Finance Assignment: Financial Statement Analysis and Valuation

VerifiedAdded on 2023/01/13

|23

|6219

|20

Homework Assignment

AI Summary

This finance assignment delves into various crucial aspects of financial management. It begins with an exploration of financial statement analysis through ratio analysis, including the calculation of Accounts Receivable Turnover and Average Collection Period. The assignment then addresses the time value of money by calculating future value and explaining its significance. Furthermore, it covers capital budgeting techniques, such as the payback period, and the capital budgeting process. The assignment also examines capital structure by calculating the Weighted Average Cost of Capital (WACC) using both book and market values, alongside a discussion of factors affecting the cost of capital. It proceeds to evaluate investment decisions using Net Present Value (NPV) and profitability index. Lastly, the assignment encompasses financial management expressions, tax liability calculations, and the importance of taxation within an economy.

Finance

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

QUESTION 1...................................................................................................................................4

Introduction..................................................................................................................................4

1. Explain the importance of analysis financial statement through ratios...................................4

2. Calculate the following ratio of Albert Ltd..............................................................................5

QUESTION 2...................................................................................................................................6

Introduction..................................................................................................................................6

1. Calculation of future value.......................................................................................................7

2. Explanation of time value of money........................................................................................8

QUESTION 3...................................................................................................................................8

Introduction..................................................................................................................................8

1. Calculation of pay back period................................................................................................8

2. Capital budgeting process of an organisation..........................................................................9

QUESTION 4.................................................................................................................................10

Introduction................................................................................................................................10

(a). Calculate WACC by using Book Value..............................................................................10

(b). Calculate WACC by using Market Value...........................................................................11

(c). Explain the factors which affect the Cost of Capital...........................................................12

QUESTION 5.................................................................................................................................13

Introduction................................................................................................................................13

(a). Calculate the NPV or Profitable Index and suggest that which project should be adopted 13

(b). Explain the key decisions which taken by the finance manager in the organization..........15

QUESTION 6.................................................................................................................................16

Introduction................................................................................................................................16

1. Short note on Financial Management Expression.................................................................16

QUESTION 7.................................................................................................................................18

Introduction................................................................................................................................18

1. Calculate tax liability of Robbins Corporation......................................................................19

2

QUESTION 1...................................................................................................................................4

Introduction..................................................................................................................................4

1. Explain the importance of analysis financial statement through ratios...................................4

2. Calculate the following ratio of Albert Ltd..............................................................................5

QUESTION 2...................................................................................................................................6

Introduction..................................................................................................................................6

1. Calculation of future value.......................................................................................................7

2. Explanation of time value of money........................................................................................8

QUESTION 3...................................................................................................................................8

Introduction..................................................................................................................................8

1. Calculation of pay back period................................................................................................8

2. Capital budgeting process of an organisation..........................................................................9

QUESTION 4.................................................................................................................................10

Introduction................................................................................................................................10

(a). Calculate WACC by using Book Value..............................................................................10

(b). Calculate WACC by using Market Value...........................................................................11

(c). Explain the factors which affect the Cost of Capital...........................................................12

QUESTION 5.................................................................................................................................13

Introduction................................................................................................................................13

(a). Calculate the NPV or Profitable Index and suggest that which project should be adopted 13

(b). Explain the key decisions which taken by the finance manager in the organization..........15

QUESTION 6.................................................................................................................................16

Introduction................................................................................................................................16

1. Short note on Financial Management Expression.................................................................16

QUESTION 7.................................................................................................................................18

Introduction................................................................................................................................18

1. Calculate tax liability of Robbins Corporation......................................................................19

2

2. Explain the importance of taxation in the economy and how it contributes in the society for

its welfare...................................................................................................................................19

REFERENCES .............................................................................................................................21

3

its welfare...................................................................................................................................19

REFERENCES .............................................................................................................................21

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUESTION 1

Introduction

Financial ratio also called accounting ratio which help the organization to know about

company's abilities and performance. Different ratio calculated for the different purpose such as

gross profit, net profit ratio used to identify the profitability of the company and the other hand,

account receivables ratio used to calculate business efficiency (Antonopoulos and Hall, 2016).

This question is about the importance of financial analysis with the help of ratio. In addition, it

includes the calculation of Account Receivable Turnover ( ART ) or Average Collection Period

Ratio ( ACPR) .

1. Explain the importance of analysis financial statement through ratios

Analysis of financial statements is the process of reviewing, monitoring or take better

decisions in order to improve their economic performance as well as profitability (Ward and

Forker, 2017). These statements are profit & loss statement, cash flow, balance sheet, change in

equity statement etc. basically it is required for the stakeholder analysis and it includes creditors,

investors, shareholders, general public, government, management of the company to make

effective decisions etc. With the help of ratio, business able to evaluate the overall performance

which is very important for the organizations which are discussed below:

Judging efficiency: With aid of ratio analysis business able to justify the company's

performance in terms of operations and management. Also beneficial in terms of

analysing how business utilize their business assets or maximise their profit margin using

various accounting principles or standards.

Locating weakness: It helps in locating operational weakness and further management

have to pay more attention to improve their their performance as well as productivity.

Ratio analysis used to evaluate efficiency of the business and which part required

improvement. Management used to locate the area or factor which affect the overall

profit or production. After that, managers formulate strategies to improve the

performance as well as productivity.

Formulating strategies: with the help of ratio analysis, management identify the growth

of the business (Brusca, Gómez‐villegas and Montesinos, 2016). If any improvement

4

Introduction

Financial ratio also called accounting ratio which help the organization to know about

company's abilities and performance. Different ratio calculated for the different purpose such as

gross profit, net profit ratio used to identify the profitability of the company and the other hand,

account receivables ratio used to calculate business efficiency (Antonopoulos and Hall, 2016).

This question is about the importance of financial analysis with the help of ratio. In addition, it

includes the calculation of Account Receivable Turnover ( ART ) or Average Collection Period

Ratio ( ACPR) .

1. Explain the importance of analysis financial statement through ratios

Analysis of financial statements is the process of reviewing, monitoring or take better

decisions in order to improve their economic performance as well as profitability (Ward and

Forker, 2017). These statements are profit & loss statement, cash flow, balance sheet, change in

equity statement etc. basically it is required for the stakeholder analysis and it includes creditors,

investors, shareholders, general public, government, management of the company to make

effective decisions etc. With the help of ratio, business able to evaluate the overall performance

which is very important for the organizations which are discussed below:

Judging efficiency: With aid of ratio analysis business able to justify the company's

performance in terms of operations and management. Also beneficial in terms of

analysing how business utilize their business assets or maximise their profit margin using

various accounting principles or standards.

Locating weakness: It helps in locating operational weakness and further management

have to pay more attention to improve their their performance as well as productivity.

Ratio analysis used to evaluate efficiency of the business and which part required

improvement. Management used to locate the area or factor which affect the overall

profit or production. After that, managers formulate strategies to improve the

performance as well as productivity.

Formulating strategies: with the help of ratio analysis, management identify the growth

of the business (Brusca, Gómez‐villegas and Montesinos, 2016). If any improvement

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

required then managers formulate strategies on the basis of actual outcomes. By using

past financial information business make future plans in order to reach company's goals

& objectives.

Comparing performance: Ratio analysis help the organization to compare their current

operational performances with the help of previous one. It will show clear difference in

the performance in terms of profit or loss (Vasu, Stewart and Garson, 2017). Further

management build strategies accordingly and make sure to implement in order to

maximise overall productivity as well as profit margin of the business.

Above mention elements are the beneficial for the organizations and it will be possible

with the help of ratios analysis. Managers used to compare results and formulate further plans in

order to maximise their performance as well as efficiency which helps in meeting business goals

& objectives.

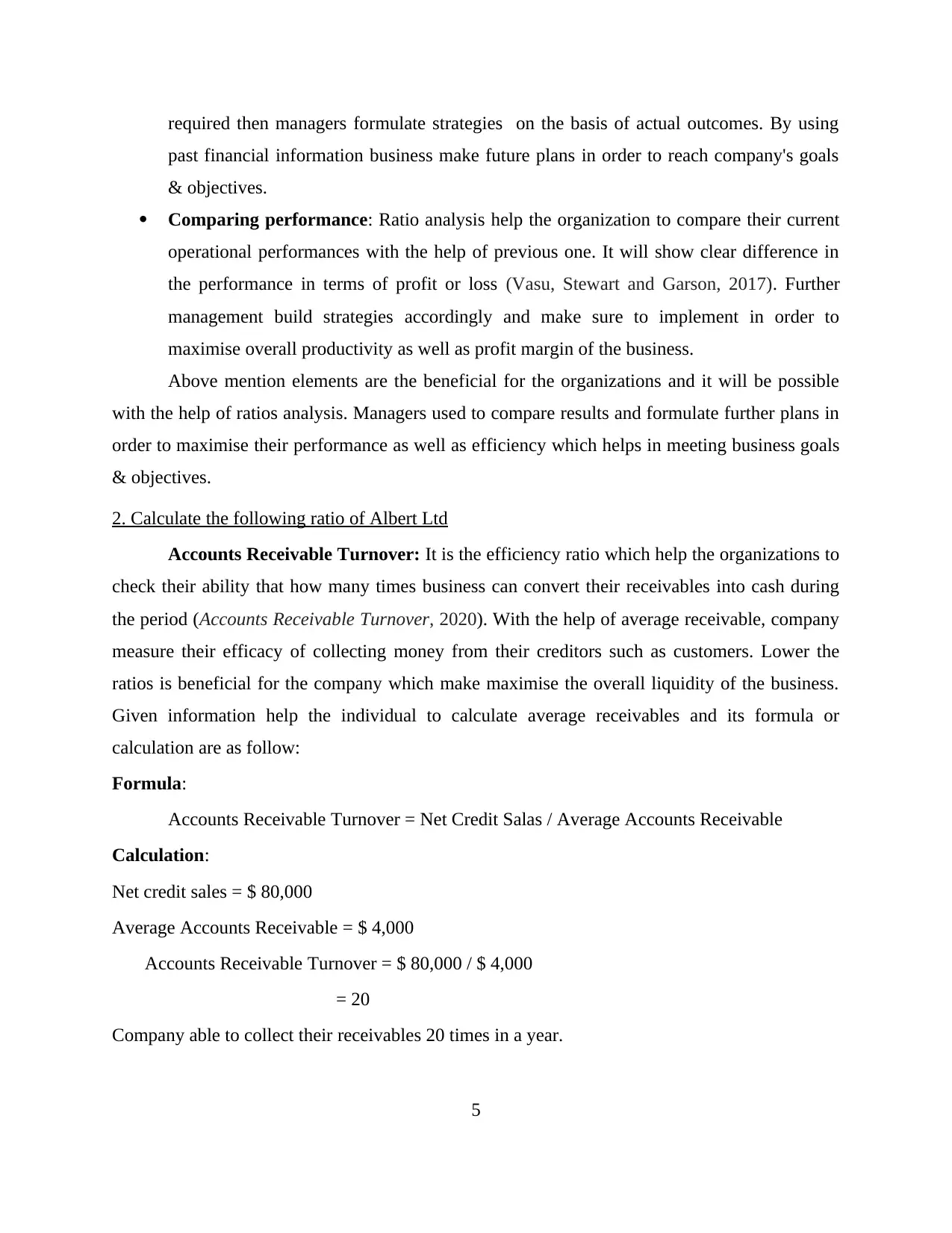

2. Calculate the following ratio of Albert Ltd

Accounts Receivable Turnover: It is the efficiency ratio which help the organizations to

check their ability that how many times business can convert their receivables into cash during

the period (Accounts Receivable Turnover, 2020). With the help of average receivable, company

measure their efficacy of collecting money from their creditors such as customers. Lower the

ratios is beneficial for the company which make maximise the overall liquidity of the business.

Given information help the individual to calculate average receivables and its formula or

calculation are as follow:

Formula:

Accounts Receivable Turnover = Net Credit Salas / Average Accounts Receivable

Calculation:

Net credit sales = $ 80,000

Average Accounts Receivable = $ 4,000

Accounts Receivable Turnover = $ 80,000 / $ 4,000

= 20

Company able to collect their receivables 20 times in a year.

5

past financial information business make future plans in order to reach company's goals

& objectives.

Comparing performance: Ratio analysis help the organization to compare their current

operational performances with the help of previous one. It will show clear difference in

the performance in terms of profit or loss (Vasu, Stewart and Garson, 2017). Further

management build strategies accordingly and make sure to implement in order to

maximise overall productivity as well as profit margin of the business.

Above mention elements are the beneficial for the organizations and it will be possible

with the help of ratios analysis. Managers used to compare results and formulate further plans in

order to maximise their performance as well as efficiency which helps in meeting business goals

& objectives.

2. Calculate the following ratio of Albert Ltd

Accounts Receivable Turnover: It is the efficiency ratio which help the organizations to

check their ability that how many times business can convert their receivables into cash during

the period (Accounts Receivable Turnover, 2020). With the help of average receivable, company

measure their efficacy of collecting money from their creditors such as customers. Lower the

ratios is beneficial for the company which make maximise the overall liquidity of the business.

Given information help the individual to calculate average receivables and its formula or

calculation are as follow:

Formula:

Accounts Receivable Turnover = Net Credit Salas / Average Accounts Receivable

Calculation:

Net credit sales = $ 80,000

Average Accounts Receivable = $ 4,000

Accounts Receivable Turnover = $ 80,000 / $ 4,000

= 20

Company able to collect their receivables 20 times in a year.

5

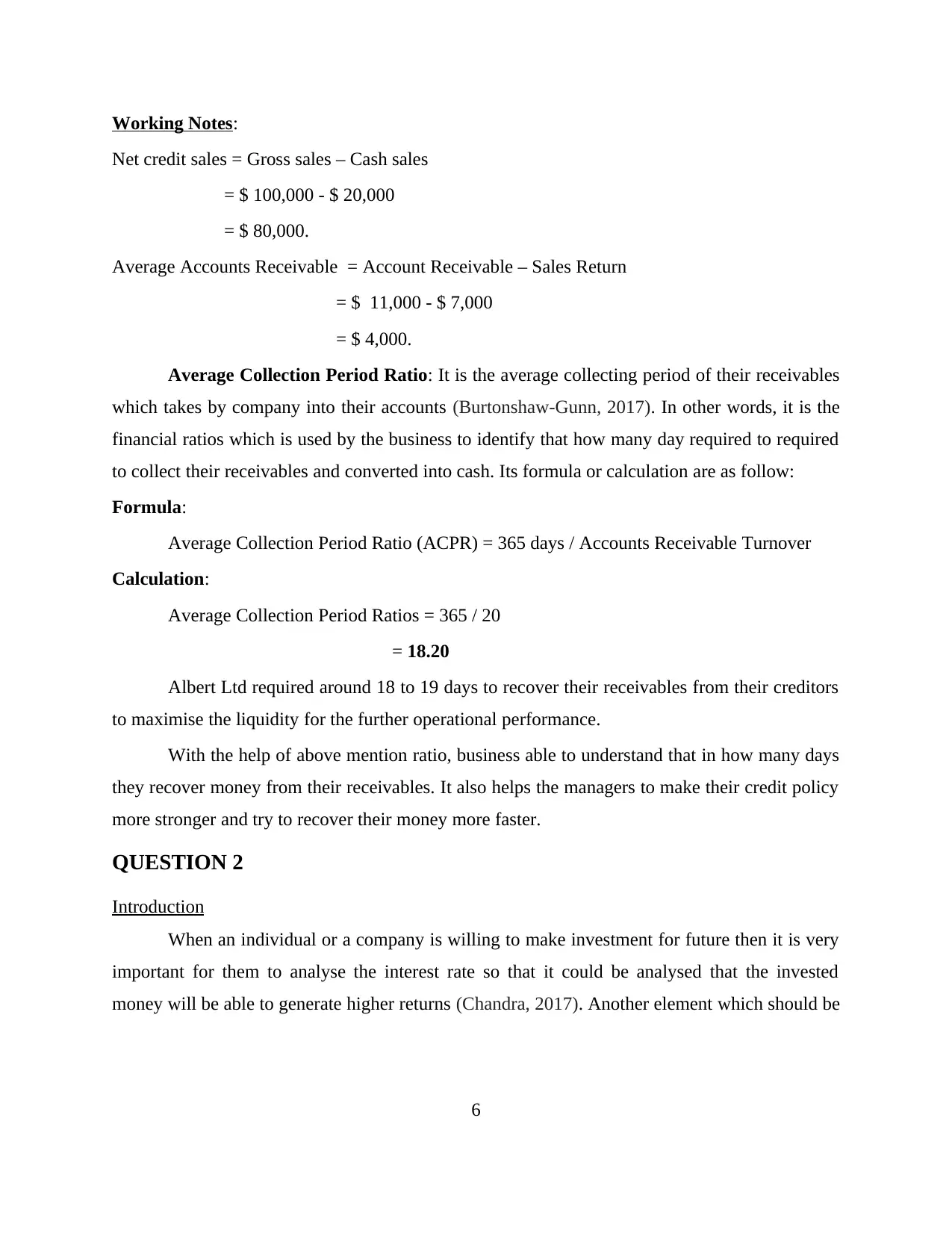

Working Notes:

Net credit sales = Gross sales – Cash sales

= $ 100,000 - $ 20,000

= $ 80,000.

Average Accounts Receivable = Account Receivable – Sales Return

= $ 11,000 - $ 7,000

= $ 4,000.

Average Collection Period Ratio: It is the average collecting period of their receivables

which takes by company into their accounts (Burtonshaw-Gunn, 2017). In other words, it is the

financial ratios which is used by the business to identify that how many day required to required

to collect their receivables and converted into cash. Its formula or calculation are as follow:

Formula:

Average Collection Period Ratio (ACPR) = 365 days / Accounts Receivable Turnover

Calculation:

Average Collection Period Ratios = 365 / 20

= 18.20

Albert Ltd required around 18 to 19 days to recover their receivables from their creditors

to maximise the liquidity for the further operational performance.

With the help of above mention ratio, business able to understand that in how many days

they recover money from their receivables. It also helps the managers to make their credit policy

more stronger and try to recover their money more faster.

QUESTION 2

Introduction

When an individual or a company is willing to make investment for future then it is very

important for them to analyse the interest rate so that it could be analysed that the invested

money will be able to generate higher returns (Chandra, 2017). Another element which should be

6

Net credit sales = Gross sales – Cash sales

= $ 100,000 - $ 20,000

= $ 80,000.

Average Accounts Receivable = Account Receivable – Sales Return

= $ 11,000 - $ 7,000

= $ 4,000.

Average Collection Period Ratio: It is the average collecting period of their receivables

which takes by company into their accounts (Burtonshaw-Gunn, 2017). In other words, it is the

financial ratios which is used by the business to identify that how many day required to required

to collect their receivables and converted into cash. Its formula or calculation are as follow:

Formula:

Average Collection Period Ratio (ACPR) = 365 days / Accounts Receivable Turnover

Calculation:

Average Collection Period Ratios = 365 / 20

= 18.20

Albert Ltd required around 18 to 19 days to recover their receivables from their creditors

to maximise the liquidity for the further operational performance.

With the help of above mention ratio, business able to understand that in how many days

they recover money from their receivables. It also helps the managers to make their credit policy

more stronger and try to recover their money more faster.

QUESTION 2

Introduction

When an individual or a company is willing to make investment for future then it is very

important for them to analyse the interest rate so that it could be analysed that the invested

money will be able to generate higher returns (Chandra, 2017). Another element which should be

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

focused by an investor is time value of money because with the help of it higher returns could be

generated.

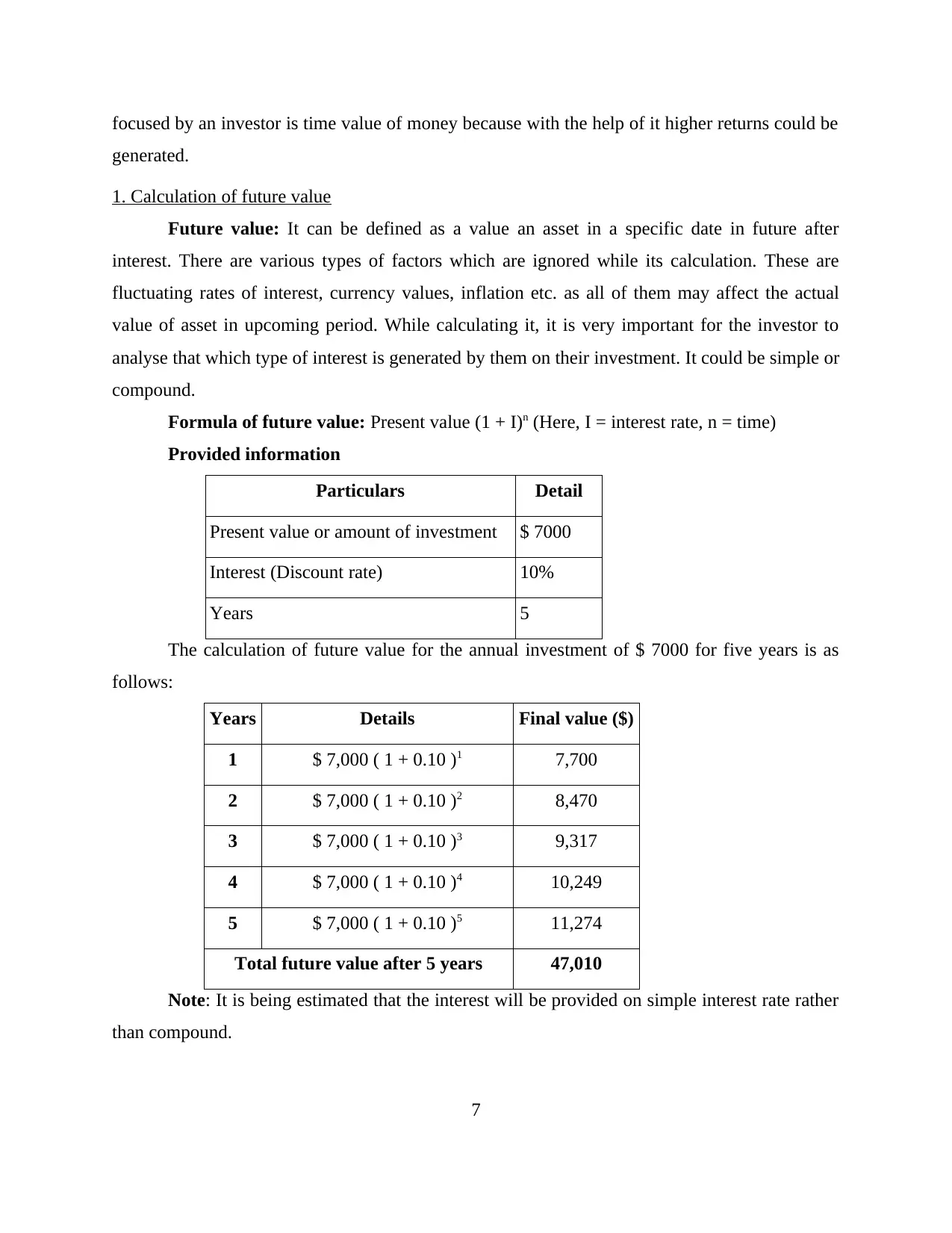

1. Calculation of future value

Future value: It can be defined as a value an asset in a specific date in future after

interest. There are various types of factors which are ignored while its calculation. These are

fluctuating rates of interest, currency values, inflation etc. as all of them may affect the actual

value of asset in upcoming period. While calculating it, it is very important for the investor to

analyse that which type of interest is generated by them on their investment. It could be simple or

compound.

Formula of future value: Present value (1 + I)n (Here, I = interest rate, n = time)

Provided information

Particulars Detail

Present value or amount of investment $ 7000

Interest (Discount rate) 10%

Years 5

The calculation of future value for the annual investment of $ 7000 for five years is as

follows:

Years Details Final value ($)

1 $ 7,000 ( 1 + 0.10 )1 7,700

2 $ 7,000 ( 1 + 0.10 )2 8,470

3 $ 7,000 ( 1 + 0.10 )3 9,317

4 $ 7,000 ( 1 + 0.10 )4 10,249

5 $ 7,000 ( 1 + 0.10 )5 11,274

Total future value after 5 years 47,010

Note: It is being estimated that the interest will be provided on simple interest rate rather

than compound.

7

generated.

1. Calculation of future value

Future value: It can be defined as a value an asset in a specific date in future after

interest. There are various types of factors which are ignored while its calculation. These are

fluctuating rates of interest, currency values, inflation etc. as all of them may affect the actual

value of asset in upcoming period. While calculating it, it is very important for the investor to

analyse that which type of interest is generated by them on their investment. It could be simple or

compound.

Formula of future value: Present value (1 + I)n (Here, I = interest rate, n = time)

Provided information

Particulars Detail

Present value or amount of investment $ 7000

Interest (Discount rate) 10%

Years 5

The calculation of future value for the annual investment of $ 7000 for five years is as

follows:

Years Details Final value ($)

1 $ 7,000 ( 1 + 0.10 )1 7,700

2 $ 7,000 ( 1 + 0.10 )2 8,470

3 $ 7,000 ( 1 + 0.10 )3 9,317

4 $ 7,000 ( 1 + 0.10 )4 10,249

5 $ 7,000 ( 1 + 0.10 )5 11,274

Total future value after 5 years 47,010

Note: It is being estimated that the interest will be provided on simple interest rate rather

than compound.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

From the above table it has been analysed that at the end of fifth year the future value will

be $ 11274 and total value on this date will be $ 47010 for the investor.

2. Explanation of time value of money

Time value of money: It can be defined as a concept which demonstrates that monetary

resources which are available at present are worth more than identical sum in the upcoming

period because of its capacity to generate potential earning. For investors it is very important to

have detailed information of it because a dollar which could be invested by them in a project

worth more than that one which is promised in future (Chung and Chuang, 2016). By focusing

upon it they will be able to invest their funds appropriately and generate capital gain for future.

QUESTION 3

Introduction

Capital budgeting can be defined as a process which is focused by business entities to

select best suitable investment option to invest monetary resources (Ferguson and Morton-

Huddleston, 2016). There are various investment appraisal techniques which could be used by

organisations to evaluate different alternatives. These are pay back period, NPV, ARR and IRR.

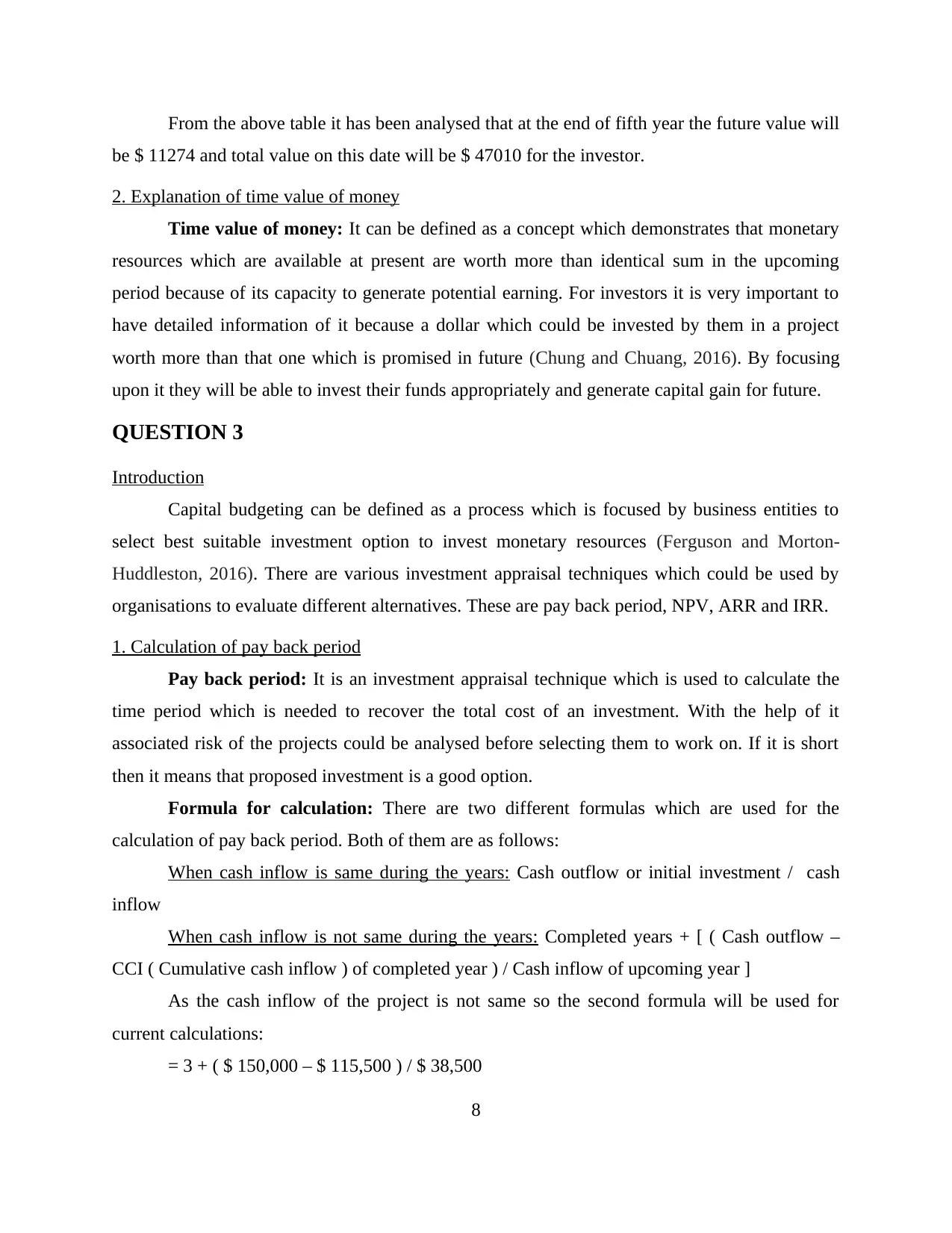

1. Calculation of pay back period

Pay back period: It is an investment appraisal technique which is used to calculate the

time period which is needed to recover the total cost of an investment. With the help of it

associated risk of the projects could be analysed before selecting them to work on. If it is short

then it means that proposed investment is a good option.

Formula for calculation: There are two different formulas which are used for the

calculation of pay back period. Both of them are as follows:

When cash inflow is same during the years: Cash outflow or initial investment / cash

inflow

When cash inflow is not same during the years: Completed years + [ ( Cash outflow –

CCI ( Cumulative cash inflow ) of completed year ) / Cash inflow of upcoming year ]

As the cash inflow of the project is not same so the second formula will be used for

current calculations:

= 3 + ( $ 150,000 – $ 115,500 ) / $ 38,500

8

be $ 11274 and total value on this date will be $ 47010 for the investor.

2. Explanation of time value of money

Time value of money: It can be defined as a concept which demonstrates that monetary

resources which are available at present are worth more than identical sum in the upcoming

period because of its capacity to generate potential earning. For investors it is very important to

have detailed information of it because a dollar which could be invested by them in a project

worth more than that one which is promised in future (Chung and Chuang, 2016). By focusing

upon it they will be able to invest their funds appropriately and generate capital gain for future.

QUESTION 3

Introduction

Capital budgeting can be defined as a process which is focused by business entities to

select best suitable investment option to invest monetary resources (Ferguson and Morton-

Huddleston, 2016). There are various investment appraisal techniques which could be used by

organisations to evaluate different alternatives. These are pay back period, NPV, ARR and IRR.

1. Calculation of pay back period

Pay back period: It is an investment appraisal technique which is used to calculate the

time period which is needed to recover the total cost of an investment. With the help of it

associated risk of the projects could be analysed before selecting them to work on. If it is short

then it means that proposed investment is a good option.

Formula for calculation: There are two different formulas which are used for the

calculation of pay back period. Both of them are as follows:

When cash inflow is same during the years: Cash outflow or initial investment / cash

inflow

When cash inflow is not same during the years: Completed years + [ ( Cash outflow –

CCI ( Cumulative cash inflow ) of completed year ) / Cash inflow of upcoming year ]

As the cash inflow of the project is not same so the second formula will be used for

current calculations:

= 3 + ( $ 150,000 – $ 115,500 ) / $ 38,500

8

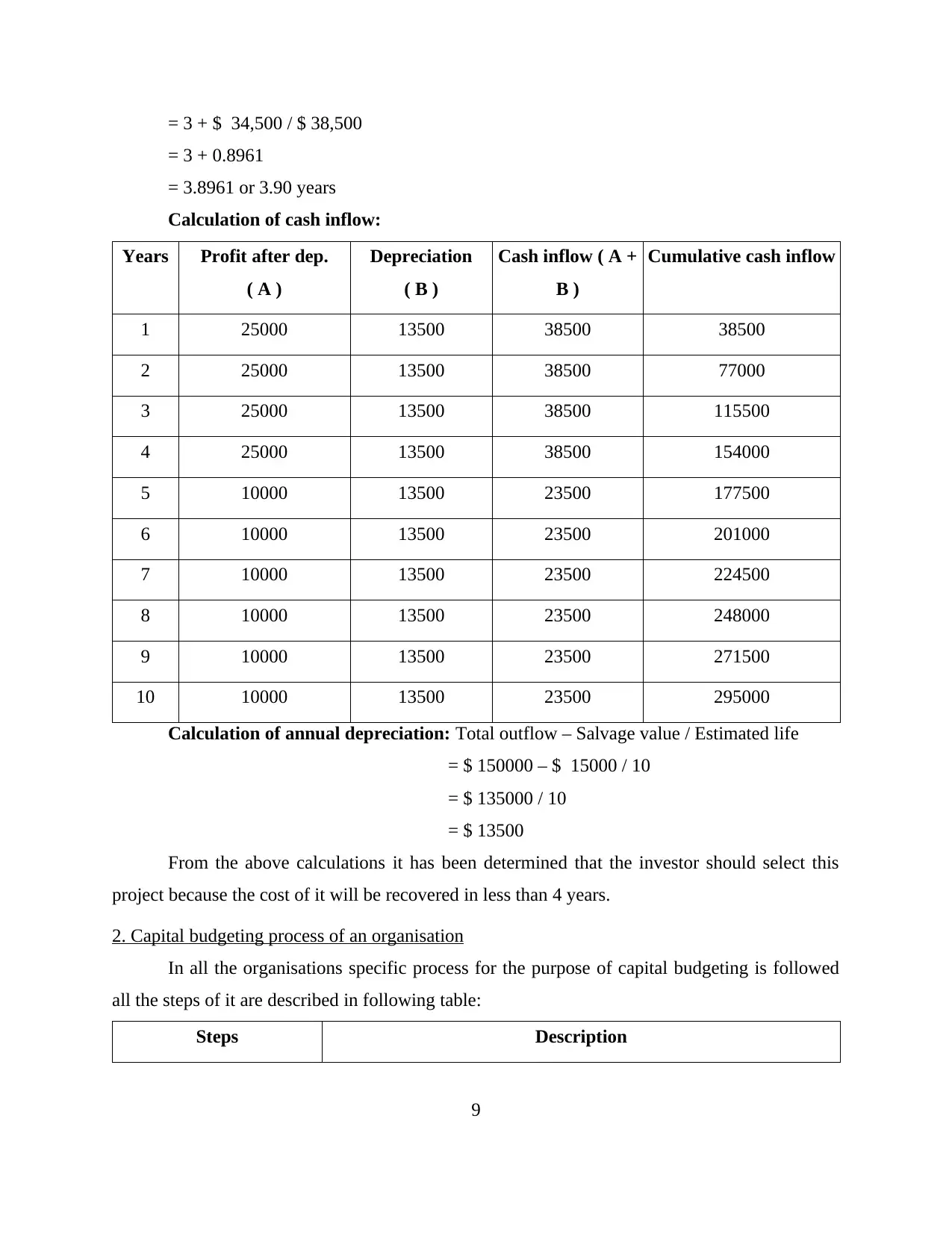

= 3 + $ 34,500 / $ 38,500

= 3 + 0.8961

= 3.8961 or 3.90 years

Calculation of cash inflow:

Years Profit after dep.

( A )

Depreciation

( B )

Cash inflow ( A +

B )

Cumulative cash inflow

1 25000 13500 38500 38500

2 25000 13500 38500 77000

3 25000 13500 38500 115500

4 25000 13500 38500 154000

5 10000 13500 23500 177500

6 10000 13500 23500 201000

7 10000 13500 23500 224500

8 10000 13500 23500 248000

9 10000 13500 23500 271500

10 10000 13500 23500 295000

Calculation of annual depreciation: Total outflow – Salvage value / Estimated life

= $ 150000 – $ 15000 / 10

= $ 135000 / 10

= $ 13500

From the above calculations it has been determined that the investor should select this

project because the cost of it will be recovered in less than 4 years.

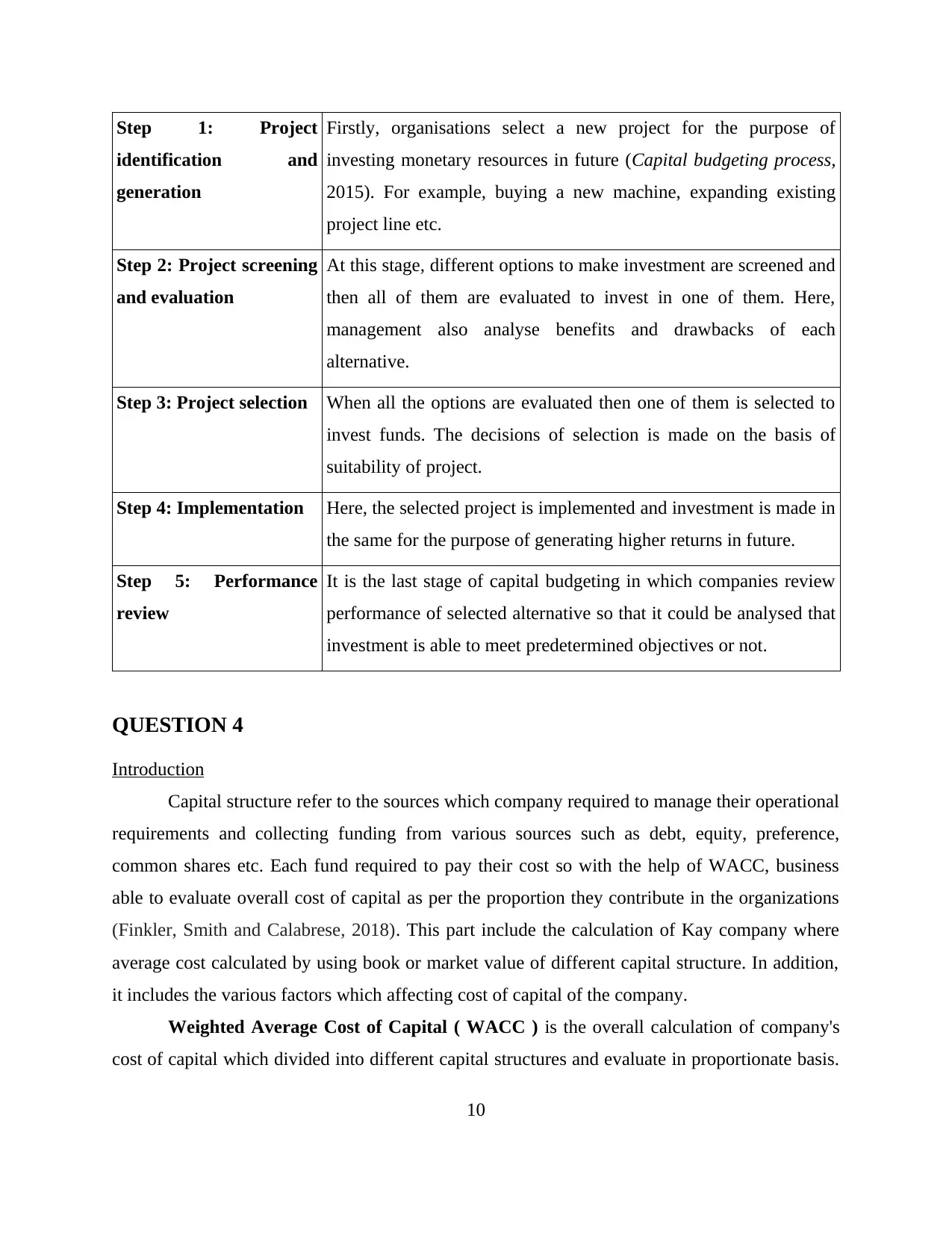

2. Capital budgeting process of an organisation

In all the organisations specific process for the purpose of capital budgeting is followed

all the steps of it are described in following table:

Steps Description

9

= 3 + 0.8961

= 3.8961 or 3.90 years

Calculation of cash inflow:

Years Profit after dep.

( A )

Depreciation

( B )

Cash inflow ( A +

B )

Cumulative cash inflow

1 25000 13500 38500 38500

2 25000 13500 38500 77000

3 25000 13500 38500 115500

4 25000 13500 38500 154000

5 10000 13500 23500 177500

6 10000 13500 23500 201000

7 10000 13500 23500 224500

8 10000 13500 23500 248000

9 10000 13500 23500 271500

10 10000 13500 23500 295000

Calculation of annual depreciation: Total outflow – Salvage value / Estimated life

= $ 150000 – $ 15000 / 10

= $ 135000 / 10

= $ 13500

From the above calculations it has been determined that the investor should select this

project because the cost of it will be recovered in less than 4 years.

2. Capital budgeting process of an organisation

In all the organisations specific process for the purpose of capital budgeting is followed

all the steps of it are described in following table:

Steps Description

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Step 1: Project

identification and

generation

Firstly, organisations select a new project for the purpose of

investing monetary resources in future (Capital budgeting process,

2015). For example, buying a new machine, expanding existing

project line etc.

Step 2: Project screening

and evaluation

At this stage, different options to make investment are screened and

then all of them are evaluated to invest in one of them. Here,

management also analyse benefits and drawbacks of each

alternative.

Step 3: Project selection When all the options are evaluated then one of them is selected to

invest funds. The decisions of selection is made on the basis of

suitability of project.

Step 4: Implementation Here, the selected project is implemented and investment is made in

the same for the purpose of generating higher returns in future.

Step 5: Performance

review

It is the last stage of capital budgeting in which companies review

performance of selected alternative so that it could be analysed that

investment is able to meet predetermined objectives or not.

QUESTION 4

Introduction

Capital structure refer to the sources which company required to manage their operational

requirements and collecting funding from various sources such as debt, equity, preference,

common shares etc. Each fund required to pay their cost so with the help of WACC, business

able to evaluate overall cost of capital as per the proportion they contribute in the organizations

(Finkler, Smith and Calabrese, 2018). This part include the calculation of Kay company where

average cost calculated by using book or market value of different capital structure. In addition,

it includes the various factors which affecting cost of capital of the company.

Weighted Average Cost of Capital ( WACC ) is the overall calculation of company's

cost of capital which divided into different capital structures and evaluate in proportionate basis.

10

identification and

generation

Firstly, organisations select a new project for the purpose of

investing monetary resources in future (Capital budgeting process,

2015). For example, buying a new machine, expanding existing

project line etc.

Step 2: Project screening

and evaluation

At this stage, different options to make investment are screened and

then all of them are evaluated to invest in one of them. Here,

management also analyse benefits and drawbacks of each

alternative.

Step 3: Project selection When all the options are evaluated then one of them is selected to

invest funds. The decisions of selection is made on the basis of

suitability of project.

Step 4: Implementation Here, the selected project is implemented and investment is made in

the same for the purpose of generating higher returns in future.

Step 5: Performance

review

It is the last stage of capital budgeting in which companies review

performance of selected alternative so that it could be analysed that

investment is able to meet predetermined objectives or not.

QUESTION 4

Introduction

Capital structure refer to the sources which company required to manage their operational

requirements and collecting funding from various sources such as debt, equity, preference,

common shares etc. Each fund required to pay their cost so with the help of WACC, business

able to evaluate overall cost of capital as per the proportion they contribute in the organizations

(Finkler, Smith and Calabrese, 2018). This part include the calculation of Kay company where

average cost calculated by using book or market value of different capital structure. In addition,

it includes the various factors which affecting cost of capital of the company.

Weighted Average Cost of Capital ( WACC ) is the overall calculation of company's

cost of capital which divided into different capital structures and evaluate in proportionate basis.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In the organizations, there are various source of capital such as debenture, preference shares,

common stocks, bonds, equity, other debt etc. Further calculation of WACC is mentioned below

along with the formula:

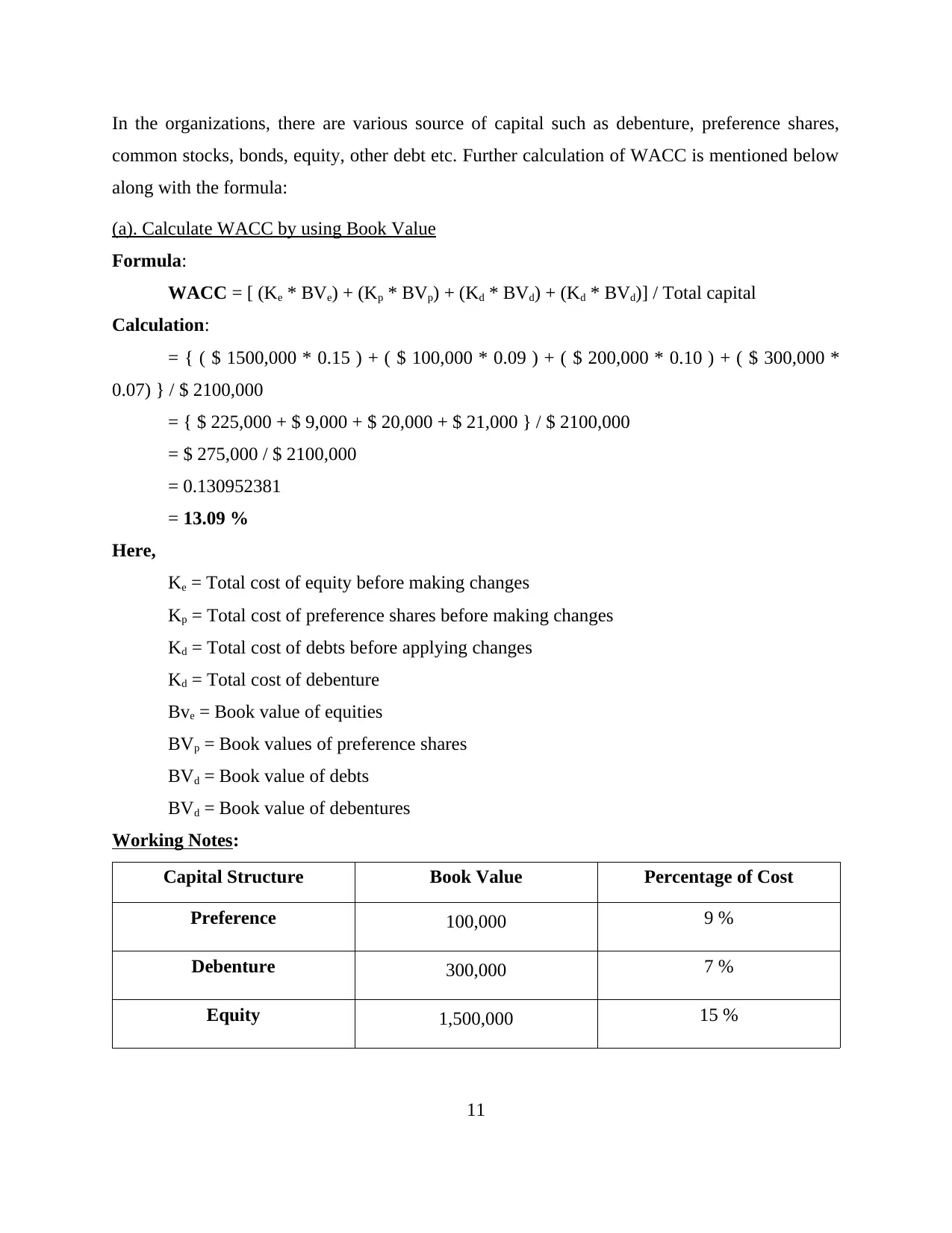

(a). Calculate WACC by using Book Value

Formula:

WACC = [ (Ke * BVe) + (Kp * BVp) + (Kd * BVd) + (Kd * BVd)] / Total capital

Calculation:

= { ( $ 1500,000 * 0.15 ) + ( $ 100,000 * 0.09 ) + ( $ 200,000 * 0.10 ) + ( $ 300,000 *

0.07) } / $ 2100,000

= { $ 225,000 + $ 9,000 + $ 20,000 + $ 21,000 } / $ 2100,000

= $ 275,000 / $ 2100,000

= 0.130952381

= 13.09 %

Here,

Ke = Total cost of equity before making changes

Kp = Total cost of preference shares before making changes

Kd = Total cost of debts before applying changes

Kd = Total cost of debenture

Bve = Book value of equities

BVp = Book values of preference shares

BVd = Book value of debts

BVd = Book value of debentures

Working Notes:

Capital Structure Book Value Percentage of Cost

Preference 100,000 9 %

Debenture 300,000 7 %

Equity 1,500,000 15 %

11

common stocks, bonds, equity, other debt etc. Further calculation of WACC is mentioned below

along with the formula:

(a). Calculate WACC by using Book Value

Formula:

WACC = [ (Ke * BVe) + (Kp * BVp) + (Kd * BVd) + (Kd * BVd)] / Total capital

Calculation:

= { ( $ 1500,000 * 0.15 ) + ( $ 100,000 * 0.09 ) + ( $ 200,000 * 0.10 ) + ( $ 300,000 *

0.07) } / $ 2100,000

= { $ 225,000 + $ 9,000 + $ 20,000 + $ 21,000 } / $ 2100,000

= $ 275,000 / $ 2100,000

= 0.130952381

= 13.09 %

Here,

Ke = Total cost of equity before making changes

Kp = Total cost of preference shares before making changes

Kd = Total cost of debts before applying changes

Kd = Total cost of debenture

Bve = Book value of equities

BVp = Book values of preference shares

BVd = Book value of debts

BVd = Book value of debentures

Working Notes:

Capital Structure Book Value Percentage of Cost

Preference 100,000 9 %

Debenture 300,000 7 %

Equity 1,500,000 15 %

11

Debt 200,000 10 %

Total Capital 21,00,000

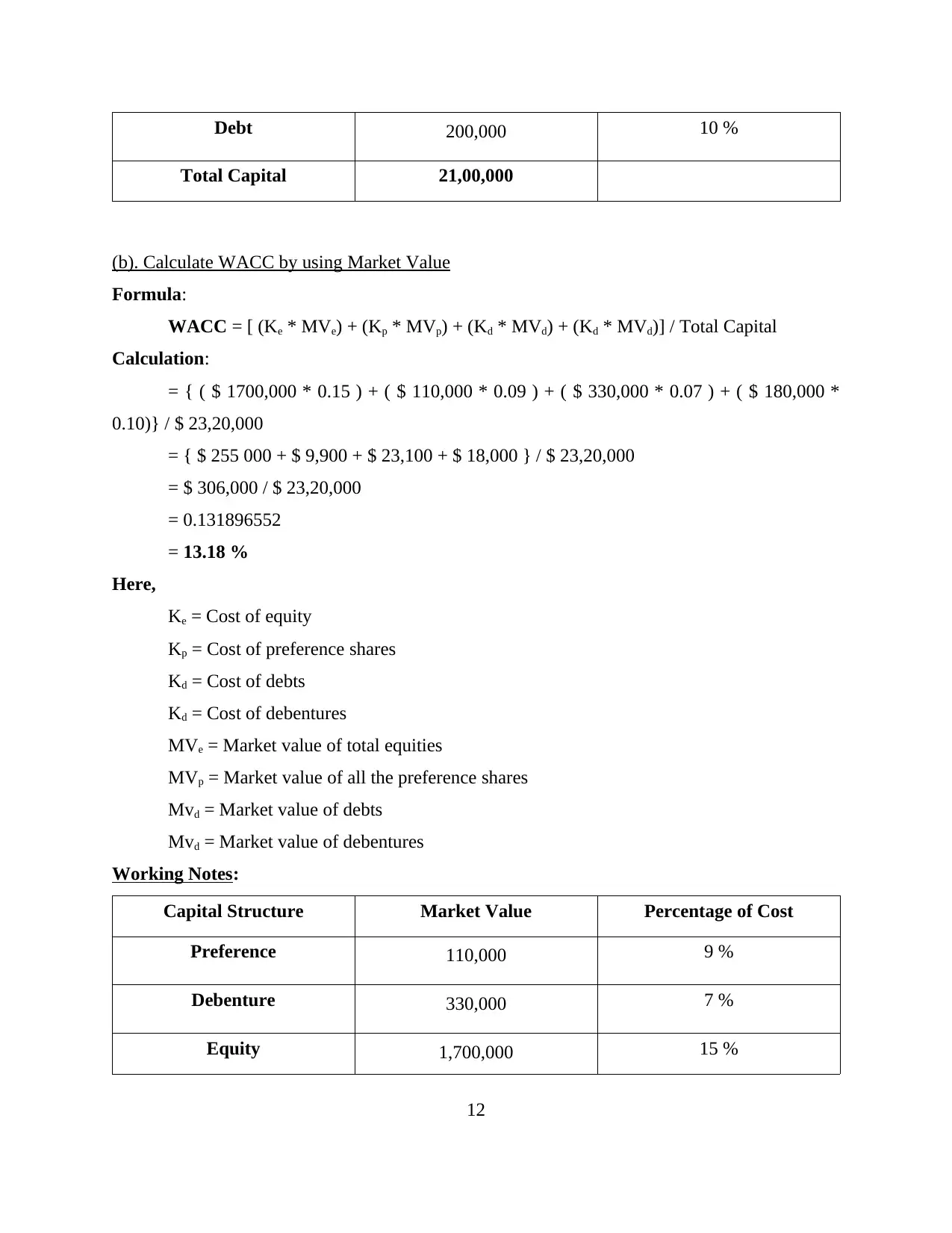

(b). Calculate WACC by using Market Value

Formula:

WACC = [ (Ke * MVe) + (Kp * MVp) + (Kd * MVd) + (Kd * MVd)] / Total Capital

Calculation:

= { ( $ 1700,000 * 0.15 ) + ( $ 110,000 * 0.09 ) + ( $ 330,000 * 0.07 ) + ( $ 180,000 *

0.10)} / $ 23,20,000

= { $ 255 000 + $ 9,900 + $ 23,100 + $ 18,000 } / $ 23,20,000

= $ 306,000 / $ 23,20,000

= 0.131896552

= 13.18 %

Here,

Ke = Cost of equity

Kp = Cost of preference shares

Kd = Cost of debts

Kd = Cost of debentures

MVe = Market value of total equities

MVp = Market value of all the preference shares

Mvd = Market value of debts

Mvd = Market value of debentures

Working Notes:

Capital Structure Market Value Percentage of Cost

Preference 110,000 9 %

Debenture 330,000 7 %

Equity 1,700,000 15 %

12

Total Capital 21,00,000

(b). Calculate WACC by using Market Value

Formula:

WACC = [ (Ke * MVe) + (Kp * MVp) + (Kd * MVd) + (Kd * MVd)] / Total Capital

Calculation:

= { ( $ 1700,000 * 0.15 ) + ( $ 110,000 * 0.09 ) + ( $ 330,000 * 0.07 ) + ( $ 180,000 *

0.10)} / $ 23,20,000

= { $ 255 000 + $ 9,900 + $ 23,100 + $ 18,000 } / $ 23,20,000

= $ 306,000 / $ 23,20,000

= 0.131896552

= 13.18 %

Here,

Ke = Cost of equity

Kp = Cost of preference shares

Kd = Cost of debts

Kd = Cost of debentures

MVe = Market value of total equities

MVp = Market value of all the preference shares

Mvd = Market value of debts

Mvd = Market value of debentures

Working Notes:

Capital Structure Market Value Percentage of Cost

Preference 110,000 9 %

Debenture 330,000 7 %

Equity 1,700,000 15 %

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.