Management Accounting Report: Tech (UK) Ltd. Performance Analysis

VerifiedAdded on 2020/12/24

|17

|3786

|118

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles applied to Tech (UK) Ltd., a company specializing in mobile phone chargers and other gadgets. The report begins with an introduction to management accounting, differentiating it from financial accounting and highlighting its importance in performance appraisal, future planning, and risk assessment. It then delves into various management accounting systems like cost management and inventory management, including techniques such as FIFO, LIFO, and AVCO. Different types of managerial accounting reports, such as budget reports and accounts receivable reports, are discussed, emphasizing their role in cost reduction and decision-making. The report further explores cost calculation methods, comparing marginal and absorption costing, and includes income statements prepared using both methods. Finally, it examines different types of budgets, including operational, rolling, fixed, and flexible budgets, outlining their merits and demerits. The report concludes with a discussion on the use of management accounting to address financial problems, providing a holistic view of how accounting practices can drive effective business decisions.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...................................................................................................................................3

TASK 1....................................................................................................................................................3

P1 Management accounting concept and its essential requirements...................................................3

P2: Different types of managerial accounting reports and their importance.......................................6

TASK 2....................................................................................................................................................7

P3: Calculation of cost and preparation of income statement.............................................................7

TASK 3..................................................................................................................................................10

P4: Different kind of Budgets and their merits and demerits............................................................10

TASK 4..................................................................................................................................................12

P5: Use of management accounting to respond financial problem...................................................12

CONCLUSION......................................................................................................................................16

REFERENCES......................................................................................................................................17

INTRODUCTION...................................................................................................................................3

TASK 1....................................................................................................................................................3

P1 Management accounting concept and its essential requirements...................................................3

P2: Different types of managerial accounting reports and their importance.......................................6

TASK 2....................................................................................................................................................7

P3: Calculation of cost and preparation of income statement.............................................................7

TASK 3..................................................................................................................................................10

P4: Different kind of Budgets and their merits and demerits............................................................10

TASK 4..................................................................................................................................................12

P5: Use of management accounting to respond financial problem...................................................12

CONCLUSION......................................................................................................................................16

REFERENCES......................................................................................................................................17

INTRODUCTION

Management accounting play a valuable in helping management to make an effective

decision and suitable plans to execute future business activities in such an effective manner

that will help in getting profitable result in near future. The manager of accounting

department are held liable to prepare financial statements which includes balance sheet, Profit

& Loss a/c, Cash flow statement with the help of collecting information available through

various management accounting system. The present assignment report is based on Tech

(UK) Ltd. which is engaged in providing special charger for mobile telephones and other

various gadgets for the retail outlets. The project includes the comparison between

management and financial accounting along with the benefits of management accounting and

different reporting systems. Financial tools which help in resolving financial issues faced by

company during accounting period are also covered under this report (Garrison and et. al.,

2010).

TASK 1

P1 Management accounting concept and its essential requirements

Management accounting: One of the important system which is used within the

organisation is to record the performance of different departments. It is big concept which

includes the provision of cost and managerial accounting. Application of the provisions of

different systems provides financial and statistical data which improves the decision making

power of internal parties to make their organisational activities more effective and efficient. It

helps the organisation is to accomplish their objectives within given period of time frame.

Through implementation of management accounting systems large number of benefit are

ascertained by Tech (UK) Ltd. Like risk management, planning of future actions, appraisal of

performance of employees etc.

Difference between management and financial accounting

Management accounting Financial accounting

Behind the application of the concepts

management accounting is to make the

different kind of reports according to the

performance of departments for the purpose of

operating different organisational activities

The main objective behind the application of

the methods of financial accounting is to assess

the financial position of organisation.

Management accounting play a valuable in helping management to make an effective

decision and suitable plans to execute future business activities in such an effective manner

that will help in getting profitable result in near future. The manager of accounting

department are held liable to prepare financial statements which includes balance sheet, Profit

& Loss a/c, Cash flow statement with the help of collecting information available through

various management accounting system. The present assignment report is based on Tech

(UK) Ltd. which is engaged in providing special charger for mobile telephones and other

various gadgets for the retail outlets. The project includes the comparison between

management and financial accounting along with the benefits of management accounting and

different reporting systems. Financial tools which help in resolving financial issues faced by

company during accounting period are also covered under this report (Garrison and et. al.,

2010).

TASK 1

P1 Management accounting concept and its essential requirements

Management accounting: One of the important system which is used within the

organisation is to record the performance of different departments. It is big concept which

includes the provision of cost and managerial accounting. Application of the provisions of

different systems provides financial and statistical data which improves the decision making

power of internal parties to make their organisational activities more effective and efficient. It

helps the organisation is to accomplish their objectives within given period of time frame.

Through implementation of management accounting systems large number of benefit are

ascertained by Tech (UK) Ltd. Like risk management, planning of future actions, appraisal of

performance of employees etc.

Difference between management and financial accounting

Management accounting Financial accounting

Behind the application of the concepts

management accounting is to make the

different kind of reports according to the

performance of departments for the purpose of

operating different organisational activities

The main objective behind the application of

the methods of financial accounting is to assess

the financial position of organisation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

smoothly.

It contributes in formulation of future plans to

accomplish desired objectives and

improvement of the decision making of

internal parties

This can be further used by the external parties

to make decisions regarding investments within

the organisation

These accounts are formulate as per the needs

of organisation

It is prepared at the end of the year to analyse

the profit and loss of organisation.

It is used regarding assessment of performance

of each and every department

This will helps in assessment of the financial

performance of whole organisation

Importance of management accounting

Appraisal of performance: One of the important function in which these system

contributes their efforts includes appraisal of the actual performance of employees

through comparison with standards. Different budgets are prepared as per using the

provisions management accounting which contains standards. This comparison helps

to identify the deviations and providence more accurate solutions to attain desired

results.

Formulation of future plans: There is huge role is played by the management

accounting to make the better future plans. This will be possible because use of

management accounting provisions helps to gather information from the different

departments. On the basis of such information future strategies are formulated which

directs the employees of organisation.

Determination of aim: The management of organisation uses the information to set

their targets and objectives which are need to achieve through their business

functions. These targets are set through identification of the working capacity of each

and every department of organisation.

Assessment of risks: Application of the management accounting systems not only

helps in identification of the risks which are faced by the organisation while providing

their activities but also helps to assess the future risks which are associated with the

business transactions (Fullerton, Kennedy and Widener, 2014). It provides the

opportunity regarding formulation contingency provisions.

Different management accounting systems

It contributes in formulation of future plans to

accomplish desired objectives and

improvement of the decision making of

internal parties

This can be further used by the external parties

to make decisions regarding investments within

the organisation

These accounts are formulate as per the needs

of organisation

It is prepared at the end of the year to analyse

the profit and loss of organisation.

It is used regarding assessment of performance

of each and every department

This will helps in assessment of the financial

performance of whole organisation

Importance of management accounting

Appraisal of performance: One of the important function in which these system

contributes their efforts includes appraisal of the actual performance of employees

through comparison with standards. Different budgets are prepared as per using the

provisions management accounting which contains standards. This comparison helps

to identify the deviations and providence more accurate solutions to attain desired

results.

Formulation of future plans: There is huge role is played by the management

accounting to make the better future plans. This will be possible because use of

management accounting provisions helps to gather information from the different

departments. On the basis of such information future strategies are formulated which

directs the employees of organisation.

Determination of aim: The management of organisation uses the information to set

their targets and objectives which are need to achieve through their business

functions. These targets are set through identification of the working capacity of each

and every department of organisation.

Assessment of risks: Application of the management accounting systems not only

helps in identification of the risks which are faced by the organisation while providing

their activities but also helps to assess the future risks which are associated with the

business transactions (Fullerton, Kennedy and Widener, 2014). It provides the

opportunity regarding formulation contingency provisions.

Different management accounting systems

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

There are different management accounting systems with having different roles and

functions within the organisation. There are many benefits are achieved by organisation

through use of these systems. The different systems which are adopted by Tech (UK) Ltd.

Are defined below:

Cost management system: The main role of this system is to identify the total cost of

products which is incurred by organisation. It is important for manufacturing organisation is

to adopt these systems to ascertain the profitability which is associated with their profit. Tech

(UK) Ltd. Uses this system to calculate the total cost of their products and make efforts for

reduction of the wastages which contributes in improvement of their profit margin. The costs

are further classified into three different types which are mentioned below:

Actual costing Standard costing Normal costing

Through application of this

method actual cost are

apportioned to the different

aspects like aspects direct

material, labour and overhead

This will includes the setting

of budgeted cost of different

items which work as

standards need to achieve

while consider actual cost of

product

This will include first

analysis of direct material

and labour cost which is

going to incurred in future

period of time. On the basis

of such evaluation actual cost

identified.

Inventory management system: One of the effective method which is needed to

implement by every organisation for effective management of the level of stock and non

capitalized asset within the organisation. This will provides the management of organisation

is to maintain the minimum level of stock to grab the future opportunities and satisfaction of

the different needs of customers. This system further used in the effective allocation of

inventories to different departments according to their needs for attainment of optimum

results. There are many techniques which contribute in valuation of stock are defined below:

FIFO: This method is called as first in first out method. Here, cost of stock is

ascertained which is purchased first and old in type (Dillard and Roslender, 2011).

LIFO: This method is called as Last in First out method. As per the provision of this

method the stock purchased last is first used in production process.

functions within the organisation. There are many benefits are achieved by organisation

through use of these systems. The different systems which are adopted by Tech (UK) Ltd.

Are defined below:

Cost management system: The main role of this system is to identify the total cost of

products which is incurred by organisation. It is important for manufacturing organisation is

to adopt these systems to ascertain the profitability which is associated with their profit. Tech

(UK) Ltd. Uses this system to calculate the total cost of their products and make efforts for

reduction of the wastages which contributes in improvement of their profit margin. The costs

are further classified into three different types which are mentioned below:

Actual costing Standard costing Normal costing

Through application of this

method actual cost are

apportioned to the different

aspects like aspects direct

material, labour and overhead

This will includes the setting

of budgeted cost of different

items which work as

standards need to achieve

while consider actual cost of

product

This will include first

analysis of direct material

and labour cost which is

going to incurred in future

period of time. On the basis

of such evaluation actual cost

identified.

Inventory management system: One of the effective method which is needed to

implement by every organisation for effective management of the level of stock and non

capitalized asset within the organisation. This will provides the management of organisation

is to maintain the minimum level of stock to grab the future opportunities and satisfaction of

the different needs of customers. This system further used in the effective allocation of

inventories to different departments according to their needs for attainment of optimum

results. There are many techniques which contribute in valuation of stock are defined below:

FIFO: This method is called as first in first out method. Here, cost of stock is

ascertained which is purchased first and old in type (Dillard and Roslender, 2011).

LIFO: This method is called as Last in First out method. As per the provision of this

method the stock purchased last is first used in production process.

AVCO: This method includes the process of calculating average where cost of

inventory is divided by the number of raw material which is present within the

organisation.

Job costing method: This method is important for the manufacturing organisation which

produces which different types of products. This will includes the process of allocation of

cost to each and every item which is used in the production process of products. Through use

of this method manager track the different expenses and make efforts to control them.

P2: Different types of managerial accounting reports and their importance

There different kinds of reports are formulated by the management of Tech (UK) Ltd.

For the purpose of enhancing decision making and improvement of the understanding

between different departments. The different kind of reports and their functions are defined

below:

Budget report: The main role of this report is to provide the standards which are need

to adhere by the employees while performing their functions. This will be further used

regarding determination of incentive plan of employees as per their actual performances.

Accounts receivable report: The main function of this report is to assess the amount

which is yet not paid by the debtors of organisation. To make their assessment more accurate

and reliable need to do segmentation of invoices on the basis of their due date. This will helps

the manager is to rethink about their credit policies and bring necessary changes to make

more effective.

Inventory and manufacturing report: This report provides the information about the

resources which available with the organisation at present for production of different

products. The main aim of this report is to ascertain the amount of stock which is required all

the time to continue their business operations without any interruptions.

Importance of management accounting reports

Reduction of cost: Different information is gathered regarding which helps to

identify the aspects which are not only wastage for organisation but also reduces their profit

margin. These reports help to bring more focus on profitable aspects to improve earnings and

reduce costs (Cinquini and Tenucci, 2010).

inventory is divided by the number of raw material which is present within the

organisation.

Job costing method: This method is important for the manufacturing organisation which

produces which different types of products. This will includes the process of allocation of

cost to each and every item which is used in the production process of products. Through use

of this method manager track the different expenses and make efforts to control them.

P2: Different types of managerial accounting reports and their importance

There different kinds of reports are formulated by the management of Tech (UK) Ltd.

For the purpose of enhancing decision making and improvement of the understanding

between different departments. The different kind of reports and their functions are defined

below:

Budget report: The main role of this report is to provide the standards which are need

to adhere by the employees while performing their functions. This will be further used

regarding determination of incentive plan of employees as per their actual performances.

Accounts receivable report: The main function of this report is to assess the amount

which is yet not paid by the debtors of organisation. To make their assessment more accurate

and reliable need to do segmentation of invoices on the basis of their due date. This will helps

the manager is to rethink about their credit policies and bring necessary changes to make

more effective.

Inventory and manufacturing report: This report provides the information about the

resources which available with the organisation at present for production of different

products. The main aim of this report is to ascertain the amount of stock which is required all

the time to continue their business operations without any interruptions.

Importance of management accounting reports

Reduction of cost: Different information is gathered regarding which helps to

identify the aspects which are not only wastage for organisation but also reduces their profit

margin. These reports help to bring more focus on profitable aspects to improve earnings and

reduce costs (Cinquini and Tenucci, 2010).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Decision making: Different reports provide different departmental information which

improves overall decision making ability of internal parties.

TASK 2

P3: Calculation of cost and preparation of income statement

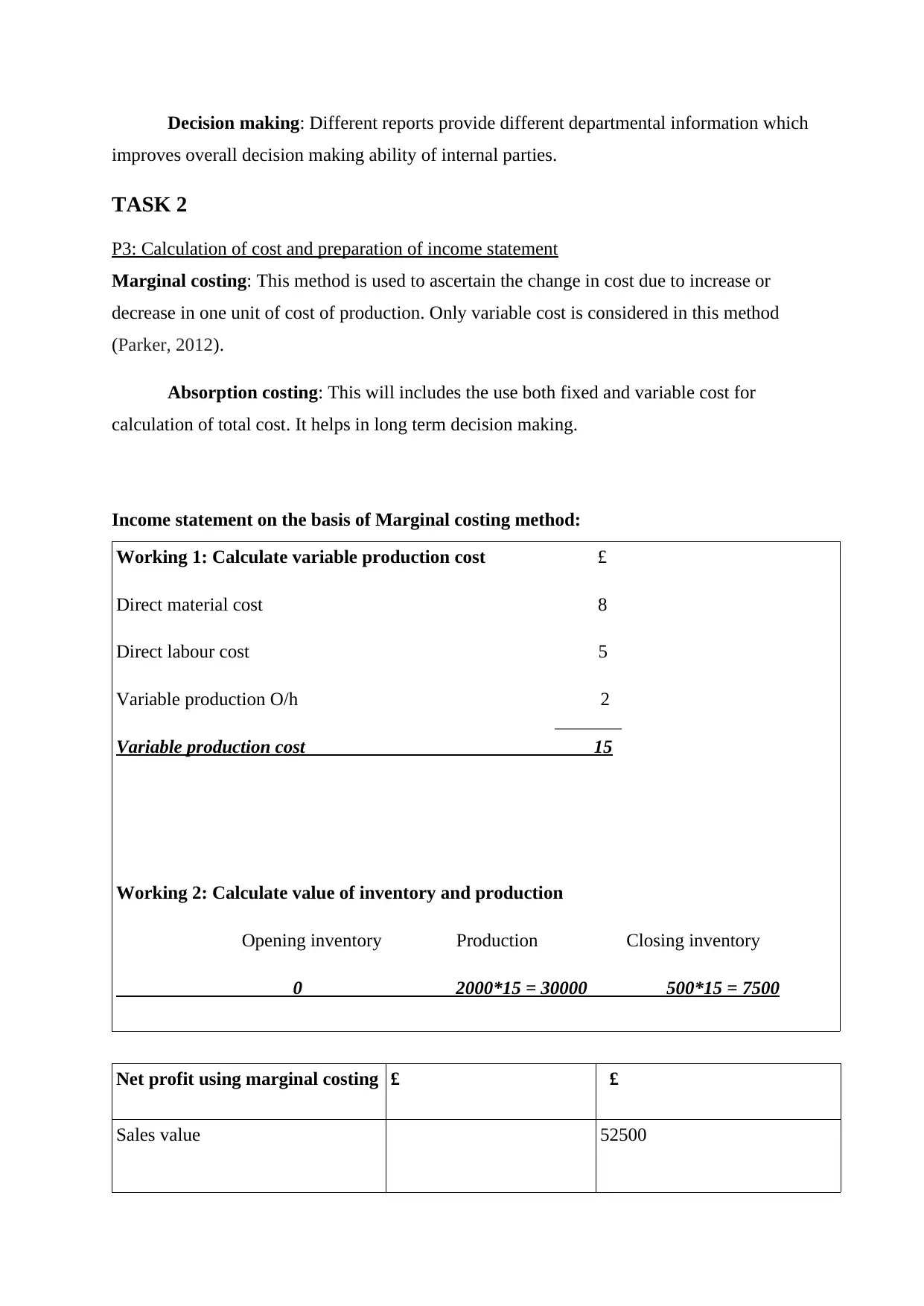

Marginal costing: This method is used to ascertain the change in cost due to increase or

decrease in one unit of cost of production. Only variable cost is considered in this method

(Parker, 2012).

Absorption costing: This will includes the use both fixed and variable cost for

calculation of total cost. It helps in long term decision making.

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material cost 8

Direct labour cost 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £ £

Sales value 52500

improves overall decision making ability of internal parties.

TASK 2

P3: Calculation of cost and preparation of income statement

Marginal costing: This method is used to ascertain the change in cost due to increase or

decrease in one unit of cost of production. Only variable cost is considered in this method

(Parker, 2012).

Absorption costing: This will includes the use both fixed and variable cost for

calculation of total cost. It helps in long term decision making.

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material cost 8

Direct labour cost 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £ £

Sales value 52500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

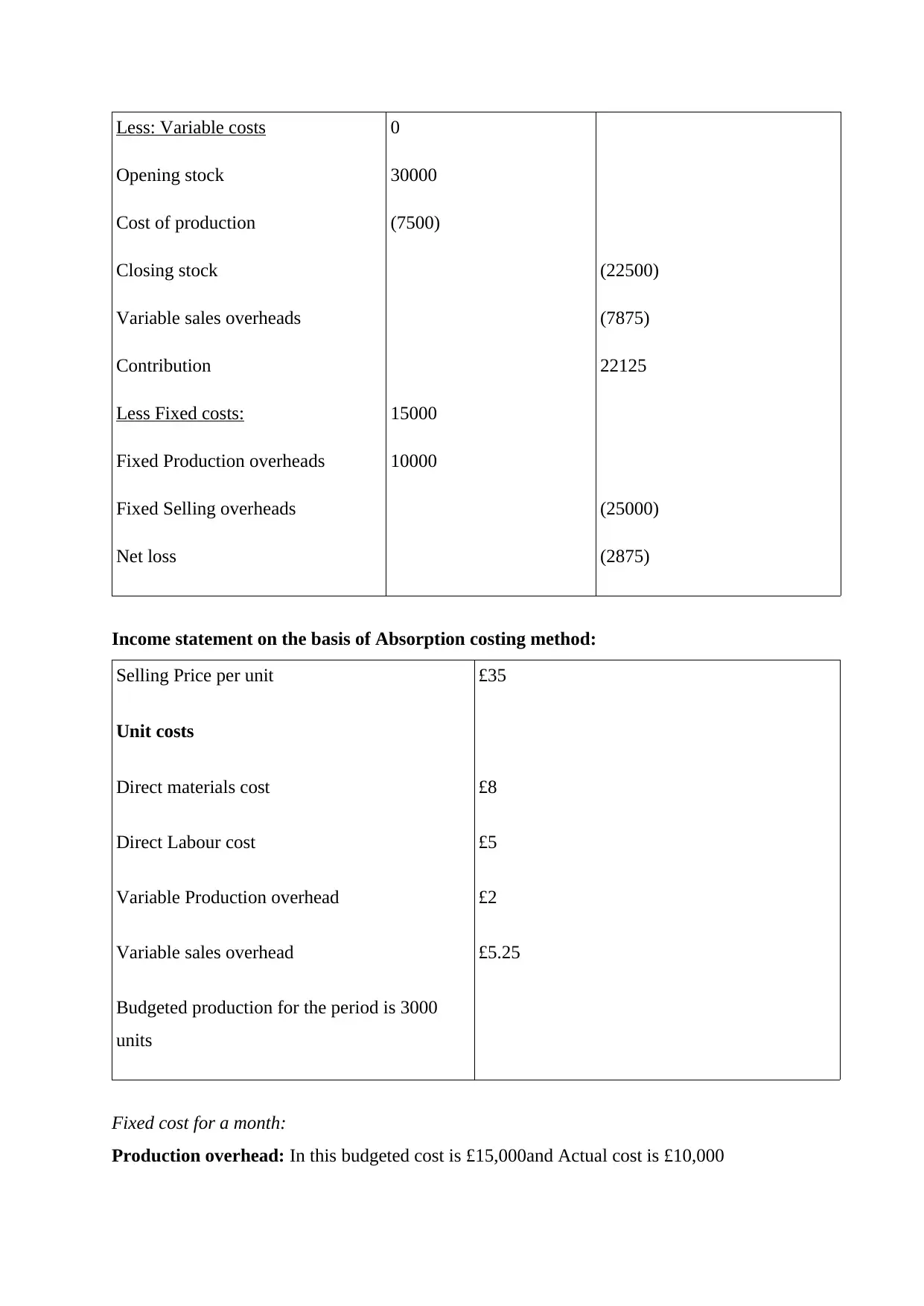

Less: Variable costs

Opening stock

Cost of production

Closing stock

Variable sales overheads

Contribution

Less Fixed costs:

Fixed Production overheads

Fixed Selling overheads

Net loss

0

30000

(7500)

15000

10000

(22500)

(7875)

22125

(25000)

(2875)

Income statement on the basis of Absorption costing method:

Selling Price per unit £35

Unit costs

Direct materials cost £8

Direct Labour cost £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted production for the period is 3000

units

Fixed cost for a month:

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Opening stock

Cost of production

Closing stock

Variable sales overheads

Contribution

Less Fixed costs:

Fixed Production overheads

Fixed Selling overheads

Net loss

0

30000

(7500)

15000

10000

(22500)

(7875)

22125

(25000)

(2875)

Income statement on the basis of Absorption costing method:

Selling Price per unit £35

Unit costs

Direct materials cost £8

Direct Labour cost £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted production for the period is 3000

units

Fixed cost for a month:

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: In this budgeted cost is £10,000 and Actual cost is £7875

Absorption costing working notes

Working Note 1: Calculate full production cost

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40000 500*20 = £10000

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000(under absorbed)

Net profit using absorption costing £ £

Sales value

(-) Cost of Sales:

Opening stock

Cost of production

Closing stock

0

40000

(10000)

52500

(30000)

Absorption costing working notes

Working Note 1: Calculate full production cost

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40000 500*20 = £10000

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000(under absorbed)

Net profit using absorption costing £ £

Sales value

(-) Cost of Sales:

Opening stock

Cost of production

Closing stock

0

40000

(10000)

52500

(30000)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

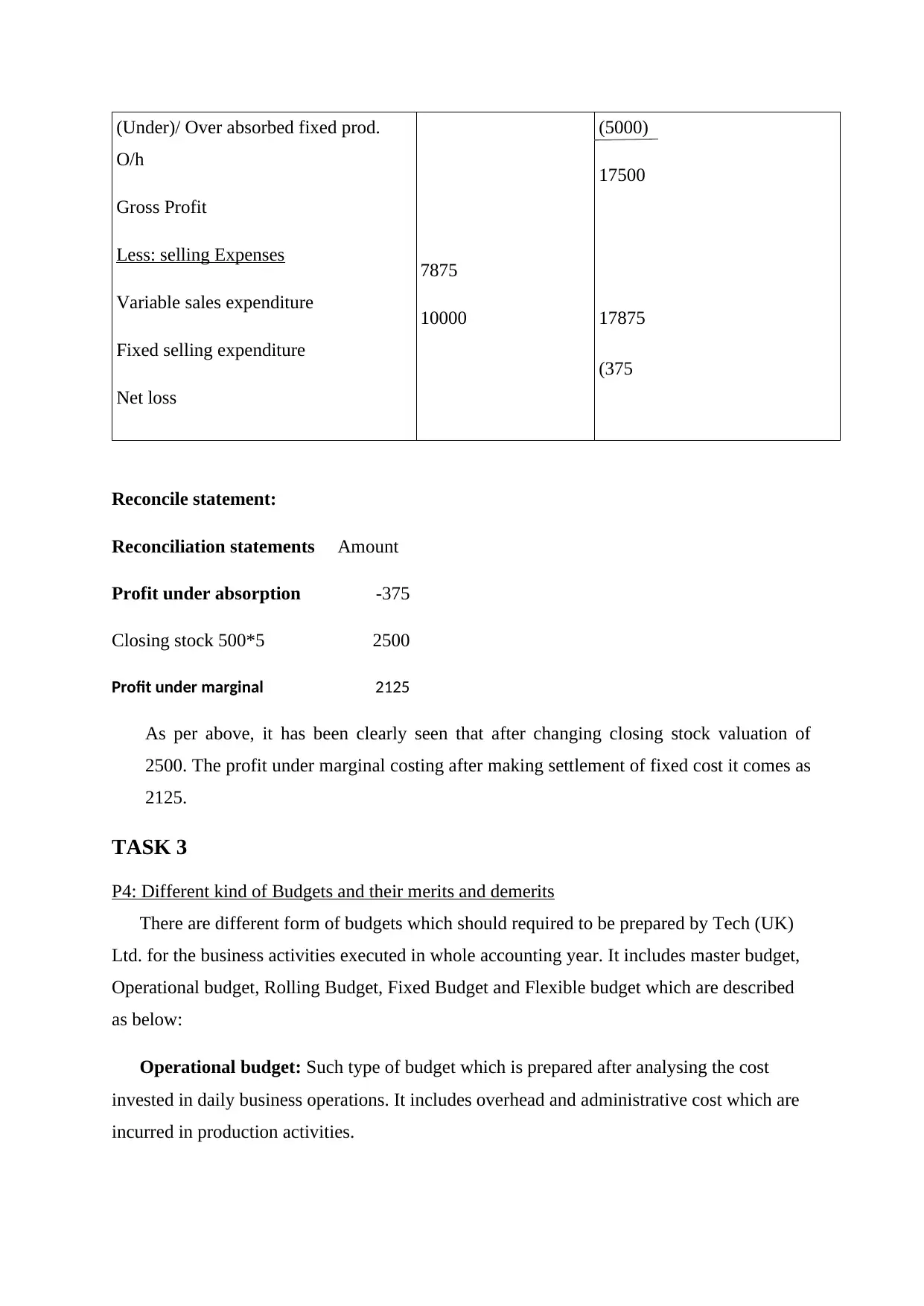

(Under)/ Over absorbed fixed prod.

O/h

Gross Profit

Less: selling Expenses

Variable sales expenditure

Fixed selling expenditure

Net loss

7875

10000

(5000)

17500

17875

(375

Reconcile statement:

Reconciliation statements Amount

Profit under absorption -375

Closing stock 500*5 2500

Profit under marginal 2125

As per above, it has been clearly seen that after changing closing stock valuation of

2500. The profit under marginal costing after making settlement of fixed cost it comes as

2125.

TASK 3

P4: Different kind of Budgets and their merits and demerits

There are different form of budgets which should required to be prepared by Tech (UK)

Ltd. for the business activities executed in whole accounting year. It includes master budget,

Operational budget, Rolling Budget, Fixed Budget and Flexible budget which are described

as below:

Operational budget: Such type of budget which is prepared after analysing the cost

invested in daily business operations. It includes overhead and administrative cost which are

incurred in production activities.

O/h

Gross Profit

Less: selling Expenses

Variable sales expenditure

Fixed selling expenditure

Net loss

7875

10000

(5000)

17500

17875

(375

Reconcile statement:

Reconciliation statements Amount

Profit under absorption -375

Closing stock 500*5 2500

Profit under marginal 2125

As per above, it has been clearly seen that after changing closing stock valuation of

2500. The profit under marginal costing after making settlement of fixed cost it comes as

2125.

TASK 3

P4: Different kind of Budgets and their merits and demerits

There are different form of budgets which should required to be prepared by Tech (UK)

Ltd. for the business activities executed in whole accounting year. It includes master budget,

Operational budget, Rolling Budget, Fixed Budget and Flexible budget which are described

as below:

Operational budget: Such type of budget which is prepared after analysing the cost

invested in daily business operations. It includes overhead and administrative cost which are

incurred in production activities.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advantage: Such budget is prepared on the basis of cost and revenue earned from

daily business operations thus it help management in reducing expenses of business

activities.

Disadvantage: It takes lots of time to prepare budget as it includes all cost incurred in

company on daily basis.

Rolling Budget: It is such type of budget which is newly prepared after revising the

financial plans for the next upcoming years replacing the old one in order to continue

business operation.

Advantage: The chances of getting profitable outcomes will be more as the budget is

prepared after revising the financial plans.

Disadvantage: It takes more time to prepare budget as the financial information are

given by company due to which the company may competitive advantage.

Fixed Budget: It is an effective budget which is fixed and should not be changes with the

change in volume of output. It restricts management to modify changes in budget and direct

them to continue as per pre-planned (Pipan and Czarniawska, 2010).

Advantage: It helps management in analysing the chances of achieving growth and

success of an organisation operates at small scale.

Disadvantage: Sometimes it will be difficult for management to grab competitive

opportunities as the budget are fixed thus not allowed them to invest money in other

areas here the profitable outcomes will be received.

Flexible budget: It is also of the type of budget which can be changes with the changes

in business activities. Thus, it allows management to make changes according to the needs

and requirements in execution of business activities.

Advantage: It helps management to makes changes in budget in order to grab

competitive advantage to company.

Disadvantage: Sometimes the manager has notices the requirements of additional

funds in execution of business activities which results in increasing cost of production

activities.

Different pricing systems:

daily business operations thus it help management in reducing expenses of business

activities.

Disadvantage: It takes lots of time to prepare budget as it includes all cost incurred in

company on daily basis.

Rolling Budget: It is such type of budget which is newly prepared after revising the

financial plans for the next upcoming years replacing the old one in order to continue

business operation.

Advantage: The chances of getting profitable outcomes will be more as the budget is

prepared after revising the financial plans.

Disadvantage: It takes more time to prepare budget as the financial information are

given by company due to which the company may competitive advantage.

Fixed Budget: It is an effective budget which is fixed and should not be changes with the

change in volume of output. It restricts management to modify changes in budget and direct

them to continue as per pre-planned (Pipan and Czarniawska, 2010).

Advantage: It helps management in analysing the chances of achieving growth and

success of an organisation operates at small scale.

Disadvantage: Sometimes it will be difficult for management to grab competitive

opportunities as the budget are fixed thus not allowed them to invest money in other

areas here the profitable outcomes will be received.

Flexible budget: It is also of the type of budget which can be changes with the changes

in business activities. Thus, it allows management to make changes according to the needs

and requirements in execution of business activities.

Advantage: It helps management to makes changes in budget in order to grab

competitive advantage to company.

Disadvantage: Sometimes the manager has notices the requirements of additional

funds in execution of business activities which results in increasing cost of production

activities.

Different pricing systems:

Price skimming: It is such a strategy in which the company first raises the prices of

product at the time of introducing product into market and thereafter reducing prices in order

to compete with their rivals.

Economy pricing: It is an effective strategy of lowering price of product as compared

to the rivals in order to influence buying behaviour of customers. This it is essential for Tech

(UK) Ltd. to adopt such pricing strategies.

Cost plus pricing: It includes cost which is related with direct material, labour and

overhead expenses to set effective prices for products and services (Qian, Burritt and Monroe,

2011).

Full cost pricing: It includes fixation of price after identifying the direct cost incurred

in producing unit of output.

Marginal cost pricing: It includes cost which is invested in production process in

order to produce extra units of products and services.

Importance of Budget for planning and control:

Preparing of financial roadmap: The budget helps in giving right direction to

execute future business activities in profitable manner. On the basis of previous year budget,

the management are able to make roadmap in order to ensure that future business activities

are executed in decided manner.

Limit Expenditures: Budget restricts employees to spend less on executing each

business activities after analysing the allocation of cost to specific cost centres.

Plan for future growth: Preparation of budget is not enough for management as it also

requires to make an effective plan to invest money in such areas where the chances of getting

profitable result are more.

TASK 4

P5: Use of management accounting to respond financial problem

According to the Tech (UK) Ltd. financial reports, it has been found that the company

has faces huge losses i.e. £1.5 million which decreases their financial situation in market.

Thus, it is important for the management of Tech (UK) Ltd. to adopt effective financial tools

product at the time of introducing product into market and thereafter reducing prices in order

to compete with their rivals.

Economy pricing: It is an effective strategy of lowering price of product as compared

to the rivals in order to influence buying behaviour of customers. This it is essential for Tech

(UK) Ltd. to adopt such pricing strategies.

Cost plus pricing: It includes cost which is related with direct material, labour and

overhead expenses to set effective prices for products and services (Qian, Burritt and Monroe,

2011).

Full cost pricing: It includes fixation of price after identifying the direct cost incurred

in producing unit of output.

Marginal cost pricing: It includes cost which is invested in production process in

order to produce extra units of products and services.

Importance of Budget for planning and control:

Preparing of financial roadmap: The budget helps in giving right direction to

execute future business activities in profitable manner. On the basis of previous year budget,

the management are able to make roadmap in order to ensure that future business activities

are executed in decided manner.

Limit Expenditures: Budget restricts employees to spend less on executing each

business activities after analysing the allocation of cost to specific cost centres.

Plan for future growth: Preparation of budget is not enough for management as it also

requires to make an effective plan to invest money in such areas where the chances of getting

profitable result are more.

TASK 4

P5: Use of management accounting to respond financial problem

According to the Tech (UK) Ltd. financial reports, it has been found that the company

has faces huge losses i.e. £1.5 million which decreases their financial situation in market.

Thus, it is important for the management of Tech (UK) Ltd. to adopt effective financial tools

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.