Financial Management: Ratio Analysis of Zurich Plc. for 2015 and 2016

Analyzing the financial statements of Zurich Plc and addressing concerns regarding profitability and liquidity.

22 Pages4315 Words262 Views

Added on 2023-06-11

About This Document

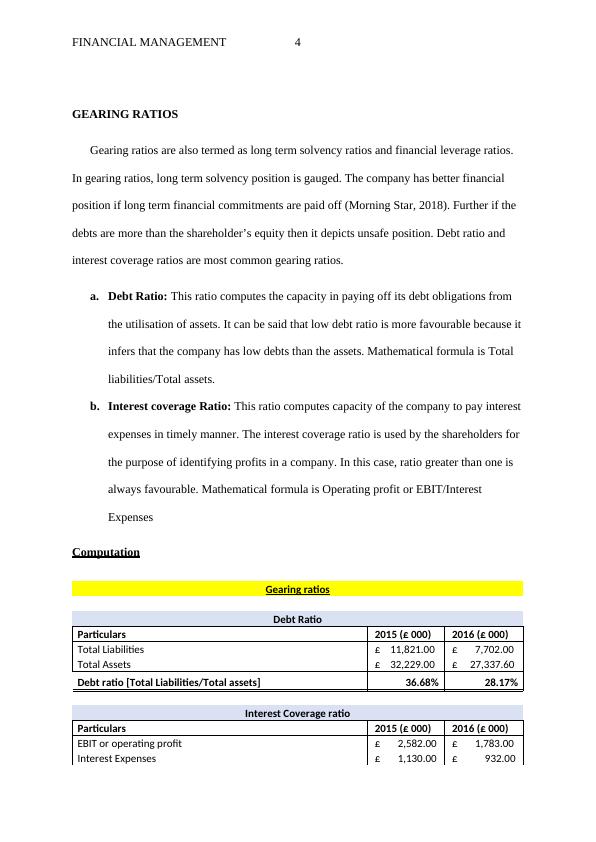

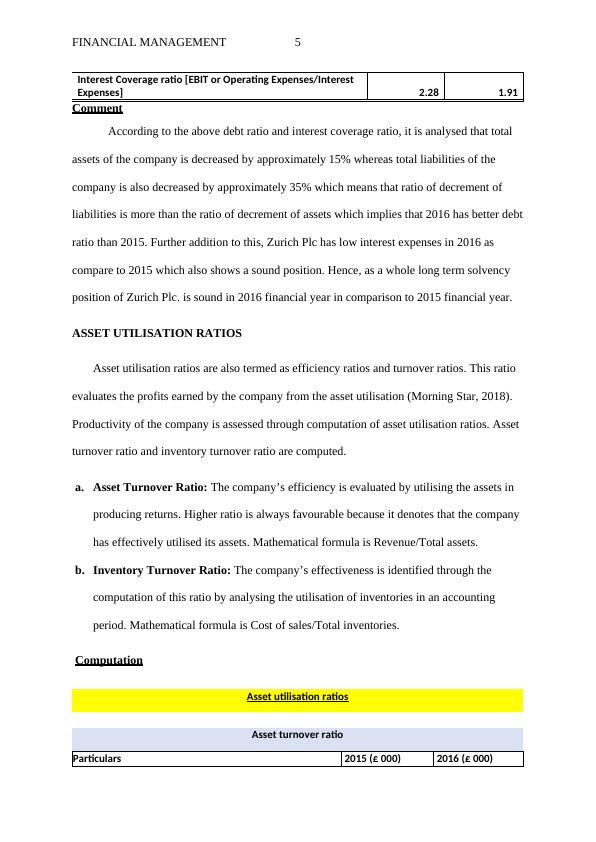

This report analyses the profitability and liquidity position of Zurich Plc. for 2015 and 2016 financial years through the computation of five categories of ratios. It also critically assesses the limitations of ratio analysis for decision making purposes.

Financial Management: Ratio Analysis of Zurich Plc. for 2015 and 2016

Analyzing the financial statements of Zurich Plc and addressing concerns regarding profitability and liquidity.

Added on 2023-06-11

ShareRelated Documents

End of preview

Want to access all the pages? Upload your documents or become a member.

Financial Marketing

|24

|3883

|42

Auditing Theory and Practice: Financial Statement Analysis and Ratio Calculation

|13

|1932

|401

Financial Ratios and Analysis for ABC Ltd

|11

|1963

|69

Financial Analysis of Tesco: Liquidity, Profitability, Efficiency, and Leverage Ratios

|14

|2135

|73

Report | Comparison Of NEXT Plc & Morrison | Profitability, Liquidity

|14

|2058

|80

Financial Performance Analysis of Qantas Airways

|20

|4490

|470