Calculation of Net Income and Fringe Benefit Tax

VerifiedAdded on 2020/10/22

|9

|2184

|127

AI Summary

The provided assignment involves two main parts: calculation of net income for the partnership of Daniel and Olivia Smith, and calculation of Fringe Benefit Tax (FBT) for the employer of John who provides him with a taxable value of AUS $ 15000 for children's private school fees and accommodation rent. The assignment requires applying relevant tax laws and regulations to determine the FBT payable by the employer on behalf of John.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Taxation Theory, Practice

and Law

and Law

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

QUESTION 1 Calculation of net income of partnership firm.........................................................3

QUESTION 2 Fringe Benefits Tax Consequences of John's Remuneration Package By its

Employer..........................................................................................................................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................3

QUESTION 1 Calculation of net income of partnership firm.........................................................3

QUESTION 2 Fringe Benefits Tax Consequences of John's Remuneration Package By its

Employer..........................................................................................................................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

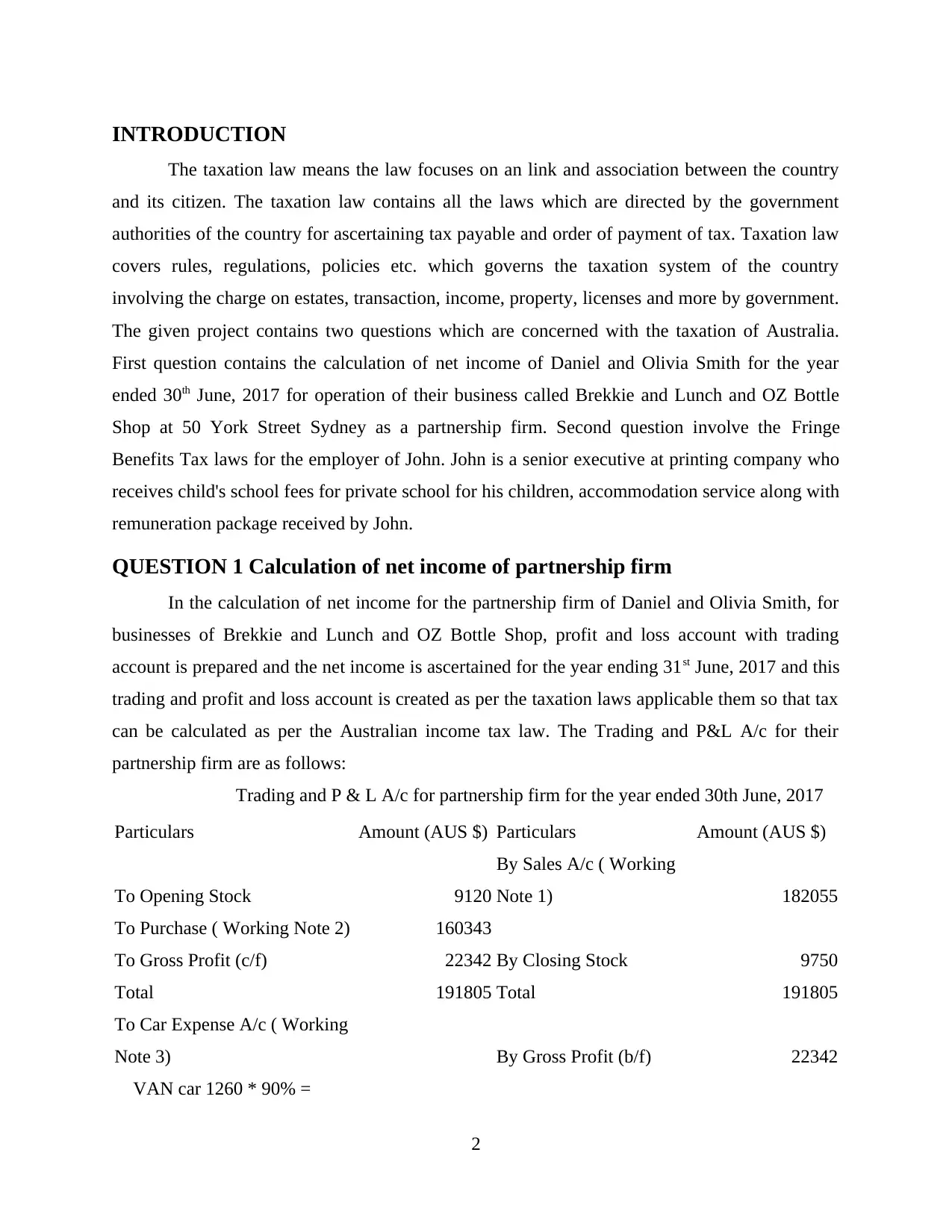

INTRODUCTION

The taxation law means the law focuses on an link and association between the country

and its citizen. The taxation law contains all the laws which are directed by the government

authorities of the country for ascertaining tax payable and order of payment of tax. Taxation law

covers rules, regulations, policies etc. which governs the taxation system of the country

involving the charge on estates, transaction, income, property, licenses and more by government.

The given project contains two questions which are concerned with the taxation of Australia.

First question contains the calculation of net income of Daniel and Olivia Smith for the year

ended 30th June, 2017 for operation of their business called Brekkie and Lunch and OZ Bottle

Shop at 50 York Street Sydney as a partnership firm. Second question involve the Fringe

Benefits Tax laws for the employer of John. John is a senior executive at printing company who

receives child's school fees for private school for his children, accommodation service along with

remuneration package received by John.

QUESTION 1 Calculation of net income of partnership firm

In the calculation of net income for the partnership firm of Daniel and Olivia Smith, for

businesses of Brekkie and Lunch and OZ Bottle Shop, profit and loss account with trading

account is prepared and the net income is ascertained for the year ending 31st June, 2017 and this

trading and profit and loss account is created as per the taxation laws applicable them so that tax

can be calculated as per the Australian income tax law. The Trading and P&L A/c for their

partnership firm are as follows:

Trading and P & L A/c for partnership firm for the year ended 30th June, 2017

Particulars Amount (AUS $) Particulars Amount (AUS $)

To Opening Stock 9120

By Sales A/c ( Working

Note 1) 182055

To Purchase ( Working Note 2) 160343

To Gross Profit (c/f) 22342 By Closing Stock 9750

Total 191805 Total 191805

To Car Expense A/c ( Working

Note 3) By Gross Profit (b/f) 22342

VAN car 1260 * 90% =

2

The taxation law means the law focuses on an link and association between the country

and its citizen. The taxation law contains all the laws which are directed by the government

authorities of the country for ascertaining tax payable and order of payment of tax. Taxation law

covers rules, regulations, policies etc. which governs the taxation system of the country

involving the charge on estates, transaction, income, property, licenses and more by government.

The given project contains two questions which are concerned with the taxation of Australia.

First question contains the calculation of net income of Daniel and Olivia Smith for the year

ended 30th June, 2017 for operation of their business called Brekkie and Lunch and OZ Bottle

Shop at 50 York Street Sydney as a partnership firm. Second question involve the Fringe

Benefits Tax laws for the employer of John. John is a senior executive at printing company who

receives child's school fees for private school for his children, accommodation service along with

remuneration package received by John.

QUESTION 1 Calculation of net income of partnership firm

In the calculation of net income for the partnership firm of Daniel and Olivia Smith, for

businesses of Brekkie and Lunch and OZ Bottle Shop, profit and loss account with trading

account is prepared and the net income is ascertained for the year ending 31st June, 2017 and this

trading and profit and loss account is created as per the taxation laws applicable them so that tax

can be calculated as per the Australian income tax law. The Trading and P&L A/c for their

partnership firm are as follows:

Trading and P & L A/c for partnership firm for the year ended 30th June, 2017

Particulars Amount (AUS $) Particulars Amount (AUS $)

To Opening Stock 9120

By Sales A/c ( Working

Note 1) 182055

To Purchase ( Working Note 2) 160343

To Gross Profit (c/f) 22342 By Closing Stock 9750

Total 191805 Total 191805

To Car Expense A/c ( Working

Note 3) By Gross Profit (b/f) 22342

VAN car 1260 * 90% =

2

1134

SUV car 2050 * 60% =

1230 2364

To Electricity Expenses A/c

( 1470 * 80%) (W / N 4) 1176

To Council Rates A/c ( 517 *

60%) (W / N 4) 310

To Business Insurance

Expenses A/c 1250

To Mobile Bill Expenses A/c

(704 * 90%) (W / N 4) 634

To Union Bill Expenses A/c 284

To Account Charges A/c

( ANZ Bank) 595

To Repair Expenses A/c 1490

Air condition installation 1200

Shop painting 150

Refrigerator motor replacement

140

To Interest on loan A/c ( W/N

7) 5500

Loan Repayment 8500

Less: Principal amount 3000

To Depreciation A/c ( W/N 5

and 6) 250

New Restaurant freezer

(3500 – 500) / 12 years

To Net Profit 8489

Total 22342 Total 22342

3

SUV car 2050 * 60% =

1230 2364

To Electricity Expenses A/c

( 1470 * 80%) (W / N 4) 1176

To Council Rates A/c ( 517 *

60%) (W / N 4) 310

To Business Insurance

Expenses A/c 1250

To Mobile Bill Expenses A/c

(704 * 90%) (W / N 4) 634

To Union Bill Expenses A/c 284

To Account Charges A/c

( ANZ Bank) 595

To Repair Expenses A/c 1490

Air condition installation 1200

Shop painting 150

Refrigerator motor replacement

140

To Interest on loan A/c ( W/N

7) 5500

Loan Repayment 8500

Less: Principal amount 3000

To Depreciation A/c ( W/N 5

and 6) 250

New Restaurant freezer

(3500 – 500) / 12 years

To Net Profit 8489

Total 22342 Total 22342

3

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

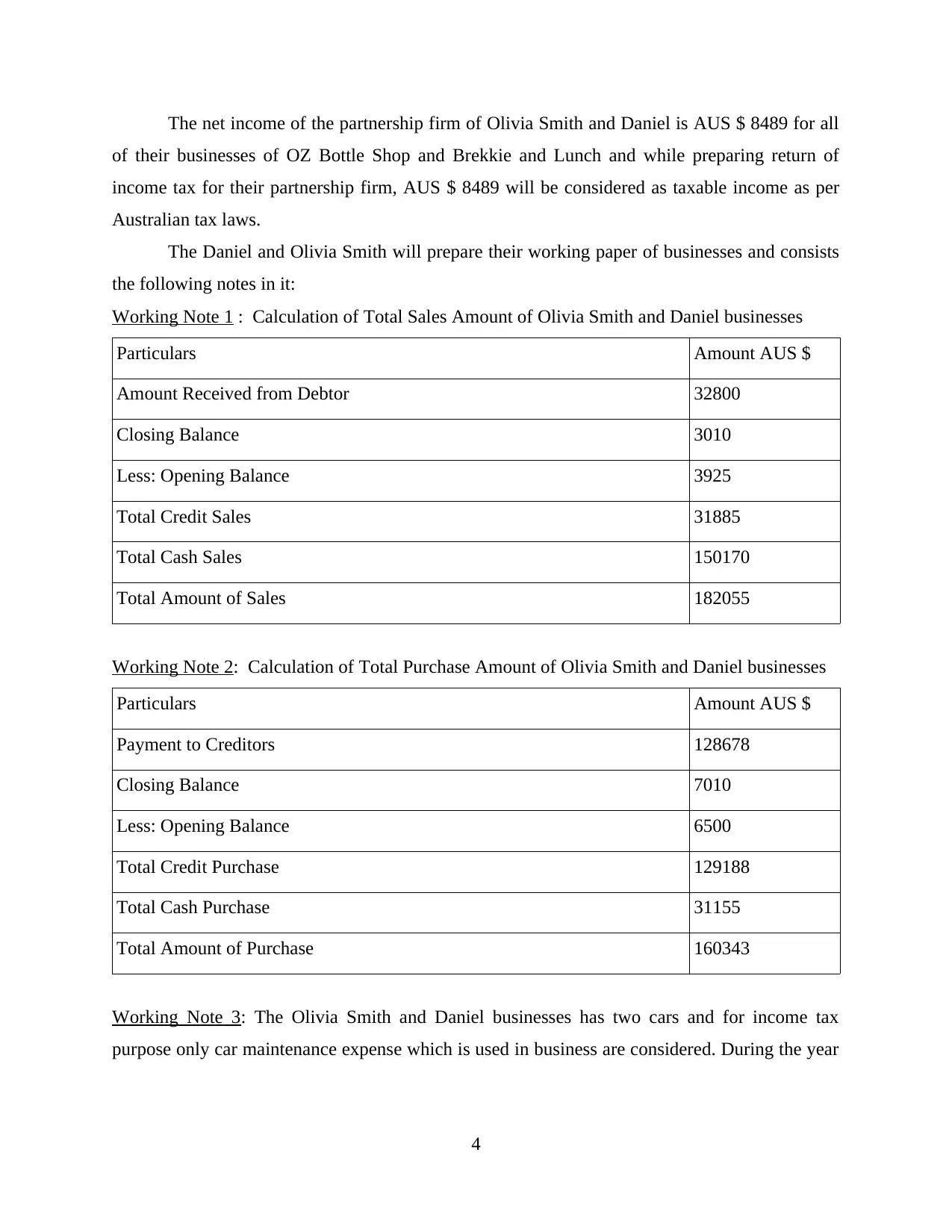

The net income of the partnership firm of Olivia Smith and Daniel is AUS $ 8489 for all

of their businesses of OZ Bottle Shop and Brekkie and Lunch and while preparing return of

income tax for their partnership firm, AUS $ 8489 will be considered as taxable income as per

Australian tax laws.

The Daniel and Olivia Smith will prepare their working paper of businesses and consists

the following notes in it:

Working Note 1 : Calculation of Total Sales Amount of Olivia Smith and Daniel businesses

Particulars Amount AUS $

Amount Received from Debtor 32800

Closing Balance 3010

Less: Opening Balance 3925

Total Credit Sales 31885

Total Cash Sales 150170

Total Amount of Sales 182055

Working Note 2: Calculation of Total Purchase Amount of Olivia Smith and Daniel businesses

Particulars Amount AUS $

Payment to Creditors 128678

Closing Balance 7010

Less: Opening Balance 6500

Total Credit Purchase 129188

Total Cash Purchase 31155

Total Amount of Purchase 160343

Working Note 3: The Olivia Smith and Daniel businesses has two cars and for income tax

purpose only car maintenance expense which is used in business are considered. During the year

4

of their businesses of OZ Bottle Shop and Brekkie and Lunch and while preparing return of

income tax for their partnership firm, AUS $ 8489 will be considered as taxable income as per

Australian tax laws.

The Daniel and Olivia Smith will prepare their working paper of businesses and consists

the following notes in it:

Working Note 1 : Calculation of Total Sales Amount of Olivia Smith and Daniel businesses

Particulars Amount AUS $

Amount Received from Debtor 32800

Closing Balance 3010

Less: Opening Balance 3925

Total Credit Sales 31885

Total Cash Sales 150170

Total Amount of Sales 182055

Working Note 2: Calculation of Total Purchase Amount of Olivia Smith and Daniel businesses

Particulars Amount AUS $

Payment to Creditors 128678

Closing Balance 7010

Less: Opening Balance 6500

Total Credit Purchase 129188

Total Cash Purchase 31155

Total Amount of Purchase 160343

Working Note 3: The Olivia Smith and Daniel businesses has two cars and for income tax

purpose only car maintenance expense which is used in business are considered. During the year

4

ended June, 2017, maintaining expense which are used business purpose are 90% for van and

60% for SUV car, therefore only this portion is considered as allowable expense in income tax.

Working Note 4 : The mobile bill expense, electricity bill expenses and council rates expenses

are related to the personal and business purpose both. Therefore 10% of mobile bills, 20% of

electricity expense and 40% of council rates are disallowed as expense because they are used for

personal purpose as calculated in profit and loss account.

Working Note 5: In the given question, all the fixed assets of the business of Olivia Smith and

Daniel are purchased before 27 February, 1992, therefore the useful life of restaurant freezer

whose cost is $ 8000 and adjusted value is $1480, restaurant refrigeration (cost $ 14600 and

adjusted value $ 3580), shop fitting structure ( cost $ 7800 and adjusted value $ 2965), kitchen

electrical appliances ( cost $ 3900 and adjusted value $ 754), Van car ( cost $ 16500 and adjusted

value $ 1550) and SUV car ( cost $ 42200 and adjusted value $ 10350) are expired before the

current year ending 30th June, 2017 as per the provisions of depreciation of the Australian tax law

and rates which are published by the ATO of Australia government. So, no depreciation will be

charged on the on these assets because whole of its useful life is expired in the current year

ended 30 June, 2017 for partnership business of Daniel and Olivia Smith.

Working Note 6: As per the depreciation rule of ATO, useful life of freezer will be 12 years and

therefore depreciation will be charged in the year ended 30 June, 2017 by taking useful life as 12

year which start in current year 30 June, 2017 on AUS $ 3000 only because $500 is permitted on

the old unit in purchase of new one.

Working Note 7: AUS $ 3000 which is an principal amount of loan taken for business purpose.

As per income tax rules only interest will be allowed as deduction, therefore, $3000 will not be

allowed as deduction, whereas only its interest component will be allowed expenses for tax

purpose

Working Note 8: Drawing of $ 6000 for cash, $5600 for private purpose and $ 3200 for private

use of owner will never be allowed as deduction for Daniel and Olivia Smith businesses. So,

these expenses are disallowed.

QUESTION 2 Fringe Benefits Tax Consequences of John's Remuneration

Package By its Employer

John is received a remuneration package which involve child's school fees at private

school from his employer @ $ 15000 and also receives accommodation in a apartment of

5

60% for SUV car, therefore only this portion is considered as allowable expense in income tax.

Working Note 4 : The mobile bill expense, electricity bill expenses and council rates expenses

are related to the personal and business purpose both. Therefore 10% of mobile bills, 20% of

electricity expense and 40% of council rates are disallowed as expense because they are used for

personal purpose as calculated in profit and loss account.

Working Note 5: In the given question, all the fixed assets of the business of Olivia Smith and

Daniel are purchased before 27 February, 1992, therefore the useful life of restaurant freezer

whose cost is $ 8000 and adjusted value is $1480, restaurant refrigeration (cost $ 14600 and

adjusted value $ 3580), shop fitting structure ( cost $ 7800 and adjusted value $ 2965), kitchen

electrical appliances ( cost $ 3900 and adjusted value $ 754), Van car ( cost $ 16500 and adjusted

value $ 1550) and SUV car ( cost $ 42200 and adjusted value $ 10350) are expired before the

current year ending 30th June, 2017 as per the provisions of depreciation of the Australian tax law

and rates which are published by the ATO of Australia government. So, no depreciation will be

charged on the on these assets because whole of its useful life is expired in the current year

ended 30 June, 2017 for partnership business of Daniel and Olivia Smith.

Working Note 6: As per the depreciation rule of ATO, useful life of freezer will be 12 years and

therefore depreciation will be charged in the year ended 30 June, 2017 by taking useful life as 12

year which start in current year 30 June, 2017 on AUS $ 3000 only because $500 is permitted on

the old unit in purchase of new one.

Working Note 7: AUS $ 3000 which is an principal amount of loan taken for business purpose.

As per income tax rules only interest will be allowed as deduction, therefore, $3000 will not be

allowed as deduction, whereas only its interest component will be allowed expenses for tax

purpose

Working Note 8: Drawing of $ 6000 for cash, $5600 for private purpose and $ 3200 for private

use of owner will never be allowed as deduction for Daniel and Olivia Smith businesses. So,

these expenses are disallowed.

QUESTION 2 Fringe Benefits Tax Consequences of John's Remuneration

Package By its Employer

John is received a remuneration package which involve child's school fees at private

school from his employer @ $ 15000 and also receives accommodation in a apartment of

5

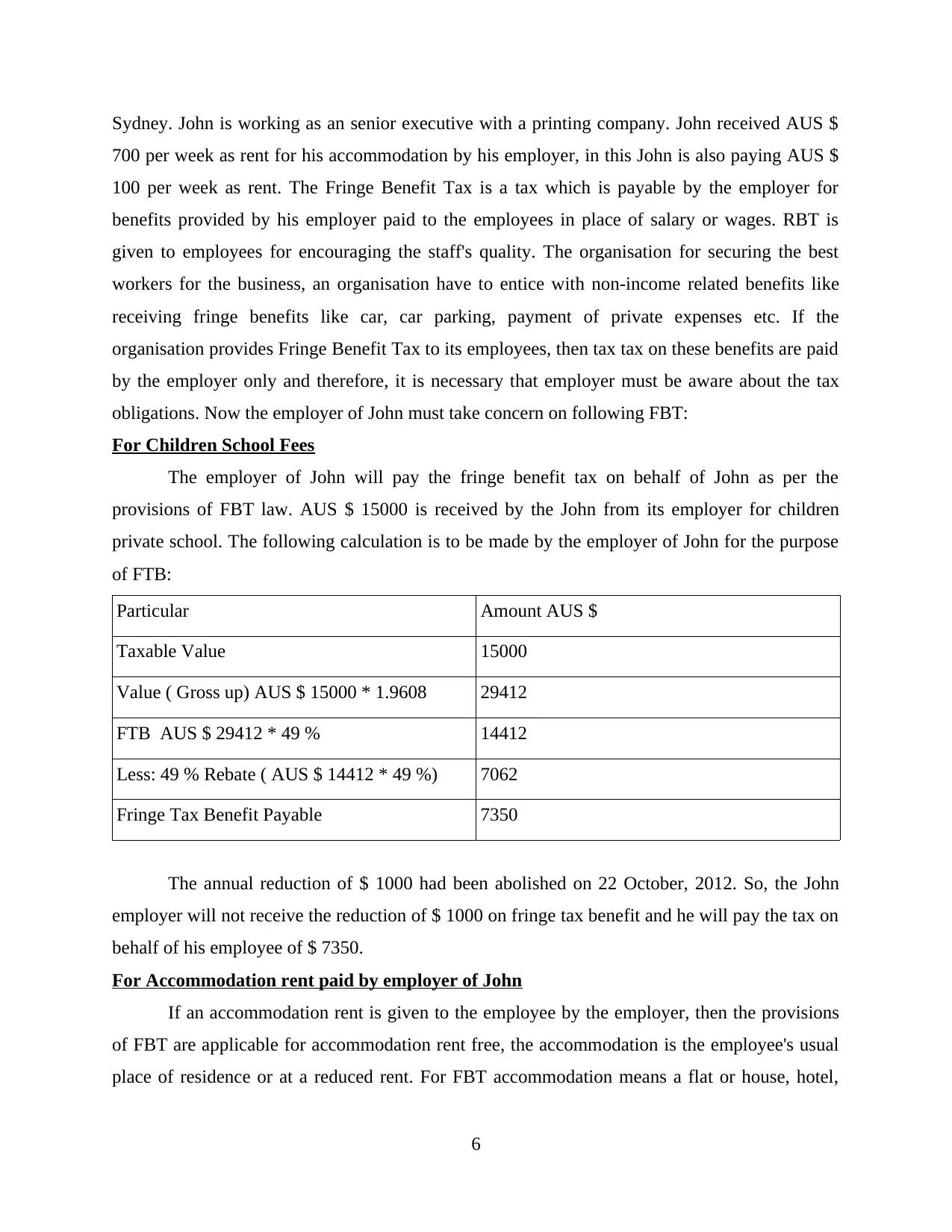

Sydney. John is working as an senior executive with a printing company. John received AUS $

700 per week as rent for his accommodation by his employer, in this John is also paying AUS $

100 per week as rent. The Fringe Benefit Tax is a tax which is payable by the employer for

benefits provided by his employer paid to the employees in place of salary or wages. RBT is

given to employees for encouraging the staff's quality. The organisation for securing the best

workers for the business, an organisation have to entice with non-income related benefits like

receiving fringe benefits like car, car parking, payment of private expenses etc. If the

organisation provides Fringe Benefit Tax to its employees, then tax tax on these benefits are paid

by the employer only and therefore, it is necessary that employer must be aware about the tax

obligations. Now the employer of John must take concern on following FBT:

For Children School Fees

The employer of John will pay the fringe benefit tax on behalf of John as per the

provisions of FBT law. AUS $ 15000 is received by the John from its employer for children

private school. The following calculation is to be made by the employer of John for the purpose

of FTB:

Particular Amount AUS $

Taxable Value 15000

Value ( Gross up) AUS $ 15000 * 1.9608 29412

FTB AUS $ 29412 * 49 % 14412

Less: 49 % Rebate ( AUS $ 14412 * 49 %) 7062

Fringe Tax Benefit Payable 7350

The annual reduction of $ 1000 had been abolished on 22 October, 2012. So, the John

employer will not receive the reduction of $ 1000 on fringe tax benefit and he will pay the tax on

behalf of his employee of $ 7350.

For Accommodation rent paid by employer of John

If an accommodation rent is given to the employee by the employer, then the provisions

of FBT are applicable for accommodation rent free, the accommodation is the employee's usual

place of residence or at a reduced rent. For FBT accommodation means a flat or house, hotel,

6

700 per week as rent for his accommodation by his employer, in this John is also paying AUS $

100 per week as rent. The Fringe Benefit Tax is a tax which is payable by the employer for

benefits provided by his employer paid to the employees in place of salary or wages. RBT is

given to employees for encouraging the staff's quality. The organisation for securing the best

workers for the business, an organisation have to entice with non-income related benefits like

receiving fringe benefits like car, car parking, payment of private expenses etc. If the

organisation provides Fringe Benefit Tax to its employees, then tax tax on these benefits are paid

by the employer only and therefore, it is necessary that employer must be aware about the tax

obligations. Now the employer of John must take concern on following FBT:

For Children School Fees

The employer of John will pay the fringe benefit tax on behalf of John as per the

provisions of FBT law. AUS $ 15000 is received by the John from its employer for children

private school. The following calculation is to be made by the employer of John for the purpose

of FTB:

Particular Amount AUS $

Taxable Value 15000

Value ( Gross up) AUS $ 15000 * 1.9608 29412

FTB AUS $ 29412 * 49 % 14412

Less: 49 % Rebate ( AUS $ 14412 * 49 %) 7062

Fringe Tax Benefit Payable 7350

The annual reduction of $ 1000 had been abolished on 22 October, 2012. So, the John

employer will not receive the reduction of $ 1000 on fringe tax benefit and he will pay the tax on

behalf of his employee of $ 7350.

For Accommodation rent paid by employer of John

If an accommodation rent is given to the employee by the employer, then the provisions

of FBT are applicable for accommodation rent free, the accommodation is the employee's usual

place of residence or at a reduced rent. For FBT accommodation means a flat or house, hotel,

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

motel, caravan home, accommodation on ship etc. John pays a rent of $100 per week. Value of

FBT will be calculated on $ 700 per week, $ 36400 annually.

CONCLUSION

From the above report it is concluded that for the calculation of the net income provisions

of income tax are to be followed. In this project net income of partnership of Daniel and Olivia

Smith are calculated and Fringe Benefit Tax is also calculated as for the employer of John who

give him FTB for children school fees at a private school and accommodation service.

REFERENCES

Books and Journals

Hill, F. R. and Mancino, D. M., 2014. Taxation of exempt organizations.

Faure, M. G. and Weishaar, S. E., 2012. 22 The role of environmental taxation: economics and

the law. Handbook of research on environmental taxation, p.399.

Aprill, E. P., 2012. Once and Future Gift Taxation of Transfers to Section 501 (c)(4)

Organizations: Current Law, Constitutional Issues, and Policy Considerations. NYUJ

Legis. & Pub. Pol'y. 15. p.289.

Fox, W. F., 2012. Retail sales and use taxation. In The Oxford handbook of state and local

government finance.

Alzahrani, M. and Lasfer, M., 2012. Investor protection, taxation, and dividends. Journal of

Corporate Finance. 18(4). pp.745-762.

Sendetska, O., 2014. ECJ Case Law on Corporate Exit Taxation: From National Grid Indus to

DMC: What Is the Current State of Law?. EC Tax Review. 23(4). pp.230-237.

Navez, E. J., 2012. Influence of EU Law on Inheritance Taxation: Is the Intensification of

Negative Integration Enough to Eliminate Obstacles Preventing EU Citizens from

Crossing Borders within the Single Market. EC Tax Rev. 21. p.84.

7

FBT will be calculated on $ 700 per week, $ 36400 annually.

CONCLUSION

From the above report it is concluded that for the calculation of the net income provisions

of income tax are to be followed. In this project net income of partnership of Daniel and Olivia

Smith are calculated and Fringe Benefit Tax is also calculated as for the employer of John who

give him FTB for children school fees at a private school and accommodation service.

REFERENCES

Books and Journals

Hill, F. R. and Mancino, D. M., 2014. Taxation of exempt organizations.

Faure, M. G. and Weishaar, S. E., 2012. 22 The role of environmental taxation: economics and

the law. Handbook of research on environmental taxation, p.399.

Aprill, E. P., 2012. Once and Future Gift Taxation of Transfers to Section 501 (c)(4)

Organizations: Current Law, Constitutional Issues, and Policy Considerations. NYUJ

Legis. & Pub. Pol'y. 15. p.289.

Fox, W. F., 2012. Retail sales and use taxation. In The Oxford handbook of state and local

government finance.

Alzahrani, M. and Lasfer, M., 2012. Investor protection, taxation, and dividends. Journal of

Corporate Finance. 18(4). pp.745-762.

Sendetska, O., 2014. ECJ Case Law on Corporate Exit Taxation: From National Grid Indus to

DMC: What Is the Current State of Law?. EC Tax Review. 23(4). pp.230-237.

Navez, E. J., 2012. Influence of EU Law on Inheritance Taxation: Is the Intensification of

Negative Integration Enough to Eliminate Obstacles Preventing EU Citizens from

Crossing Borders within the Single Market. EC Tax Rev. 21. p.84.

7

8

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.