Business Accounting 3 Portfolio Activities Assessment 1

Added on 2023-06-03

41 Pages4611 Words467 Views

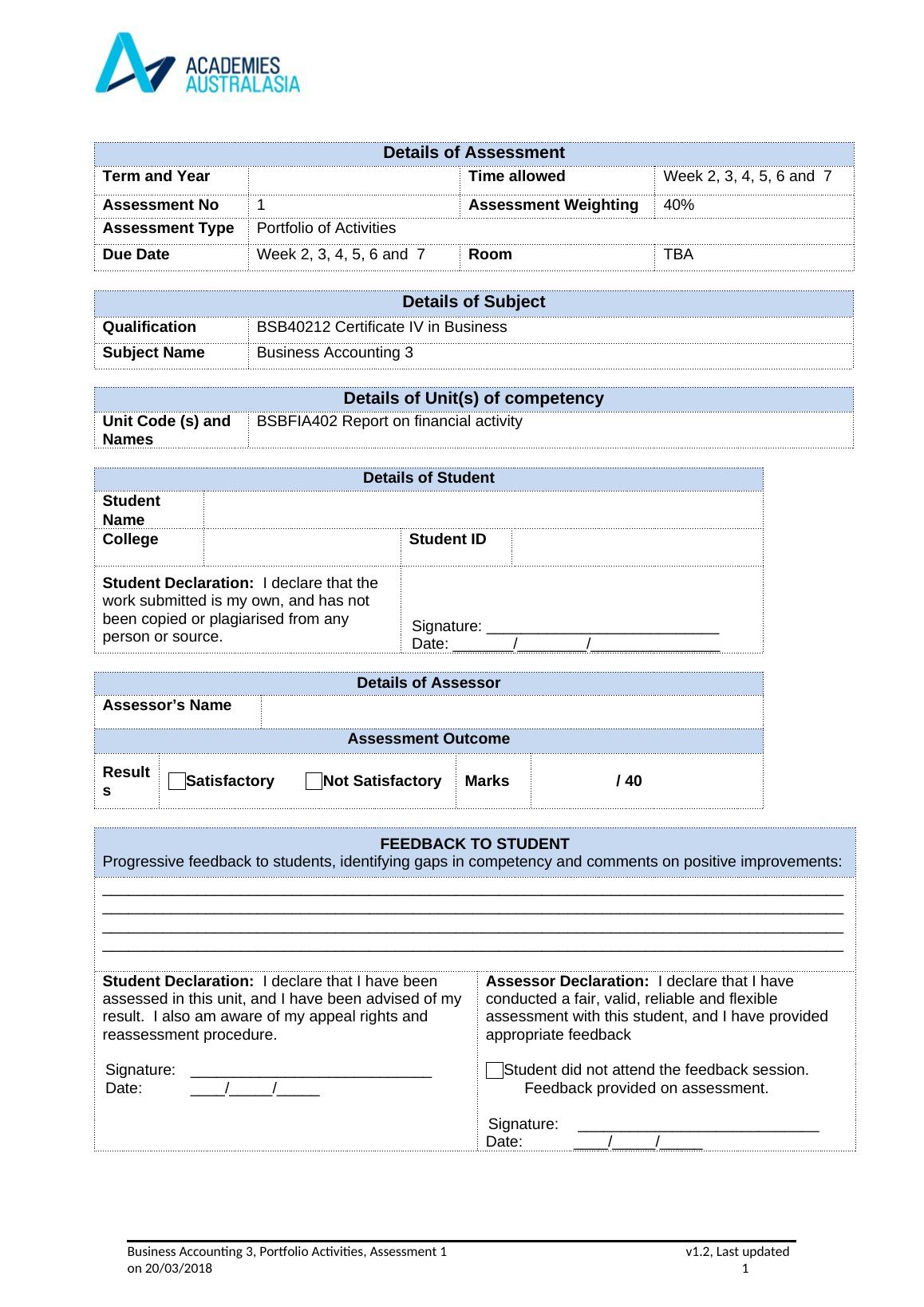

Details of Assessment

Term and Year Time allowed Week 2, 3, 4, 5, 6 and 7

Assessment No 1 Assessment Weighting 40%

Assessment Type Portfolio of Activities

Due Date Week 2, 3, 4, 5, 6 and 7 Room TBA

Details of Subject

Qualification BSB40212 Certificate IV in Business

Subject Name Business Accounting 3

Details of Unit(s) of competency

Unit Code (s) and

Names

BSBFIA402 Report on financial activity

Details of Student

Student

Name

College Student ID

Student Declaration: I declare that the

work submitted is my own, and has not

been copied or plagiarised from any

person or source. Signature: ___________________________

Date: _______/________/_______________

Details of Assessor

Assessor’s Name

Assessment Outcome

Result

s Satisfactory Not Satisfactory Marks / 40

FEEDBACK TO STUDENT

Progressive feedback to students, identifying gaps in competency and comments on positive improvements:

______________________________________________________________________________________

______________________________________________________________________________________

______________________________________________________________________________________

______________________________________________________________________________________

Student Declaration: I declare that I have been

assessed in this unit, and I have been advised of my

result. I also am aware of my appeal rights and

reassessment procedure.

Signature: ____________________________

Date: ____/_____/_____

Assessor Declaration: I declare that I have

conducted a fair, valid, reliable and flexible

assessment with this student, and I have provided

appropriate feedback

Student did not attend the feedback session.

Feedback provided on assessment.

Signature: ____________________________

Date: ____/_____/_____

Business Accounting 3, Portfolio Activities, Assessment 1 v1.2, Last updated

on 20/03/2018 1

Term and Year Time allowed Week 2, 3, 4, 5, 6 and 7

Assessment No 1 Assessment Weighting 40%

Assessment Type Portfolio of Activities

Due Date Week 2, 3, 4, 5, 6 and 7 Room TBA

Details of Subject

Qualification BSB40212 Certificate IV in Business

Subject Name Business Accounting 3

Details of Unit(s) of competency

Unit Code (s) and

Names

BSBFIA402 Report on financial activity

Details of Student

Student

Name

College Student ID

Student Declaration: I declare that the

work submitted is my own, and has not

been copied or plagiarised from any

person or source. Signature: ___________________________

Date: _______/________/_______________

Details of Assessor

Assessor’s Name

Assessment Outcome

Result

s Satisfactory Not Satisfactory Marks / 40

FEEDBACK TO STUDENT

Progressive feedback to students, identifying gaps in competency and comments on positive improvements:

______________________________________________________________________________________

______________________________________________________________________________________

______________________________________________________________________________________

______________________________________________________________________________________

Student Declaration: I declare that I have been

assessed in this unit, and I have been advised of my

result. I also am aware of my appeal rights and

reassessment procedure.

Signature: ____________________________

Date: ____/_____/_____

Assessor Declaration: I declare that I have

conducted a fair, valid, reliable and flexible

assessment with this student, and I have provided

appropriate feedback

Student did not attend the feedback session.

Feedback provided on assessment.

Signature: ____________________________

Date: ____/_____/_____

Business Accounting 3, Portfolio Activities, Assessment 1 v1.2, Last updated

on 20/03/2018 1

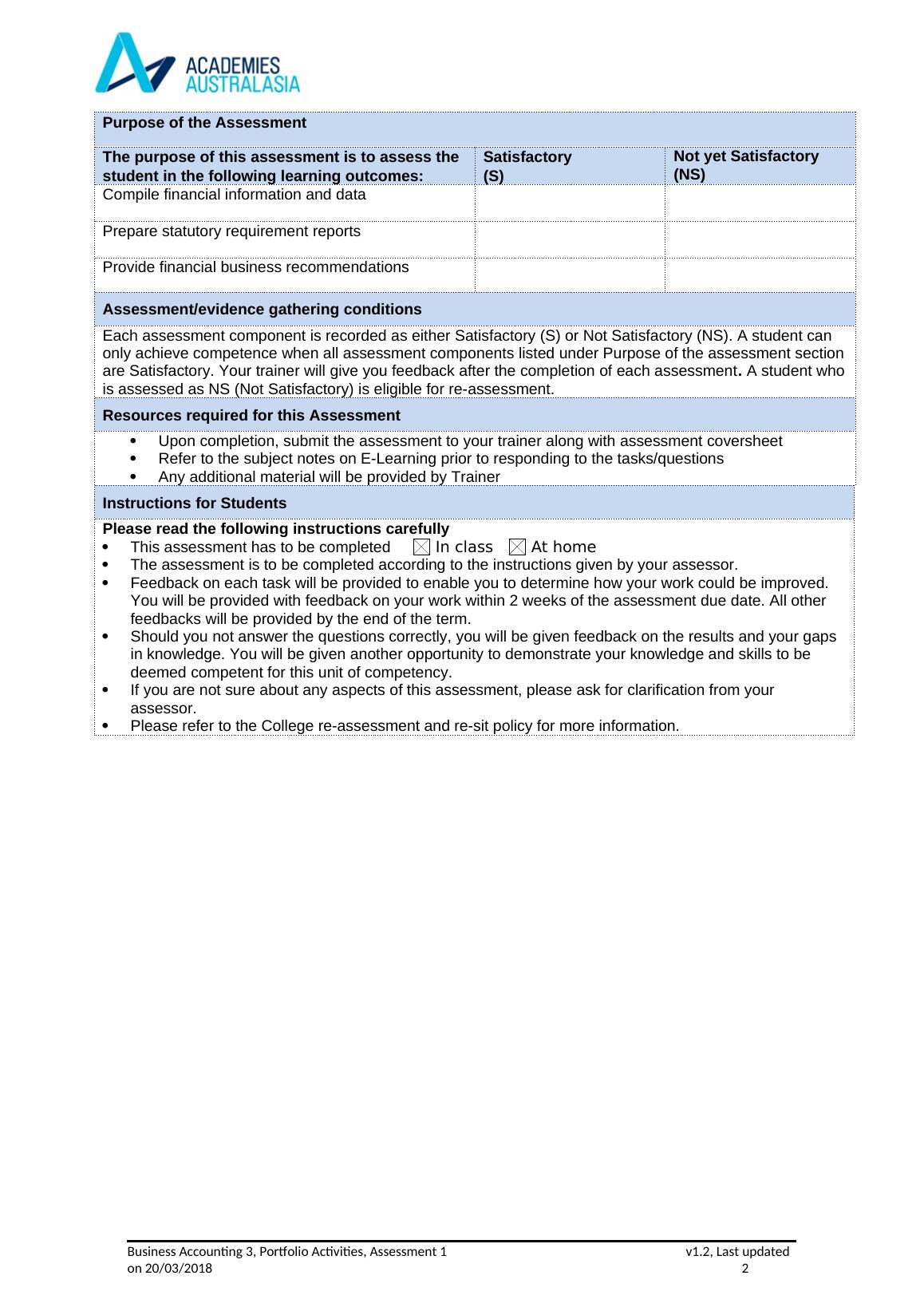

Purpose of the Assessment

The purpose of this assessment is to assess the

student in the following learning outcomes:

Satisfactory

(S)

Not yet Satisfactory

(NS)

Compile financial information and data

Prepare statutory requirement reports

Provide financial business recommendations

Assessment/evidence gathering conditions

Each assessment component is recorded as either Satisfactory (S) or Not Satisfactory (NS). A student can

only achieve competence when all assessment components listed under Purpose of the assessment section

are Satisfactory. Your trainer will give you feedback after the completion of each assessment. A student who

is assessed as NS (Not Satisfactory) is eligible for re-assessment.

Resources required for this Assessment

Upon completion, submit the assessment to your trainer along with assessment coversheet

Refer to the subject notes on E-Learning prior to responding to the tasks/questions

Any additional material will be provided by Trainer

Instructions for Students

Please read the following instructions carefully

This assessment has to be completed In class At home

The assessment is to be completed according to the instructions given by your assessor.

Feedback on each task will be provided to enable you to determine how your work could be improved.

You will be provided with feedback on your work within 2 weeks of the assessment due date. All other

feedbacks will be provided by the end of the term.

Should you not answer the questions correctly, you will be given feedback on the results and your gaps

in knowledge. You will be given another opportunity to demonstrate your knowledge and skills to be

deemed competent for this unit of competency.

If you are not sure about any aspects of this assessment, please ask for clarification from your

assessor.

Please refer to the College re-assessment and re-sit policy for more information.

Business Accounting 3, Portfolio Activities, Assessment 1 v1.2, Last updated

on 20/03/2018 2

The purpose of this assessment is to assess the

student in the following learning outcomes:

Satisfactory

(S)

Not yet Satisfactory

(NS)

Compile financial information and data

Prepare statutory requirement reports

Provide financial business recommendations

Assessment/evidence gathering conditions

Each assessment component is recorded as either Satisfactory (S) or Not Satisfactory (NS). A student can

only achieve competence when all assessment components listed under Purpose of the assessment section

are Satisfactory. Your trainer will give you feedback after the completion of each assessment. A student who

is assessed as NS (Not Satisfactory) is eligible for re-assessment.

Resources required for this Assessment

Upon completion, submit the assessment to your trainer along with assessment coversheet

Refer to the subject notes on E-Learning prior to responding to the tasks/questions

Any additional material will be provided by Trainer

Instructions for Students

Please read the following instructions carefully

This assessment has to be completed In class At home

The assessment is to be completed according to the instructions given by your assessor.

Feedback on each task will be provided to enable you to determine how your work could be improved.

You will be provided with feedback on your work within 2 weeks of the assessment due date. All other

feedbacks will be provided by the end of the term.

Should you not answer the questions correctly, you will be given feedback on the results and your gaps

in knowledge. You will be given another opportunity to demonstrate your knowledge and skills to be

deemed competent for this unit of competency.

If you are not sure about any aspects of this assessment, please ask for clarification from your

assessor.

Please refer to the College re-assessment and re-sit policy for more information.

Business Accounting 3, Portfolio Activities, Assessment 1 v1.2, Last updated

on 20/03/2018 2

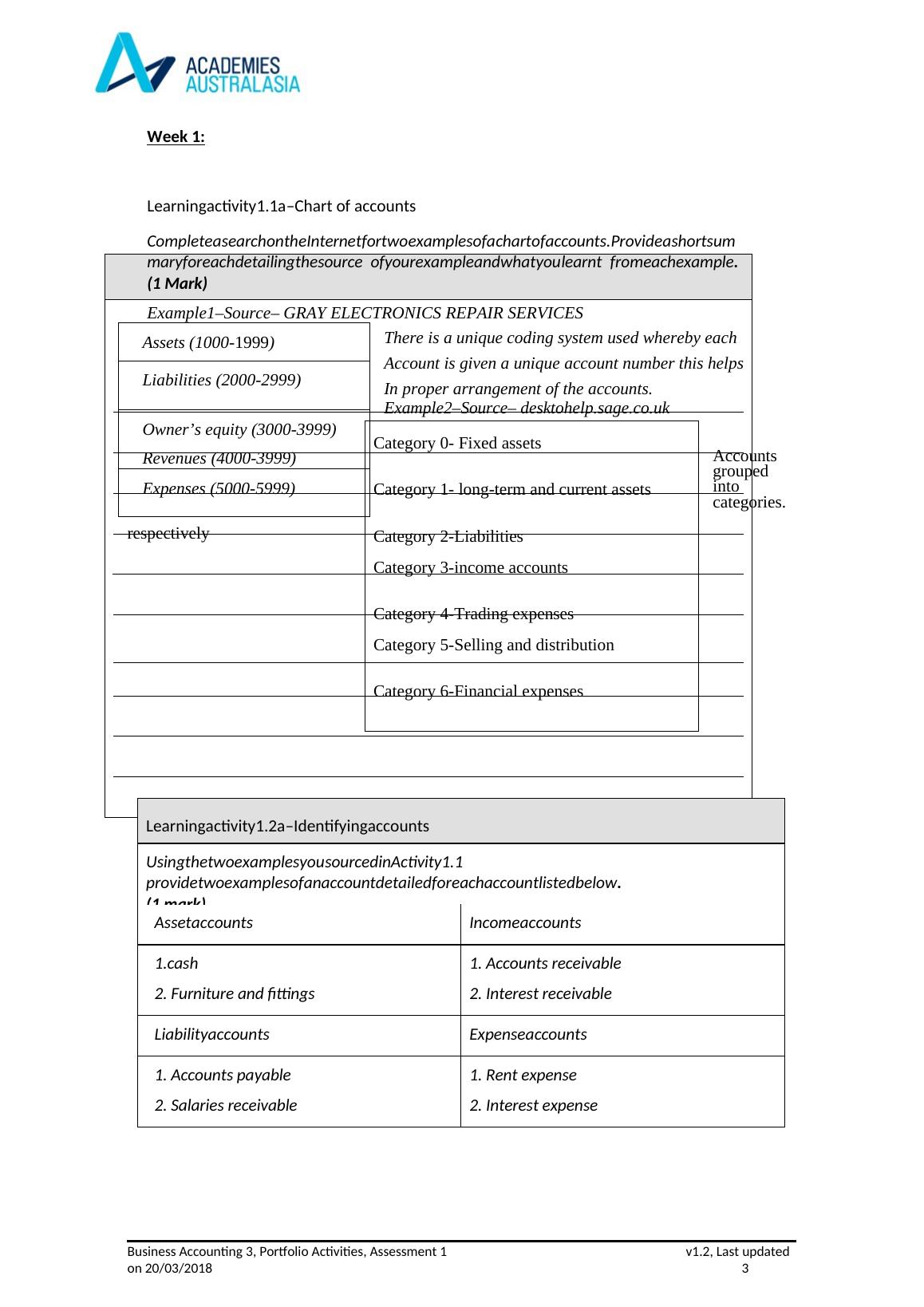

Week 1:

Learningactivity1.1a–Chart of accounts

Complete

asearchontheInternetfortwoexamplesofachartofaccounts.Provideashortsummaryfore

achdetailingthesource ofyourexampleandwhatyoulearnt fromeachexample.

(1 Mark)

Example1–Source– GRAY ELECTRONICS REPAIR SERVICES

There is a unique coding system used whereby each

Account is given a unique account number this helps

In proper arrangement of the accounts.

Accounts grouped into categories.

respectively

Learningactivity1.2a–Identifyingaccounts

Business Accounting 3, Portfolio Activities, Assessment 1 v1.2, Last updated

on 20/03/2018 3

Assets (1000-1999)

Liabilities (2000-2999)

Owner’s equity (3000-3999)

Revenues (4000-3999)

Expenses (5000-5999)

Category 0- Fixed assets

Category 1- long-term and current assets

Category 2-Liabilities

Category 3-income accounts

Category 4-Trading expenses

Category 5-Selling and distribution

Category 6-Financial expenses

Learningactivity1.1a–Chart of accounts

Complete

asearchontheInternetfortwoexamplesofachartofaccounts.Provideashortsummaryfore

achdetailingthesource ofyourexampleandwhatyoulearnt fromeachexample.

(1 Mark)

Example1–Source– GRAY ELECTRONICS REPAIR SERVICES

There is a unique coding system used whereby each

Account is given a unique account number this helps

In proper arrangement of the accounts.

Accounts grouped into categories.

respectively

Learningactivity1.2a–Identifyingaccounts

Business Accounting 3, Portfolio Activities, Assessment 1 v1.2, Last updated

on 20/03/2018 3

Assets (1000-1999)

Liabilities (2000-2999)

Owner’s equity (3000-3999)

Revenues (4000-3999)

Expenses (5000-5999)

Category 0- Fixed assets

Category 1- long-term and current assets

Category 2-Liabilities

Category 3-income accounts

Category 4-Trading expenses

Category 5-Selling and distribution

Category 6-Financial expenses

UsingthetwoexamplesyousourcedinActivity1.1

providetwoexamplesofanaccountdetailedforeachaccountlistedbelow.

(1 mark)

Assetaccounts Incomeaccounts

1.cash

2. Furniture and fittings

1. Accounts receivable

2. Interest receivable

Liabilityaccounts Expenseaccounts

1. Accounts payable

2. Salaries receivable

1. Rent expense

2. Interest expense

Learningactivity1.3a–Organizingandcodingaccounts (2marks)

Organizethefollowingaccountsin toachart ofaccounts and thencodeeachaccount.

stafftraining

ownercapital

income–

salesofgoodsandservices

accountspayable

pettycashaccount

freight

salariesandwages.

officeEquipment

companyownedvehicles

motorvehicleexpenses

ANZbankloan

Business Accounting 3, Portfolio Activities, Assessment 1 v1.2, Last updated

on 20/03/2018 4

providetwoexamplesofanaccountdetailedforeachaccountlistedbelow.

(1 mark)

Assetaccounts Incomeaccounts

1.cash

2. Furniture and fittings

1. Accounts receivable

2. Interest receivable

Liabilityaccounts Expenseaccounts

1. Accounts payable

2. Salaries receivable

1. Rent expense

2. Interest expense

Learningactivity1.3a–Organizingandcodingaccounts (2marks)

Organizethefollowingaccountsin toachart ofaccounts and thencodeeachaccount.

stafftraining

ownercapital

income–

salesofgoodsandservices

accountspayable

pettycashaccount

freight

salariesandwages.

officeEquipment

companyownedvehicles

motorvehicleexpenses

ANZbankloan

Business Accounting 3, Portfolio Activities, Assessment 1 v1.2, Last updated

on 20/03/2018 4

GSTcollected

ANZbank account

inventory

ANZbankaccountinterest–received

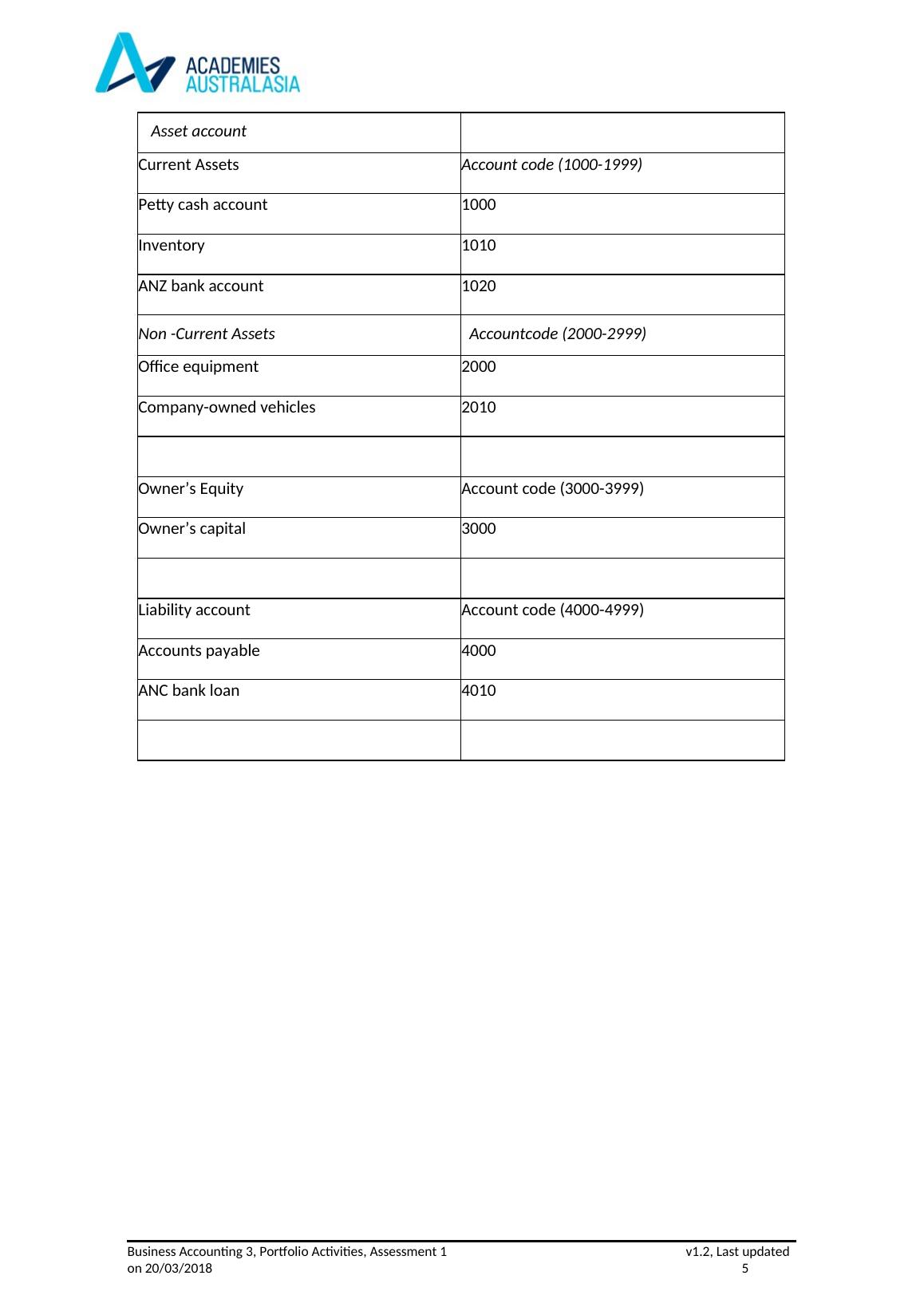

Asset account

Current Assets Account code (1000-1999)

Petty cash account 1000

Inventory 1010

ANZ bank account 1020

Non -Current Assets Accountcode (2000-2999)

Office equipment 2000

Company-owned vehicles 2010

Owner’s Equity Account code (3000-3999)

Owner’s capital 3000

Liability account Account code (4000-4999)

Accounts payable 4000

ANC bank loan 4010

Business Accounting 3, Portfolio Activities, Assessment 1 v1.2, Last updated

on 20/03/2018 5

ANZbank account

inventory

ANZbankaccountinterest–received

Asset account

Current Assets Account code (1000-1999)

Petty cash account 1000

Inventory 1010

ANZ bank account 1020

Non -Current Assets Accountcode (2000-2999)

Office equipment 2000

Company-owned vehicles 2010

Owner’s Equity Account code (3000-3999)

Owner’s capital 3000

Liability account Account code (4000-4999)

Accounts payable 4000

ANC bank loan 4010

Business Accounting 3, Portfolio Activities, Assessment 1 v1.2, Last updated

on 20/03/2018 5

Business Accounting 3, Portfolio Activities, Assessment 1 v1.2, Last updated

on 20/03/2018 6

on 20/03/2018 6

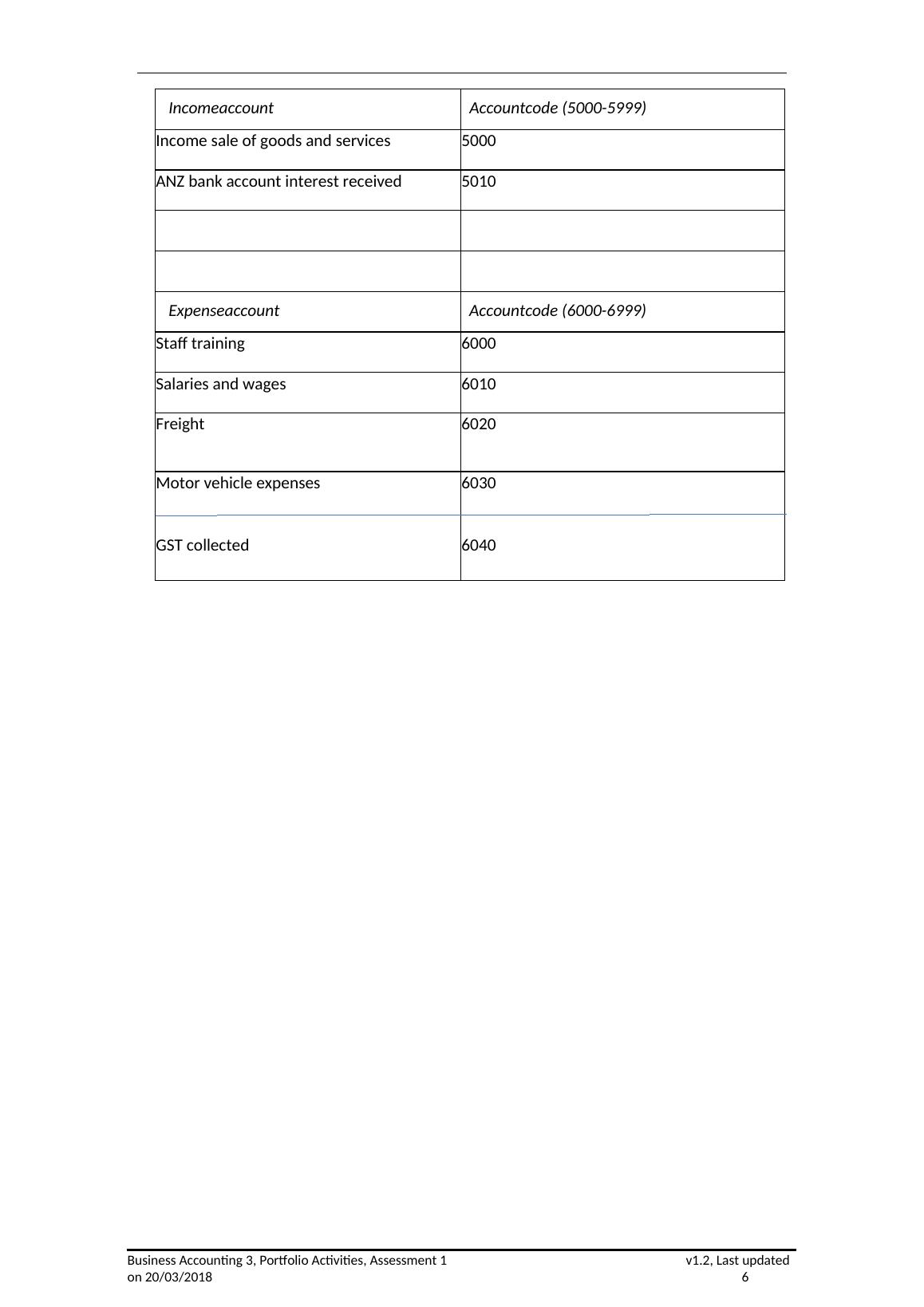

Incomeaccount Accountcode (5000-5999)

Income sale of goods and services 5000

ANZ bank account interest received 5010

Expenseaccount Accountcode (6000-6999)

Staff training 6000

Salaries and wages 6010

Freight 6020

Motor vehicle expenses

GST collected

6030

6040

Business Accounting 3, Portfolio Activities, Assessment 1 v1.2, Last updated

on 20/03/2018 7

Income sale of goods and services 5000

ANZ bank account interest received 5010

Expenseaccount Accountcode (6000-6999)

Staff training 6000

Salaries and wages 6010

Freight 6020

Motor vehicle expenses

GST collected

6030

6040

Business Accounting 3, Portfolio Activities, Assessment 1 v1.2, Last updated

on 20/03/2018 7

Week 2:

Learningactivity2.1a–Assetandliabilityvaluations

Whatisthedifferencebetweencurrentandnon-currentassets?(1 mark)

Current assets are the assets which can be converted to cash easily and are used to fund

the on-going operations of the company and pay the current expenses while non-current

assets are fixed assets that have a useful life of more than a year and cannot be easily

converted into cash.

Business Accounting 3, Portfolio Activities, Assessment 1 v1.2, Last updated

on 20/03/2018 8

Learningactivity2.1a–Assetandliabilityvaluations

Whatisthedifferencebetweencurrentandnon-currentassets?(1 mark)

Current assets are the assets which can be converted to cash easily and are used to fund

the on-going operations of the company and pay the current expenses while non-current

assets are fixed assets that have a useful life of more than a year and cannot be easily

converted into cash.

Business Accounting 3, Portfolio Activities, Assessment 1 v1.2, Last updated

on 20/03/2018 8

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

BSBFIM501 Diploma of Leadership and Managementlg...

|11

|2741

|112

Instructions Given by your Assessorlg...

|22

|2338

|307

BSBINM501 Manage An Information Or Knowledge Management Systemlg...

|7

|1728

|43

BSBINN601 Lead and Manage Organisational Changelg...

|40

|8755

|1486

Accounting & Budgeting Assessment No. 1lg...

|46

|10474

|359

BSBFIA402 Report on Financial Activitylg...

|6

|1519

|171