BTEC HND Management Accounting Report: Cost Analysis and Planning

VerifiedAdded on 2023/03/20

|16

|4364

|78

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and their application within a manufacturing context, specifically Tech (UK) Ltd. It delves into the significance of management accounting as a decision-making tool, contrasting it with financial accounting, and explores various management accounting systems, including cost accounting and inventory management. The report then examines different types of management accounting reports, such as budgeting, job cost, and performance reports, highlighting their importance in minimizing losses and enhancing financial returns. Furthermore, it analyzes cost analysis techniques, differentiating between fixed and variable costs, and applying absorption and marginal costing methods. Finally, the report discusses planning tools used for budgetary control, exploring their advantages and disadvantages, and addresses the adaptation of management accounting systems to overcome financial issues. The report concludes with a discussion of the advantages of different management accounting systems.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and different types of management accounting systems...............1

P2 Different types of management accounting reports...............................................................3

D1................................................................................................................................................5

TASK 2............................................................................................................................................5

P3 Calculation of cost after application cost analysis techniques...............................................5

M2...............................................................................................................................................9

D2................................................................................................................................................9

TASK 3............................................................................................................................................9

P4 Advantages and disadvantages of different types of planning tools used for budgetary

control.........................................................................................................................................9

M3.............................................................................................................................................11

D3..............................................................................................................................................11

P5 Adaptation of management accounting systems to overcome from financial issues...........11

M4.............................................................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and different types of management accounting systems...............1

P2 Different types of management accounting reports...............................................................3

D1................................................................................................................................................5

TASK 2............................................................................................................................................5

P3 Calculation of cost after application cost analysis techniques...............................................5

M2...............................................................................................................................................9

D2................................................................................................................................................9

TASK 3............................................................................................................................................9

P4 Advantages and disadvantages of different types of planning tools used for budgetary

control.........................................................................................................................................9

M3.............................................................................................................................................11

D3..............................................................................................................................................11

P5 Adaptation of management accounting systems to overcome from financial issues...........11

M4.............................................................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting is important concept which contributes in enhancing the

decision making power of internal parties. It is broad concept which includes the provisions of

cost and managerial accounting. Through application of such provisions different kind of

accounts are formulate which depicts the performance of different departments. It further helps

in improvement of the understanding among the different team members which provides

collective efforts in accomplishment of desired objectives of organisation. Large number of

benefits are gathered by organisation through implementation of such accounting provisions like

strategic planning, risk management etc. Tech (UK)Ltd. Is manufacturing organisation which

prepare special chargers for retailers (Zimmerman and Yahya-Zadeh, 2011).

In the present report explain about, management accounting and their requirement in

effective operation of business activities, application of different methods of management

accounting reports and their importance for organisation and application of marginal and

absorption costing in preparation of income statement. Also, advantages and disadvantages of

different type of planning tools used for budgetary control and adaption of effective accounting

technique to overcome from financial issues.

TASK 1

P1 Management accounting and different types of management accounting systems

Management accounting is a procedure of preparing management accounts and reports

which gives timely and accurate statistical information which are needed through managers in

order to make all short term and daily decisions. In this, employers use provisions related to

accounting information in order to take better or effective decisions and control management

functions as well. Management accounting consists process regarding analysis, determination,

execution of the accounting information with the help of cost accounting and managerial

Management accounting is important concept which contributes in enhancing the

decision making power of internal parties. It is broad concept which includes the provisions of

cost and managerial accounting. Through application of such provisions different kind of

accounts are formulate which depicts the performance of different departments. It further helps

in improvement of the understanding among the different team members which provides

collective efforts in accomplishment of desired objectives of organisation. Large number of

benefits are gathered by organisation through implementation of such accounting provisions like

strategic planning, risk management etc. Tech (UK)Ltd. Is manufacturing organisation which

prepare special chargers for retailers (Zimmerman and Yahya-Zadeh, 2011).

In the present report explain about, management accounting and their requirement in

effective operation of business activities, application of different methods of management

accounting reports and their importance for organisation and application of marginal and

absorption costing in preparation of income statement. Also, advantages and disadvantages of

different type of planning tools used for budgetary control and adaption of effective accounting

technique to overcome from financial issues.

TASK 1

P1 Management accounting and different types of management accounting systems

Management accounting is a procedure of preparing management accounts and reports

which gives timely and accurate statistical information which are needed through managers in

order to make all short term and daily decisions. In this, employers use provisions related to

accounting information in order to take better or effective decisions and control management

functions as well. Management accounting consists process regarding analysis, determination,

execution of the accounting information with the help of cost accounting and managerial

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

principles. It offers effective opportunities to Tech (UK) Ltd manager to develop better policies

in order to achieving aims and goals with in given period of time.

Importance of management accounting as decision-making tool

Tech (UK) Ltd. is a manufacturer of mobile telephones, special chargers and the other

different gadgets for retail stored in United Kingdom. It provides special features in its mobile

phones so that people can be attracted. The main issues which Tech(UK)Ltd. Faced is lack of

finance related information which develops negative impact on the decision making of business

firm. In addition to this, management accounting consists cost accounting provisions. It will be

helpful for firm to improve performance level of the various departments. Some of the

importance of management accounting given below as above:

Rate of return evaluation- Effective provisions of management accounting is helpful in

evaluation of return those are regarded with the various projects. It is contribute those projects

which are profitable and also improve earnings (Weißenberger and Angelkort, 2011).

Forecasting of cash flows- It assess in estimation of cash flow in company with in the

particular time period. It gives better opportunity to manage its all future transactions on the

basis of working capital availability.

Variances predictions- It is a necessary function and helpful in determine deviations in

performance of staff members and then compare them with actual standards. It is helpful to use

the analytical, tool in order to sustain positive variances.

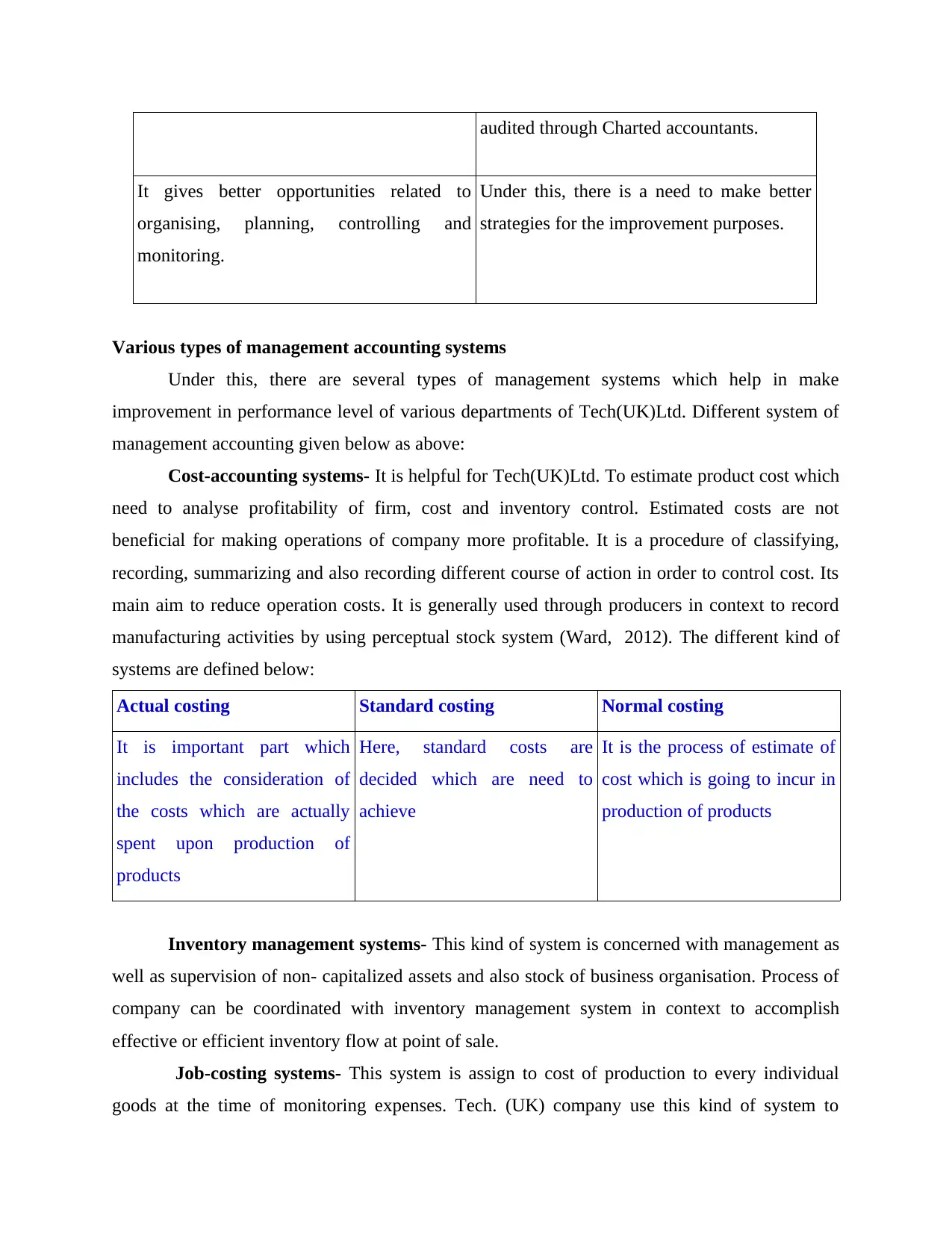

Difference between management and financial accounting

Management Accounting Financial Accounting

It is helpful for managers to take effective

decisions which can satisfy goals as

objectives of firm.

Under this, there is a need of communicate

financial position of firm to related users.

Its primary users are internal and these are

managers of firm.

Its users are external and these banks,

suppliers, investors and regulators.

These types of statements are used for

internal use not needed to audited through

Charted accountants.

Under this, these statements are published

for the use of general public and then sent

to the shareholders. There is a need to

in order to achieving aims and goals with in given period of time.

Importance of management accounting as decision-making tool

Tech (UK) Ltd. is a manufacturer of mobile telephones, special chargers and the other

different gadgets for retail stored in United Kingdom. It provides special features in its mobile

phones so that people can be attracted. The main issues which Tech(UK)Ltd. Faced is lack of

finance related information which develops negative impact on the decision making of business

firm. In addition to this, management accounting consists cost accounting provisions. It will be

helpful for firm to improve performance level of the various departments. Some of the

importance of management accounting given below as above:

Rate of return evaluation- Effective provisions of management accounting is helpful in

evaluation of return those are regarded with the various projects. It is contribute those projects

which are profitable and also improve earnings (Weißenberger and Angelkort, 2011).

Forecasting of cash flows- It assess in estimation of cash flow in company with in the

particular time period. It gives better opportunity to manage its all future transactions on the

basis of working capital availability.

Variances predictions- It is a necessary function and helpful in determine deviations in

performance of staff members and then compare them with actual standards. It is helpful to use

the analytical, tool in order to sustain positive variances.

Difference between management and financial accounting

Management Accounting Financial Accounting

It is helpful for managers to take effective

decisions which can satisfy goals as

objectives of firm.

Under this, there is a need of communicate

financial position of firm to related users.

Its primary users are internal and these are

managers of firm.

Its users are external and these banks,

suppliers, investors and regulators.

These types of statements are used for

internal use not needed to audited through

Charted accountants.

Under this, these statements are published

for the use of general public and then sent

to the shareholders. There is a need to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

audited through Charted accountants.

It gives better opportunities related to

organising, planning, controlling and

monitoring.

Under this, there is a need to make better

strategies for the improvement purposes.

Various types of management accounting systems

Under this, there are several types of management systems which help in make

improvement in performance level of various departments of Tech(UK)Ltd. Different system of

management accounting given below as above:

Cost-accounting systems- It is helpful for Tech(UK)Ltd. To estimate product cost which

need to analyse profitability of firm, cost and inventory control. Estimated costs are not

beneficial for making operations of company more profitable. It is a procedure of classifying,

recording, summarizing and also recording different course of action in order to control cost. Its

main aim to reduce operation costs. It is generally used through producers in context to record

manufacturing activities by using perceptual stock system (Ward, 2012). The different kind of

systems are defined below:

Actual costing Standard costing Normal costing

It is important part which

includes the consideration of

the costs which are actually

spent upon production of

products

Here, standard costs are

decided which are need to

achieve

It is the process of estimate of

cost which is going to incur in

production of products

Inventory management systems- This kind of system is concerned with management as

well as supervision of non- capitalized assets and also stock of business organisation. Process of

company can be coordinated with inventory management system in context to accomplish

effective or efficient inventory flow at point of sale.

Job-costing systems- This system is assign to cost of production to every individual

goods at the time of monitoring expenses. Tech. (UK) company use this kind of system to

It gives better opportunities related to

organising, planning, controlling and

monitoring.

Under this, there is a need to make better

strategies for the improvement purposes.

Various types of management accounting systems

Under this, there are several types of management systems which help in make

improvement in performance level of various departments of Tech(UK)Ltd. Different system of

management accounting given below as above:

Cost-accounting systems- It is helpful for Tech(UK)Ltd. To estimate product cost which

need to analyse profitability of firm, cost and inventory control. Estimated costs are not

beneficial for making operations of company more profitable. It is a procedure of classifying,

recording, summarizing and also recording different course of action in order to control cost. Its

main aim to reduce operation costs. It is generally used through producers in context to record

manufacturing activities by using perceptual stock system (Ward, 2012). The different kind of

systems are defined below:

Actual costing Standard costing Normal costing

It is important part which

includes the consideration of

the costs which are actually

spent upon production of

products

Here, standard costs are

decided which are need to

achieve

It is the process of estimate of

cost which is going to incur in

production of products

Inventory management systems- This kind of system is concerned with management as

well as supervision of non- capitalized assets and also stock of business organisation. Process of

company can be coordinated with inventory management system in context to accomplish

effective or efficient inventory flow at point of sale.

Job-costing systems- This system is assign to cost of production to every individual

goods at the time of monitoring expenses. Tech. (UK) company use this kind of system to

identify other expenses. This system is used in case when goods are produced in a significant

manner. This management accounting systems gives better opportunities to monitoring expenses

for improve profit margins (Van Helden and Northcott, 2010).

P2 Different types of management accounting reports

Management accounting reports are accounting practices which are necessary for

development of business. It is varied from financial accounting and it helps in produce effective

reports for for internal stakeholders of firm as comparison to external stakeholders. All reports

give various information as well as data of the different segments which are used through

managers in context to develop future policies. These reports give reliable as well as accurate

statistical information to firm. There are various kinds of management accounting reports given

below as above:

Budgeting reports- It is a set of plan to evaluate performance level of firm at the time of

making better evaluations regarding performance of departments and control amount. For

preparation of budget, an actual expenses are occurred in the previous periods get used. This

kind of report is used to give incentives to staff members so that they can motivates and work for

achieving the set objectives with in specific period of time.

Job cost reports- These are related with determining cost, profitability and also expenses

of each specific job. There is an evaluation which can be made regarding earning of project to

earn more profit. Job cost reports are helpful in examine cost when the project is in progress so

that it can earn more money (Shah, Malik and Malik, 2011).

Manufacturing and inventory reports- Business firms which are included in

production process, they develop these kinds of reports to make inventory and production

process more effective. These reports involves labour cost, wastages, per unit overhead which

are related with stock. In addition to this, managers do comparison among various assembly lines

for see improvement opportunities which can exploited through different departments and also

their staff members.

Performance reports- Under this, differences are calculated on comparison of budgeted

performance with actual results regarding this performance reports. Generally, it is prepared on

yearly, monthly and quarterly basis. These reports are helpful in determining performance level

of firm on continuous basis and comparison with the last year performance.

manner. This management accounting systems gives better opportunities to monitoring expenses

for improve profit margins (Van Helden and Northcott, 2010).

P2 Different types of management accounting reports

Management accounting reports are accounting practices which are necessary for

development of business. It is varied from financial accounting and it helps in produce effective

reports for for internal stakeholders of firm as comparison to external stakeholders. All reports

give various information as well as data of the different segments which are used through

managers in context to develop future policies. These reports give reliable as well as accurate

statistical information to firm. There are various kinds of management accounting reports given

below as above:

Budgeting reports- It is a set of plan to evaluate performance level of firm at the time of

making better evaluations regarding performance of departments and control amount. For

preparation of budget, an actual expenses are occurred in the previous periods get used. This

kind of report is used to give incentives to staff members so that they can motivates and work for

achieving the set objectives with in specific period of time.

Job cost reports- These are related with determining cost, profitability and also expenses

of each specific job. There is an evaluation which can be made regarding earning of project to

earn more profit. Job cost reports are helpful in examine cost when the project is in progress so

that it can earn more money (Shah, Malik and Malik, 2011).

Manufacturing and inventory reports- Business firms which are included in

production process, they develop these kinds of reports to make inventory and production

process more effective. These reports involves labour cost, wastages, per unit overhead which

are related with stock. In addition to this, managers do comparison among various assembly lines

for see improvement opportunities which can exploited through different departments and also

their staff members.

Performance reports- Under this, differences are calculated on comparison of budgeted

performance with actual results regarding this performance reports. Generally, it is prepared on

yearly, monthly and quarterly basis. These reports are helpful in determining performance level

of firm on continuous basis and comparison with the last year performance.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Order information report- It helps for management to determining current trends in an

effective or efficient manner. Different kinds of reports which are prepared in this reporting

assess operations of integrating management ion order to accomplish minimum cost in order

placing and also management (Qian, Burritt and Monroe, 2011).

Significance of management accounting reports

Minimization in loss- Various kinds of reports give information regarding present

problems faced through firm to generate more profit and reduce loss.

Enhance financial returns- Lack information is main issue which is faced through given

form but through execution of better management accounting systems firm developed different

reports which help in decision making and improve productivity.

M1

There are advantages of different management accounting systems given below as above:

Management accounting systems Benefits

Cost accounting systems a. It is beneficial to maintain proper

investment in stocks.

b. Through this systems, firm can

measure its efficiency and make

improvement in performance.

Inventory management systems Helpful in saving cost and time.

Through this, firm can make

improvement in accuracy of stock

costs.

D1

REPORTING TYPE INTERGRATION WITH

ORGANISATIONAL PROCESSES

Performance reports An integration among processes included in

effective or efficient manner. Different kinds of reports which are prepared in this reporting

assess operations of integrating management ion order to accomplish minimum cost in order

placing and also management (Qian, Burritt and Monroe, 2011).

Significance of management accounting reports

Minimization in loss- Various kinds of reports give information regarding present

problems faced through firm to generate more profit and reduce loss.

Enhance financial returns- Lack information is main issue which is faced through given

form but through execution of better management accounting systems firm developed different

reports which help in decision making and improve productivity.

M1

There are advantages of different management accounting systems given below as above:

Management accounting systems Benefits

Cost accounting systems a. It is beneficial to maintain proper

investment in stocks.

b. Through this systems, firm can

measure its efficiency and make

improvement in performance.

Inventory management systems Helpful in saving cost and time.

Through this, firm can make

improvement in accuracy of stock

costs.

D1

REPORTING TYPE INTERGRATION WITH

ORGANISATIONAL PROCESSES

Performance reports An integration among processes included in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

firm and this kind of report gives better

management of stock levels and production

costs.

Order information report An integration among process of firm and this

kind of reporting can give management with

sales analysis to generate different reports.

TASK 2

P3 Calculation of cost after application cost analysis techniques

Cost: It refers as the amount which is spend by the organisation for creation of something

valuable which results in completion of their desired objectives. There are many resources are

used in the process of production (Otley and Emmanuel, 2013). The cost related to all such

resources are considered in the total amount of cost. Such different aspects includes:

Raw materials

Efforts

Resources

Risks incurred

Opportunity foregone

The cost are classified into different types which are defined below:

Fixed cost: It is that part of cost which always remain constant and does not get

fluctuated with the change in production level. However, per unit amount of fixed cost is

decreased with the increase in the level of production. The different costs which are included in

fixed cost are rent, depreciation etc.

Variable cost: It is considered as such cost which varies with the change in the level of

output. This cost has direct relation with production. So, it increases and decreases with the

variation in level of production. This includes the cost related to raw material, labour etc.

Cost volume profit: This analysis helps to determine that if change is happen in costs

and volume then what is the impact upon operating income and net income. While doing this

analysis, need to make several assumptions including sales price per unit id constant (Nixon and

Burns, 2012).

management of stock levels and production

costs.

Order information report An integration among process of firm and this

kind of reporting can give management with

sales analysis to generate different reports.

TASK 2

P3 Calculation of cost after application cost analysis techniques

Cost: It refers as the amount which is spend by the organisation for creation of something

valuable which results in completion of their desired objectives. There are many resources are

used in the process of production (Otley and Emmanuel, 2013). The cost related to all such

resources are considered in the total amount of cost. Such different aspects includes:

Raw materials

Efforts

Resources

Risks incurred

Opportunity foregone

The cost are classified into different types which are defined below:

Fixed cost: It is that part of cost which always remain constant and does not get

fluctuated with the change in production level. However, per unit amount of fixed cost is

decreased with the increase in the level of production. The different costs which are included in

fixed cost are rent, depreciation etc.

Variable cost: It is considered as such cost which varies with the change in the level of

output. This cost has direct relation with production. So, it increases and decreases with the

variation in level of production. This includes the cost related to raw material, labour etc.

Cost volume profit: This analysis helps to determine that if change is happen in costs

and volume then what is the impact upon operating income and net income. While doing this

analysis, need to make several assumptions including sales price per unit id constant (Nixon and

Burns, 2012).

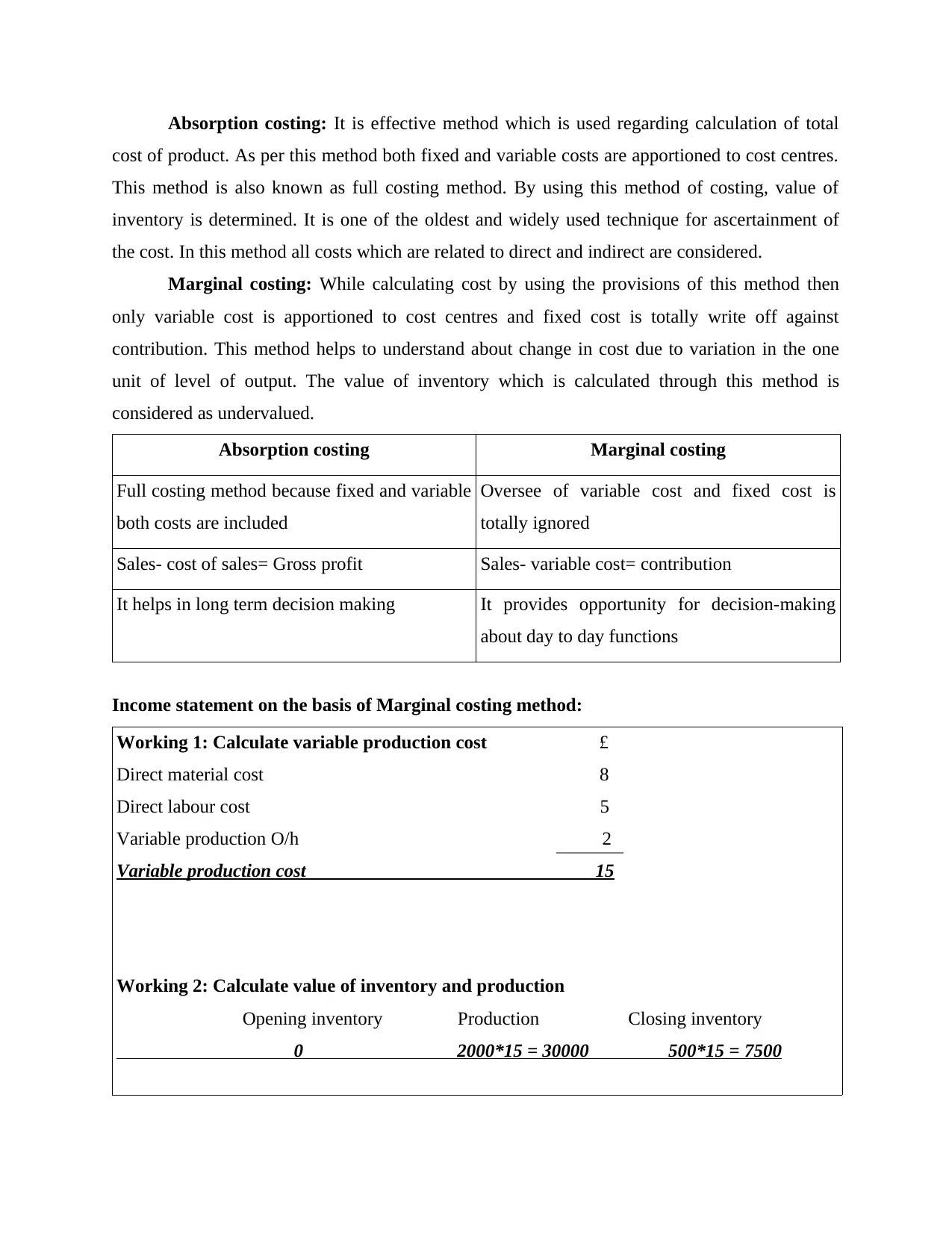

Absorption costing: It is effective method which is used regarding calculation of total

cost of product. As per this method both fixed and variable costs are apportioned to cost centres.

This method is also known as full costing method. By using this method of costing, value of

inventory is determined. It is one of the oldest and widely used technique for ascertainment of

the cost. In this method all costs which are related to direct and indirect are considered.

Marginal costing: While calculating cost by using the provisions of this method then

only variable cost is apportioned to cost centres and fixed cost is totally write off against

contribution. This method helps to understand about change in cost due to variation in the one

unit of level of output. The value of inventory which is calculated through this method is

considered as undervalued.

Absorption costing Marginal costing

Full costing method because fixed and variable

both costs are included

Oversee of variable cost and fixed cost is

totally ignored

Sales- cost of sales= Gross profit Sales- variable cost= contribution

It helps in long term decision making It provides opportunity for decision-making

about day to day functions

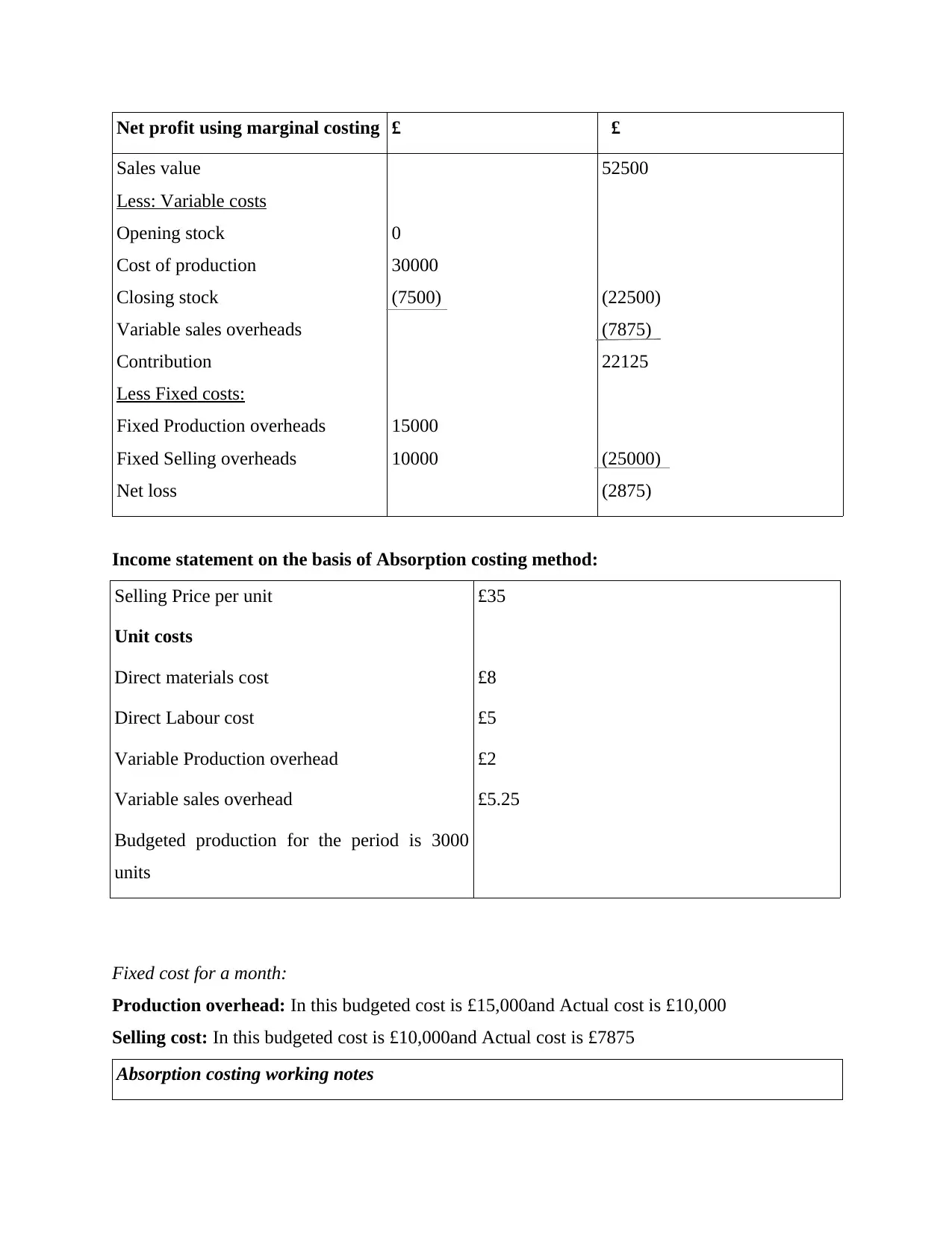

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material cost 8

Direct labour cost 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 2000*15 = 30000 500*15 = 7500

cost of product. As per this method both fixed and variable costs are apportioned to cost centres.

This method is also known as full costing method. By using this method of costing, value of

inventory is determined. It is one of the oldest and widely used technique for ascertainment of

the cost. In this method all costs which are related to direct and indirect are considered.

Marginal costing: While calculating cost by using the provisions of this method then

only variable cost is apportioned to cost centres and fixed cost is totally write off against

contribution. This method helps to understand about change in cost due to variation in the one

unit of level of output. The value of inventory which is calculated through this method is

considered as undervalued.

Absorption costing Marginal costing

Full costing method because fixed and variable

both costs are included

Oversee of variable cost and fixed cost is

totally ignored

Sales- cost of sales= Gross profit Sales- variable cost= contribution

It helps in long term decision making It provides opportunity for decision-making

about day to day functions

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material cost 8

Direct labour cost 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 2000*15 = 30000 500*15 = 7500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Net profit using marginal costing £ £

Sales value

Less: Variable costs

Opening stock

Cost of production

Closing stock

Variable sales overheads

Contribution

Less Fixed costs:

Fixed Production overheads

Fixed Selling overheads

Net loss

0

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

(2875)

Income statement on the basis of Absorption costing method:

Selling Price per unit £35

Unit costs

Direct materials cost £8

Direct Labour cost £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted production for the period is 3000

units

Fixed cost for a month:

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: In this budgeted cost is £10,000and Actual cost is £7875

Absorption costing working notes

Sales value

Less: Variable costs

Opening stock

Cost of production

Closing stock

Variable sales overheads

Contribution

Less Fixed costs:

Fixed Production overheads

Fixed Selling overheads

Net loss

0

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

(2875)

Income statement on the basis of Absorption costing method:

Selling Price per unit £35

Unit costs

Direct materials cost £8

Direct Labour cost £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted production for the period is 3000

units

Fixed cost for a month:

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: In this budgeted cost is £10,000and Actual cost is £7875

Absorption costing working notes

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

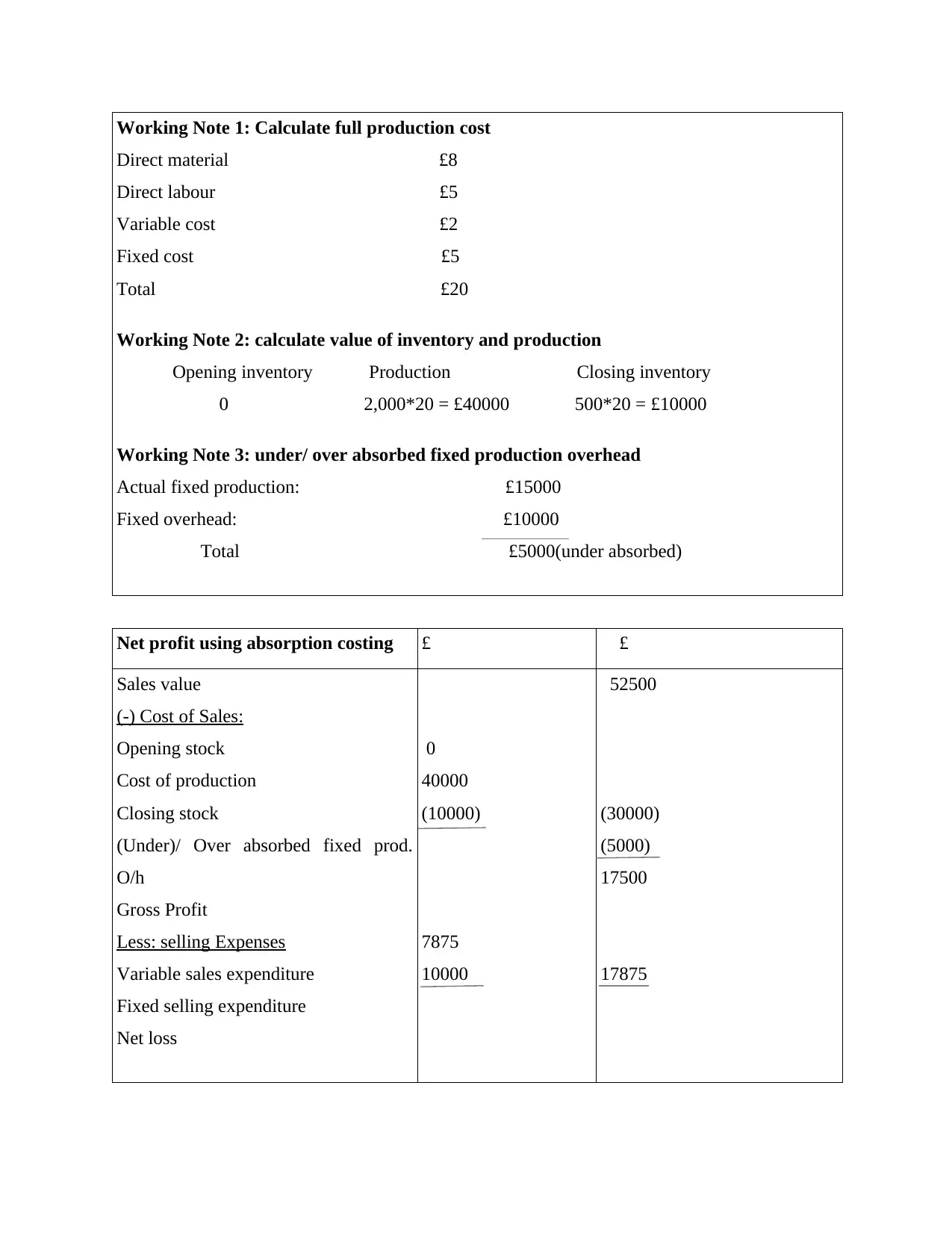

Working Note 1: Calculate full production cost

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40000 500*20 = £10000

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000(under absorbed)

Net profit using absorption costing £ £

Sales value

(-) Cost of Sales:

Opening stock

Cost of production

Closing stock

(Under)/ Over absorbed fixed prod.

O/h

Gross Profit

Less: selling Expenses

Variable sales expenditure

Fixed selling expenditure

Net loss

0

40000

(10000)

7875

10000

52500

(30000)

(5000)

17500

17875

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40000 500*20 = £10000

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000(under absorbed)

Net profit using absorption costing £ £

Sales value

(-) Cost of Sales:

Opening stock

Cost of production

Closing stock

(Under)/ Over absorbed fixed prod.

O/h

Gross Profit

Less: selling Expenses

Variable sales expenditure

Fixed selling expenditure

Net loss

0

40000

(10000)

7875

10000

52500

(30000)

(5000)

17500

17875

M2

Income statement is one of the important document which helps to ascertain about the

financial position of organisation. Through such collected information better financial decisions

are taken. It is observed from the above analysis of income statement of Tech (UK)Ltd is that it

is working in loss.

D2

From the above analysis of income statement, it is noticed that through use of the method

of marginal costing the loss is ascertained of the amount of 375. But with the help of absorption

costing method loss of 2875 is identified. This difference is arise due to the acceptance of fixed

cost in absorption costing method (Garrison And et. al., 2010).

TASK 3

P4 Advantages and disadvantages of different types of planning tools used for budgetary control

Different types of budgets

There are different types of budgets which provides the direction to the employees of

organisation in performance of their functions in effective manner. All budgets prepared by

organisation different in nature and having different roles. The different budgets which are

formulate by Tech(UK)Ltd. Are defined below:

Capital budget: This budgets includes the information regarding capital receipts and

payments which are going to come from different sources in future. It helps in effective

use of funds regarding purchase of their fixed assets.

Operational budget: This budget is prepared by the management of organisation for

effective performance of different business activities in more appropriate manner. It helps

in planning of their different types of expenditures which further contributes in

improvement in the number of profits.

Cash flow budget: It is effective budget which provides the information regarding

availability of cash in organisation. It helps the manager of organisation is to effective

perform their day to day functions (Fullerton, Kennedy and Widener, 2014).

Budget preparation process

Calculation of expenses: For preparation of budget need to identify expenses.

Income statement is one of the important document which helps to ascertain about the

financial position of organisation. Through such collected information better financial decisions

are taken. It is observed from the above analysis of income statement of Tech (UK)Ltd is that it

is working in loss.

D2

From the above analysis of income statement, it is noticed that through use of the method

of marginal costing the loss is ascertained of the amount of 375. But with the help of absorption

costing method loss of 2875 is identified. This difference is arise due to the acceptance of fixed

cost in absorption costing method (Garrison And et. al., 2010).

TASK 3

P4 Advantages and disadvantages of different types of planning tools used for budgetary control

Different types of budgets

There are different types of budgets which provides the direction to the employees of

organisation in performance of their functions in effective manner. All budgets prepared by

organisation different in nature and having different roles. The different budgets which are

formulate by Tech(UK)Ltd. Are defined below:

Capital budget: This budgets includes the information regarding capital receipts and

payments which are going to come from different sources in future. It helps in effective

use of funds regarding purchase of their fixed assets.

Operational budget: This budget is prepared by the management of organisation for

effective performance of different business activities in more appropriate manner. It helps

in planning of their different types of expenditures which further contributes in

improvement in the number of profits.

Cash flow budget: It is effective budget which provides the information regarding

availability of cash in organisation. It helps the manager of organisation is to effective

perform their day to day functions (Fullerton, Kennedy and Widener, 2014).

Budget preparation process

Calculation of expenses: For preparation of budget need to identify expenses.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.