Stock Price Comparison: Boeing (BA) and General Dynamics (GD)

VerifiedAdded on 2023/04/25

|15

|4454

|391

Homework Assignment

AI Summary

This assignment provides a comprehensive comparison of Boeing (BA) and General Dynamics (GD) stock prices from October 2010 to October 2015. The analysis begins with calculating and visualizing stock returns using line charts, followed by a Jarque-Berra test to assess the normality of returns. The assignment then employs side-by-side boxplots and histograms to compare the distribution of returns, revealing that GD stock had a higher average return than BA stock. A risk-return relationship analysis is presented, including the calculation of coefficients of variation. The assignment further explores hypothesis testing, including a one-sample t-test to determine if the average return on GD stock differs from 2.8%, an F-test to compare the risks associated with GD and BA stocks, and a two-sample t-test to determine if both stocks have the same population average return. The statistical tests, including t-tests and F-tests, are performed with Excel outputs and interpretations. The analysis concludes that, based on the data, GD stock appears to be a better investment due to its higher average return and risk-reward profile. This assignment demonstrates the application of financial analysis techniques to evaluate and compare investment opportunities.

1

Comparison between Boeing Company- BA's Stock Price and General

Dynamics- GD's Stock Price

Task B

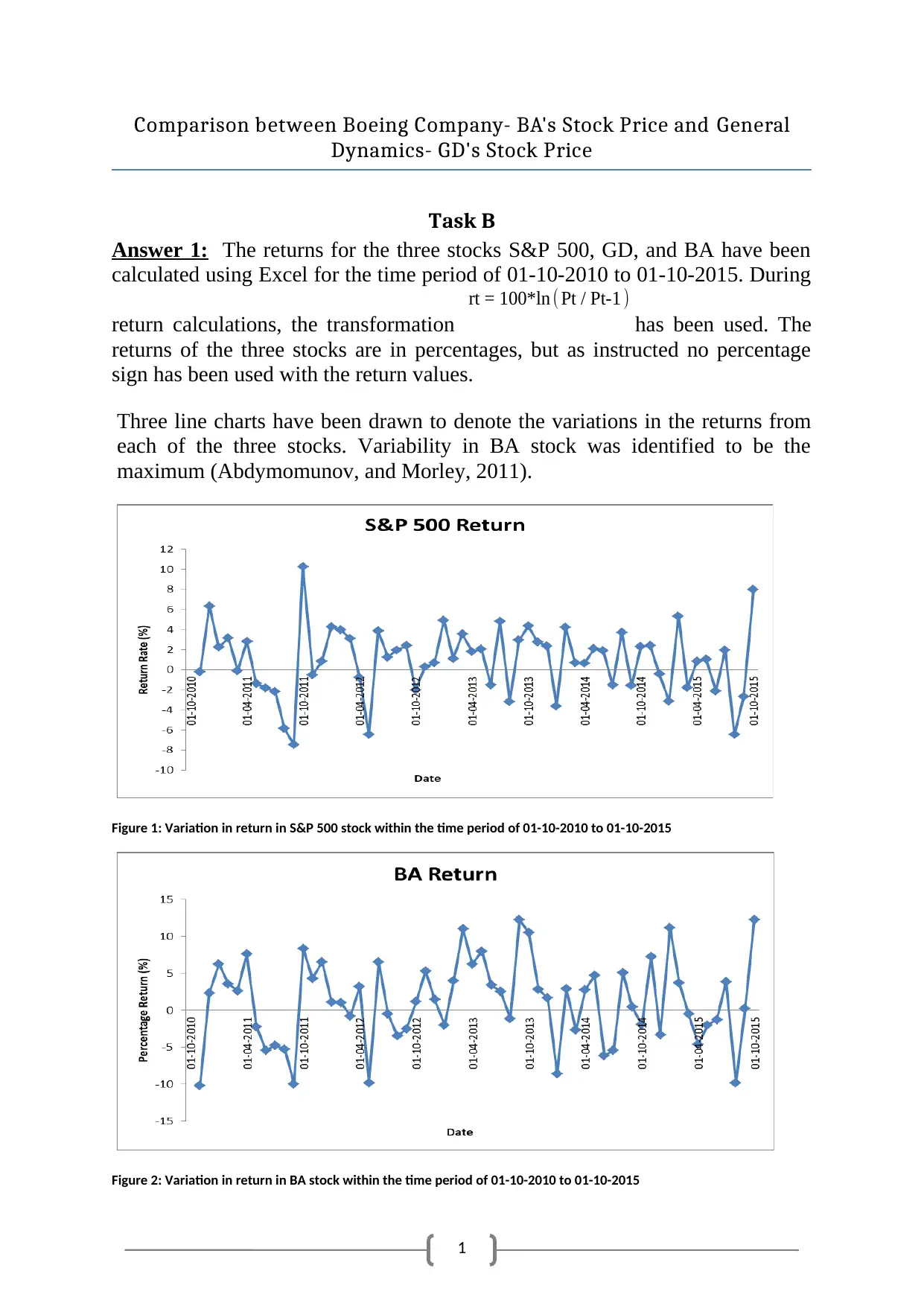

Answer 1: The returns for the three stocks S&P 500, GD, and BA have been

calculated using Excel for the time period of 01-10-2010 to 01-10-2015. During

return calculations, the transformation

rt = 100*ln ( Pt / Pt-1 )

has been used. The

returns of the three stocks are in percentages, but as instructed no percentage

sign has been used with the return values.

Three line charts have been drawn to denote the variations in the returns from

each of the three stocks. Variability in BA stock was identified to be the

maximum (Abdymomunov, and Morley, 2011).

Figure 1: Variation in return in S&P 500 stock within the time period of 01-10-2010 to 01-10-2015

Figure 2: Variation in return in BA stock within the time period of 01-10-2010 to 01-10-2015

Comparison between Boeing Company- BA's Stock Price and General

Dynamics- GD's Stock Price

Task B

Answer 1: The returns for the three stocks S&P 500, GD, and BA have been

calculated using Excel for the time period of 01-10-2010 to 01-10-2015. During

return calculations, the transformation

rt = 100*ln ( Pt / Pt-1 )

has been used. The

returns of the three stocks are in percentages, but as instructed no percentage

sign has been used with the return values.

Three line charts have been drawn to denote the variations in the returns from

each of the three stocks. Variability in BA stock was identified to be the

maximum (Abdymomunov, and Morley, 2011).

Figure 1: Variation in return in S&P 500 stock within the time period of 01-10-2010 to 01-10-2015

Figure 2: Variation in return in BA stock within the time period of 01-10-2010 to 01-10-2015

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

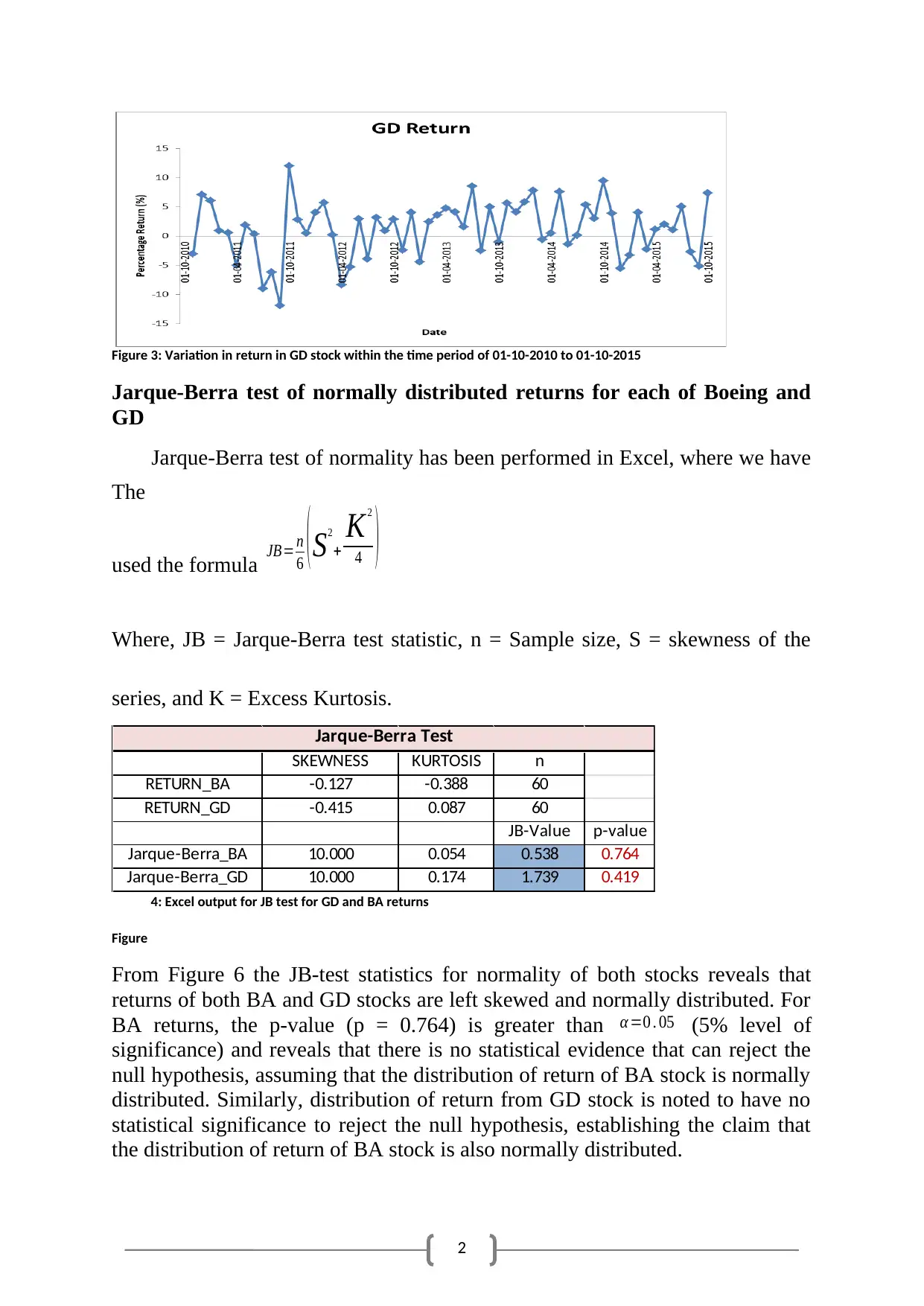

Figure 3: Variation in return in GD stock within the time period of 01-10-2010 to 01-10-2015

Jarque-Berra test of normally distributed returns for each of Boeing and

GD

The

Jarque-Berra test of normality has been performed in Excel, where we have

used the formula JB= n

6 ( S2

+

K2

4 )

Where, JB = Jarque-Berra test statistic, n = Sample size, S = skewness of the

series, and K = Excess Kurtosis.

SKEWNESS KURTOSIS n

RETURN_BA -0.127 -0.388 60

RETURN_GD -0.415 0.087 60

JB-Value p-value

Jarque-Berra_BA 10.000 0.054 0.538 0.764

Jarque-Berra_GD 10.000 0.174 1.739 0.419

Jarque-Berra Test

Figure

4: Excel output for JB test for GD and BA returns

From Figure 6 the JB-test statistics for normality of both stocks reveals that

returns of both BA and GD stocks are left skewed and normally distributed. For

BA returns, the p-value (p = 0.764) is greater than α =0 . 05 (5% level of

significance) and reveals that there is no statistical evidence that can reject the

null hypothesis, assuming that the distribution of return of BA stock is normally

distributed. Similarly, distribution of return from GD stock is noted to have no

statistical significance to reject the null hypothesis, establishing the claim that

the distribution of return of BA stock is also normally distributed.

Figure 3: Variation in return in GD stock within the time period of 01-10-2010 to 01-10-2015

Jarque-Berra test of normally distributed returns for each of Boeing and

GD

The

Jarque-Berra test of normality has been performed in Excel, where we have

used the formula JB= n

6 ( S2

+

K2

4 )

Where, JB = Jarque-Berra test statistic, n = Sample size, S = skewness of the

series, and K = Excess Kurtosis.

SKEWNESS KURTOSIS n

RETURN_BA -0.127 -0.388 60

RETURN_GD -0.415 0.087 60

JB-Value p-value

Jarque-Berra_BA 10.000 0.054 0.538 0.764

Jarque-Berra_GD 10.000 0.174 1.739 0.419

Jarque-Berra Test

Figure

4: Excel output for JB test for GD and BA returns

From Figure 6 the JB-test statistics for normality of both stocks reveals that

returns of both BA and GD stocks are left skewed and normally distributed. For

BA returns, the p-value (p = 0.764) is greater than α =0 . 05 (5% level of

significance) and reveals that there is no statistical evidence that can reject the

null hypothesis, assuming that the distribution of return of BA stock is normally

distributed. Similarly, distribution of return from GD stock is noted to have no

statistical significance to reject the null hypothesis, establishing the claim that

the distribution of return of BA stock is also normally distributed.

3

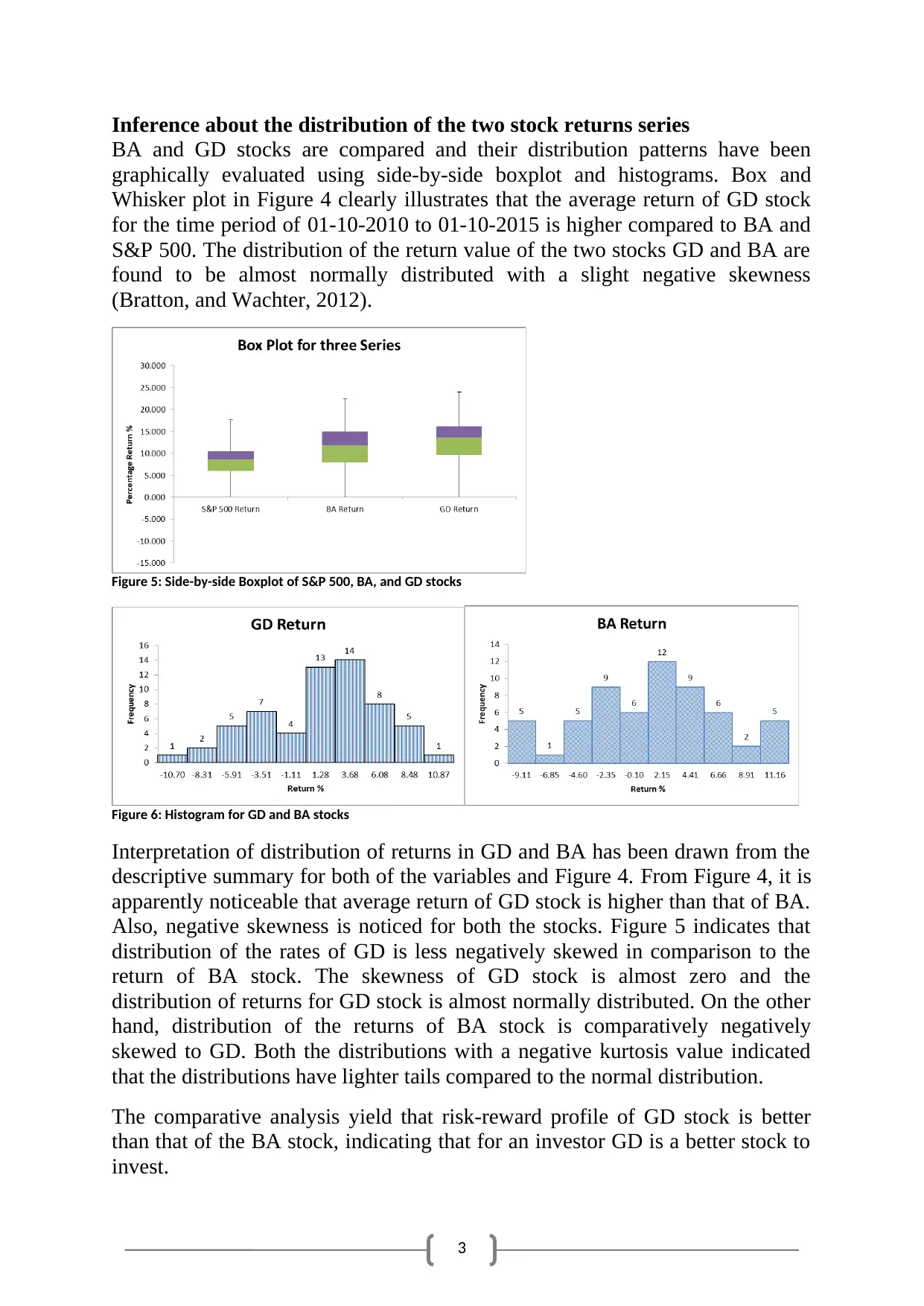

Inference about the distribution of the two stock returns series

BA and GD stocks are compared and their distribution patterns have been

graphically evaluated using side-by-side boxplot and histograms. Box and

Whisker plot in Figure 4 clearly illustrates that the average return of GD stock

for the time period of 01-10-2010 to 01-10-2015 is higher compared to BA and

S&P 500. The distribution of the return value of the two stocks GD and BA are

found to be almost normally distributed with a slight negative skewness

(Bratton, and Wachter, 2012).

Figure 5: Side-by-side Boxplot of S&P 500, BA, and GD stocks

Figure 6: Histogram for GD and BA stocks

Interpretation of distribution of returns in GD and BA has been drawn from the

descriptive summary for both of the variables and Figure 4. From Figure 4, it is

apparently noticeable that average return of GD stock is higher than that of BA.

Also, negative skewness is noticed for both the stocks. Figure 5 indicates that

distribution of the rates of GD is less negatively skewed in comparison to the

return of BA stock. The skewness of GD stock is almost zero and the

distribution of returns for GD stock is almost normally distributed. On the other

hand, distribution of the returns of BA stock is comparatively negatively

skewed to GD. Both the distributions with a negative kurtosis value indicated

that the distributions have lighter tails compared to the normal distribution.

The comparative analysis yield that risk-reward profile of GD stock is better

than that of the BA stock, indicating that for an investor GD is a better stock to

invest.

Inference about the distribution of the two stock returns series

BA and GD stocks are compared and their distribution patterns have been

graphically evaluated using side-by-side boxplot and histograms. Box and

Whisker plot in Figure 4 clearly illustrates that the average return of GD stock

for the time period of 01-10-2010 to 01-10-2015 is higher compared to BA and

S&P 500. The distribution of the return value of the two stocks GD and BA are

found to be almost normally distributed with a slight negative skewness

(Bratton, and Wachter, 2012).

Figure 5: Side-by-side Boxplot of S&P 500, BA, and GD stocks

Figure 6: Histogram for GD and BA stocks

Interpretation of distribution of returns in GD and BA has been drawn from the

descriptive summary for both of the variables and Figure 4. From Figure 4, it is

apparently noticeable that average return of GD stock is higher than that of BA.

Also, negative skewness is noticed for both the stocks. Figure 5 indicates that

distribution of the rates of GD is less negatively skewed in comparison to the

return of BA stock. The skewness of GD stock is almost zero and the

distribution of returns for GD stock is almost normally distributed. On the other

hand, distribution of the returns of BA stock is comparatively negatively

skewed to GD. Both the distributions with a negative kurtosis value indicated

that the distributions have lighter tails compared to the normal distribution.

The comparative analysis yield that risk-reward profile of GD stock is better

than that of the BA stock, indicating that for an investor GD is a better stock to

invest.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

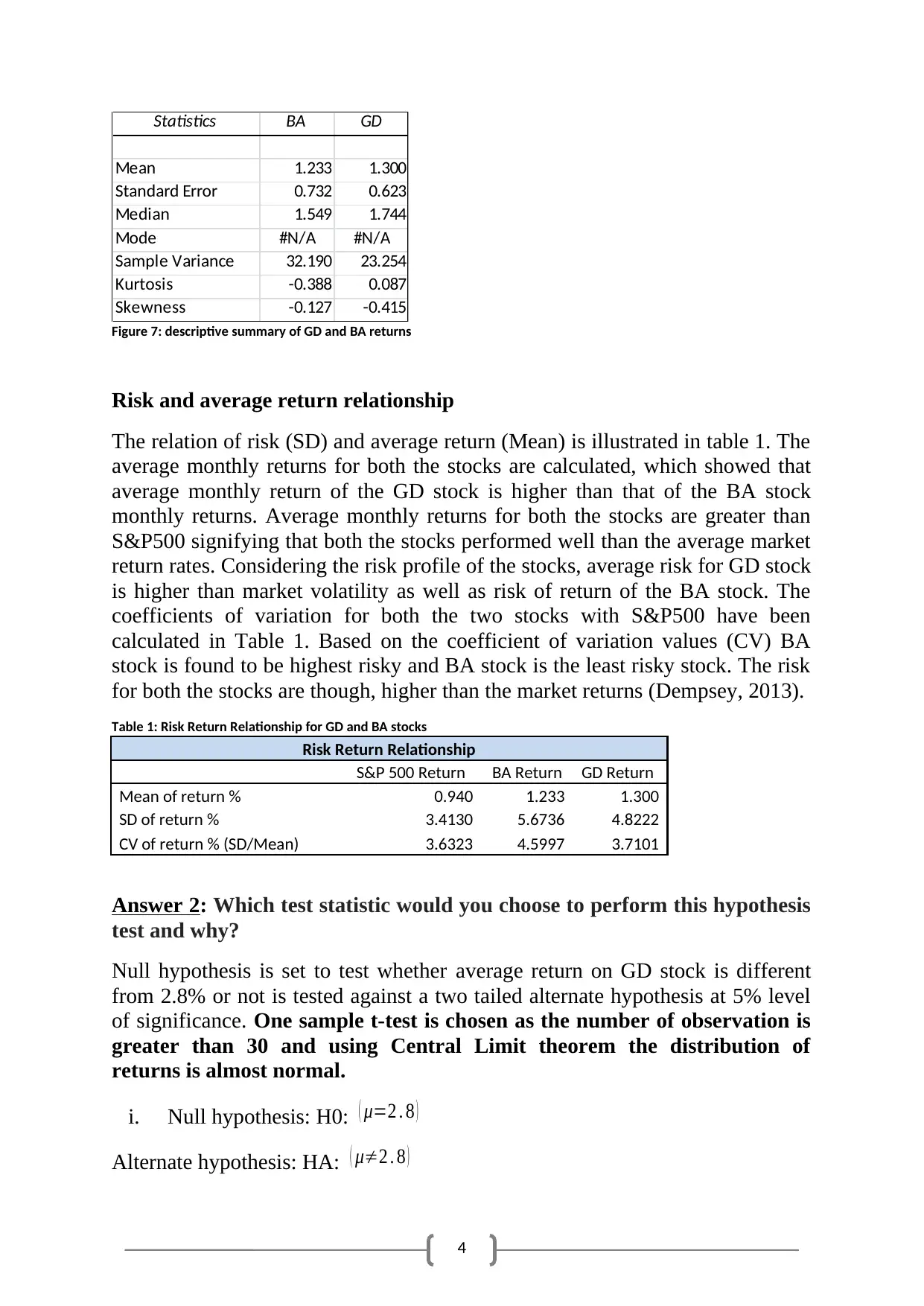

Statistics BA GD

Mean 1.233 1.300

Standard Error 0.732 0.623

Median 1.549 1.744

Mode #N/A #N/A

Sample Variance 32.190 23.254

Kurtosis -0.388 0.087

Skewness -0.127 -0.415

Figure 7: descriptive summary of GD and BA returns

Risk and average return relationship

The relation of risk (SD) and average return (Mean) is illustrated in table 1. The

average monthly returns for both the stocks are calculated, which showed that

average monthly return of the GD stock is higher than that of the BA stock

monthly returns. Average monthly returns for both the stocks are greater than

S&P500 signifying that both the stocks performed well than the average market

return rates. Considering the risk profile of the stocks, average risk for GD stock

is higher than market volatility as well as risk of return of the BA stock. The

coefficients of variation for both the two stocks with S&P500 have been

calculated in Table 1. Based on the coefficient of variation values (CV) BA

stock is found to be highest risky and BA stock is the least risky stock. The risk

for both the stocks are though, higher than the market returns (Dempsey, 2013).

Table 1: Risk Return Relationship for GD and BA stocks

Risk Return Relationship

S&P 500 Return BA Return GD Return

Mean of return % 0.940 1.233 1.300

SD of return % 3.4130 5.6736 4.8222

CV of return % (SD/Mean) 3.6323 4.5997 3.7101

Answer 2: Which test statistic would you choose to perform this hypothesis

test and why?

Null hypothesis is set to test whether average return on GD stock is different

from 2.8% or not is tested against a two tailed alternate hypothesis at 5% level

of significance. One sample t-test is chosen as the number of observation is

greater than 30 and using Central Limit theorem the distribution of

returns is almost normal.

i. Null hypothesis: H0: ( μ=2 . 8 )

Alternate hypothesis: HA: ( μ≠2 . 8 )

Statistics BA GD

Mean 1.233 1.300

Standard Error 0.732 0.623

Median 1.549 1.744

Mode #N/A #N/A

Sample Variance 32.190 23.254

Kurtosis -0.388 0.087

Skewness -0.127 -0.415

Figure 7: descriptive summary of GD and BA returns

Risk and average return relationship

The relation of risk (SD) and average return (Mean) is illustrated in table 1. The

average monthly returns for both the stocks are calculated, which showed that

average monthly return of the GD stock is higher than that of the BA stock

monthly returns. Average monthly returns for both the stocks are greater than

S&P500 signifying that both the stocks performed well than the average market

return rates. Considering the risk profile of the stocks, average risk for GD stock

is higher than market volatility as well as risk of return of the BA stock. The

coefficients of variation for both the two stocks with S&P500 have been

calculated in Table 1. Based on the coefficient of variation values (CV) BA

stock is found to be highest risky and BA stock is the least risky stock. The risk

for both the stocks are though, higher than the market returns (Dempsey, 2013).

Table 1: Risk Return Relationship for GD and BA stocks

Risk Return Relationship

S&P 500 Return BA Return GD Return

Mean of return % 0.940 1.233 1.300

SD of return % 3.4130 5.6736 4.8222

CV of return % (SD/Mean) 3.6323 4.5997 3.7101

Answer 2: Which test statistic would you choose to perform this hypothesis

test and why?

Null hypothesis is set to test whether average return on GD stock is different

from 2.8% or not is tested against a two tailed alternate hypothesis at 5% level

of significance. One sample t-test is chosen as the number of observation is

greater than 30 and using Central Limit theorem the distribution of

returns is almost normal.

i. Null hypothesis: H0: ( μ=2 . 8 )

Alternate hypothesis: HA: ( μ≠2 . 8 )

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

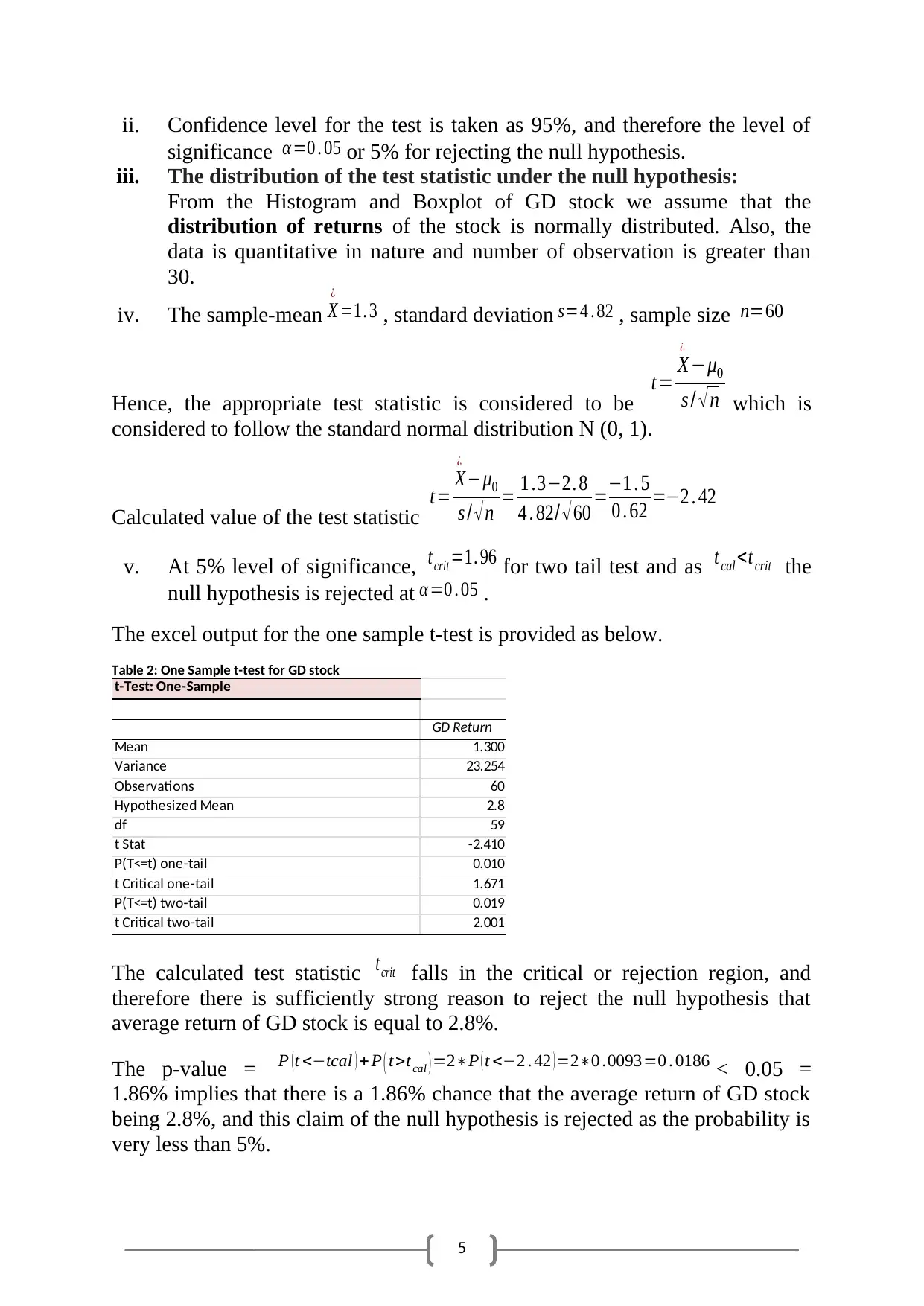

ii. Confidence level for the test is taken as 95%, and therefore the level of

significance α=0 . 05 or 5% for rejecting the null hypothesis.

iii. The distribution of the test statistic under the null hypothesis:

From the Histogram and Boxplot of GD stock we assume that the

distribution of returns of the stock is normally distributed. Also, the

data is quantitative in nature and number of observation is greater than

30.

iv. The sample-mean X

¿

=1. 3 , standard deviation s=4 . 82 , sample size n=60

Hence, the appropriate test statistic is considered to be t= X

¿

−μ0

s / √ n which is

considered to follow the standard normal distribution N (0, 1).

Calculated value of the test statistic t= X

¿

−μ0

s / √ n = 1 .3−2. 8

4 . 82/ √ 60 =−1 . 5

0 . 62 =−2 . 42

v. At 5% level of significance, tcrit =1. 96 for two tail test and as t cal <t crit the

null hypothesis is rejected at α=0 . 05 .

The excel output for the one sample t-test is provided as below.

Table 2: One Sample t-test for GD stock

t-Test: One-Sample

GD Return

Mean 1.300

Variance 23.254

Observations 60

Hypothesized Mean 2.8

df 59

t Stat -2.410

P(T<=t) one-tail 0.010

t Critical one-tail 1.671

P(T<=t) two-tail 0.019

t Critical two-tail 2.001

The calculated test statistic tcrit falls in the critical or rejection region, and

therefore there is sufficiently strong reason to reject the null hypothesis that

average return of GD stock is equal to 2.8%.

The p-value = P ( t <−tcal ) + P ( t>t cal ) =2∗P ( t <−2 . 42 ) =2∗0 .0093=0 . 0186 < 0.05 =

1.86% implies that there is a 1.86% chance that the average return of GD stock

being 2.8%, and this claim of the null hypothesis is rejected as the probability is

very less than 5%.

ii. Confidence level for the test is taken as 95%, and therefore the level of

significance α=0 . 05 or 5% for rejecting the null hypothesis.

iii. The distribution of the test statistic under the null hypothesis:

From the Histogram and Boxplot of GD stock we assume that the

distribution of returns of the stock is normally distributed. Also, the

data is quantitative in nature and number of observation is greater than

30.

iv. The sample-mean X

¿

=1. 3 , standard deviation s=4 . 82 , sample size n=60

Hence, the appropriate test statistic is considered to be t= X

¿

−μ0

s / √ n which is

considered to follow the standard normal distribution N (0, 1).

Calculated value of the test statistic t= X

¿

−μ0

s / √ n = 1 .3−2. 8

4 . 82/ √ 60 =−1 . 5

0 . 62 =−2 . 42

v. At 5% level of significance, tcrit =1. 96 for two tail test and as t cal <t crit the

null hypothesis is rejected at α=0 . 05 .

The excel output for the one sample t-test is provided as below.

Table 2: One Sample t-test for GD stock

t-Test: One-Sample

GD Return

Mean 1.300

Variance 23.254

Observations 60

Hypothesized Mean 2.8

df 59

t Stat -2.410

P(T<=t) one-tail 0.010

t Critical one-tail 1.671

P(T<=t) two-tail 0.019

t Critical two-tail 2.001

The calculated test statistic tcrit falls in the critical or rejection region, and

therefore there is sufficiently strong reason to reject the null hypothesis that

average return of GD stock is equal to 2.8%.

The p-value = P ( t <−tcal ) + P ( t>t cal ) =2∗P ( t <−2 . 42 ) =2∗0 .0093=0 . 0186 < 0.05 =

1.86% implies that there is a 1.86% chance that the average return of GD stock

being 2.8%, and this claim of the null hypothesis is rejected as the probability is

very less than 5%.

6

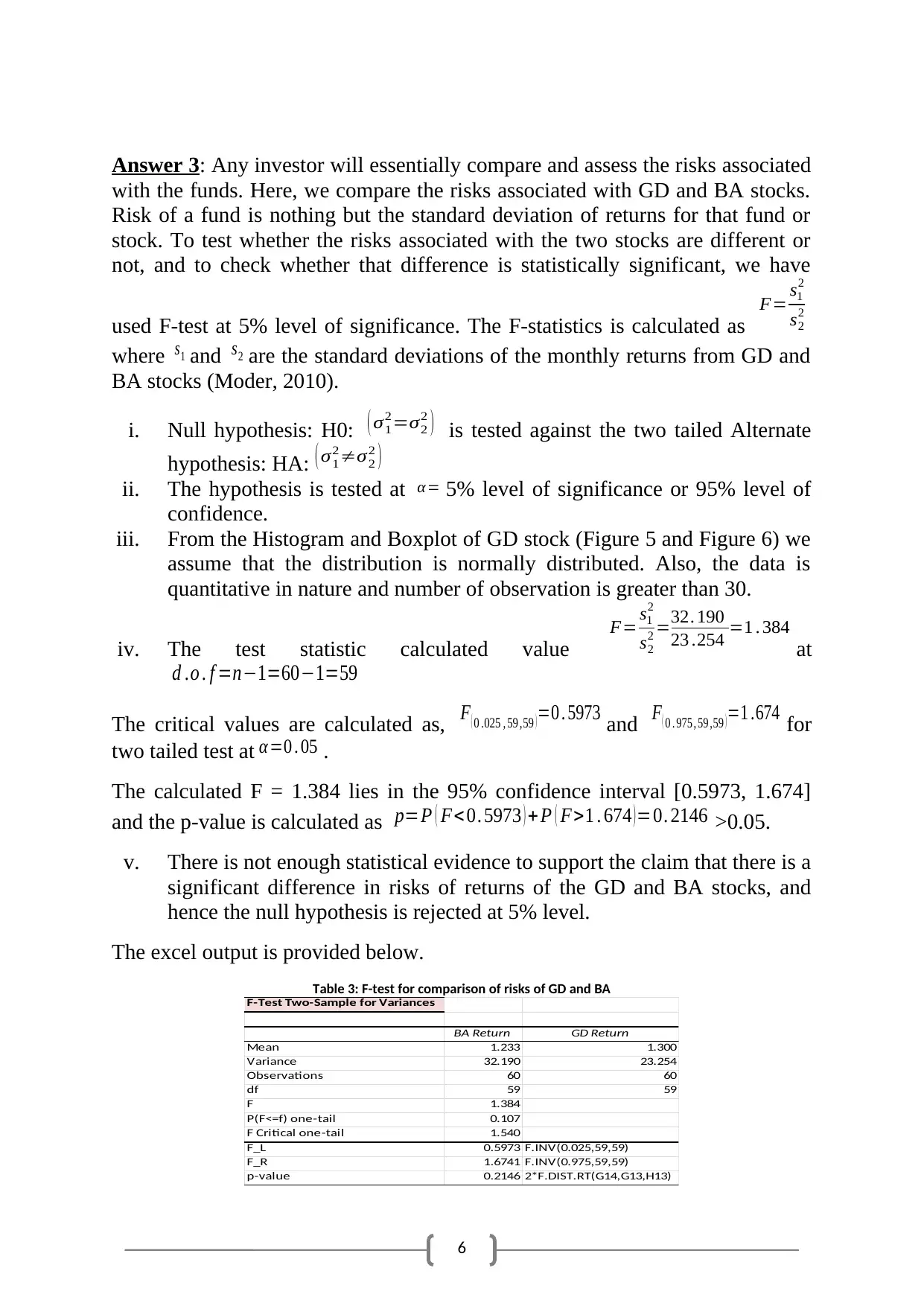

Answer 3: Any investor will essentially compare and assess the risks associated

with the funds. Here, we compare the risks associated with GD and BA stocks.

Risk of a fund is nothing but the standard deviation of returns for that fund or

stock. To test whether the risks associated with the two stocks are different or

not, and to check whether that difference is statistically significant, we have

used F-test at 5% level of significance. The F-statistics is calculated as

F= s1

2

s2

2

where s1 and s2 are the standard deviations of the monthly returns from GD and

BA stocks (Moder, 2010).

i. Null hypothesis: H0: ( σ1

2=σ2

2 ) is tested against the two tailed Alternate

hypothesis: HA: ( σ1

2≠σ2

2 )

ii. The hypothesis is tested at α = 5% level of significance or 95% level of

confidence.

iii. From the Histogram and Boxplot of GD stock (Figure 5 and Figure 6) we

assume that the distribution is normally distributed. Also, the data is

quantitative in nature and number of observation is greater than 30.

iv. The test statistic calculated value

F= s1

2

s2

2 =32. 190

23 .254 =1 . 384

at

d .o . f =n−1=60−1=59

The critical values are calculated as, F ( 0 .025 , 59 ,59 ) =0 . 5973 and F ( 0 . 975, 59 ,59 ) =1 .674 for

two tailed test at α=0 . 05 .

The calculated F = 1.384 lies in the 95% confidence interval [0.5973, 1.674]

and the p-value is calculated as p=P ( F< 0. 5973 ) + P ( F>1 . 674 ) =0. 2146 >0.05.

v. There is not enough statistical evidence to support the claim that there is a

significant difference in risks of returns of the GD and BA stocks, and

hence the null hypothesis is rejected at 5% level.

The excel output is provided below.

Table 3: F-test for comparison of risks of GD and BA

F-Test Two-Sample for Variances

BA Return GD Return

Mean 1.233 1.300

Variance 32.190 23.254

Observations 60 60

df 59 59

F 1.384

P(F<=f) one-tail 0.107

F Critical one-tail 1.540

F_L 0.5973 F.INV(0.025,59,59)

F_R 1.6741 F.INV(0.975,59,59)

p-value 0.2146 2*F.DIST.RT(G14,G13,H13)

Answer 3: Any investor will essentially compare and assess the risks associated

with the funds. Here, we compare the risks associated with GD and BA stocks.

Risk of a fund is nothing but the standard deviation of returns for that fund or

stock. To test whether the risks associated with the two stocks are different or

not, and to check whether that difference is statistically significant, we have

used F-test at 5% level of significance. The F-statistics is calculated as

F= s1

2

s2

2

where s1 and s2 are the standard deviations of the monthly returns from GD and

BA stocks (Moder, 2010).

i. Null hypothesis: H0: ( σ1

2=σ2

2 ) is tested against the two tailed Alternate

hypothesis: HA: ( σ1

2≠σ2

2 )

ii. The hypothesis is tested at α = 5% level of significance or 95% level of

confidence.

iii. From the Histogram and Boxplot of GD stock (Figure 5 and Figure 6) we

assume that the distribution is normally distributed. Also, the data is

quantitative in nature and number of observation is greater than 30.

iv. The test statistic calculated value

F= s1

2

s2

2 =32. 190

23 .254 =1 . 384

at

d .o . f =n−1=60−1=59

The critical values are calculated as, F ( 0 .025 , 59 ,59 ) =0 . 5973 and F ( 0 . 975, 59 ,59 ) =1 .674 for

two tailed test at α=0 . 05 .

The calculated F = 1.384 lies in the 95% confidence interval [0.5973, 1.674]

and the p-value is calculated as p=P ( F< 0. 5973 ) + P ( F>1 . 674 ) =0. 2146 >0.05.

v. There is not enough statistical evidence to support the claim that there is a

significant difference in risks of returns of the GD and BA stocks, and

hence the null hypothesis is rejected at 5% level.

The excel output is provided below.

Table 3: F-test for comparison of risks of GD and BA

F-Test Two-Sample for Variances

BA Return GD Return

Mean 1.233 1.300

Variance 32.190 23.254

Observations 60 60

df 59 59

F 1.384

P(F<=f) one-tail 0.107

F Critical one-tail 1.540

F_L 0.5973 F.INV(0.025,59,59)

F_R 1.6741 F.INV(0.975,59,59)

p-value 0.2146 2*F.DIST.RT(G14,G13,H13)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

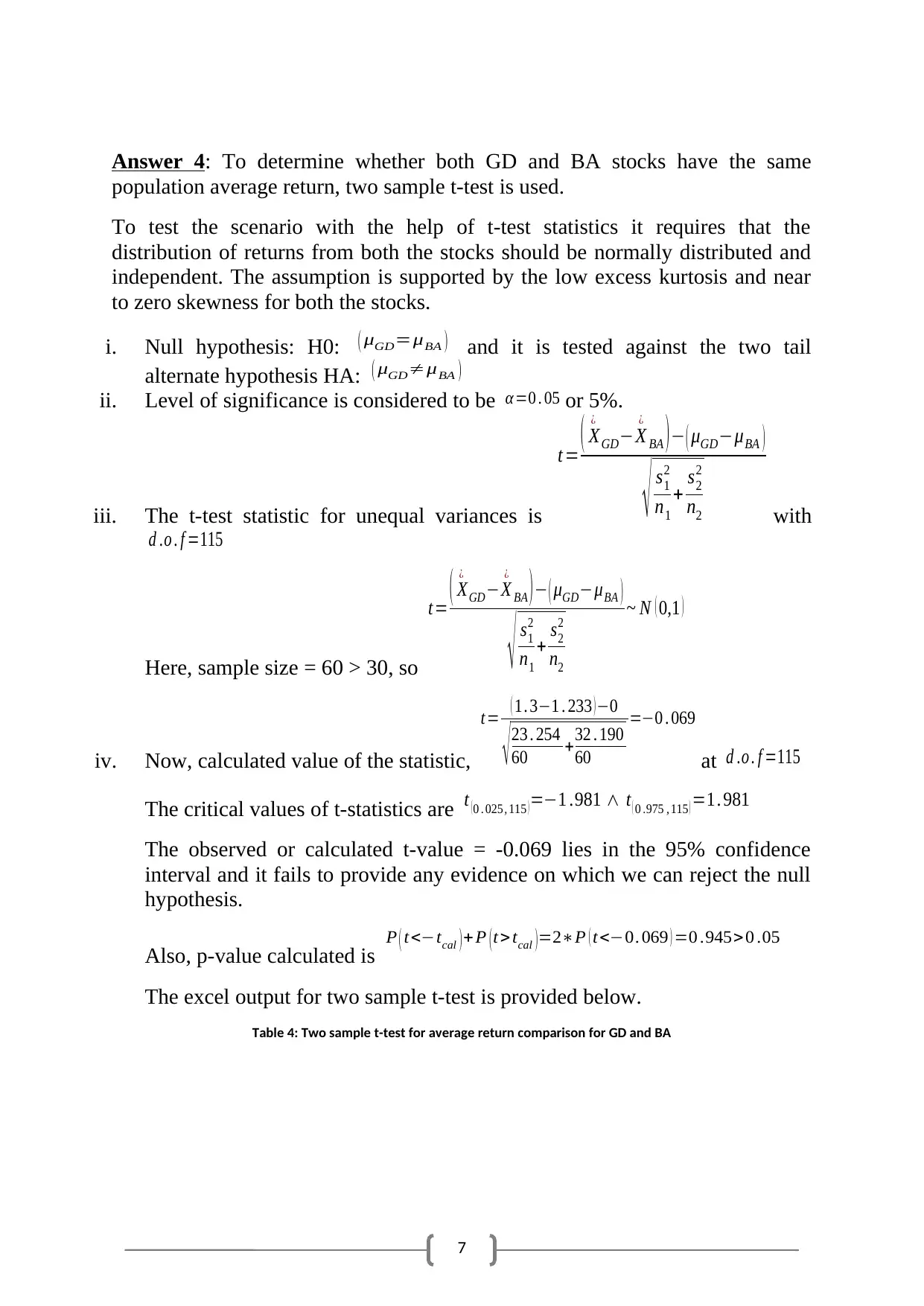

Answer 4: To determine whether both GD and BA stocks have the same

population average return, two sample t-test is used.

To test the scenario with the help of t-test statistics it requires that the

distribution of returns from both the stocks should be normally distributed and

independent. The assumption is supported by the low excess kurtosis and near

to zero skewness for both the stocks.

i. Null hypothesis: H0: ( μGD=μBA ) and it is tested against the two tail

alternate hypothesis HA: ( μGD≠μBA )

ii. Level of significance is considered to be α=0 . 05 or 5%.

iii. The t-test statistic for unequal variances is

t = ( X

¿

GD−X

¿

BA ) − ( μGD−μBA )

√ s1

2

n1

+ s2

2

n2 with

d .o . f =115

Here, sample size = 60 > 30, so

t= ( X

¿

GD−X

¿

BA ) − ( μGD−μBA )

√ s1

2

n1

+ s2

2

n2

~ N ( 0,1 )

iv. Now, calculated value of the statistic,

t= ( 1. 3−1 . 233 ) −0

√ 23 . 254

60 +32 . 190

60

=−0 . 069

at d .o . f =115

The critical values of t-statistics are t ( 0 . 025, 115 ) =−1 .981 ∧ t ( 0 .975 , 115 ) =1. 981

The observed or calculated t-value = -0.069 lies in the 95% confidence

interval and it fails to provide any evidence on which we can reject the null

hypothesis.

Also, p-value calculated is P ( t<−tcal ) +P ( t > tcal )=2∗P ( t<−0. 069 ) =0 .945> 0 .05

The excel output for two sample t-test is provided below.

Table 4: Two sample t-test for average return comparison for GD and BA

Answer 4: To determine whether both GD and BA stocks have the same

population average return, two sample t-test is used.

To test the scenario with the help of t-test statistics it requires that the

distribution of returns from both the stocks should be normally distributed and

independent. The assumption is supported by the low excess kurtosis and near

to zero skewness for both the stocks.

i. Null hypothesis: H0: ( μGD=μBA ) and it is tested against the two tail

alternate hypothesis HA: ( μGD≠μBA )

ii. Level of significance is considered to be α=0 . 05 or 5%.

iii. The t-test statistic for unequal variances is

t = ( X

¿

GD−X

¿

BA ) − ( μGD−μBA )

√ s1

2

n1

+ s2

2

n2 with

d .o . f =115

Here, sample size = 60 > 30, so

t= ( X

¿

GD−X

¿

BA ) − ( μGD−μBA )

√ s1

2

n1

+ s2

2

n2

~ N ( 0,1 )

iv. Now, calculated value of the statistic,

t= ( 1. 3−1 . 233 ) −0

√ 23 . 254

60 +32 . 190

60

=−0 . 069

at d .o . f =115

The critical values of t-statistics are t ( 0 . 025, 115 ) =−1 .981 ∧ t ( 0 .975 , 115 ) =1. 981

The observed or calculated t-value = -0.069 lies in the 95% confidence

interval and it fails to provide any evidence on which we can reject the null

hypothesis.

Also, p-value calculated is P ( t<−tcal ) +P ( t > tcal )=2∗P ( t<−0. 069 ) =0 .945> 0 .05

The excel output for two sample t-test is provided below.

Table 4: Two sample t-test for average return comparison for GD and BA

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

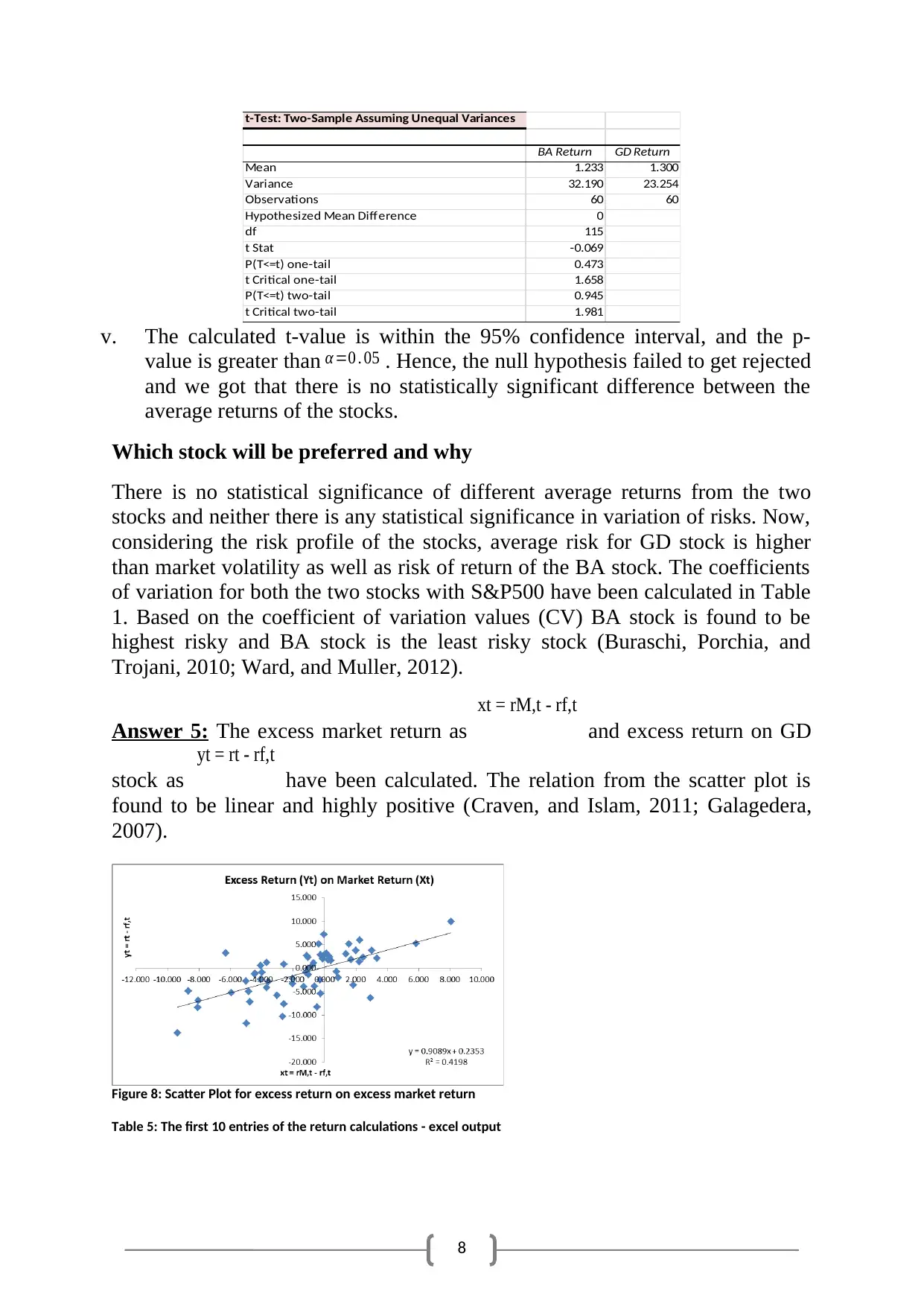

t-Test: Two-Sample Assuming Unequal Variances

BA Return GD Return

Mean 1.233 1.300

Variance 32.190 23.254

Observations 60 60

Hypothesized Mean Difference 0

df 115

t Stat -0.069

P(T<=t) one-tail 0.473

t Critical one-tail 1.658

P(T<=t) two-tail 0.945

t Critical two-tail 1.981

v. The calculated t-value is within the 95% confidence interval, and the p-

value is greater than α =0 . 05 . Hence, the null hypothesis failed to get rejected

and we got that there is no statistically significant difference between the

average returns of the stocks.

Which stock will be preferred and why

There is no statistical significance of different average returns from the two

stocks and neither there is any statistical significance in variation of risks. Now,

considering the risk profile of the stocks, average risk for GD stock is higher

than market volatility as well as risk of return of the BA stock. The coefficients

of variation for both the two stocks with S&P500 have been calculated in Table

1. Based on the coefficient of variation values (CV) BA stock is found to be

highest risky and BA stock is the least risky stock (Buraschi, Porchia, and

Trojani, 2010; Ward, and Muller, 2012).

Answer 5: The excess market return as

xt = rM,t - rf,t

and excess return on GD

stock as

yt = rt - rf,t

have been calculated. The relation from the scatter plot is

found to be linear and highly positive (Craven, and Islam, 2011; Galagedera,

2007).

Figure 8: Scatter Plot for excess return on excess market return

Table 5: The first 10 entries of the return calculations - excel output

t-Test: Two-Sample Assuming Unequal Variances

BA Return GD Return

Mean 1.233 1.300

Variance 32.190 23.254

Observations 60 60

Hypothesized Mean Difference 0

df 115

t Stat -0.069

P(T<=t) one-tail 0.473

t Critical one-tail 1.658

P(T<=t) two-tail 0.945

t Critical two-tail 1.981

v. The calculated t-value is within the 95% confidence interval, and the p-

value is greater than α =0 . 05 . Hence, the null hypothesis failed to get rejected

and we got that there is no statistically significant difference between the

average returns of the stocks.

Which stock will be preferred and why

There is no statistical significance of different average returns from the two

stocks and neither there is any statistical significance in variation of risks. Now,

considering the risk profile of the stocks, average risk for GD stock is higher

than market volatility as well as risk of return of the BA stock. The coefficients

of variation for both the two stocks with S&P500 have been calculated in Table

1. Based on the coefficient of variation values (CV) BA stock is found to be

highest risky and BA stock is the least risky stock (Buraschi, Porchia, and

Trojani, 2010; Ward, and Muller, 2012).

Answer 5: The excess market return as

xt = rM,t - rf,t

and excess return on GD

stock as

yt = rt - rf,t

have been calculated. The relation from the scatter plot is

found to be linear and highly positive (Craven, and Islam, 2011; Galagedera,

2007).

Figure 8: Scatter Plot for excess return on excess market return

Table 5: The first 10 entries of the return calculations - excel output

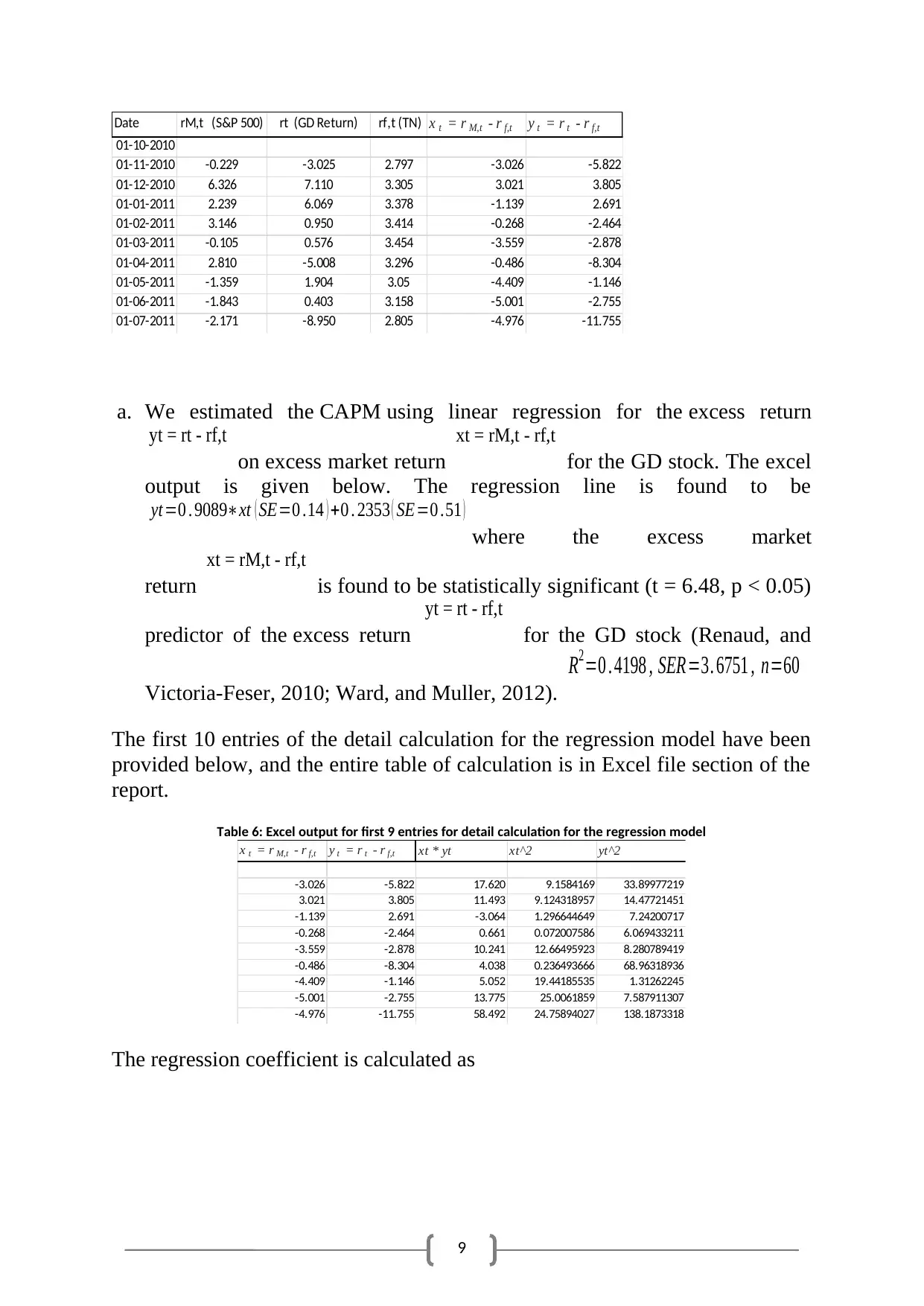

9

Date rM,t (S&P 500) rt (GD Return) rf,t (TN) x t = r M,t - r f,t y t = r t - r f,t

01-10-2010

01-11-2010 -0.229 -3.025 2.797 -3.026 -5.822

01-12-2010 6.326 7.110 3.305 3.021 3.805

01-01-2011 2.239 6.069 3.378 -1.139 2.691

01-02-2011 3.146 0.950 3.414 -0.268 -2.464

01-03-2011 -0.105 0.576 3.454 -3.559 -2.878

01-04-2011 2.810 -5.008 3.296 -0.486 -8.304

01-05-2011 -1.359 1.904 3.05 -4.409 -1.146

01-06-2011 -1.843 0.403 3.158 -5.001 -2.755

01-07-2011 -2.171 -8.950 2.805 -4.976 -11.755

a. We estimated the CAPM using linear regression for the excess return

yt = rt - rf,t

on excess market return

xt = rM,t - rf,t

for the GD stock. The excel

output is given below. The regression line is found to be

yt=0 . 9089∗xt ( SE=0 .14 ) +0 . 2353 ( SE=0 .51 )

where the excess market

return

xt = rM,t - rf,t

is found to be statistically significant (t = 6.48, p < 0.05)

predictor of the excess return

yt = rt - rf,t

for the GD stock (Renaud, and

Victoria-Feser, 2010; Ward, and Muller, 2012).

R2=0 . 4198 , SER=3. 6751 , n=60

The first 10 entries of the detail calculation for the regression model have been

provided below, and the entire table of calculation is in Excel file section of the

report.

Table 6: Excel output for first 9 entries for detail calculation for the regression model

x t = r M,t - r f,t y t = r t - r f,t xt * yt xt^2 yt^2

-3.026 -5.822 17.620 9.1584169 33.89977219

3.021 3.805 11.493 9.124318957 14.47721451

-1.139 2.691 -3.064 1.296644649 7.24200717

-0.268 -2.464 0.661 0.072007586 6.069433211

-3.559 -2.878 10.241 12.66495923 8.280789419

-0.486 -8.304 4.038 0.236493666 68.96318936

-4.409 -1.146 5.052 19.44185535 1.31262245

-5.001 -2.755 13.775 25.0061859 7.587911307

-4.976 -11.755 58.492 24.75894027 138.1873318

The regression coefficient is calculated as

Date rM,t (S&P 500) rt (GD Return) rf,t (TN) x t = r M,t - r f,t y t = r t - r f,t

01-10-2010

01-11-2010 -0.229 -3.025 2.797 -3.026 -5.822

01-12-2010 6.326 7.110 3.305 3.021 3.805

01-01-2011 2.239 6.069 3.378 -1.139 2.691

01-02-2011 3.146 0.950 3.414 -0.268 -2.464

01-03-2011 -0.105 0.576 3.454 -3.559 -2.878

01-04-2011 2.810 -5.008 3.296 -0.486 -8.304

01-05-2011 -1.359 1.904 3.05 -4.409 -1.146

01-06-2011 -1.843 0.403 3.158 -5.001 -2.755

01-07-2011 -2.171 -8.950 2.805 -4.976 -11.755

a. We estimated the CAPM using linear regression for the excess return

yt = rt - rf,t

on excess market return

xt = rM,t - rf,t

for the GD stock. The excel

output is given below. The regression line is found to be

yt=0 . 9089∗xt ( SE=0 .14 ) +0 . 2353 ( SE=0 .51 )

where the excess market

return

xt = rM,t - rf,t

is found to be statistically significant (t = 6.48, p < 0.05)

predictor of the excess return

yt = rt - rf,t

for the GD stock (Renaud, and

Victoria-Feser, 2010; Ward, and Muller, 2012).

R2=0 . 4198 , SER=3. 6751 , n=60

The first 10 entries of the detail calculation for the regression model have been

provided below, and the entire table of calculation is in Excel file section of the

report.

Table 6: Excel output for first 9 entries for detail calculation for the regression model

x t = r M,t - r f,t y t = r t - r f,t xt * yt xt^2 yt^2

-3.026 -5.822 17.620 9.1584169 33.89977219

3.021 3.805 11.493 9.124318957 14.47721451

-1.139 2.691 -3.064 1.296644649 7.24200717

-0.268 -2.464 0.661 0.072007586 6.069433211

-3.559 -2.878 10.241 12.66495923 8.280789419

-0.486 -8.304 4.038 0.236493666 68.96318936

-4.409 -1.146 5.052 19.44185535 1.31262245

-5.001 -2.755 13.775 25.0061859 7.587911307

-4.976 -11.755 58.492 24.75894027 138.1873318

The regression coefficient is calculated as

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

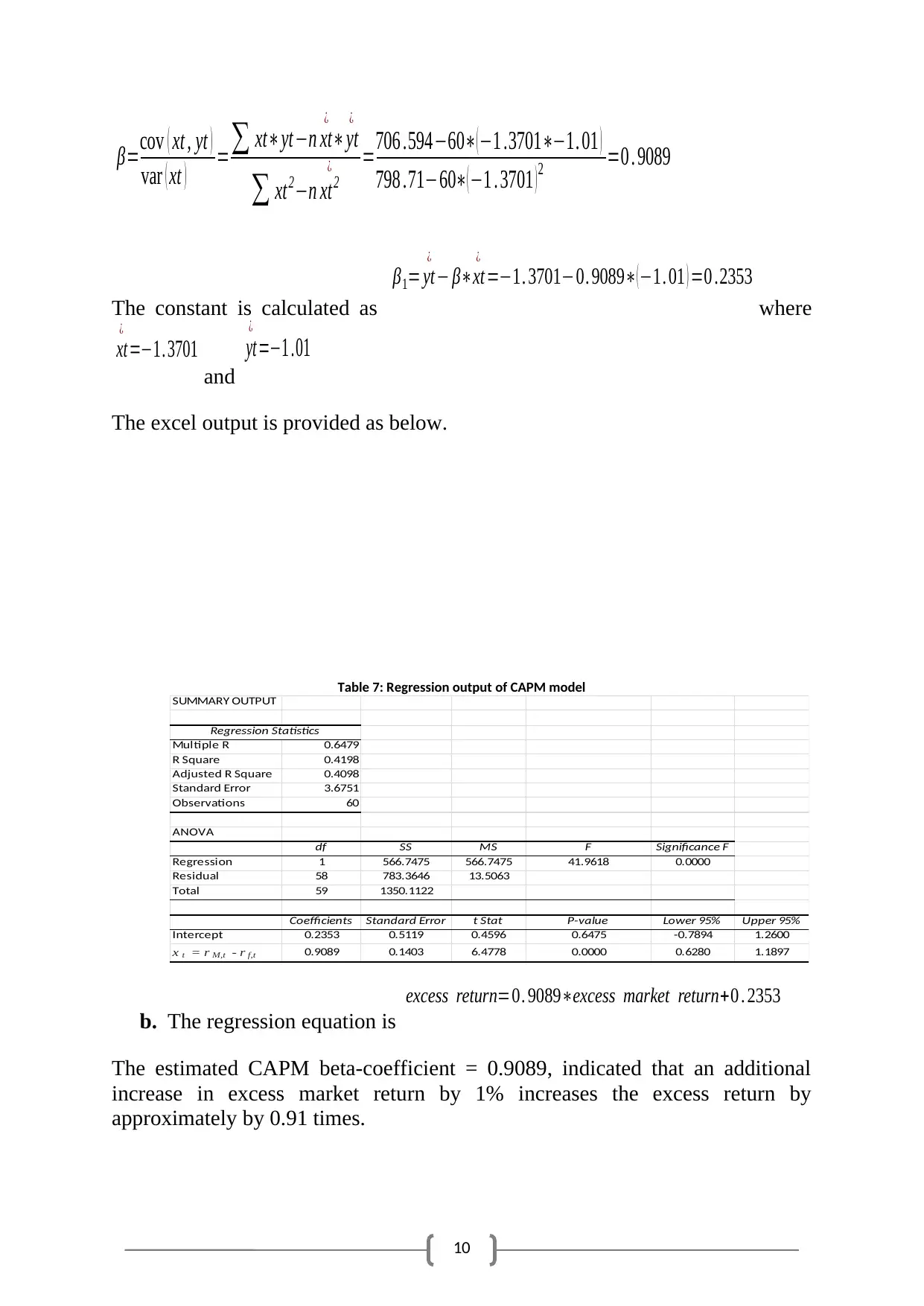

β=cov ( xt , yt )

var ( xt ) =∑ xt∗yt−n xt

¿

∗yt

¿

∑ xt2−n xt2

¿ =706 .594−60∗( −1 .3701∗−1. 01 )

798 .71−60∗( −1 . 3701 ) 2 =0 . 9089

The constant is calculated as

β1= yt

¿

− β∗xt

¿

=−1. 3701−0. 9089∗( −1. 01 ) =0 .2353

where

xt

¿

=−1. 3701

and

yt

¿

=−1 .01

The excel output is provided as below.

Table 7: Regression output of CAPM model

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.6479

R Square 0.4198

Adjusted R Square 0.4098

Standard Error 3.6751

Observations 60

ANOVA

df SS MS F Significance F

Regression 1 566.7475 566.7475 41.9618 0.0000

Residual 58 783.3646 13.5063

Total 59 1350.1122

Coefficients Standard Error t Stat P-value Lower 95% Upper 95%

Intercept 0.2353 0.5119 0.4596 0.6475 -0.7894 1.2600

x t = r M,t - r f,t 0.9089 0.1403 6.4778 0.0000 0.6280 1.1897

b. The regression equation is

excess return=0. 9089∗excess market return+0 . 2353

The estimated CAPM beta-coefficient = 0.9089, indicated that an additional

increase in excess market return by 1% increases the excess return by

approximately by 0.91 times.

β=cov ( xt , yt )

var ( xt ) =∑ xt∗yt−n xt

¿

∗yt

¿

∑ xt2−n xt2

¿ =706 .594−60∗( −1 .3701∗−1. 01 )

798 .71−60∗( −1 . 3701 ) 2 =0 . 9089

The constant is calculated as

β1= yt

¿

− β∗xt

¿

=−1. 3701−0. 9089∗( −1. 01 ) =0 .2353

where

xt

¿

=−1. 3701

and

yt

¿

=−1 .01

The excel output is provided as below.

Table 7: Regression output of CAPM model

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.6479

R Square 0.4198

Adjusted R Square 0.4098

Standard Error 3.6751

Observations 60

ANOVA

df SS MS F Significance F

Regression 1 566.7475 566.7475 41.9618 0.0000

Residual 58 783.3646 13.5063

Total 59 1350.1122

Coefficients Standard Error t Stat P-value Lower 95% Upper 95%

Intercept 0.2353 0.5119 0.4596 0.6475 -0.7894 1.2600

x t = r M,t - r f,t 0.9089 0.1403 6.4778 0.0000 0.6280 1.1897

b. The regression equation is

excess return=0. 9089∗excess market return+0 . 2353

The estimated CAPM beta-coefficient = 0.9089, indicated that an additional

increase in excess market return by 1% increases the excess return by

approximately by 0.91 times.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

Compared to the risk of the GD portfolio, the CAPM beta is an indicator and a

benchmark for measuring instability or systemic risks across the market. The

beta dividend will be used by the asset pricing model (CAPM), which calculates

the expected return on expected market return. The beta in the regression model

reflects the GD stock’s tendency to fluctuate in the market. The beta is

calculated as:

β=cov ( asset and market )

var ( market )

The beta value of 0.9089 indicates that the GD stock moves in same direction as

the rest of the market (S&P500). Also the beta value of less than 1 indicated that

the GD stock is less volatile compared to the market (S&P500 profile).

c.

R2=0 . 4198

Indicates that there 41.98% variation in excess return is

explained by the excess market returns for GD stock, where the rest of the

58.02% variation remains unexplained (Miles, 2014).

d. The 95% confidence interval (CI) is noted to be [0.628, 1.1897] for the

slope coefficient. This is illustrated as the relation and estimation of excess

return for increase in excess market return. With 95% confidence, it is possible

to state that accurate impact of increase in excess market return by 1% would

be approximately somewhere between 0.63% and 1.19%.

Answer 6: A stock with volatility exactly the same as varied as the market is

known to be neutral stock. This means that the stock's riskiness is quantified at

the exact same rate as the wider market. This is expressed by stating that the

stock as a beta of exactly 1 (Frazzini, and Pedersen, 2014; Fernandez, 2015).

i. Null hypothesis: H0:

( β=1 )

and tested against the two tailed alternate

hypotheses HA:

( β≠1 )

ii. Level of significance

α=0 . 05

iii. We assume that the errors of the regression model are normally distributed,

and take the test statistic as

t= β

^¿− β0

se ¿ ¿ ¿ ¿ ¿

that approximately follows

N ( 0,1 )

due to

the fact that

n=60>30

. Hence, calculated

t= 0. 9089−1

0 . 1403 =−0 .6493

Compared to the risk of the GD portfolio, the CAPM beta is an indicator and a

benchmark for measuring instability or systemic risks across the market. The

beta dividend will be used by the asset pricing model (CAPM), which calculates

the expected return on expected market return. The beta in the regression model

reflects the GD stock’s tendency to fluctuate in the market. The beta is

calculated as:

β=cov ( asset and market )

var ( market )

The beta value of 0.9089 indicates that the GD stock moves in same direction as

the rest of the market (S&P500). Also the beta value of less than 1 indicated that

the GD stock is less volatile compared to the market (S&P500 profile).

c.

R2=0 . 4198

Indicates that there 41.98% variation in excess return is

explained by the excess market returns for GD stock, where the rest of the

58.02% variation remains unexplained (Miles, 2014).

d. The 95% confidence interval (CI) is noted to be [0.628, 1.1897] for the

slope coefficient. This is illustrated as the relation and estimation of excess

return for increase in excess market return. With 95% confidence, it is possible

to state that accurate impact of increase in excess market return by 1% would

be approximately somewhere between 0.63% and 1.19%.

Answer 6: A stock with volatility exactly the same as varied as the market is

known to be neutral stock. This means that the stock's riskiness is quantified at

the exact same rate as the wider market. This is expressed by stating that the

stock as a beta of exactly 1 (Frazzini, and Pedersen, 2014; Fernandez, 2015).

i. Null hypothesis: H0:

( β=1 )

and tested against the two tailed alternate

hypotheses HA:

( β≠1 )

ii. Level of significance

α=0 . 05

iii. We assume that the errors of the regression model are normally distributed,

and take the test statistic as

t= β

^¿− β0

se ¿ ¿ ¿ ¿ ¿

that approximately follows

N ( 0,1 )

due to

the fact that

n=60>30

. Hence, calculated

t= 0. 9089−1

0 . 1403 =−0 .6493

12

iv. The critical t-value at 5% level and 59 degrees of freedom is = 2.001.

The95% confidence interval is calculated as

−2. 001<t= 0 . 9089−β

0. 1403 < 2. 001

or

0 .628< β<1 . 1897

.

v. CI approach to test a hypothesis:

With 95% it is possible to infer that the estimated value of beta coefficient

will be somewhere between 0.628 and 1.1897. The population beta for

neutral stock is 1.0 that lies between the limits of the confidence interval.

Hence, at

α =0 . 05

the population beta of 1.0 is found to be well within the

95% confidence interval which indicates that the null hypothesis assuming

that the GD stock is neutral cannot be rejected. Therefore, we conclude that

the GD stock is indeed neutral (Pollet, and Wilson, 2010).

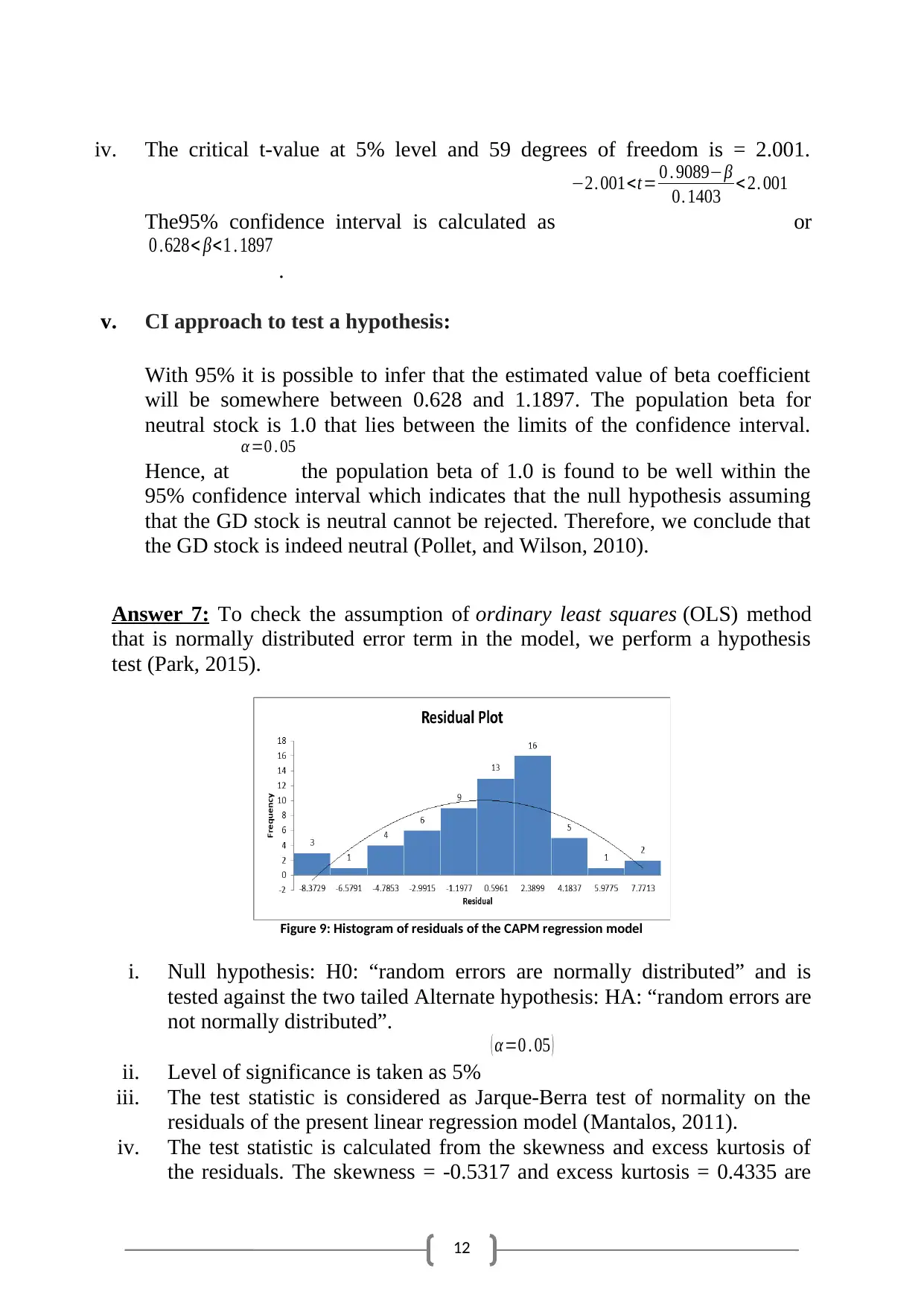

Answer 7: To check the assumption of ordinary least squares (OLS) method

that is normally distributed error term in the model, we perform a hypothesis

test (Park, 2015).

Figure 9: Histogram of residuals of the CAPM regression model

i. Null hypothesis: H0: “random errors are normally distributed” and is

tested against the two tailed Alternate hypothesis: HA: “random errors are

not normally distributed”.

ii. Level of significance is taken as 5%

( α=0 . 05 )

iii. The test statistic is considered as Jarque-Berra test of normality on the

residuals of the present linear regression model (Mantalos, 2011).

iv. The test statistic is calculated from the skewness and excess kurtosis of

the residuals. The skewness = -0.5317 and excess kurtosis = 0.4335 are

iv. The critical t-value at 5% level and 59 degrees of freedom is = 2.001.

The95% confidence interval is calculated as

−2. 001<t= 0 . 9089−β

0. 1403 < 2. 001

or

0 .628< β<1 . 1897

.

v. CI approach to test a hypothesis:

With 95% it is possible to infer that the estimated value of beta coefficient

will be somewhere between 0.628 and 1.1897. The population beta for

neutral stock is 1.0 that lies between the limits of the confidence interval.

Hence, at

α =0 . 05

the population beta of 1.0 is found to be well within the

95% confidence interval which indicates that the null hypothesis assuming

that the GD stock is neutral cannot be rejected. Therefore, we conclude that

the GD stock is indeed neutral (Pollet, and Wilson, 2010).

Answer 7: To check the assumption of ordinary least squares (OLS) method

that is normally distributed error term in the model, we perform a hypothesis

test (Park, 2015).

Figure 9: Histogram of residuals of the CAPM regression model

i. Null hypothesis: H0: “random errors are normally distributed” and is

tested against the two tailed Alternate hypothesis: HA: “random errors are

not normally distributed”.

ii. Level of significance is taken as 5%

( α=0 . 05 )

iii. The test statistic is considered as Jarque-Berra test of normality on the

residuals of the present linear regression model (Mantalos, 2011).

iv. The test statistic is calculated from the skewness and excess kurtosis of

the residuals. The skewness = -0.5317 and excess kurtosis = 0.4335 are

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.