An Analysis of Traditional versus Activity Based Costing Methods

VerifiedAdded on 2021/04/21

|7

|1239

|82

Essay

AI Summary

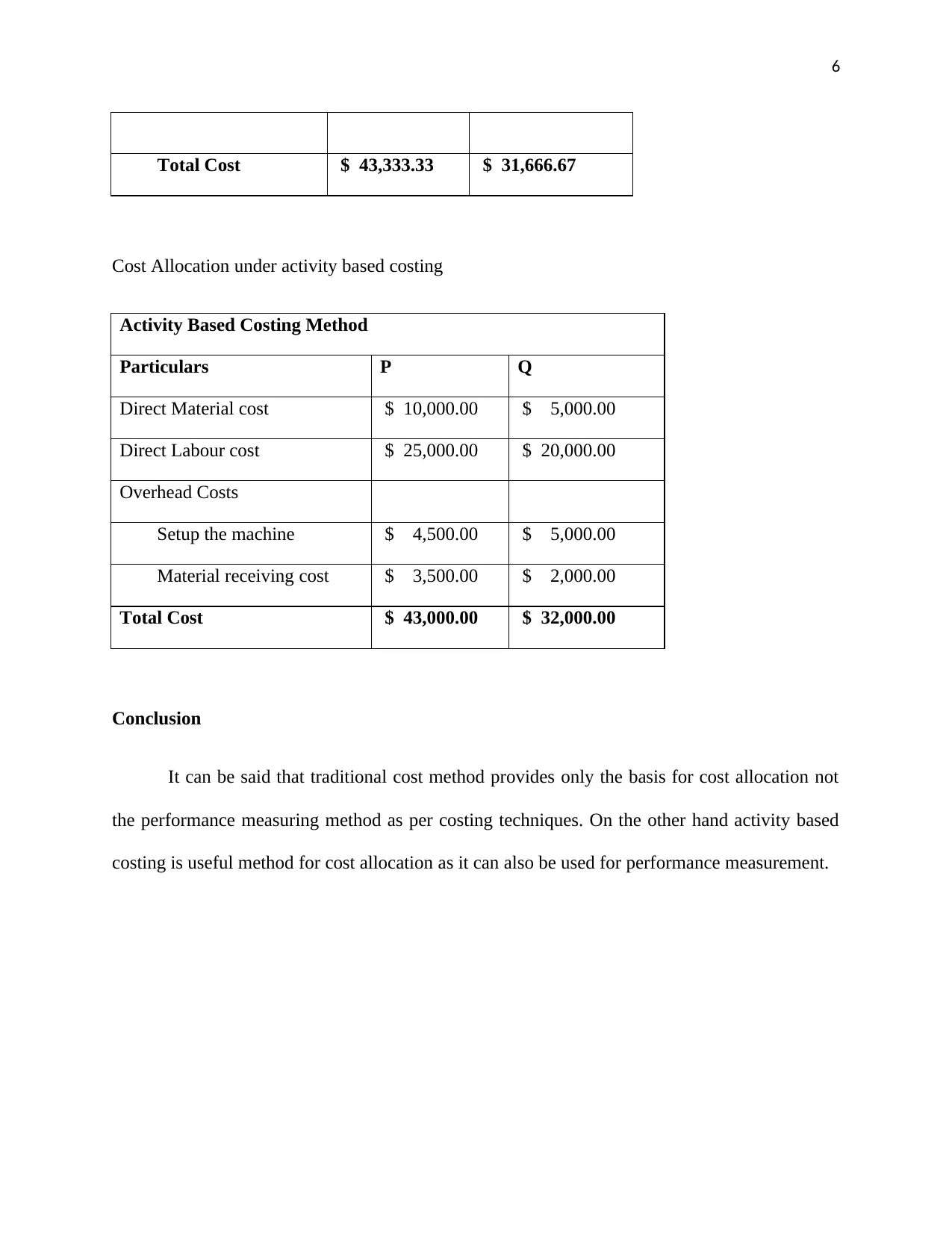

This essay provides a comprehensive comparison of traditional and activity-based costing methods. It begins by introducing the context of cost allocation in manufacturing and service industries, emphasizing the need to distribute costs like raw materials, labor, and overhead to determine the overall cost of goods. The essay then delves into the specifics of both costing methods, highlighting the simplicity of traditional costing, which uses a single cost driver like direct labor hours or machine hours, and its limitations in modern manufacturing environments. The activity-based costing method is presented as a more accurate approach that divides the manufacturing process into stages, using multiple cost drivers linked to specific activities. The essay includes a detailed comparison table and a numerical example to illustrate the differences in cost allocation between the two methods, and concludes by emphasizing the value of activity-based costing for performance measurement and improved business decision-making. References from Cooper and Kaplan, Bromwich and Bhimani, and Hayden are provided.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.