TAXATION LAW Assignment - Taxation Issues Analysis, University

VerifiedAdded on 2020/02/24

|13

|3000

|71

Homework Assignment

AI Summary

This taxation law assignment provides a detailed analysis of various tax-related issues. It begins by addressing specific issues, such as the taxation of flight rewards, compensation for damaged capital assets, gifts, and other income sources, referencing relevant taxation rulings and legal precedents. The assignment then delves into the assessment of Manpreet's tax situation, considering his residential status, educational expenses, and work-related expenditures. It examines whether Manpreet can claim deductions for self-education expenses, printer and computer expenses, and a new mobile phone, referencing Section 8-1 of the Income Tax Assessment Act 1997 and relevant case law such as Lunney v. FC of T and Ronpibon Tin NL v. FC of T to support its arguments. The assignment concludes by determining the allowability of various expenses and providing a comprehensive overview of tax principles.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to Question 1:................................................................................................................2

Answer to Issue (I).....................................................................................................................2

Answer to Issue (II)....................................................................................................................3

Answer to Issue (III)..................................................................................................................3

Answer to Issue (IV):.................................................................................................................4

Answer to Issue (V)...................................................................................................................4

Answer to Issue (VI):.................................................................................................................4

Answer to Issue (VII):................................................................................................................5

Answer to Issue (VIII):..............................................................................................................5

Answer to Issue (IX):.................................................................................................................6

Answer to Issue (X):..................................................................................................................6

Answer to question 2:.................................................................................................................7

Reference List:.........................................................................................................................11

Table of Contents

Answer to Question 1:................................................................................................................2

Answer to Issue (I).....................................................................................................................2

Answer to Issue (II)....................................................................................................................3

Answer to Issue (III)..................................................................................................................3

Answer to Issue (IV):.................................................................................................................4

Answer to Issue (V)...................................................................................................................4

Answer to Issue (VI):.................................................................................................................4

Answer to Issue (VII):................................................................................................................5

Answer to Issue (VIII):..............................................................................................................5

Answer to Issue (IX):.................................................................................................................6

Answer to Issue (X):..................................................................................................................6

Answer to question 2:.................................................................................................................7

Reference List:.........................................................................................................................11

2TAXATION LAW

Answer to Question 1:

Answer to Issue (I)

According to the taxation ruling of TR 1999/6 it lay down the provision that is related to

the flight rewards that are offered to the loyal consumers by the airline service providers

(Pinto, 2013). As per the ruling flight reward that are provided to the consumers by the airline

companies are generally not considered for taxation purpose as income though Fringe Benefit

Tax can be imposed on the rewards given that the below stated creation are satisfied;

a. There is a form of family connection amid the employer and the employee and reward

for flight travel by the employees in regard to the employment.

b. The flight reward are provided to the employee under the precise arrangement

As defined under the taxation ruling TR 1999/6 when habitual fliers are given with the

flight rewards by the airline companies it shall be considered for the purpose of taxation

(Barkoczy, 2016). However, if a person has received reward depending upon the fact that

flight reward entitlement will accrue with the services and the flight reward will be viewed as

business expenditure for the employer.

On considering the nature of the above stated expiation it can be viewed that Webjet

received a frequent flier point that is received by the business analysis employed under the

large business consultancy concerning the work related travel will be considered neither for

the purpose of taxation nor any form of FBT shall be applied on such kinds of rewards.

Answer to Question 1:

Answer to Issue (I)

According to the taxation ruling of TR 1999/6 it lay down the provision that is related to

the flight rewards that are offered to the loyal consumers by the airline service providers

(Pinto, 2013). As per the ruling flight reward that are provided to the consumers by the airline

companies are generally not considered for taxation purpose as income though Fringe Benefit

Tax can be imposed on the rewards given that the below stated creation are satisfied;

a. There is a form of family connection amid the employer and the employee and reward

for flight travel by the employees in regard to the employment.

b. The flight reward are provided to the employee under the precise arrangement

As defined under the taxation ruling TR 1999/6 when habitual fliers are given with the

flight rewards by the airline companies it shall be considered for the purpose of taxation

(Barkoczy, 2016). However, if a person has received reward depending upon the fact that

flight reward entitlement will accrue with the services and the flight reward will be viewed as

business expenditure for the employer.

On considering the nature of the above stated expiation it can be viewed that Webjet

received a frequent flier point that is received by the business analysis employed under the

large business consultancy concerning the work related travel will be considered neither for

the purpose of taxation nor any form of FBT shall be applied on such kinds of rewards.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Answer to Issue (II)

Compensation received by a person from the customers for causing damage to the capital

asset in rendering service then those receipts will not be considered for assessment by the

recipients. Below stated are the necessary considerations that must be followed;

a. The asset should be in the nature of the capital and must be actively employed for the

purpose of business by the recipient

b. The amount should be received by the customers to whom such kind of services must

be rendered for the users of the asset and damaged during the use

c. The amount received was used for repairing the damaged portion of the asset

d. The asset should be of depreciable type and stable depreciation should be recorded in

the books of accounts concerning the asset (Snape & Souza, 2016).

The receipt of sum by the Crane Hire Company for the crane that is damaged by the

customers must not be considered for the purpose of taxation by the Crane hire company

provided that the above discussed criterion are fulfilled.

Answer to Issue (III)

As per the Australian taxation gifts that are received by the person will not be

regarded as exempted income nor any kind of non-assessable non-exempt income. Gifts that

are of small amount should not be included in determining the taxable income of the taxpayer

(Braithwaite, 2017). In respect of large amount of receipt of cash gift or gifts that are

convertible in cash or kind that are given to the employee then such kind of gifts shall be

considered in determining the assessable income of the recipient. Therefore, abroad holiday

package received by manager of the night club from the alcohol dealer will be included in

calculating the chargeable income of the night club manager.

Answer to Issue (II)

Compensation received by a person from the customers for causing damage to the capital

asset in rendering service then those receipts will not be considered for assessment by the

recipients. Below stated are the necessary considerations that must be followed;

a. The asset should be in the nature of the capital and must be actively employed for the

purpose of business by the recipient

b. The amount should be received by the customers to whom such kind of services must

be rendered for the users of the asset and damaged during the use

c. The amount received was used for repairing the damaged portion of the asset

d. The asset should be of depreciable type and stable depreciation should be recorded in

the books of accounts concerning the asset (Snape & Souza, 2016).

The receipt of sum by the Crane Hire Company for the crane that is damaged by the

customers must not be considered for the purpose of taxation by the Crane hire company

provided that the above discussed criterion are fulfilled.

Answer to Issue (III)

As per the Australian taxation gifts that are received by the person will not be

regarded as exempted income nor any kind of non-assessable non-exempt income. Gifts that

are of small amount should not be included in determining the taxable income of the taxpayer

(Braithwaite, 2017). In respect of large amount of receipt of cash gift or gifts that are

convertible in cash or kind that are given to the employee then such kind of gifts shall be

considered in determining the assessable income of the recipient. Therefore, abroad holiday

package received by manager of the night club from the alcohol dealer will be included in

calculating the chargeable income of the night club manager.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Answer to Issue (IV):

The return of additional fund to the member of the Canoe Club for the fund

accumulated to purchase canoes will not be viewed as taxable income for the receipt (Cao et

al., 2015). The reason behind this is that receipt of funds does not constitute any form of

income rather than an additional fund that are contributed to procure the canoes however does

not states that a fund accumulated were beyond the required amount of purchase.

Answer to Issue (V)

In the current scenario the amount that is received by the Australian football player by

the television company shall be included in the assessable income of the taxpayer within the

ordinary concept. The taxation rulings of TR 1999/17 deal with the benefit for the amount

received by the sportsman for their engagement in sport (Saad, 2014). As per the ruling if

such receipts becomes the part of the revenue within the ordinary concept.

Answer to Issue (VI):

The taxation ruling of TR 95/22 lays down the ruling concerning the allowance or

reimbursement received by the building employee. The ruling defines the building and

construction employee represents of the following;

a. Project manager and the person doing the work of supervision for the construction of

building

b. Labours that are employed for construction of building

c. Project manager that are employed at the site of construction

d. Carpenter, apprentice and person undergoing trainee

Answer to Issue (IV):

The return of additional fund to the member of the Canoe Club for the fund

accumulated to purchase canoes will not be viewed as taxable income for the receipt (Cao et

al., 2015). The reason behind this is that receipt of funds does not constitute any form of

income rather than an additional fund that are contributed to procure the canoes however does

not states that a fund accumulated were beyond the required amount of purchase.

Answer to Issue (V)

In the current scenario the amount that is received by the Australian football player by

the television company shall be included in the assessable income of the taxpayer within the

ordinary concept. The taxation rulings of TR 1999/17 deal with the benefit for the amount

received by the sportsman for their engagement in sport (Saad, 2014). As per the ruling if

such receipts becomes the part of the revenue within the ordinary concept.

Answer to Issue (VI):

The taxation ruling of TR 95/22 lays down the ruling concerning the allowance or

reimbursement received by the building employee. The ruling defines the building and

construction employee represents of the following;

a. Project manager and the person doing the work of supervision for the construction of

building

b. Labours that are employed for construction of building

c. Project manager that are employed at the site of construction

d. Carpenter, apprentice and person undergoing trainee

5TAXATION LAW

Expenses that are occurred concerning the building qualification for building apprentice

have been defined as the building construction worker for reimbursement and other form of

allowance (Robin, 2017).

Answer to Issue (VII):

In computing the assessable income, the below stated expenses that are incurred for the

short term course of an artist should allowed in the form of deductions;

a. Course fees that are occurred for short term course on art

b. Training for different types of software and modules

c. Cost that are involved in travelling to and from the place of course

d. Expenditure that are recommended on meal

From the above stated discussion expenses must be considered as allowable deductions

given the expenses that are connected with the short term course. In spite of the expenditure

that are incurred however not correctly correlated for the such kind of short term course than

those expenditure will be allowable as deductions for taxation (Blakelock & King, 2017).

Hence, expenditure in the current circumstances can be considered as allowable deductions

on assuming that the course was in the nature of short term and are under the above stated

scope.

Answer to Issue (VIII):

As defined by the Australian Taxation Office expenses associated with performing artist

are allowable as deductions until they are associated in context of the performing artist

(Vann, 2016). As per the taxation ruling provided by the Australian Taxation Office

performing artist are defined as;

Expenses that are occurred concerning the building qualification for building apprentice

have been defined as the building construction worker for reimbursement and other form of

allowance (Robin, 2017).

Answer to Issue (VII):

In computing the assessable income, the below stated expenses that are incurred for the

short term course of an artist should allowed in the form of deductions;

a. Course fees that are occurred for short term course on art

b. Training for different types of software and modules

c. Cost that are involved in travelling to and from the place of course

d. Expenditure that are recommended on meal

From the above stated discussion expenses must be considered as allowable deductions

given the expenses that are connected with the short term course. In spite of the expenditure

that are incurred however not correctly correlated for the such kind of short term course than

those expenditure will be allowable as deductions for taxation (Blakelock & King, 2017).

Hence, expenditure in the current circumstances can be considered as allowable deductions

on assuming that the course was in the nature of short term and are under the above stated

scope.

Answer to Issue (VIII):

As defined by the Australian Taxation Office expenses associated with performing artist

are allowable as deductions until they are associated in context of the performing artist

(Vann, 2016). As per the taxation ruling provided by the Australian Taxation Office

performing artist are defined as;

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

a. A music composer will be viewed as performing artist

b. An artist shall be viewed as performing artist

c. A singer shall be viewed as performing artist

d. A variety artist shall be viewed as performing artist

e. A dancer and circus performer shall be viewed as performing artist

On assuming in the present context that the expenditure are connected to work of makeup

and dresses of the performing artist then those kind of expenses can be viewed as deductions

in ascertaining the chargeable revenue of the performing artist (Dunne et al., 2016).

Answer to Issue (IX):

As a general rule, travel by a person from the place of work to home is viewed as

private travel but there exists a specific provision where allowable deductions can be claimed

for such kind of travelling expenditure (Anderson et al., 2016). If the expenses incurred is for

official use and in cases where the expenditure are partially for the purpose of office and

partly for private purpose then those kind of expenditure will not be regarded as official

travel for claiming allowable deductions. In respect of the current situation, it can be

understood that the travel expenditure was for the purpose of work and the expenditure

incurred can be claimed as allowable deductions in deterring the assessable income of the

taxpayer.

Answer to Issue (X):

Expenses that are occurred for travelling between two work places are usually

regarded as deductions (Tan et al., 2016). Henceforth, in the current circumstances expenses

occurred on travelling between two employers will not be viewed as allowable deductions.

a. A music composer will be viewed as performing artist

b. An artist shall be viewed as performing artist

c. A singer shall be viewed as performing artist

d. A variety artist shall be viewed as performing artist

e. A dancer and circus performer shall be viewed as performing artist

On assuming in the present context that the expenditure are connected to work of makeup

and dresses of the performing artist then those kind of expenses can be viewed as deductions

in ascertaining the chargeable revenue of the performing artist (Dunne et al., 2016).

Answer to Issue (IX):

As a general rule, travel by a person from the place of work to home is viewed as

private travel but there exists a specific provision where allowable deductions can be claimed

for such kind of travelling expenditure (Anderson et al., 2016). If the expenses incurred is for

official use and in cases where the expenditure are partially for the purpose of office and

partly for private purpose then those kind of expenditure will not be regarded as official

travel for claiming allowable deductions. In respect of the current situation, it can be

understood that the travel expenditure was for the purpose of work and the expenditure

incurred can be claimed as allowable deductions in deterring the assessable income of the

taxpayer.

Answer to Issue (X):

Expenses that are occurred for travelling between two work places are usually

regarded as deductions (Tan et al., 2016). Henceforth, in the current circumstances expenses

occurred on travelling between two employers will not be viewed as allowable deductions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

This is due to the fact that deductions cannot be considered as allowable deductions from

travelling between two different employers.

Answer to question 2:

To work out the taxable circumstances of a person, it is necessary to assess the residential

status for the purpose of tax. A student from overseas country enrolled in a course that has the

duration of more than six months in Australian institutions will be regarded as the Australian

resident for the purpose of taxation (Tran-Nam & Walpole, 2016). From the present scenario

of Manpreet, it can be considered that he is an Australian resident for the taxation purpose

because he is enrolled in a course that has more than six months of duration in an Australian

institute. Furthermore, Manpreet even worked as the part time office assistant in an

Australian firm for a monthly salary of $45,000.

As evident from the case study it is found that Manpreet incurred several educational

expenses that cannot be viewed as allowable deductions. As evident Manpreet incurred self-

education expenses of $18,000 that cannot be allowed as permissible deductions. A person

can claim for deductions for any kind of self-education if their course is linked with work or

if a person receives a taxable bonded scholarship (James, 2016). It should be understood that

the course should have appropriate relation with the current employment and;

a. Improve or maintain the required skills or knowledge which a person is required to

have in their current employment (Russell, 2016).

b. Lead to, or it is almost certainly leading to an increase in the income from their

current employment

A person will not be entitled to claim deductions for the self-education purpose for a

course that is not have appropriate connection with their current employment yet it;

This is due to the fact that deductions cannot be considered as allowable deductions from

travelling between two different employers.

Answer to question 2:

To work out the taxable circumstances of a person, it is necessary to assess the residential

status for the purpose of tax. A student from overseas country enrolled in a course that has the

duration of more than six months in Australian institutions will be regarded as the Australian

resident for the purpose of taxation (Tran-Nam & Walpole, 2016). From the present scenario

of Manpreet, it can be considered that he is an Australian resident for the taxation purpose

because he is enrolled in a course that has more than six months of duration in an Australian

institute. Furthermore, Manpreet even worked as the part time office assistant in an

Australian firm for a monthly salary of $45,000.

As evident from the case study it is found that Manpreet incurred several educational

expenses that cannot be viewed as allowable deductions. As evident Manpreet incurred self-

education expenses of $18,000 that cannot be allowed as permissible deductions. A person

can claim for deductions for any kind of self-education if their course is linked with work or

if a person receives a taxable bonded scholarship (James, 2016). It should be understood that

the course should have appropriate relation with the current employment and;

a. Improve or maintain the required skills or knowledge which a person is required to

have in their current employment (Russell, 2016).

b. Lead to, or it is almost certainly leading to an increase in the income from their

current employment

A person will not be entitled to claim deductions for the self-education purpose for a

course that is not have appropriate connection with their current employment yet it;

8TAXATION LAW

a. Might be generally connected to it; or

b. Offers a person with the opportunity of gaining new employment

Section 8-1 of the Income Tax Assessment Act 1997, defines that expenses are

considered as allowable deductions if there is an appropriate link with the income generating

activities (Richardson et al., 2014). It should become a necessary feature of work and should

not constitute in the nature of personal or domestic. Citing the reference of Lunney v. FC of

T; Hayley v. FC of T (1958) 100 CLR 478; (1958) for an expenses to qualify under the

section 8-1 of the ITAA 1997 it must hold the necessary feature of outgoing in nature in

producing the taxable income or represents an income producing expenses (Nyst & McAdam,

2014).

The point of view is supported in the case of Ronpibon Tin NL v. FC of T (1949)

where the income must satisfy the necessary relation between the outgoing and the taxable

income in order to satisfy that the outgoing is accompanying and it is vital in gaining the

taxable income (Xynas et al., 2014). The expenses occurred on self education by Manpreet

will not be allowable as deductions. This is because the expenditure is incurred to gain a new

employment or to open the new employment opportunity.

Manpreet at the same time incurred expenses on printer and computer and also on

new mobile phone that was for work purpose. As defined under the section 8-1 of the ITAA

1997 expenses are viewed as allowable deductions where there is an appropriate connection

between the expenses and the income producing ability, such that is holds the necessary

feature of work and not private or domestic in nature (Edmonds et al., 2015). It is noteworthy

to denote that expenditure are regarded as perquisite in producing the taxable income. The

expenditure must be relevant and subsidiary to the activities that results in producing the

income.

a. Might be generally connected to it; or

b. Offers a person with the opportunity of gaining new employment

Section 8-1 of the Income Tax Assessment Act 1997, defines that expenses are

considered as allowable deductions if there is an appropriate link with the income generating

activities (Richardson et al., 2014). It should become a necessary feature of work and should

not constitute in the nature of personal or domestic. Citing the reference of Lunney v. FC of

T; Hayley v. FC of T (1958) 100 CLR 478; (1958) for an expenses to qualify under the

section 8-1 of the ITAA 1997 it must hold the necessary feature of outgoing in nature in

producing the taxable income or represents an income producing expenses (Nyst & McAdam,

2014).

The point of view is supported in the case of Ronpibon Tin NL v. FC of T (1949)

where the income must satisfy the necessary relation between the outgoing and the taxable

income in order to satisfy that the outgoing is accompanying and it is vital in gaining the

taxable income (Xynas et al., 2014). The expenses occurred on self education by Manpreet

will not be allowable as deductions. This is because the expenditure is incurred to gain a new

employment or to open the new employment opportunity.

Manpreet at the same time incurred expenses on printer and computer and also on

new mobile phone that was for work purpose. As defined under the section 8-1 of the ITAA

1997 expenses are viewed as allowable deductions where there is an appropriate connection

between the expenses and the income producing ability, such that is holds the necessary

feature of work and not private or domestic in nature (Edmonds et al., 2015). It is noteworthy

to denote that expenditure are regarded as perquisite in producing the taxable income. The

expenditure must be relevant and subsidiary to the activities that results in producing the

income.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

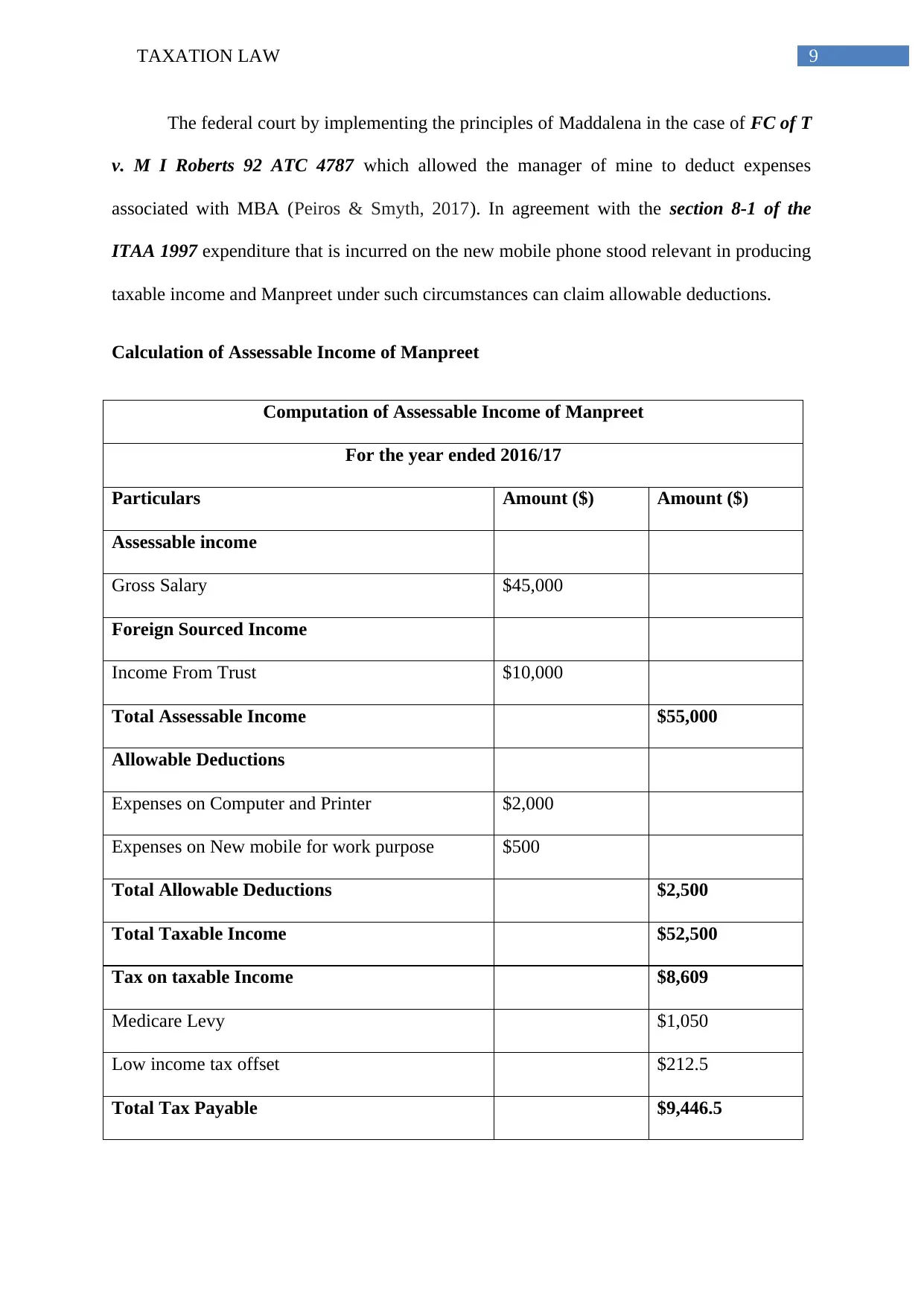

The federal court by implementing the principles of Maddalena in the case of FC of T

v. M I Roberts 92 ATC 4787 which allowed the manager of mine to deduct expenses

associated with MBA (Peiros & Smyth, 2017). In agreement with the section 8-1 of the

ITAA 1997 expenditure that is incurred on the new mobile phone stood relevant in producing

taxable income and Manpreet under such circumstances can claim allowable deductions.

Calculation of Assessable Income of Manpreet

Computation of Assessable Income of Manpreet

For the year ended 2016/17

Particulars Amount ($) Amount ($)

Assessable income

Gross Salary $45,000

Foreign Sourced Income

Income From Trust $10,000

Total Assessable Income $55,000

Allowable Deductions

Expenses on Computer and Printer $2,000

Expenses on New mobile for work purpose $500

Total Allowable Deductions $2,500

Total Taxable Income $52,500

Tax on taxable Income $8,609

Medicare Levy $1,050

Low income tax offset $212.5

Total Tax Payable $9,446.5

The federal court by implementing the principles of Maddalena in the case of FC of T

v. M I Roberts 92 ATC 4787 which allowed the manager of mine to deduct expenses

associated with MBA (Peiros & Smyth, 2017). In agreement with the section 8-1 of the

ITAA 1997 expenditure that is incurred on the new mobile phone stood relevant in producing

taxable income and Manpreet under such circumstances can claim allowable deductions.

Calculation of Assessable Income of Manpreet

Computation of Assessable Income of Manpreet

For the year ended 2016/17

Particulars Amount ($) Amount ($)

Assessable income

Gross Salary $45,000

Foreign Sourced Income

Income From Trust $10,000

Total Assessable Income $55,000

Allowable Deductions

Expenses on Computer and Printer $2,000

Expenses on New mobile for work purpose $500

Total Allowable Deductions $2,500

Total Taxable Income $52,500

Tax on taxable Income $8,609

Medicare Levy $1,050

Low income tax offset $212.5

Total Tax Payable $9,446.5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

11TAXATION LAW

Reference List:

Pinto, D. (2013). State taxes. In Australian Taxation Law (pp. 1763-1762). CCH Australia

Limited.

Barkoczy, S. (2016). Foundations of Taxation Law 2016. OUP Catalogue.

Snape, J., & De Souza, J. (2016). Environmental taxation law: policy, contexts and practice.

Routledge.

Braithwaite, V. (Ed.). (2017). Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., ... & Wende, S.

(2015). Understanding the economy-wide efficiency and incidence of major Australian

taxes. Treasury WP, 1.

Saad, N. (2014). Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, 1069-1075.

ROBIN, H. (2017). AUSTRALIAN TAXATION LAW 2017. OXFORD University Press.

Blakelock, S., & King, P. (2017). Taxation law: The advance of ATO data matching. Proctor,

The, 37(6), 18.

Vann, R. J. (2016). Hybrid Entities in Australia: Resource Capital Fund III LP Case.

Anderson, C., Dickfos, J., & Brown, C. (2016). The Australian Taxation Office-what role

does it play in anti-phoenix activity?. INSOLVENCY LAW JOURNAL, 24(2), 127-140.

Reference List:

Pinto, D. (2013). State taxes. In Australian Taxation Law (pp. 1763-1762). CCH Australia

Limited.

Barkoczy, S. (2016). Foundations of Taxation Law 2016. OUP Catalogue.

Snape, J., & De Souza, J. (2016). Environmental taxation law: policy, contexts and practice.

Routledge.

Braithwaite, V. (Ed.). (2017). Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., ... & Wende, S.

(2015). Understanding the economy-wide efficiency and incidence of major Australian

taxes. Treasury WP, 1.

Saad, N. (2014). Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, 1069-1075.

ROBIN, H. (2017). AUSTRALIAN TAXATION LAW 2017. OXFORD University Press.

Blakelock, S., & King, P. (2017). Taxation law: The advance of ATO data matching. Proctor,

The, 37(6), 18.

Vann, R. J. (2016). Hybrid Entities in Australia: Resource Capital Fund III LP Case.

Anderson, C., Dickfos, J., & Brown, C. (2016). The Australian Taxation Office-what role

does it play in anti-phoenix activity?. INSOLVENCY LAW JOURNAL, 24(2), 127-140.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.