Financial Resource Management and Analysis for Sweet Menu Restaurant

VerifiedAdded on 2020/01/28

|16

|5425

|200

Report

AI Summary

This report provides a comprehensive financial analysis of Sweet Menu Restaurant, focusing on its expansion plans and resource management. It begins by identifying available financial resources, including bank loans, capital markets, retained earnings, and franchising, while also considering short-term options like bank overdrafts and trade credit. The report delves into the legal, financial, and ownership implications of each financing source. It then evaluates the most appropriate sources for the restaurant's needs, considering both long-term and short-term options, including a bank loan and trade credit. The report analyzes the costs associated with different financing options, emphasizing the importance of financial planning within the business. It also assesses the information needs of decision-makers and the impact of finance on financial statements. Furthermore, the report includes a discussion on budgeting, unit cost calculations, pricing decisions, and investment appraisal techniques. Finally, it examines financial statements, compares financial formats used by different businesses, and provides a ratio analysis to evaluate the financial performance of Sweet Menu Restaurant.

MFRD

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................3

TASK 1.................................................................................................................................................3

1.1 Available source of finances to Sweet Menu restaurant............................................................3

2.2 Legal, Financial and ownership implication of the financial sources. ......................................4

1.3 Evaluation of the most appropriate sources for Sweet Menu restaurant...................................6

TASK 2.................................................................................................................................................6

2.1 Analysing cost of different sources of finances chosen by Sweet Menu restaurant..................6

2.2 Importance of financial planning within a business. ................................................................6

2.3 Assessment of information needs of decision makers...............................................................7

2.4 Impact of finance on the financial statements ..........................................................................8

TASK 3.................................................................................................................................................8

3.1 Analysing budget and recommending........................................................................................8

3.2 Calculation of the unit costs i.e. the meal cost and making pricing decisions.........................8

3.3 Assessing by Investment appraisal technique............................................................................9

TASK 4...............................................................................................................................................11

4.1 Discussion on the financial statements....................................................................................11

4.2 Comparison between financial formats used by different business.........................................12

4.3 Analysing Ratio........................................................................................................................12

CONCLUSION..................................................................................................................................13

REFERENCES...................................................................................................................................15

INTRODUCTION................................................................................................................................3

TASK 1.................................................................................................................................................3

1.1 Available source of finances to Sweet Menu restaurant............................................................3

2.2 Legal, Financial and ownership implication of the financial sources. ......................................4

1.3 Evaluation of the most appropriate sources for Sweet Menu restaurant...................................6

TASK 2.................................................................................................................................................6

2.1 Analysing cost of different sources of finances chosen by Sweet Menu restaurant..................6

2.2 Importance of financial planning within a business. ................................................................6

2.3 Assessment of information needs of decision makers...............................................................7

2.4 Impact of finance on the financial statements ..........................................................................8

TASK 3.................................................................................................................................................8

3.1 Analysing budget and recommending........................................................................................8

3.2 Calculation of the unit costs i.e. the meal cost and making pricing decisions.........................8

3.3 Assessing by Investment appraisal technique............................................................................9

TASK 4...............................................................................................................................................11

4.1 Discussion on the financial statements....................................................................................11

4.2 Comparison between financial formats used by different business.........................................12

4.3 Analysing Ratio........................................................................................................................12

CONCLUSION..................................................................................................................................13

REFERENCES...................................................................................................................................15

Index of Tables

Table 1: Unit Cost...............................................................................................................................10

Table 2: Proposal 1, Table 1................................................................................................................11

Table 3: Proposal 1, Table 2................................................................................................................11

Table 4: Proposal 2, Table 1...............................................................................................................12

Table 5: Proposal 2, Table 2...............................................................................................................12

Table 6: Ratio Analysis.......................................................................................................................14

Table 1: Unit Cost...............................................................................................................................10

Table 2: Proposal 1, Table 1................................................................................................................11

Table 3: Proposal 1, Table 2................................................................................................................11

Table 4: Proposal 2, Table 1...............................................................................................................12

Table 5: Proposal 2, Table 2...............................................................................................................12

Table 6: Ratio Analysis.......................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Managing financial resources is the method to procure and allocate financial resources after

a decision making process. Each business is required to conduct financial analysis to understand the

probability and risk attached to each financial decision. Business has to understand different types

of financial resources that are available to them (Barrett, 2007). Financial resource is the back bone

for every business. Thus, the financial manager is responsible to evaluate different sources of fund

resources available and then evaluate them as to which sources best fits business's requirements.

Thus, management of financial resources is interrelated to the decision making process. This is

because of the reason that right decision making ability of the manager can help to boost the

business whereas one wrong decision can hamper the financial growth of a business.

The report discusses about two restaurants and their financial decision. Sweet Menu

restaurant wants to expand its trade by opening two new locations in Central London and Croydon

(Bonham, 2008). In order to expand, the restaurant requires infusing €300,000 and €500,000

respectively. On the other hand, Blue Island restaurant owners want to conduct financial study of its

records. Both of the restaurants require making legitimate and viable decision to raise financial

resources and analyse business proposals.

TASK 1

1.1 Available source of finances to Sweet Menu restaurant

The available resources are those resources that are currently accessible to the business.

Financial manager is required to analyse these resources in order to select feasible resources for

Sweet Menu restaurant (Sources of finance, 2012). They to expand to two new locations located in

Central London and Croydon. In order to do that the available sources of finance are as followed:

Long term Sources- These are those resources which are available to be used after a year.

They are-

Bank Loan- Loan is the debt taken from a financial institute or a bank. They require

studying the strength of profit earned by the respective business. Banker asks for a guarantee

which is a security deposit in proportion to the loan amount (Chazi,2010).

Capital Market- This market refers to issue of new shares by a company. In this process, the

company is required to issue new shares to the public or investors. With the purchase of

share, the investors receive ownership right in the company as per the deed or the contract of

issue.

Retained Earnings- Each year i.e. annually or semi annually the business is required to save

an amount of money from the profits in the form of retained earnings. In simple terms,

retained earnings are the profit re-invested in a business activity by them (Benedict, and

Managing financial resources is the method to procure and allocate financial resources after

a decision making process. Each business is required to conduct financial analysis to understand the

probability and risk attached to each financial decision. Business has to understand different types

of financial resources that are available to them (Barrett, 2007). Financial resource is the back bone

for every business. Thus, the financial manager is responsible to evaluate different sources of fund

resources available and then evaluate them as to which sources best fits business's requirements.

Thus, management of financial resources is interrelated to the decision making process. This is

because of the reason that right decision making ability of the manager can help to boost the

business whereas one wrong decision can hamper the financial growth of a business.

The report discusses about two restaurants and their financial decision. Sweet Menu

restaurant wants to expand its trade by opening two new locations in Central London and Croydon

(Bonham, 2008). In order to expand, the restaurant requires infusing €300,000 and €500,000

respectively. On the other hand, Blue Island restaurant owners want to conduct financial study of its

records. Both of the restaurants require making legitimate and viable decision to raise financial

resources and analyse business proposals.

TASK 1

1.1 Available source of finances to Sweet Menu restaurant

The available resources are those resources that are currently accessible to the business.

Financial manager is required to analyse these resources in order to select feasible resources for

Sweet Menu restaurant (Sources of finance, 2012). They to expand to two new locations located in

Central London and Croydon. In order to do that the available sources of finance are as followed:

Long term Sources- These are those resources which are available to be used after a year.

They are-

Bank Loan- Loan is the debt taken from a financial institute or a bank. They require

studying the strength of profit earned by the respective business. Banker asks for a guarantee

which is a security deposit in proportion to the loan amount (Chazi,2010).

Capital Market- This market refers to issue of new shares by a company. In this process, the

company is required to issue new shares to the public or investors. With the purchase of

share, the investors receive ownership right in the company as per the deed or the contract of

issue.

Retained Earnings- Each year i.e. annually or semi annually the business is required to save

an amount of money from the profits in the form of retained earnings. In simple terms,

retained earnings are the profit re-invested in a business activity by them (Benedict, and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Elliott, 2008).

Franchising- In this method, the business pays the right to the franchisor to operate the

business. He/she is also entitled to bear establishment cost, marketing and day–to-day

expense of the business. This way the business is operated on the responsibility of the

franchisor (Davies and Drexler, 2010).

Short term sources- These sources are available to the business to be used within the

financial year. They are as follow:

Bank overdraft- It is a facility provided by the bank or a financial institution. The business

can withdraw or overdraft money in excess of the balance available in the current account of

the business (Benedict, and Elliott, 2008).

Trade credit- This is the purchasing of services or goods from a trader on credit basis.

Businesses that have goodwill in the market are provided with trade credit facility to pay the

amount after a period of 90 days.

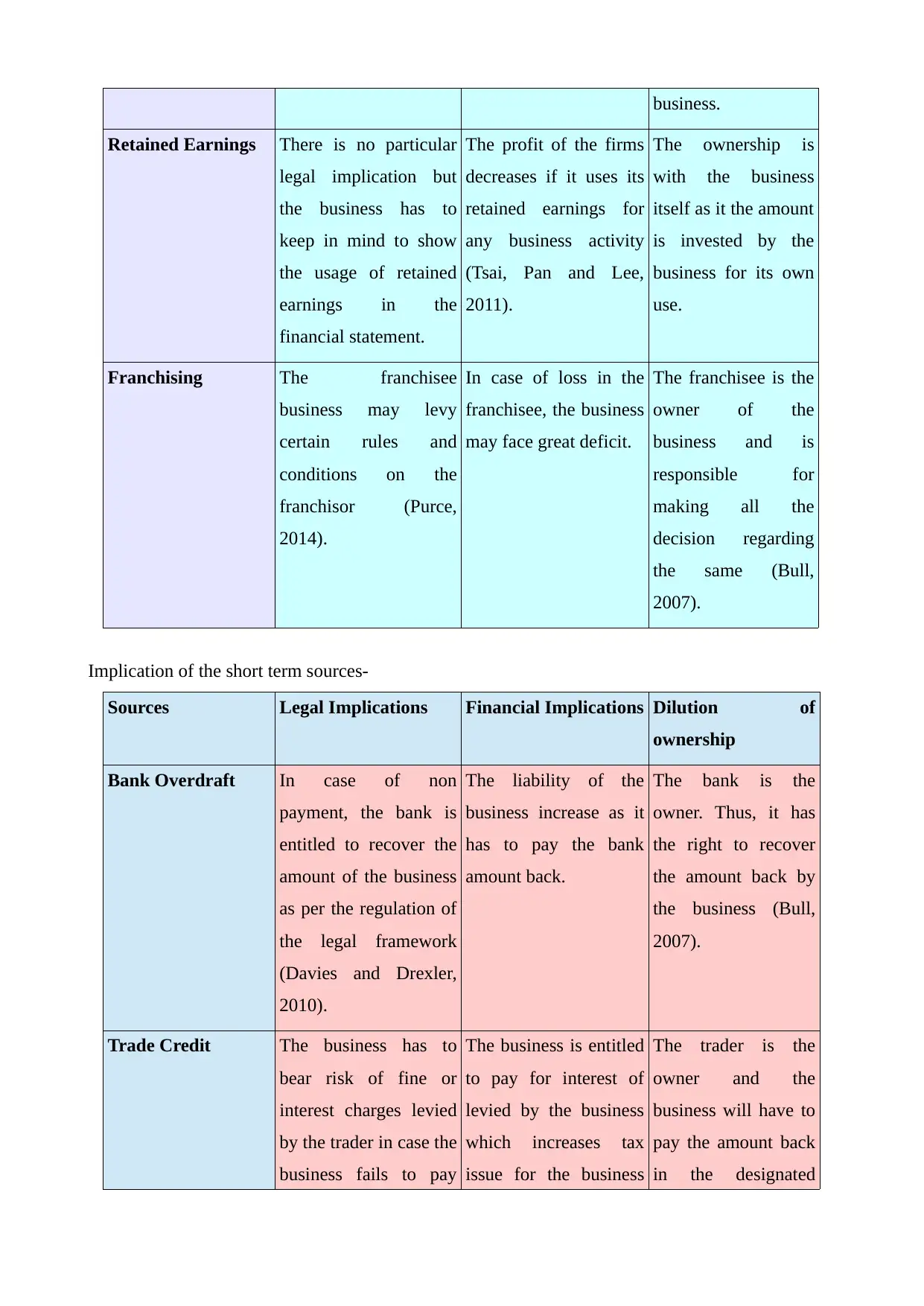

2.2 Legal, Financial and ownership implication of the financial sources.

Implication of the long terms sources-

Sources Legal Implications Financial Implications Dilution of

ownership

Bank loan In case of non payment

of loan, the bank or

financial institute have

the right to cease the

property of the

business to recover

their amount (Rasid,

Rahman and Ismail,

2011).

By raising a loan, the

business will have to be

sure to pay the interest

as well as the principal

amount.

The ownership

remains with the

bank until repayment

of the loan amount

(Siano,Kitchen and

Confetto, 2010).

Capital Market In case of business

becoming bankrupt, the

organisation has to pay

the amount to the

investor by selling of

capital assets.

The shareholders may

demand for a rise in the

dividends. Thus, the

retained earnings of the

business may reduce by

the same.

The ownership is

with the investors

who purchases shares

of the company.

They also have the

right in the decision

making of the

Franchising- In this method, the business pays the right to the franchisor to operate the

business. He/she is also entitled to bear establishment cost, marketing and day–to-day

expense of the business. This way the business is operated on the responsibility of the

franchisor (Davies and Drexler, 2010).

Short term sources- These sources are available to the business to be used within the

financial year. They are as follow:

Bank overdraft- It is a facility provided by the bank or a financial institution. The business

can withdraw or overdraft money in excess of the balance available in the current account of

the business (Benedict, and Elliott, 2008).

Trade credit- This is the purchasing of services or goods from a trader on credit basis.

Businesses that have goodwill in the market are provided with trade credit facility to pay the

amount after a period of 90 days.

2.2 Legal, Financial and ownership implication of the financial sources.

Implication of the long terms sources-

Sources Legal Implications Financial Implications Dilution of

ownership

Bank loan In case of non payment

of loan, the bank or

financial institute have

the right to cease the

property of the

business to recover

their amount (Rasid,

Rahman and Ismail,

2011).

By raising a loan, the

business will have to be

sure to pay the interest

as well as the principal

amount.

The ownership

remains with the

bank until repayment

of the loan amount

(Siano,Kitchen and

Confetto, 2010).

Capital Market In case of business

becoming bankrupt, the

organisation has to pay

the amount to the

investor by selling of

capital assets.

The shareholders may

demand for a rise in the

dividends. Thus, the

retained earnings of the

business may reduce by

the same.

The ownership is

with the investors

who purchases shares

of the company.

They also have the

right in the decision

making of the

business.

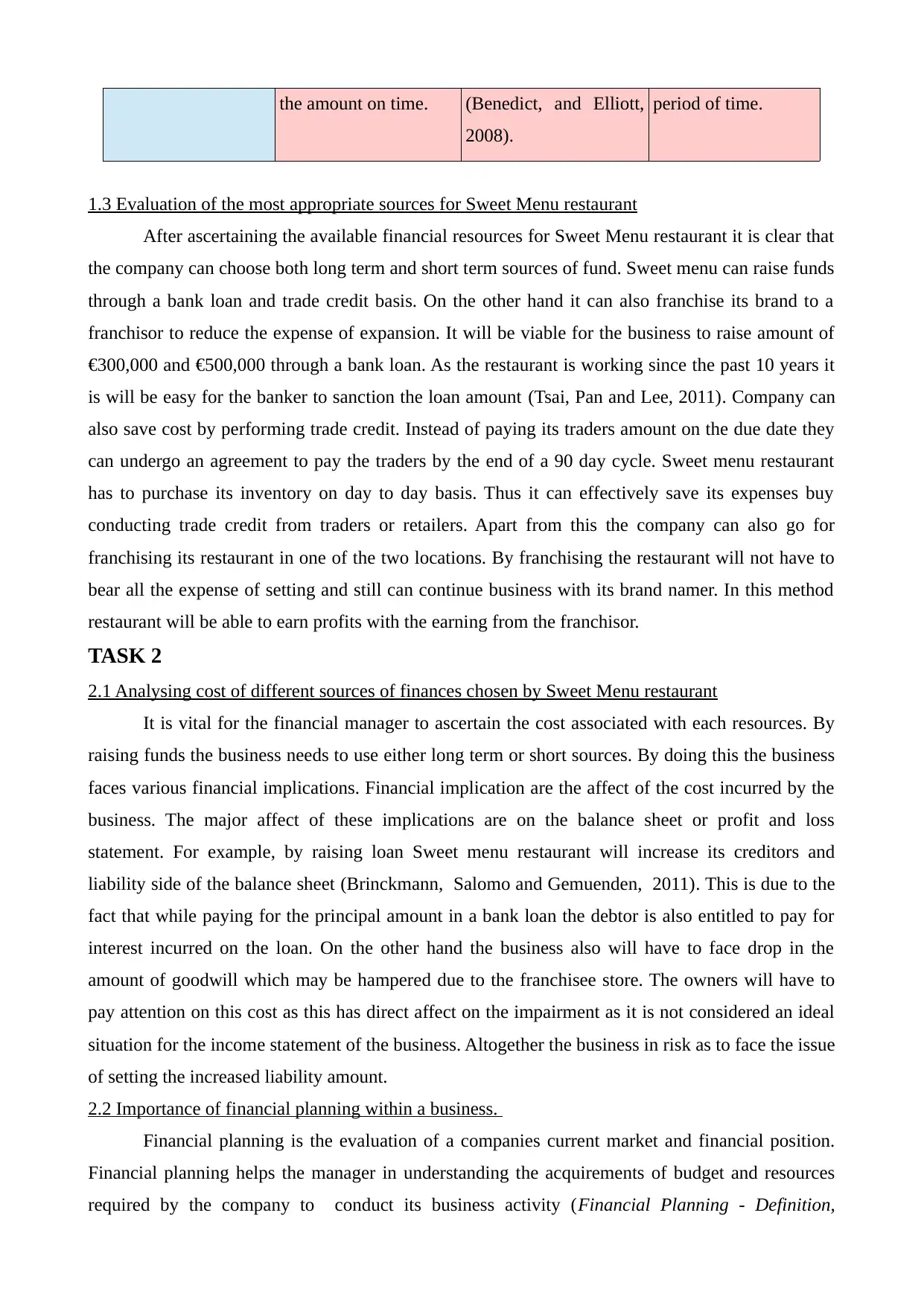

Retained Earnings There is no particular

legal implication but

the business has to

keep in mind to show

the usage of retained

earnings in the

financial statement.

The profit of the firms

decreases if it uses its

retained earnings for

any business activity

(Tsai, Pan and Lee,

2011).

The ownership is

with the business

itself as it the amount

is invested by the

business for its own

use.

Franchising The franchisee

business may levy

certain rules and

conditions on the

franchisor (Purce,

2014).

In case of loss in the

franchisee, the business

may face great deficit.

The franchisee is the

owner of the

business and is

responsible for

making all the

decision regarding

the same (Bull,

2007).

Implication of the short term sources-

Sources Legal Implications Financial Implications Dilution of

ownership

Bank Overdraft In case of non

payment, the bank is

entitled to recover the

amount of the business

as per the regulation of

the legal framework

(Davies and Drexler,

2010).

The liability of the

business increase as it

has to pay the bank

amount back.

The bank is the

owner. Thus, it has

the right to recover

the amount back by

the business (Bull,

2007).

Trade Credit The business has to

bear risk of fine or

interest charges levied

by the trader in case the

business fails to pay

The business is entitled

to pay for interest of

levied by the business

which increases tax

issue for the business

The trader is the

owner and the

business will have to

pay the amount back

in the designated

Retained Earnings There is no particular

legal implication but

the business has to

keep in mind to show

the usage of retained

earnings in the

financial statement.

The profit of the firms

decreases if it uses its

retained earnings for

any business activity

(Tsai, Pan and Lee,

2011).

The ownership is

with the business

itself as it the amount

is invested by the

business for its own

use.

Franchising The franchisee

business may levy

certain rules and

conditions on the

franchisor (Purce,

2014).

In case of loss in the

franchisee, the business

may face great deficit.

The franchisee is the

owner of the

business and is

responsible for

making all the

decision regarding

the same (Bull,

2007).

Implication of the short term sources-

Sources Legal Implications Financial Implications Dilution of

ownership

Bank Overdraft In case of non

payment, the bank is

entitled to recover the

amount of the business

as per the regulation of

the legal framework

(Davies and Drexler,

2010).

The liability of the

business increase as it

has to pay the bank

amount back.

The bank is the

owner. Thus, it has

the right to recover

the amount back by

the business (Bull,

2007).

Trade Credit The business has to

bear risk of fine or

interest charges levied

by the trader in case the

business fails to pay

The business is entitled

to pay for interest of

levied by the business

which increases tax

issue for the business

The trader is the

owner and the

business will have to

pay the amount back

in the designated

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the amount on time. (Benedict, and Elliott,

2008).

period of time.

1.3 Evaluation of the most appropriate sources for Sweet Menu restaurant

After ascertaining the available financial resources for Sweet Menu restaurant it is clear that

the company can choose both long term and short term sources of fund. Sweet menu can raise funds

through a bank loan and trade credit basis. On the other hand it can also franchise its brand to a

franchisor to reduce the expense of expansion. It will be viable for the business to raise amount of

€300,000 and €500,000 through a bank loan. As the restaurant is working since the past 10 years it

is will be easy for the banker to sanction the loan amount (Tsai, Pan and Lee, 2011). Company can

also save cost by performing trade credit. Instead of paying its traders amount on the due date they

can undergo an agreement to pay the traders by the end of a 90 day cycle. Sweet menu restaurant

has to purchase its inventory on day to day basis. Thus it can effectively save its expenses buy

conducting trade credit from traders or retailers. Apart from this the company can also go for

franchising its restaurant in one of the two locations. By franchising the restaurant will not have to

bear all the expense of setting and still can continue business with its brand namer. In this method

restaurant will be able to earn profits with the earning from the franchisor.

TASK 2

2.1 Analysing cost of different sources of finances chosen by Sweet Menu restaurant

It is vital for the financial manager to ascertain the cost associated with each resources. By

raising funds the business needs to use either long term or short sources. By doing this the business

faces various financial implications. Financial implication are the affect of the cost incurred by the

business. The major affect of these implications are on the balance sheet or profit and loss

statement. For example, by raising loan Sweet menu restaurant will increase its creditors and

liability side of the balance sheet (Brinckmann, Salomo and Gemuenden, 2011). This is due to the

fact that while paying for the principal amount in a bank loan the debtor is also entitled to pay for

interest incurred on the loan. On the other hand the business also will have to face drop in the

amount of goodwill which may be hampered due to the franchisee store. The owners will have to

pay attention on this cost as this has direct affect on the impairment as it is not considered an ideal

situation for the income statement of the business. Altogether the business in risk as to face the issue

of setting the increased liability amount.

2.2 Importance of financial planning within a business.

Financial planning is the evaluation of a companies current market and financial position.

Financial planning helps the manager in understanding the acquirements of budget and resources

required by the company to conduct its business activity (Financial Planning - Definition,

2008).

period of time.

1.3 Evaluation of the most appropriate sources for Sweet Menu restaurant

After ascertaining the available financial resources for Sweet Menu restaurant it is clear that

the company can choose both long term and short term sources of fund. Sweet menu can raise funds

through a bank loan and trade credit basis. On the other hand it can also franchise its brand to a

franchisor to reduce the expense of expansion. It will be viable for the business to raise amount of

€300,000 and €500,000 through a bank loan. As the restaurant is working since the past 10 years it

is will be easy for the banker to sanction the loan amount (Tsai, Pan and Lee, 2011). Company can

also save cost by performing trade credit. Instead of paying its traders amount on the due date they

can undergo an agreement to pay the traders by the end of a 90 day cycle. Sweet menu restaurant

has to purchase its inventory on day to day basis. Thus it can effectively save its expenses buy

conducting trade credit from traders or retailers. Apart from this the company can also go for

franchising its restaurant in one of the two locations. By franchising the restaurant will not have to

bear all the expense of setting and still can continue business with its brand namer. In this method

restaurant will be able to earn profits with the earning from the franchisor.

TASK 2

2.1 Analysing cost of different sources of finances chosen by Sweet Menu restaurant

It is vital for the financial manager to ascertain the cost associated with each resources. By

raising funds the business needs to use either long term or short sources. By doing this the business

faces various financial implications. Financial implication are the affect of the cost incurred by the

business. The major affect of these implications are on the balance sheet or profit and loss

statement. For example, by raising loan Sweet menu restaurant will increase its creditors and

liability side of the balance sheet (Brinckmann, Salomo and Gemuenden, 2011). This is due to the

fact that while paying for the principal amount in a bank loan the debtor is also entitled to pay for

interest incurred on the loan. On the other hand the business also will have to face drop in the

amount of goodwill which may be hampered due to the franchisee store. The owners will have to

pay attention on this cost as this has direct affect on the impairment as it is not considered an ideal

situation for the income statement of the business. Altogether the business in risk as to face the issue

of setting the increased liability amount.

2.2 Importance of financial planning within a business.

Financial planning is the evaluation of a companies current market and financial position.

Financial planning helps the manager in understanding the acquirements of budget and resources

required by the company to conduct its business activity (Financial Planning - Definition,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Objectives and Importance, 2016). With the help of planning the company can allocate financial

resources to various types of expenses that incur in the business. The importance of financial

planning is described as below-

Financial planning is an effective tool in identifying the flow of cash. The manager is able to

make a balance between outflow and inflow of cash in the organisation. This assists the

manager in maintaining the stability of the business activities (Lusardi and Mitchell, 2011).

By properly planning the financial requirements of the business. The manager can ensure

about the current availability of funds for the organisation. It can only be done by pre

planning and finding activities that may require financial help in the near future.

Allocation and procurement of resources can be evaluated with the help of financial

planning. The business can identify proper utilisation of its financial resource by the

employees through financial planning (Bonham, 2008).

Financial planning provides various tools and techniques to assist the business in making

right choices while investing. The business at many times is required to invest its money

internally as well as externally. By planning the manager can ascertain ass to where return in

investment will be higher.

Financial planning helps in making the right decision for the business. The manager is able

to effectively understand the financial position of the business by proper planning (Shaoul,

Stafford and Stapleton, 2010). This helps the business in achieving better results and

increase the performance of the activities.

2.3 Assessment of information needs of decision makers

Decision makers are this individual or parties who have a superior authority over the

decision making process of the company. Stakeholders like the employees, suppliers, customer's

and competitors are the major stakeholders. They are as followed.

Employee's- The employees or the staff working at the Sweet menu restaurant among the

key decision makers. They provide various suggestions and ideas to the management (Boyd,

Dyhr Ulrich and Hollensen, S2012). The brand image of the business depends on the

customer service employee's generate. The restaurant responsible to provide with the

financial information to the employees in order to motivate them and increase their loyalty

with the business.

Supplier's- The restaurant must maintain cordial relationship with the suppliers. They must

be given information regarding their payment on timely basis. It is important for the

business to make timely payments to them so as to maintain trust worthiness among the

suppliers like the itinerary items of Sweet menu.

Customer's- They are among the most important decision makers (Jara and Ebrero, Zapata,

resources to various types of expenses that incur in the business. The importance of financial

planning is described as below-

Financial planning is an effective tool in identifying the flow of cash. The manager is able to

make a balance between outflow and inflow of cash in the organisation. This assists the

manager in maintaining the stability of the business activities (Lusardi and Mitchell, 2011).

By properly planning the financial requirements of the business. The manager can ensure

about the current availability of funds for the organisation. It can only be done by pre

planning and finding activities that may require financial help in the near future.

Allocation and procurement of resources can be evaluated with the help of financial

planning. The business can identify proper utilisation of its financial resource by the

employees through financial planning (Bonham, 2008).

Financial planning provides various tools and techniques to assist the business in making

right choices while investing. The business at many times is required to invest its money

internally as well as externally. By planning the manager can ascertain ass to where return in

investment will be higher.

Financial planning helps in making the right decision for the business. The manager is able

to effectively understand the financial position of the business by proper planning (Shaoul,

Stafford and Stapleton, 2010). This helps the business in achieving better results and

increase the performance of the activities.

2.3 Assessment of information needs of decision makers

Decision makers are this individual or parties who have a superior authority over the

decision making process of the company. Stakeholders like the employees, suppliers, customer's

and competitors are the major stakeholders. They are as followed.

Employee's- The employees or the staff working at the Sweet menu restaurant among the

key decision makers. They provide various suggestions and ideas to the management (Boyd,

Dyhr Ulrich and Hollensen, S2012). The brand image of the business depends on the

customer service employee's generate. The restaurant responsible to provide with the

financial information to the employees in order to motivate them and increase their loyalty

with the business.

Supplier's- The restaurant must maintain cordial relationship with the suppliers. They must

be given information regarding their payment on timely basis. It is important for the

business to make timely payments to them so as to maintain trust worthiness among the

suppliers like the itinerary items of Sweet menu.

Customer's- They are among the most important decision makers (Jara and Ebrero, Zapata,

2011). The business must highlight in media about its goodwill and achievement and

financial information like profit earned by the restaurant. This way Sweet Menu can raise

customers interest and increase its customer support in two new locations.

Competitor's- They are the external factors that affect the decision making of the

restaurant. The management at Sweet menu restaurant is required to make alterations in its

pricing policies s per its competitors.

2.4 Impact of finance on the financial statements

Financial decision have an impact on the ability of the business to get finances for its

business activities. The finances accessible to Sweet menu restaurant also created an impact on the

financial statement of the business. In order to expand business to two new locations the business

requires to raise finances. This shows that the company has dis-balance in its capital structure as it

has to raise money through bank loan (Mayne and Zapico-Goni, 2007). The liability of the company

rises due to taking credit from the bank as well as the trader. The goodwill of the company also

hampers as it has to take credit from its suppliers and traders. It shows that the company is short in

finance and also this can destroy the cordial relationship with the traders of Sweet menu restaurant.

Due to high interest levied on the loan the profit of the company reduces. This is not considered as

an ideal for any business. The business brand image depletes due to low earning and profit. As the

restaurant is in liability to pat for the interest and creditors its balance sheet also looks disoriented.

TASK 3

3.1 Analysing budget and recommending

Budget analysis is to evaluate the budget generated by the financial manager of the

company. Budget analysis helps in identifying the loopholes faced by expenses and deficits in the

business. From the budget made by the accountant it is clear that the business is doing good while

making cash in sale. This shows that the business is not facing any issue through credit sales

(Nickel, Saldanha-da-Gama and Ziegler, 2012). On the other hand the expenses of the business are

more then the income earned by the business. This is evident that in the month of December

specifically business had to face greatest negative net balance. Apart from this each month

company is facing losses instead of making profits, the Blue Island restaurant needs to reduce its

expenses. It was observed that the restaurant has to expend money on furnitures and fittings which

is considered as a huge wastage of money. Despite of this company can purchase furniture made of

plastic which does not deplete and last longer. Apart from this the restaurant can also improve its

infrastructure by introducing more natural light in the restaurant. This will help in reducing the

expense incurred on the lighting bills. From the trade payables statement it is clear that the company

can reduce cost on purchasing inventory from its suppliers (Davies and Drexler, 2010). The

company can find new wholesaler who provide quality product in a lower cost in comparison to the

financial information like profit earned by the restaurant. This way Sweet Menu can raise

customers interest and increase its customer support in two new locations.

Competitor's- They are the external factors that affect the decision making of the

restaurant. The management at Sweet menu restaurant is required to make alterations in its

pricing policies s per its competitors.

2.4 Impact of finance on the financial statements

Financial decision have an impact on the ability of the business to get finances for its

business activities. The finances accessible to Sweet menu restaurant also created an impact on the

financial statement of the business. In order to expand business to two new locations the business

requires to raise finances. This shows that the company has dis-balance in its capital structure as it

has to raise money through bank loan (Mayne and Zapico-Goni, 2007). The liability of the company

rises due to taking credit from the bank as well as the trader. The goodwill of the company also

hampers as it has to take credit from its suppliers and traders. It shows that the company is short in

finance and also this can destroy the cordial relationship with the traders of Sweet menu restaurant.

Due to high interest levied on the loan the profit of the company reduces. This is not considered as

an ideal for any business. The business brand image depletes due to low earning and profit. As the

restaurant is in liability to pat for the interest and creditors its balance sheet also looks disoriented.

TASK 3

3.1 Analysing budget and recommending

Budget analysis is to evaluate the budget generated by the financial manager of the

company. Budget analysis helps in identifying the loopholes faced by expenses and deficits in the

business. From the budget made by the accountant it is clear that the business is doing good while

making cash in sale. This shows that the business is not facing any issue through credit sales

(Nickel, Saldanha-da-Gama and Ziegler, 2012). On the other hand the expenses of the business are

more then the income earned by the business. This is evident that in the month of December

specifically business had to face greatest negative net balance. Apart from this each month

company is facing losses instead of making profits, the Blue Island restaurant needs to reduce its

expenses. It was observed that the restaurant has to expend money on furnitures and fittings which

is considered as a huge wastage of money. Despite of this company can purchase furniture made of

plastic which does not deplete and last longer. Apart from this the restaurant can also improve its

infrastructure by introducing more natural light in the restaurant. This will help in reducing the

expense incurred on the lighting bills. From the trade payables statement it is clear that the company

can reduce cost on purchasing inventory from its suppliers (Davies and Drexler, 2010). The

company can find new wholesaler who provide quality product in a lower cost in comparison to the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

other suppliers.

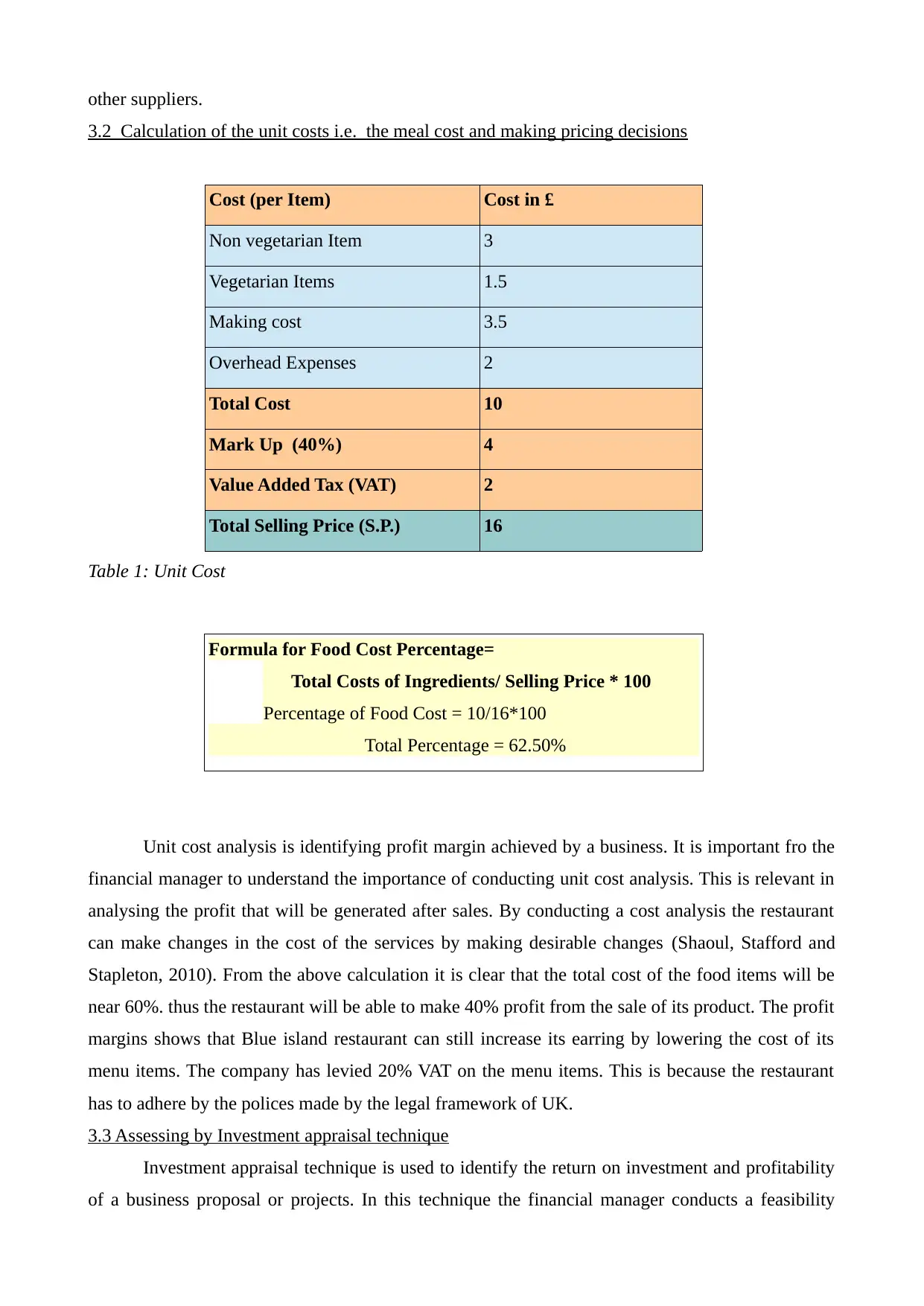

3.2 Calculation of the unit costs i.e. the meal cost and making pricing decisions

Cost (per Item) Cost in £

Non vegetarian Item 3

Vegetarian Items 1.5

Making cost 3.5

Overhead Expenses 2

Total Cost 10

Mark Up (40%) 4

Value Added Tax (VAT) 2

Total Selling Price (S.P.) 16

Table 1: Unit Cost

Formula for Food Cost Percentage=

Total Costs of Ingredients/ Selling Price * 100

Percentage of Food Cost = 10/16*100

Total Percentage = 62.50%

Unit cost analysis is identifying profit margin achieved by a business. It is important fro the

financial manager to understand the importance of conducting unit cost analysis. This is relevant in

analysing the profit that will be generated after sales. By conducting a cost analysis the restaurant

can make changes in the cost of the services by making desirable changes (Shaoul, Stafford and

Stapleton, 2010). From the above calculation it is clear that the total cost of the food items will be

near 60%. thus the restaurant will be able to make 40% profit from the sale of its product. The profit

margins shows that Blue island restaurant can still increase its earring by lowering the cost of its

menu items. The company has levied 20% VAT on the menu items. This is because the restaurant

has to adhere by the polices made by the legal framework of UK.

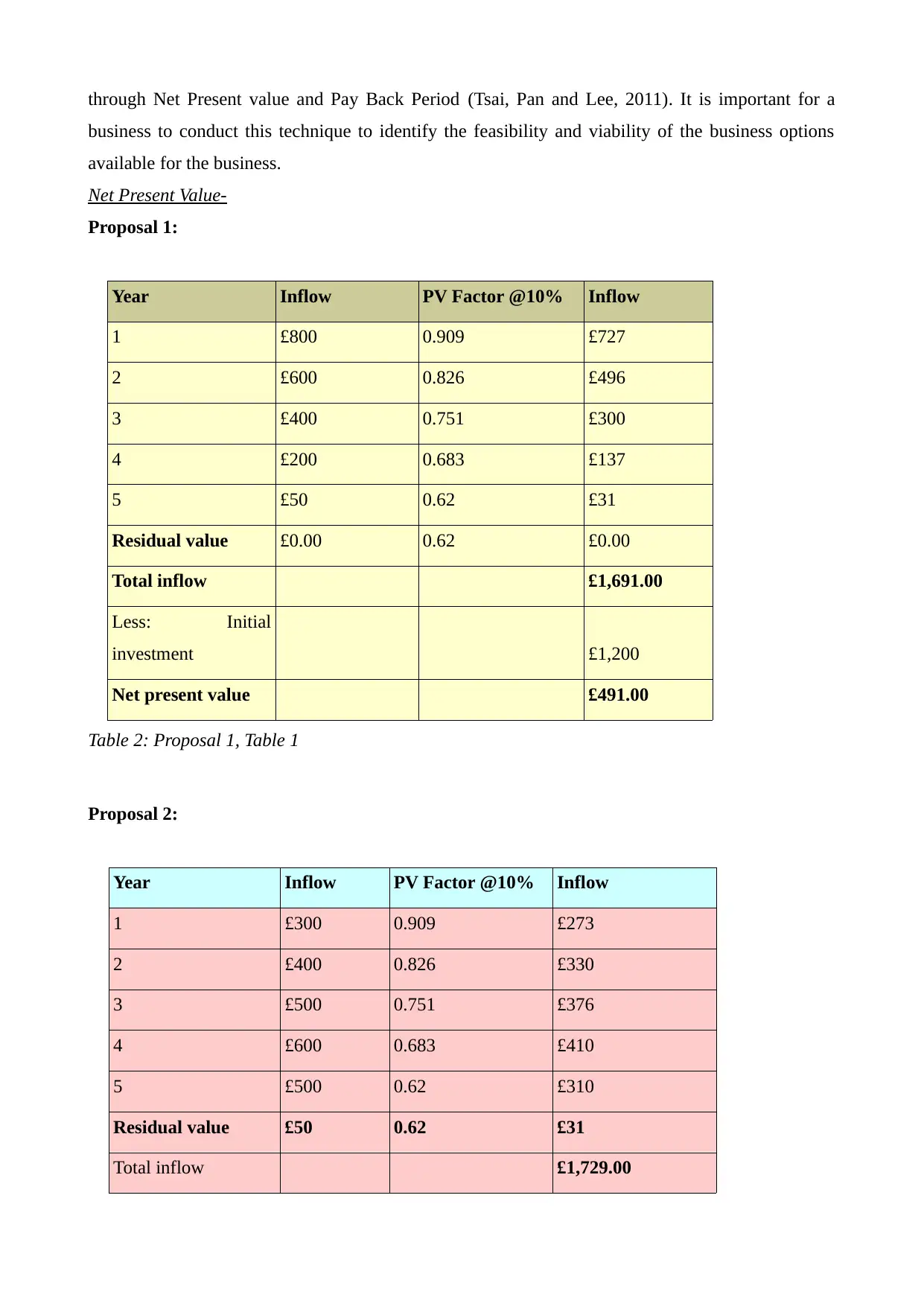

3.3 Assessing by Investment appraisal technique

Investment appraisal technique is used to identify the return on investment and profitability

of a business proposal or projects. In this technique the financial manager conducts a feasibility

3.2 Calculation of the unit costs i.e. the meal cost and making pricing decisions

Cost (per Item) Cost in £

Non vegetarian Item 3

Vegetarian Items 1.5

Making cost 3.5

Overhead Expenses 2

Total Cost 10

Mark Up (40%) 4

Value Added Tax (VAT) 2

Total Selling Price (S.P.) 16

Table 1: Unit Cost

Formula for Food Cost Percentage=

Total Costs of Ingredients/ Selling Price * 100

Percentage of Food Cost = 10/16*100

Total Percentage = 62.50%

Unit cost analysis is identifying profit margin achieved by a business. It is important fro the

financial manager to understand the importance of conducting unit cost analysis. This is relevant in

analysing the profit that will be generated after sales. By conducting a cost analysis the restaurant

can make changes in the cost of the services by making desirable changes (Shaoul, Stafford and

Stapleton, 2010). From the above calculation it is clear that the total cost of the food items will be

near 60%. thus the restaurant will be able to make 40% profit from the sale of its product. The profit

margins shows that Blue island restaurant can still increase its earring by lowering the cost of its

menu items. The company has levied 20% VAT on the menu items. This is because the restaurant

has to adhere by the polices made by the legal framework of UK.

3.3 Assessing by Investment appraisal technique

Investment appraisal technique is used to identify the return on investment and profitability

of a business proposal or projects. In this technique the financial manager conducts a feasibility

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

through Net Present value and Pay Back Period (Tsai, Pan and Lee, 2011). It is important for a

business to conduct this technique to identify the feasibility and viability of the business options

available for the business.

Net Present Value-

Proposal 1:

Year Inflow PV Factor @10% Inflow

1 £800 0.909 £727

2 £600 0.826 £496

3 £400 0.751 £300

4 £200 0.683 £137

5 £50 0.62 £31

Residual value £0.00 0.62 £0.00

Total inflow £1,691.00

Less: Initial

investment £1,200

Net present value £491.00

Table 2: Proposal 1, Table 1

Proposal 2:

Year Inflow PV Factor @10% Inflow

1 £300 0.909 £273

2 £400 0.826 £330

3 £500 0.751 £376

4 £600 0.683 £410

5 £500 0.62 £310

Residual value £50 0.62 £31

Total inflow £1,729.00

business to conduct this technique to identify the feasibility and viability of the business options

available for the business.

Net Present Value-

Proposal 1:

Year Inflow PV Factor @10% Inflow

1 £800 0.909 £727

2 £600 0.826 £496

3 £400 0.751 £300

4 £200 0.683 £137

5 £50 0.62 £31

Residual value £0.00 0.62 £0.00

Total inflow £1,691.00

Less: Initial

investment £1,200

Net present value £491.00

Table 2: Proposal 1, Table 1

Proposal 2:

Year Inflow PV Factor @10% Inflow

1 £300 0.909 £273

2 £400 0.826 £330

3 £500 0.751 £376

4 £600 0.683 £410

5 £500 0.62 £310

Residual value £50 0.62 £31

Total inflow £1,729.00

Less: Initial

investment £1,200

Net present value £529.00

Table 3: Proposal 1, Table 2

From the above calculation it is evident that project 2 has a higher NPV as compared to

project 1. Net Present value or NPV is the difference between the cash inflow and cash outflow.

This is done to ascertain the profitability of a project (Purce, 2014). Thus it can be said that project

2 will yield more earnings to the business then project 1.

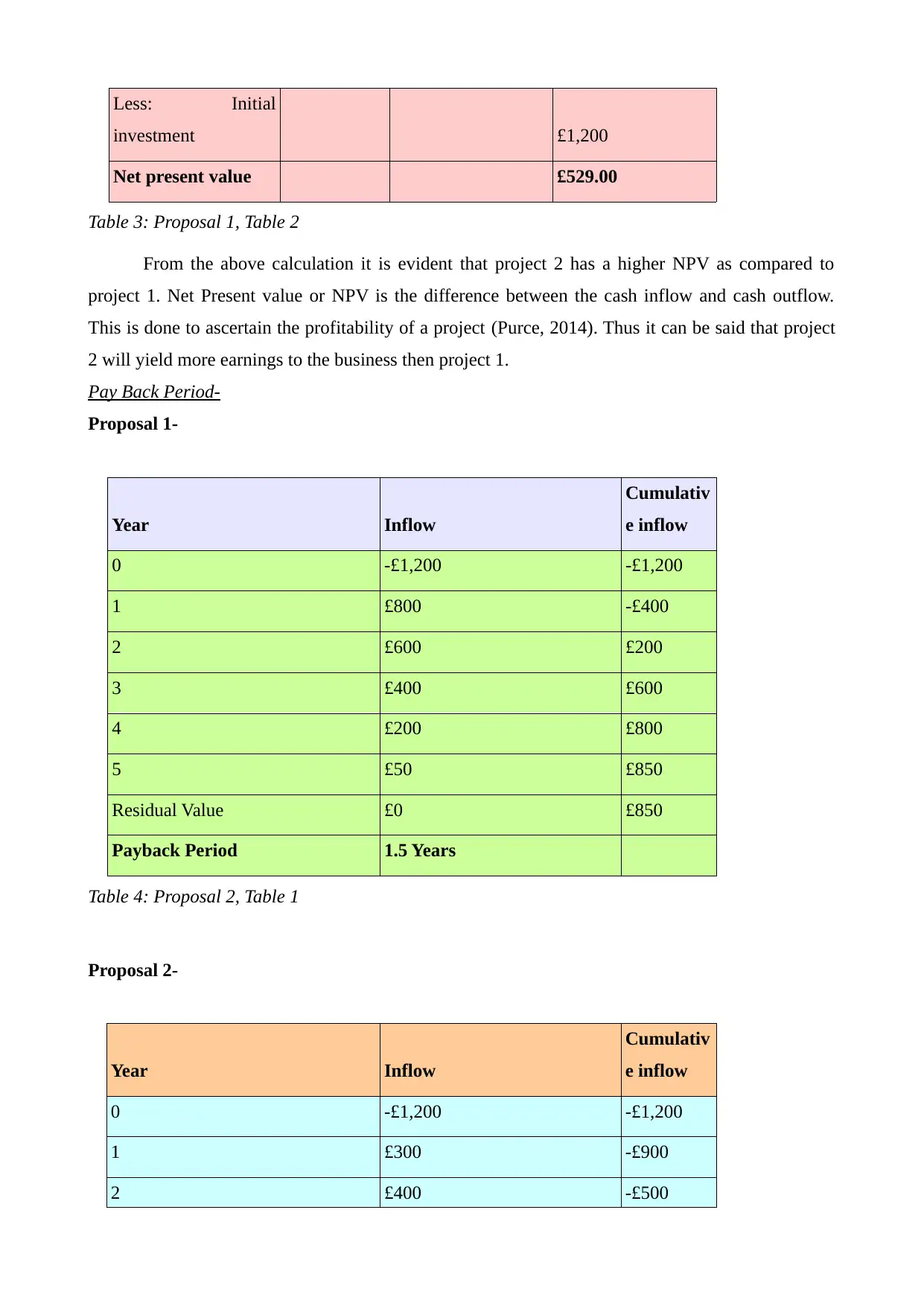

Pay Back Period-

Proposal 1-

Year Inflow

Cumulativ

e inflow

0 -£1,200 -£1,200

1 £800 -£400

2 £600 £200

3 £400 £600

4 £200 £800

5 £50 £850

Residual Value £0 £850

Payback Period 1.5 Years

Table 4: Proposal 2, Table 1

Proposal 2-

Year Inflow

Cumulativ

e inflow

0 -£1,200 -£1,200

1 £300 -£900

2 £400 -£500

investment £1,200

Net present value £529.00

Table 3: Proposal 1, Table 2

From the above calculation it is evident that project 2 has a higher NPV as compared to

project 1. Net Present value or NPV is the difference between the cash inflow and cash outflow.

This is done to ascertain the profitability of a project (Purce, 2014). Thus it can be said that project

2 will yield more earnings to the business then project 1.

Pay Back Period-

Proposal 1-

Year Inflow

Cumulativ

e inflow

0 -£1,200 -£1,200

1 £800 -£400

2 £600 £200

3 £400 £600

4 £200 £800

5 £50 £850

Residual Value £0 £850

Payback Period 1.5 Years

Table 4: Proposal 2, Table 1

Proposal 2-

Year Inflow

Cumulativ

e inflow

0 -£1,200 -£1,200

1 £300 -£900

2 £400 -£500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.