-147.

Mountain, B., & Szuster, P. (2014). Australia's million solar roofs; disruption on the fringes or

the beginning of a new order?'. Distributed Generation and its Implications for the Utility

Industry, 1.

O'Connell, A., Martin, F., & Chia, J. (2013). Law, policy and politics in Australia's recent not-

for-profit sector reforms. Austl. Tax F., 28, 289.

Samuel, G. (2013). Law of Obligations & Legal Remedies. Routledge.

Tang, R., & Wan, J. (2015). Fringe benefits tax and fly-in fly-out arrangements: John Holland

Group Pty Ltd v Commissioner of Taxation. Australian Resources and Energy Law

Journal, 34(1), 17.

12TAXATION LAW

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.