Taxation Law: Deductions, Assessable Income, and Tax Implications

VerifiedAdded on 2020/02/24

|13

|2133

|338

Homework Assignment

AI Summary

This taxation law assignment provides a comprehensive analysis of various tax scenarios under Australian law. The document examines the treatment of frequent flier benefits, compensation for damaged capital assets, gifts, additional funds, and income from sports. It also addresses deductions for construction expenses, short-term art courses, performing artists' expenses, and travel expenses. The assignment further explores the tax implications for an individual, Manpreet, focusing on assessable income, self-education expenses, and the deductibility of work-related expenses such as computer, printer, and phone costs. The solution references relevant taxation rulings and legislation to support its conclusions. Overall, the assignment provides a thorough understanding of key taxation concepts and their application in real-world scenarios.

Running head: TAXATION LAW

Taxation law

Name of the student

Name of the university

Author note

Taxation law

Name of the student

Name of the university

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer I.................................................................................................................................2

Answer II................................................................................................................................2

Answer III..............................................................................................................................3

Answer IV..............................................................................................................................3

Answer V...............................................................................................................................4

Answer VI..............................................................................................................................4

Answer VII.............................................................................................................................5

Answer VIII...........................................................................................................................5

Answer IX..............................................................................................................................6

Answer X...............................................................................................................................6

Answer 2....................................................................................................................................7

References................................................................................................................................10

Table of Contents

Answer I.................................................................................................................................2

Answer II................................................................................................................................2

Answer III..............................................................................................................................3

Answer IV..............................................................................................................................3

Answer V...............................................................................................................................4

Answer VI..............................................................................................................................4

Answer VII.............................................................................................................................5

Answer VIII...........................................................................................................................5

Answer IX..............................................................................................................................6

Answer X...............................................................................................................................6

Answer 2....................................................................................................................................7

References................................................................................................................................10

2TAXATION LAW

Answer I

Under Taxation Ruling under TR 1996/6, benefits accrue under the standard program

of frequent flier are not added with the assessable income of the member as the benefits

accrue from the personal relationship that is contractual that is not the productive under the

assessable income. The deductions is subjected to the following provisions –

The membership is restricted exclusively for the natural persons

Points can be redeemed only for services or goods1

However, as per the ruling, the amount shall be treated and will be taxable as Fringe

benefit tax if the following conditions are satisfied –

The employees are entitled to the rewards owing to some special arrangements

The employer and employee is related as family member and he is entitled to the

point owing to his employment with the airline company

As per the given situation the employees are getting the points with regard to their

employment with the company and therefore the amount will be treated as business expense

for the employer. Therefore, the reward points received by the employees will be allowed for

deduction as it will not come under fringe benefit tax

Answer II

Compensation paid on account of damaging the capital asset of the service provider

the amount will not be added to the assessable income of the service provider who will

receive the amount. However, the received amount to be qualified as deduction some specific

conditions are required to be met. These conditions are –

1 Chartered Accountants Australia & New Zealand (2017) CAANZ https://www.charteredaccountantsanz.com/

Answer I

Under Taxation Ruling under TR 1996/6, benefits accrue under the standard program

of frequent flier are not added with the assessable income of the member as the benefits

accrue from the personal relationship that is contractual that is not the productive under the

assessable income. The deductions is subjected to the following provisions –

The membership is restricted exclusively for the natural persons

Points can be redeemed only for services or goods1

However, as per the ruling, the amount shall be treated and will be taxable as Fringe

benefit tax if the following conditions are satisfied –

The employees are entitled to the rewards owing to some special arrangements

The employer and employee is related as family member and he is entitled to the

point owing to his employment with the airline company

As per the given situation the employees are getting the points with regard to their

employment with the company and therefore the amount will be treated as business expense

for the employer. Therefore, the reward points received by the employees will be allowed for

deduction as it will not come under fringe benefit tax

Answer II

Compensation paid on account of damaging the capital asset of the service provider

the amount will not be added to the assessable income of the service provider who will

receive the amount. However, the received amount to be qualified as deduction some specific

conditions are required to be met. These conditions are –

1 Chartered Accountants Australia & New Zealand (2017) CAANZ https://www.charteredaccountantsanz.com/

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

The asset offered for providing service shall be of capital nature and exclusively used

by the service provider for business purpose only

Depreciation must be provided for the asset and the depreciation must be recorded in

the books of accounts

The amount received for damage must be used solely for repairing the part that was

damaged2

The asset must be damaged during the time period under which the asset was using

for providing the service

From the above discussion, it can be concluded that the amount received by crane

Hire Company on account of damage of their asset shall not be included as assessable income

for tax if the above mentions conditions are satisfied.

Answer III

As per TR 1999/10, Para 71 to 78, gifts received by any person will not form part of

the assessable income for tax if the gift is received due to personal reasons and it is no way

connected with the person’s work related activities. However, if the gift is received with

respect to or in consideration with the work-related activities of the person, the gift will be

added under the assessable income for tax. Further, the gift can be transformed into money or

kind or cash, however the assessable nature of gift will not alter3. Therefore, holiday package

offered by alcohol supplier to the night club manager will be treated as income under the

assessable income for tax.

2 CPA Australia (2017) Cpaaustralia.com.au https://www.cpaaustralia.com.au/

3 Karin Simon, Sara McDonald, Accident Investigation - Databases - Library Guides At Cquniversity (2017)

Libguides.library.cqu.edu.au http://libguides.library.cqu.edu.au/content.php?pid=166733&sid=2668174

The asset offered for providing service shall be of capital nature and exclusively used

by the service provider for business purpose only

Depreciation must be provided for the asset and the depreciation must be recorded in

the books of accounts

The amount received for damage must be used solely for repairing the part that was

damaged2

The asset must be damaged during the time period under which the asset was using

for providing the service

From the above discussion, it can be concluded that the amount received by crane

Hire Company on account of damage of their asset shall not be included as assessable income

for tax if the above mentions conditions are satisfied.

Answer III

As per TR 1999/10, Para 71 to 78, gifts received by any person will not form part of

the assessable income for tax if the gift is received due to personal reasons and it is no way

connected with the person’s work related activities. However, if the gift is received with

respect to or in consideration with the work-related activities of the person, the gift will be

added under the assessable income for tax. Further, the gift can be transformed into money or

kind or cash, however the assessable nature of gift will not alter3. Therefore, holiday package

offered by alcohol supplier to the night club manager will be treated as income under the

assessable income for tax.

2 CPA Australia (2017) Cpaaustralia.com.au https://www.cpaaustralia.com.au/

3 Karin Simon, Sara McDonald, Accident Investigation - Databases - Library Guides At Cquniversity (2017)

Libguides.library.cqu.edu.au http://libguides.library.cqu.edu.au/content.php?pid=166733&sid=2668174

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Answer IV

Additional fund if raised and then returned to the persons from whom the money were

received will not be treated as taxable in the hand of the recipient as the amount were raised

for a specific purpose and it was never been the income in hands of the receiver. It is just the

error in forecasting the requirement4. Therefore, extra amount raised from purchasing

additional canoes that were subsequently returned to the members will not be treated as

income.

Answer V

Any amount received by any sportsman on account of his involvement in any sport

will be treated as income for the purpose of calculating the assessable income. Here in the

given case the Australian sportsman received money from a television channel for performing

as the best and the fairest player in AFL5. As per the TR 1999/17 of Taxation ruling, the

amount will not be qualified for deduction and will be included under income as the money

received in connection with the sports.

Answer VI

When the employer incurs any expenses with regard to construction of the apprentice

or trainees, the amount will be qualified as deduction. The TR 95/22 of Taxation ruling deals

with the treatment of reimbursement and allowance by the employer for building the

4 Taylor, Grantley, and Grant Richardson. "The determinants of thinly capitalized tax avoidance structures:

Evidence from Australian firms." Journal of International Accounting, Auditing and Taxation 22.1 (2013): 12-

25.

5 Cao, Liangyue, et al. "Understanding the economy-wide efficiency and incidence of major Australian

taxes." Treasury WP 1 (2015).

Answer IV

Additional fund if raised and then returned to the persons from whom the money were

received will not be treated as taxable in the hand of the recipient as the amount were raised

for a specific purpose and it was never been the income in hands of the receiver. It is just the

error in forecasting the requirement4. Therefore, extra amount raised from purchasing

additional canoes that were subsequently returned to the members will not be treated as

income.

Answer V

Any amount received by any sportsman on account of his involvement in any sport

will be treated as income for the purpose of calculating the assessable income. Here in the

given case the Australian sportsman received money from a television channel for performing

as the best and the fairest player in AFL5. As per the TR 1999/17 of Taxation ruling, the

amount will not be qualified for deduction and will be included under income as the money

received in connection with the sports.

Answer VI

When the employer incurs any expenses with regard to construction of the apprentice

or trainees, the amount will be qualified as deduction. The TR 95/22 of Taxation ruling deals

with the treatment of reimbursement and allowance by the employer for building the

4 Taylor, Grantley, and Grant Richardson. "The determinants of thinly capitalized tax avoidance structures:

Evidence from Australian firms." Journal of International Accounting, Auditing and Taxation 22.1 (2013): 12-

25.

5 Cao, Liangyue, et al. "Understanding the economy-wide efficiency and incidence of major Australian

taxes." Treasury WP 1 (2015).

5TAXATION LAW

employees. However, the below mentioned persons will be regarded as building of the

employees –

Trainees, carpenter and apprentice

Overseer or the project administrator for any under construction building

Labours who are engaged for building construction

The project administrator or supervisor engaged under the site of construction

Therefore, expenses with regard to construction of qualification or the apprentice will

be considered as construction of the employees and thus will be qualified for deduction.

Answer VII

While the taxable income is calculated some specific expenses that are spend for the

purpose of undertaking any short-term course related to art the amount will be qualified for

deduction. However, the deduction allowance is limited with the following conditions –

Any expenses required to be incurred on food

Training cost incurred for various modules and software

Course fee paid for undertaking the course

Cost spend for going to and coming back from the institution

Further, the above mentioned cost will be allowed if and only if the expenses incurred

for the course exclusively. Moreover, if out of the total expenses only a part is spend for the

course, that part only will be considered for deduction. In absence of sufficient information, it

is assumed that the expenses incurred for the course only and will therefore be allowed for

deduction.

employees. However, the below mentioned persons will be regarded as building of the

employees –

Trainees, carpenter and apprentice

Overseer or the project administrator for any under construction building

Labours who are engaged for building construction

The project administrator or supervisor engaged under the site of construction

Therefore, expenses with regard to construction of qualification or the apprentice will

be considered as construction of the employees and thus will be qualified for deduction.

Answer VII

While the taxable income is calculated some specific expenses that are spend for the

purpose of undertaking any short-term course related to art the amount will be qualified for

deduction. However, the deduction allowance is limited with the following conditions –

Any expenses required to be incurred on food

Training cost incurred for various modules and software

Course fee paid for undertaking the course

Cost spend for going to and coming back from the institution

Further, the above mentioned cost will be allowed if and only if the expenses incurred

for the course exclusively. Moreover, if out of the total expenses only a part is spend for the

course, that part only will be considered for deduction. In absence of sufficient information, it

is assumed that the expenses incurred for the course only and will therefore be allowed for

deduction.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Answer VIII

The expenses in association with the performing of an artist will be allowed as

deduction under the ATO ruling provided the expenses incurred by the person can be

considered as performing artist. ATO mentioned following persons as performing artist –

The musician who performs music will be considered as performing artist

The actor who acts will be considered as performing artist

The singer who sings will be considered as performing artist

A person who dance will be considered as performing artist

A person who performs in circus will be considered as performing artist

In absence of sufficient information, it will be assumed that the expenses are incurred

with regard to the performing artist’s dresses and make-up and therefore will be allowed as

deduction.

Answer IX

As per the Australian Tax Office the amount of expenses incurred for going to the

office and coming back from the office is not allowed as deduction. However, the amount is

allowed for deduction if the expenditure is incurred solely for travelling for official

purposes6. Further, if out of the total expenses only a part is spend for the office purpose

travel, that part only will be considered for deduction. In absence of sufficient information, it

will be assumed that the expenses are incurred with regard to the travelling of official

purpose and therefore will be allowed as deduction.

6 Berg, Chris, and Sinclair Davidson. "Submission to the House of Representatives Standing Committee on Tax

and Revenue Inquiry into the External Scrutiny of the Australian Taxation Office." (2016).

Answer VIII

The expenses in association with the performing of an artist will be allowed as

deduction under the ATO ruling provided the expenses incurred by the person can be

considered as performing artist. ATO mentioned following persons as performing artist –

The musician who performs music will be considered as performing artist

The actor who acts will be considered as performing artist

The singer who sings will be considered as performing artist

A person who dance will be considered as performing artist

A person who performs in circus will be considered as performing artist

In absence of sufficient information, it will be assumed that the expenses are incurred

with regard to the performing artist’s dresses and make-up and therefore will be allowed as

deduction.

Answer IX

As per the Australian Tax Office the amount of expenses incurred for going to the

office and coming back from the office is not allowed as deduction. However, the amount is

allowed for deduction if the expenditure is incurred solely for travelling for official

purposes6. Further, if out of the total expenses only a part is spend for the office purpose

travel, that part only will be considered for deduction. In absence of sufficient information, it

will be assumed that the expenses are incurred with regard to the travelling of official

purpose and therefore will be allowed as deduction.

6 Berg, Chris, and Sinclair Davidson. "Submission to the House of Representatives Standing Committee on Tax

and Revenue Inquiry into the External Scrutiny of the Australian Taxation Office." (2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Answer X

The amounts of travelling expenses are allowed for deduction if the expenditure is

incurred solely for travelling for official purposes. Further, deduction is allowable for

travelling to two workplaces, provided both the workplaces are under the control of one

employer7. Therefore, in the present situation, travelling to tow workplaces will not be

allowed as deduction as the two workplaces belong to two different employers.

7 Woellner, R. H., et al. Australian Taxation Law Select: Legislation and Commentary 2016. Oxford University

Press, 2016.

Answer X

The amounts of travelling expenses are allowed for deduction if the expenditure is

incurred solely for travelling for official purposes. Further, deduction is allowable for

travelling to two workplaces, provided both the workplaces are under the control of one

employer7. Therefore, in the present situation, travelling to tow workplaces will not be

allowed as deduction as the two workplaces belong to two different employers.

7 Woellner, R. H., et al. Australian Taxation Law Select: Legislation and Commentary 2016. Oxford University

Press, 2016.

8TAXATION LAW

Answer 2

The taxable scenario of an individual is determined on the basis of the nature of the

citizenship of an individual that is whether the concerned individual is foreign resident or

Australian. For taxation purpose, a foreign student, enrolled in any Australian institution’s

course, of more than six months duration, is considered tobe a resident of the country. In this

context, Manpreet also will e considered as an Australian resident. Manpreet had a part time

job as an office assistant in an Australian firm, with a salary of $45000 per month. The self-

educational expenses, which are of worth o $18000 cannot be allowed for deductions, as

deductions can only be claimed in this context, if the concerned individual gets a bonded

scholarship which is taxable. The courses, in this case should be related to the current

employment and:

Lead to or is expected to lead to an increase in the income of the individual from the

present employment.

Improve or at least maintain the level of necessary knowledge and skills that the

individual needs to have in the current employment8.

Deductions cannot be claimed by the individuals, for expenses on self –education for

a course with no substantial connection to the current employment of the individual even

though the course:

May allow the individual to get new job, or,

Maybe associated in general with it.

8 Blakelock, Sarah, and Peter King. "Taxation law: The advance of ATO data matching." Proctor, The 37.6

(2017): 18.

Answer 2

The taxable scenario of an individual is determined on the basis of the nature of the

citizenship of an individual that is whether the concerned individual is foreign resident or

Australian. For taxation purpose, a foreign student, enrolled in any Australian institution’s

course, of more than six months duration, is considered tobe a resident of the country. In this

context, Manpreet also will e considered as an Australian resident. Manpreet had a part time

job as an office assistant in an Australian firm, with a salary of $45000 per month. The self-

educational expenses, which are of worth o $18000 cannot be allowed for deductions, as

deductions can only be claimed in this context, if the concerned individual gets a bonded

scholarship which is taxable. The courses, in this case should be related to the current

employment and:

Lead to or is expected to lead to an increase in the income of the individual from the

present employment.

Improve or at least maintain the level of necessary knowledge and skills that the

individual needs to have in the current employment8.

Deductions cannot be claimed by the individuals, for expenses on self –education for

a course with no substantial connection to the current employment of the individual even

though the course:

May allow the individual to get new job, or,

Maybe associated in general with it.

8 Blakelock, Sarah, and Peter King. "Taxation law: The advance of ATO data matching." Proctor, The 37.6

(2017): 18.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

As stated in Lunney v. FC of T; Hayley v. FC of T (1958) 100 CLR 478; (1958), to

meet test under section 8-1 of the ITAA 1997, an expenditure should mandatorily have the

characteristic of an outgoing one, which is incurred to gain accessible income. As held under

section 8-1 of the ITAA 1997 for an expenditure to be deductible, there should be adequate

relation between the activities that generate income and the expenses, such that its feature is

not domestic in nature and is related to the work9.

Ronpibon Tin NL v. FC of T (1949) supports this, where it is stated that there should

be a nexus between taxable and outgoing income such that outgoing is important to gain an

accessible income. Deduction for self-education expenditures are not allowed if the course

helps in opening up new avenues for employment or income generating activity. This implies

that the expenses of Manpreet shall not be allowed for deductions.

The expense should not only be considered as a pre-requirement for generation of

assessable income, they should also have relevance to the activities resulting in generation of

income. Manpreet has incurred expenses on computer, printer and a new phone, which is

related to her work purpose10. This can be considered under section 8-1 of the ITAA 1997,

where a sufficient nexus is present between the income generating capacity and the expenses,

such that it has the characteristics of work essentially. Referring to section 8-1 of the ITAA

1997 the expenses on new phone is relevant t gain assessable income which implies Manpreet

is allowed to claim deductions. The FC of T v. M I Roberts 92 ATC 4787 shows that by the

principles of Maddalena, the federal court gave allowance to deduct MBA related

expenditure to a mine manager.

9 The Tax Institute (2017) Taxinstitute.com.au https://www.taxinstitute.com.au/

10 Ato.Gov.Au/ (2017) Ato.gov.au https://www.ato.gov.au/

As stated in Lunney v. FC of T; Hayley v. FC of T (1958) 100 CLR 478; (1958), to

meet test under section 8-1 of the ITAA 1997, an expenditure should mandatorily have the

characteristic of an outgoing one, which is incurred to gain accessible income. As held under

section 8-1 of the ITAA 1997 for an expenditure to be deductible, there should be adequate

relation between the activities that generate income and the expenses, such that its feature is

not domestic in nature and is related to the work9.

Ronpibon Tin NL v. FC of T (1949) supports this, where it is stated that there should

be a nexus between taxable and outgoing income such that outgoing is important to gain an

accessible income. Deduction for self-education expenditures are not allowed if the course

helps in opening up new avenues for employment or income generating activity. This implies

that the expenses of Manpreet shall not be allowed for deductions.

The expense should not only be considered as a pre-requirement for generation of

assessable income, they should also have relevance to the activities resulting in generation of

income. Manpreet has incurred expenses on computer, printer and a new phone, which is

related to her work purpose10. This can be considered under section 8-1 of the ITAA 1997,

where a sufficient nexus is present between the income generating capacity and the expenses,

such that it has the characteristics of work essentially. Referring to section 8-1 of the ITAA

1997 the expenses on new phone is relevant t gain assessable income which implies Manpreet

is allowed to claim deductions. The FC of T v. M I Roberts 92 ATC 4787 shows that by the

principles of Maddalena, the federal court gave allowance to deduct MBA related

expenditure to a mine manager.

9 The Tax Institute (2017) Taxinstitute.com.au https://www.taxinstitute.com.au/

10 Ato.Gov.Au/ (2017) Ato.gov.au https://www.ato.gov.au/

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

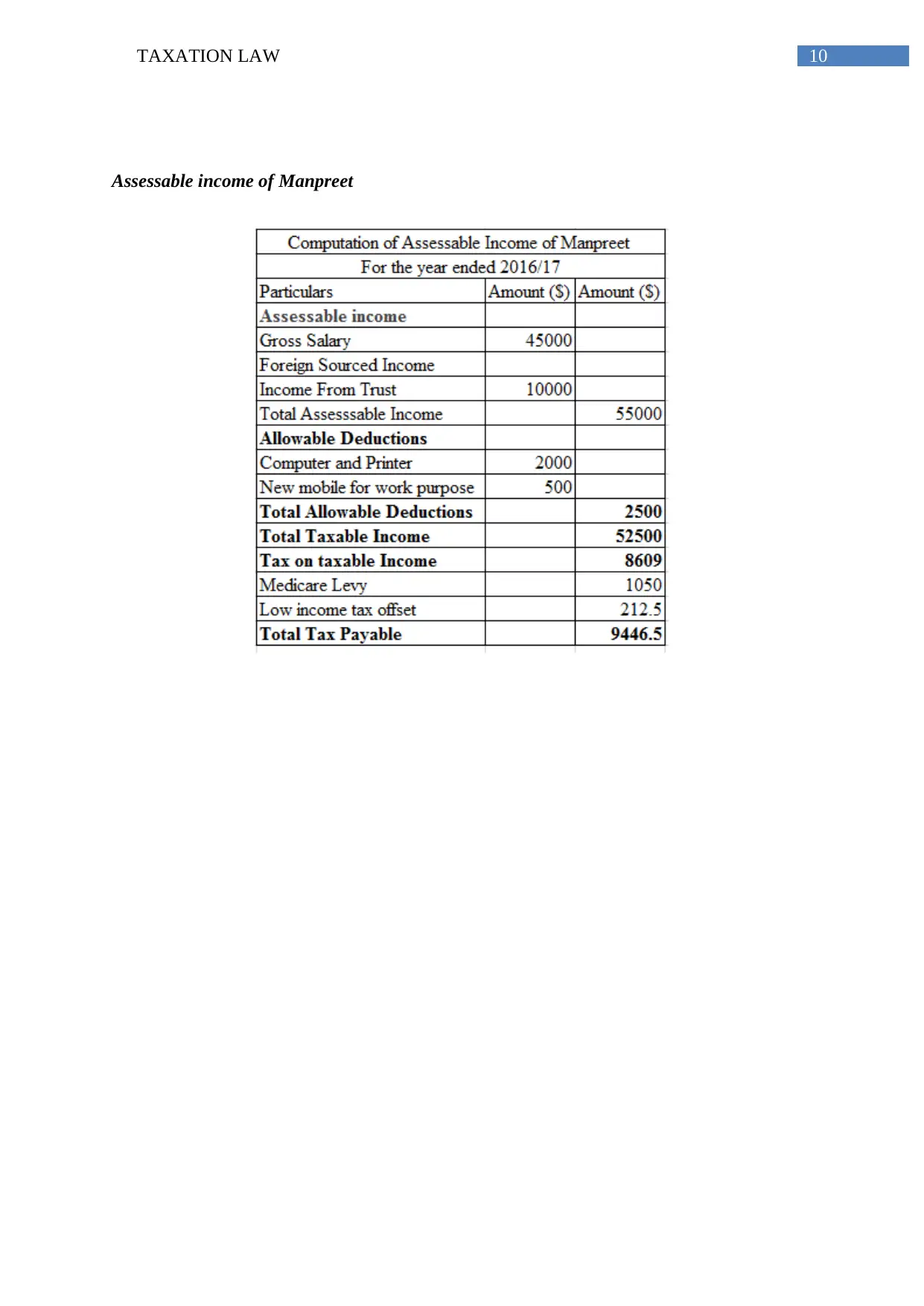

Assessable income of Manpreet

Assessable income of Manpreet

11TAXATION LAW

References

Ato.Gov.Au/ (2017) Ato.gov.au https://www.ato.gov.au/

Berg, Chris, and Sinclair Davidson. "Submission to the House of Representatives Standing

Committee on Tax and Revenue Inquiry into the External Scrutiny of the Australian Taxation

Office." (2016).

Blakelock, Sarah, and Peter King. "Taxation law: The advance of ATO data

matching." Proctor, The 37.6 (2017): 18.

Cao, Liangyue, et al. "Understanding the economy-wide efficiency and incidence of major

Australian taxes." Treasury WP 1 (2015).

Chartered Accountants Australia & New Zealand (2017) CAANZ

https://www.charteredaccountantsanz.com/

CPA Australia (2017) Cpaaustralia.com.au https://www.cpaaustralia.com.au/

Karin Simon, Sara McDonald, Accident Investigation - Databases - Library Guides At

Cquniversity (2017) Libguides.library.cqu.edu.au

http://libguides.library.cqu.edu.au/content.php?pid=166733&sid=2668174

Taylor, Grantley, and Grant Richardson. "The determinants of thinly capitalized tax

avoidance structures: Evidence from Australian firms." Journal of International Accounting,

Auditing and Taxation 22.1 (2013): 12-25.

The Tax Institute (2017) Taxinstitute.com.au https://www.taxinstitute.com.au/

Woellner, R. H., et al. Australian Taxation Law Select: Legislation and Commentary 2016.

Oxford University Press, 2016.

References

Ato.Gov.Au/ (2017) Ato.gov.au https://www.ato.gov.au/

Berg, Chris, and Sinclair Davidson. "Submission to the House of Representatives Standing

Committee on Tax and Revenue Inquiry into the External Scrutiny of the Australian Taxation

Office." (2016).

Blakelock, Sarah, and Peter King. "Taxation law: The advance of ATO data

matching." Proctor, The 37.6 (2017): 18.

Cao, Liangyue, et al. "Understanding the economy-wide efficiency and incidence of major

Australian taxes." Treasury WP 1 (2015).

Chartered Accountants Australia & New Zealand (2017) CAANZ

https://www.charteredaccountantsanz.com/

CPA Australia (2017) Cpaaustralia.com.au https://www.cpaaustralia.com.au/

Karin Simon, Sara McDonald, Accident Investigation - Databases - Library Guides At

Cquniversity (2017) Libguides.library.cqu.edu.au

http://libguides.library.cqu.edu.au/content.php?pid=166733&sid=2668174

Taylor, Grantley, and Grant Richardson. "The determinants of thinly capitalized tax

avoidance structures: Evidence from Australian firms." Journal of International Accounting,

Auditing and Taxation 22.1 (2013): 12-25.

The Tax Institute (2017) Taxinstitute.com.au https://www.taxinstitute.com.au/

Woellner, R. H., et al. Australian Taxation Law Select: Legislation and Commentary 2016.

Oxford University Press, 2016.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.