Comprehensive Financial Management: Capital Budgeting & Analysis

VerifiedAdded on 2023/04/21

|14

|2117

|81

Homework Assignment

AI Summary

This document provides a comprehensive solution to a Financial Management assignment, covering key areas such as ratio analysis and capital budgeting. Part A addresses theoretical questions related to institutional vs. individual investors, illiquid investments, fundamental analysis, ratio analysis, and capital budgeting methods like Net Present Value (NPV), Payback Period, and Internal Rate of Return (IRR). Part B includes practical exercises involving activity ratios, sustainable growth rate calculation, and cash flow statement analysis. The solution demonstrates the application of financial concepts and provides insights into investment decision-making. Desklib offers similar solved assignments and resources to support students in their studies.

Running Head: FINANCIAL MANAGEMENT 0

FINANCIAL MANAGEMENT

FINANCIAL MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL MANAGEMENT 1

Contents

Part A...............................................................................................................................................2

Question 1........................................................................................................................................2

Question 2........................................................................................................................................2

Question 3........................................................................................................................................2

Question 4........................................................................................................................................2

Question 5........................................................................................................................................2

Question 7........................................................................................................................................2

PART B...........................................................................................................................................3

Exercise 1.........................................................................................................................................3

Part a............................................................................................................................................3

Part b............................................................................................................................................4

Exercise 2.........................................................................................................................................5

Exercise 3.........................................................................................................................................5

Part a)...........................................................................................................................................5

Part b)...........................................................................................................................................5

Exercise 4.........................................................................................................................................6

Part I)............................................................................................................................................6

Part II)..........................................................................................................................................6

Contents

Part A...............................................................................................................................................2

Question 1........................................................................................................................................2

Question 2........................................................................................................................................2

Question 3........................................................................................................................................2

Question 4........................................................................................................................................2

Question 5........................................................................................................................................2

Question 7........................................................................................................................................2

PART B...........................................................................................................................................3

Exercise 1.........................................................................................................................................3

Part a............................................................................................................................................3

Part b............................................................................................................................................4

Exercise 2.........................................................................................................................................5

Exercise 3.........................................................................................................................................5

Part a)...........................................................................................................................................5

Part b)...........................................................................................................................................5

Exercise 4.........................................................................................................................................6

Part I)............................................................................................................................................6

Part II)..........................................................................................................................................6

FINANCIAL MANAGEMENT 2

References........................................................................................................................................7

References........................................................................................................................................7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL MANAGEMENT 3

Part A

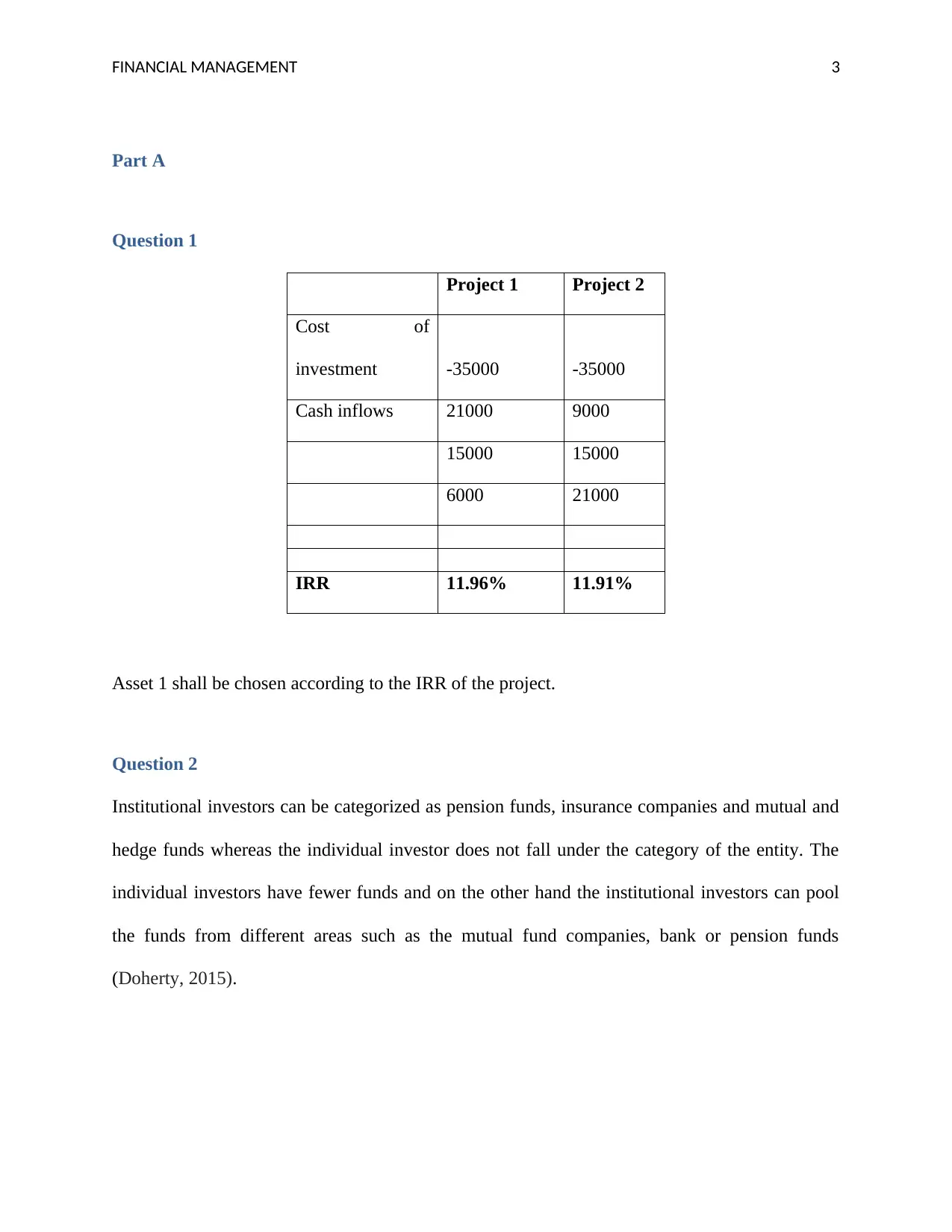

Question 1

Project 1 Project 2

Cost of

investment -35000 -35000

Cash inflows 21000 9000

15000 15000

6000 21000

IRR 11.96% 11.91%

Asset 1 shall be chosen according to the IRR of the project.

Question 2

Institutional investors can be categorized as pension funds, insurance companies and mutual and

hedge funds whereas the individual investor does not fall under the category of the entity. The

individual investors have fewer funds and on the other hand the institutional investors can pool

the funds from different areas such as the mutual fund companies, bank or pension funds

(Doherty, 2015).

Part A

Question 1

Project 1 Project 2

Cost of

investment -35000 -35000

Cash inflows 21000 9000

15000 15000

6000 21000

IRR 11.96% 11.91%

Asset 1 shall be chosen according to the IRR of the project.

Question 2

Institutional investors can be categorized as pension funds, insurance companies and mutual and

hedge funds whereas the individual investor does not fall under the category of the entity. The

individual investors have fewer funds and on the other hand the institutional investors can pool

the funds from different areas such as the mutual fund companies, bank or pension funds

(Doherty, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL MANAGEMENT 4

Question 3

The illiquid investment can be described as the asset that cannot be readily converted into cash

on selling. This happens mainly because of the lack of the interest of the buyers or non-

establishment of the trading market. One examples of such stock is collectibles art and antique,

Liquid investments are those investments which can be converted into cash. One example of

such investment is marketable securities (Campbell, 2015).

Question 4

Fundamental analysis is the process of supervising the fundamental level of the business such as

sales, earnings, potential assets, debt management, products and the competition. Fundamental

analysis is performed on the historical and the present data but with the intention of the making

the financial forecasts. There are further objectives and the goals for which the fundamental

analysis is carried on to conduct a company’s stock valuation and predict its probable price, to

evaluate, the management and the business decisions are calculated (Steinbrook, 2015).

Question 5

Ratio analysis is a technique which is used for the measurement of the financial position of the

company. Generally the ratios depict the position of the company in the form of the liquidity,

efficiency, profitability and the market stability. Most of times the ratio analysis technique is

successful when compared to the previous year or against the industry benchmarks, however one

of the biggest disadvantages it carries is, that it depicts the monetary comparison and avoids the

factors like key intangibles, like brand and relationships also (Uechi, et al 2015).

Question 3

The illiquid investment can be described as the asset that cannot be readily converted into cash

on selling. This happens mainly because of the lack of the interest of the buyers or non-

establishment of the trading market. One examples of such stock is collectibles art and antique,

Liquid investments are those investments which can be converted into cash. One example of

such investment is marketable securities (Campbell, 2015).

Question 4

Fundamental analysis is the process of supervising the fundamental level of the business such as

sales, earnings, potential assets, debt management, products and the competition. Fundamental

analysis is performed on the historical and the present data but with the intention of the making

the financial forecasts. There are further objectives and the goals for which the fundamental

analysis is carried on to conduct a company’s stock valuation and predict its probable price, to

evaluate, the management and the business decisions are calculated (Steinbrook, 2015).

Question 5

Ratio analysis is a technique which is used for the measurement of the financial position of the

company. Generally the ratios depict the position of the company in the form of the liquidity,

efficiency, profitability and the market stability. Most of times the ratio analysis technique is

successful when compared to the previous year or against the industry benchmarks, however one

of the biggest disadvantages it carries is, that it depicts the monetary comparison and avoids the

factors like key intangibles, like brand and relationships also (Uechi, et al 2015).

FINANCIAL MANAGEMENT 5

Question 7

The various methods of the capital budgeting are net present value, payback period, internal rate

of return and profitability index. These methods are required to make the investment decisions.

Currently the profitability index or the IRR method is most widely used in the process of the

decision making. In simpler terms if explained the net present value is the difference of the

inflows and the outflows of the cash. The positive NPV indicates that the investment can be

selected. Payback period on the other hand can be determined as the time period in which the

cost of the investment can be recovered by the company.

The major importance of the NPV method is that it considers the concept off time value of

money and also helps in maximization of the value of the firm. The only biggest disadvantage

this method carries is that, if the two projects are not exclusive mutually then the comparison is

impossible. The premium advantage for calculating the payback period is that it is the simplest

method to calculate and it can be treated as a measure of the risk inheritance of the project

(Bhutto, Abbas, Rehman and Shah, 2015). On the contrary the disadvantage of the payback

period is that it ignores the time value of money. It does not account for the cash flow that occurs

after the payback period. The IRR commonly known as the internal rate of return is the rate that

is used in the capital budgeting to estimate the real potential of the investments. The internal rate

of return is a discount that makes the present value of the investment equals to zero. The

advantages of the time value of money is considered and it’s simple to interpret after the IRR is

calculated. The economies of scale are ignored and moreover there are certain assumptions of

reinvestment rate of return for the remaining period of the investment or proposal. Therefore

these are the capital budgeting methods that are used to make the investment decisions (Bülow,

2017).

Question 7

The various methods of the capital budgeting are net present value, payback period, internal rate

of return and profitability index. These methods are required to make the investment decisions.

Currently the profitability index or the IRR method is most widely used in the process of the

decision making. In simpler terms if explained the net present value is the difference of the

inflows and the outflows of the cash. The positive NPV indicates that the investment can be

selected. Payback period on the other hand can be determined as the time period in which the

cost of the investment can be recovered by the company.

The major importance of the NPV method is that it considers the concept off time value of

money and also helps in maximization of the value of the firm. The only biggest disadvantage

this method carries is that, if the two projects are not exclusive mutually then the comparison is

impossible. The premium advantage for calculating the payback period is that it is the simplest

method to calculate and it can be treated as a measure of the risk inheritance of the project

(Bhutto, Abbas, Rehman and Shah, 2015). On the contrary the disadvantage of the payback

period is that it ignores the time value of money. It does not account for the cash flow that occurs

after the payback period. The IRR commonly known as the internal rate of return is the rate that

is used in the capital budgeting to estimate the real potential of the investments. The internal rate

of return is a discount that makes the present value of the investment equals to zero. The

advantages of the time value of money is considered and it’s simple to interpret after the IRR is

calculated. The economies of scale are ignored and moreover there are certain assumptions of

reinvestment rate of return for the remaining period of the investment or proposal. Therefore

these are the capital budgeting methods that are used to make the investment decisions (Bülow,

2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

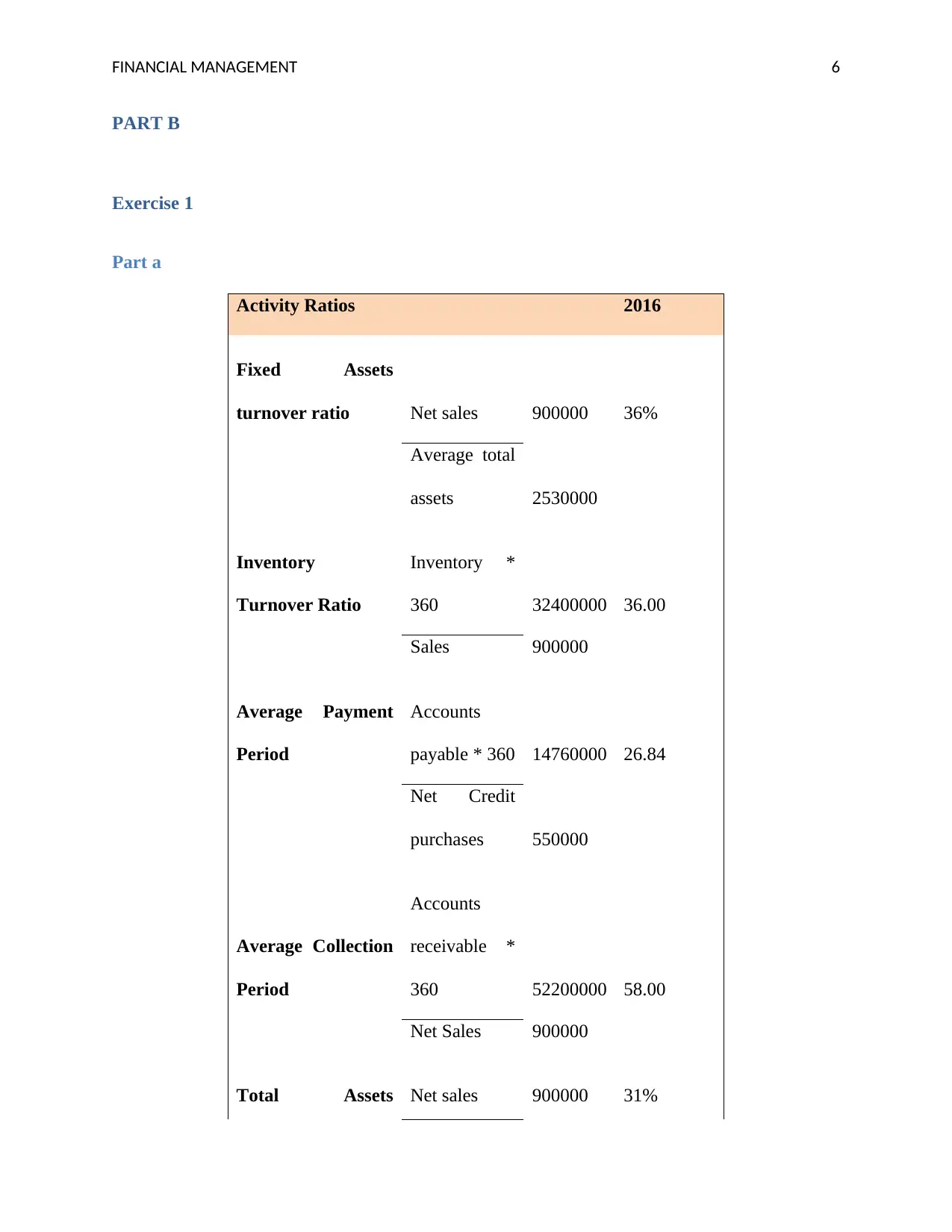

FINANCIAL MANAGEMENT 6

PART B

Exercise 1

Part a

Activity Ratios 2016

Fixed Assets

turnover ratio Net sales 900000 36%

Average total

assets 2530000

Inventory

Turnover Ratio

Inventory *

360 32400000 36.00

Sales 900000

Average Payment

Period

Accounts

payable * 360 14760000 26.84

Net Credit

purchases 550000

Average Collection

Period

Accounts

receivable *

360 52200000 58.00

Net Sales 900000

Total Assets Net sales 900000 31%

PART B

Exercise 1

Part a

Activity Ratios 2016

Fixed Assets

turnover ratio Net sales 900000 36%

Average total

assets 2530000

Inventory

Turnover Ratio

Inventory *

360 32400000 36.00

Sales 900000

Average Payment

Period

Accounts

payable * 360 14760000 26.84

Net Credit

purchases 550000

Average Collection

Period

Accounts

receivable *

360 52200000 58.00

Net Sales 900000

Total Assets Net sales 900000 31%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

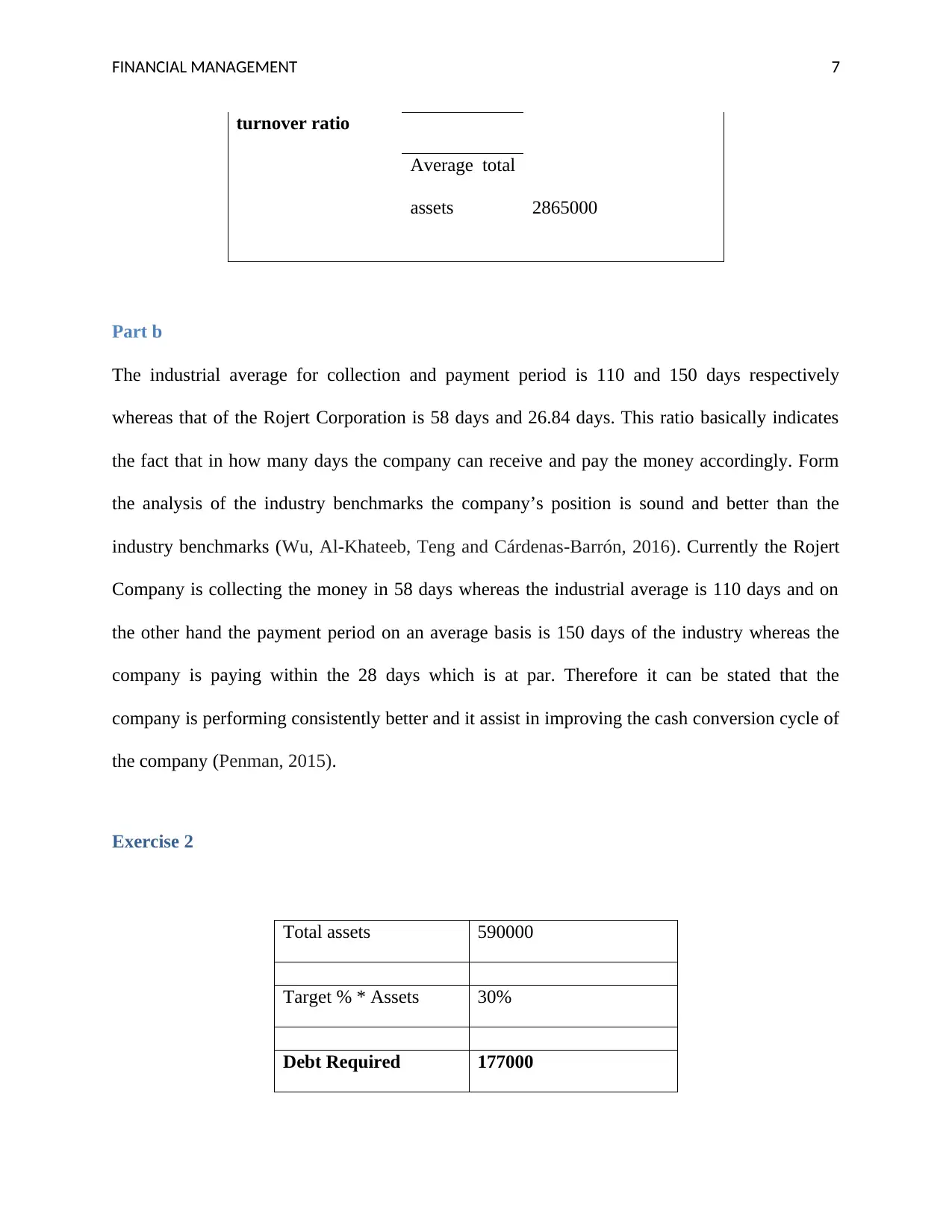

FINANCIAL MANAGEMENT 7

turnover ratio

Average total

assets 2865000

Part b

The industrial average for collection and payment period is 110 and 150 days respectively

whereas that of the Rojert Corporation is 58 days and 26.84 days. This ratio basically indicates

the fact that in how many days the company can receive and pay the money accordingly. Form

the analysis of the industry benchmarks the company’s position is sound and better than the

industry benchmarks (Wu, Al-Khateeb, Teng and Cárdenas-Barrón, 2016). Currently the Rojert

Company is collecting the money in 58 days whereas the industrial average is 110 days and on

the other hand the payment period on an average basis is 150 days of the industry whereas the

company is paying within the 28 days which is at par. Therefore it can be stated that the

company is performing consistently better and it assist in improving the cash conversion cycle of

the company (Penman, 2015).

Exercise 2

Total assets 590000

Target % * Assets 30%

Debt Required 177000

turnover ratio

Average total

assets 2865000

Part b

The industrial average for collection and payment period is 110 and 150 days respectively

whereas that of the Rojert Corporation is 58 days and 26.84 days. This ratio basically indicates

the fact that in how many days the company can receive and pay the money accordingly. Form

the analysis of the industry benchmarks the company’s position is sound and better than the

industry benchmarks (Wu, Al-Khateeb, Teng and Cárdenas-Barrón, 2016). Currently the Rojert

Company is collecting the money in 58 days whereas the industrial average is 110 days and on

the other hand the payment period on an average basis is 150 days of the industry whereas the

company is paying within the 28 days which is at par. Therefore it can be stated that the

company is performing consistently better and it assist in improving the cash conversion cycle of

the company (Penman, 2015).

Exercise 2

Total assets 590000

Target % * Assets 30%

Debt Required 177000

FINANCIAL MANAGEMENT 8

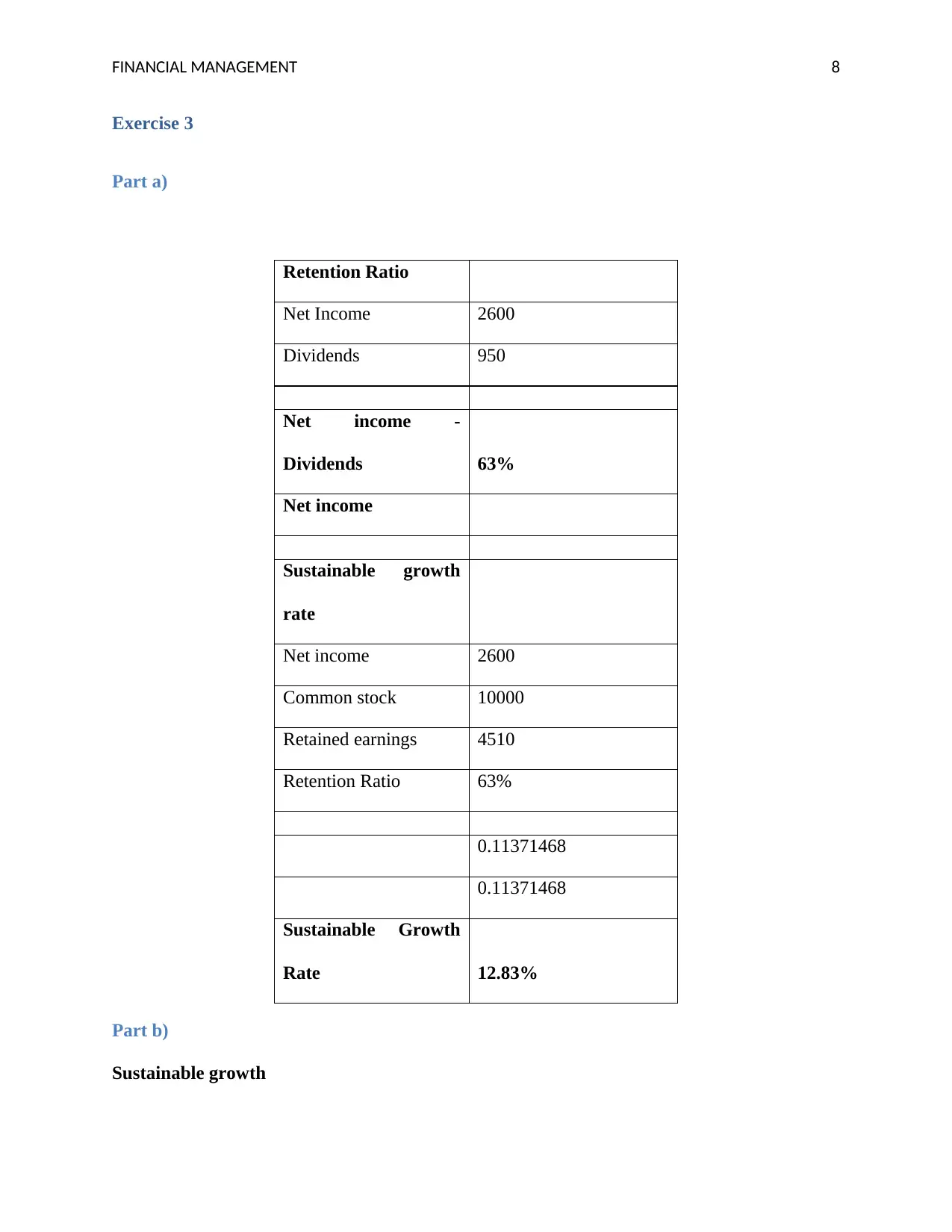

Exercise 3

Part a)

Retention Ratio

Net Income 2600

Dividends 950

Net income -

Dividends 63%

Net income

Sustainable growth

rate

Net income 2600

Common stock 10000

Retained earnings 4510

Retention Ratio 63%

0.11371468

0.11371468

Sustainable Growth

Rate 12.83%

Part b)

Sustainable growth

Exercise 3

Part a)

Retention Ratio

Net Income 2600

Dividends 950

Net income -

Dividends 63%

Net income

Sustainable growth

rate

Net income 2600

Common stock 10000

Retained earnings 4510

Retention Ratio 63%

0.11371468

0.11371468

Sustainable Growth

Rate 12.83%

Part b)

Sustainable growth

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL MANAGEMENT 9

Sustainable growth rate can be termed as the maximum growth rate which can be achieved by

the company through maintenance of the constant debt to equity ratio, exclusive of any external

financing. The sustainable growth rate assists the corporation in the overall growth by

maximizing the sales and the growth of the revenue without increasing the financial leverage that

means the company is safe in terms of the financial distress (Kalemli-Ozcan, Kamil and

Villegas-Sanchez, 2016).

The SGR of the company can reflect the working style of the company, mainly with regards to

the handling of the daily expenses and whether the company is paying the bills on time and

managing the payables or short term debts or not. In this way the company can grow if the

proper scrutiny of the accounts is done and if the company comes across any variance the same

can be rectified immediately. This not only provides the financial stability to the company but

also helps in enhancing the social sustainability (DeFusco, McLeavey Pinto, Anson and Runkle,

2015).

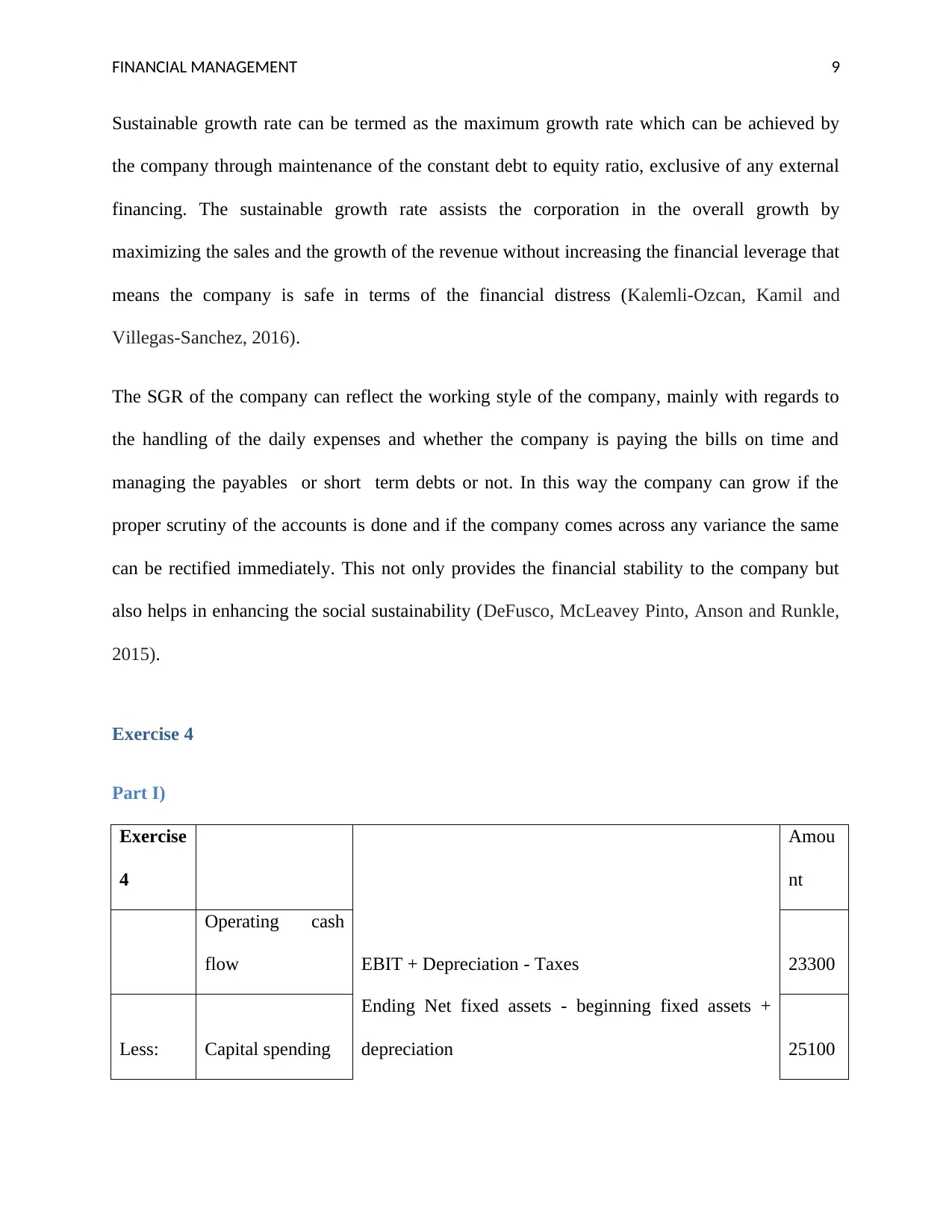

Exercise 4

Part I)

Exercise

4

Amou

nt

Operating cash

flow EBIT + Depreciation - Taxes 23300

Less: Capital spending

Ending Net fixed assets - beginning fixed assets +

depreciation 25100

Sustainable growth rate can be termed as the maximum growth rate which can be achieved by

the company through maintenance of the constant debt to equity ratio, exclusive of any external

financing. The sustainable growth rate assists the corporation in the overall growth by

maximizing the sales and the growth of the revenue without increasing the financial leverage that

means the company is safe in terms of the financial distress (Kalemli-Ozcan, Kamil and

Villegas-Sanchez, 2016).

The SGR of the company can reflect the working style of the company, mainly with regards to

the handling of the daily expenses and whether the company is paying the bills on time and

managing the payables or short term debts or not. In this way the company can grow if the

proper scrutiny of the accounts is done and if the company comes across any variance the same

can be rectified immediately. This not only provides the financial stability to the company but

also helps in enhancing the social sustainability (DeFusco, McLeavey Pinto, Anson and Runkle,

2015).

Exercise 4

Part I)

Exercise

4

Amou

nt

Operating cash

flow EBIT + Depreciation - Taxes 23300

Less: Capital spending

Ending Net fixed assets - beginning fixed assets +

depreciation 25100

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL MANAGEMENT 10

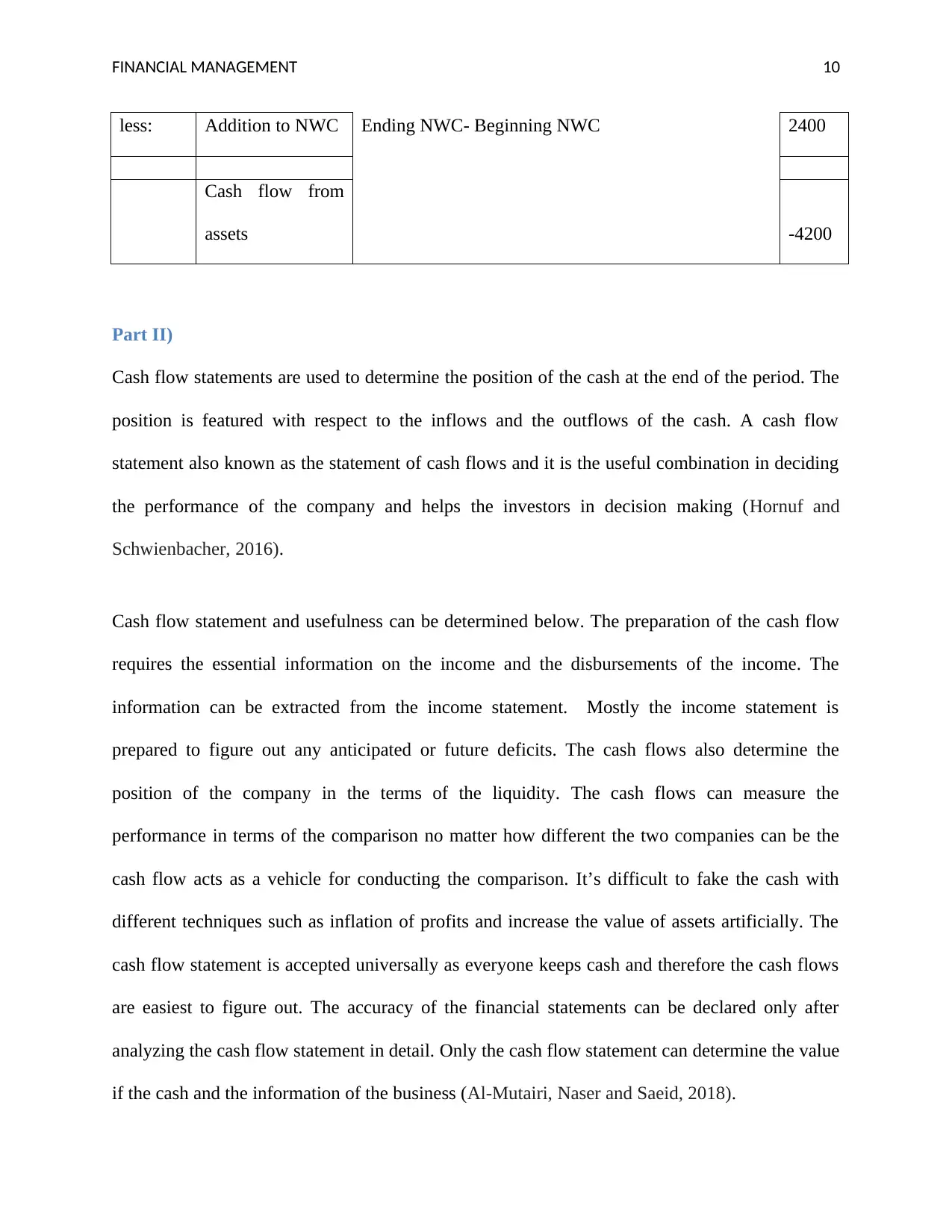

less: Addition to NWC Ending NWC- Beginning NWC 2400

Cash flow from

assets -4200

Part II)

Cash flow statements are used to determine the position of the cash at the end of the period. The

position is featured with respect to the inflows and the outflows of the cash. A cash flow

statement also known as the statement of cash flows and it is the useful combination in deciding

the performance of the company and helps the investors in decision making (Hornuf and

Schwienbacher, 2016).

Cash flow statement and usefulness can be determined below. The preparation of the cash flow

requires the essential information on the income and the disbursements of the income. The

information can be extracted from the income statement. Mostly the income statement is

prepared to figure out any anticipated or future deficits. The cash flows also determine the

position of the company in the terms of the liquidity. The cash flows can measure the

performance in terms of the comparison no matter how different the two companies can be the

cash flow acts as a vehicle for conducting the comparison. It’s difficult to fake the cash with

different techniques such as inflation of profits and increase the value of assets artificially. The

cash flow statement is accepted universally as everyone keeps cash and therefore the cash flows

are easiest to figure out. The accuracy of the financial statements can be declared only after

analyzing the cash flow statement in detail. Only the cash flow statement can determine the value

if the cash and the information of the business (Al-Mutairi, Naser and Saeid, 2018).

less: Addition to NWC Ending NWC- Beginning NWC 2400

Cash flow from

assets -4200

Part II)

Cash flow statements are used to determine the position of the cash at the end of the period. The

position is featured with respect to the inflows and the outflows of the cash. A cash flow

statement also known as the statement of cash flows and it is the useful combination in deciding

the performance of the company and helps the investors in decision making (Hornuf and

Schwienbacher, 2016).

Cash flow statement and usefulness can be determined below. The preparation of the cash flow

requires the essential information on the income and the disbursements of the income. The

information can be extracted from the income statement. Mostly the income statement is

prepared to figure out any anticipated or future deficits. The cash flows also determine the

position of the company in the terms of the liquidity. The cash flows can measure the

performance in terms of the comparison no matter how different the two companies can be the

cash flow acts as a vehicle for conducting the comparison. It’s difficult to fake the cash with

different techniques such as inflation of profits and increase the value of assets artificially. The

cash flow statement is accepted universally as everyone keeps cash and therefore the cash flows

are easiest to figure out. The accuracy of the financial statements can be declared only after

analyzing the cash flow statement in detail. Only the cash flow statement can determine the value

if the cash and the information of the business (Al-Mutairi, Naser and Saeid, 2018).

FINANCIAL MANAGEMENT 11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.