Comparison of Boeing Company (BA) and General Dynamics (GD) Stock Prices: Analysis and Findings

15 Pages4454 Words391 Views

Added on 2023-04-25

About This Document

In this document we will discuss about Comparison of Boeing Company (BA) and General Dynamics (GD) Stock Prices and below are the summary points of this document:-

-

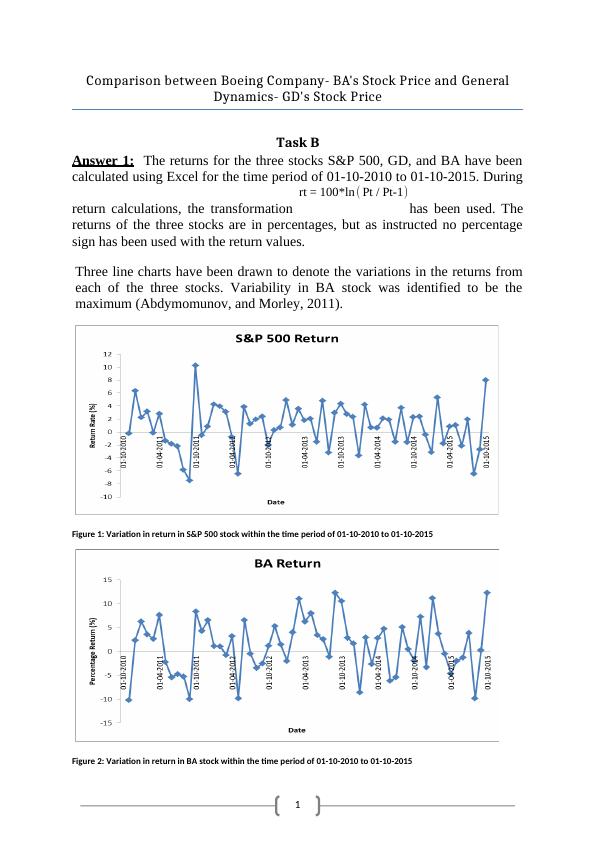

BA's stock price had the highest variability compared to GD and S&P 500.

-

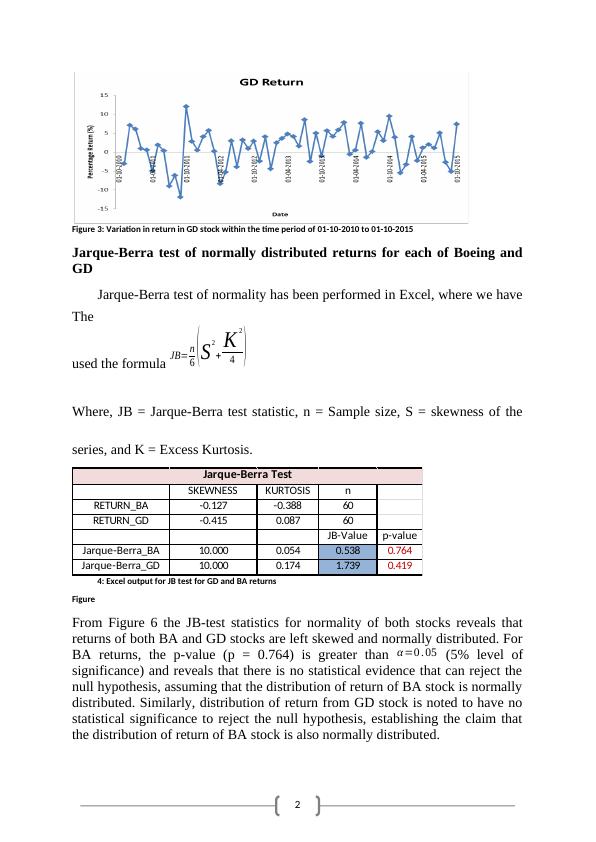

Both BA and GD stocks exhibited left-skewed and normally distributed returns.

-

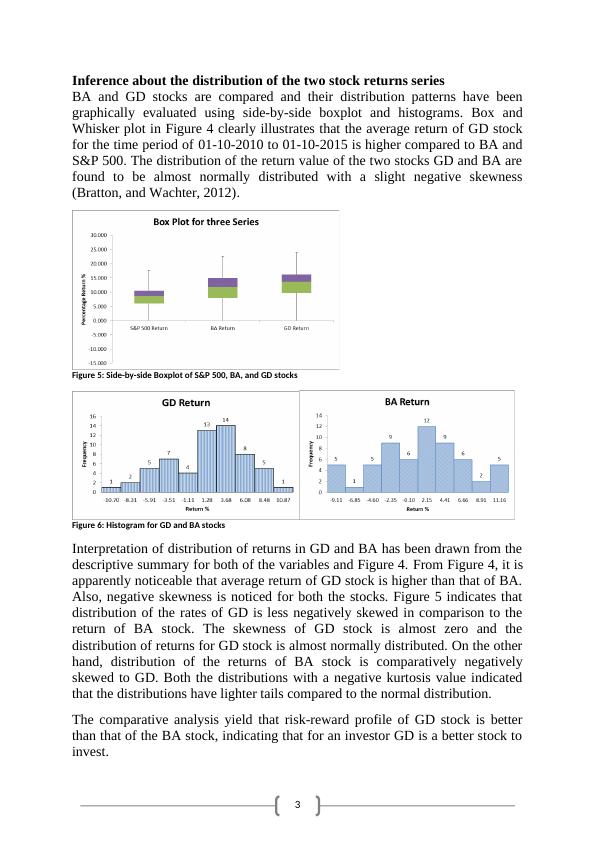

GD stock had a higher average return compared to BA and showed a less negatively skewed distribution.

Comparison of Boeing Company (BA) and General Dynamics (GD) Stock Prices: Analysis and Findings

Added on 2023-04-25

ShareRelated Documents

End of preview

Want to access all the pages? Upload your documents or become a member.

Statistical Analysis and Comparison between Stock Prices of Boeing Company and General Dynamics

|12

|4094

|443

Statistics for Business and Finance Assignment

|15

|3064

|264

Which Stock Should I Invest In PHUONG THAO BUI

|11

|2540

|64

Stock Returns: Boeing & IBM Analysis Report

|14

|2616

|155

Statistics for Business: Statistical Inference and Simple Regression Analysis

|9

|1819

|319

Statistics of Business and Finance

|9

|1388

|439