Management Accounting Report: Financial Analysis of Tech Ltd

VerifiedAdded on 2020/06/06

|24

|6442

|54

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles, focusing on a case study of Tech Ltd, a company producing special chargers for mobile telephones. The report begins by differentiating between management and financial accounting, emphasizing the role of management accounting in decision-making for department managers. It explores various management accounting systems, including cost accounting, inventory management, and job costing, along with their advantages and disadvantages. The report presents financial information, discussing different types of managerial accounting reports and their importance. It delves into preparing income statements using marginal and absorption costing methods and includes a reconciliation statement. Furthermore, the report examines budgeting, presenting different types of budgets, their preparation processes, and their significance for planning and control. Finally, it compares the effectiveness of management accounting approaches undertaken by Tech Ltd against those of other organizations, offering a conclusion based on the analysis.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................4

TASK 1......................................................................................................................................4

a. Explaining management accounting and its systems.........................................................4

1. Difference between management and financial accounting...............................................4

2. Stating the importance of management accounting as a decision making tool for

department managers.............................................................................................................5

3. and M1 Cost accounting system........................................................................................6

4 and M1 Inventory management system..............................................................................7

5 and M1 Job costing system.................................................................................................7

b. Presenting financial information........................................................................................8

1 and d1 Presenting different types of managerial accounting report....................................8

2 and d1 Stating why information presented in managerial reports must be understandable9

TASK 2....................................................................................................................................10

Question and D2 Preparing income statement for Tech Ltd as per marginal and absorption

costing system......................................................................................................................10

M2 Reconciliation statement................................................................................................13

TASK 3....................................................................................................................................13

A and M3 Presenting different kinds of budget along with their advantages and

disadvantages.......................................................................................................................13

b. Presenting budget preparation process.............................................................................15

c. Stating the importance of budget as a tool for planning and control...............................16

TASK 4....................................................................................................................................16

Question, M4 and D3 Comparing the effectiveness of management accounting approaches

undertaken by Tech Ltd in against to the other organization..............................................16

CONCLUSION........................................................................................................................18

REFERENCES.........................................................................................................................19

INTRODUCTION......................................................................................................................4

TASK 1......................................................................................................................................4

a. Explaining management accounting and its systems.........................................................4

1. Difference between management and financial accounting...............................................4

2. Stating the importance of management accounting as a decision making tool for

department managers.............................................................................................................5

3. and M1 Cost accounting system........................................................................................6

4 and M1 Inventory management system..............................................................................7

5 and M1 Job costing system.................................................................................................7

b. Presenting financial information........................................................................................8

1 and d1 Presenting different types of managerial accounting report....................................8

2 and d1 Stating why information presented in managerial reports must be understandable9

TASK 2....................................................................................................................................10

Question and D2 Preparing income statement for Tech Ltd as per marginal and absorption

costing system......................................................................................................................10

M2 Reconciliation statement................................................................................................13

TASK 3....................................................................................................................................13

A and M3 Presenting different kinds of budget along with their advantages and

disadvantages.......................................................................................................................13

b. Presenting budget preparation process.............................................................................15

c. Stating the importance of budget as a tool for planning and control...............................16

TASK 4....................................................................................................................................16

Question, M4 and D3 Comparing the effectiveness of management accounting approaches

undertaken by Tech Ltd in against to the other organization..............................................16

CONCLUSION........................................................................................................................18

REFERENCES.........................................................................................................................19

INTRODUCTION

Management accounting is the most importance part of finance which in turn provides

manager with valuable information for decision making. It lays high level of emphasis on

recording information about business operations and functions. In the recent times, each

business unit makes focus on employing management accounting tools as it enables manager

to make appropriate decisions within the suitable time period. Through maintaining financial

records pertaining to the operations manager can analyze business cost and thereby would

become able to prepare internal financial reports for decision making. This report is based on

the case situation of Tech Ltd which is involved in producing special charger for mobile

telephone. In this, report will present the manner in which aspects of management accounting

differ from the financial aspects. Besides this, it will provide deeper insight about

management accounting systems and reporting. Further, in this, how marginal and

absorption costing method helps in evaluating cost as well as profit margin will be assessed.

It also depicts how tools of management accounting can be used by the business for planning

purpose and responding monetary problems.

TASK 1

a. Explaining management accounting and its systems

1. Difference between management and financial accounting

Management accounting serves relevant as well as material information and thereby

assists management in formulating policies, planning, forecasting & controlling day to day

business operations (Macintosh and Quattrone, 2010).

Financial accounting system is highly concerned with the preparation of monetary

statements such as income, cash flow and balance sheet. All such statements assist both

internal and external stakeholders in decision making.

Both management and financial accounting systems aid in the decision making aspect

but they vary in the following manner:

Management accounting is the most importance part of finance which in turn provides

manager with valuable information for decision making. It lays high level of emphasis on

recording information about business operations and functions. In the recent times, each

business unit makes focus on employing management accounting tools as it enables manager

to make appropriate decisions within the suitable time period. Through maintaining financial

records pertaining to the operations manager can analyze business cost and thereby would

become able to prepare internal financial reports for decision making. This report is based on

the case situation of Tech Ltd which is involved in producing special charger for mobile

telephone. In this, report will present the manner in which aspects of management accounting

differ from the financial aspects. Besides this, it will provide deeper insight about

management accounting systems and reporting. Further, in this, how marginal and

absorption costing method helps in evaluating cost as well as profit margin will be assessed.

It also depicts how tools of management accounting can be used by the business for planning

purpose and responding monetary problems.

TASK 1

a. Explaining management accounting and its systems

1. Difference between management and financial accounting

Management accounting serves relevant as well as material information and thereby

assists management in formulating policies, planning, forecasting & controlling day to day

business operations (Macintosh and Quattrone, 2010).

Financial accounting system is highly concerned with the preparation of monetary

statements such as income, cash flow and balance sheet. All such statements assist both

internal and external stakeholders in decision making.

Both management and financial accounting systems aid in the decision making aspect

but they vary in the following manner:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

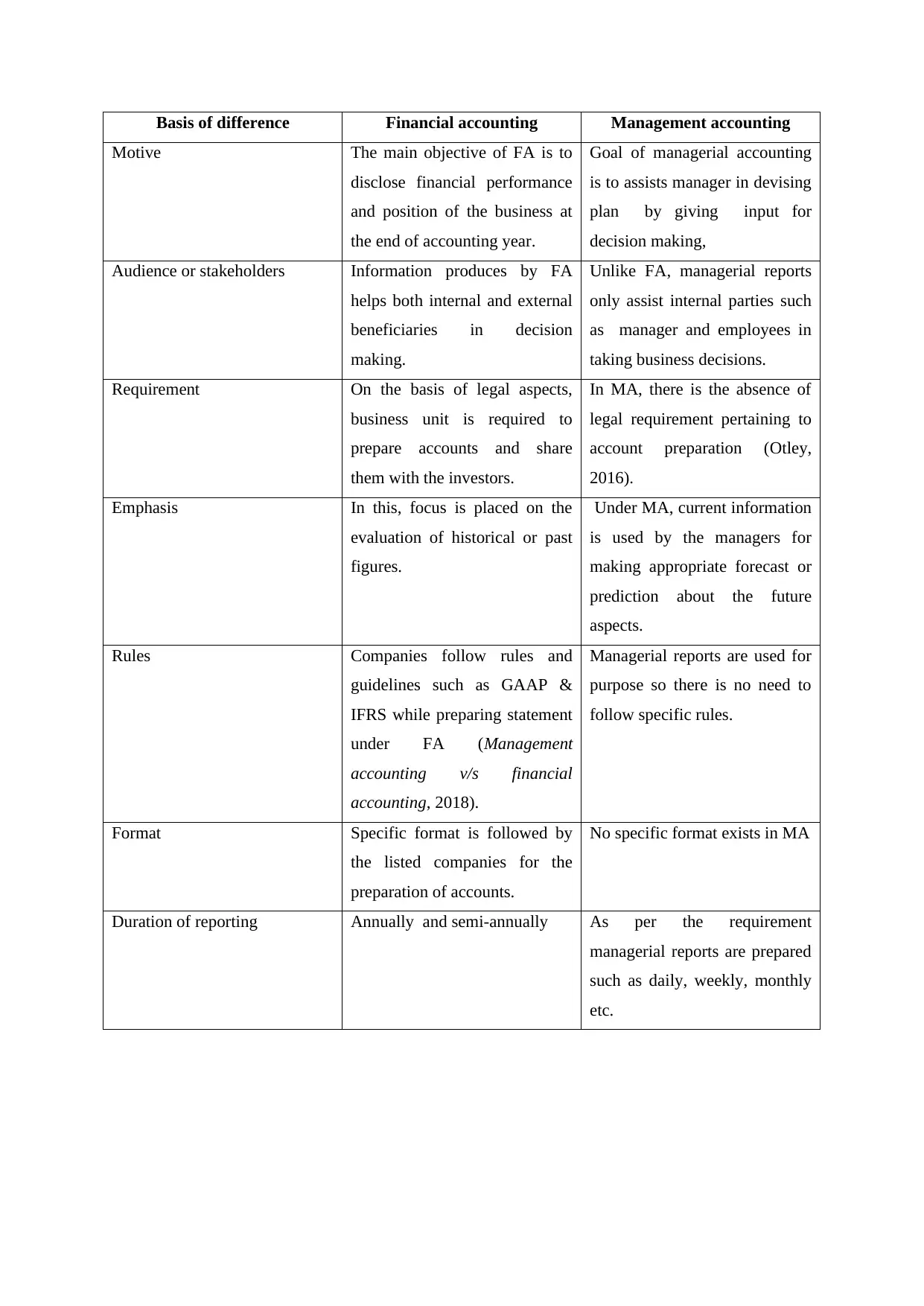

Basis of difference Financial accounting Management accounting

Motive The main objective of FA is to

disclose financial performance

and position of the business at

the end of accounting year.

Goal of managerial accounting

is to assists manager in devising

plan by giving input for

decision making,

Audience or stakeholders Information produces by FA

helps both internal and external

beneficiaries in decision

making.

Unlike FA, managerial reports

only assist internal parties such

as manager and employees in

taking business decisions.

Requirement On the basis of legal aspects,

business unit is required to

prepare accounts and share

them with the investors.

In MA, there is the absence of

legal requirement pertaining to

account preparation (Otley,

2016).

Emphasis In this, focus is placed on the

evaluation of historical or past

figures.

Under MA, current information

is used by the managers for

making appropriate forecast or

prediction about the future

aspects.

Rules Companies follow rules and

guidelines such as GAAP &

IFRS while preparing statement

under FA (Management

accounting v/s financial

accounting, 2018).

Managerial reports are used for

purpose so there is no need to

follow specific rules.

Format Specific format is followed by

the listed companies for the

preparation of accounts.

No specific format exists in MA

Duration of reporting Annually and semi-annually As per the requirement

managerial reports are prepared

such as daily, weekly, monthly

etc.

Motive The main objective of FA is to

disclose financial performance

and position of the business at

the end of accounting year.

Goal of managerial accounting

is to assists manager in devising

plan by giving input for

decision making,

Audience or stakeholders Information produces by FA

helps both internal and external

beneficiaries in decision

making.

Unlike FA, managerial reports

only assist internal parties such

as manager and employees in

taking business decisions.

Requirement On the basis of legal aspects,

business unit is required to

prepare accounts and share

them with the investors.

In MA, there is the absence of

legal requirement pertaining to

account preparation (Otley,

2016).

Emphasis In this, focus is placed on the

evaluation of historical or past

figures.

Under MA, current information

is used by the managers for

making appropriate forecast or

prediction about the future

aspects.

Rules Companies follow rules and

guidelines such as GAAP &

IFRS while preparing statement

under FA (Management

accounting v/s financial

accounting, 2018).

Managerial reports are used for

purpose so there is no need to

follow specific rules.

Format Specific format is followed by

the listed companies for the

preparation of accounts.

No specific format exists in MA

Duration of reporting Annually and semi-annually As per the requirement

managerial reports are prepared

such as daily, weekly, monthly

etc.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. Stating the importance of management accounting as a decision making tool for

department managers

Management accounting tools are highly significant in the context of Tech Ltd which

in turn assists manager in taking appropriate business decisions. For managing funds and

business activities manager has to take several decisions each day. In this regard, by using

calculations generated through management accounting tools manager of Tech Ltd can

improve decision making to a great extent. Significance of management accounting as a

decision making tool can be understood in the following manner.

Manager of Tech Ltd can do relevant cost analysis by taking into account managerial

accounting information. It furnishes valuable information to the company and helps in

determining products that need to be produced (Reome and Sinclair, 2017). Along

with this, management accounting information provides assistance to the company in

assessing profitable areas and thereby helps in making marketing efforts in the right

direction.

MA helps company in making forecast about income as well as expenses and thereby

helps in developing competent financial plan for the near future. Budgeting is highly

needed within the business unit for the purpose of making optimal use of financial

resources. Hence, using MA information manager of Tech Ltd can take decision

about future cash inflow and outflows.

Along with this, MA assists company in taking decision pertaining to make or buy.

Usually, with the motive to save cost or reducing expense level company conducts

evaluation whether they should manufacture product in-house or buy from outside.

Hence, referring the outcome of such evaluation Tech Ltd can suitable decision.

3. and M1 Cost accounting system

This management accounting enables manager of Tech Ltd in making estimation

regarding the cost of product or services. It helps in ascertaining expenses incurred for

producing or generating specific output level. Using this system, manager of the company

can track the level of material in terms of raw and finished goods (Simons, 2013). It lays

emphasis on measuring and recording cost individually that is associated with the production.

Hence, by doing evaluation of input with output or actual results company can measure

financial performance. This area of MA mainly includes standard costing system which in

turn helps in assessing deviations. Moreover, such system of MA focuses on finding

deficiencies through comparing actual performance with the predetermined figures. Thus,

department managers

Management accounting tools are highly significant in the context of Tech Ltd which

in turn assists manager in taking appropriate business decisions. For managing funds and

business activities manager has to take several decisions each day. In this regard, by using

calculations generated through management accounting tools manager of Tech Ltd can

improve decision making to a great extent. Significance of management accounting as a

decision making tool can be understood in the following manner.

Manager of Tech Ltd can do relevant cost analysis by taking into account managerial

accounting information. It furnishes valuable information to the company and helps in

determining products that need to be produced (Reome and Sinclair, 2017). Along

with this, management accounting information provides assistance to the company in

assessing profitable areas and thereby helps in making marketing efforts in the right

direction.

MA helps company in making forecast about income as well as expenses and thereby

helps in developing competent financial plan for the near future. Budgeting is highly

needed within the business unit for the purpose of making optimal use of financial

resources. Hence, using MA information manager of Tech Ltd can take decision

about future cash inflow and outflows.

Along with this, MA assists company in taking decision pertaining to make or buy.

Usually, with the motive to save cost or reducing expense level company conducts

evaluation whether they should manufacture product in-house or buy from outside.

Hence, referring the outcome of such evaluation Tech Ltd can suitable decision.

3. and M1 Cost accounting system

This management accounting enables manager of Tech Ltd in making estimation

regarding the cost of product or services. It helps in ascertaining expenses incurred for

producing or generating specific output level. Using this system, manager of the company

can track the level of material in terms of raw and finished goods (Simons, 2013). It lays

emphasis on measuring and recording cost individually that is associated with the production.

Hence, by doing evaluation of input with output or actual results company can measure

financial performance. This area of MA mainly includes standard costing system which in

turn helps in assessing deviations. Moreover, such system of MA focuses on finding

deficiencies through comparing actual performance with the predetermined figures. Thus,

considering deficiencies and associated causes Tech Ltd can formulate suitable strategies and

policy framework.

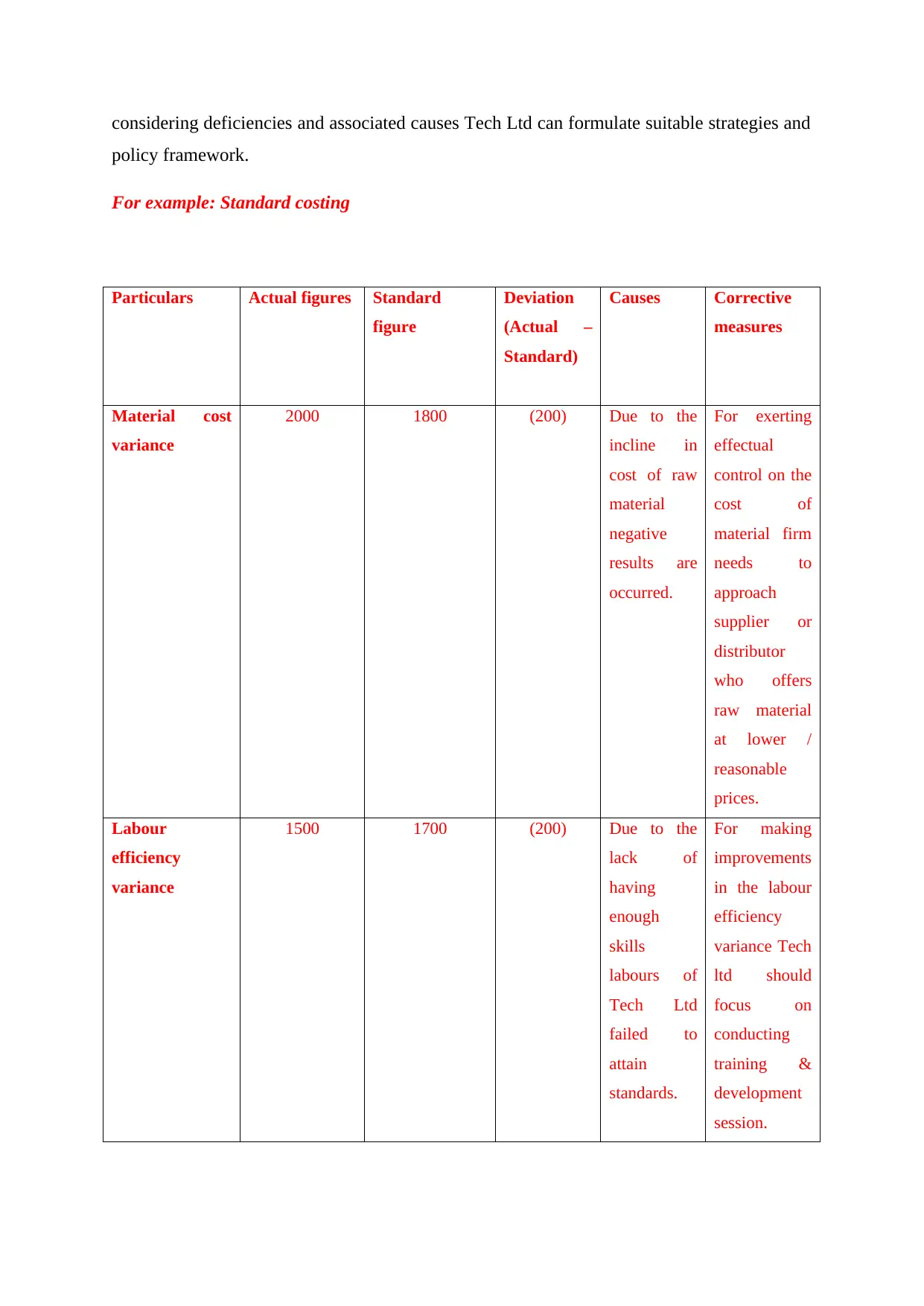

For example: Standard costing

Particulars Actual figures Standard

figure

Deviation

(Actual –

Standard)

Causes Corrective

measures

Material cost

variance

2000 1800 (200) Due to the

incline in

cost of raw

material

negative

results are

occurred.

For exerting

effectual

control on the

cost of

material firm

needs to

approach

supplier or

distributor

who offers

raw material

at lower /

reasonable

prices.

Labour

efficiency

variance

1500 1700 (200) Due to the

lack of

having

enough

skills

labours of

Tech Ltd

failed to

attain

standards.

For making

improvements

in the labour

efficiency

variance Tech

ltd should

focus on

conducting

training &

development

session.

policy framework.

For example: Standard costing

Particulars Actual figures Standard

figure

Deviation

(Actual –

Standard)

Causes Corrective

measures

Material cost

variance

2000 1800 (200) Due to the

incline in

cost of raw

material

negative

results are

occurred.

For exerting

effectual

control on the

cost of

material firm

needs to

approach

supplier or

distributor

who offers

raw material

at lower /

reasonable

prices.

Labour

efficiency

variance

1500 1700 (200) Due to the

lack of

having

enough

skills

labours of

Tech Ltd

failed to

attain

standards.

For making

improvements

in the labour

efficiency

variance Tech

ltd should

focus on

conducting

training &

development

session.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Advantages

By undertaking the system of cost accounting Tech Ltd can eliminate waste, losses

and inefficiencies to the significant level.

In this, focus is placed on the identification of reasons behind profit or loss.

Assists management team in taking make or buy decision (Advantages and

disadvantages of cost accounting, 2018).

Cost accounting system facilitates cost control and thereby helps in improving profit

margin

Disadvantages

In this, only past records are available, whereas management is taking decision about

the future aspects.

For the installation of cost accounting system firm has to maintain several costing

records. This in turn imposes high expenses and thereby impacts margin.

4 and M1 Inventory management system

Stock management is vital within the organization for ensuring smooth functioning of

the business activities and operations. Production and sales related activities are highly

influenced from the aspects pertaining to the availability of raw and finished goods. In

addition to this, ineffective stock management enhances holding & ordering cost level and

thereby overall expenses (Ward, 2012). Hence, under management accounting, several tools

are available such as EOQ, Just in time etc which Tech Ltd can use for inventory

management. Moreover, economic order quantity method clearly presents the time when

order for inventory needs to be placed. Along with this, there are several other methods such

as LIFO, FIFO & AVCO etc which can be used by Tech Ltd for recording and management

of inventory. IFRS emphasizes on the adoption of LIFO method which in turn helps in

reducing tax liabilities or obligations over the time frame. On the contrary to this, FIFO

method does not provide suitable value of stock under inflationary conditions. Thus, using

LIFO method manager of Tech Ltd can ensure proper inventory management. Apart from

this, under batch costing homogenous products are undertaken for the determination of cost

per unit.

Advantages

Facilitates effective functioning of the operations

By undertaking the system of cost accounting Tech Ltd can eliminate waste, losses

and inefficiencies to the significant level.

In this, focus is placed on the identification of reasons behind profit or loss.

Assists management team in taking make or buy decision (Advantages and

disadvantages of cost accounting, 2018).

Cost accounting system facilitates cost control and thereby helps in improving profit

margin

Disadvantages

In this, only past records are available, whereas management is taking decision about

the future aspects.

For the installation of cost accounting system firm has to maintain several costing

records. This in turn imposes high expenses and thereby impacts margin.

4 and M1 Inventory management system

Stock management is vital within the organization for ensuring smooth functioning of

the business activities and operations. Production and sales related activities are highly

influenced from the aspects pertaining to the availability of raw and finished goods. In

addition to this, ineffective stock management enhances holding & ordering cost level and

thereby overall expenses (Ward, 2012). Hence, under management accounting, several tools

are available such as EOQ, Just in time etc which Tech Ltd can use for inventory

management. Moreover, economic order quantity method clearly presents the time when

order for inventory needs to be placed. Along with this, there are several other methods such

as LIFO, FIFO & AVCO etc which can be used by Tech Ltd for recording and management

of inventory. IFRS emphasizes on the adoption of LIFO method which in turn helps in

reducing tax liabilities or obligations over the time frame. On the contrary to this, FIFO

method does not provide suitable value of stock under inflationary conditions. Thus, using

LIFO method manager of Tech Ltd can ensure proper inventory management. Apart from

this, under batch costing homogenous products are undertaken for the determination of cost

per unit.

Advantages

Facilitates effective functioning of the operations

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Reduction in cost level in terms of holding and ordering

Enhancement of profit margin

Avoid situation pertaining to the shortage of stock

Disadvantages

Inventory management software impose high cost

Requires in-depth knowledge and understanding

5 and M1 Job costing system

Tech Ltd can manage its internal operations and functions by taking into account job

costing system. This system focuses on the accumulation of cost associated with the specific

products or services. In the case of having contract with the customers, using such system,

manager of the business unit can provide information to the customers about the areas where

cost reimbursed. Job costing system also allows firm to get reasonable profit margin by

quoting a suitable price. Hence, using such system manager of firm can take suitable pricing

decisions and thereby becomes able to get desired level of profit margin.

Further, job costing includes several other tools or methods which can be used for

price determination namely process, batch, contract and service. Under such costing separate

numbers are allotted and records maintained separately.

Contract costing may be served as the main part of job system which in turn highly

applicable on long term deals. Under such method, separate numbers are allotted to each

contract and records are maintained separately in relation to the same.

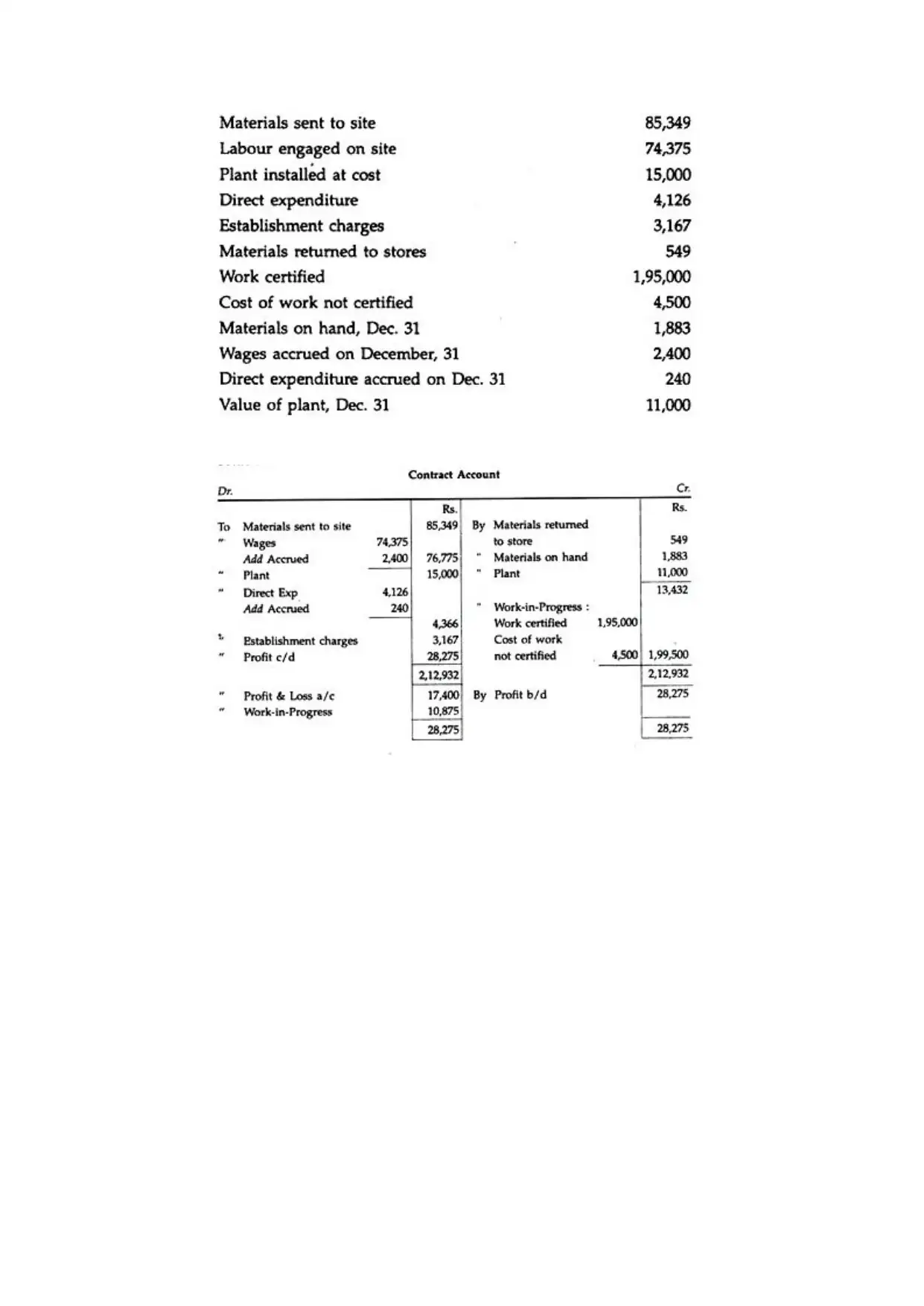

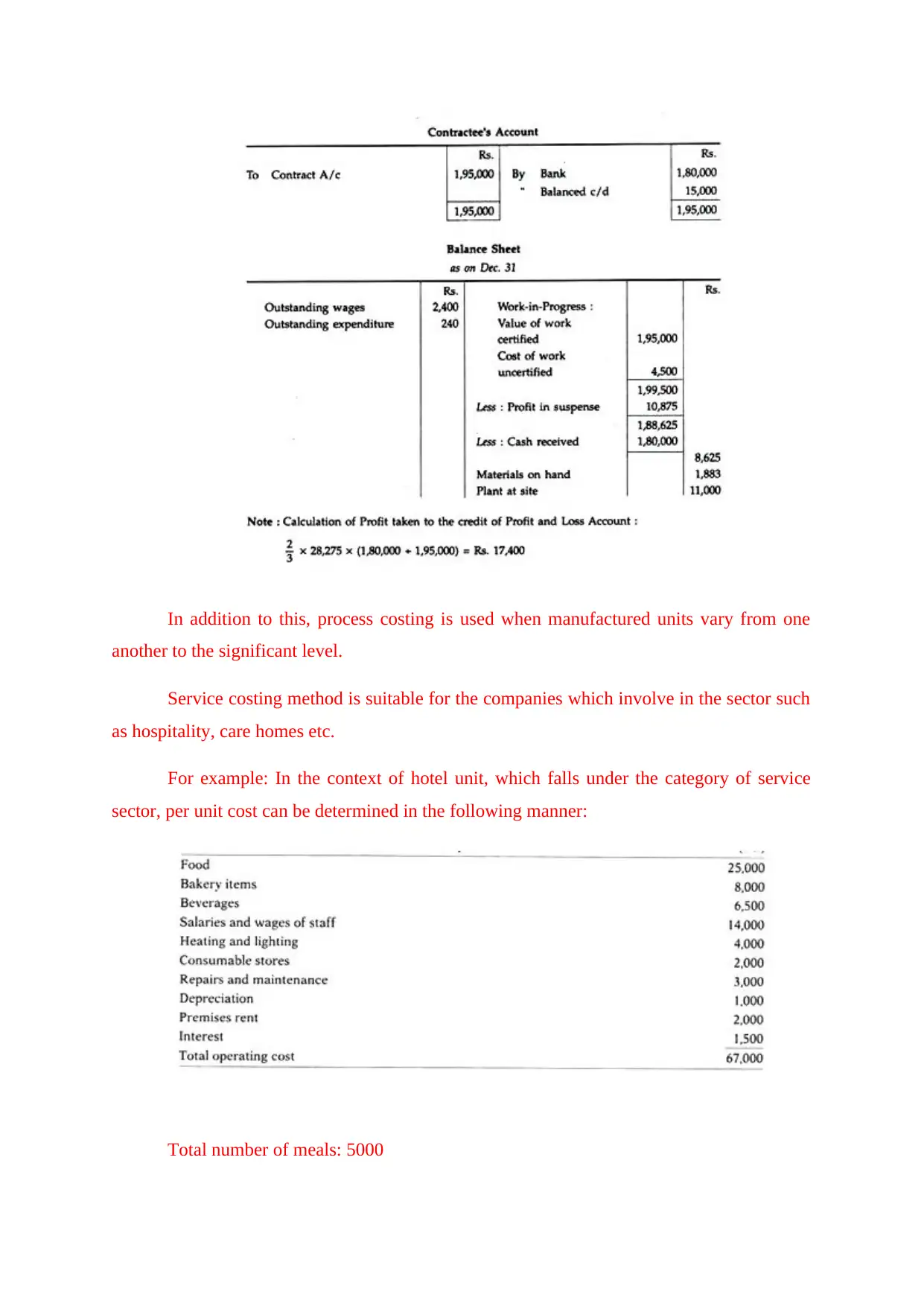

For example:

Enhancement of profit margin

Avoid situation pertaining to the shortage of stock

Disadvantages

Inventory management software impose high cost

Requires in-depth knowledge and understanding

5 and M1 Job costing system

Tech Ltd can manage its internal operations and functions by taking into account job

costing system. This system focuses on the accumulation of cost associated with the specific

products or services. In the case of having contract with the customers, using such system,

manager of the business unit can provide information to the customers about the areas where

cost reimbursed. Job costing system also allows firm to get reasonable profit margin by

quoting a suitable price. Hence, using such system manager of firm can take suitable pricing

decisions and thereby becomes able to get desired level of profit margin.

Further, job costing includes several other tools or methods which can be used for

price determination namely process, batch, contract and service. Under such costing separate

numbers are allotted and records maintained separately.

Contract costing may be served as the main part of job system which in turn highly

applicable on long term deals. Under such method, separate numbers are allotted to each

contract and records are maintained separately in relation to the same.

For example:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In addition to this, process costing is used when manufactured units vary from one

another to the significant level.

Service costing method is suitable for the companies which involve in the sector such

as hospitality, care homes etc.

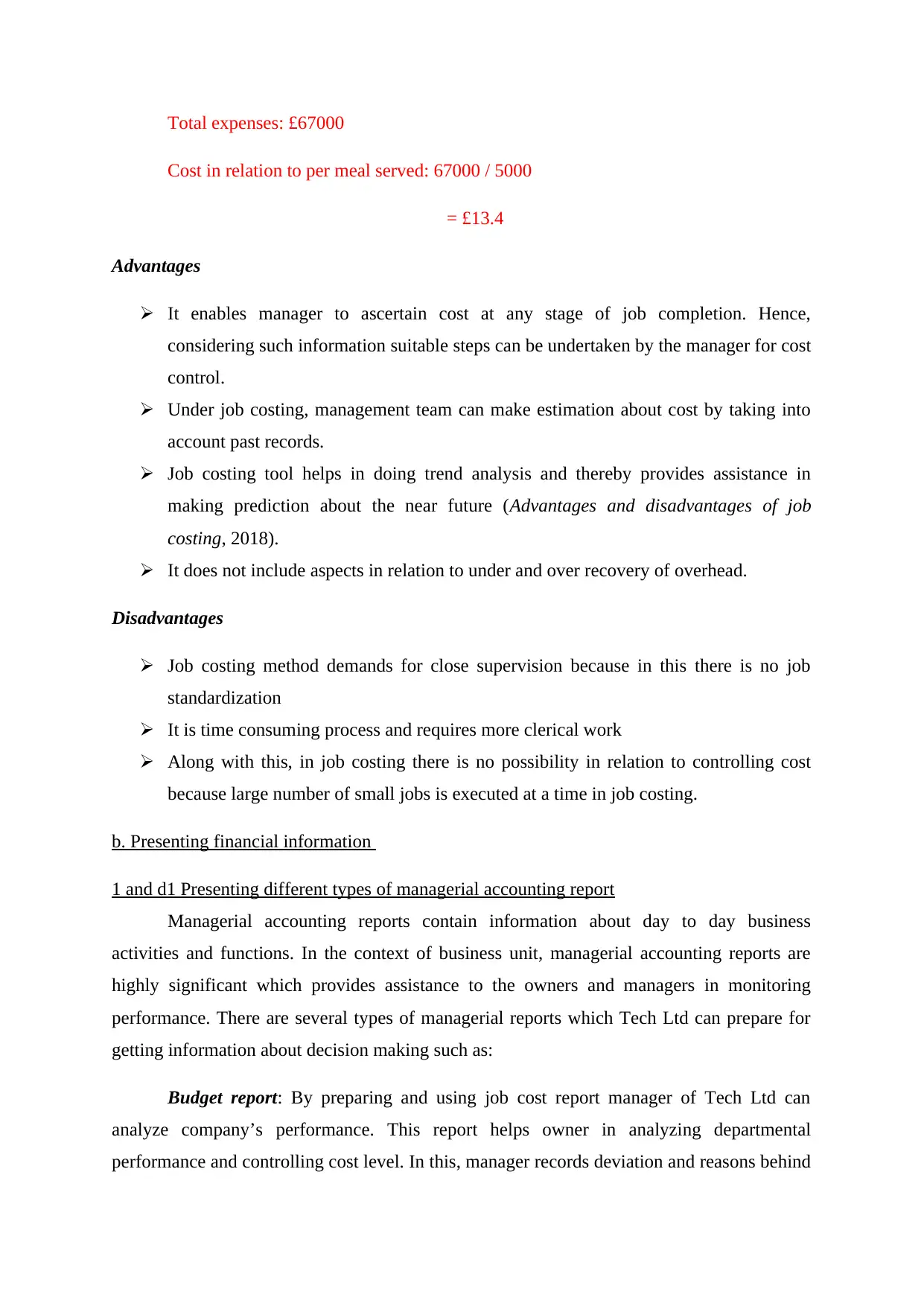

For example: In the context of hotel unit, which falls under the category of service

sector, per unit cost can be determined in the following manner:

Total number of meals: 5000

another to the significant level.

Service costing method is suitable for the companies which involve in the sector such

as hospitality, care homes etc.

For example: In the context of hotel unit, which falls under the category of service

sector, per unit cost can be determined in the following manner:

Total number of meals: 5000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total expenses: £67000

Cost in relation to per meal served: 67000 / 5000

= £13.4

Advantages

It enables manager to ascertain cost at any stage of job completion. Hence,

considering such information suitable steps can be undertaken by the manager for cost

control.

Under job costing, management team can make estimation about cost by taking into

account past records.

Job costing tool helps in doing trend analysis and thereby provides assistance in

making prediction about the near future (Advantages and disadvantages of job

costing, 2018).

It does not include aspects in relation to under and over recovery of overhead.

Disadvantages

Job costing method demands for close supervision because in this there is no job

standardization

It is time consuming process and requires more clerical work

Along with this, in job costing there is no possibility in relation to controlling cost

because large number of small jobs is executed at a time in job costing.

b. Presenting financial information

1 and d1 Presenting different types of managerial accounting report

Managerial accounting reports contain information about day to day business

activities and functions. In the context of business unit, managerial accounting reports are

highly significant which provides assistance to the owners and managers in monitoring

performance. There are several types of managerial reports which Tech Ltd can prepare for

getting information about decision making such as:

Budget report: By preparing and using job cost report manager of Tech Ltd can

analyze company’s performance. This report helps owner in analyzing departmental

performance and controlling cost level. In this, manager records deviation and reasons behind

Cost in relation to per meal served: 67000 / 5000

= £13.4

Advantages

It enables manager to ascertain cost at any stage of job completion. Hence,

considering such information suitable steps can be undertaken by the manager for cost

control.

Under job costing, management team can make estimation about cost by taking into

account past records.

Job costing tool helps in doing trend analysis and thereby provides assistance in

making prediction about the near future (Advantages and disadvantages of job

costing, 2018).

It does not include aspects in relation to under and over recovery of overhead.

Disadvantages

Job costing method demands for close supervision because in this there is no job

standardization

It is time consuming process and requires more clerical work

Along with this, in job costing there is no possibility in relation to controlling cost

because large number of small jobs is executed at a time in job costing.

b. Presenting financial information

1 and d1 Presenting different types of managerial accounting report

Managerial accounting reports contain information about day to day business

activities and functions. In the context of business unit, managerial accounting reports are

highly significant which provides assistance to the owners and managers in monitoring

performance. There are several types of managerial reports which Tech Ltd can prepare for

getting information about decision making such as:

Budget report: By preparing and using job cost report manager of Tech Ltd can

analyze company’s performance. This report helps owner in analyzing departmental

performance and controlling cost level. In this, manager records deviation and reasons behind

the occurrence of same by comparing actual financial figures with the budgeted aspects.

Hence, by taking into account such report owner of Tech Ltd can make appropriate

estimation about future expenses and thereby would become able to prepare competent

financial plan (Kaplan and Atkinson, 2015). Further, manager of Tech Ltd can also use

budget report for providing incentives to the employees.

Accounts receivable ageing: For the purpose of cash flow management, accounts

receivable ageing report is highly suitable. Receivable reports furnish information to the

company about the balances of customers by how long they have been owed. Through

undertaking such report owner of Tech Ltd can assess issues associated with the collection

process. For instance: If business unit finds that most of the customers are not in position to

pay due amount on time then focus needs to be placed on tightening policies.

Job cost report: It presents cost or expenses that are associated with specific projects.

For evaluating job profitability usually expenses are matched with revenue. Using this report,

firm can assess high earning areas of business unit and thereby become able to allocate

resources in an effectual way. In other words, job costing report helps in making efforts in the

right direction rather than wasting time in low profit margin areas. Hence, job cost report

offers opportunity to Tech Ltd in improving the areas of waste before cost escalation.

Inventory and manufacturing: Tech Ltd can make its manufacturing process more

efficient by taking into account in stock report. Moreover, this report serves information

about inventory wastage, per unit overhead cost etc. Hence, getting information about such

aspects manager can take suitable decision for improvement purpose (Wijaya and et.al.,

2015). Along with this, such report also gives indication whether company needs to take

suitable measure for controlling holding and ordering cost or not.

Hence, by taking into account all the above depicted aspects it can be presented that

managerial reports are highly prominent and aid in significant decision making.

2 and d1 Stating why information presented in managerial reports must be understandable

In the current times, company prepares managerial accounting reports more

frequently with an objective to take quality and appropriate decision which makes

contribution in the attainment of goals. In accordance with the aspects of managerial

accounting reporting, information must be reliable, comparable and need to be presented in a

Hence, by taking into account such report owner of Tech Ltd can make appropriate

estimation about future expenses and thereby would become able to prepare competent

financial plan (Kaplan and Atkinson, 2015). Further, manager of Tech Ltd can also use

budget report for providing incentives to the employees.

Accounts receivable ageing: For the purpose of cash flow management, accounts

receivable ageing report is highly suitable. Receivable reports furnish information to the

company about the balances of customers by how long they have been owed. Through

undertaking such report owner of Tech Ltd can assess issues associated with the collection

process. For instance: If business unit finds that most of the customers are not in position to

pay due amount on time then focus needs to be placed on tightening policies.

Job cost report: It presents cost or expenses that are associated with specific projects.

For evaluating job profitability usually expenses are matched with revenue. Using this report,

firm can assess high earning areas of business unit and thereby become able to allocate

resources in an effectual way. In other words, job costing report helps in making efforts in the

right direction rather than wasting time in low profit margin areas. Hence, job cost report

offers opportunity to Tech Ltd in improving the areas of waste before cost escalation.

Inventory and manufacturing: Tech Ltd can make its manufacturing process more

efficient by taking into account in stock report. Moreover, this report serves information

about inventory wastage, per unit overhead cost etc. Hence, getting information about such

aspects manager can take suitable decision for improvement purpose (Wijaya and et.al.,

2015). Along with this, such report also gives indication whether company needs to take

suitable measure for controlling holding and ordering cost or not.

Hence, by taking into account all the above depicted aspects it can be presented that

managerial reports are highly prominent and aid in significant decision making.

2 and d1 Stating why information presented in managerial reports must be understandable

In the current times, company prepares managerial accounting reports more

frequently with an objective to take quality and appropriate decision which makes

contribution in the attainment of goals. In accordance with the aspects of managerial

accounting reporting, information must be reliable, comparable and need to be presented in a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.