Financial Analysis of Companies Using Various Ratios

VerifiedAdded on 2020/07/22

|22

|4906

|242

Report

AI Summary

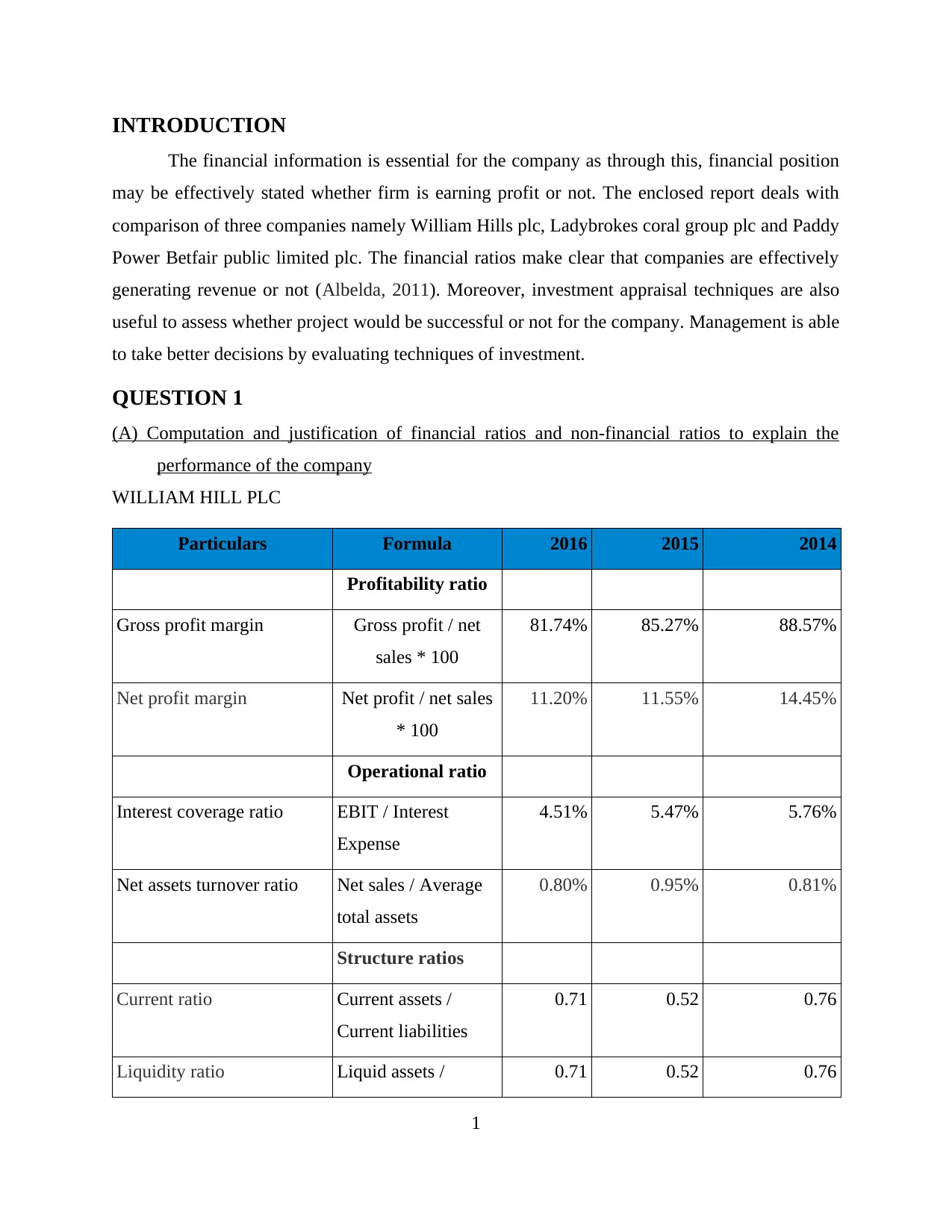

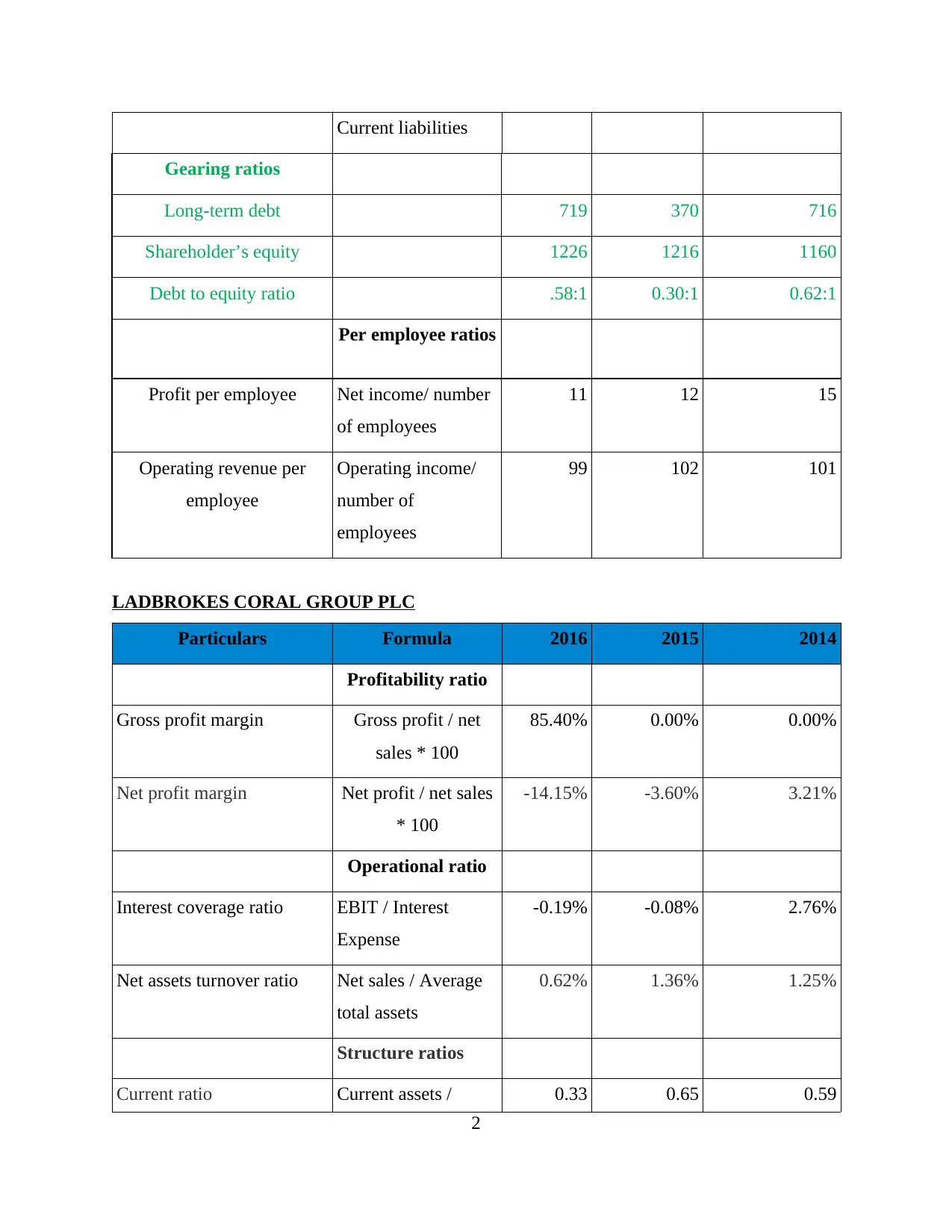

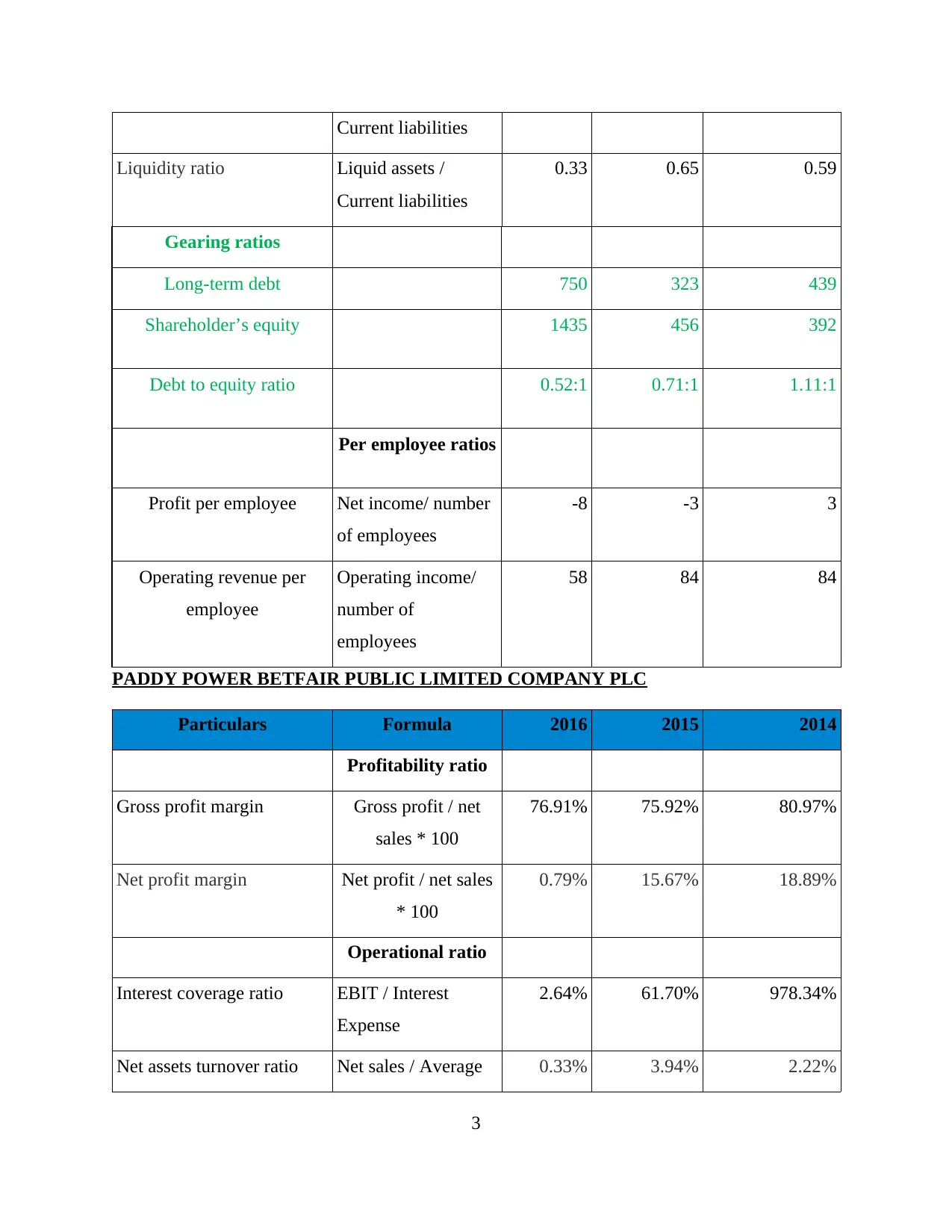

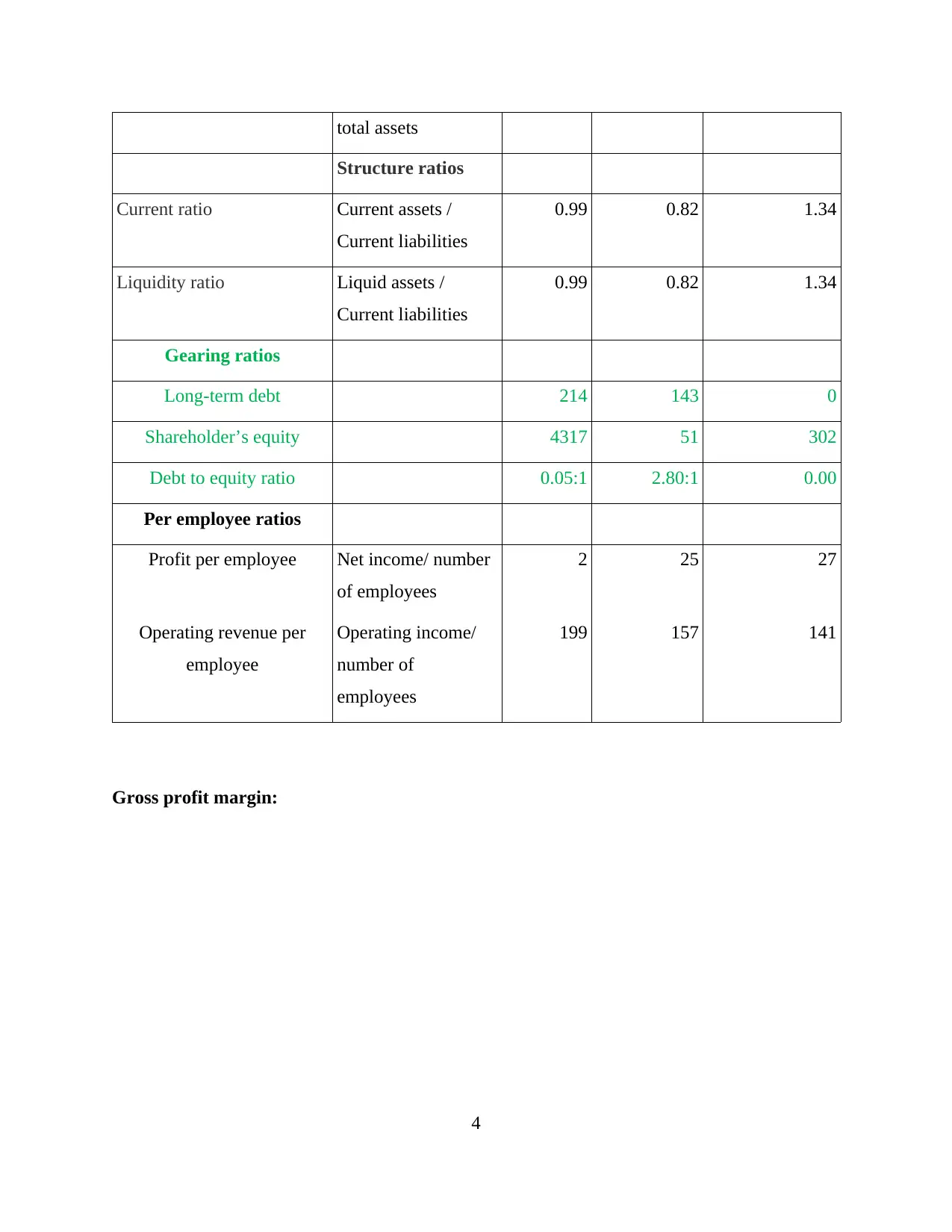

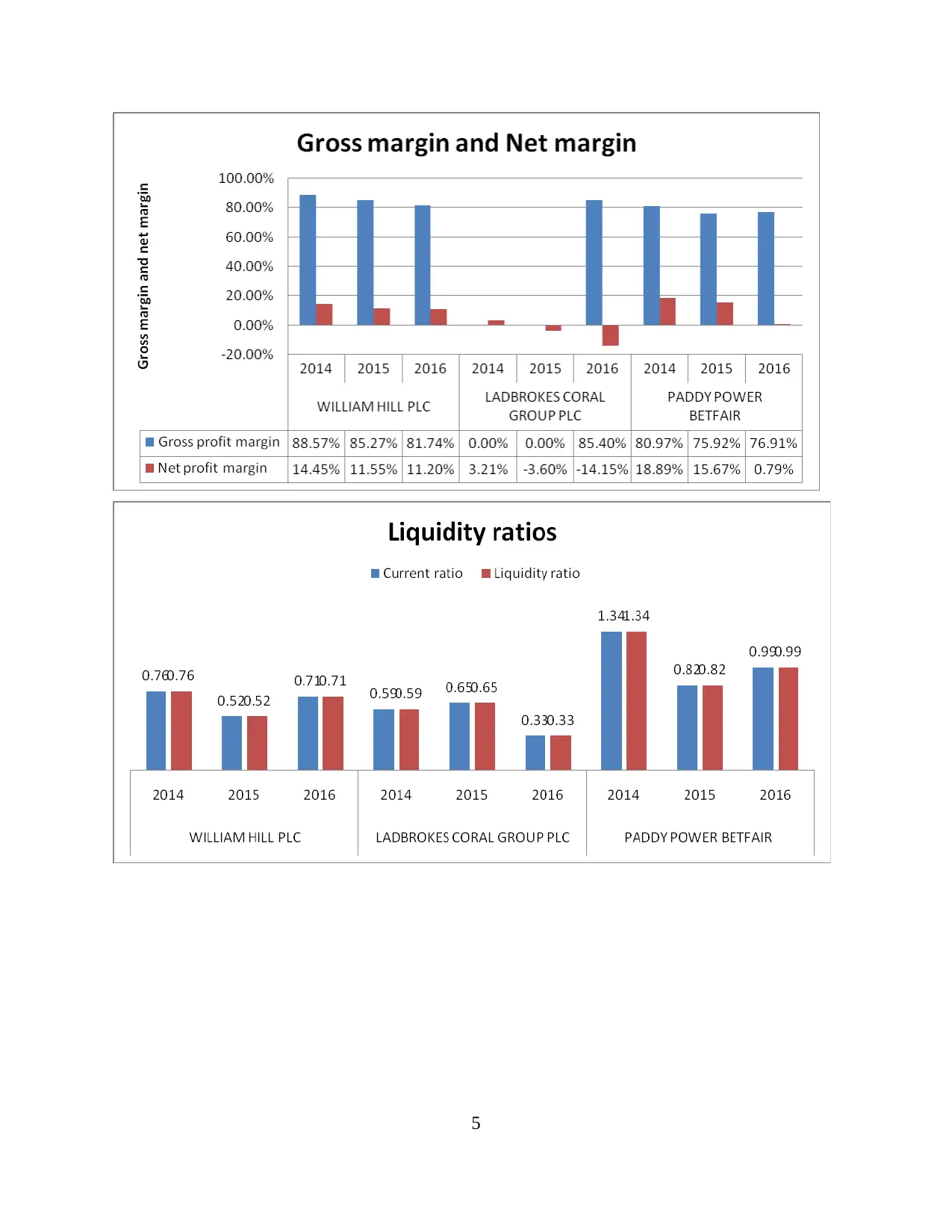

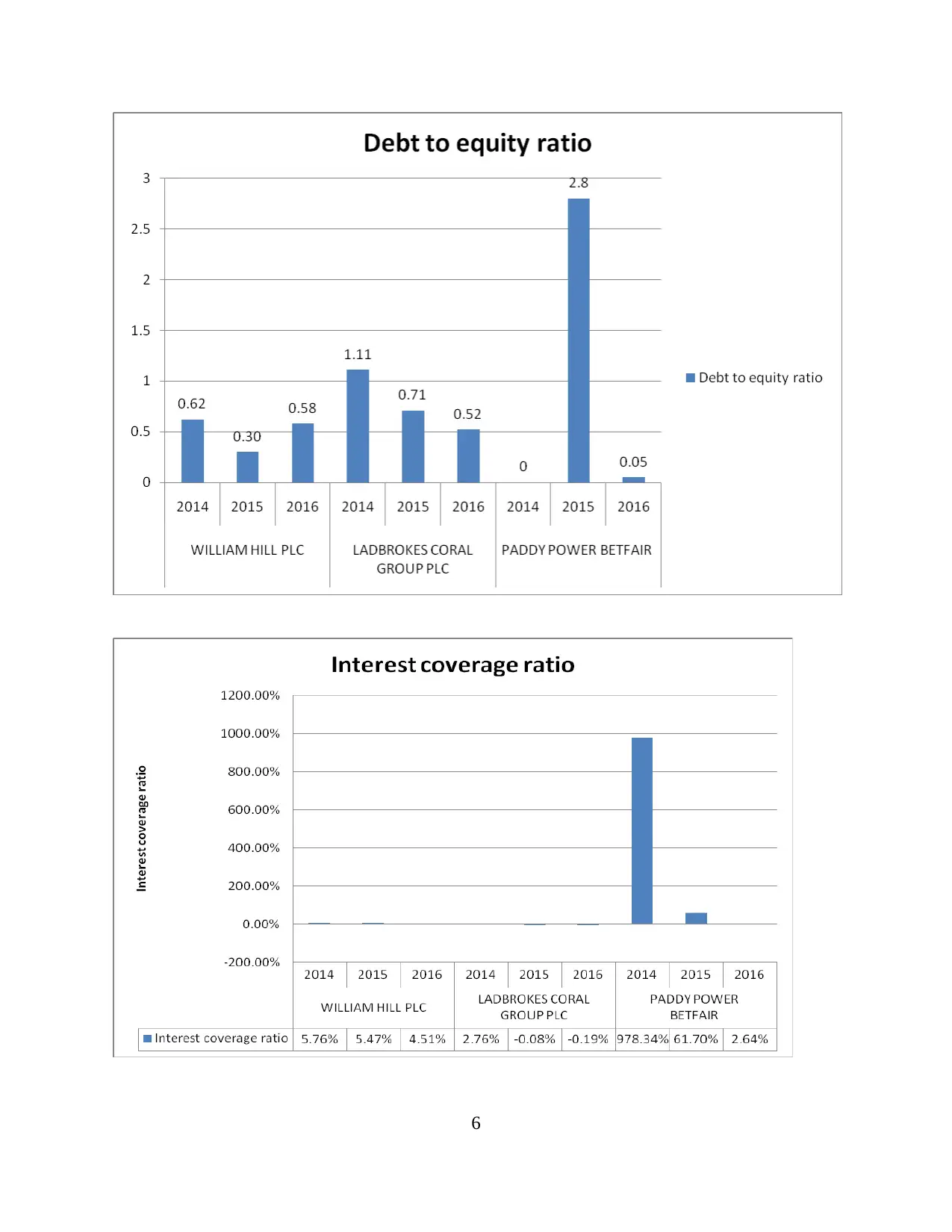

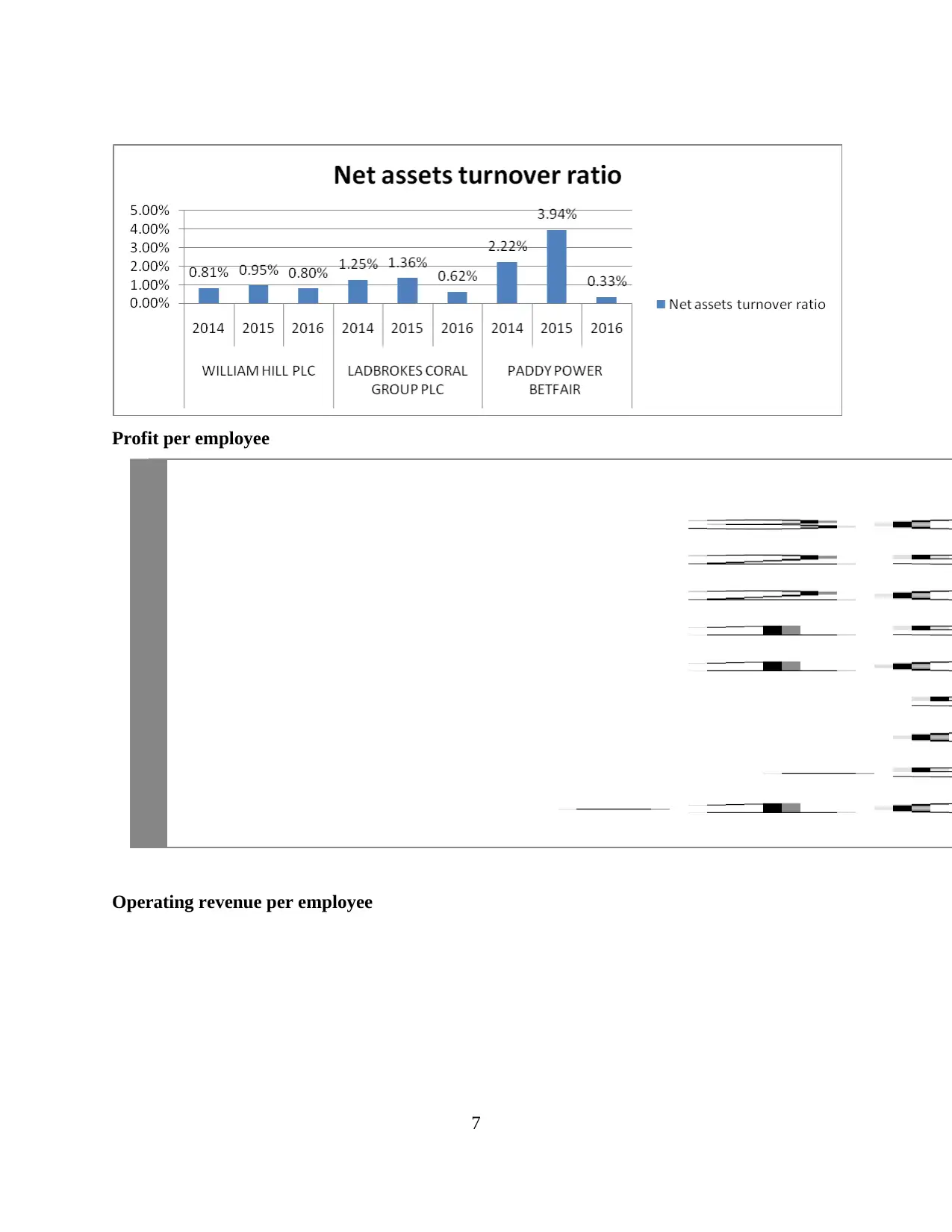

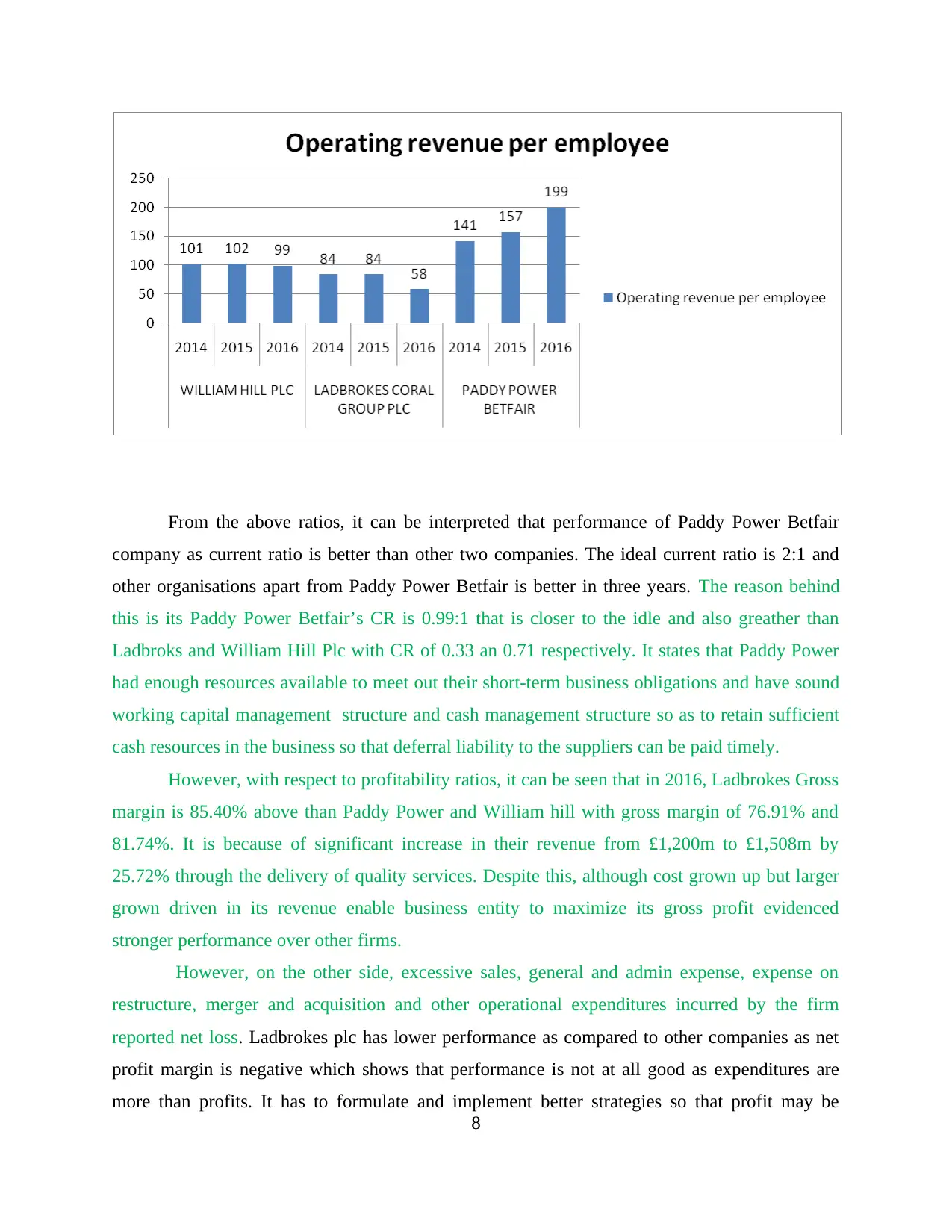

This report undertakes a comprehensive financial analysis of three companies: William Hill plc, Ladbrokes Coral Group plc, and Paddy Power Betfair public limited plc. It begins with an executive summary highlighting the importance of financial ratios and investment techniques for managerial decision-making. The report computes and justifies various financial ratios (profitability, operational, structure, and gearing ratios) to explain each company's performance over three years. The analysis reveals the strengths and weaknesses of each company, with William Hill plc emerging as the best-performing entity due to its strong profitability and solvency ratios. The report also analyzes the investment appraisal process, discussing its stages and methods, including numerical examples. Non-financial ratios, such as staff turnover and customer loyalty, are also considered to provide a holistic view of the companies' performance. The report concludes with a ranking of the companies based on their financial and non-financial performance and provides recommendations for improvement. The analysis emphasizes the importance of efficient resource utilization, cost control, and customer satisfaction for achieving financial success.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.