Taxation Law Assignment: Comprehensive Analysis of Australian Tax Law

VerifiedAdded on 2023/01/24

|12

|2912

|77

Homework Assignment

AI Summary

This taxation law assignment provides a detailed analysis of the Australian tax system, covering various aspects such as the legislative powers of the Commonwealth, the roles of key institutions like the Australian Taxation Office (ATO) and the High Court, and the application of double taxation agreements. The assignment delves into the taxation of business income, capital gains, and post-cessation of business expenses, with practical examples and case studies. It examines the implications of capital gains tax on different scenarios involving property subdivision and sales. Furthermore, the assignment includes an analysis of relevant articles concerning ATO measures for addressing tax avoidance and inequities, highlighting the interplay of tax policies, legislation, and practical application. The document also explores the treatment of CGT, personal use assets, and related expenses. This assignment provides a comprehensive overview of Australian taxation law, offering valuable insights into its complexities and applications.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to A:..........................................................................................................................2

Answer to B:..........................................................................................................................2

Answer to question 2:.................................................................................................................3

Answer to question 3:.................................................................................................................3

Part 1:.....................................................................................................................................3

Answer to A:..........................................................................................................................3

Answer to B:..........................................................................................................................4

Answer to part 2:........................................................................................................................4

Answer to question 4:.................................................................................................................5

Answer to question 5:.................................................................................................................6

Answer to question 6:.................................................................................................................7

Article 1: ATO measures of removing “inequitable” inquiry:...................................................7

Article 1: ATO considers measures for closing gap on multinational Tax Avoidance:........8

Answer to question 7:.................................................................................................................9

References:...............................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to A:..........................................................................................................................2

Answer to B:..........................................................................................................................2

Answer to question 2:.................................................................................................................3

Answer to question 3:.................................................................................................................3

Part 1:.....................................................................................................................................3

Answer to A:..........................................................................................................................3

Answer to B:..........................................................................................................................4

Answer to part 2:........................................................................................................................4

Answer to question 4:.................................................................................................................5

Answer to question 5:.................................................................................................................6

Answer to question 6:.................................................................................................................7

Article 1: ATO measures of removing “inequitable” inquiry:...................................................7

Article 1: ATO considers measures for closing gap on multinational Tax Avoidance:........8

Answer to question 7:.................................................................................................................9

References:...............................................................................................................................10

2TAXATION LAW

Answer to question 1:

Answer to A:

Australian is viewed as the federation and its legislative power is widespread between

the commonwealth and states. Referring to “Section 51 (ii)” the commonwealth power are

given under this section. This “Section 51 (ii)” provides commonwealth with the permission

of making laws in respect to tax but does not requires making discrimination among the states

or any parts of states (Miller & Oats, 2016). The commonwealth board has the power of

imposing tax which must be considered as substance to the commencement of “Section 51”

that explains the right of making power and are subject to constitutions. The exclusive power

of applying tax on customs and excise duties by Commonwealth is given under “section 90”.

Answer to B:

The progress of tax policy rests with Australian government and the treasury minister

is responsible for its application. The Australian taxation office plays the vital role in the

formation of tax policy and legislation process that reflects the interdependence of laws,

policy and managerial aspects of tax system (Gamage & Livingston, 2018). The primary role

of ATO is to administer tax and laws relating to superannuation which the parliament passes.

To execute this, the administrative arrangement of applying taxation law is developed by the

ATO which also includes educating and advising the taxpayers relating to their duties and

rights.

The High Court of Australia plays an important role of interpreting and applying the

tax in Australia to determine the cases that have specific federal significances along with

challenges of constitutional validity of law and hearing the appeals of territory courts, federal

and state courts. The parliament consists of lower and upper houses and the parliamentary

Answer to question 1:

Answer to A:

Australian is viewed as the federation and its legislative power is widespread between

the commonwealth and states. Referring to “Section 51 (ii)” the commonwealth power are

given under this section. This “Section 51 (ii)” provides commonwealth with the permission

of making laws in respect to tax but does not requires making discrimination among the states

or any parts of states (Miller & Oats, 2016). The commonwealth board has the power of

imposing tax which must be considered as substance to the commencement of “Section 51”

that explains the right of making power and are subject to constitutions. The exclusive power

of applying tax on customs and excise duties by Commonwealth is given under “section 90”.

Answer to B:

The progress of tax policy rests with Australian government and the treasury minister

is responsible for its application. The Australian taxation office plays the vital role in the

formation of tax policy and legislation process that reflects the interdependence of laws,

policy and managerial aspects of tax system (Gamage & Livingston, 2018). The primary role

of ATO is to administer tax and laws relating to superannuation which the parliament passes.

To execute this, the administrative arrangement of applying taxation law is developed by the

ATO which also includes educating and advising the taxpayers relating to their duties and

rights.

The High Court of Australia plays an important role of interpreting and applying the

tax in Australia to determine the cases that have specific federal significances along with

challenges of constitutional validity of law and hearing the appeals of territory courts, federal

and state courts. The parliament consists of lower and upper houses and the parliamentary

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

bills must be passed through parliament (Butler, 2019). The lower house introduces the bills

of taxation to parliament and those bills is processed to upper house so that it can be passed.

Answer to question 2:

As per the Double Taxation Agreement amid Australia and US, the profits made by

one contracting states would be levied taxes only in that state only unless the company

carrying out the business in different contracting nations through permanent establishment. If

an enterprise performs the business as mentioned above, the profits made by business would

attract tax liability only in other state up to the extent that is attributable to permanent

establishment (Schön, 2016). As per “section 6-5, ITAA 1997”, an Australian tax resident

should pay taxes on income made from all the sources however, “section 6-10, ITAA 1997”

requires a non-resident to pay tax only on the income sourced from Australia.

A company is viewed as Australian resident company if the company is performing

business in Australia having its central management and control in Australia. Generally,

income from business is held taxable where the transactions are carried out. The taxation

commissioner in “C of T (NSW) v Hillsdon Watts Ltd (1937)” explained that income from

business originates where the business is actually carried on (Picciotto, 2015). Conversely, it

represents those place where the contract is carried out and regarded as the only applicable

factor in ascertaining the source. Referring to Double Taxation Agreement profits made from

the Australian sourced sales by the US manufacturer will be taxable in Australia for the US

based manufacturer since the profits are sourced in Australia.

bills must be passed through parliament (Butler, 2019). The lower house introduces the bills

of taxation to parliament and those bills is processed to upper house so that it can be passed.

Answer to question 2:

As per the Double Taxation Agreement amid Australia and US, the profits made by

one contracting states would be levied taxes only in that state only unless the company

carrying out the business in different contracting nations through permanent establishment. If

an enterprise performs the business as mentioned above, the profits made by business would

attract tax liability only in other state up to the extent that is attributable to permanent

establishment (Schön, 2016). As per “section 6-5, ITAA 1997”, an Australian tax resident

should pay taxes on income made from all the sources however, “section 6-10, ITAA 1997”

requires a non-resident to pay tax only on the income sourced from Australia.

A company is viewed as Australian resident company if the company is performing

business in Australia having its central management and control in Australia. Generally,

income from business is held taxable where the transactions are carried out. The taxation

commissioner in “C of T (NSW) v Hillsdon Watts Ltd (1937)” explained that income from

business originates where the business is actually carried on (Picciotto, 2015). Conversely, it

represents those place where the contract is carried out and regarded as the only applicable

factor in ascertaining the source. Referring to Double Taxation Agreement profits made from

the Australian sourced sales by the US manufacturer will be taxable in Australia for the US

based manufacturer since the profits are sourced in Australia.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Answer to question 3:

Part 1:

Answer to A:

Capital gains is usually implemented on the assets that are bought or events that are

taking place after the 20th September 1985. Accordingly, the term Pre-CGT and Post-CGT

asset is usually implemented on the assets that are bought or events that are taking place prior

to or after the date. If Indiana undertakes the decision of sub-dividing the property in 80 lots

and then sell off the sub-divided lots, then any capital gains made thereon will be treated

assessable profit making undertaking (Mumford, 2017). However, if the land is bought before

the introduction of CGT event then the land will be exempted from the capital gains tax

because it is regarded as the pre-CGT asset and any gains made from the disposal of land will

not be attract capital gains tax.

Answer to B:

If in the alternative situation Indiana purchases the land on 1st November 1986 and

disposes the subdivided undeveloped lot to property developer, then in such situation the

probable revenue provision should be applied. It is assumed that land should not be

considered as trading stock and the profits derived from the sales will be included as taxable

income under “section 6-5, ITAA 1997”.

In an alternative option if Indiana undertakes the decision of holding auction for 80

lots of land in the form of separate packages to the highest bidder then the subdivided block

of land will be considered as trading stock. The profits that would be made from disposal of

80 lots would attract tax liability under “section 6-5, ITAA 1997”.

In the final option if Indiana does not take the decision of subdividing the land and

rather decides to sale the land completely to the property developer company then the sale of

Answer to question 3:

Part 1:

Answer to A:

Capital gains is usually implemented on the assets that are bought or events that are

taking place after the 20th September 1985. Accordingly, the term Pre-CGT and Post-CGT

asset is usually implemented on the assets that are bought or events that are taking place prior

to or after the date. If Indiana undertakes the decision of sub-dividing the property in 80 lots

and then sell off the sub-divided lots, then any capital gains made thereon will be treated

assessable profit making undertaking (Mumford, 2017). However, if the land is bought before

the introduction of CGT event then the land will be exempted from the capital gains tax

because it is regarded as the pre-CGT asset and any gains made from the disposal of land will

not be attract capital gains tax.

Answer to B:

If in the alternative situation Indiana purchases the land on 1st November 1986 and

disposes the subdivided undeveloped lot to property developer, then in such situation the

probable revenue provision should be applied. It is assumed that land should not be

considered as trading stock and the profits derived from the sales will be included as taxable

income under “section 6-5, ITAA 1997”.

In an alternative option if Indiana undertakes the decision of holding auction for 80

lots of land in the form of separate packages to the highest bidder then the subdivided block

of land will be considered as trading stock. The profits that would be made from disposal of

80 lots would attract tax liability under “section 6-5, ITAA 1997”.

In the final option if Indiana does not take the decision of subdividing the land and

rather decides to sale the land completely to the property developer company then the sale of

5TAXATION LAW

land would be treated as the capital asset that will be subjected to capital gains tax (Yang &

Metallo, 2018). The profits would be considered taxable as the ordinary income and will also

be the subject of GST as well.

Answer to part 2:

Option A:

Given the projected subdivision by Indiana goes beyond the mere realisation of

capital asset then it would be considered as profit making undertaking and it will be treated as

carrying the business of land development. Selling of subdivided 80 block of land will result

in treating the land as capital asset rather than the capital asset and the profits would be

considered taxable under the ordinary meaning of “section 6-5, ITAA 1997”.

Option B:

If Indiana undertakes the identical activity by holding the action of 80 lots of land,

then the land being the capital asset would be regarded as carrying the business of land

development. The subdivided 80 blocks of land will be considered as the trading stock

starting from the date when the business commenced. Indiana is assumed to have disposed

the 80 lots based on the market value (Picciotto, 2019). The taxpayer in the current situation

would be regarded taxable because the taxpayer has undertaken commercial approach to

dispose the land with the intention of making profit. The income derived would be considered

taxable under the ordinary concepts of “section 6-5, ITAA 1997”.

Option C:

If Indiana undertook the decision of subdividing the land and selling it to the property

development company, then any profits made thereon is taxable as ordinary income.

land would be treated as the capital asset that will be subjected to capital gains tax (Yang &

Metallo, 2018). The profits would be considered taxable as the ordinary income and will also

be the subject of GST as well.

Answer to part 2:

Option A:

Given the projected subdivision by Indiana goes beyond the mere realisation of

capital asset then it would be considered as profit making undertaking and it will be treated as

carrying the business of land development. Selling of subdivided 80 block of land will result

in treating the land as capital asset rather than the capital asset and the profits would be

considered taxable under the ordinary meaning of “section 6-5, ITAA 1997”.

Option B:

If Indiana undertakes the identical activity by holding the action of 80 lots of land,

then the land being the capital asset would be regarded as carrying the business of land

development. The subdivided 80 blocks of land will be considered as the trading stock

starting from the date when the business commenced. Indiana is assumed to have disposed

the 80 lots based on the market value (Picciotto, 2019). The taxpayer in the current situation

would be regarded taxable because the taxpayer has undertaken commercial approach to

dispose the land with the intention of making profit. The income derived would be considered

taxable under the ordinary concepts of “section 6-5, ITAA 1997”.

Option C:

If Indiana undertook the decision of subdividing the land and selling it to the property

development company, then any profits made thereon is taxable as ordinary income.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Answer to question 4:

Post cessation of business expenses is held as allowable deduction provided the event

of loss or expenses is occurred during business operations which was earlier performed by the

taxpayer for producing taxable income. The federal court in “FCT v Placer Pacific

Management Pty Ltd (1995)” explained that the taxpayer is permitted to obtain tax deduction

for outgoings occurred in settlement of dispute with customer for the faulty supply of

conveyor belt (Graetz & Warren, 2016). The expenditure was regarded as outgoing that was

occurred by taxpayer in producing the assessable income from business. The taxation

commissioner held the expense deductible because it was regarded as business arrangement

which was entered by taxpayer and the customer.

In the current case of Amity, an allowable deduction can be claimed by her for

interest on loan under “section 8-1, ITAA 1997” as the outgoing was occurred for loan

agreement and also for producing taxable income.

Answer to question 5:

Capital gains tax is implemented on assets that is purchased on or after the 20th

September 1985. A CGT event A1 takes place under “section 104-10 (1)) of the ITAA 1997”

when the asset is sold (Butler, 2019). The main residence of taxpayer is exempted from CGT.

However, to get exemption, there must be dwelling on the property. Maurice bought a home

for $140,000 and was sold on 1st March 325,000. Maurice did not used the home to generate

income and she can claim full main residence exemption.

She also bought FUL shares for $15,000 in 1984 that was eventually disposed for

$19,000 on 15th March. The shares purchased by Maurice should be viewed as pre-CGT asset

that is exempted from CGT. Personal use asset under “section 108-20 (2), ITAA 1997”

implies asset that are kept by the taxpayer for private usage and enjoyment (Morgan et al.,

Answer to question 4:

Post cessation of business expenses is held as allowable deduction provided the event

of loss or expenses is occurred during business operations which was earlier performed by the

taxpayer for producing taxable income. The federal court in “FCT v Placer Pacific

Management Pty Ltd (1995)” explained that the taxpayer is permitted to obtain tax deduction

for outgoings occurred in settlement of dispute with customer for the faulty supply of

conveyor belt (Graetz & Warren, 2016). The expenditure was regarded as outgoing that was

occurred by taxpayer in producing the assessable income from business. The taxation

commissioner held the expense deductible because it was regarded as business arrangement

which was entered by taxpayer and the customer.

In the current case of Amity, an allowable deduction can be claimed by her for

interest on loan under “section 8-1, ITAA 1997” as the outgoing was occurred for loan

agreement and also for producing taxable income.

Answer to question 5:

Capital gains tax is implemented on assets that is purchased on or after the 20th

September 1985. A CGT event A1 takes place under “section 104-10 (1)) of the ITAA 1997”

when the asset is sold (Butler, 2019). The main residence of taxpayer is exempted from CGT.

However, to get exemption, there must be dwelling on the property. Maurice bought a home

for $140,000 and was sold on 1st March 325,000. Maurice did not used the home to generate

income and she can claim full main residence exemption.

She also bought FUL shares for $15,000 in 1984 that was eventually disposed for

$19,000 on 15th March. The shares purchased by Maurice should be viewed as pre-CGT asset

that is exempted from CGT. Personal use asset under “section 108-20 (2), ITAA 1997”

implies asset that are kept by the taxpayer for private usage and enjoyment (Morgan et al.,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

2018). Whereas, “section 118-10 (3), ITAA 1997” explains that capital gains or loss must be

ignored when the cost base of personal use asset is less than $10,000. Maurice also purchased

the furniture at a cost of $9,500 for 20th May that was disposed on 1st May for 2018 for

$5,000. Consequently, the capital loss that is derived from the disposal of furniture must be

ignored by Maurice because the cost of assets is less than $10,000.

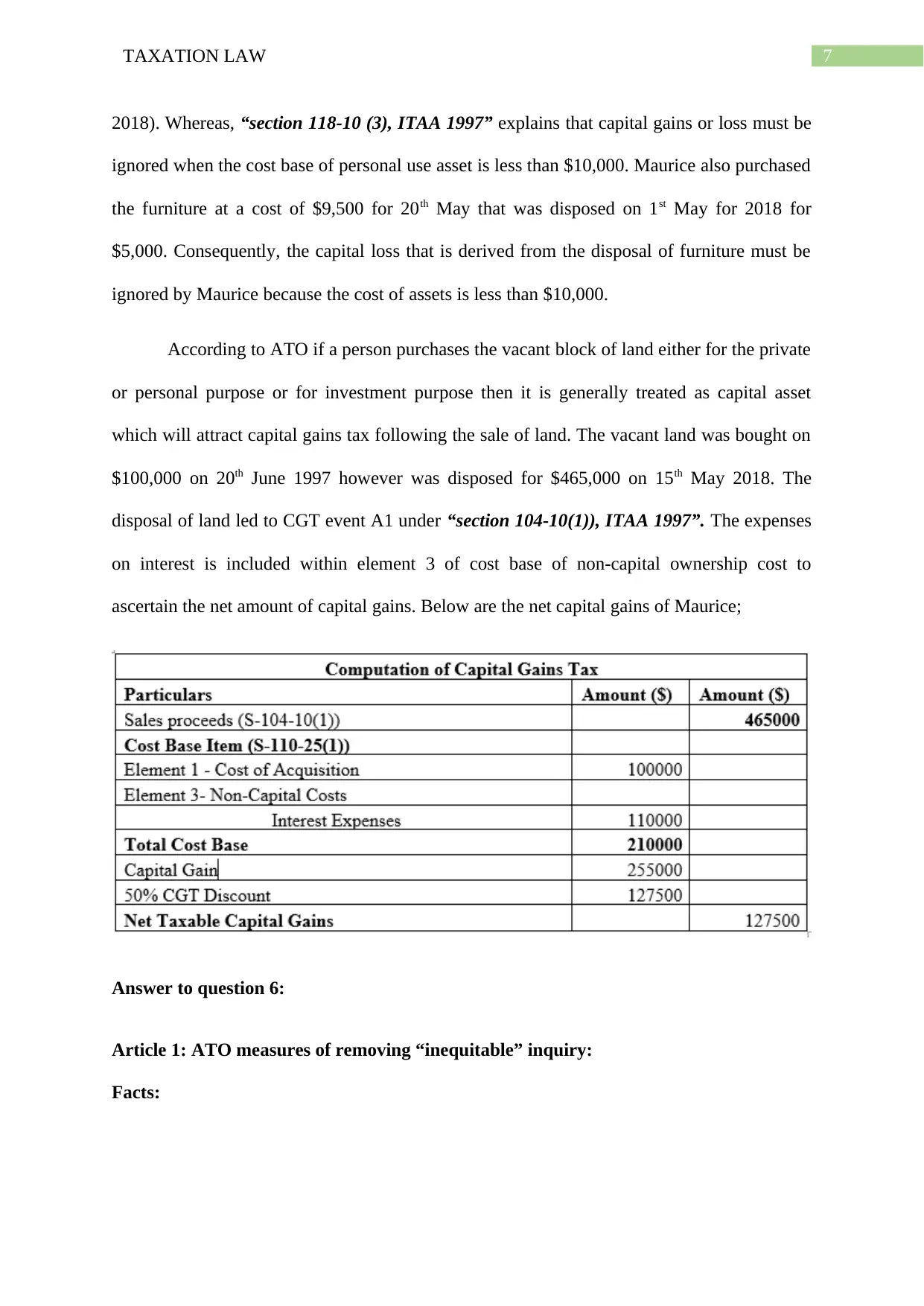

According to ATO if a person purchases the vacant block of land either for the private

or personal purpose or for investment purpose then it is generally treated as capital asset

which will attract capital gains tax following the sale of land. The vacant land was bought on

$100,000 on 20th June 1997 however was disposed for $465,000 on 15th May 2018. The

disposal of land led to CGT event A1 under “section 104-10(1)), ITAA 1997”. The expenses

on interest is included within element 3 of cost base of non-capital ownership cost to

ascertain the net amount of capital gains. Below are the net capital gains of Maurice;

Answer to question 6:

Article 1: ATO measures of removing “inequitable” inquiry:

Facts:

2018). Whereas, “section 118-10 (3), ITAA 1997” explains that capital gains or loss must be

ignored when the cost base of personal use asset is less than $10,000. Maurice also purchased

the furniture at a cost of $9,500 for 20th May that was disposed on 1st May for 2018 for

$5,000. Consequently, the capital loss that is derived from the disposal of furniture must be

ignored by Maurice because the cost of assets is less than $10,000.

According to ATO if a person purchases the vacant block of land either for the private

or personal purpose or for investment purpose then it is generally treated as capital asset

which will attract capital gains tax following the sale of land. The vacant land was bought on

$100,000 on 20th June 1997 however was disposed for $465,000 on 15th May 2018. The

disposal of land led to CGT event A1 under “section 104-10(1)), ITAA 1997”. The expenses

on interest is included within element 3 of cost base of non-capital ownership cost to

ascertain the net amount of capital gains. Below are the net capital gains of Maurice;

Answer to question 6:

Article 1: ATO measures of removing “inequitable” inquiry:

Facts:

8TAXATION LAW

Labour has proposed removing the refundable franking credit for individuals and self-

managed super funds which the parliamentary found inequitable and highly flawed (Afr.com,

2019). The committee has taken into the account the situation of removal of refundable

franking credits for individuals and the SMSF. The commissioner considers the policy

inequitable and highly flawed.

Concise explanation of taxation concepts:

The committee has recommended the removal of refundable franking credit may

unfairly create an effect on the modest incomes that are already retired and those that are not

likely be able to return to workforce in order to cover the lost income. The report however

recommends that such kind of policy reformation may only be treated as the portion of

equitable package for the purpose of wholesale tax reformation.

Explanation of connection between concepts and indicators of good tax policy:

The members of labour in Parliament has stated its criticism following the inquiry and

have reported that the entire exercise is a waste of taxpayer’s money (Afr.com, 2019). The

article clearly explains that the policy is not fair to those earn moderate income.

Article 1: ATO considers measures for closing gap on multinational Tax Avoidance:

Facts:

A special tax avoidance taskforce is run by the ATO and has recovered greater than

$8 billion from the foreign-owned multinational companies. The new estimation suggests that

greater than 95 per cent of largest companies are new meeting their entire liabilities in

Australia (Afr.com, 2019). The article suggest that taxpayers presently paid around 29% of

all the company tax while 42% of tax is obtained from top 100 companies.

Concise explanation of taxation concepts:

Labour has proposed removing the refundable franking credit for individuals and self-

managed super funds which the parliamentary found inequitable and highly flawed (Afr.com,

2019). The committee has taken into the account the situation of removal of refundable

franking credits for individuals and the SMSF. The commissioner considers the policy

inequitable and highly flawed.

Concise explanation of taxation concepts:

The committee has recommended the removal of refundable franking credit may

unfairly create an effect on the modest incomes that are already retired and those that are not

likely be able to return to workforce in order to cover the lost income. The report however

recommends that such kind of policy reformation may only be treated as the portion of

equitable package for the purpose of wholesale tax reformation.

Explanation of connection between concepts and indicators of good tax policy:

The members of labour in Parliament has stated its criticism following the inquiry and

have reported that the entire exercise is a waste of taxpayer’s money (Afr.com, 2019). The

article clearly explains that the policy is not fair to those earn moderate income.

Article 1: ATO considers measures for closing gap on multinational Tax Avoidance:

Facts:

A special tax avoidance taskforce is run by the ATO and has recovered greater than

$8 billion from the foreign-owned multinational companies. The new estimation suggests that

greater than 95 per cent of largest companies are new meeting their entire liabilities in

Australia (Afr.com, 2019). The article suggest that taxpayers presently paid around 29% of

all the company tax while 42% of tax is obtained from top 100 companies.

Concise explanation of taxation concepts:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

As per the article the tax gap that was released in last year represents the trend that the

gap is reducing (Afr.com, 2019). There is a significant improvement in tax gap as around

1500 largest companies pay approximately $44 billion as tax revenue each year in Australia.

Explanation of connection between concepts and indicators of good tax policy:

The article explains that the present compliance may be greater in Australia’s

corporate companies, together with new multinational tax avoidance laws, country-by-

country tax reporting and anti-hybrid laws and have also updated the rules relating to transfer

pricing.

Answer to question 7:

The role of tax advisor comprises of assuring the clients to adhere with the necessary

laws of tax which are as follows;

a. The tax practitioner assists the clients in managing their taxation affairs by allowing

them to assure that their clients are able to understand their duties and rights.

b. The advisors play a vital role in leveraging point for customers in the form of vital

intermediary for tax and superannuation system.

c. The tax agents play the vital role in encouraging compliance amid the clients through

improved risks and compliance strategies for better information and exchange of ideas

with clients.

As per the article the tax gap that was released in last year represents the trend that the

gap is reducing (Afr.com, 2019). There is a significant improvement in tax gap as around

1500 largest companies pay approximately $44 billion as tax revenue each year in Australia.

Explanation of connection between concepts and indicators of good tax policy:

The article explains that the present compliance may be greater in Australia’s

corporate companies, together with new multinational tax avoidance laws, country-by-

country tax reporting and anti-hybrid laws and have also updated the rules relating to transfer

pricing.

Answer to question 7:

The role of tax advisor comprises of assuring the clients to adhere with the necessary

laws of tax which are as follows;

a. The tax practitioner assists the clients in managing their taxation affairs by allowing

them to assure that their clients are able to understand their duties and rights.

b. The advisors play a vital role in leveraging point for customers in the form of vital

intermediary for tax and superannuation system.

c. The tax agents play the vital role in encouraging compliance amid the clients through

improved risks and compliance strategies for better information and exchange of ideas

with clients.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

ATO closing the gap on multinational tax avoidance. (2019). Retrieved from

https://www.afr.com/personal-finance/tax/ato-closing-the-gap-on-multinational-tax-

avoidance-20190318-p51577

Butler, D. (2019). Who can provide taxation advice?. Taxation in Australia, 53(7), 381.

Butler, D. (2019). Who can provide taxation advice?. Taxation in Australia, 53(7), 381.

Chapter 7: Tax practitioners and advisors | Inspector-General of Taxation. (2019). Retrieved

from http://igt.gov.au/publications/reports-of-reviews/use-of-compliance-risk-

assessment-tools/chapter-7-tax-practitioners-and-advisors/#P2035_307929

Franking credit removal 'inequitable': inquiry. (2019). Retrieved from

https://www.afr.com/personal-finance/tax/franking-credit-removal-inequitable-and-

deeply-flawed-inquiry-20190404-p51az9

Freudenberg, B., Chardon, T., Brimble, M., & Isle, M. B. (2017). Tax literacy of Australian

small businesses. J. Austl. Tax'n, 19, 21.

Gamage, D., & Livingston, M. A. (2018). Taxation: Law, Planning.

Graetz, M. J., & Warren, A. C. (2016). Integration of corporate and shareholder

taxes. National Tax Journal, Forthcoming, 16-36.

Miller, A., & Oats, L. (2016). Principles of international taxation. Bloomsbury Publishing.

Morgan, A., Mortimer, C., & Pinto, D. (2018). A practical introduction to Australian

taxation law 2018. Oxford University Press.

Mumford, A. (2017). Taxing culture: towards a theory of tax collection law. Routledge.

References:

ATO closing the gap on multinational tax avoidance. (2019). Retrieved from

https://www.afr.com/personal-finance/tax/ato-closing-the-gap-on-multinational-tax-

avoidance-20190318-p51577

Butler, D. (2019). Who can provide taxation advice?. Taxation in Australia, 53(7), 381.

Butler, D. (2019). Who can provide taxation advice?. Taxation in Australia, 53(7), 381.

Chapter 7: Tax practitioners and advisors | Inspector-General of Taxation. (2019). Retrieved

from http://igt.gov.au/publications/reports-of-reviews/use-of-compliance-risk-

assessment-tools/chapter-7-tax-practitioners-and-advisors/#P2035_307929

Franking credit removal 'inequitable': inquiry. (2019). Retrieved from

https://www.afr.com/personal-finance/tax/franking-credit-removal-inequitable-and-

deeply-flawed-inquiry-20190404-p51az9

Freudenberg, B., Chardon, T., Brimble, M., & Isle, M. B. (2017). Tax literacy of Australian

small businesses. J. Austl. Tax'n, 19, 21.

Gamage, D., & Livingston, M. A. (2018). Taxation: Law, Planning.

Graetz, M. J., & Warren, A. C. (2016). Integration of corporate and shareholder

taxes. National Tax Journal, Forthcoming, 16-36.

Miller, A., & Oats, L. (2016). Principles of international taxation. Bloomsbury Publishing.

Morgan, A., Mortimer, C., & Pinto, D. (2018). A practical introduction to Australian

taxation law 2018. Oxford University Press.

Mumford, A. (2017). Taxing culture: towards a theory of tax collection law. Routledge.

11TAXATION LAW

Picciotto, S. (2015). Indeterminacy, complexity, technocracy and the reform of international

corporate taxation. Social & Legal Studies, 24(2), 165-184.

Picciotto, S. (2019). Constructing compliance: Game-playing, tax law and the State.

Schön, W. (2016). Destination-Based Income Taxation and WTO Law: A Note.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C., & Pinto, D. (2016). Australian Taxation

Law 2016. OUP Catalogue.

Yang, J., & Metallo, V. (2018). The Emerging International Taxation

Problems. International Journal of Financial Studies, 6(1), 6.

Picciotto, S. (2015). Indeterminacy, complexity, technocracy and the reform of international

corporate taxation. Social & Legal Studies, 24(2), 165-184.

Picciotto, S. (2019). Constructing compliance: Game-playing, tax law and the State.

Schön, W. (2016). Destination-Based Income Taxation and WTO Law: A Note.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C., & Pinto, D. (2016). Australian Taxation

Law 2016. OUP Catalogue.

Yang, J., & Metallo, V. (2018). The Emerging International Taxation

Problems. International Journal of Financial Studies, 6(1), 6.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.