Management Accounting Report: Analysis and Financial Systems

VerifiedAdded on 2020/06/04

|18

|4618

|54

Report

AI Summary

This report delves into the realm of management accounting, exploring its core concepts and practical applications within the context of Tech (UK) Ltd. It begins by defining management accounting, contrasting it with financial accounting, and highlighting its significance as a decision-making tool for departmental managers. The report examines various management accounting systems, including cost accounting and inventory management, and their roles in performance measurement, resource allocation, and risk assessment. It then proceeds to analyze different types of management accounting reports, such as budgeting, job cost, and performance reports, emphasizing their importance in loss minimization, decision-making, and enhancing financial returns. Furthermore, the report explores the application of absorption and marginal costing in preparing income statements, along with the significance of various budgeting techniques as planning tools. The report concludes by assessing the contribution of management accounting systems in addressing financial challenges, offering a comprehensive overview of the subject matter.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Analysis of management accounting and their essential requirement in organisation..........1

P2 Different types of management accounting reports and their importance.............................3

M1...............................................................................................................................................5

TASK 2............................................................................................................................................6

P3 Application of absorption and marginal costing for preparation of income statements........6

M2...............................................................................................................................................9

D2................................................................................................................................................9

TASK 3............................................................................................................................................9

P4 Different kind of budgets and their importance as planning tool..........................................9

M3.............................................................................................................................................11

TASK 4..........................................................................................................................................11

P5 Use of management accounting systems to respond financial problems.............................11

M4.............................................................................................................................................12

D3..............................................................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Analysis of management accounting and their essential requirement in organisation..........1

P2 Different types of management accounting reports and their importance.............................3

M1...............................................................................................................................................5

TASK 2............................................................................................................................................6

P3 Application of absorption and marginal costing for preparation of income statements........6

M2...............................................................................................................................................9

D2................................................................................................................................................9

TASK 3............................................................................................................................................9

P4 Different kind of budgets and their importance as planning tool..........................................9

M3.............................................................................................................................................11

TASK 4..........................................................................................................................................11

P5 Use of management accounting systems to respond financial problems.............................11

M4.............................................................................................................................................12

D3..............................................................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION

Every organisation is need to adopt effective management accounting systems which

helps in recording of business transactions in more effective and appropriate manner.

Management accounting systems are considered as decision making tool which is used internally

by manager. The different tools which are included in this system are budgeting, variance

analysis, BEP, cost-volume-profit analysis etc. It helps the manager to formulate different reports

for improvement of understanding among different departments about their functions

(Baldvinsdottir, Mitchell and Nørreklit, 2010). Overall, it helps in completion of their

organisational objectives within stipulated period of time. Tech(UK)Ltd. Is manufacturing

organisation which provides their products to retailer.

In the present report explain about, concepts of management accounting and its

distinguish with financial accounting, importance of management accounting information as

decision making tool for departmental managers, application of different management

accounting systems in organisation, different types of managerial reports and its importance in

organisational scenario. Also, contribution of cost accounting techniques in preparation of

income statements, budget preparation process and contribution of management accounting

system to overcome from financial issues.

TASK 1

P1 Analysis of management accounting and their essential requirement in organisation

Management accounting- It is a procedure of preparing the management accounts as

well as reports which gives timely and accurate statistical and financial information needed

through employers to take decision on short term basis and day- to- day (Christ and Burritt,

2013). Manager of Tech business organisation uses accounting provisions in context to provide

the better and effective information before taking any kind of decisions in company.

Every organisation is need to adopt effective management accounting systems which

helps in recording of business transactions in more effective and appropriate manner.

Management accounting systems are considered as decision making tool which is used internally

by manager. The different tools which are included in this system are budgeting, variance

analysis, BEP, cost-volume-profit analysis etc. It helps the manager to formulate different reports

for improvement of understanding among different departments about their functions

(Baldvinsdottir, Mitchell and Nørreklit, 2010). Overall, it helps in completion of their

organisational objectives within stipulated period of time. Tech(UK)Ltd. Is manufacturing

organisation which provides their products to retailer.

In the present report explain about, concepts of management accounting and its

distinguish with financial accounting, importance of management accounting information as

decision making tool for departmental managers, application of different management

accounting systems in organisation, different types of managerial reports and its importance in

organisational scenario. Also, contribution of cost accounting techniques in preparation of

income statements, budget preparation process and contribution of management accounting

system to overcome from financial issues.

TASK 1

P1 Analysis of management accounting and their essential requirement in organisation

Management accounting- It is a procedure of preparing the management accounts as

well as reports which gives timely and accurate statistical and financial information needed

through employers to take decision on short term basis and day- to- day (Christ and Burritt,

2013). Manager of Tech business organisation uses accounting provisions in context to provide

the better and effective information before taking any kind of decisions in company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management accounting systems are use different accounting provisions in order to

develop various accounts which gives relevant information or data related to various

organisational functions. It is helpful for Tech company in developing policies, process of

decision making and also day to day operations.

Importance of management accounting as decision-making tool

Performance measurement- It assess company in measuring performance of staff

members as well as their efficiency. Under this, there is a comparison of the actual performance

with standardised performance to set deviations under which important steps can executed

(Fullerton, Kennedy and Widener, 2014).

Resources allocation- Tech firm able to accomplish proper utilisation of available

resources through resource allocation to different departments and divisions in company.

Risk assessment- It helps and determines all risk related factors with in Tech

organisation which can reduced by the effective management.

Presentation of financial statement- Management accounting gives proper or effective

presentation of Tech company with needed data or information. Different financial and cost data

makes easy for firm to show precise and better financial reports which will be helpful in taking

better decision making.

Formulation of budgets: Management accounting system helps in formulation of

different kind of reports as per the performance of different departments. It helps in formulation

of budgets according to their needs.

Difference among financial and management accounting

Financial accounting is an area of accounting which is related with analysis, summary

and also reporting of all financial transactions come to business (Garrison and et. al., 2010). It

consists make of financial statements which are available for public consumption.

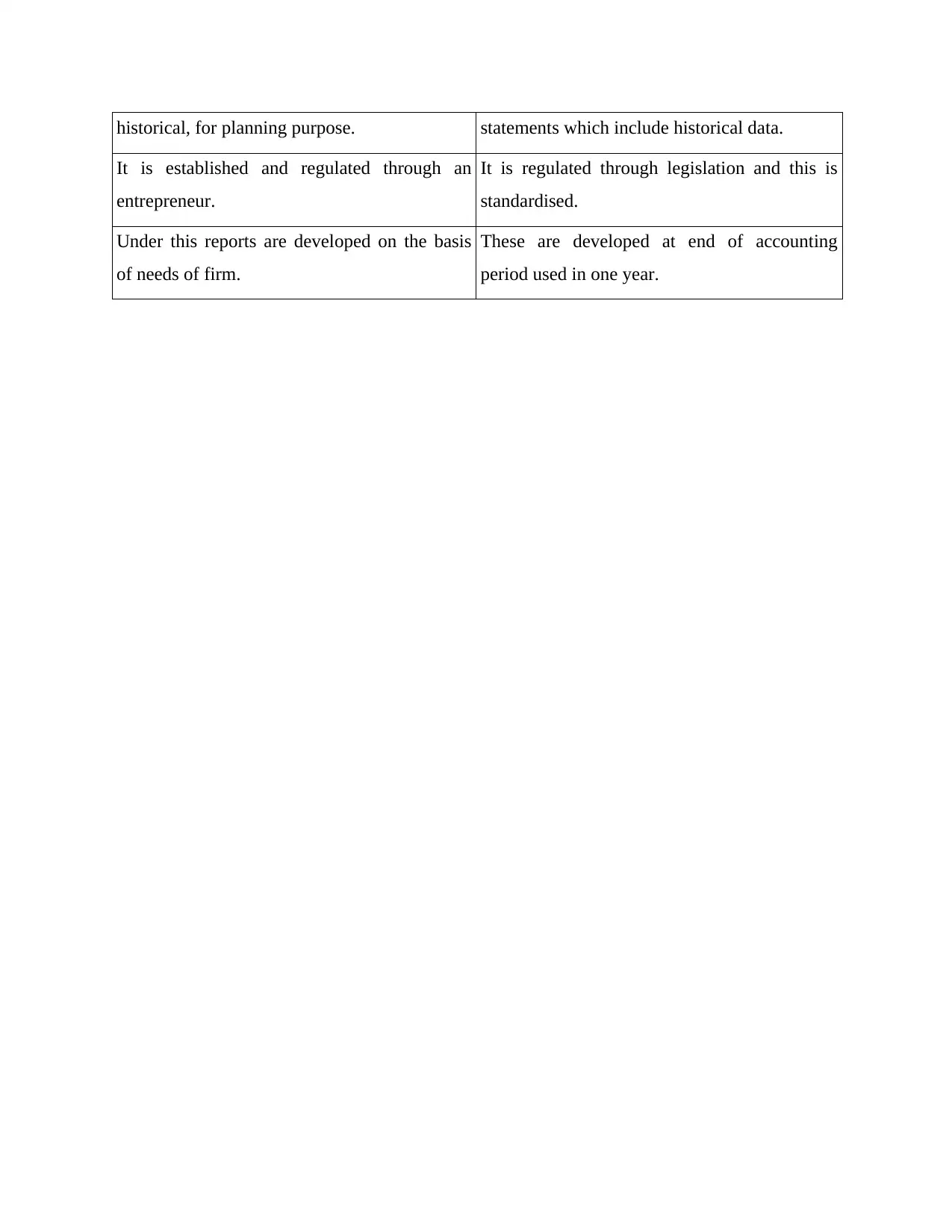

Management Accounting Financial Accounting

It gives relevant and accurate data to

employers to prepare strategies, policies and

plans for running business in an effective

manner.

It is an effective accounting system which

focus on developing financial statement of firm

to give financial information and data to

interested parties.

It used future information and data not Its main focus on past economic events,

develop various accounts which gives relevant information or data related to various

organisational functions. It is helpful for Tech company in developing policies, process of

decision making and also day to day operations.

Importance of management accounting as decision-making tool

Performance measurement- It assess company in measuring performance of staff

members as well as their efficiency. Under this, there is a comparison of the actual performance

with standardised performance to set deviations under which important steps can executed

(Fullerton, Kennedy and Widener, 2014).

Resources allocation- Tech firm able to accomplish proper utilisation of available

resources through resource allocation to different departments and divisions in company.

Risk assessment- It helps and determines all risk related factors with in Tech

organisation which can reduced by the effective management.

Presentation of financial statement- Management accounting gives proper or effective

presentation of Tech company with needed data or information. Different financial and cost data

makes easy for firm to show precise and better financial reports which will be helpful in taking

better decision making.

Formulation of budgets: Management accounting system helps in formulation of

different kind of reports as per the performance of different departments. It helps in formulation

of budgets according to their needs.

Difference among financial and management accounting

Financial accounting is an area of accounting which is related with analysis, summary

and also reporting of all financial transactions come to business (Garrison and et. al., 2010). It

consists make of financial statements which are available for public consumption.

Management Accounting Financial Accounting

It gives relevant and accurate data to

employers to prepare strategies, policies and

plans for running business in an effective

manner.

It is an effective accounting system which

focus on developing financial statement of firm

to give financial information and data to

interested parties.

It used future information and data not Its main focus on past economic events,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

historical, for planning purpose. statements which include historical data.

It is established and regulated through an

entrepreneur.

It is regulated through legislation and this is

standardised.

Under this reports are developed on the basis

of needs of firm.

These are developed at end of accounting

period used in one year.

It is established and regulated through an

entrepreneur.

It is regulated through legislation and this is

standardised.

Under this reports are developed on the basis

of needs of firm.

These are developed at end of accounting

period used in one year.

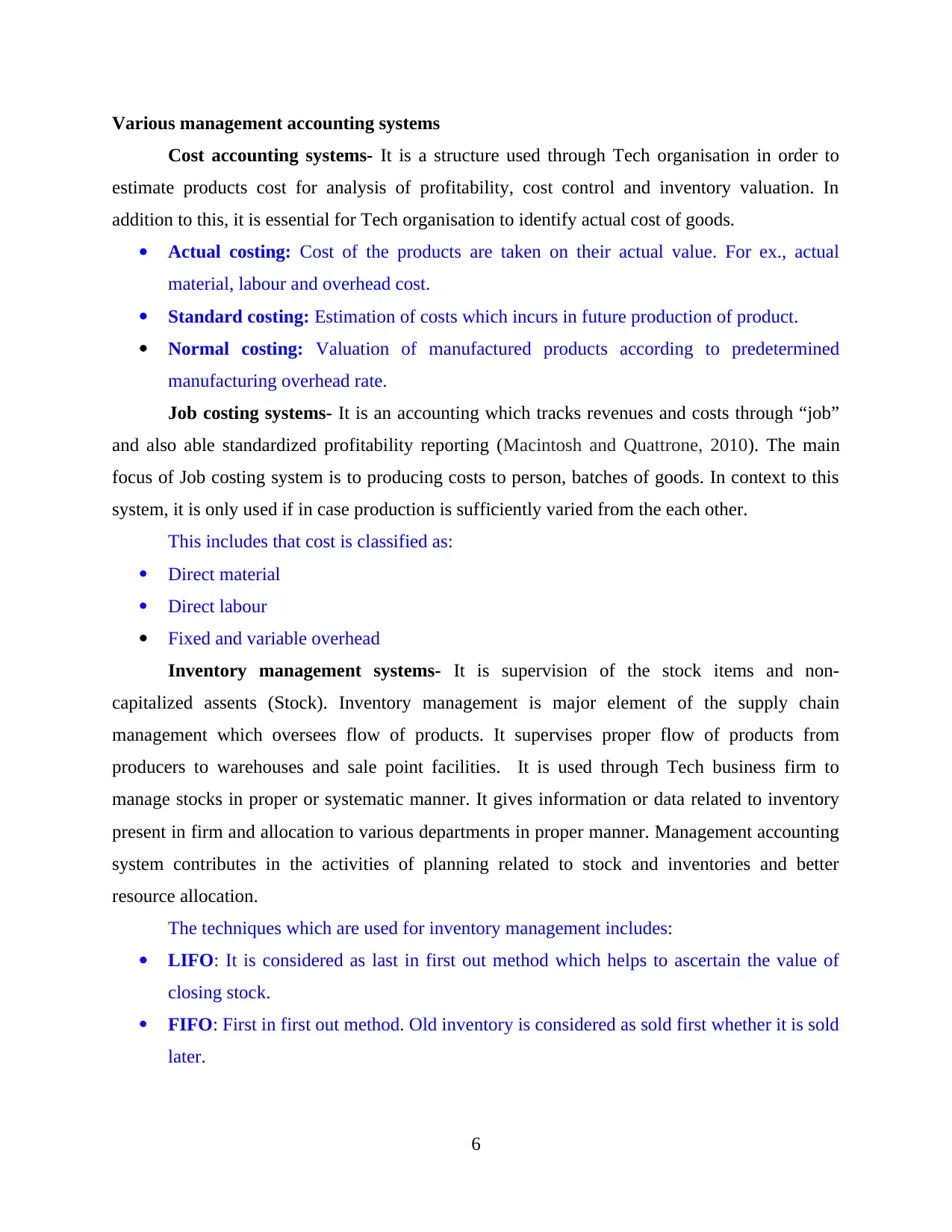

Various management accounting systems

Cost accounting systems- It is a structure used through Tech organisation in order to

estimate products cost for analysis of profitability, cost control and inventory valuation. In

addition to this, it is essential for Tech organisation to identify actual cost of goods.

Actual costing: Cost of the products are taken on their actual value. For ex., actual

material, labour and overhead cost.

Standard costing: Estimation of costs which incurs in future production of product.

Normal costing: Valuation of manufactured products according to predetermined

manufacturing overhead rate.

Job costing systems- It is an accounting which tracks revenues and costs through “job”

and also able standardized profitability reporting (Macintosh and Quattrone, 2010). The main

focus of Job costing system is to producing costs to person, batches of goods. In context to this

system, it is only used if in case production is sufficiently varied from the each other.

This includes that cost is classified as:

Direct material

Direct labour

Fixed and variable overhead

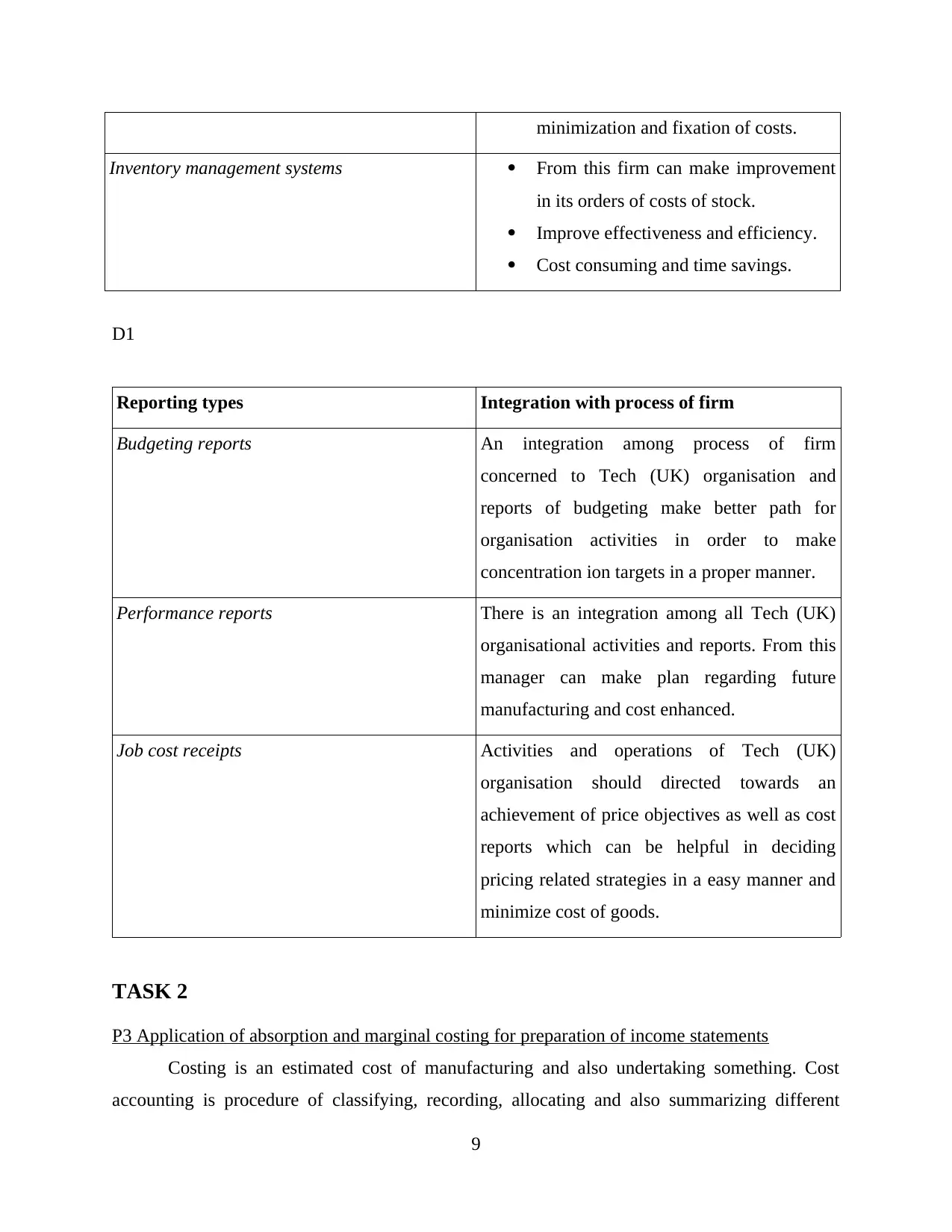

Inventory management systems- It is supervision of the stock items and non-

capitalized assents (Stock). Inventory management is major element of the supply chain

management which oversees flow of products. It supervises proper flow of products from

producers to warehouses and sale point facilities. It is used through Tech business firm to

manage stocks in proper or systematic manner. It gives information or data related to inventory

present in firm and allocation to various departments in proper manner. Management accounting

system contributes in the activities of planning related to stock and inventories and better

resource allocation.

The techniques which are used for inventory management includes:

LIFO: It is considered as last in first out method which helps to ascertain the value of

closing stock.

FIFO: First in first out method. Old inventory is considered as sold first whether it is sold

later.

6

Cost accounting systems- It is a structure used through Tech organisation in order to

estimate products cost for analysis of profitability, cost control and inventory valuation. In

addition to this, it is essential for Tech organisation to identify actual cost of goods.

Actual costing: Cost of the products are taken on their actual value. For ex., actual

material, labour and overhead cost.

Standard costing: Estimation of costs which incurs in future production of product.

Normal costing: Valuation of manufactured products according to predetermined

manufacturing overhead rate.

Job costing systems- It is an accounting which tracks revenues and costs through “job”

and also able standardized profitability reporting (Macintosh and Quattrone, 2010). The main

focus of Job costing system is to producing costs to person, batches of goods. In context to this

system, it is only used if in case production is sufficiently varied from the each other.

This includes that cost is classified as:

Direct material

Direct labour

Fixed and variable overhead

Inventory management systems- It is supervision of the stock items and non-

capitalized assents (Stock). Inventory management is major element of the supply chain

management which oversees flow of products. It supervises proper flow of products from

producers to warehouses and sale point facilities. It is used through Tech business firm to

manage stocks in proper or systematic manner. It gives information or data related to inventory

present in firm and allocation to various departments in proper manner. Management accounting

system contributes in the activities of planning related to stock and inventories and better

resource allocation.

The techniques which are used for inventory management includes:

LIFO: It is considered as last in first out method which helps to ascertain the value of

closing stock.

FIFO: First in first out method. Old inventory is considered as sold first whether it is sold

later.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

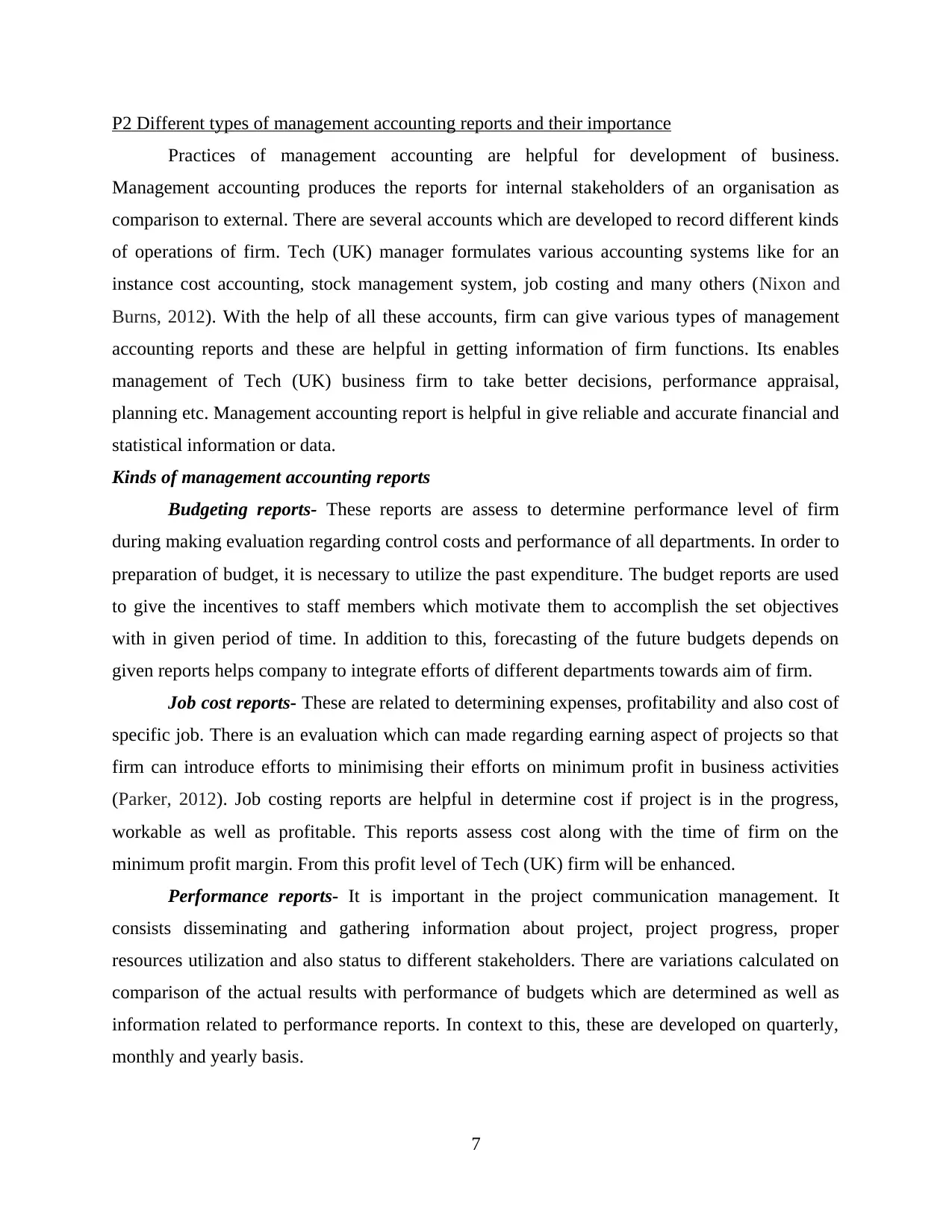

P2 Different types of management accounting reports and their importance

Practices of management accounting are helpful for development of business.

Management accounting produces the reports for internal stakeholders of an organisation as

comparison to external. There are several accounts which are developed to record different kinds

of operations of firm. Tech (UK) manager formulates various accounting systems like for an

instance cost accounting, stock management system, job costing and many others (Nixon and

Burns, 2012). With the help of all these accounts, firm can give various types of management

accounting reports and these are helpful in getting information of firm functions. Its enables

management of Tech (UK) business firm to take better decisions, performance appraisal,

planning etc. Management accounting report is helpful in give reliable and accurate financial and

statistical information or data.

Kinds of management accounting reports

Budgeting reports- These reports are assess to determine performance level of firm

during making evaluation regarding control costs and performance of all departments. In order to

preparation of budget, it is necessary to utilize the past expenditure. The budget reports are used

to give the incentives to staff members which motivate them to accomplish the set objectives

with in given period of time. In addition to this, forecasting of the future budgets depends on

given reports helps company to integrate efforts of different departments towards aim of firm.

Job cost reports- These are related to determining expenses, profitability and also cost of

specific job. There is an evaluation which can made regarding earning aspect of projects so that

firm can introduce efforts to minimising their efforts on minimum profit in business activities

(Parker, 2012). Job costing reports are helpful in determine cost if project is in the progress,

workable as well as profitable. This reports assess cost along with the time of firm on the

minimum profit margin. From this profit level of Tech (UK) firm will be enhanced.

Performance reports- It is important in the project communication management. It

consists disseminating and gathering information about project, project progress, proper

resources utilization and also status to different stakeholders. There are variations calculated on

comparison of the actual results with performance of budgets which are determined as well as

information related to performance reports. In context to this, these are developed on quarterly,

monthly and yearly basis.

7

Practices of management accounting are helpful for development of business.

Management accounting produces the reports for internal stakeholders of an organisation as

comparison to external. There are several accounts which are developed to record different kinds

of operations of firm. Tech (UK) manager formulates various accounting systems like for an

instance cost accounting, stock management system, job costing and many others (Nixon and

Burns, 2012). With the help of all these accounts, firm can give various types of management

accounting reports and these are helpful in getting information of firm functions. Its enables

management of Tech (UK) business firm to take better decisions, performance appraisal,

planning etc. Management accounting report is helpful in give reliable and accurate financial and

statistical information or data.

Kinds of management accounting reports

Budgeting reports- These reports are assess to determine performance level of firm

during making evaluation regarding control costs and performance of all departments. In order to

preparation of budget, it is necessary to utilize the past expenditure. The budget reports are used

to give the incentives to staff members which motivate them to accomplish the set objectives

with in given period of time. In addition to this, forecasting of the future budgets depends on

given reports helps company to integrate efforts of different departments towards aim of firm.

Job cost reports- These are related to determining expenses, profitability and also cost of

specific job. There is an evaluation which can made regarding earning aspect of projects so that

firm can introduce efforts to minimising their efforts on minimum profit in business activities

(Parker, 2012). Job costing reports are helpful in determine cost if project is in the progress,

workable as well as profitable. This reports assess cost along with the time of firm on the

minimum profit margin. From this profit level of Tech (UK) firm will be enhanced.

Performance reports- It is important in the project communication management. It

consists disseminating and gathering information about project, project progress, proper

resources utilization and also status to different stakeholders. There are variations calculated on

comparison of the actual results with performance of budgets which are determined as well as

information related to performance reports. In context to this, these are developed on quarterly,

monthly and yearly basis.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

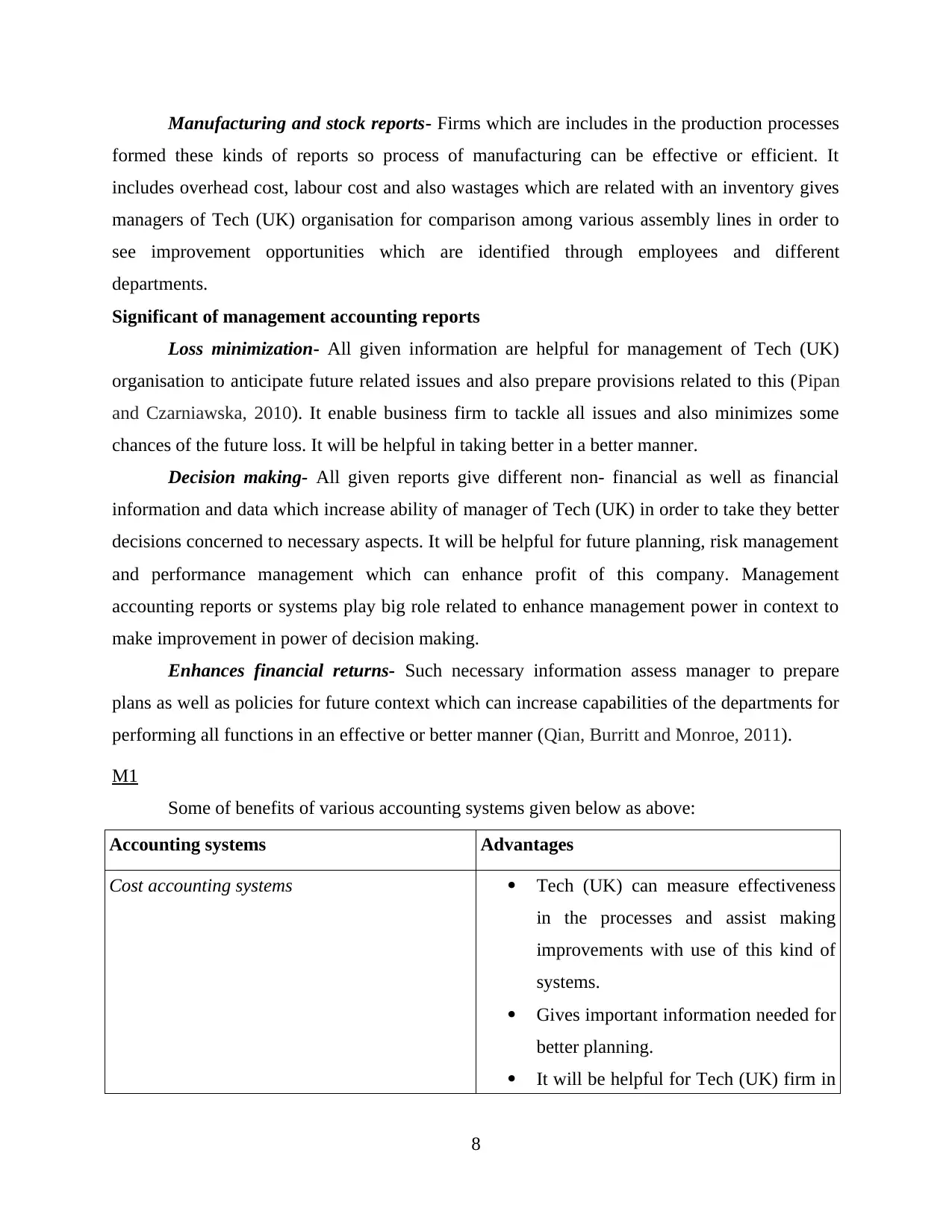

Manufacturing and stock reports- Firms which are includes in the production processes

formed these kinds of reports so process of manufacturing can be effective or efficient. It

includes overhead cost, labour cost and also wastages which are related with an inventory gives

managers of Tech (UK) organisation for comparison among various assembly lines in order to

see improvement opportunities which are identified through employees and different

departments.

Significant of management accounting reports

Loss minimization- All given information are helpful for management of Tech (UK)

organisation to anticipate future related issues and also prepare provisions related to this (Pipan

and Czarniawska, 2010). It enable business firm to tackle all issues and also minimizes some

chances of the future loss. It will be helpful in taking better in a better manner.

Decision making- All given reports give different non- financial as well as financial

information and data which increase ability of manager of Tech (UK) in order to take they better

decisions concerned to necessary aspects. It will be helpful for future planning, risk management

and performance management which can enhance profit of this company. Management

accounting reports or systems play big role related to enhance management power in context to

make improvement in power of decision making.

Enhances financial returns- Such necessary information assess manager to prepare

plans as well as policies for future context which can increase capabilities of the departments for

performing all functions in an effective or better manner (Qian, Burritt and Monroe, 2011).

M1

Some of benefits of various accounting systems given below as above:

Accounting systems Advantages

Cost accounting systems Tech (UK) can measure effectiveness

in the processes and assist making

improvements with use of this kind of

systems.

Gives important information needed for

better planning.

It will be helpful for Tech (UK) firm in

8

formed these kinds of reports so process of manufacturing can be effective or efficient. It

includes overhead cost, labour cost and also wastages which are related with an inventory gives

managers of Tech (UK) organisation for comparison among various assembly lines in order to

see improvement opportunities which are identified through employees and different

departments.

Significant of management accounting reports

Loss minimization- All given information are helpful for management of Tech (UK)

organisation to anticipate future related issues and also prepare provisions related to this (Pipan

and Czarniawska, 2010). It enable business firm to tackle all issues and also minimizes some

chances of the future loss. It will be helpful in taking better in a better manner.

Decision making- All given reports give different non- financial as well as financial

information and data which increase ability of manager of Tech (UK) in order to take they better

decisions concerned to necessary aspects. It will be helpful for future planning, risk management

and performance management which can enhance profit of this company. Management

accounting reports or systems play big role related to enhance management power in context to

make improvement in power of decision making.

Enhances financial returns- Such necessary information assess manager to prepare

plans as well as policies for future context which can increase capabilities of the departments for

performing all functions in an effective or better manner (Qian, Burritt and Monroe, 2011).

M1

Some of benefits of various accounting systems given below as above:

Accounting systems Advantages

Cost accounting systems Tech (UK) can measure effectiveness

in the processes and assist making

improvements with use of this kind of

systems.

Gives important information needed for

better planning.

It will be helpful for Tech (UK) firm in

8

minimization and fixation of costs.

Inventory management systems From this firm can make improvement

in its orders of costs of stock.

Improve effectiveness and efficiency.

Cost consuming and time savings.

D1

Reporting types Integration with process of firm

Budgeting reports An integration among process of firm

concerned to Tech (UK) organisation and

reports of budgeting make better path for

organisation activities in order to make

concentration ion targets in a proper manner.

Performance reports There is an integration among all Tech (UK)

organisational activities and reports. From this

manager can make plan regarding future

manufacturing and cost enhanced.

Job cost receipts Activities and operations of Tech (UK)

organisation should directed towards an

achievement of price objectives as well as cost

reports which can be helpful in deciding

pricing related strategies in a easy manner and

minimize cost of goods.

TASK 2

P3 Application of absorption and marginal costing for preparation of income statements

Costing is an estimated cost of manufacturing and also undertaking something. Cost

accounting is procedure of classifying, recording, allocating and also summarizing different

9

Inventory management systems From this firm can make improvement

in its orders of costs of stock.

Improve effectiveness and efficiency.

Cost consuming and time savings.

D1

Reporting types Integration with process of firm

Budgeting reports An integration among process of firm

concerned to Tech (UK) organisation and

reports of budgeting make better path for

organisation activities in order to make

concentration ion targets in a proper manner.

Performance reports There is an integration among all Tech (UK)

organisational activities and reports. From this

manager can make plan regarding future

manufacturing and cost enhanced.

Job cost receipts Activities and operations of Tech (UK)

organisation should directed towards an

achievement of price objectives as well as cost

reports which can be helpful in deciding

pricing related strategies in a easy manner and

minimize cost of goods.

TASK 2

P3 Application of absorption and marginal costing for preparation of income statements

Costing is an estimated cost of manufacturing and also undertaking something. Cost

accounting is procedure of classifying, recording, allocating and also summarizing different

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

alternative action course for control of pricing (Vaivio and Sirén, 2010). There are different

kinds of costing mention below:

Absorption costing- It is a main method of calculating cost of goods or an organisation

through taking in to an account all indirect expenses and direct costs.

Marginal costing- It is an additional cost which are incurred in manufacture of extra

units of products. It is an significant economic theory due to increasing profit.

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material cost 8

Direct labour cost 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

Nil 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £Amount £ Amount

Sales value

Less: Variable costs

Stock at the begining

Cost of production

Stock at the closing

Variable sales overheads

Contribution

Less: Fixed costs:

Fixed Production overheads

Fixed Selling overheads

NIL

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

10

kinds of costing mention below:

Absorption costing- It is a main method of calculating cost of goods or an organisation

through taking in to an account all indirect expenses and direct costs.

Marginal costing- It is an additional cost which are incurred in manufacture of extra

units of products. It is an significant economic theory due to increasing profit.

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material cost 8

Direct labour cost 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

Nil 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £Amount £ Amount

Sales value

Less: Variable costs

Stock at the begining

Cost of production

Stock at the closing

Variable sales overheads

Contribution

Less: Fixed costs:

Fixed Production overheads

Fixed Selling overheads

NIL

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net loss -2875

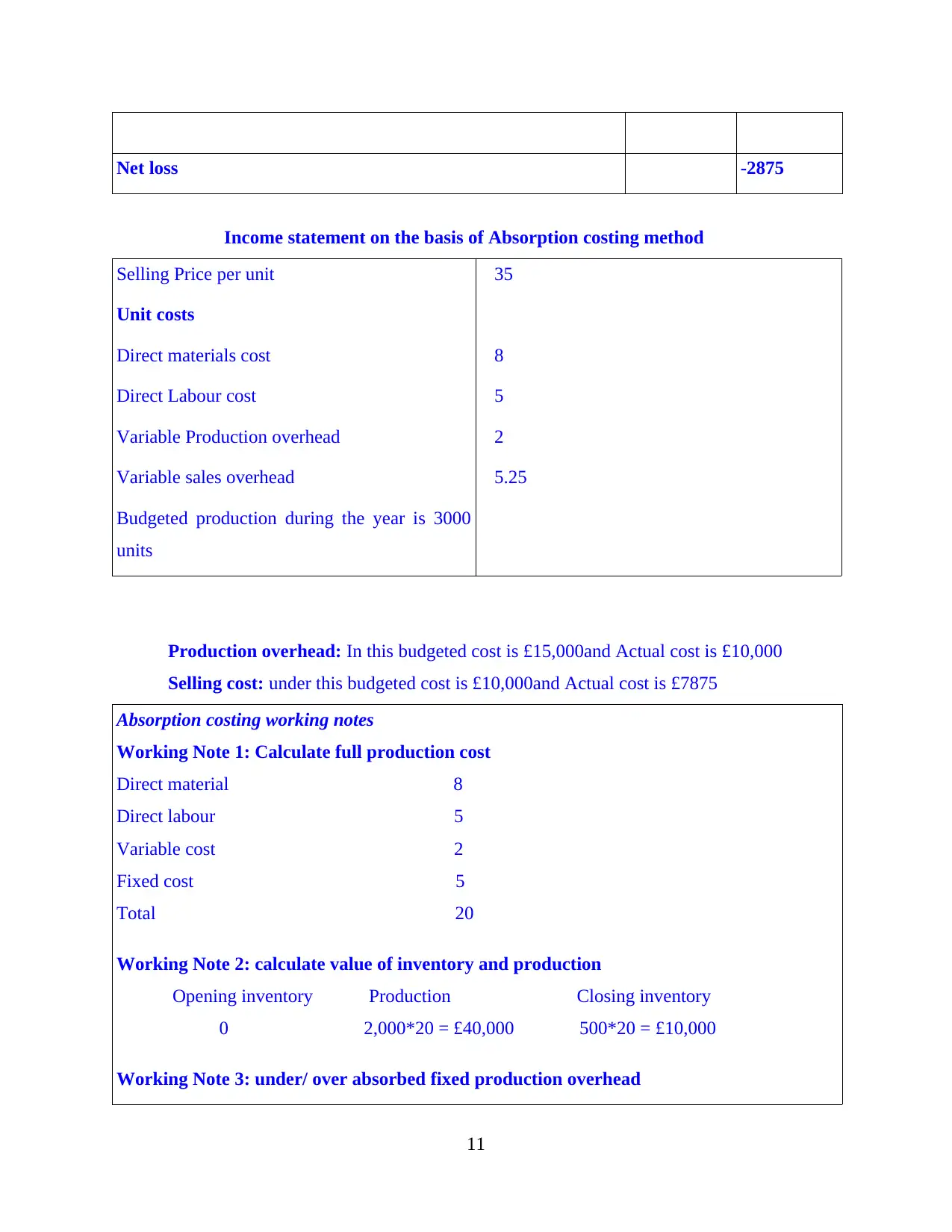

Income statement on the basis of Absorption costing method

Selling Price per unit £35

Unit costs

Direct materials cost £8

Direct Labour cost £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted production during the year is 3000

units

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: under this budgeted cost is £10,000and Actual cost is £7875

Absorption costing working notes

Working Note 1: Calculate full production cost

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40,000 500*20 = £10,000

Working Note 3: under/ over absorbed fixed production overhead

11

Income statement on the basis of Absorption costing method

Selling Price per unit £35

Unit costs

Direct materials cost £8

Direct Labour cost £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted production during the year is 3000

units

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: under this budgeted cost is £10,000and Actual cost is £7875

Absorption costing working notes

Working Note 1: Calculate full production cost

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40,000 500*20 = £10,000

Working Note 3: under/ over absorbed fixed production overhead

11

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000 (under absorbed)

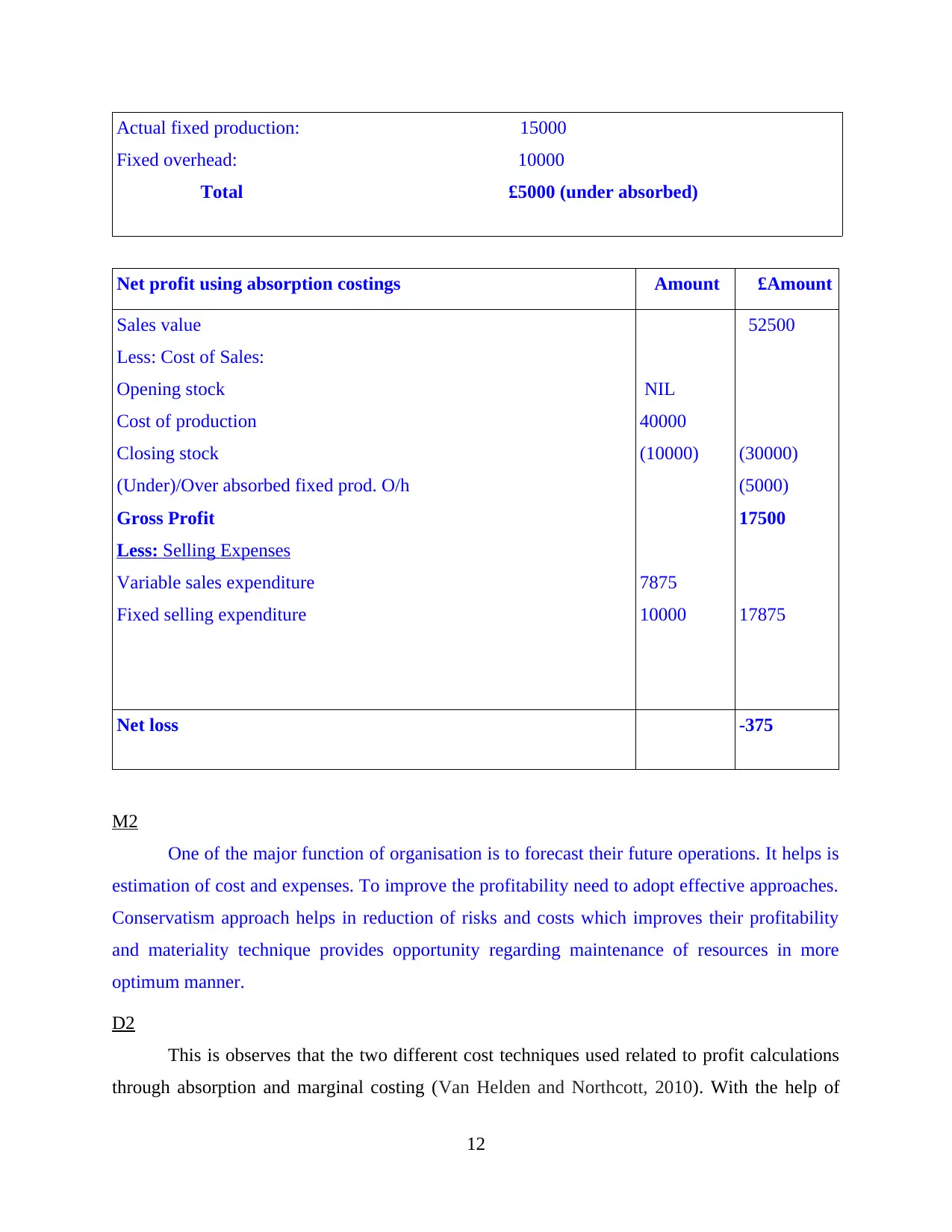

Net profit using absorption costings £Amount £Amount

Sales value

Less: Cost of Sales:

Opening stock

Cost of production

Closing stock

(Under)/Over absorbed fixed prod. O/h

Gross Profit

Less: Selling Expenses

Variable sales expenditure

Fixed selling expenditure

NIL

40000

(10000)

7875

10000

52500

(30000)

(5000)

17500

17875

Net loss -375

M2

One of the major function of organisation is to forecast their future operations. It helps is

estimation of cost and expenses. To improve the profitability need to adopt effective approaches.

Conservatism approach helps in reduction of risks and costs which improves their profitability

and materiality technique provides opportunity regarding maintenance of resources in more

optimum manner.

D2

This is observes that the two different cost techniques used related to profit calculations

through absorption and marginal costing (Van Helden and Northcott, 2010). With the help of

12

Fixed overhead: £10000

Total £5000 (under absorbed)

Net profit using absorption costings £Amount £Amount

Sales value

Less: Cost of Sales:

Opening stock

Cost of production

Closing stock

(Under)/Over absorbed fixed prod. O/h

Gross Profit

Less: Selling Expenses

Variable sales expenditure

Fixed selling expenditure

NIL

40000

(10000)

7875

10000

52500

(30000)

(5000)

17500

17875

Net loss -375

M2

One of the major function of organisation is to forecast their future operations. It helps is

estimation of cost and expenses. To improve the profitability need to adopt effective approaches.

Conservatism approach helps in reduction of risks and costs which improves their profitability

and materiality technique provides opportunity regarding maintenance of resources in more

optimum manner.

D2

This is observes that the two different cost techniques used related to profit calculations

through absorption and marginal costing (Van Helden and Northcott, 2010). With the help of

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.