Time Series Analysis for VAR Model and Engle-Granger Test

Solve two exercises on time series analysis using a VAR model with a specific information set.

11 Pages1401 Words415 Views

Added on 2023-06-16

About This Document

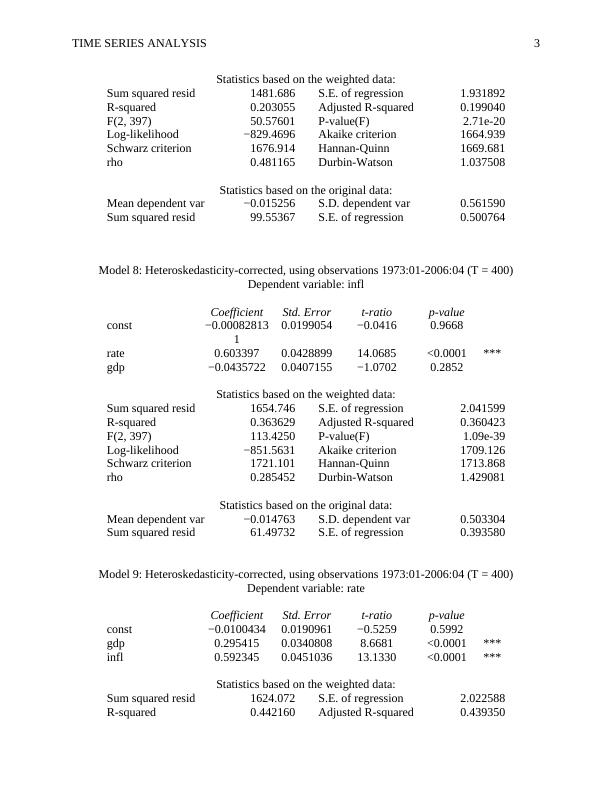

This article explains the process of time series analysis for VAR model and Engle-Granger test. It covers the identification of unit root, stationary points, and cointegration. It also discusses the transmission mechanism of monetary policy and the impact of growth rate, inflation rate, and policy interest rate. The article is relevant for students studying economics, finance, and related courses.

Time Series Analysis for VAR Model and Engle-Granger Test

Solve two exercises on time series analysis using a VAR model with a specific information set.

Added on 2023-06-16

ShareRelated Documents

End of preview

Want to access all the pages? Upload your documents or become a member.

Applied Finance with Eviews : Assignment - Desklib

|31

|5859

|216

Forecasting Nike Quarterly Revenue with Regression Analysis

|14

|1538

|318

Data Presentation and Hypotheses Testing for Banks in Nigeria

|12

|2086

|475

Probability of Chi Square Statistics

|17

|3311

|188

Econ241 Major Assignment: Linear Model

|15

|2173

|42

Total panel observations: Variable Coefficient t-Statistic

|7

|1148

|117