Detailed Analysis of Australian Taxation Law Assignment, Semester 2

VerifiedAdded on 2020/03/04

|13

|2189

|45

Homework Assignment

AI Summary

This document presents a comprehensive solution to an Australian taxation law assignment. The solution addresses various scenarios, including frequent flier programs, compensation for damaged assets, gifts related to employment, and the tax implications of awards and reimbursements. It covers aspects like assessable income, deductions, and the application of relevant tax rulings, such as TR 1999/6 and TR 1999/10. The assignment also analyzes the tax treatment of self-education expenses, expenses related to performing assets, and travel expenses. Additionally, the solution examines the tax residency of an overseas student and the deductibility of work-related expenses, referencing relevant case law and legislation like ITAA 1997. The assignment demonstrates a strong understanding of Australian taxation principles and their practical application. The document also includes a detailed reference list of sources used in the preparation of the assignment.

Running head: TAXATION LAW OF AUSTRALIA

Taxation law of Australia

Name of the student

Name of the university

Author note

Taxation law of Australia

Name of the student

Name of the university

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW OF AUSTRALIA

Table of Contents

Answer 1....................................................................................................................................2

Answer to question I..................................................................................................................2

Answer to question II.................................................................................................................2

Answer to question III................................................................................................................3

Answer to question IV...............................................................................................................4

Answer to question V.................................................................................................................4

Answer to question VI...............................................................................................................5

Answer to question VII..............................................................................................................5

Answer to question VIII.............................................................................................................6

Answer to question IX...............................................................................................................7

Answer to question X.................................................................................................................7

Answer 2....................................................................................................................................8

References................................................................................................................................11

Table of Contents

Answer 1....................................................................................................................................2

Answer to question I..................................................................................................................2

Answer to question II.................................................................................................................2

Answer to question III................................................................................................................3

Answer to question IV...............................................................................................................4

Answer to question V.................................................................................................................4

Answer to question VI...............................................................................................................5

Answer to question VII..............................................................................................................5

Answer to question VIII.............................................................................................................6

Answer to question IX...............................................................................................................7

Answer to question X.................................................................................................................7

Answer 2....................................................................................................................................8

References................................................................................................................................11

2TAXATION LAW OF AUSTRALIA

Answer 1

Answer to question I

As per the TR 19996/6 of the Australian taxation ruling, if any person is benefitted

through the rewards or points under frequent flier standard program, the amount of benefit

will be qualified for deduction and will not be included under the assessable income of the

recipient. However, to get the qualification for deductions, the following conditions must be

satisfied –

The shall be provided exclusively for goods or services

Only the natural persons are entitled to the membership

On the contrary, the amount of benefit can be included under the fringe benefit tax if –

The employee got the reward under special arrangement rather than getting it as

general entitlement

There exists a family relationship among the employer and employee and the point

was allocated owing to that relationship

In the given circumstance, the employees were rewarded with the points only for their

association with Webjet as employees and therefore, the reward points shall be qualified for

deduction and the expenses will be allowable expense for the employer.

Answer to question II

If the service provider receives any compensation for the damage of his asset while

the asset was under use by the service recipient, the compensation amount will not be taxed

Answer 1

Answer to question I

As per the TR 19996/6 of the Australian taxation ruling, if any person is benefitted

through the rewards or points under frequent flier standard program, the amount of benefit

will be qualified for deduction and will not be included under the assessable income of the

recipient. However, to get the qualification for deductions, the following conditions must be

satisfied –

The shall be provided exclusively for goods or services

Only the natural persons are entitled to the membership

On the contrary, the amount of benefit can be included under the fringe benefit tax if –

The employee got the reward under special arrangement rather than getting it as

general entitlement

There exists a family relationship among the employer and employee and the point

was allocated owing to that relationship

In the given circumstance, the employees were rewarded with the points only for their

association with Webjet as employees and therefore, the reward points shall be qualified for

deduction and the expenses will be allowable expense for the employer.

Answer to question II

If the service provider receives any compensation for the damage of his asset while

the asset was under use by the service recipient, the compensation amount will not be taxed

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW OF AUSTRALIA

under the hands of the service provider. Some specific conditions are there those are required

to fulfil to be eligible for deduction –

The asset for which the compensation is received must be damaged while it was in

use under the service1

The compensation amount shall exclusively used for restructuring the damaged part

The asset shall be depreciable asset for which the depreciation shall be measured and

recorded in the books of accounts2.

The asset that was provided for service shall be capital asset and service provider

must use the asset only for the purposes of businesses.

Therefore, the compensation amount that was received on account of damage of the

asset by Crane Hire Company shall be allowed for deduction assuming that above mentioned

all conditions are satisfied.

Answer to question III

Under the Para 71 – 78 of TR 1999/10, if any person receives any gifts on account of

his employment associated activities, then the amount of gift shall be included under his total

taxable income for the purpose of taxation. However, it the gift is received on account on

personal relations or personal reason and in no way it is related with the employment

activities, the gift amount will be qualified for deduction under the taxable income3.

1 Chartered Accountants Australia & New Zealand (2017) CAANZ https://www.charteredaccountantsanz.com/

2 The Tax Institute (2017) Taxinstitute.com.au https://www.taxinstitute.com.au/

3 Barkoczy, Stephen, et al. Foundations Student Tax Pack 3 2016. Oxford University Press Australia & New

Zealand, 2016.

under the hands of the service provider. Some specific conditions are there those are required

to fulfil to be eligible for deduction –

The asset for which the compensation is received must be damaged while it was in

use under the service1

The compensation amount shall exclusively used for restructuring the damaged part

The asset shall be depreciable asset for which the depreciation shall be measured and

recorded in the books of accounts2.

The asset that was provided for service shall be capital asset and service provider

must use the asset only for the purposes of businesses.

Therefore, the compensation amount that was received on account of damage of the

asset by Crane Hire Company shall be allowed for deduction assuming that above mentioned

all conditions are satisfied.

Answer to question III

Under the Para 71 – 78 of TR 1999/10, if any person receives any gifts on account of

his employment associated activities, then the amount of gift shall be included under his total

taxable income for the purpose of taxation. However, it the gift is received on account on

personal relations or personal reason and in no way it is related with the employment

activities, the gift amount will be qualified for deduction under the taxable income3.

1 Chartered Accountants Australia & New Zealand (2017) CAANZ https://www.charteredaccountantsanz.com/

2 The Tax Institute (2017) Taxinstitute.com.au https://www.taxinstitute.com.au/

3 Barkoczy, Stephen, et al. Foundations Student Tax Pack 3 2016. Oxford University Press Australia & New

Zealand, 2016.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW OF AUSTRALIA

Moreover, the transformation of the gift into cash or kind will not alter its original nature that

is taxable or deductible. Thus, the offer of oversees package for holiday received by manager

of night club from the alcohol supplier will be included under the taxable income as the offer

received on account of work related activities.

Answer to question IV

If any money is raised from the member for any specific purpose and eventually it

was found that the raised money were more than the requirement and owing to that the

money is again returned to the member from whom it was raised, then that amount will not be

included under the assessable income of the person who raised the money4. The amount will

not be taxable for the person as it was never been his income rather it will be considered as

the error in the requirement budget. Thus, the amount rose which were eventually found to be

more than requirement will not be taxed in the hands of recipient.

Answer to question V

If any sportsman receives any award in form of cash or kind owing to his association

to any sport the amount will be considered as taxable income in the hands of the sportsman.

In the given situation, the Sportsman from Australia received the award money for being the

best and fairest player in the AFL. Therefore, under TR 1999/17, that deals with this

provision, the amount in the hands of the sportsman will be considered as taxable5.

4 CPA Australia (2017) Cpaaustralia.com.au https://www.cpaaustralia.com.au/

5 Karin Simon, Sara McDonald, Accident Investigation - Databases - Library Guides At Cquniversity (2017)

Libguides.library.cqu.edu.au http://libguides.library.cqu.edu.au/content.php?pid=166733&sid=2668174

Moreover, the transformation of the gift into cash or kind will not alter its original nature that

is taxable or deductible. Thus, the offer of oversees package for holiday received by manager

of night club from the alcohol supplier will be included under the taxable income as the offer

received on account of work related activities.

Answer to question IV

If any money is raised from the member for any specific purpose and eventually it

was found that the raised money were more than the requirement and owing to that the

money is again returned to the member from whom it was raised, then that amount will not be

included under the assessable income of the person who raised the money4. The amount will

not be taxable for the person as it was never been his income rather it will be considered as

the error in the requirement budget. Thus, the amount rose which were eventually found to be

more than requirement will not be taxed in the hands of recipient.

Answer to question V

If any sportsman receives any award in form of cash or kind owing to his association

to any sport the amount will be considered as taxable income in the hands of the sportsman.

In the given situation, the Sportsman from Australia received the award money for being the

best and fairest player in the AFL. Therefore, under TR 1999/17, that deals with this

provision, the amount in the hands of the sportsman will be considered as taxable5.

4 CPA Australia (2017) Cpaaustralia.com.au https://www.cpaaustralia.com.au/

5 Karin Simon, Sara McDonald, Accident Investigation - Databases - Library Guides At Cquniversity (2017)

Libguides.library.cqu.edu.au http://libguides.library.cqu.edu.au/content.php?pid=166733&sid=2668174

5TAXATION LAW OF AUSTRALIA

Answer to question VI

Any expenditure incurred by the employer for the purpose of reconstruction of his

trainees, employees or apprentices shall be allowed as deduction provided the amount was

spend for the reconstruction of the employees. The Taxation Ruling 95/22 that deals with the

reimbursement allowance and treatment states that the following persons will be considered

for the purpose of employee’s construction –

Supervisor or the project administrator who are engaged in the construction site

Manual labour employed for the purpose of construction of the building

The apprentice, carpenters and the trainees

Project administrator or the overseer engaged for the construction of any building

Thus, amount spend for the purpose of building the qualification of the employees or

trainees shall be qualified for deduction

Answer to question VII

While the assessable income measures some particular costs that are spend with the

end goal of undertaking any short-run course identified with art, the sum will be allowed as

the deductible expenses. However, the deduction allowances are there with the accompanying

conditions –

Any costs required to be brought about on meals

Course charge paid for undertaking the course

Training cost brought about for different modules and programming

Cost spend for going to and returning from the organization 6

6 Woellner, R. H., et al. Australian Taxation Law Select: Legislation and Commentary 2016.

Oxford University Press, 2016.

Answer to question VI

Any expenditure incurred by the employer for the purpose of reconstruction of his

trainees, employees or apprentices shall be allowed as deduction provided the amount was

spend for the reconstruction of the employees. The Taxation Ruling 95/22 that deals with the

reimbursement allowance and treatment states that the following persons will be considered

for the purpose of employee’s construction –

Supervisor or the project administrator who are engaged in the construction site

Manual labour employed for the purpose of construction of the building

The apprentice, carpenters and the trainees

Project administrator or the overseer engaged for the construction of any building

Thus, amount spend for the purpose of building the qualification of the employees or

trainees shall be qualified for deduction

Answer to question VII

While the assessable income measures some particular costs that are spend with the

end goal of undertaking any short-run course identified with art, the sum will be allowed as

the deductible expenses. However, the deduction allowances are there with the accompanying

conditions –

Any costs required to be brought about on meals

Course charge paid for undertaking the course

Training cost brought about for different modules and programming

Cost spend for going to and returning from the organization 6

6 Woellner, R. H., et al. Australian Taxation Law Select: Legislation and Commentary 2016.

Oxford University Press, 2016.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW OF AUSTRALIA

Further, the previously mentioned cost will be permitted if and just if the costs

brought about for the course only. In addition, if out of the aggregate costs just a part is spend

for the course, that part just will be considered for finding. Without adequate data, it is

expected that the costs brought about for the course was spend exclusively for the course and

therefore will be an allowable expense7.

Answer to question VIII

As per the ruling of the ATO, the expenditure for the performing asset shall be

allowed for deduction. However, the deduction will be allowed if the expenses related to the

person are considered as the performing artist. To get the deductions, ATO mentioned the

following persons as performing asset –

Person performing in circus is a performing asset

Person performing dance is a performing asset

Musician performing music is a performing asset

Actor who acts is a performing asset

A singer who sings is a performing artist

With the insufficient data, it is presumed that the expenses were related to the make-

up and dresses expenses of the performing asset and will qualify for deduction.

Answer to question IX

The amount spend for travelling can be taken into consideration for deduction if the

expenses is done exclusively to travel for official purposes, though according to the

7 Davis, Angela K., et al. "Do socially responsible firms pay more taxes?." The Accounting Review 91.1 (2015):

47-68.

Further, the previously mentioned cost will be permitted if and just if the costs

brought about for the course only. In addition, if out of the aggregate costs just a part is spend

for the course, that part just will be considered for finding. Without adequate data, it is

expected that the costs brought about for the course was spend exclusively for the course and

therefore will be an allowable expense7.

Answer to question VIII

As per the ruling of the ATO, the expenditure for the performing asset shall be

allowed for deduction. However, the deduction will be allowed if the expenses related to the

person are considered as the performing artist. To get the deductions, ATO mentioned the

following persons as performing asset –

Person performing in circus is a performing asset

Person performing dance is a performing asset

Musician performing music is a performing asset

Actor who acts is a performing asset

A singer who sings is a performing artist

With the insufficient data, it is presumed that the expenses were related to the make-

up and dresses expenses of the performing asset and will qualify for deduction.

Answer to question IX

The amount spend for travelling can be taken into consideration for deduction if the

expenses is done exclusively to travel for official purposes, though according to the

7 Davis, Angela K., et al. "Do socially responsible firms pay more taxes?." The Accounting Review 91.1 (2015):

47-68.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW OF AUSTRALIA

Australian Tax Office the measure of costs brought about for heading off to the workplace

and returning from the workplace is not permitted as deduction. Further, if out of the

aggregate costs just a part is spend for the workplace reason travel, that part just will be

considered for deduction8. Without adequate data, it will be expected that the costs are

incurred for the official travel purpose only and will be qualified for deduction.

Answer to question X

Generally, the travelling expenses are not allowed for deduction and for getting

deduction on travelling expense the amount shall be spend for official travel purposes only.

Further, deduction for travelling to 2 workplaces will be allowed only if both the work places

are of the same employer. As in the given case, both the workplaces are of the same

employer, the amount will not qualify for deduction.

8 Feld, Alan. "Federal Taxation of State Tax Credits." (2016).

Australian Tax Office the measure of costs brought about for heading off to the workplace

and returning from the workplace is not permitted as deduction. Further, if out of the

aggregate costs just a part is spend for the workplace reason travel, that part just will be

considered for deduction8. Without adequate data, it will be expected that the costs are

incurred for the official travel purpose only and will be qualified for deduction.

Answer to question X

Generally, the travelling expenses are not allowed for deduction and for getting

deduction on travelling expense the amount shall be spend for official travel purposes only.

Further, deduction for travelling to 2 workplaces will be allowed only if both the work places

are of the same employer. As in the given case, both the workplaces are of the same

employer, the amount will not qualify for deduction.

8 Feld, Alan. "Federal Taxation of State Tax Credits." (2016).

8TAXATION LAW OF AUSTRALIA

Answer 2

The assessable situation of an individual is resolved on the foundation of the idea of the

citizenship of a person that is whether the concerned individual is outside inhabitant or

Australian. For tax assessment reason, an oversees student, selected in any Australian

establishment's course, of over a half year term, is considered to be a citizen of the nation. In

this specific circumstance, with respect to the mentioned fact, Manpreet will be considered as

an Australian resident. Manpreet had part time work as as the office assistant in an Australian

organization, with a pay of $45,000 every month. The costs related to his self-education,

which are of worth $18,000 can't be took into consideration for deduction, as findings must

be guaranteed in this specific circumstance, if the concerned individual gets a bonded

scholarship which is assessable. In the given situation, the case of Manpreet will be

considered for deduction if –

Maintain the level of knowledge or enhance the level of knowledge and the skills for

the requirement of present job

Will enhance or are expected to enhance the income of the person from present job9.

If the self-education expenses in no way is associated with the present job, the

expenses on the self-education course will not be allowed as deduction even if –

It is generally associated with it

It may enable to get any new opportunity for the job

The cost ought to not exclusively be considered as a pre-necessity for era of

assessable pay, they ought to likewise have significance to the exercises bringing about era of

9 Braithwaite, Valerie, ed. Taxing democracy: Understanding tax avoidance and evasion. Routledge, 2017.

Answer 2

The assessable situation of an individual is resolved on the foundation of the idea of the

citizenship of a person that is whether the concerned individual is outside inhabitant or

Australian. For tax assessment reason, an oversees student, selected in any Australian

establishment's course, of over a half year term, is considered to be a citizen of the nation. In

this specific circumstance, with respect to the mentioned fact, Manpreet will be considered as

an Australian resident. Manpreet had part time work as as the office assistant in an Australian

organization, with a pay of $45,000 every month. The costs related to his self-education,

which are of worth $18,000 can't be took into consideration for deduction, as findings must

be guaranteed in this specific circumstance, if the concerned individual gets a bonded

scholarship which is assessable. In the given situation, the case of Manpreet will be

considered for deduction if –

Maintain the level of knowledge or enhance the level of knowledge and the skills for

the requirement of present job

Will enhance or are expected to enhance the income of the person from present job9.

If the self-education expenses in no way is associated with the present job, the

expenses on the self-education course will not be allowed as deduction even if –

It is generally associated with it

It may enable to get any new opportunity for the job

The cost ought to not exclusively be considered as a pre-necessity for era of

assessable pay, they ought to likewise have significance to the exercises bringing about era of

9 Braithwaite, Valerie, ed. Taxing democracy: Understanding tax avoidance and evasion. Routledge, 2017.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW OF AUSTRALIA

salary. Manpreet has caused costs on PC, printer and another telephone, which is identified

with her work reason . This can be considered under segment 8-1 of the ITAA 1997, where

an adequate nexus is available between the pay producing limit and the costs, with the end

goal that it has the qualities of work basically. Alluding to segment 8-1 of the ITAA 1997 the

costs on new telephone is important t increase assessable salary which suggests Manpreet is

permitted to assert conclusions. The FC of T v. M I Roberts 92 ATC 4787 demonstrates that

by the standards of Maddalena, the government court offered remittance to deduct MBA

related use to a mine supervisor.

Ronpibon Tin NL v. FC of T (1949) stated this, where it is expressed that there ought

to be a relation amongst assessable and the outgoing income with the end goal that active is

imperative to pick up an open salary. Deduction for self-education expenses are not permitted

if the course helps in opening up new roads for work or wage creating movement. This infers

the costs of Manpreet should not be considered for deduction.

As expressed in Lunney v. FC of T; Hayley v. FC of T (1958) 100 CLR 478; (1958),

to meet the criteria as per sectin 8-1 of the ITAA 1997, the cost shall be obligatorily have the

normal for an active one, which is brought about to increase available pay10. As held in the

section of 8-1 of the ITAA 1997 for the cost to be deductible, there ought to be satisfactory

connection between the exercises that create earnings and the costs, with the end goal that its

element is not domestic in nature and is identified with the work.

10 Ato.Gov.Au/ (2017) Ato.gov.au https://www.ato.gov.au/

salary. Manpreet has caused costs on PC, printer and another telephone, which is identified

with her work reason . This can be considered under segment 8-1 of the ITAA 1997, where

an adequate nexus is available between the pay producing limit and the costs, with the end

goal that it has the qualities of work basically. Alluding to segment 8-1 of the ITAA 1997 the

costs on new telephone is important t increase assessable salary which suggests Manpreet is

permitted to assert conclusions. The FC of T v. M I Roberts 92 ATC 4787 demonstrates that

by the standards of Maddalena, the government court offered remittance to deduct MBA

related use to a mine supervisor.

Ronpibon Tin NL v. FC of T (1949) stated this, where it is expressed that there ought

to be a relation amongst assessable and the outgoing income with the end goal that active is

imperative to pick up an open salary. Deduction for self-education expenses are not permitted

if the course helps in opening up new roads for work or wage creating movement. This infers

the costs of Manpreet should not be considered for deduction.

As expressed in Lunney v. FC of T; Hayley v. FC of T (1958) 100 CLR 478; (1958),

to meet the criteria as per sectin 8-1 of the ITAA 1997, the cost shall be obligatorily have the

normal for an active one, which is brought about to increase available pay10. As held in the

section of 8-1 of the ITAA 1997 for the cost to be deductible, there ought to be satisfactory

connection between the exercises that create earnings and the costs, with the end goal that its

element is not domestic in nature and is identified with the work.

10 Ato.Gov.Au/ (2017) Ato.gov.au https://www.ato.gov.au/

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW OF AUSTRALIA

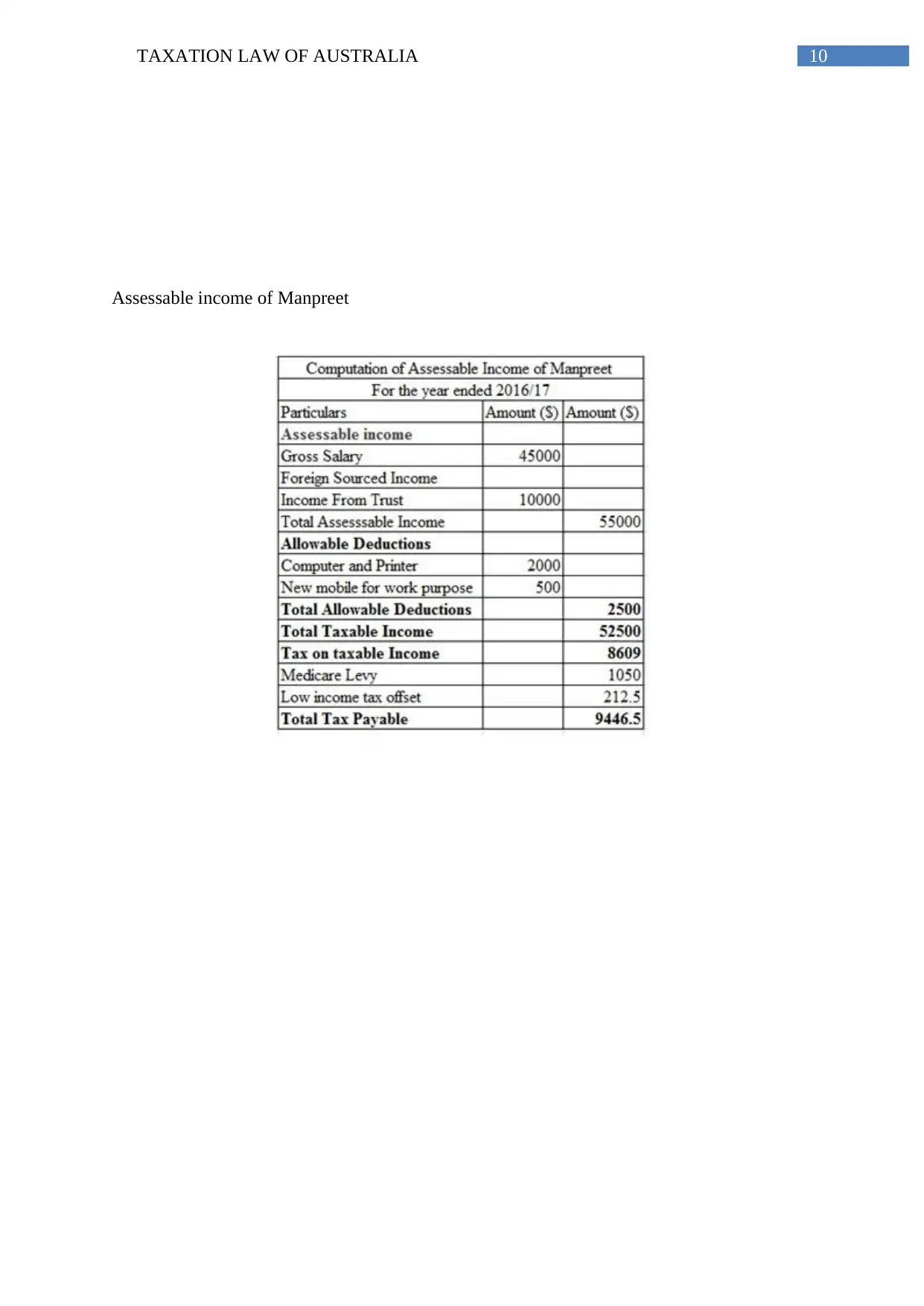

Assessable income of Manpreet

Assessable income of Manpreet

11TAXATION LAW OF AUSTRALIA

References

Ato.Gov.Au/ (2017) Ato.gov.au https://www.ato.gov.au/

Barkoczy, Stephen, et al. Foundations Student Tax Pack 3 2016. Oxford University Press

Australia & New Zealand, 2016.

Braithwaite, Valerie, ed. Taxing democracy: Understanding tax avoidance and evasion.

Routledge, 2017.

Chartered Accountants Australia & New Zealand (2017) CAANZ

https://www.charteredaccountantsanz.com/

CPA Australia (2017) Cpaaustralia.com.au https://www.cpaaustralia.com.au/

Davis, Angela K., et al. "Do socially responsible firms pay more taxes?." The Accounting

Review 91.1 (2015): 47-68.

Feld, Alan. "Federal Taxation of State Tax Credits." (2016).

Karin Simon, Sara McDonald, Accident Investigation - Databases - Library Guides At

Cquniversity (2017) Libguides.library.cqu.edu.au

http://libguides.library.cqu.edu.au/content.php?pid=166733&sid=2668174

The Tax Institute (2017) Taxinstitute.com.au https://www.taxinstitute.com.au/

Woellner, R. H., et al. Australian Taxation Law Select: Legislation and Commentary 2016.

Oxford University Press, 2016.

References

Ato.Gov.Au/ (2017) Ato.gov.au https://www.ato.gov.au/

Barkoczy, Stephen, et al. Foundations Student Tax Pack 3 2016. Oxford University Press

Australia & New Zealand, 2016.

Braithwaite, Valerie, ed. Taxing democracy: Understanding tax avoidance and evasion.

Routledge, 2017.

Chartered Accountants Australia & New Zealand (2017) CAANZ

https://www.charteredaccountantsanz.com/

CPA Australia (2017) Cpaaustralia.com.au https://www.cpaaustralia.com.au/

Davis, Angela K., et al. "Do socially responsible firms pay more taxes?." The Accounting

Review 91.1 (2015): 47-68.

Feld, Alan. "Federal Taxation of State Tax Credits." (2016).

Karin Simon, Sara McDonald, Accident Investigation - Databases - Library Guides At

Cquniversity (2017) Libguides.library.cqu.edu.au

http://libguides.library.cqu.edu.au/content.php?pid=166733&sid=2668174

The Tax Institute (2017) Taxinstitute.com.au https://www.taxinstitute.com.au/

Woellner, R. H., et al. Australian Taxation Law Select: Legislation and Commentary 2016.

Oxford University Press, 2016.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.