HI6028 Taxation Law T3 2018: Partnership, Income, & Benefits

VerifiedAdded on 2023/04/23

|13

|2590

|334

Homework Assignment

AI Summary

This assignment solution addresses two key questions related to taxation law. The first question involves calculating the net income from a partnership, considering various receipts, expenses, and relevant tax provisions such as Section 90 of ITAA 1936 and Section 8-1 of ITAA 1997. It analyzes the deductibility of expenses like electricity bills, repairs, and asset purchases, while also addressing non-deductible items like personal drawings. A detailed computation of the partnership's net income is provided. The second question focuses on determining the taxable value of fringe benefits, specifically school fees paid by an employer and housing benefits provided to an employee, referencing Section 20 and Section 25 of FBTA Act 1986. The solution calculates the taxable value of the housing fringe benefit, considering the market value and employee contributions.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Issues:.....................................................................................................................................2

Rule:.......................................................................................................................................2

Applications:..........................................................................................................................4

Conclusion:............................................................................................................................5

Answer to question 2:.................................................................................................................5

Issues:.....................................................................................................................................5

Rule:.......................................................................................................................................5

Application:............................................................................................................................6

Conclusion:............................................................................................................................7

References:.................................................................................................................................8

Table of Contents

Answer to question 1:.................................................................................................................2

Issues:.....................................................................................................................................2

Rule:.......................................................................................................................................2

Applications:..........................................................................................................................4

Conclusion:............................................................................................................................5

Answer to question 2:.................................................................................................................5

Issues:.....................................................................................................................................5

Rule:.......................................................................................................................................5

Application:............................................................................................................................6

Conclusion:............................................................................................................................7

References:.................................................................................................................................8

2TAXATION LAW

Answer to question 1:

Issues:

The case introduces the issues that is related to the calculation of the net income from

the partnership made by the partners during the year.

Rule:

As per the “division 5 of the ITAA 1936”, a partnership is not treated as the separate

business under the general law and partnerships is not required to the tax. Instead the partners

pay the tax on the profits that is distributed to the partners (Arnold, 2016). Under the “section

90, ITAA 1936” the calculation of the net income or loss of the partnership is done after

deducting the allowable expenses.

Assessable income of the taxpayers is regarded as the taxable income that is included

for taxation purpose. Ordinary income is viewed as the income that an individual derives

under the ordinary concepts and the same is considered for taxable purpose under the

“section 6-5, ITAA 1997” (Carlisle & Harrington, 2017). Income as per the ordinary

concepts is explained under the “Scott v CT (1935)” income should be interpreted based on

the ordinary notions and use of mankind.

The provision of general deduction under the “section 8-1, ITAA 1997” explains that

the taxpayer can obtain the deduction for the expenditure if the expenses are sustained at the

time of earning income. The general provision of “section 8-1, ITAA 1997” has the potential

of being implemented to any taxpayer (Deutsch, 2018). Expenses or outgoings that is

necessarily occurred at the time of gaining or producing the assessable income is allowed for

deduction under the general provision of “section 8-1, ITAA 1997”.

Answer to question 1:

Issues:

The case introduces the issues that is related to the calculation of the net income from

the partnership made by the partners during the year.

Rule:

As per the “division 5 of the ITAA 1936”, a partnership is not treated as the separate

business under the general law and partnerships is not required to the tax. Instead the partners

pay the tax on the profits that is distributed to the partners (Arnold, 2016). Under the “section

90, ITAA 1936” the calculation of the net income or loss of the partnership is done after

deducting the allowable expenses.

Assessable income of the taxpayers is regarded as the taxable income that is included

for taxation purpose. Ordinary income is viewed as the income that an individual derives

under the ordinary concepts and the same is considered for taxable purpose under the

“section 6-5, ITAA 1997” (Carlisle & Harrington, 2017). Income as per the ordinary

concepts is explained under the “Scott v CT (1935)” income should be interpreted based on

the ordinary notions and use of mankind.

The provision of general deduction under the “section 8-1, ITAA 1997” explains that

the taxpayer can obtain the deduction for the expenditure if the expenses are sustained at the

time of earning income. The general provision of “section 8-1, ITAA 1997” has the potential

of being implemented to any taxpayer (Deutsch, 2018). Expenses or outgoings that is

necessarily occurred at the time of gaining or producing the assessable income is allowed for

deduction under the general provision of “section 8-1, ITAA 1997”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

In “Amalgamated Zinc Ltd v FCT (1935)” gaining or producing the assessable

income must hold the adequate nexus with the losses or outgoings (James, 2016). This

implies that the expenses should be incurred in the course of producing assessable income.

It is noteworthy to denote that as per the negative limbs of “section 8-1(2))”,

expenses or losses or not allowed for deduction under the general deduction rule given that it

meets the criteria for negative limbs. Expenses that are capital, domestic or private is not

treated for deduction under the negative limbs of “S-8-1 (2))”.

As it has been described under the “sec 25-10” deductions are permitted to the

taxpayer for expenses which is occurred for repairs to the premises or assets that are

depreciative in nature and used for generating the income under “section 25-10” (Kenny et

al., 2018). Similarly, under the “TR 97/23” work that is performed to satisfy the requirement

of the regulatory bodies is not held as repair unless the work is involve remedies to defects.

Item should be used for producing income in order to be permitted for deduction

under the “section 25-10”. This includes the repairs that is occurred in carrying on the

business or repairs that is made to the investment property (McCouat, 2018). Maintenance

work is regarded as repair such as painting on the plant or business premises for rectifying the

damage is held as deductible repair.

The costs that is occurred in replacing the items that are permanent fixtures installed

in the premises used for producing the income is regarded as the deductible repairs under the

“section 25-10” given that the replacement is for damaged out unit by the new one of

identical design to normally restore the function of the asset.

As per the ATO if a taxpayer buys an asset and it is costing $20,000, the taxpayer can

write-off the business part of the asset in their tax return. The taxpayers are eligible for using

In “Amalgamated Zinc Ltd v FCT (1935)” gaining or producing the assessable

income must hold the adequate nexus with the losses or outgoings (James, 2016). This

implies that the expenses should be incurred in the course of producing assessable income.

It is noteworthy to denote that as per the negative limbs of “section 8-1(2))”,

expenses or losses or not allowed for deduction under the general deduction rule given that it

meets the criteria for negative limbs. Expenses that are capital, domestic or private is not

treated for deduction under the negative limbs of “S-8-1 (2))”.

As it has been described under the “sec 25-10” deductions are permitted to the

taxpayer for expenses which is occurred for repairs to the premises or assets that are

depreciative in nature and used for generating the income under “section 25-10” (Kenny et

al., 2018). Similarly, under the “TR 97/23” work that is performed to satisfy the requirement

of the regulatory bodies is not held as repair unless the work is involve remedies to defects.

Item should be used for producing income in order to be permitted for deduction

under the “section 25-10”. This includes the repairs that is occurred in carrying on the

business or repairs that is made to the investment property (McCouat, 2018). Maintenance

work is regarded as repair such as painting on the plant or business premises for rectifying the

damage is held as deductible repair.

The costs that is occurred in replacing the items that are permanent fixtures installed

in the premises used for producing the income is regarded as the deductible repairs under the

“section 25-10” given that the replacement is for damaged out unit by the new one of

identical design to normally restore the function of the asset.

As per the ATO if a taxpayer buys an asset and it is costing $20,000, the taxpayer can

write-off the business part of the asset in their tax return. The taxpayers are eligible for using

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

the simplified rules of depreciation and can claim an immediate deduction for the business

part of every asset that has the loss of less than $20,000.

Applications:

As per the evidence from the case Olivia and Daniel are operating a business as the

partners. Any kind of receipts that is made by Olivia and Daniel from the partnership will be

included for ordinary income within the meaning of ordinary concepts. Under the “section

90, ITAA 1936” the calculation of the net income or loss of the partnership between Olivia

and Daniel is done after deducting the allowable expenses.

The partnership furnished the information that it is earned cash payments from the

sales proceeds and the payment that is obtained from the debtors. The business receipts that is

made by the partners is the real gain that satisfies the prerequisite of the ordinary income.

Denoting the judgement made in “Scott v CT (1935)” the cash receipts and the payments

obtained by the debtors is interpreted as the ordinary business income and is included for

determining the partnership net income.

In the course of carrying on the partnership business the partners also incurred for

electricity bills, council rates, telephone charges, insurance etc. Referring to “Amalgamated

Zinc Ltd v FCT (1935)” the expenses are incurred in gaining or producing the assessable

income and holds the adequate nexus for the losses or outgoings (Raftery, 2015). Therefore,

under the general provision of “section 8-1, ITAA 1997” the expenses are allowed for

deductions.

The partnership also reported certain drawings that were made by them in the form of

cash withdraw and goods withdraw for personal use. The drawings that is made by Olivia and

Daniel during partnership meets the criteria for negative limbs under “section 8-1(2))”. The

expenses will not be permitted for deduction as they are private type of expenses.

the simplified rules of depreciation and can claim an immediate deduction for the business

part of every asset that has the loss of less than $20,000.

Applications:

As per the evidence from the case Olivia and Daniel are operating a business as the

partners. Any kind of receipts that is made by Olivia and Daniel from the partnership will be

included for ordinary income within the meaning of ordinary concepts. Under the “section

90, ITAA 1936” the calculation of the net income or loss of the partnership between Olivia

and Daniel is done after deducting the allowable expenses.

The partnership furnished the information that it is earned cash payments from the

sales proceeds and the payment that is obtained from the debtors. The business receipts that is

made by the partners is the real gain that satisfies the prerequisite of the ordinary income.

Denoting the judgement made in “Scott v CT (1935)” the cash receipts and the payments

obtained by the debtors is interpreted as the ordinary business income and is included for

determining the partnership net income.

In the course of carrying on the partnership business the partners also incurred for

electricity bills, council rates, telephone charges, insurance etc. Referring to “Amalgamated

Zinc Ltd v FCT (1935)” the expenses are incurred in gaining or producing the assessable

income and holds the adequate nexus for the losses or outgoings (Raftery, 2015). Therefore,

under the general provision of “section 8-1, ITAA 1997” the expenses are allowed for

deductions.

The partnership also reported certain drawings that were made by them in the form of

cash withdraw and goods withdraw for personal use. The drawings that is made by Olivia and

Daniel during partnership meets the criteria for negative limbs under “section 8-1(2))”. The

expenses will not be permitted for deduction as they are private type of expenses.

5TAXATION LAW

The repairs and maintenance expenses were occurred by the partners in the form of

shop painting. Under the “sec 25-10” the shop painting amounts to repairs to the premises for

rectifying the damage and it is held as deductible repair (Richelle et al., 2016). Additionally,

there was a replacement costs of refrigerator motor that amounted to $140. The costs that is

occurred in replacing the motor of refrigerator constitutes a permanent fixtures installed on

the premises and used for producing the income. The replacement costs are a repair and it is

assumed as the deductible repairs under the “section 25-10, ITAA 1997”.

The taxpayer also reports the purchase of air-conditions for $1,200. As the expenses

are below $20,000 ATO prescribed limit. The taxpayers are eligible for using the simplified

rules of depreciation and can claim an immediate deduction for the business part of the air-

conditions that is installed.

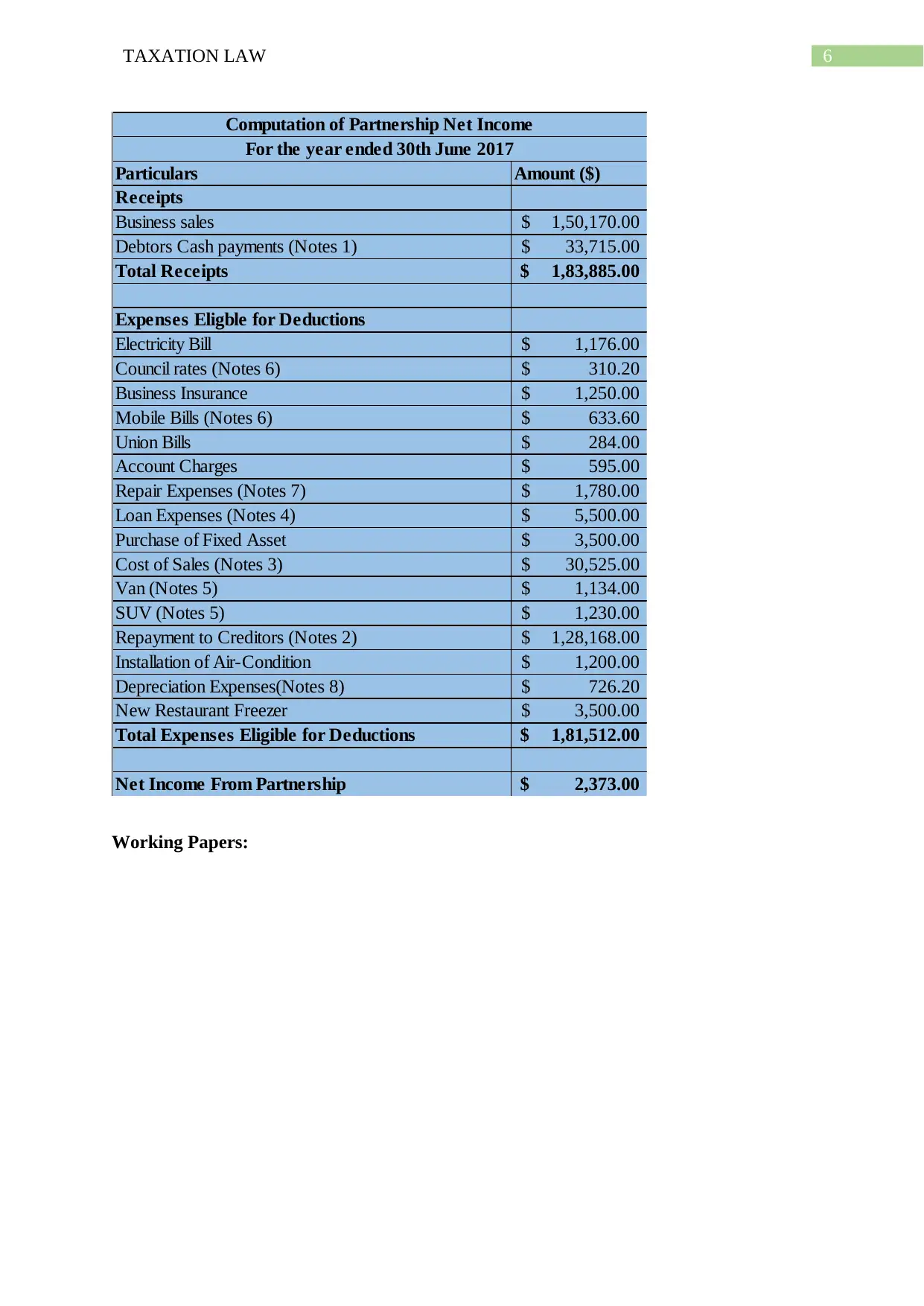

Net Income from Partnership:

The repairs and maintenance expenses were occurred by the partners in the form of

shop painting. Under the “sec 25-10” the shop painting amounts to repairs to the premises for

rectifying the damage and it is held as deductible repair (Richelle et al., 2016). Additionally,

there was a replacement costs of refrigerator motor that amounted to $140. The costs that is

occurred in replacing the motor of refrigerator constitutes a permanent fixtures installed on

the premises and used for producing the income. The replacement costs are a repair and it is

assumed as the deductible repairs under the “section 25-10, ITAA 1997”.

The taxpayer also reports the purchase of air-conditions for $1,200. As the expenses

are below $20,000 ATO prescribed limit. The taxpayers are eligible for using the simplified

rules of depreciation and can claim an immediate deduction for the business part of the air-

conditions that is installed.

Net Income from Partnership:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Particulars Amount ($)

Receipts

Business sales 1,50,170.00$

Debtors Cash payments (Notes 1) 33,715.00$

Total Receipts 1,83,885.00$

Expenses Eligble for Deductions

Electricity Bill 1,176.00$

Council rates (Notes 6) 310.20$

Business Insurance 1,250.00$

Mobile Bills (Notes 6) 633.60$

Union Bills 284.00$

Account Charges 595.00$

Repair Expenses (Notes 7) 1,780.00$

Loan Expenses (Notes 4) 5,500.00$

Purchase of Fixed Asset 3,500.00$

Cost of Sales (Notes 3) 30,525.00$

Van (Notes 5) 1,134.00$

SUV (Notes 5) 1,230.00$

Repayment to Creditors (Notes 2) 1,28,168.00$

Installation of Air-Condition 1,200.00$

Depreciation Expenses(Notes 8) 726.20$

New Restaurant Freezer 3,500.00$

Total Expenses Eligible for Deductions 1,81,512.00$

Net Income From Partnership 2,373.00$

Computation of Partnership Net Income

For the year ended 30th June 2017

Working Papers:

Particulars Amount ($)

Receipts

Business sales 1,50,170.00$

Debtors Cash payments (Notes 1) 33,715.00$

Total Receipts 1,83,885.00$

Expenses Eligble for Deductions

Electricity Bill 1,176.00$

Council rates (Notes 6) 310.20$

Business Insurance 1,250.00$

Mobile Bills (Notes 6) 633.60$

Union Bills 284.00$

Account Charges 595.00$

Repair Expenses (Notes 7) 1,780.00$

Loan Expenses (Notes 4) 5,500.00$

Purchase of Fixed Asset 3,500.00$

Cost of Sales (Notes 3) 30,525.00$

Van (Notes 5) 1,134.00$

SUV (Notes 5) 1,230.00$

Repayment to Creditors (Notes 2) 1,28,168.00$

Installation of Air-Condition 1,200.00$

Depreciation Expenses(Notes 8) 726.20$

New Restaurant Freezer 3,500.00$

Total Expenses Eligible for Deductions 1,81,512.00$

Net Income From Partnership 2,373.00$

Computation of Partnership Net Income

For the year ended 30th June 2017

Working Papers:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Notes 1

Debtors at 1st July 2016 3,925.00$

Debtors Cash Payments 32,800.00$

Debtors at 30th June 2017 3,010.00$

Debtors Net 33,715.00$

Notes 2

Creditors at 1st July 2016 6,500.00$

Add: Repayment to Creditors 1,28,678.00$

Less: Creditors at 30 June 2017 7,010.00$

Creditors Net 1,28,168.00$

Notes 3

Cost of Sales

Stock on 1st July 2016 9,120.00$

Add: Purchase 31,155.00$

Less: Stock on 30th June 2017 9,750.00$

Notes 4 30,525.00$

Loan Repayment

Business Loan 8,500.00$

Less: Reduction of loan 3,000.00$

Net Loan Re-Payment 5,500.00$

Notes 5

Cost of Maintainance

Van 1,260.00$

Less: Business use 90% 1,134.00$

SUV 2,050.00$

Less: Business use 60% 1,230.00$

Total cost of Maintainance 2,364.00$

Notes 6

Mobile Bills 704.00$

Less: 90% Business Use 633.60$

Electricity Expenses 1,470.00$

Less: 80% Business Use 1,176.00$

Council Rates 517.00$

Less: 60% Business Use 310.20$

Notes 7

Repairs Expenses 1,780.00$

Add: Shop painting 150.00$

Add: Motor replacement expenses 140.00$

Total Repairs 2,070.00$

Notes 1

Debtors at 1st July 2016 3,925.00$

Debtors Cash Payments 32,800.00$

Debtors at 30th June 2017 3,010.00$

Debtors Net 33,715.00$

Notes 2

Creditors at 1st July 2016 6,500.00$

Add: Repayment to Creditors 1,28,678.00$

Less: Creditors at 30 June 2017 7,010.00$

Creditors Net 1,28,168.00$

Notes 3

Cost of Sales

Stock on 1st July 2016 9,120.00$

Add: Purchase 31,155.00$

Less: Stock on 30th June 2017 9,750.00$

Notes 4 30,525.00$

Loan Repayment

Business Loan 8,500.00$

Less: Reduction of loan 3,000.00$

Net Loan Re-Payment 5,500.00$

Notes 5

Cost of Maintainance

Van 1,260.00$

Less: Business use 90% 1,134.00$

SUV 2,050.00$

Less: Business use 60% 1,230.00$

Total cost of Maintainance 2,364.00$

Notes 6

Mobile Bills 704.00$

Less: 90% Business Use 633.60$

Electricity Expenses 1,470.00$

Less: 80% Business Use 1,176.00$

Council Rates 517.00$

Less: 60% Business Use 310.20$

Notes 7

Repairs Expenses 1,780.00$

Add: Shop painting 150.00$

Add: Motor replacement expenses 140.00$

Total Repairs 2,070.00$

8TAXATION LAW

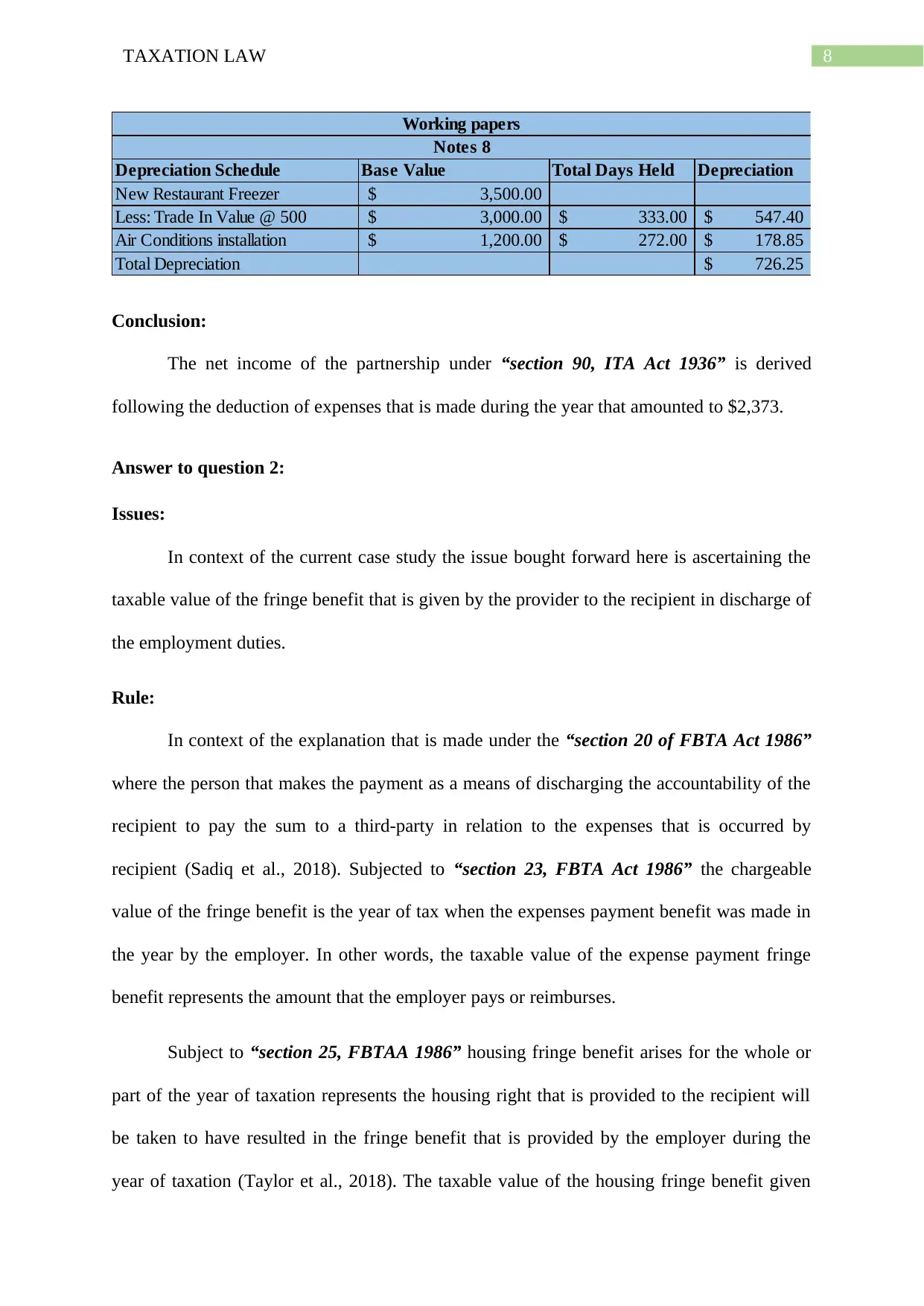

Depreciation Schedule Base Value Total Days Held Depreciation

New Restaurant Freezer 3,500.00$

Less: Trade In Value @ 500 3,000.00$ 333.00$ 547.40$

Air Conditions installation 1,200.00$ 272.00$ 178.85$

Total Depreciation 726.25$

Working papers

Notes 8

Conclusion:

The net income of the partnership under “section 90, ITA Act 1936” is derived

following the deduction of expenses that is made during the year that amounted to $2,373.

Answer to question 2:

Issues:

In context of the current case study the issue bought forward here is ascertaining the

taxable value of the fringe benefit that is given by the provider to the recipient in discharge of

the employment duties.

Rule:

In context of the explanation that is made under the “section 20 of FBTA Act 1986”

where the person that makes the payment as a means of discharging the accountability of the

recipient to pay the sum to a third-party in relation to the expenses that is occurred by

recipient (Sadiq et al., 2018). Subjected to “section 23, FBTA Act 1986” the chargeable

value of the fringe benefit is the year of tax when the expenses payment benefit was made in

the year by the employer. In other words, the taxable value of the expense payment fringe

benefit represents the amount that the employer pays or reimburses.

Subject to “section 25, FBTAA 1986” housing fringe benefit arises for the whole or

part of the year of taxation represents the housing right that is provided to the recipient will

be taken to have resulted in the fringe benefit that is provided by the employer during the

year of taxation (Taylor et al., 2018). The taxable value of the housing fringe benefit given

Depreciation Schedule Base Value Total Days Held Depreciation

New Restaurant Freezer 3,500.00$

Less: Trade In Value @ 500 3,000.00$ 333.00$ 547.40$

Air Conditions installation 1,200.00$ 272.00$ 178.85$

Total Depreciation 726.25$

Working papers

Notes 8

Conclusion:

The net income of the partnership under “section 90, ITA Act 1936” is derived

following the deduction of expenses that is made during the year that amounted to $2,373.

Answer to question 2:

Issues:

In context of the current case study the issue bought forward here is ascertaining the

taxable value of the fringe benefit that is given by the provider to the recipient in discharge of

the employment duties.

Rule:

In context of the explanation that is made under the “section 20 of FBTA Act 1986”

where the person that makes the payment as a means of discharging the accountability of the

recipient to pay the sum to a third-party in relation to the expenses that is occurred by

recipient (Sadiq et al., 2018). Subjected to “section 23, FBTA Act 1986” the chargeable

value of the fringe benefit is the year of tax when the expenses payment benefit was made in

the year by the employer. In other words, the taxable value of the expense payment fringe

benefit represents the amount that the employer pays or reimburses.

Subject to “section 25, FBTAA 1986” housing fringe benefit arises for the whole or

part of the year of taxation represents the housing right that is provided to the recipient will

be taken to have resulted in the fringe benefit that is provided by the employer during the

year of taxation (Taylor et al., 2018). The taxable value of the housing fringe benefit given

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

under the “section 27, FBTA Act 1986” represents the market value of right of using the

accommodations that can be further reduced by the rental payments which is made by

employee.

Application:

In context of the John the employer here as the part of remuneration package paid the

school fees of his child that studied in the private school. As per “sec 20 of FBTA Act 1986”,

the payment made by the employer for John’s child school fees amounts to fringe benefit

(Williams et al., 2017). The employer under “section 23, FBTA Act 1986” will be

accountable for the taxable amount of the expense payment fringe benefit made to John

throughout the FBT year.

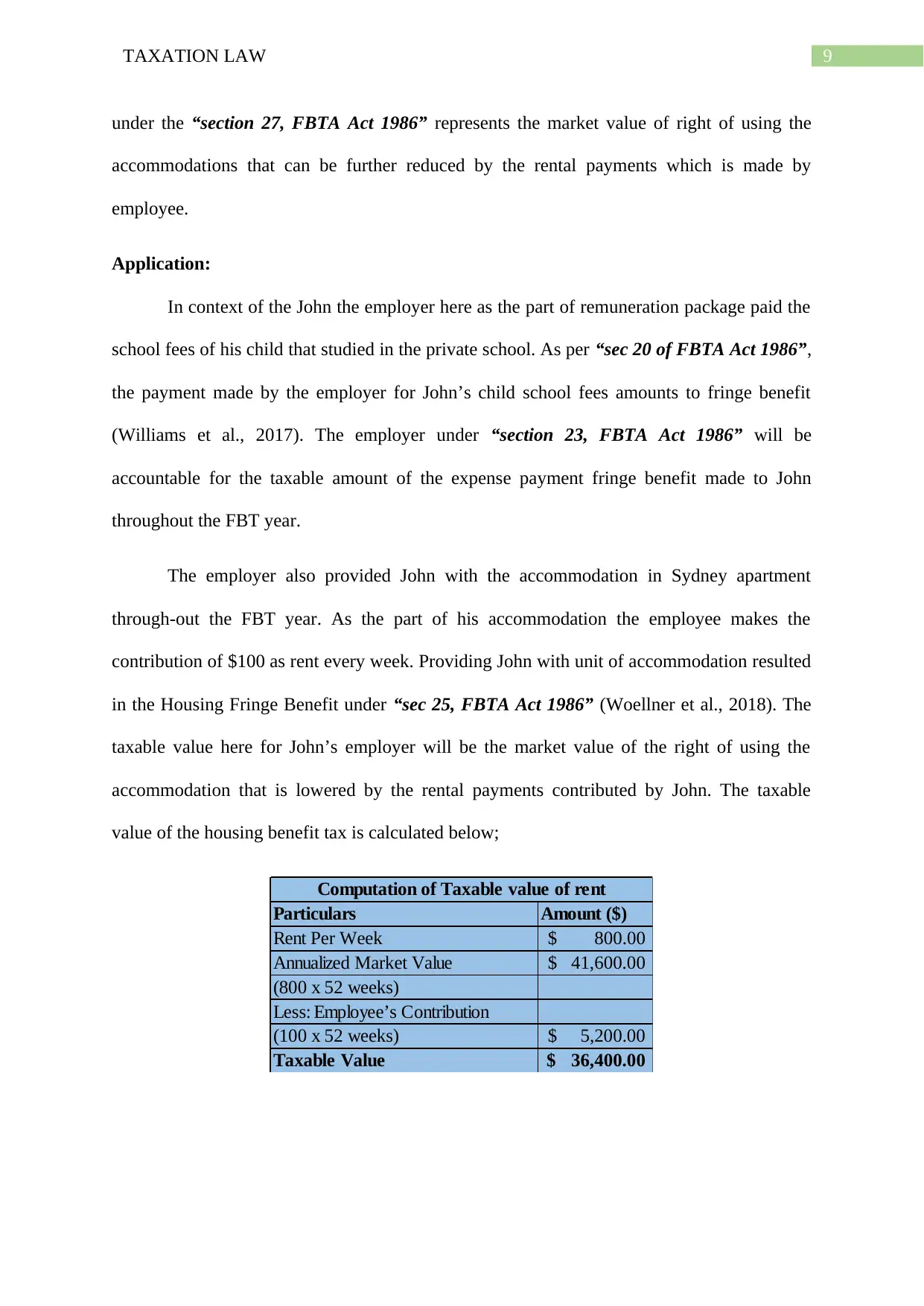

The employer also provided John with the accommodation in Sydney apartment

through-out the FBT year. As the part of his accommodation the employee makes the

contribution of $100 as rent every week. Providing John with unit of accommodation resulted

in the Housing Fringe Benefit under “sec 25, FBTA Act 1986” (Woellner et al., 2018). The

taxable value here for John’s employer will be the market value of the right of using the

accommodation that is lowered by the rental payments contributed by John. The taxable

value of the housing benefit tax is calculated below;

Particulars Amount ($)

Rent Per Week 800.00$

Annualized Market Value 41,600.00$

(800 x 52 weeks)

Less: Employee’s Contribution

(100 x 52 weeks) 5,200.00$

Taxable Value 36,400.00$

Computation of Taxable value of rent

under the “section 27, FBTA Act 1986” represents the market value of right of using the

accommodations that can be further reduced by the rental payments which is made by

employee.

Application:

In context of the John the employer here as the part of remuneration package paid the

school fees of his child that studied in the private school. As per “sec 20 of FBTA Act 1986”,

the payment made by the employer for John’s child school fees amounts to fringe benefit

(Williams et al., 2017). The employer under “section 23, FBTA Act 1986” will be

accountable for the taxable amount of the expense payment fringe benefit made to John

throughout the FBT year.

The employer also provided John with the accommodation in Sydney apartment

through-out the FBT year. As the part of his accommodation the employee makes the

contribution of $100 as rent every week. Providing John with unit of accommodation resulted

in the Housing Fringe Benefit under “sec 25, FBTA Act 1986” (Woellner et al., 2018). The

taxable value here for John’s employer will be the market value of the right of using the

accommodation that is lowered by the rental payments contributed by John. The taxable

value of the housing benefit tax is calculated below;

Particulars Amount ($)

Rent Per Week 800.00$

Annualized Market Value 41,600.00$

(800 x 52 weeks)

Less: Employee’s Contribution

(100 x 52 weeks) 5,200.00$

Taxable Value 36,400.00$

Computation of Taxable value of rent

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Conclusion:

As the employer here paid the school fees of John’s child and also provided an

apartment to John, he will be chargeable for the taxable value of the expense payment benefit

and the market value of the accommodation following the deduction of contribution made by

employee during the FBT year.

Conclusion:

As the employer here paid the school fees of John’s child and also provided an

apartment to John, he will be chargeable for the taxable value of the expense payment benefit

and the market value of the accommodation following the deduction of contribution made by

employee during the FBT year.

11TAXATION LAW

References:

Arnold, B. (2016). International tax primer. The Hague: Kluwer Law International.

Carlisle, L., & Harrington, J. (2017) Basics of international taxation 2017.

Deutsch, R. (2018). Australian tax handbook (2018): THOMSON REUTERS AUSTRALIA.

James, S. (2016). Economics of taxation (2016): Fiscal Publications.

Kenny, P., Blissenden, M., & Villios, S. (2018) Australian Tax.

McCouat, P. (2018) Australian master GST guide.

Raftery, A. (2015) 101 Ways to Save Money on Your Tax - Legally! (2015). Milton:

Wrightbooks.

Richelle, I., Schön, W., & Traversa, E. (2016) State Aid Law and Business Taxation.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., & Obst, W. et al. (2018)

Principles of taxation law 2018.

Taylor, C., Walpole, M., Burton, M., Ciro, T., & Murray, I. (2018) Understanding taxation

law 2018.

Williams, D., Morse, G., Eden, S., & Davies, F. (2017) Davies, principles of tax law.

Woellner, R., Barkoczy, S., & Murphy, S. (2018). Australian Taxation Law 2018 ebook 28e.

Melbourne: OUPANZ.

References:

Arnold, B. (2016). International tax primer. The Hague: Kluwer Law International.

Carlisle, L., & Harrington, J. (2017) Basics of international taxation 2017.

Deutsch, R. (2018). Australian tax handbook (2018): THOMSON REUTERS AUSTRALIA.

James, S. (2016). Economics of taxation (2016): Fiscal Publications.

Kenny, P., Blissenden, M., & Villios, S. (2018) Australian Tax.

McCouat, P. (2018) Australian master GST guide.

Raftery, A. (2015) 101 Ways to Save Money on Your Tax - Legally! (2015). Milton:

Wrightbooks.

Richelle, I., Schön, W., & Traversa, E. (2016) State Aid Law and Business Taxation.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., & Obst, W. et al. (2018)

Principles of taxation law 2018.

Taylor, C., Walpole, M., Burton, M., Ciro, T., & Murray, I. (2018) Understanding taxation

law 2018.

Williams, D., Morse, G., Eden, S., & Davies, F. (2017) Davies, principles of tax law.

Woellner, R., Barkoczy, S., & Murphy, S. (2018). Australian Taxation Law 2018 ebook 28e.

Melbourne: OUPANZ.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.