Air New Zealand Limited Financial Performance Analysis Report

VerifiedAdded on 2020/10/22

|20

|6653

|106

Report

AI Summary

This report provides a comprehensive financial analysis of Air New Zealand Limited, evaluating its performance through various financial ratios, including profitability, liquidity, efficiency, and market value ratios. The analysis encompasses a comparative study with Kingfisher Plc, examining their income statements and balance sheets using horizontal and vertical analysis techniques. The report delves into the gross profit margin, operating income, and net profit margin of both companies, highlighting their respective strengths and weaknesses. It also assesses liquidity positions through current and quick ratios, inventory turnover, and interest coverage ratios. Furthermore, the report includes a horizontal analysis of Air New Zealand's income statement, detailing changes in revenue, cost of goods sold, operating expenses, and net income over a three-year period. A vertical analysis is also conducted to assess the percentage changes in key financial metrics. The conclusion identifies which company demonstrates a better financial position and market value, based on the comparative analysis.

AIR NEW ZEALAND

LIMITED

LIMITED

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

Financial ratio analysis...........................................................................................................1

Horizontal analysis.................................................................................................................3

Vertical analysis ....................................................................................................................4

Horizontal Analysis................................................................................................................6

Vertical analysis.....................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

APPENDIX....................................................................................................................................10

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

Financial ratio analysis...........................................................................................................1

Horizontal analysis.................................................................................................................3

Vertical analysis ....................................................................................................................4

Horizontal Analysis................................................................................................................6

Vertical analysis.....................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

APPENDIX....................................................................................................................................10

EXECUTIVE SUMMARY

Financial performance indicator is the predefined structure which help the organization to

identify and analyse the organization's performance. This can be done with calculation of

different financial ratios such as profitability, liquidity, market value, investment and efficiency

ratio. In this present report, This can be done with calculation of different financial ratios such as

profitability, liquidity, market value, investment and efficiency ratio. Gross profit margin of

Kingfisher Plc has seen slight increment from 2015 to 2017 of around $.03 million. This not a

major increment for a big organisation in a period of 3 years. For Air New Zealand limited the

growth was 77.89% in 2015 to 83.81% in 2017, there is slight more increase in profits as

compared to Kingfisher. The will remain unhold 106 to 110 days in Kingfisher Plc and in new

air it is between 41 to 48 days. This indicates that inventory is fast moving in New air as it has a

time period of less than 50 days. The interest coverage ratio for Air new was 5.39 in 2105 and

7.06 in 2107 this shows that company is putting its step forward to cover its interest expenses.

For Kingfisher plc earnings were 0. 24 in 2015, 0.18 in 2016 and 0.51 in 2017. Earnings per

share are very low for all three years yet it is increasing with a slow pace. For Air New earnings

in 2015 and 2016 were 23.31 and 40.21 respectively. This shows that company provides a good

return to shareholders on their investments.

Financial performance indicator is the predefined structure which help the organization to

identify and analyse the organization's performance. This can be done with calculation of

different financial ratios such as profitability, liquidity, market value, investment and efficiency

ratio. In this present report, This can be done with calculation of different financial ratios such as

profitability, liquidity, market value, investment and efficiency ratio. Gross profit margin of

Kingfisher Plc has seen slight increment from 2015 to 2017 of around $.03 million. This not a

major increment for a big organisation in a period of 3 years. For Air New Zealand limited the

growth was 77.89% in 2015 to 83.81% in 2017, there is slight more increase in profits as

compared to Kingfisher. The will remain unhold 106 to 110 days in Kingfisher Plc and in new

air it is between 41 to 48 days. This indicates that inventory is fast moving in New air as it has a

time period of less than 50 days. The interest coverage ratio for Air new was 5.39 in 2105 and

7.06 in 2107 this shows that company is putting its step forward to cover its interest expenses.

For Kingfisher plc earnings were 0. 24 in 2015, 0.18 in 2016 and 0.51 in 2017. Earnings per

share are very low for all three years yet it is increasing with a slow pace. For Air New earnings

in 2015 and 2016 were 23.31 and 40.21 respectively. This shows that company provides a good

return to shareholders on their investments.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial performance indicator of an organisation is the analysis and evaluation of

accounting statements. This can be done with calculation of different financial ratios such as

profitability, liquidity, market value, investment and efficiency ratio. A comparison of two

different firms in same industry can also be carried out with comparison of these ratios. In the

present case study, This can be done with calculation of different financial ratios such as

profitability, liquidity, market value, investment and efficiency ratio It is done in a way of

evaluation of their income statement and balance sheet in form of vertical and horizontal

analysis. A ratio analysis of both organisations is also presented in this report. At the end of this

report, it will present one company from both of them which has a better financial position and

market value.

MAIN BODY

Financial ratio analysis

Profitability ratios

Gross profit margin of Kingfisher Plc has seen slight increment from 2015 to 2017 of

around $.03 million. This not a major increment for a big organisation in a period of 3 years. For

Air New Zealand limited the growth was 77.89% in 2015 to 83.81% in 2017, there is slight more

increase in profits as compared to Kingfisher (Gub & et.al., 2015). for operating income it can

be said that Air New Zealand have seen a increment in 2016 and then a downfall in 2017, there is

consistent rise in operating income of kingfisher Plc. Same is the case with net profit margin for

both organisations. This can be said that kingfisher have gained a control over its operating

overhead and it is reflected in its net profits. Though gross profits of Air new Zealand Limited

are very high for every year but it does not have an effective control over its administrative cost

and this resulted in lower net profit margin and also, they are decreasing in this period of 3 years.

Liquidity ration

The liquidity position of both firms is compared through current and quick ratios. Current

ratio for all the three years is below 1 which is not a good sign of liquidity position for a

business. For Kingfisher Plc in two years it was constant and for 2014 it rose to 1.3 with a minor

1

Financial performance indicator of an organisation is the analysis and evaluation of

accounting statements. This can be done with calculation of different financial ratios such as

profitability, liquidity, market value, investment and efficiency ratio. A comparison of two

different firms in same industry can also be carried out with comparison of these ratios. In the

present case study, This can be done with calculation of different financial ratios such as

profitability, liquidity, market value, investment and efficiency ratio It is done in a way of

evaluation of their income statement and balance sheet in form of vertical and horizontal

analysis. A ratio analysis of both organisations is also presented in this report. At the end of this

report, it will present one company from both of them which has a better financial position and

market value.

MAIN BODY

Financial ratio analysis

Profitability ratios

Gross profit margin of Kingfisher Plc has seen slight increment from 2015 to 2017 of

around $.03 million. This not a major increment for a big organisation in a period of 3 years. For

Air New Zealand limited the growth was 77.89% in 2015 to 83.81% in 2017, there is slight more

increase in profits as compared to Kingfisher (Gub & et.al., 2015). for operating income it can

be said that Air New Zealand have seen a increment in 2016 and then a downfall in 2017, there is

consistent rise in operating income of kingfisher Plc. Same is the case with net profit margin for

both organisations. This can be said that kingfisher have gained a control over its operating

overhead and it is reflected in its net profits. Though gross profits of Air new Zealand Limited

are very high for every year but it does not have an effective control over its administrative cost

and this resulted in lower net profit margin and also, they are decreasing in this period of 3 years.

Liquidity ration

The liquidity position of both firms is compared through current and quick ratios. Current

ratio for all the three years is below 1 which is not a good sign of liquidity position for a

business. For Kingfisher Plc in two years it was constant and for 2014 it rose to 1.3 with a minor

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

increment. Quick ratio for Air new Zealand Limited was constant for all three years with minor

ups and down and of Kingfisher plc it felled down by 0.10. This indicates that both of them not

enjoy a liquidity position and do not have sufficient cash and profit equivalent resource to meet

their current liabilities (Financial ratio, 2018). This ratio ensures short term solvency of business

in meeting small debts at right time.

Air new Zealand Limited is not even near the standard ratio of 2:1. when a comparison of

these ratios of both companies is done it is found that kingfisher plc has a better liquidity

position as compared to new air. The will remain unhold 106 to 110 days in Kingfisher Plc and

in new air it is between 41 to 48 days. This indicates that inventory is fast moving in New air as

it has a time period of less than 50 days.

Efficiency ratio

Returns earned on assets for Air New Zealand limited was 5.3 in 2015 which saw an

increment in next year in 2017 fell down to 5.18. For Kingfisher Plc there was an increment from

2015 to 2017 by 0.22, though it is a minor increment yet there is an slight progress rather than

increase in ratio of Air New Zealand Limited . Earning on capital employed for Air new was

constant for both 2015 and 2017 at 9.02 and with an increase in 2016 as 11.07. In Kingfisher Plc

as for 2015 it was 5.9 it decreased in 2016 to 4.25 and again increased to 6.12, this reflects that

company has again maintained its position and earned sufficient return on its capital employed.

The interest coverage ratio for Air new was 5.39 in 2105 and 7.06 in 2107 this shows that

company is putting its step forward to cover its interest expenses (Read & et.al., 2016).

Kingfisher Plc has a very high interest coverage that means it have higher resources to cover its

interest expenses and also, it has more debt in this capital structure. For 2015 ratio was 31.12

which increased to 41.12 by 2017, In a period of mere 2 years this ratio increased by 10, which

indicates company is highly relying on debt capital which attracts interest.

Market ratio:

The ratio calculates actual earning for shareholders and which is a financial performance

indicator in market.To increase in the earning per share of the organization is the main aim of the

shareholder to invest in it For Kingfisher plc earnings were 0. 24 in 2015, 0.18 in 2016 and 0.51

in 2017. Earnings per share are very low for all three years yet it is increasing with a slow pace.

2

ups and down and of Kingfisher plc it felled down by 0.10. This indicates that both of them not

enjoy a liquidity position and do not have sufficient cash and profit equivalent resource to meet

their current liabilities (Financial ratio, 2018). This ratio ensures short term solvency of business

in meeting small debts at right time.

Air new Zealand Limited is not even near the standard ratio of 2:1. when a comparison of

these ratios of both companies is done it is found that kingfisher plc has a better liquidity

position as compared to new air. The will remain unhold 106 to 110 days in Kingfisher Plc and

in new air it is between 41 to 48 days. This indicates that inventory is fast moving in New air as

it has a time period of less than 50 days.

Efficiency ratio

Returns earned on assets for Air New Zealand limited was 5.3 in 2015 which saw an

increment in next year in 2017 fell down to 5.18. For Kingfisher Plc there was an increment from

2015 to 2017 by 0.22, though it is a minor increment yet there is an slight progress rather than

increase in ratio of Air New Zealand Limited . Earning on capital employed for Air new was

constant for both 2015 and 2017 at 9.02 and with an increase in 2016 as 11.07. In Kingfisher Plc

as for 2015 it was 5.9 it decreased in 2016 to 4.25 and again increased to 6.12, this reflects that

company has again maintained its position and earned sufficient return on its capital employed.

The interest coverage ratio for Air new was 5.39 in 2105 and 7.06 in 2107 this shows that

company is putting its step forward to cover its interest expenses (Read & et.al., 2016).

Kingfisher Plc has a very high interest coverage that means it have higher resources to cover its

interest expenses and also, it has more debt in this capital structure. For 2015 ratio was 31.12

which increased to 41.12 by 2017, In a period of mere 2 years this ratio increased by 10, which

indicates company is highly relying on debt capital which attracts interest.

Market ratio:

The ratio calculates actual earning for shareholders and which is a financial performance

indicator in market.To increase in the earning per share of the organization is the main aim of the

shareholder to invest in it For Kingfisher plc earnings were 0. 24 in 2015, 0.18 in 2016 and 0.51

in 2017. Earnings per share are very low for all three years yet it is increasing with a slow pace.

2

For Air New earnings in 2015 and 2016 were 23.31 and 40.21 respectively. This shows that

company provides a good return to shareholders on their investments (Kogadeeva & Zamboni,

2016). But for 2015 it went negative, means there were no earning for shareholders.

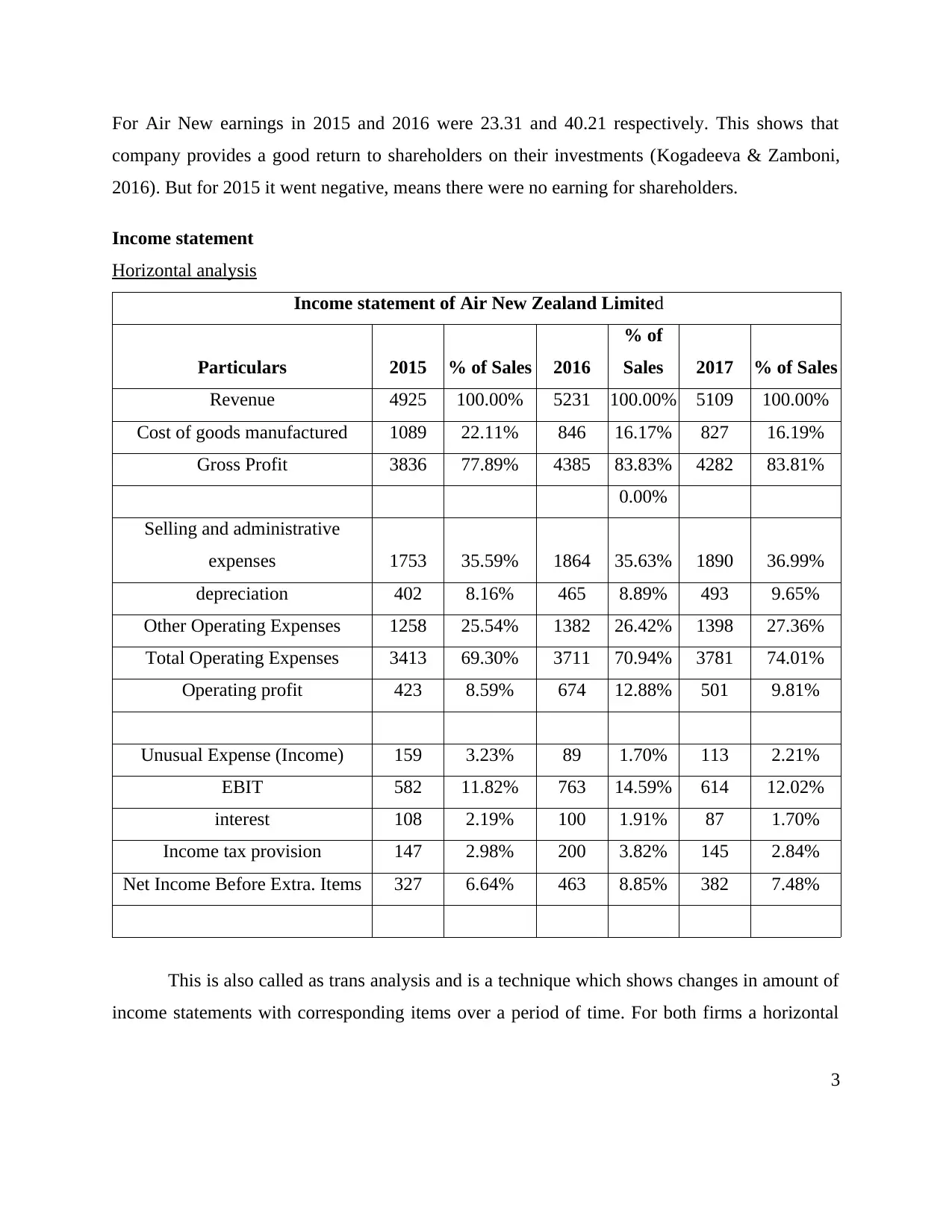

Income statement

Horizontal analysis

Income statement of Air New Zealand Limited

Particulars 2015 % of Sales 2016

% of

Sales 2017 % of Sales

Revenue 4925 100.00% 5231 100.00% 5109 100.00%

Cost of goods manufactured 1089 22.11% 846 16.17% 827 16.19%

Gross Profit 3836 77.89% 4385 83.83% 4282 83.81%

0.00%

Selling and administrative

expenses 1753 35.59% 1864 35.63% 1890 36.99%

depreciation 402 8.16% 465 8.89% 493 9.65%

Other Operating Expenses 1258 25.54% 1382 26.42% 1398 27.36%

Total Operating Expenses 3413 69.30% 3711 70.94% 3781 74.01%

Operating profit 423 8.59% 674 12.88% 501 9.81%

Unusual Expense (Income) 159 3.23% 89 1.70% 113 2.21%

EBIT 582 11.82% 763 14.59% 614 12.02%

interest 108 2.19% 100 1.91% 87 1.70%

Income tax provision 147 2.98% 200 3.82% 145 2.84%

Net Income Before Extra. Items 327 6.64% 463 8.85% 382 7.48%

This is also called as trans analysis and is a technique which shows changes in amount of

income statements with corresponding items over a period of time. For both firms a horizontal

3

company provides a good return to shareholders on their investments (Kogadeeva & Zamboni,

2016). But for 2015 it went negative, means there were no earning for shareholders.

Income statement

Horizontal analysis

Income statement of Air New Zealand Limited

Particulars 2015 % of Sales 2016

% of

Sales 2017 % of Sales

Revenue 4925 100.00% 5231 100.00% 5109 100.00%

Cost of goods manufactured 1089 22.11% 846 16.17% 827 16.19%

Gross Profit 3836 77.89% 4385 83.83% 4282 83.81%

0.00%

Selling and administrative

expenses 1753 35.59% 1864 35.63% 1890 36.99%

depreciation 402 8.16% 465 8.89% 493 9.65%

Other Operating Expenses 1258 25.54% 1382 26.42% 1398 27.36%

Total Operating Expenses 3413 69.30% 3711 70.94% 3781 74.01%

Operating profit 423 8.59% 674 12.88% 501 9.81%

Unusual Expense (Income) 159 3.23% 89 1.70% 113 2.21%

EBIT 582 11.82% 763 14.59% 614 12.02%

interest 108 2.19% 100 1.91% 87 1.70%

Income tax provision 147 2.98% 200 3.82% 145 2.84%

Net Income Before Extra. Items 327 6.64% 463 8.85% 382 7.48%

This is also called as trans analysis and is a technique which shows changes in amount of

income statements with corresponding items over a period of time. For both firms a horizontal

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

analysis for 3 years is carried out which will reflect changes in all items present in profit and loss

account with respect to sales (Luo & et.al., 2015). This will present a year wise comparison of

both firms individually and also with each other. Gross profit margin with respect to sales for Air

New was 77.89% in 2015 and it increased to 83.83% in 2016 and remained constant for 2017,

this indicates that gross profits of firm have increased and remained constant. The operating

profits with ratio to sales indicated that it increased to 12.88% from 8.59% in 2015 and for 2016

it decreased to 9.81%. A fall in operating income can be justified as there was an increment in

the oprative expenses. over a period of these 3 years and resulted in a dragging down operating

profit of firm (de Lecea, Cooper & Smit, 2016). The net profit of firm for 2015 was 6.64%

which increased in 2016 but in 2017 it fell down to 7.48%. with this it can be stated that

company has maintained its cost control so at end of 2017 it had a net profit of 7.48 % as a

percentage to its sales.

For Kingfisher plc gross profit as a percentage to sales for 2015 was 36.91%. and for

2016 it increased to 37.31% and remained constant in 2017 with a percentage to sales of

37.19%. There was a slight increase in revenues of firm and cost of production also remained

same for all 3 years and as a result there was no huge change in gross profit percentage.

Operating profit percentage increased from 5.95% to 6.83% from 2015 – 2017. This increment

was due to control and reduction of operating expenses. Net profit of firm as a percentage to

sales was same for both 2015 and 2017 as 5.23% and 5.43%.

A comparison between income statements of both firms is carried out and it can be

stated that Kingfisher Plc have gained a control over its operating expenses which helped in

increasing it operating and net profits. Air New Zealand limited have earned unusual income and

reduced its interest expenses which resulted in increment of its net profits.

Vertical analysis

Revenue of Air New Zealand limited increased by 6.21% from 2015 to 2016 and for it

reduced by 2.33% in 2017 as compared to 2016. Gross profits increased by 14.31 % in 2016 with

2015 as base year and in2017 it reduced by 2.35% when compared to 2016, this change was due

to fall in sales revenue. Net profit increased by more than 50% in 2016 and fell down by more

than 345 in 2017 and this was a major fall (Molnar & et.al.,2018). But there was a decrement in

4

account with respect to sales (Luo & et.al., 2015). This will present a year wise comparison of

both firms individually and also with each other. Gross profit margin with respect to sales for Air

New was 77.89% in 2015 and it increased to 83.83% in 2016 and remained constant for 2017,

this indicates that gross profits of firm have increased and remained constant. The operating

profits with ratio to sales indicated that it increased to 12.88% from 8.59% in 2015 and for 2016

it decreased to 9.81%. A fall in operating income can be justified as there was an increment in

the oprative expenses. over a period of these 3 years and resulted in a dragging down operating

profit of firm (de Lecea, Cooper & Smit, 2016). The net profit of firm for 2015 was 6.64%

which increased in 2016 but in 2017 it fell down to 7.48%. with this it can be stated that

company has maintained its cost control so at end of 2017 it had a net profit of 7.48 % as a

percentage to its sales.

For Kingfisher plc gross profit as a percentage to sales for 2015 was 36.91%. and for

2016 it increased to 37.31% and remained constant in 2017 with a percentage to sales of

37.19%. There was a slight increase in revenues of firm and cost of production also remained

same for all 3 years and as a result there was no huge change in gross profit percentage.

Operating profit percentage increased from 5.95% to 6.83% from 2015 – 2017. This increment

was due to control and reduction of operating expenses. Net profit of firm as a percentage to

sales was same for both 2015 and 2017 as 5.23% and 5.43%.

A comparison between income statements of both firms is carried out and it can be

stated that Kingfisher Plc have gained a control over its operating expenses which helped in

increasing it operating and net profits. Air New Zealand limited have earned unusual income and

reduced its interest expenses which resulted in increment of its net profits.

Vertical analysis

Revenue of Air New Zealand limited increased by 6.21% from 2015 to 2016 and for it

reduced by 2.33% in 2017 as compared to 2016. Gross profits increased by 14.31 % in 2016 with

2015 as base year and in2017 it reduced by 2.35% when compared to 2016, this change was due

to fall in sales revenue. Net profit increased by more than 50% in 2016 and fell down by more

than 345 in 2017 and this was a major fall (Molnar & et.al.,2018). But there was a decrement in

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

net profit percentage change from 2015 to 2017. The net profit were higher in 2016as compared

to 2015 and it decreased in 2017 resulted in diminishing percentage change.

Revenue of Kingfisher Plc was seen an increment in 2017 as compared to 2016 and in

2016 they saw a downfall when compared to sales revenue of 2015. With a rise in gross income,

profit percentage also increased. In 2016 all three profits that is gross, operating and net profits

were lesser than 2015but in 2017, all of them increased showing a positive gain in percentage

increments.

Kingfisher Plc have seen a fall in all three profits and sales from2015 to 2016 and in 2017

there was increment in all of them resulted in reflecting a positive percentage rise (Verma &

Suthar, 2018). Air New Zealand Limited’s profits increased in 2016 and again fell down in 2017

which was due to lack in effective control over is operating and administrative costs.

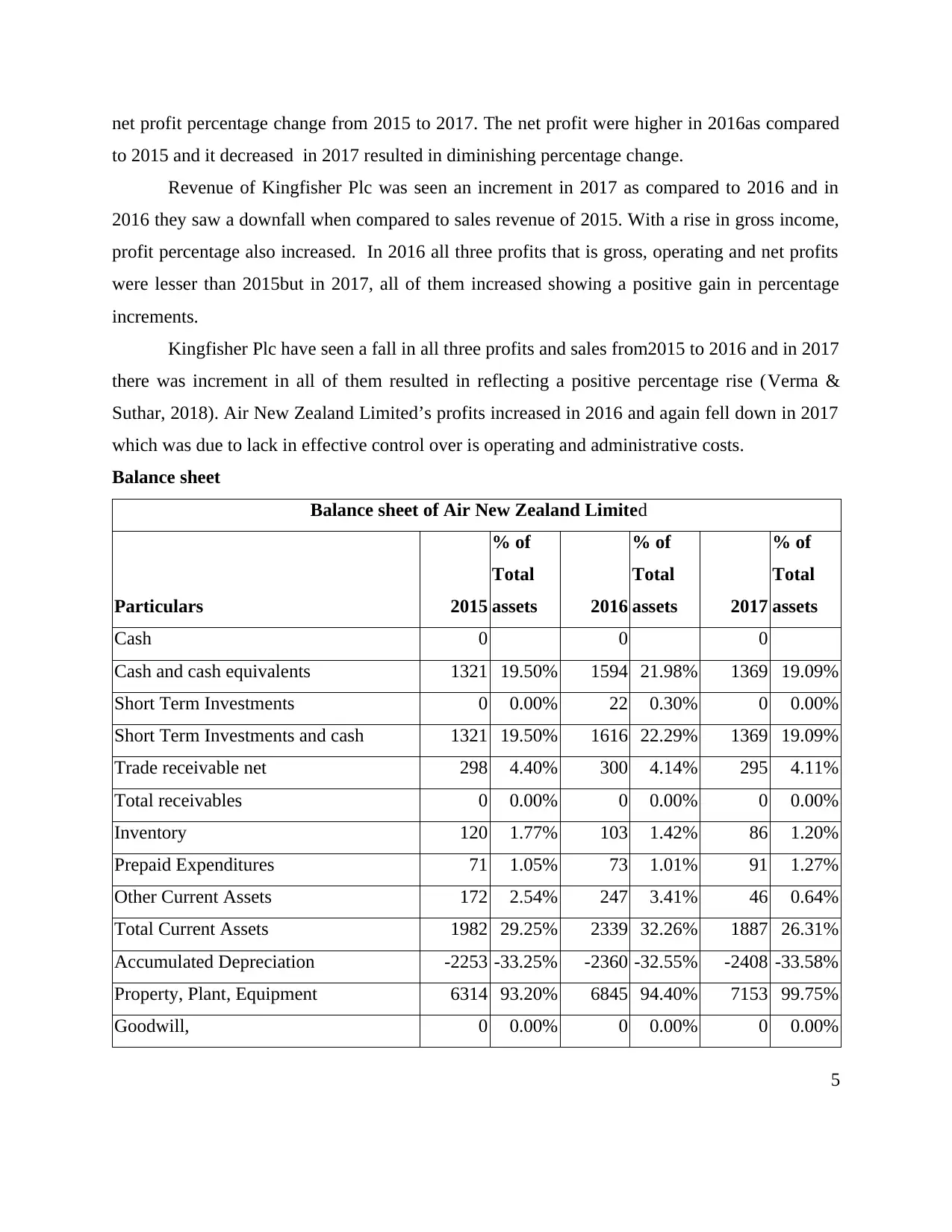

Balance sheet

Balance sheet of Air New Zealand Limited

Particulars 2015

% of

Total

assets 2016

% of

Total

assets 2017

% of

Total

assets

Cash 0 0 0

Cash and cash equivalents 1321 19.50% 1594 21.98% 1369 19.09%

Short Term Investments 0 0.00% 22 0.30% 0 0.00%

Short Term Investments and cash 1321 19.50% 1616 22.29% 1369 19.09%

Trade receivable net 298 4.40% 300 4.14% 295 4.11%

Total receivables 0 0.00% 0 0.00% 0 0.00%

Inventory 120 1.77% 103 1.42% 86 1.20%

Prepaid Expenditures 71 1.05% 73 1.01% 91 1.27%

Other Current Assets 172 2.54% 247 3.41% 46 0.64%

Total Current Assets 1982 29.25% 2339 32.26% 1887 26.31%

Accumulated Depreciation -2253 -33.25% -2360 -32.55% -2408 -33.58%

Property, Plant, Equipment 6314 93.20% 6845 94.40% 7153 99.75%

Goodwill, 0 0.00% 0 0.00% 0 0.00%

5

to 2015 and it decreased in 2017 resulted in diminishing percentage change.

Revenue of Kingfisher Plc was seen an increment in 2017 as compared to 2016 and in

2016 they saw a downfall when compared to sales revenue of 2015. With a rise in gross income,

profit percentage also increased. In 2016 all three profits that is gross, operating and net profits

were lesser than 2015but in 2017, all of them increased showing a positive gain in percentage

increments.

Kingfisher Plc have seen a fall in all three profits and sales from2015 to 2016 and in 2017

there was increment in all of them resulted in reflecting a positive percentage rise (Verma &

Suthar, 2018). Air New Zealand Limited’s profits increased in 2016 and again fell down in 2017

which was due to lack in effective control over is operating and administrative costs.

Balance sheet

Balance sheet of Air New Zealand Limited

Particulars 2015

% of

Total

assets 2016

% of

Total

assets 2017

% of

Total

assets

Cash 0 0 0

Cash and cash equivalents 1321 19.50% 1594 21.98% 1369 19.09%

Short Term Investments 0 0.00% 22 0.30% 0 0.00%

Short Term Investments and cash 1321 19.50% 1616 22.29% 1369 19.09%

Trade receivable net 298 4.40% 300 4.14% 295 4.11%

Total receivables 0 0.00% 0 0.00% 0 0.00%

Inventory 120 1.77% 103 1.42% 86 1.20%

Prepaid Expenditures 71 1.05% 73 1.01% 91 1.27%

Other Current Assets 172 2.54% 247 3.41% 46 0.64%

Total Current Assets 1982 29.25% 2339 32.26% 1887 26.31%

Accumulated Depreciation -2253 -33.25% -2360 -32.55% -2408 -33.58%

Property, Plant, Equipment 6314 93.20% 6845 94.40% 7153 99.75%

Goodwill, 0 0.00% 0 0.00% 0 0.00%

5

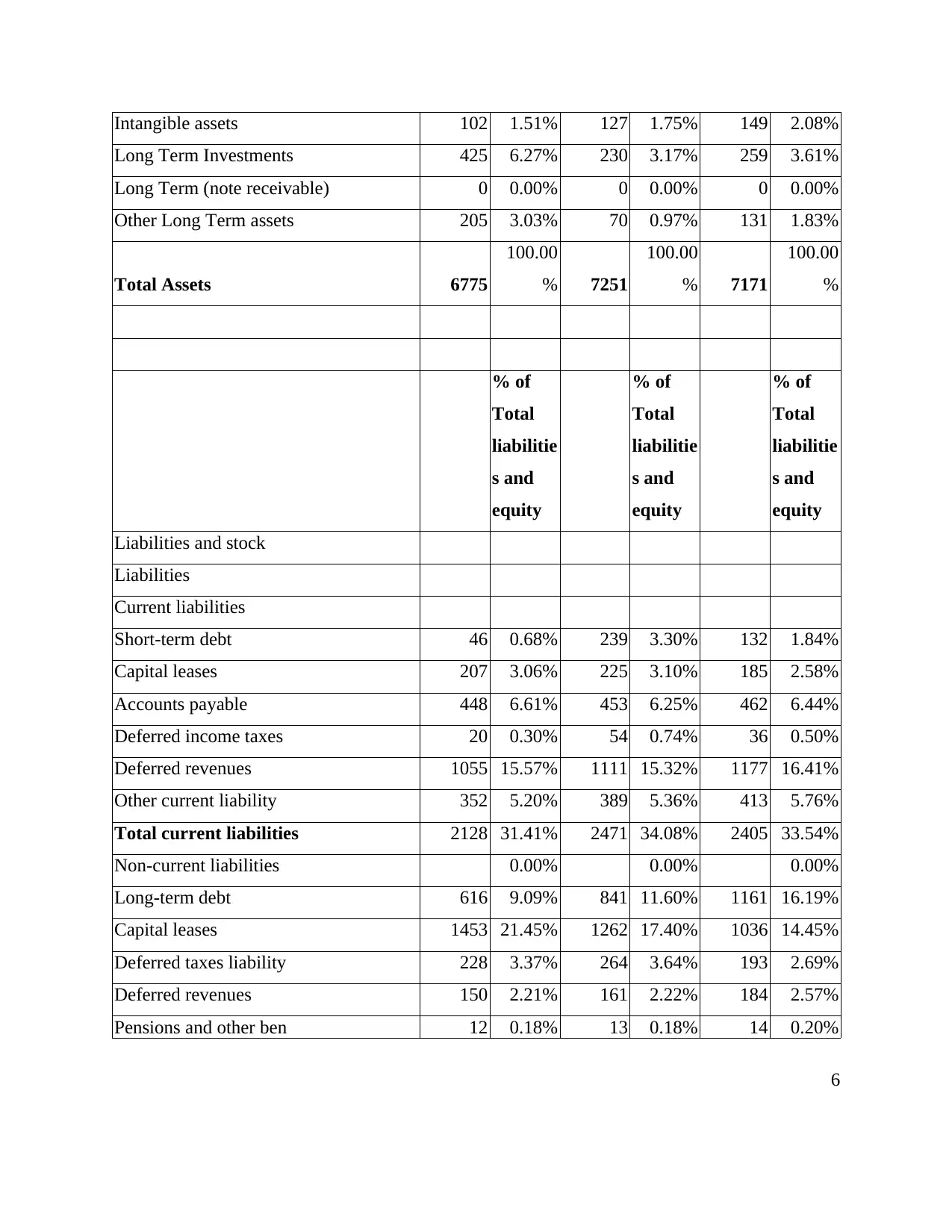

Intangible assets 102 1.51% 127 1.75% 149 2.08%

Long Term Investments 425 6.27% 230 3.17% 259 3.61%

Long Term (note receivable) 0 0.00% 0 0.00% 0 0.00%

Other Long Term assets 205 3.03% 70 0.97% 131 1.83%

Total Assets 6775

100.00

% 7251

100.00

% 7171

100.00

%

% of

Total

liabilitie

s and

equity

% of

Total

liabilitie

s and

equity

% of

Total

liabilitie

s and

equity

Liabilities and stock

Liabilities

Current liabilities

Short-term debt 46 0.68% 239 3.30% 132 1.84%

Capital leases 207 3.06% 225 3.10% 185 2.58%

Accounts payable 448 6.61% 453 6.25% 462 6.44%

Deferred income taxes 20 0.30% 54 0.74% 36 0.50%

Deferred revenues 1055 15.57% 1111 15.32% 1177 16.41%

Other current liability 352 5.20% 389 5.36% 413 5.76%

Total current liabilities 2128 31.41% 2471 34.08% 2405 33.54%

Non-current liabilities 0.00% 0.00% 0.00%

Long-term debt 616 9.09% 841 11.60% 1161 16.19%

Capital leases 1453 21.45% 1262 17.40% 1036 14.45%

Deferred taxes liability 228 3.37% 264 3.64% 193 2.69%

Deferred revenues 150 2.21% 161 2.22% 184 2.57%

Pensions and other ben 12 0.18% 13 0.18% 14 0.20%

6

Long Term Investments 425 6.27% 230 3.17% 259 3.61%

Long Term (note receivable) 0 0.00% 0 0.00% 0 0.00%

Other Long Term assets 205 3.03% 70 0.97% 131 1.83%

Total Assets 6775

100.00

% 7251

100.00

% 7171

100.00

%

% of

Total

liabilitie

s and

equity

% of

Total

liabilitie

s and

equity

% of

Total

liabilitie

s and

equity

Liabilities and stock

Liabilities

Current liabilities

Short-term debt 46 0.68% 239 3.30% 132 1.84%

Capital leases 207 3.06% 225 3.10% 185 2.58%

Accounts payable 448 6.61% 453 6.25% 462 6.44%

Deferred income taxes 20 0.30% 54 0.74% 36 0.50%

Deferred revenues 1055 15.57% 1111 15.32% 1177 16.41%

Other current liability 352 5.20% 389 5.36% 413 5.76%

Total current liabilities 2128 31.41% 2471 34.08% 2405 33.54%

Non-current liabilities 0.00% 0.00% 0.00%

Long-term debt 616 9.09% 841 11.60% 1161 16.19%

Capital leases 1453 21.45% 1262 17.40% 1036 14.45%

Deferred taxes liability 228 3.37% 264 3.64% 193 2.69%

Deferred revenues 150 2.21% 161 2.22% 184 2.57%

Pensions and other ben 12 0.18% 13 0.18% 14 0.20%

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

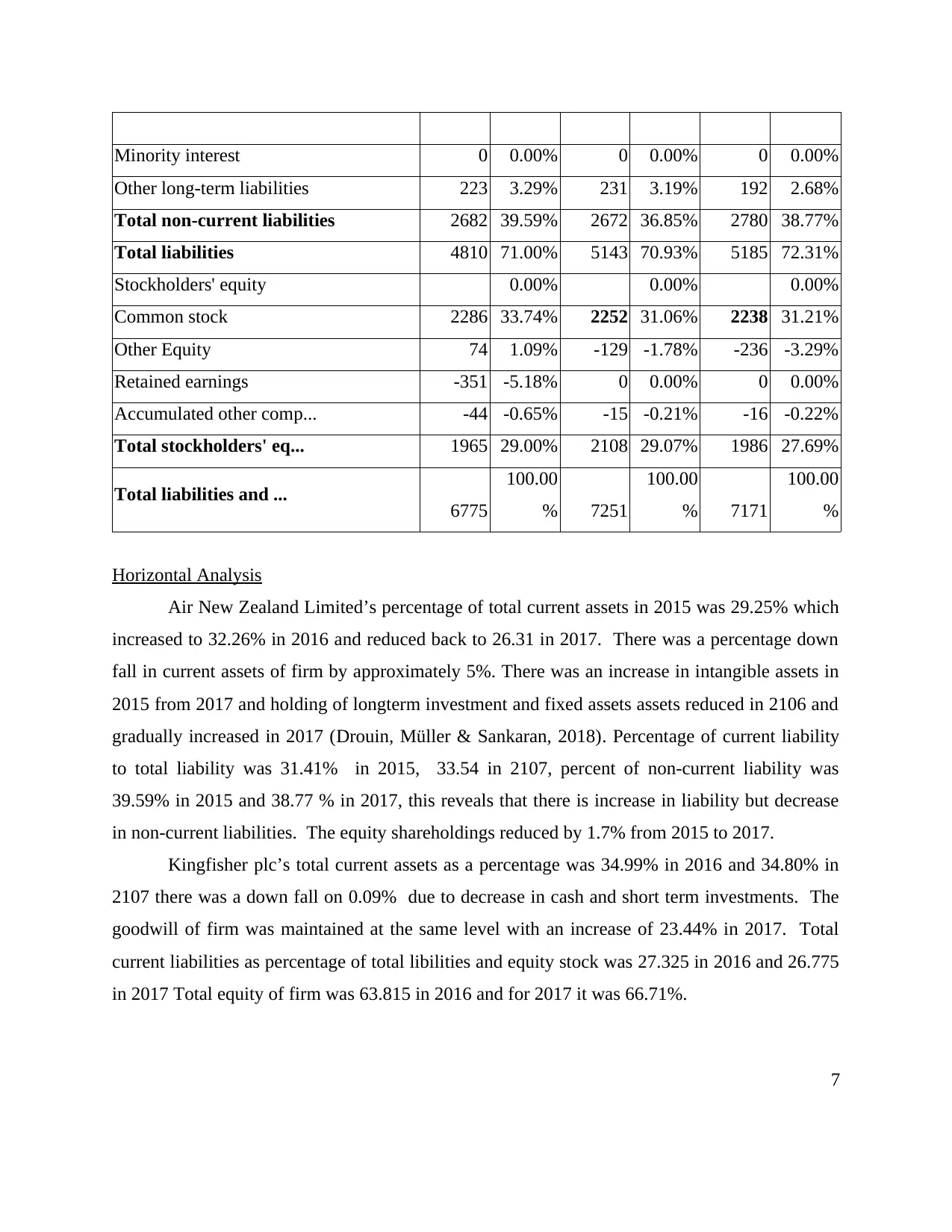

Minority interest 0 0.00% 0 0.00% 0 0.00%

Other long-term liabilities 223 3.29% 231 3.19% 192 2.68%

Total non-current liabilities 2682 39.59% 2672 36.85% 2780 38.77%

Total liabilities 4810 71.00% 5143 70.93% 5185 72.31%

Stockholders' equity 0.00% 0.00% 0.00%

Common stock 2286 33.74% 2252 31.06% 2238 31.21%

Other Equity 74 1.09% -129 -1.78% -236 -3.29%

Retained earnings -351 -5.18% 0 0.00% 0 0.00%

Accumulated other comp... -44 -0.65% -15 -0.21% -16 -0.22%

Total stockholders' eq... 1965 29.00% 2108 29.07% 1986 27.69%

Total liabilities and ... 6775

100.00

% 7251

100.00

% 7171

100.00

%

Horizontal Analysis

Air New Zealand Limited’s percentage of total current assets in 2015 was 29.25% which

increased to 32.26% in 2016 and reduced back to 26.31 in 2017. There was a percentage down

fall in current assets of firm by approximately 5%. There was an increase in intangible assets in

2015 from 2017 and holding of longterm investment and fixed assets assets reduced in 2106 and

gradually increased in 2017 (Drouin, Müller & Sankaran, 2018). Percentage of current liability

to total liability was 31.41% in 2015, 33.54 in 2107, percent of non-current liability was

39.59% in 2015 and 38.77 % in 2017, this reveals that there is increase in liability but decrease

in non-current liabilities. The equity shareholdings reduced by 1.7% from 2015 to 2017.

Kingfisher plc’s total current assets as a percentage was 34.99% in 2016 and 34.80% in

2107 there was a down fall on 0.09% due to decrease in cash and short term investments. The

goodwill of firm was maintained at the same level with an increase of 23.44% in 2017. Total

current liabilities as percentage of total libilities and equity stock was 27.325 in 2016 and 26.775

in 2017 Total equity of firm was 63.815 in 2016 and for 2017 it was 66.71%.

7

Other long-term liabilities 223 3.29% 231 3.19% 192 2.68%

Total non-current liabilities 2682 39.59% 2672 36.85% 2780 38.77%

Total liabilities 4810 71.00% 5143 70.93% 5185 72.31%

Stockholders' equity 0.00% 0.00% 0.00%

Common stock 2286 33.74% 2252 31.06% 2238 31.21%

Other Equity 74 1.09% -129 -1.78% -236 -3.29%

Retained earnings -351 -5.18% 0 0.00% 0 0.00%

Accumulated other comp... -44 -0.65% -15 -0.21% -16 -0.22%

Total stockholders' eq... 1965 29.00% 2108 29.07% 1986 27.69%

Total liabilities and ... 6775

100.00

% 7251

100.00

% 7171

100.00

%

Horizontal Analysis

Air New Zealand Limited’s percentage of total current assets in 2015 was 29.25% which

increased to 32.26% in 2016 and reduced back to 26.31 in 2017. There was a percentage down

fall in current assets of firm by approximately 5%. There was an increase in intangible assets in

2015 from 2017 and holding of longterm investment and fixed assets assets reduced in 2106 and

gradually increased in 2017 (Drouin, Müller & Sankaran, 2018). Percentage of current liability

to total liability was 31.41% in 2015, 33.54 in 2107, percent of non-current liability was

39.59% in 2015 and 38.77 % in 2017, this reveals that there is increase in liability but decrease

in non-current liabilities. The equity shareholdings reduced by 1.7% from 2015 to 2017.

Kingfisher plc’s total current assets as a percentage was 34.99% in 2016 and 34.80% in

2107 there was a down fall on 0.09% due to decrease in cash and short term investments. The

goodwill of firm was maintained at the same level with an increase of 23.44% in 2017. Total

current liabilities as percentage of total libilities and equity stock was 27.325 in 2016 and 26.775

in 2017 Total equity of firm was 63.815 in 2016 and for 2017 it was 66.71%.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

With a horizontal analysis of balance sheet of both organisations it can be stated that Air

New Zealand Limited have seen a growth in 2016 but in all aspects of item of balance sheet there

was a downfall in 2017. For kingfisher Plc it can be stated that it has maintained its position in

all these years. With a comparison between two it can be concluded that Kingfisher is better at

financial performance as compared to Air New Zealand Limited.

Vertical analysis

The percentage of increase in total assets of the Air New Zealand in increase in 2016

along with the short term investment. In 2017, there was a percentage down fall in current assets

of firm by 19.32% and this was due to reduction in holding of cash and its equivalents, short

term increments and major fall in other current assets. Total current liability increased by 16.12%

in 2016 and decreased by 2.675 in 2017. The decrement was due to reduction in capital lease

amount (Bestley & et.al., 2015). Total current liabilities decreased by 0.37% in 2016 and

increased by 4.04% in 2017 this was due to increase in long term debt. Shareholder's equity

increased by 7.03% in 2016 and diminished by 1.10% in 2017 and this down fall was due to

nullification of retained earnings.

There was a reduction in percentage holding of current assets of Kingfisher Plc by 3.55%

in 2016 and in 2017 it increased by 4.98%. The total assets reduced by 0.2% in 2016 and

increased by 5.56% in 2017. The current liability obligation of firm reduced by 3.3% in 2016 and

increased by 3.44% in 2017. Total liability of business increased by 0.43% in 2016 and reduced

by 1.31% in 2017. there was a rise in retained earnings and other resulted in raising total equity

of organisation by 9.46% in 2017.

From above vertical analysis of both business-organisations it could be stated that a percentage

rise that is calculated by taking previous years as a base of Air New Zealand Limited seen a goof

increment in 2016 and Kingfisher Plc had grown in 2017, so this can be stated that as kingfisher

Plc enjoyed a better individual incremental position between both.

CONCLUSION

From the above report it can be concluded that, for carrying out comparison between two

or more businesses belongs to same industry on which one can use financing tools such as

financial ratio, vertical and horizontal analysis of their financial statements. By using these tools

8

New Zealand Limited have seen a growth in 2016 but in all aspects of item of balance sheet there

was a downfall in 2017. For kingfisher Plc it can be stated that it has maintained its position in

all these years. With a comparison between two it can be concluded that Kingfisher is better at

financial performance as compared to Air New Zealand Limited.

Vertical analysis

The percentage of increase in total assets of the Air New Zealand in increase in 2016

along with the short term investment. In 2017, there was a percentage down fall in current assets

of firm by 19.32% and this was due to reduction in holding of cash and its equivalents, short

term increments and major fall in other current assets. Total current liability increased by 16.12%

in 2016 and decreased by 2.675 in 2017. The decrement was due to reduction in capital lease

amount (Bestley & et.al., 2015). Total current liabilities decreased by 0.37% in 2016 and

increased by 4.04% in 2017 this was due to increase in long term debt. Shareholder's equity

increased by 7.03% in 2016 and diminished by 1.10% in 2017 and this down fall was due to

nullification of retained earnings.

There was a reduction in percentage holding of current assets of Kingfisher Plc by 3.55%

in 2016 and in 2017 it increased by 4.98%. The total assets reduced by 0.2% in 2016 and

increased by 5.56% in 2017. The current liability obligation of firm reduced by 3.3% in 2016 and

increased by 3.44% in 2017. Total liability of business increased by 0.43% in 2016 and reduced

by 1.31% in 2017. there was a rise in retained earnings and other resulted in raising total equity

of organisation by 9.46% in 2017.

From above vertical analysis of both business-organisations it could be stated that a percentage

rise that is calculated by taking previous years as a base of Air New Zealand Limited seen a goof

increment in 2016 and Kingfisher Plc had grown in 2017, so this can be stated that as kingfisher

Plc enjoyed a better individual incremental position between both.

CONCLUSION

From the above report it can be concluded that, for carrying out comparison between two

or more businesses belongs to same industry on which one can use financing tools such as

financial ratio, vertical and horizontal analysis of their financial statements. By using these tools

8

a comparison of financial performance of Kingfisher Plc and Air New Zealand Limited is done

and it is analysed that both firms later enjoyed a good profitable position but former one is

goofed in liquidity and efficiency that gives regular returns to its shareholders. Evaluation of

financial statements reveals that kingfisher have kept a good record in its financial performance

as compared to Air New Zealand Limited. It grew in 2016 but in 2017 it has seen a slight

downfall.

9

and it is analysed that both firms later enjoyed a good profitable position but former one is

goofed in liquidity and efficiency that gives regular returns to its shareholders. Evaluation of

financial statements reveals that kingfisher have kept a good record in its financial performance

as compared to Air New Zealand Limited. It grew in 2016 but in 2017 it has seen a slight

downfall.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.