Taxation Law Assignment: Assessing Taxable Income and Deductions

VerifiedAdded on 2020/03/01

|15

|2805

|11

Homework Assignment

AI Summary

This taxation law assignment addresses key concepts in Australian tax law, specifically focusing on assessable income, allowable deductions, and the determination of taxable income. The assignment begins with a series of short-answer questions exploring various tax scenarios related to employee expenses, assessable income, and deductible expenses, referencing relevant sections of the ITAA97. The core of the assignment involves calculating the taxable income of an individual named Manpreet, considering his salary, foreign-sourced income, and various deductions, including computer and printer expenses and new mobile for work purposes. The analysis delves into the residency status of Manpreet, clarifying the implications of his enrollment in a course at an Australian institution and part-time employment. Furthermore, the assignment meticulously examines the deductibility of self-education expenses, referencing relevant tax rulings and case law to determine whether Manpreet can claim a deduction for his educational expenses. The assignment also addresses the tax implications of Manpreet's income and expenses, providing a detailed breakdown of his tax liability, including calculations for tax payable, Medicare levy, and low-income tax offset. The assignment provides a comprehensive overview of Australian taxation law, including assessable income, deductible expenses, and taxable income for an Australian resident.

Running head: TAXATION LAW

Taxation

Name of the Student

Name of the University

Authors Note

Course ID

Taxation

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to I:................................................................................................................................2

Answer to II:..............................................................................................................................2

Answer to III:.............................................................................................................................2

Answer to IV:.............................................................................................................................2

Answer to V:..............................................................................................................................2

Answer to VI:.............................................................................................................................3

Answer VII:................................................................................................................................3

Answer to VIII:..........................................................................................................................3

Answer to IX:.............................................................................................................................3

Answer to X:..............................................................................................................................3

Answer to question 2:.................................................................................................................4

Reference List:.........................................................................................................................13

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to I:................................................................................................................................2

Answer to II:..............................................................................................................................2

Answer to III:.............................................................................................................................2

Answer to IV:.............................................................................................................................2

Answer to V:..............................................................................................................................2

Answer to VI:.............................................................................................................................3

Answer VII:................................................................................................................................3

Answer to VIII:..........................................................................................................................3

Answer to IX:.............................................................................................................................3

Answer to X:..............................................................................................................................3

Answer to question 2:.................................................................................................................4

Reference List:.........................................................................................................................13

2TAXATION LAW

Answer to question 1:

Answer to I:

The employer can claim deductions for the expenses incur when travelling for business or

paying for employee travel1.

Answer to II:

If the damages were paid for something pertaining to income according to ordinary concepts,

s6-5 of the ITAA97 will apply. Such payments are considered as tax-free.

Answer to III:

Fully assessable to the employee with no deduction allowable even though an allowance is

received.

Answer to IV:

Non-Assessable

Answer to V:

No. The prize is not ordinary or statutory income and therefore is not assessable income

under either section 6-5 or section 6-10 of the ITAA 1997. Rather, it is a non assessable

windfall gain2.

1 Barkoczy, Stephen, et al. Foundations Student Tax Pack 3 2016. Oxford University Press

Australia & New Zealand, 2016.

2 Berg, Chris, and Sinclair Davidson. "Submission to the House of Representatives Standing

Committee on Tax and Revenue Inquiry into the External Scrutiny of the Australian Taxation

Answer to question 1:

Answer to I:

The employer can claim deductions for the expenses incur when travelling for business or

paying for employee travel1.

Answer to II:

If the damages were paid for something pertaining to income according to ordinary concepts,

s6-5 of the ITAA97 will apply. Such payments are considered as tax-free.

Answer to III:

Fully assessable to the employee with no deduction allowable even though an allowance is

received.

Answer to IV:

Non-Assessable

Answer to V:

No. The prize is not ordinary or statutory income and therefore is not assessable income

under either section 6-5 or section 6-10 of the ITAA 1997. Rather, it is a non assessable

windfall gain2.

1 Barkoczy, Stephen, et al. Foundations Student Tax Pack 3 2016. Oxford University Press

Australia & New Zealand, 2016.

2 Berg, Chris, and Sinclair Davidson. "Submission to the House of Representatives Standing

Committee on Tax and Revenue Inquiry into the External Scrutiny of the Australian Taxation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Answer to VI:

Non-Assessable: A deduction is allowable for self-education expenses if the education is

directly relevant to the taxpayer's current income-earning activities.

Answer VII:

A deduction is allowable for the cost of buying, hiring or replacing clothing, uniforms under

the taxation Ruling IT 2641.

Answer to VIII:

Non-Assessable: A deduction is allowable if the education is likely to lead to an increase in

the factory worker's income from his or her current income-earning activities.

Answer to IX:

Assessable: Trips between home and work are generally considered private travel.

Answer to X:

Deductible: A person can claim deductions in some circumstances, as well as for some travel

between two workplaces.

Answer to question 2:

Computation of Assessable income

Office." (2016).

Answer to VI:

Non-Assessable: A deduction is allowable for self-education expenses if the education is

directly relevant to the taxpayer's current income-earning activities.

Answer VII:

A deduction is allowable for the cost of buying, hiring or replacing clothing, uniforms under

the taxation Ruling IT 2641.

Answer to VIII:

Non-Assessable: A deduction is allowable if the education is likely to lead to an increase in

the factory worker's income from his or her current income-earning activities.

Answer to IX:

Assessable: Trips between home and work are generally considered private travel.

Answer to X:

Deductible: A person can claim deductions in some circumstances, as well as for some travel

between two workplaces.

Answer to question 2:

Computation of Assessable income

Office." (2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

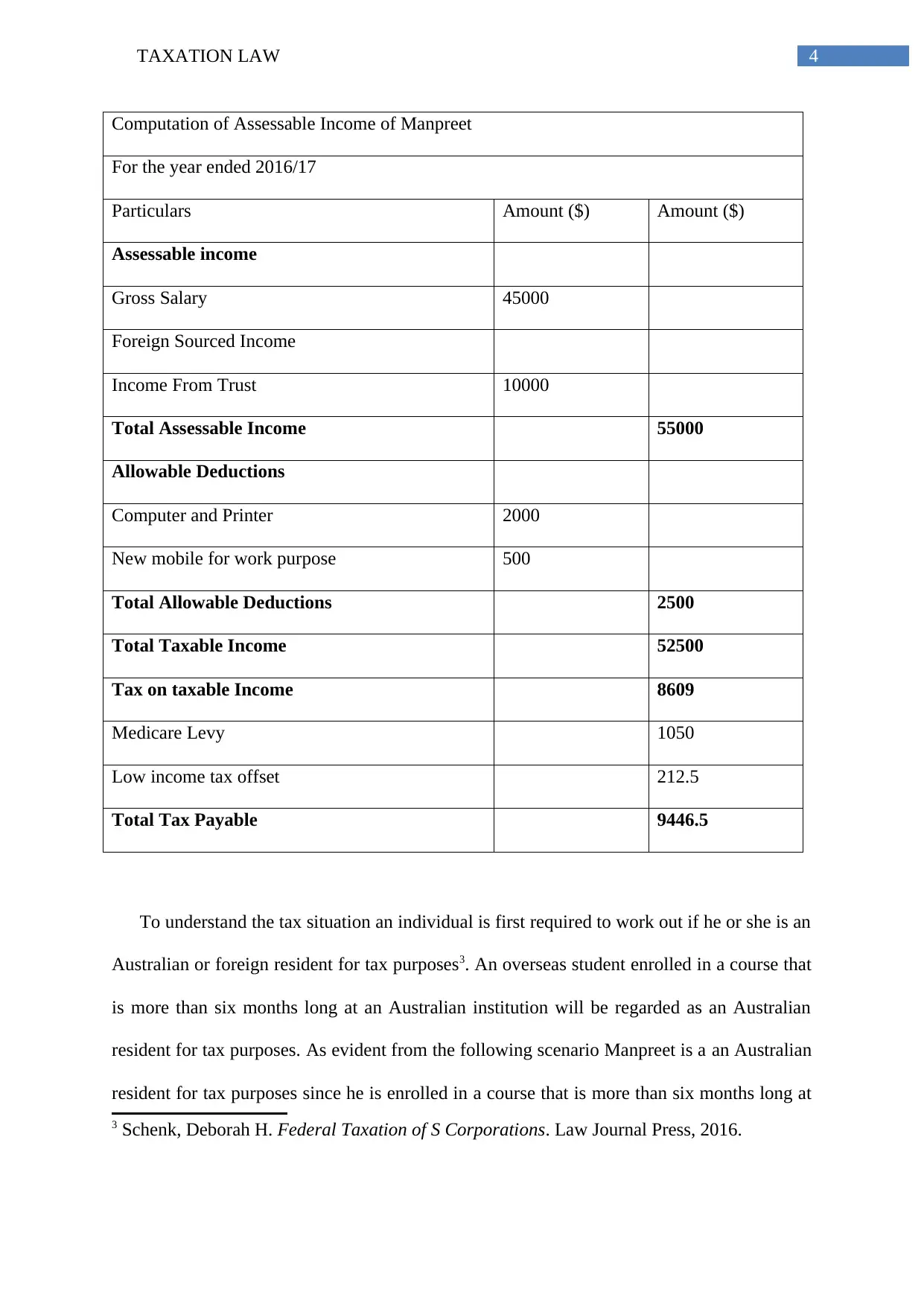

Computation of Assessable Income of Manpreet

For the year ended 2016/17

Particulars Amount ($) Amount ($)

Assessable income

Gross Salary 45000

Foreign Sourced Income

Income From Trust 10000

Total Assessable Income 55000

Allowable Deductions

Computer and Printer 2000

New mobile for work purpose 500

Total Allowable Deductions 2500

Total Taxable Income 52500

Tax on taxable Income 8609

Medicare Levy 1050

Low income tax offset 212.5

Total Tax Payable 9446.5

To understand the tax situation an individual is first required to work out if he or she is an

Australian or foreign resident for tax purposes3. An overseas student enrolled in a course that

is more than six months long at an Australian institution will be regarded as an Australian

resident for tax purposes. As evident from the following scenario Manpreet is a an Australian

resident for tax purposes since he is enrolled in a course that is more than six months long at

3 Schenk, Deborah H. Federal Taxation of S Corporations. Law Journal Press, 2016.

Computation of Assessable Income of Manpreet

For the year ended 2016/17

Particulars Amount ($) Amount ($)

Assessable income

Gross Salary 45000

Foreign Sourced Income

Income From Trust 10000

Total Assessable Income 55000

Allowable Deductions

Computer and Printer 2000

New mobile for work purpose 500

Total Allowable Deductions 2500

Total Taxable Income 52500

Tax on taxable Income 8609

Medicare Levy 1050

Low income tax offset 212.5

Total Tax Payable 9446.5

To understand the tax situation an individual is first required to work out if he or she is an

Australian or foreign resident for tax purposes3. An overseas student enrolled in a course that

is more than six months long at an Australian institution will be regarded as an Australian

resident for tax purposes. As evident from the following scenario Manpreet is a an Australian

resident for tax purposes since he is enrolled in a course that is more than six months long at

3 Schenk, Deborah H. Federal Taxation of S Corporations. Law Journal Press, 2016.

5TAXATION LAW

an Australian institution4. Furthermore, Manpreet also works as as the part time in Australia

with an Australian firm. However, Manpreet incurs several educational expenses which shall

be considered taxable. As evident Manpreet incurs a self-education expenses of $18,000 for

which he cannot claim deductions. An individual may be able to claim a deduction for self-

education expenses if your study is work-related or if you receive a taxable bonded

scholarship. It is noteworthy to denote that the course must have a sufficient connection to

your current employment and:

maintain or improve the specific skills or knowledge a person require in their current

employment, or

result in, or is likely to result in, an increase in their income from your current

employment.

A person cannot claim a deduction for self-education expenses for a course that does not

have a sufficient connection to their current employment even though it:

Might be generally related to it, or

Enables a person to get new employment.

Manpreet has incurred also incurred expenses such as $2,000 on computer and printer for

the purpose of educational purpose. There he can claim the deductions for the expenses that

are incurred for self-educations.

As a general rule Expenditure is deductible under section 8-1 of the ITAA 1997 where

there is a sufficient connection between the expense and the income earning activities, such

4 Bankman, Joseph, et al. Federal Income Taxation. Wolters Kluwer Law & Business, 2017.

an Australian institution4. Furthermore, Manpreet also works as as the part time in Australia

with an Australian firm. However, Manpreet incurs several educational expenses which shall

be considered taxable. As evident Manpreet incurs a self-education expenses of $18,000 for

which he cannot claim deductions. An individual may be able to claim a deduction for self-

education expenses if your study is work-related or if you receive a taxable bonded

scholarship. It is noteworthy to denote that the course must have a sufficient connection to

your current employment and:

maintain or improve the specific skills or knowledge a person require in their current

employment, or

result in, or is likely to result in, an increase in their income from your current

employment.

A person cannot claim a deduction for self-education expenses for a course that does not

have a sufficient connection to their current employment even though it:

Might be generally related to it, or

Enables a person to get new employment.

Manpreet has incurred also incurred expenses such as $2,000 on computer and printer for

the purpose of educational purpose. There he can claim the deductions for the expenses that

are incurred for self-educations.

As a general rule Expenditure is deductible under section 8-1 of the ITAA 1997 where

there is a sufficient connection between the expense and the income earning activities, such

4 Bankman, Joseph, et al. Federal Income Taxation. Wolters Kluwer Law & Business, 2017.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

that its essential character is work related and not private or domestic in nature5. For an

expense to satisfy the tests in section 8-1 of the ITAA 1997, it must have the essential

character of an outgoing incurred in gaining assessable income or, in other words, of an

income-producing expense (Lunney v. FC of T; Hayley v. FC of T (1958) 100 CLR 478;

(1958). It is noteworthy to denote that there must be a nexus between the outgoing and the

assessable income so that the outgoing isincidental and relevant to the gaining of assessable

income (Ronpibon Tin NL v. FC of T (1949).

Citing the reference of Charles Moore & Co (WA) Pty Ltd v. FC of T (1956) 95 CLR

344; (1956) it is necessary to determine the connection between the particular outgoing and

the operations or activities by which the taxpayer most directly gains or produces his or her

assessable income.

It is not sufficient that the expenditure is a prerequisite to the derivation of assessable

income. The expenditure must be relevant and incidental to the actual activities which gain

assessable income. The fact explained in Cooper's case, Hill J said (FCR at 200; ATC at

4414; ATR at 1636) that the expense is incurred at the employer's direction does not convert

the essential character of that expenditure from a private to a work related expense. The fact

that the employee is required, as a term of his employment, to incur a particular expenditure

does not convert expenditure that is not incurred in the course of the income-producing

operations into a deductible outgoing.

Similarly, in Mansfield's case, Hill J said (ATC at 4008; ATR at 375) it can be said

that generally expenditure on ordinary articles of apparel will not be deductible,

notwithstanding that such expenditure is necessary to ensure a suitable appearance in a

5 Feld, Alan. "Federal Taxation of State Tax Credits." (2016).

that its essential character is work related and not private or domestic in nature5. For an

expense to satisfy the tests in section 8-1 of the ITAA 1997, it must have the essential

character of an outgoing incurred in gaining assessable income or, in other words, of an

income-producing expense (Lunney v. FC of T; Hayley v. FC of T (1958) 100 CLR 478;

(1958). It is noteworthy to denote that there must be a nexus between the outgoing and the

assessable income so that the outgoing isincidental and relevant to the gaining of assessable

income (Ronpibon Tin NL v. FC of T (1949).

Citing the reference of Charles Moore & Co (WA) Pty Ltd v. FC of T (1956) 95 CLR

344; (1956) it is necessary to determine the connection between the particular outgoing and

the operations or activities by which the taxpayer most directly gains or produces his or her

assessable income.

It is not sufficient that the expenditure is a prerequisite to the derivation of assessable

income. The expenditure must be relevant and incidental to the actual activities which gain

assessable income. The fact explained in Cooper's case, Hill J said (FCR at 200; ATC at

4414; ATR at 1636) that the expense is incurred at the employer's direction does not convert

the essential character of that expenditure from a private to a work related expense. The fact

that the employee is required, as a term of his employment, to incur a particular expenditure

does not convert expenditure that is not incurred in the course of the income-producing

operations into a deductible outgoing.

Similarly, in Mansfield's case, Hill J said (ATC at 4008; ATR at 375) it can be said

that generally expenditure on ordinary articles of apparel will not be deductible,

notwithstanding that such expenditure is necessary to ensure a suitable appearance in a

5 Feld, Alan. "Federal Taxation of State Tax Credits." (2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

particular job or profession6. An employed solicitor may be required to dress in an

appropriate way by his or her employer, but that fact alone would not bring about the result

that the expenditure was deductible.

On the other hand Manpreet was enrolled in an accounting course and also incurred

expenses. An expense is deductible under section 8-1 when it has the essential character of an

income-producing expense. The essential character is to be determined by an objective

analysis of all the surrounding circumstances. There are circumstances where apportionment

under section 8-1 is required. The expenses incurred by Manpreet shall not be considered as

deductible. This is because a deduction is not allowable for self-education expenses if the

subject of self-education is designed to get employment, to obtain new employment or to

open up a new income-earning activity.

The decision of the High Court in FC of T v. Maddalena 71 ATC 4161; (1971) 2 ATR

541 establishes the principle that no deduction is allowable for self-education expenses if the

study is designed to enable a taxpayer to get employment or to obtain new employment7.

Such expenses are incurred at a point too soon to be regarded as incurred in gaining or

producing assessable income.

The Federal Court in FC of T v. M I Roberts 92 ATC 4787; (1992) 24 ATR 479

applied the principle in Maddalena when it overturned an AAT decision allowing a mine

6 Cao, Liangyue, et al. "Understanding the economy-wide efficiency and incidence of major

Australian taxes." Treasury WP 1 (2015).

7 Saad, Natrah. "Tax knowledge, tax complexity and tax compliance: Taxpayers’

view." Procedia-Social and Behavioral Sciences 109 (2014): 1069-1075.

particular job or profession6. An employed solicitor may be required to dress in an

appropriate way by his or her employer, but that fact alone would not bring about the result

that the expenditure was deductible.

On the other hand Manpreet was enrolled in an accounting course and also incurred

expenses. An expense is deductible under section 8-1 when it has the essential character of an

income-producing expense. The essential character is to be determined by an objective

analysis of all the surrounding circumstances. There are circumstances where apportionment

under section 8-1 is required. The expenses incurred by Manpreet shall not be considered as

deductible. This is because a deduction is not allowable for self-education expenses if the

subject of self-education is designed to get employment, to obtain new employment or to

open up a new income-earning activity.

The decision of the High Court in FC of T v. Maddalena 71 ATC 4161; (1971) 2 ATR

541 establishes the principle that no deduction is allowable for self-education expenses if the

study is designed to enable a taxpayer to get employment or to obtain new employment7.

Such expenses are incurred at a point too soon to be regarded as incurred in gaining or

producing assessable income.

The Federal Court in FC of T v. M I Roberts 92 ATC 4787; (1992) 24 ATR 479

applied the principle in Maddalena when it overturned an AAT decision allowing a mine

6 Cao, Liangyue, et al. "Understanding the economy-wide efficiency and incidence of major

Australian taxes." Treasury WP 1 (2015).

7 Saad, Natrah. "Tax knowledge, tax complexity and tax compliance: Taxpayers’

view." Procedia-Social and Behavioral Sciences 109 (2014): 1069-1075.

8TAXATION LAW

manager a deduction for expenses associated with a Master of Business Administration

degree. Mr Roberts was retrenched by his employer in Australia and then undertook an MBA

course in the US for two years. On his return to Australia, he was re-employed as a mine

manager by another company at a significantly increased salary when compared with his

previous position.

The AAT had relied on Kropp to allow a deduction for his MBA studies, based on a

finding that there was a sufficient connection between the expenses and the income derived

on the taxpayer's return to Australia. In overturning the AAT decision, Cooper J considered

that moneys were spent to obtain a new employment, albeit one in a better position and on

higher wages, rather than in the course of employment and that Maddalena clearly applied.

In the course of his judgement, Cooper J considered the decision in Kropp where an

accountant resigned from his employment with an Australian accounting firm to take up a

two-year development appointment with an associated firm in Canada8. Mr Kropp later

returned to Australia and recommenced work with his old employer at an increased salary.

Waddell J allowed a deduction for the cost of the taxpayer's air fare to Canada on the basis

that there was a perceived connection between the expenditure and the gaining of increased

income on Mr Kropp's return to Australia. Cooper J considered that 'the principles enunciated

by the High Court in Maddalena were not applicable ...' on the facts of Kropp.

Despite the view expressed by Cooper J, we regard the decision in Kropp as in error.

The decision fails to recognise that, because of the break in employment, the expenses in

8 Bankman, Joseph, et al. Federal Income Taxation. Wolters Kluwer Law & Business, 2017.

manager a deduction for expenses associated with a Master of Business Administration

degree. Mr Roberts was retrenched by his employer in Australia and then undertook an MBA

course in the US for two years. On his return to Australia, he was re-employed as a mine

manager by another company at a significantly increased salary when compared with his

previous position.

The AAT had relied on Kropp to allow a deduction for his MBA studies, based on a

finding that there was a sufficient connection between the expenses and the income derived

on the taxpayer's return to Australia. In overturning the AAT decision, Cooper J considered

that moneys were spent to obtain a new employment, albeit one in a better position and on

higher wages, rather than in the course of employment and that Maddalena clearly applied.

In the course of his judgement, Cooper J considered the decision in Kropp where an

accountant resigned from his employment with an Australian accounting firm to take up a

two-year development appointment with an associated firm in Canada8. Mr Kropp later

returned to Australia and recommenced work with his old employer at an increased salary.

Waddell J allowed a deduction for the cost of the taxpayer's air fare to Canada on the basis

that there was a perceived connection between the expenditure and the gaining of increased

income on Mr Kropp's return to Australia. Cooper J considered that 'the principles enunciated

by the High Court in Maddalena were not applicable ...' on the facts of Kropp.

Despite the view expressed by Cooper J, we regard the decision in Kropp as in error.

The decision fails to recognise that, because of the break in employment, the expenses in

8 Bankman, Joseph, et al. Federal Income Taxation. Wolters Kluwer Law & Business, 2017.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

issue were incurred at a point too soon to be regarded as incurred in gaining or producing

income9.

A deduction is not allowable because the study is designed to get Manpreet

employment in a new job and it is not derive income from work experience. It is incurred at a

point too soon to be regarded as incurred in gaining or producing assessable income.

An expense is deductible under section 8-1 when the essential character is that of an

income producing expense. The essential character is to be determined by an objective

analysis of all the surrounding circumstances (see Fletcher & Ors (199 ) 173 CLR 1 at 17; 91

ATC 4950 at 4957 and 4958; (1991) 22 ATR 613 at 622)10. If the purpose of a study tour or

attendance at a work-related conference or seminar is the gaining or producing of income, the

existence of an incidental private purpose does not affect the characterisation of the related

expenses as wholly incurred in gaining assessable income.

If the subject of self-education enables you to maintain or improve skills or

knowledge or is likely to lead to an increase in income from your current income-earning

activities, you can deduct an amount for the decline in value of a depreciating asset you use,

or have installed ready for use, for self-education purposes11. For example, you can deduct an

9 Taylor, Grantley, and Grant Richardson. "The determinants of thinly capitalized tax

avoidance structures: Evidence from Australian firms." Journal of International Accounting,

Auditing and Taxation 22.1 (2013): 12-25.

10 Schenk, Deborah H. Federal Taxation of S Corporations. Law Journal Press, 2016.

11 Davis, Angela K., et al. "Do socially responsible firms pay more taxes?." The Accounting

Review 91.1 (2015): 47-68.

issue were incurred at a point too soon to be regarded as incurred in gaining or producing

income9.

A deduction is not allowable because the study is designed to get Manpreet

employment in a new job and it is not derive income from work experience. It is incurred at a

point too soon to be regarded as incurred in gaining or producing assessable income.

An expense is deductible under section 8-1 when the essential character is that of an

income producing expense. The essential character is to be determined by an objective

analysis of all the surrounding circumstances (see Fletcher & Ors (199 ) 173 CLR 1 at 17; 91

ATC 4950 at 4957 and 4958; (1991) 22 ATR 613 at 622)10. If the purpose of a study tour or

attendance at a work-related conference or seminar is the gaining or producing of income, the

existence of an incidental private purpose does not affect the characterisation of the related

expenses as wholly incurred in gaining assessable income.

If the subject of self-education enables you to maintain or improve skills or

knowledge or is likely to lead to an increase in income from your current income-earning

activities, you can deduct an amount for the decline in value of a depreciating asset you use,

or have installed ready for use, for self-education purposes11. For example, you can deduct an

9 Taylor, Grantley, and Grant Richardson. "The determinants of thinly capitalized tax

avoidance structures: Evidence from Australian firms." Journal of International Accounting,

Auditing and Taxation 22.1 (2013): 12-25.

10 Schenk, Deborah H. Federal Taxation of S Corporations. Law Journal Press, 2016.

11 Davis, Angela K., et al. "Do socially responsible firms pay more taxes?." The Accounting

Review 91.1 (2015): 47-68.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

amount for the decline in value of assets such as technical instruments and equipment,

computers, calculators, professional libraries, filing cabinets and desks if the self-education

satisfies the principles outlined in paragraphs 13 and 14. You must reduce your deduction by

the extent to which you use the asset for other than a taxable purpose.

On the other Manpreet has come to Australia for studies and hence his educational

course is for more than six months therefore he shall be considered as taxable resident of

Australia.

According to the taxation rulings of IT 2650 the purpose is to provide guidelines for

determining whether individuals who leave Australia temporarily to live overseas, for

example, on temporary overseas work assignments or on overseas study leave, cease to be

Australian residents for income tax purposes during their overseas stay12.

In determining a person's domicile for the purposes of the definition of "resident" in

subsection 6(1), it is necessary to consider the person's intention as to the country in which he

or she is to make his or her home indefinitely13. Thus, a person with an Australian domicile

but living outside Australia will retain that domicile if he or she intends to return to Australia

on a clearly foreseen and reasonably anticipated contingency e.g., the end of his or her

employment.

12 Woellner, R. H., et al. Australian Taxation Law Select: Legislation and Commentary 2016.

Oxford University Press, 2016.

13 Vann, Richard J. "Hybrid Entities in Australia: Resource Capital Fund III LP Case."

(2016).

amount for the decline in value of assets such as technical instruments and equipment,

computers, calculators, professional libraries, filing cabinets and desks if the self-education

satisfies the principles outlined in paragraphs 13 and 14. You must reduce your deduction by

the extent to which you use the asset for other than a taxable purpose.

On the other Manpreet has come to Australia for studies and hence his educational

course is for more than six months therefore he shall be considered as taxable resident of

Australia.

According to the taxation rulings of IT 2650 the purpose is to provide guidelines for

determining whether individuals who leave Australia temporarily to live overseas, for

example, on temporary overseas work assignments or on overseas study leave, cease to be

Australian residents for income tax purposes during their overseas stay12.

In determining a person's domicile for the purposes of the definition of "resident" in

subsection 6(1), it is necessary to consider the person's intention as to the country in which he

or she is to make his or her home indefinitely13. Thus, a person with an Australian domicile

but living outside Australia will retain that domicile if he or she intends to return to Australia

on a clearly foreseen and reasonably anticipated contingency e.g., the end of his or her

employment.

12 Woellner, R. H., et al. Australian Taxation Law Select: Legislation and Commentary 2016.

Oxford University Press, 2016.

13 Vann, Richard J. "Hybrid Entities in Australia: Resource Capital Fund III LP Case."

(2016).

11TAXATION LAW

Liability to tax arises annually and the question where a taxpayer resides must be

determined annually according to the facts applicable to the particular year of income under

consideration. However, events which have happened since the end of the tax year may be

taken into account in determining that question.

The extended definition contained in subparagraph (a)(i) of the definition of

"resident" is alternative to the ordinary meaning of the term "resides" (Applegate 79 ATC at

p.4314; 9 ATR at p.907). In other words, even if the person is found not to "reside" in

Australia within the ordinary meaning of the word, he or she may still fall within the

extended definition of "resident"14. Conversely, if the person does "reside" in Australia within

the ordinary meaning of that word, it is not necessary to determine whether the extended

definition is satisfied. As evident from the fact that an individual has established his or her

home (in the sense of a dwelling place; a house or other shelter that is the fixed residence of a

person, family or household) in an overseas country would tend to show that the place of

abode in the overseas country is permanent. Therefore, Manpreet will be considered as the

Australian resident for the purpose of tax and his income will be assessable under the ITAA

199715.

14 ROBIN, H. AUSTRALIAN TAXATION LAW 2017. OXFORD University Press, 2017.

15 Blakelock, Sarah, and Peter King. "Taxation law: The advance of ATO data

matching." Proctor, The 37.6 (2017): 18.

Liability to tax arises annually and the question where a taxpayer resides must be

determined annually according to the facts applicable to the particular year of income under

consideration. However, events which have happened since the end of the tax year may be

taken into account in determining that question.

The extended definition contained in subparagraph (a)(i) of the definition of

"resident" is alternative to the ordinary meaning of the term "resides" (Applegate 79 ATC at

p.4314; 9 ATR at p.907). In other words, even if the person is found not to "reside" in

Australia within the ordinary meaning of the word, he or she may still fall within the

extended definition of "resident"14. Conversely, if the person does "reside" in Australia within

the ordinary meaning of that word, it is not necessary to determine whether the extended

definition is satisfied. As evident from the fact that an individual has established his or her

home (in the sense of a dwelling place; a house or other shelter that is the fixed residence of a

person, family or household) in an overseas country would tend to show that the place of

abode in the overseas country is permanent. Therefore, Manpreet will be considered as the

Australian resident for the purpose of tax and his income will be assessable under the ITAA

199715.

14 ROBIN, H. AUSTRALIAN TAXATION LAW 2017. OXFORD University Press, 2017.

15 Blakelock, Sarah, and Peter King. "Taxation law: The advance of ATO data

matching." Proctor, The 37.6 (2017): 18.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.