Qantas Airline Audit: Materiality Assessment and Audit Program Design

VerifiedAdded on 2023/06/07

|11

|2052

|349

Report

AI Summary

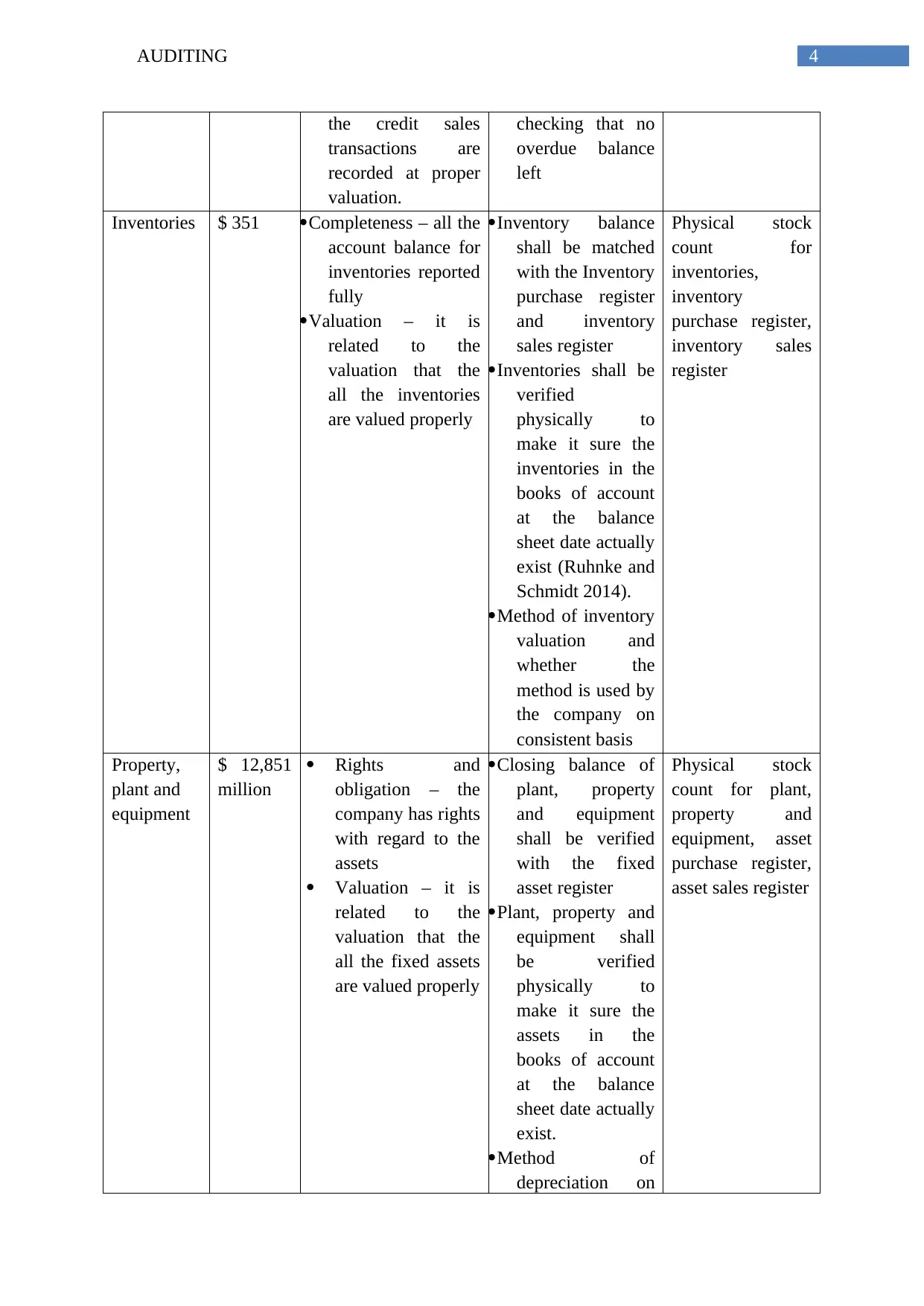

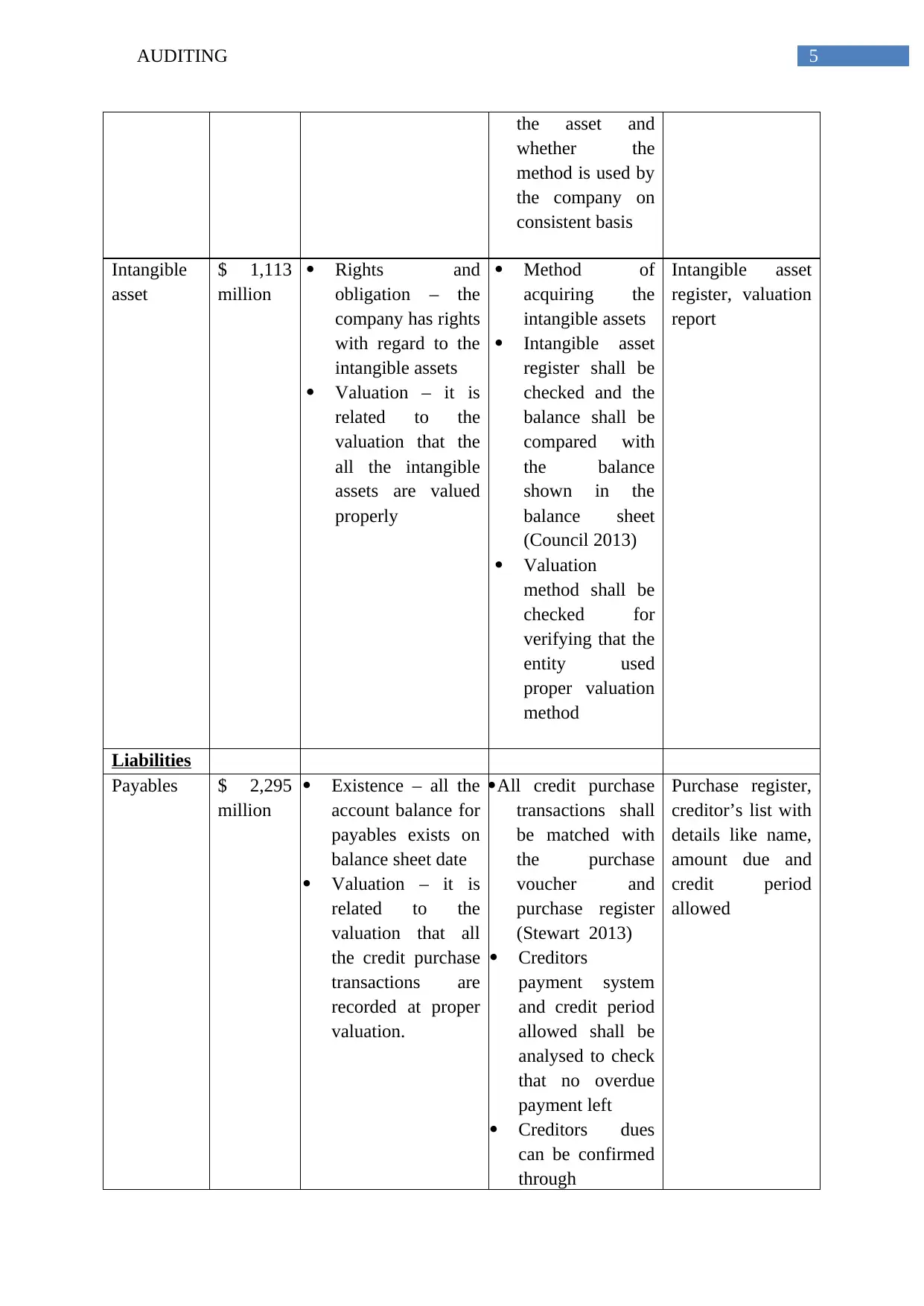

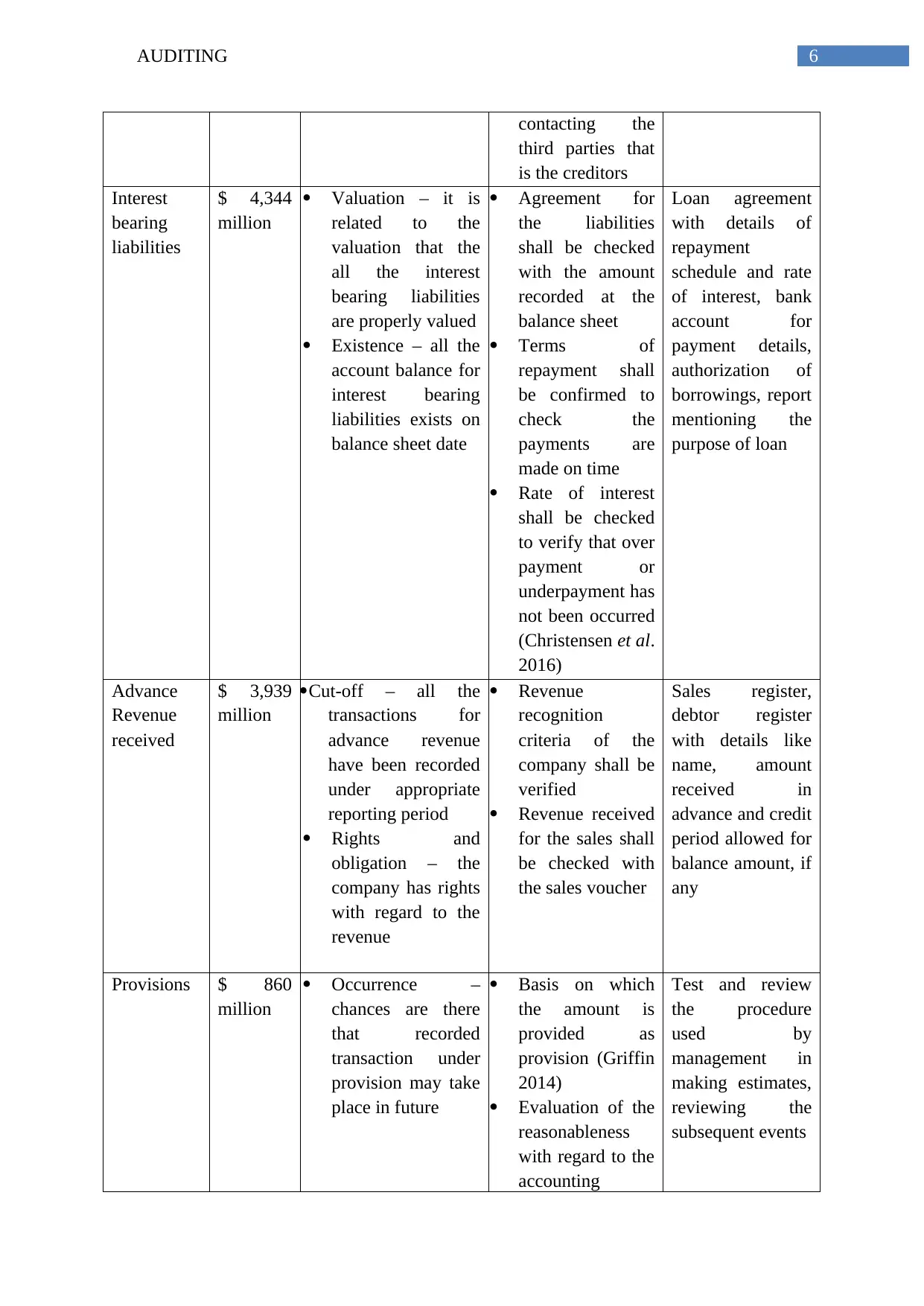

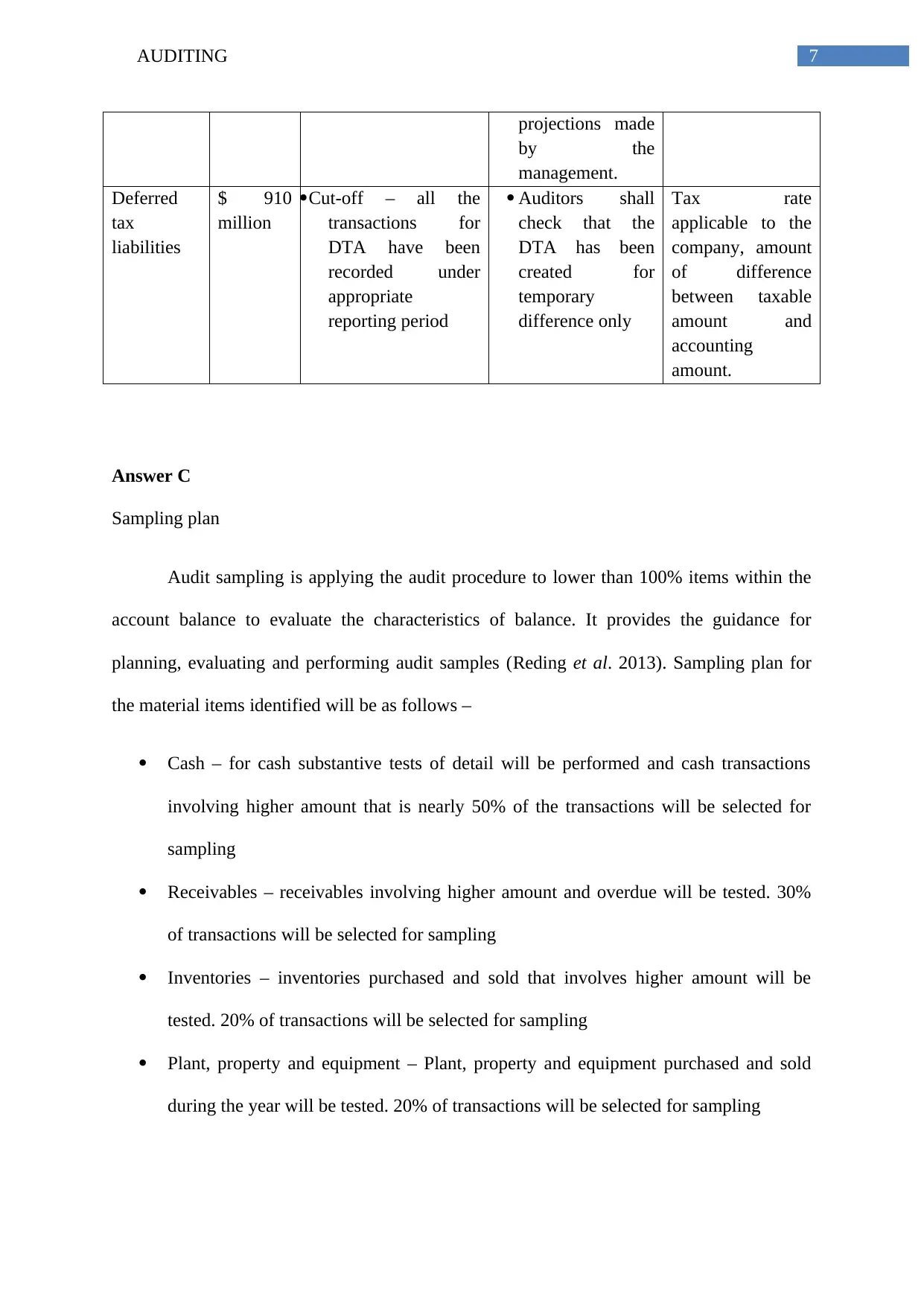

This report provides a detailed audit program for Qantas Airline, focusing on the assessment of materiality and the design of audit procedures. It identifies key account balances, including both assets (cash, receivables, inventories, property, plant, and equipment, and intangible assets) and liabilities (payables, interest-bearing liabilities, advanced revenue, provisions, and deferred tax liabilities), and discusses the relevant financial report assertions for each. The report outlines specific audit procedures to address these assertions, ensuring sufficient and appropriate audit evidence is collected. Additionally, it includes a sampling plan, detailing the use of sampling for each material account balance tested, specifying the percentage of items to be tested for each category. The materiality calculation is based on various benchmarks like sales revenue, total assets, net profit, and shareholder's equity, providing a comprehensive approach to auditing Qantas's financial statements. Desklib is your go-to platform for similar solved assignments and past papers.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.