TAXATION Assignment - Finance, Semester 1, University Name

VerifiedAdded on 2020/02/24

|12

|2531

|107

Homework Assignment

AI Summary

This TAXATION assignment solution addresses various aspects of Australian taxation, including fringe benefits tax, assessable income, and allowable deductions. It examines scenarios like flight reward points, compensation for damaged capital assets, gifts, and gains for sportspeople, providing insights into their tax implications. The assignment also covers employee reimbursements, deductions for art-related expenses, and travel expenses. Furthermore, it analyzes a case study involving a student's tax liability, calculating assessable income and tax payable, while considering self-education expenses, and work-related deductions for computers, printers and mobile phones. The solution uses relevant Australian Taxation Office rulings and case laws to support its analysis, providing a comprehensive understanding of taxation principles and their application in diverse situations.

Running head: TAXATION

Taxation

Name of the University:

Name of the Student:

Authors Note:

Taxation

Name of the University:

Name of the Student:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION

Table of Contents

Answer to Question 1.................................................................................................................1

Answer of Question i:................................................................................................................1

Answer of Question ii................................................................................................................1

Answer of Question iii...............................................................................................................2

Answer to Question iv................................................................................................................3

Answer of Question V................................................................................................................3

Answer of Question vi...............................................................................................................4

Answer of Question Vii.............................................................................................................4

Answer of Question viii.............................................................................................................5

Answer of Question ix...............................................................................................................5

Answer of Question x.................................................................................................................6

Answer to Question 2.................................................................................................................6

Reference....................................................................................................................................9

Table of Contents

Answer to Question 1.................................................................................................................1

Answer of Question i:................................................................................................................1

Answer of Question ii................................................................................................................1

Answer of Question iii...............................................................................................................2

Answer to Question iv................................................................................................................3

Answer of Question V................................................................................................................3

Answer of Question vi...............................................................................................................4

Answer of Question Vii.............................................................................................................4

Answer of Question viii.............................................................................................................5

Answer of Question ix...............................................................................................................5

Answer of Question x.................................................................................................................6

Answer to Question 2.................................................................................................................6

Reference....................................................................................................................................9

2TAXATION

Answer to Question 1

Answer of Question i:

The loyal customer of the airlines is rewarded with the Flight point or Reward by the

companies in aviation that is covered under the Taxation Ruling of TR 1999/6. The

Taxation Ruling of TR 1999/6 clearly state that the points or rewards that are received by

customers from the companies in airline business are commonly not treated under taxation as

type of income1. However, Fringe Benefit Taxes might be implemented on points or rewards

if the following scenarios occur are:

There is a relationship of family between the employees and employer. The points or

rewards from the flight are received by employee’s in context to his or her

employment.

The flight points or rewards are provided to the employee for a particular

arrangement.

The Webjet’s repeated flier rewards received by the employee from the large business

organization for the purpose of work related travel paid by a firm shall be taxed neither under

Fringe Benefit Tax nor as taxable income2.

Answer of Question ii

The person from its customer receives a compensation for damages to the capital asset

at the period of providing of the service to customers then the received amount of

compensation for damages are not assessed under taxation. This is taxable under hands of the

receiver. The important points that to be considered are:

1 Gitman, Lawrence J., Roger Juchau, and Jack Flanagan. Principles of managerial finance. Pearson Higher

Education AU, 2015.

2 Braithwaite, Valerie, ed. Taxing democracy: Understanding tax avoidance and evasion. Routledge, 2017.

Answer to Question 1

Answer of Question i:

The loyal customer of the airlines is rewarded with the Flight point or Reward by the

companies in aviation that is covered under the Taxation Ruling of TR 1999/6. The

Taxation Ruling of TR 1999/6 clearly state that the points or rewards that are received by

customers from the companies in airline business are commonly not treated under taxation as

type of income1. However, Fringe Benefit Taxes might be implemented on points or rewards

if the following scenarios occur are:

There is a relationship of family between the employees and employer. The points or

rewards from the flight are received by employee’s in context to his or her

employment.

The flight points or rewards are provided to the employee for a particular

arrangement.

The Webjet’s repeated flier rewards received by the employee from the large business

organization for the purpose of work related travel paid by a firm shall be taxed neither under

Fringe Benefit Tax nor as taxable income2.

Answer of Question ii

The person from its customer receives a compensation for damages to the capital asset

at the period of providing of the service to customers then the received amount of

compensation for damages are not assessed under taxation. This is taxable under hands of the

receiver. The important points that to be considered are:

1 Gitman, Lawrence J., Roger Juchau, and Jack Flanagan. Principles of managerial finance. Pearson Higher

Education AU, 2015.

2 Braithwaite, Valerie, ed. Taxing democracy: Understanding tax avoidance and evasion. Routledge, 2017.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION

The assets should be in the form of capital and must be dynamically be utilized in the

process of business of the receiver3.

The asset must be an asset that is depreciable asset and expected depreciation has

been gauged for the asset in the records.

The amount of compensation received was utilized to use for revamping the assets

part that are damaged.

The amount of money that is received by the Crane Hire Company for the damages to the

capital asset from the customer. This is not to be considered under taxation that is not a

taxable income of the company that provided that above mentioned must be fulfilled4.

Answer of Question iii

As per the Australian Taxation Office, the gifts in kind or in cash received by an

individual are not treated as a component of the income that are exempted neither they form

the part of non-exempted income or non-assessable income. In general, the small gift is type

of a gift that are excluded at period of computation of income tax of the person5. However, in

the context to receipt of big quantity of gifts that can change into money or cash gifts or in

kind or any amount in cash that are facilitated to the employee then that sum will be

considered in the assessment of the income by the receiver.

3 Lal, Anita, Ana Maria Mantilla-Herrera, Lennert Veerman, Kathryn Backholer, Gary Sacks, Marjory Moodie,

Mohammad Siahpush, Rob Carter, and Anna Peeters. "Modelled health benefits of a sugar-sweetened beverage

tax across different socioeconomic groups in Australia: A cost-effectiveness and equity analysis." PLoS

medicine 14, no. 6 (2017): e1002326.

4 Davis, Angela K., David A. Guenther, Linda K. Krull, and Brian M. Williams. "Do socially responsible firms

pay more taxes?." The Accounting Review 91, no. 1 (2015): 47-68.

5 Cheshire, Lynda, Jo-Anne Everingham, and Geoffrey Lawrence. "Governing the impacts of mining and the

impacts of mining governance: Challenges for rural and regional local governments in Australia." Journal of

Rural Studies36 (2014): 330-339.

The assets should be in the form of capital and must be dynamically be utilized in the

process of business of the receiver3.

The asset must be an asset that is depreciable asset and expected depreciation has

been gauged for the asset in the records.

The amount of compensation received was utilized to use for revamping the assets

part that are damaged.

The amount of money that is received by the Crane Hire Company for the damages to the

capital asset from the customer. This is not to be considered under taxation that is not a

taxable income of the company that provided that above mentioned must be fulfilled4.

Answer of Question iii

As per the Australian Taxation Office, the gifts in kind or in cash received by an

individual are not treated as a component of the income that are exempted neither they form

the part of non-exempted income or non-assessable income. In general, the small gift is type

of a gift that are excluded at period of computation of income tax of the person5. However, in

the context to receipt of big quantity of gifts that can change into money or cash gifts or in

kind or any amount in cash that are facilitated to the employee then that sum will be

considered in the assessment of the income by the receiver.

3 Lal, Anita, Ana Maria Mantilla-Herrera, Lennert Veerman, Kathryn Backholer, Gary Sacks, Marjory Moodie,

Mohammad Siahpush, Rob Carter, and Anna Peeters. "Modelled health benefits of a sugar-sweetened beverage

tax across different socioeconomic groups in Australia: A cost-effectiveness and equity analysis." PLoS

medicine 14, no. 6 (2017): e1002326.

4 Davis, Angela K., David A. Guenther, Linda K. Krull, and Brian M. Williams. "Do socially responsible firms

pay more taxes?." The Accounting Review 91, no. 1 (2015): 47-68.

5 Cheshire, Lynda, Jo-Anne Everingham, and Geoffrey Lawrence. "Governing the impacts of mining and the

impacts of mining governance: Challenges for rural and regional local governments in Australia." Journal of

Rural Studies36 (2014): 330-339.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION

The alcohol supplier has provided the package of Free Overseas holiday that is

received by the Manager of the Night Club. This will be taken in computation of income tax

of the Manager of the nightclub.

Answer to Question iv

The money that was raised by the Canoe Club for the purpose of buying the additional

canoes that was found that an extra fund was raised that was returned to the member of the

Canoe Club.

The extra money or finance that was raised will not be taken when the computation of

income tax for the acceptance. This will not be taken while computation of the income as this

finance does not display as the income in its alternative extra funds that are provided by the

members. This finance was not displaying a fund collected that was more needed for

acquiring.

Answer of Question V

The gains that are received by sports people that are usually know as sportsman as

they are in participate actively in the field of sports. This is comes under the Taxation Rulings

TR 1999/176.

As per the rulings, any sort of gains or sum received by sports people is taken as an

income that subject to tax. If these receipts cumulatively makes a part of income. In the

current situation, the amount received by footballer who is Australian from the company of

television for being the fairest and excellent player will be taken as income that is taxable as

per the normal concept.

6 Richardson, Grant, Grantley Taylor, and Roman Lanis. "The impact of board of director oversight

characteristics on corporate tax aggressiveness: An empirical analysis." Journal of Accounting and Public

Policy 32, no. 3 (2013): 68-88.

The alcohol supplier has provided the package of Free Overseas holiday that is

received by the Manager of the Night Club. This will be taken in computation of income tax

of the Manager of the nightclub.

Answer to Question iv

The money that was raised by the Canoe Club for the purpose of buying the additional

canoes that was found that an extra fund was raised that was returned to the member of the

Canoe Club.

The extra money or finance that was raised will not be taken when the computation of

income tax for the acceptance. This will not be taken while computation of the income as this

finance does not display as the income in its alternative extra funds that are provided by the

members. This finance was not displaying a fund collected that was more needed for

acquiring.

Answer of Question V

The gains that are received by sports people that are usually know as sportsman as

they are in participate actively in the field of sports. This is comes under the Taxation Rulings

TR 1999/176.

As per the rulings, any sort of gains or sum received by sports people is taken as an

income that subject to tax. If these receipts cumulatively makes a part of income. In the

current situation, the amount received by footballer who is Australian from the company of

television for being the fairest and excellent player will be taken as income that is taxable as

per the normal concept.

6 Richardson, Grant, Grantley Taylor, and Roman Lanis. "The impact of board of director oversight

characteristics on corporate tax aggressiveness: An empirical analysis." Journal of Accounting and Public

Policy 32, no. 3 (2013): 68-88.

5TAXATION

Answer of Question vi

The reimbursement, allowance, etc constructing employees is being stated under the

Taxation Ruling of TR 95/22.

As per the Taxation Ruling of TR 95/22 a constructing and building employee

composed of the following are:-

Labours who are employed for the purpose of making of a building.

In the construction site the Projected Manager is employed for the constructing of

buildings and many more.

Trainees, Carpenter and Apprentice.

The construction sites where supervisors work.

The spending occurred in context to the building aptitude for the building apprentice have

been clearly defined as the construction and building labourer as compensation and the

different allowances.

Answer of Question Vii

At the period of computing of income tax, subsequent expenses done for short period

in context to be an artiste person are authorized with the deductions like:-

Educating of modules and software’s.

Fees for the course for the term that is short course for the subject of art.

Suggested meals for a certain amount expense.

The travelling cost is involved for the course.

The above-mentioned expenses shall be taken as deductions that are allowed only if the

spending are related with the course of art management that is for short period. The spending

that is occurred but does not relate proportionately to the course of art management will not

Answer of Question vi

The reimbursement, allowance, etc constructing employees is being stated under the

Taxation Ruling of TR 95/22.

As per the Taxation Ruling of TR 95/22 a constructing and building employee

composed of the following are:-

Labours who are employed for the purpose of making of a building.

In the construction site the Projected Manager is employed for the constructing of

buildings and many more.

Trainees, Carpenter and Apprentice.

The construction sites where supervisors work.

The spending occurred in context to the building aptitude for the building apprentice have

been clearly defined as the construction and building labourer as compensation and the

different allowances.

Answer of Question Vii

At the period of computing of income tax, subsequent expenses done for short period

in context to be an artiste person are authorized with the deductions like:-

Educating of modules and software’s.

Fees for the course for the term that is short course for the subject of art.

Suggested meals for a certain amount expense.

The travelling cost is involved for the course.

The above-mentioned expenses shall be taken as deductions that are allowed only if the

spending are related with the course of art management that is for short period. The spending

that is occurred but does not relate proportionately to the course of art management will not

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION

be allowed as deductions for the taxation purpose7. Hence, the expenditures in the current

situation can be given for the deductions assuming that art management course is a short

period course and expenditures done is within the above range and influence.

Answer of Question viii

As per the tax law the expenses for the dresses provided by the employer is not taken

under the taxation system. As per the Taxation office of Australia executing of the art by the

artist are taken as deduction are allowed as the performing artist has provided them. As the

ruling of Taxation grant by the Taxation office of Australia, performing artist are the

subsequent individuals:

Performing artist means a musician

Performing artist means an actor.

Performing artist means a singer.

Performing artist means a variety artist.

Performance artist means a circus performer and dance.

In the present situation, assuming that expenditures are in context to dresses and work

make up of performing artist then this expenses are allowed as a deduction in shaping the

incomes that are taxable for the performing artist.

Answer of Question ix

Generally, the travelling between home and workplace is taken as travel for private

reasons. However, there are specific provisions where deductions that are allowable that can

be assert for the expenses for travelling8.

7

8 Kucukvar, Murat, Gokhan Egilmez, and Omer Tatari. "Sustainability assessment of US final consumption and

investments: triple-bottom-line input–output analysis." Journal of cleaner production 81 (2014): 234-243.

be allowed as deductions for the taxation purpose7. Hence, the expenditures in the current

situation can be given for the deductions assuming that art management course is a short

period course and expenditures done is within the above range and influence.

Answer of Question viii

As per the tax law the expenses for the dresses provided by the employer is not taken

under the taxation system. As per the Taxation office of Australia executing of the art by the

artist are taken as deduction are allowed as the performing artist has provided them. As the

ruling of Taxation grant by the Taxation office of Australia, performing artist are the

subsequent individuals:

Performing artist means a musician

Performing artist means an actor.

Performing artist means a singer.

Performing artist means a variety artist.

Performance artist means a circus performer and dance.

In the present situation, assuming that expenditures are in context to dresses and work

make up of performing artist then this expenses are allowed as a deduction in shaping the

incomes that are taxable for the performing artist.

Answer of Question ix

Generally, the travelling between home and workplace is taken as travel for private

reasons. However, there are specific provisions where deductions that are allowable that can

be assert for the expenses for travelling8.

7

8 Kucukvar, Murat, Gokhan Egilmez, and Omer Tatari. "Sustainability assessment of US final consumption and

investments: triple-bottom-line input–output analysis." Journal of cleaner production 81 (2014): 234-243.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION

If the travelling is for official purpose only and in case partly private and partly

official then that are component of the expenditures that is taken as travel for official purpose

where deductions that allowable can be asserted. In Current condition may be better be

understood that the travelling was the purpose of work only. The expenditures that occurred

can be asserted for deductions the period of determination of income tax.

Answer of Question x

The expenses done for the purpose of travelling in between the two places of work are

taken for the deduction purposes.

The expenditures occurred relating to travelling between another employer and

employer. Nevertheless, in the current situation costs done for travel between the two

employers is not going to be considered or taken as deductions those are allowed. This is due

to reason that deductions claim will not be claimed for commuting between the various

employers9.

Answer to Question 2

In order to determine the tax liability of an individual it is necessary to determine

whether the individual is a resident of Australia or a foreign resident for the purpose of tax.

The law provides that a student from overseas that have enrolled in Australia for a duration of

more than six shall be considered as a resident for the purpose of tax. In the present scenario

it can be seen that Manpreet shall be regarded as an Australian resident for the purpose of tax

as he is enrolled for a course more than six month in an Australian university10. In addition to

this, he also works in an office in a part-time basis and earns a remuneration of $45000. He

9 Picciotto, Sol. "Indeterminacy, complexity, technocracy and the reform of international corporate

taxation." Social & Legal Studies 24, no. 2 (2015): 165-184.

10 Lignier, Philip, Chris Evans, and Binh Tran-Nam. "Tangled up in tape: The continuing tax compliance plight

of the small and medium enterprise business sector." (2014).

If the travelling is for official purpose only and in case partly private and partly

official then that are component of the expenditures that is taken as travel for official purpose

where deductions that allowable can be asserted. In Current condition may be better be

understood that the travelling was the purpose of work only. The expenditures that occurred

can be asserted for deductions the period of determination of income tax.

Answer of Question x

The expenses done for the purpose of travelling in between the two places of work are

taken for the deduction purposes.

The expenditures occurred relating to travelling between another employer and

employer. Nevertheless, in the current situation costs done for travel between the two

employers is not going to be considered or taken as deductions those are allowed. This is due

to reason that deductions claim will not be claimed for commuting between the various

employers9.

Answer to Question 2

In order to determine the tax liability of an individual it is necessary to determine

whether the individual is a resident of Australia or a foreign resident for the purpose of tax.

The law provides that a student from overseas that have enrolled in Australia for a duration of

more than six shall be considered as a resident for the purpose of tax. In the present scenario

it can be seen that Manpreet shall be regarded as an Australian resident for the purpose of tax

as he is enrolled for a course more than six month in an Australian university10. In addition to

this, he also works in an office in a part-time basis and earns a remuneration of $45000. He

9 Picciotto, Sol. "Indeterminacy, complexity, technocracy and the reform of international corporate

taxation." Social & Legal Studies 24, no. 2 (2015): 165-184.

10 Lignier, Philip, Chris Evans, and Binh Tran-Nam. "Tangled up in tape: The continuing tax compliance plight

of the small and medium enterprise business sector." (2014).

8TAXATION

had to incur expenses for education and this are not allowed as deduction. The self-education

expenses of $18000 will not be allowed as deduction. The law states that an individual can

claim expenses related to self-education if the study is relate to work or the individual has

received scholarship of taxable bond. The course undertaken for self-education should have

beneficial interest with the current employment. The course should:

Improve or enhance the necessary skill that is required by the individual in the current

place of employment;

The course will help to increase the income from the current employment.

Therefore, it can be said that an individual should not claim for expenses related to self-

education that does not have any relation or bearing with the current employment.

The section 8-1 of the Income Tax Assessment Act provides that an expense is allowed

as deduction if there is sufficient relationship between the expenses and the income

producing activities. The expenses related to private ort domestic nature is not allowed as

deduction. In the case of Lunney v. FC of T; Hayley v. FC of T (1958) 100 CLR 478;

(1958) it was held that an expense can satisfy the test under section 8-1 if it has the

characteristic of constituting as an income generating activity11.

The judgement in the case of Ronpibon Tin NL v. FC of T (1949) supports the

viewpoint. It states that an outgoing can only be allowed as tax deduction if the outgoing is

resulted in producing taxable income. The expenses that have been incurred for self-

education will not be allowed as deduction.

There are certain expenses that have been incurred by Manpreet on computers and

printers. He has also incurred expenses for mobile phones that are used for the work related

11 Faccio, Mara, and Jin Xu. "Taxes and capital structure." Journal of Financial and Quantitative Analysis 50,

no. 3 (2015): 277-300.

had to incur expenses for education and this are not allowed as deduction. The self-education

expenses of $18000 will not be allowed as deduction. The law states that an individual can

claim expenses related to self-education if the study is relate to work or the individual has

received scholarship of taxable bond. The course undertaken for self-education should have

beneficial interest with the current employment. The course should:

Improve or enhance the necessary skill that is required by the individual in the current

place of employment;

The course will help to increase the income from the current employment.

Therefore, it can be said that an individual should not claim for expenses related to self-

education that does not have any relation or bearing with the current employment.

The section 8-1 of the Income Tax Assessment Act provides that an expense is allowed

as deduction if there is sufficient relationship between the expenses and the income

producing activities. The expenses related to private ort domestic nature is not allowed as

deduction. In the case of Lunney v. FC of T; Hayley v. FC of T (1958) 100 CLR 478;

(1958) it was held that an expense can satisfy the test under section 8-1 if it has the

characteristic of constituting as an income generating activity11.

The judgement in the case of Ronpibon Tin NL v. FC of T (1949) supports the

viewpoint. It states that an outgoing can only be allowed as tax deduction if the outgoing is

resulted in producing taxable income. The expenses that have been incurred for self-

education will not be allowed as deduction.

There are certain expenses that have been incurred by Manpreet on computers and

printers. He has also incurred expenses for mobile phones that are used for the work related

11 Faccio, Mara, and Jin Xu. "Taxes and capital structure." Journal of Financial and Quantitative Analysis 50,

no. 3 (2015): 277-300.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION

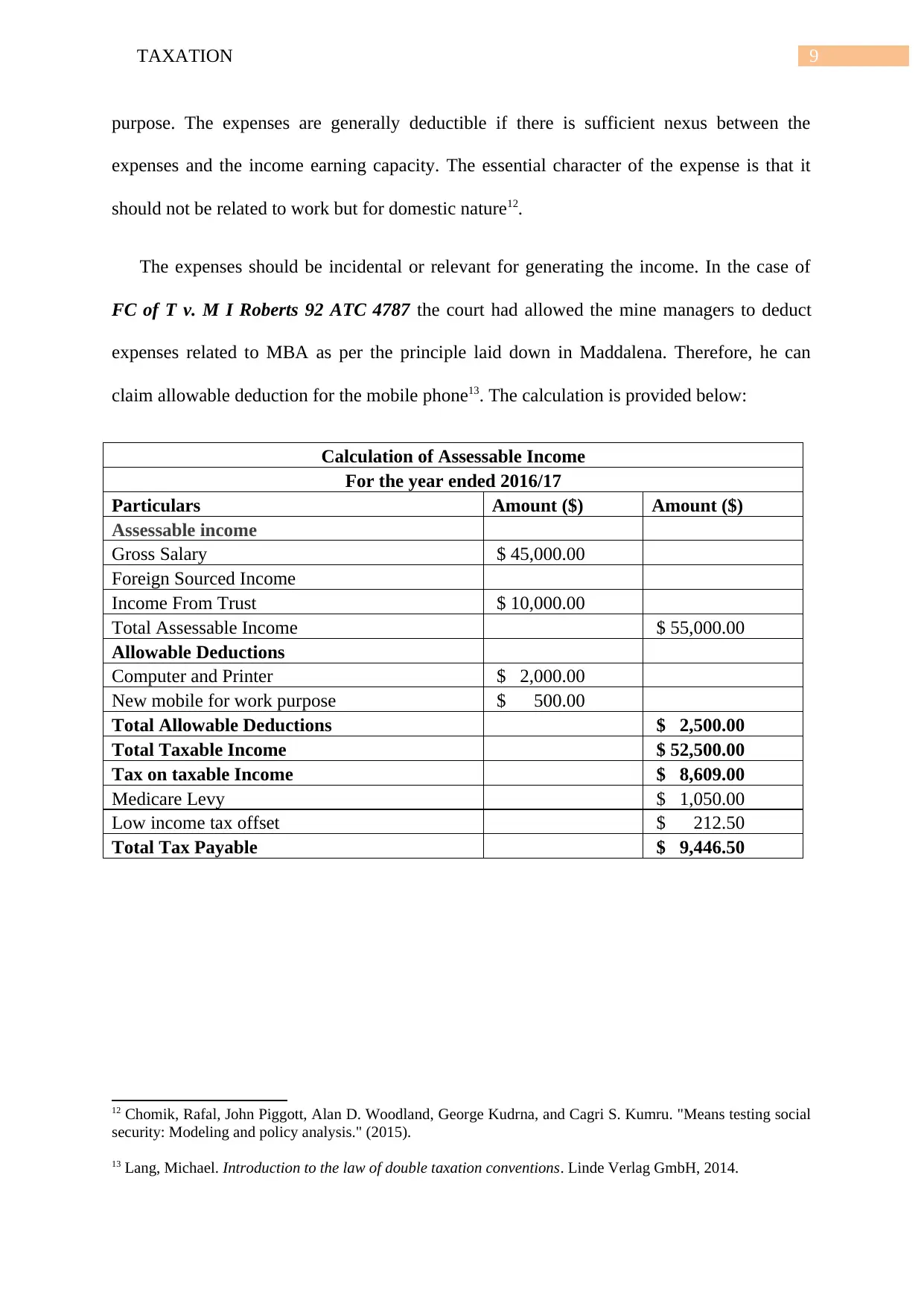

purpose. The expenses are generally deductible if there is sufficient nexus between the

expenses and the income earning capacity. The essential character of the expense is that it

should not be related to work but for domestic nature12.

The expenses should be incidental or relevant for generating the income. In the case of

FC of T v. M I Roberts 92 ATC 4787 the court had allowed the mine managers to deduct

expenses related to MBA as per the principle laid down in Maddalena. Therefore, he can

claim allowable deduction for the mobile phone13. The calculation is provided below:

Calculation of Assessable Income

For the year ended 2016/17

Particulars Amount ($) Amount ($)

Assessable income

Gross Salary $ 45,000.00

Foreign Sourced Income

Income From Trust $ 10,000.00

Total Assessable Income $ 55,000.00

Allowable Deductions

Computer and Printer $ 2,000.00

New mobile for work purpose $ 500.00

Total Allowable Deductions $ 2,500.00

Total Taxable Income $ 52,500.00

Tax on taxable Income $ 8,609.00

Medicare Levy $ 1,050.00

Low income tax offset $ 212.50

Total Tax Payable $ 9,446.50

12 Chomik, Rafal, John Piggott, Alan D. Woodland, George Kudrna, and Cagri S. Kumru. "Means testing social

security: Modeling and policy analysis." (2015).

13 Lang, Michael. Introduction to the law of double taxation conventions. Linde Verlag GmbH, 2014.

purpose. The expenses are generally deductible if there is sufficient nexus between the

expenses and the income earning capacity. The essential character of the expense is that it

should not be related to work but for domestic nature12.

The expenses should be incidental or relevant for generating the income. In the case of

FC of T v. M I Roberts 92 ATC 4787 the court had allowed the mine managers to deduct

expenses related to MBA as per the principle laid down in Maddalena. Therefore, he can

claim allowable deduction for the mobile phone13. The calculation is provided below:

Calculation of Assessable Income

For the year ended 2016/17

Particulars Amount ($) Amount ($)

Assessable income

Gross Salary $ 45,000.00

Foreign Sourced Income

Income From Trust $ 10,000.00

Total Assessable Income $ 55,000.00

Allowable Deductions

Computer and Printer $ 2,000.00

New mobile for work purpose $ 500.00

Total Allowable Deductions $ 2,500.00

Total Taxable Income $ 52,500.00

Tax on taxable Income $ 8,609.00

Medicare Levy $ 1,050.00

Low income tax offset $ 212.50

Total Tax Payable $ 9,446.50

12 Chomik, Rafal, John Piggott, Alan D. Woodland, George Kudrna, and Cagri S. Kumru. "Means testing social

security: Modeling and policy analysis." (2015).

13 Lang, Michael. Introduction to the law of double taxation conventions. Linde Verlag GmbH, 2014.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION

Reference

Braithwaite, Valerie, ed. Taxing democracy: Understanding tax avoidance and evasion.

Routledge, 2017.

Cheshire, Lynda, Jo-Anne Everingham, and Geoffrey Lawrence. "Governing the impacts of

mining and the impacts of mining governance: Challenges for rural and regional local

governments in Australia." Journal of Rural Studies36 (2014): 330-339.

Chomik, Rafal, John Piggott, Alan D. Woodland, George Kudrna, and Cagri S. Kumru.

"Means testing social security: Modeling and policy analysis." (2015).

Davis, Angela K., David A. Guenther, Linda K. Krull, and Brian M. Williams. "Do socially

responsible firms pay more taxes?." The Accounting Review 91, no. 1 (2015): 47-68.

Faccio, Mara, and Jin Xu. "Taxes and capital structure." Journal of Financial and

Quantitative Analysis 50, no. 3 (2015): 277-300.

Gitman, Lawrence J., Roger Juchau, and Jack Flanagan. Principles of managerial finance.

Pearson Higher Education AU, 2015.

Kucukvar, Murat, Gokhan Egilmez, and Omer Tatari. "Sustainability assessment of US final

consumption and investments: triple-bottom-line input–output analysis." Journal of cleaner

production 81 (2014): 234-243.

Lal, Anita, Ana Maria Mantilla-Herrera, Lennert Veerman, Kathryn Backholer, Gary Sacks,

Marjory Moodie, Mohammad Siahpush, Rob Carter, and Anna Peeters. "Modelled health

benefits of a sugar-sweetened beverage tax across different socioeconomic groups in

Australia: A cost-effectiveness and equity analysis." PLoS medicine 14, no. 6 (2017):

e1002326.

Reference

Braithwaite, Valerie, ed. Taxing democracy: Understanding tax avoidance and evasion.

Routledge, 2017.

Cheshire, Lynda, Jo-Anne Everingham, and Geoffrey Lawrence. "Governing the impacts of

mining and the impacts of mining governance: Challenges for rural and regional local

governments in Australia." Journal of Rural Studies36 (2014): 330-339.

Chomik, Rafal, John Piggott, Alan D. Woodland, George Kudrna, and Cagri S. Kumru.

"Means testing social security: Modeling and policy analysis." (2015).

Davis, Angela K., David A. Guenther, Linda K. Krull, and Brian M. Williams. "Do socially

responsible firms pay more taxes?." The Accounting Review 91, no. 1 (2015): 47-68.

Faccio, Mara, and Jin Xu. "Taxes and capital structure." Journal of Financial and

Quantitative Analysis 50, no. 3 (2015): 277-300.

Gitman, Lawrence J., Roger Juchau, and Jack Flanagan. Principles of managerial finance.

Pearson Higher Education AU, 2015.

Kucukvar, Murat, Gokhan Egilmez, and Omer Tatari. "Sustainability assessment of US final

consumption and investments: triple-bottom-line input–output analysis." Journal of cleaner

production 81 (2014): 234-243.

Lal, Anita, Ana Maria Mantilla-Herrera, Lennert Veerman, Kathryn Backholer, Gary Sacks,

Marjory Moodie, Mohammad Siahpush, Rob Carter, and Anna Peeters. "Modelled health

benefits of a sugar-sweetened beverage tax across different socioeconomic groups in

Australia: A cost-effectiveness and equity analysis." PLoS medicine 14, no. 6 (2017):

e1002326.

11TAXATION

Lang, Michael. Introduction to the law of double taxation conventions. Linde Verlag GmbH,

2014.

Lignier, Philip, Chris Evans, and Binh Tran-Nam. "Tangled up in tape: The continuing tax

compliance plight of the small and medium enterprise business sector." (2014).

Picciotto, Sol. "Indeterminacy, complexity, technocracy and the reform of international

corporate taxation." Social & Legal Studies 24, no. 2 (2015): 165-184.

Richardson, Grant, Grantley Taylor, and Roman Lanis. "The impact of board of director

oversight characteristics on corporate tax aggressiveness: An empirical analysis." Journal of

Accounting and Public Policy 32, no. 3 (2013): 68-88.

Lang, Michael. Introduction to the law of double taxation conventions. Linde Verlag GmbH,

2014.

Lignier, Philip, Chris Evans, and Binh Tran-Nam. "Tangled up in tape: The continuing tax

compliance plight of the small and medium enterprise business sector." (2014).

Picciotto, Sol. "Indeterminacy, complexity, technocracy and the reform of international

corporate taxation." Social & Legal Studies 24, no. 2 (2015): 165-184.

Richardson, Grant, Grantley Taylor, and Roman Lanis. "The impact of board of director

oversight characteristics on corporate tax aggressiveness: An empirical analysis." Journal of

Accounting and Public Policy 32, no. 3 (2013): 68-88.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.