Corporate Accounting Solutions

VerifiedAdded on 2019/11/19

|10

|2247

|73

Homework Assignment

AI Summary

This document provides solutions to a corporate accounting assignment. It covers several topics including the calculation and recording of deferred tax assets and liabilities, accounting for employee advances, revaluation of assets (including intangible assets), analysis of control in business combinations according to AASB 10, and the preparation of a consolidation worksheet and consolidated balance sheet. The solutions include detailed explanations, journal entries, and calculations. References to external resources are also provided.

Corporate Accounting 1

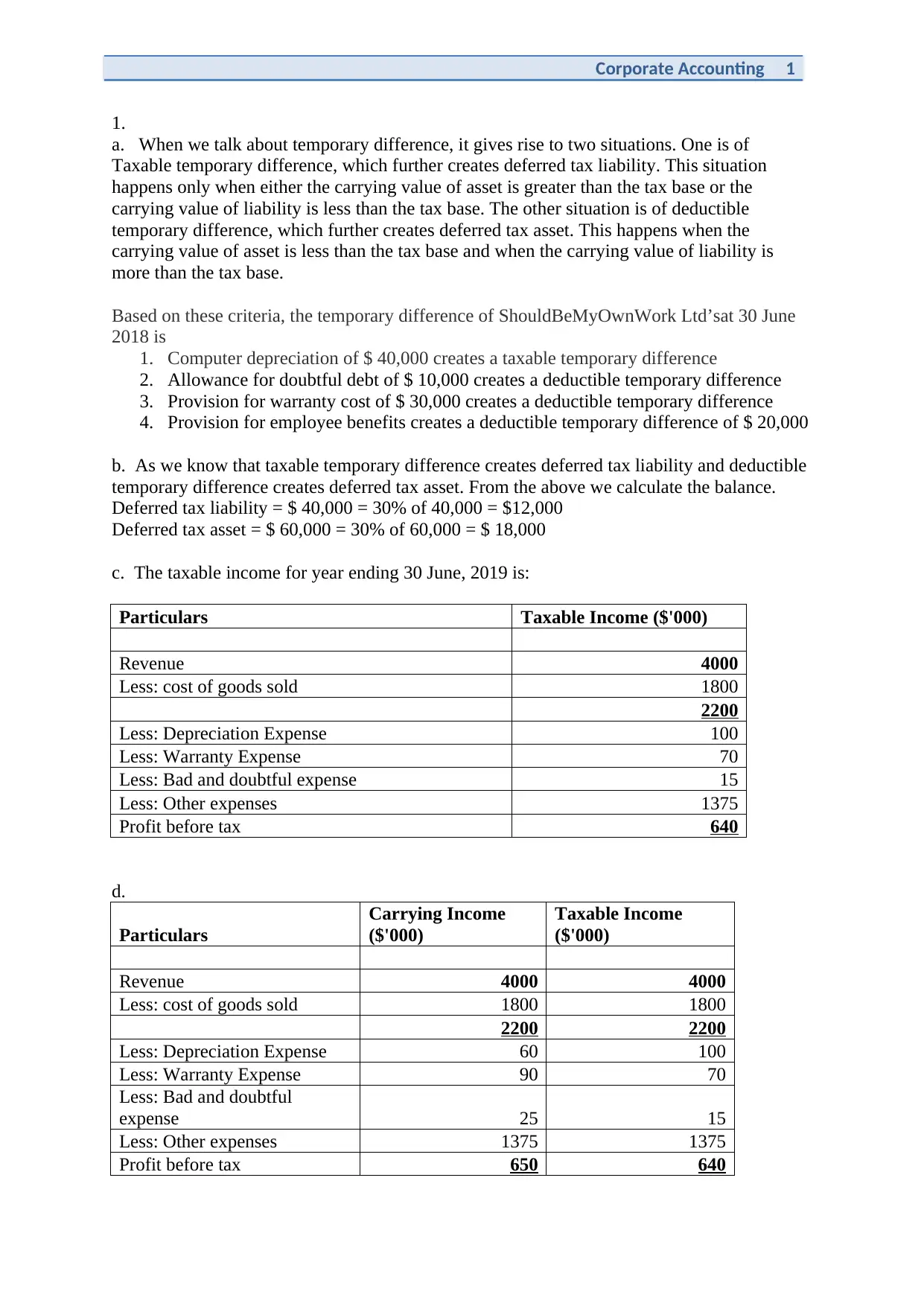

1.

a. When we talk about temporary difference, it gives rise to two situations. One is of

Taxable temporary difference, which further creates deferred tax liability. This situation

happens only when either the carrying value of asset is greater than the tax base or the

carrying value of liability is less than the tax base. The other situation is of deductible

temporary difference, which further creates deferred tax asset. This happens when the

carrying value of asset is less than the tax base and when the carrying value of liability is

more than the tax base.

Based on these criteria, the temporary difference of ShouldBeMyOwnWork Ltd’sat 30 June

2018 is

1. Computer depreciation of $ 40,000 creates a taxable temporary difference

2. Allowance for doubtful debt of $ 10,000 creates a deductible temporary difference

3. Provision for warranty cost of $ 30,000 creates a deductible temporary difference

4. Provision for employee benefits creates a deductible temporary difference of $ 20,000

b. As we know that taxable temporary difference creates deferred tax liability and deductible

temporary difference creates deferred tax asset. From the above we calculate the balance.

Deferred tax liability = $ 40,000 = 30% of 40,000 = $12,000

Deferred tax asset = $ 60,000 = 30% of 60,000 = $ 18,000

c. The taxable income for year ending 30 June, 2019 is:

Particulars Taxable Income ($'000)

Revenue 4000

Less: cost of goods sold 1800

2200

Less: Depreciation Expense 100

Less: Warranty Expense 70

Less: Bad and doubtful expense 15

Less: Other expenses 1375

Profit before tax 640

d.

Particulars

Carrying Income

($'000)

Taxable Income

($'000)

Revenue 4000 4000

Less: cost of goods sold 1800 1800

2200 2200

Less: Depreciation Expense 60 100

Less: Warranty Expense 90 70

Less: Bad and doubtful

expense 25 15

Less: Other expenses 1375 1375

Profit before tax 650 640

1.

a. When we talk about temporary difference, it gives rise to two situations. One is of

Taxable temporary difference, which further creates deferred tax liability. This situation

happens only when either the carrying value of asset is greater than the tax base or the

carrying value of liability is less than the tax base. The other situation is of deductible

temporary difference, which further creates deferred tax asset. This happens when the

carrying value of asset is less than the tax base and when the carrying value of liability is

more than the tax base.

Based on these criteria, the temporary difference of ShouldBeMyOwnWork Ltd’sat 30 June

2018 is

1. Computer depreciation of $ 40,000 creates a taxable temporary difference

2. Allowance for doubtful debt of $ 10,000 creates a deductible temporary difference

3. Provision for warranty cost of $ 30,000 creates a deductible temporary difference

4. Provision for employee benefits creates a deductible temporary difference of $ 20,000

b. As we know that taxable temporary difference creates deferred tax liability and deductible

temporary difference creates deferred tax asset. From the above we calculate the balance.

Deferred tax liability = $ 40,000 = 30% of 40,000 = $12,000

Deferred tax asset = $ 60,000 = 30% of 60,000 = $ 18,000

c. The taxable income for year ending 30 June, 2019 is:

Particulars Taxable Income ($'000)

Revenue 4000

Less: cost of goods sold 1800

2200

Less: Depreciation Expense 100

Less: Warranty Expense 70

Less: Bad and doubtful expense 15

Less: Other expenses 1375

Profit before tax 640

d.

Particulars

Carrying Income

($'000)

Taxable Income

($'000)

Revenue 4000 4000

Less: cost of goods sold 1800 1800

2200 2200

Less: Depreciation Expense 60 100

Less: Warranty Expense 90 70

Less: Bad and doubtful

expense 25 15

Less: Other expenses 1375 1375

Profit before tax 650 640

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting

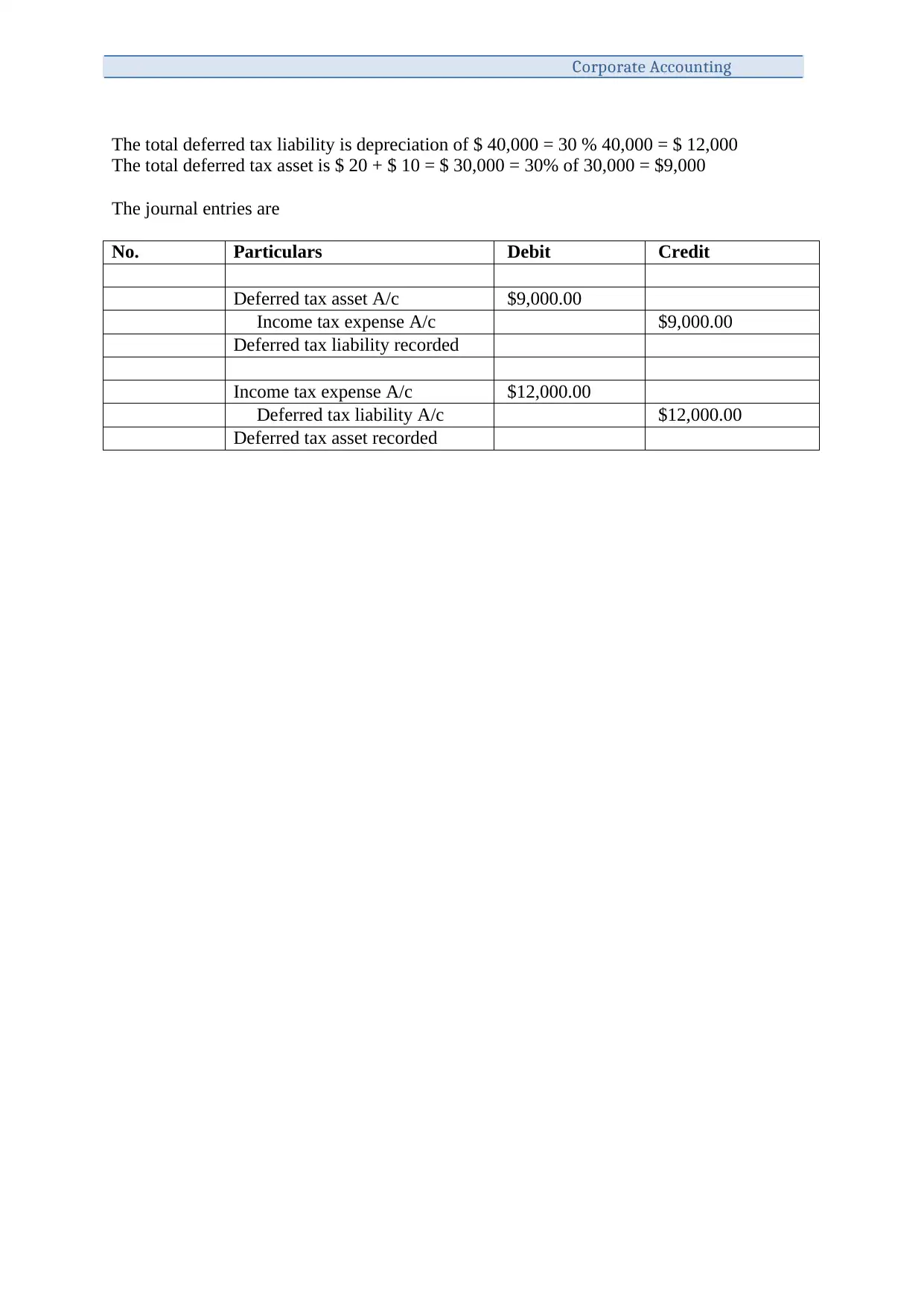

The total deferred tax liability is depreciation of $ 40,000 = 30 % 40,000 = $ 12,000

The total deferred tax asset is $ 20 + $ 10 = $ 30,000 = 30% of 30,000 = $9,000

The journal entries are

No. Particulars Debit Credit

Deferred tax asset A/c $9,000.00

Income tax expense A/c $9,000.00

Deferred tax liability recorded

Income tax expense A/c $12,000.00

Deferred tax liability A/c $12,000.00

Deferred tax asset recorded

The total deferred tax liability is depreciation of $ 40,000 = 30 % 40,000 = $ 12,000

The total deferred tax asset is $ 20 + $ 10 = $ 30,000 = 30% of 30,000 = $9,000

The journal entries are

No. Particulars Debit Credit

Deferred tax asset A/c $9,000.00

Income tax expense A/c $9,000.00

Deferred tax liability recorded

Income tax expense A/c $12,000.00

Deferred tax liability A/c $12,000.00

Deferred tax asset recorded

Corporate Accounting 3

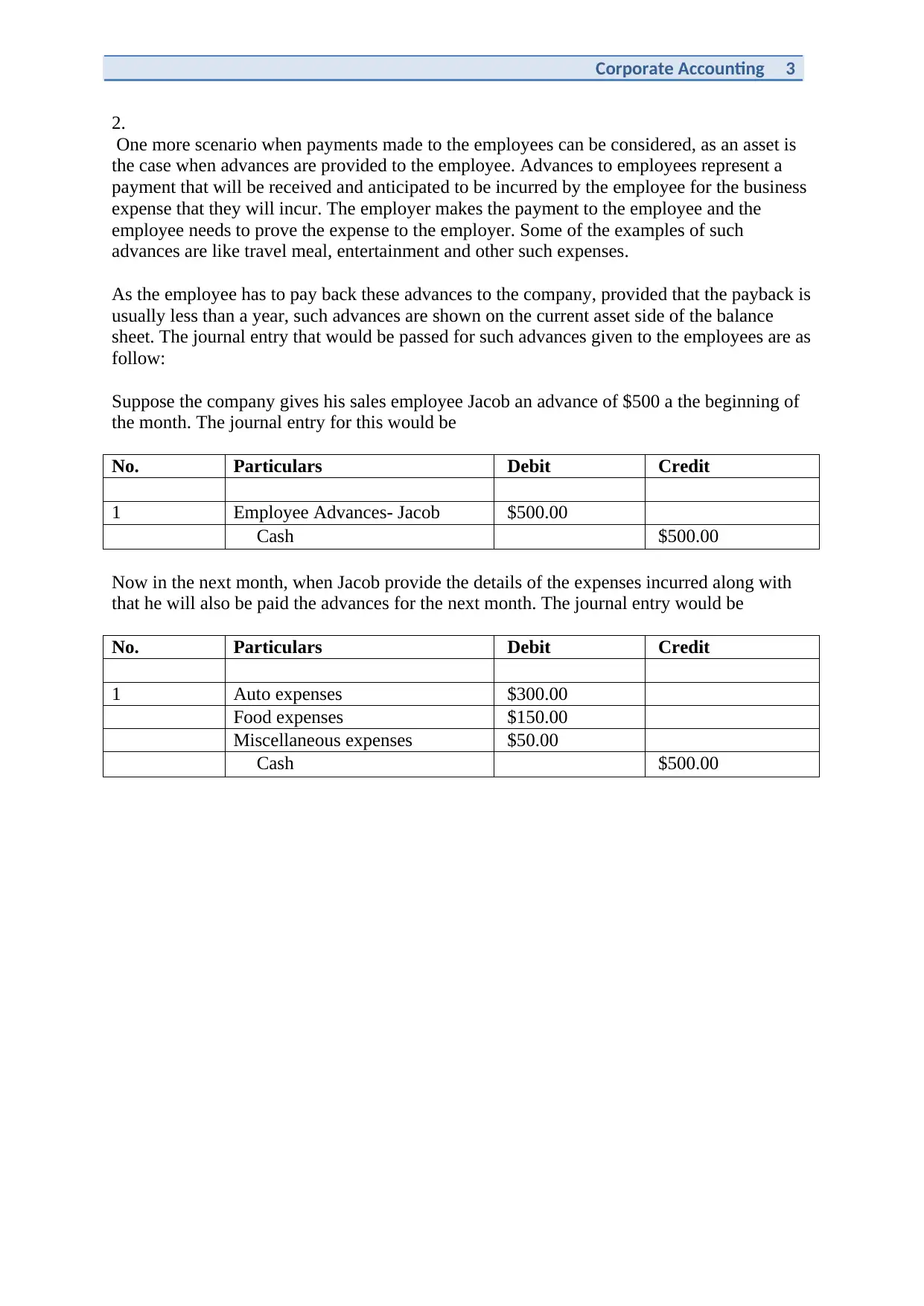

2.

One more scenario when payments made to the employees can be considered, as an asset is

the case when advances are provided to the employee. Advances to employees represent a

payment that will be received and anticipated to be incurred by the employee for the business

expense that they will incur. The employer makes the payment to the employee and the

employee needs to prove the expense to the employer. Some of the examples of such

advances are like travel meal, entertainment and other such expenses.

As the employee has to pay back these advances to the company, provided that the payback is

usually less than a year, such advances are shown on the current asset side of the balance

sheet. The journal entry that would be passed for such advances given to the employees are as

follow:

Suppose the company gives his sales employee Jacob an advance of $500 a the beginning of

the month. The journal entry for this would be

No. Particulars Debit Credit

1 Employee Advances- Jacob $500.00

Cash $500.00

Now in the next month, when Jacob provide the details of the expenses incurred along with

that he will also be paid the advances for the next month. The journal entry would be

No. Particulars Debit Credit

1 Auto expenses $300.00

Food expenses $150.00

Miscellaneous expenses $50.00

Cash $500.00

2.

One more scenario when payments made to the employees can be considered, as an asset is

the case when advances are provided to the employee. Advances to employees represent a

payment that will be received and anticipated to be incurred by the employee for the business

expense that they will incur. The employer makes the payment to the employee and the

employee needs to prove the expense to the employer. Some of the examples of such

advances are like travel meal, entertainment and other such expenses.

As the employee has to pay back these advances to the company, provided that the payback is

usually less than a year, such advances are shown on the current asset side of the balance

sheet. The journal entry that would be passed for such advances given to the employees are as

follow:

Suppose the company gives his sales employee Jacob an advance of $500 a the beginning of

the month. The journal entry for this would be

No. Particulars Debit Credit

1 Employee Advances- Jacob $500.00

Cash $500.00

Now in the next month, when Jacob provide the details of the expenses incurred along with

that he will also be paid the advances for the next month. The journal entry would be

No. Particulars Debit Credit

1 Auto expenses $300.00

Food expenses $150.00

Miscellaneous expenses $50.00

Cash $500.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Accounting

3

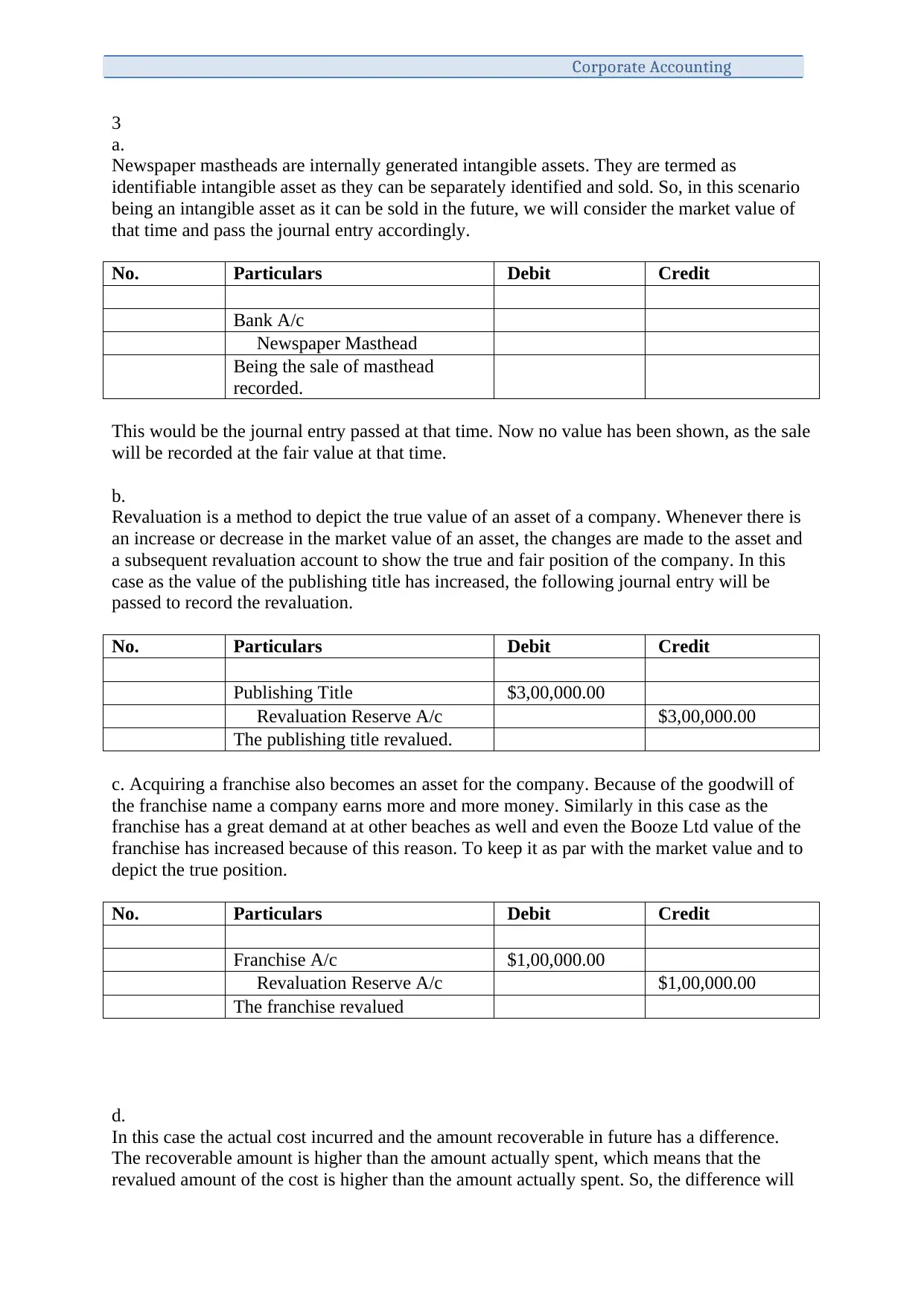

a.

Newspaper mastheads are internally generated intangible assets. They are termed as

identifiable intangible asset as they can be separately identified and sold. So, in this scenario

being an intangible asset as it can be sold in the future, we will consider the market value of

that time and pass the journal entry accordingly.

No. Particulars Debit Credit

Bank A/c

Newspaper Masthead

Being the sale of masthead

recorded.

This would be the journal entry passed at that time. Now no value has been shown, as the sale

will be recorded at the fair value at that time.

b.

Revaluation is a method to depict the true value of an asset of a company. Whenever there is

an increase or decrease in the market value of an asset, the changes are made to the asset and

a subsequent revaluation account to show the true and fair position of the company. In this

case as the value of the publishing title has increased, the following journal entry will be

passed to record the revaluation.

No. Particulars Debit Credit

Publishing Title $3,00,000.00

Revaluation Reserve A/c $3,00,000.00

The publishing title revalued.

c. Acquiring a franchise also becomes an asset for the company. Because of the goodwill of

the franchise name a company earns more and more money. Similarly in this case as the

franchise has a great demand at at other beaches as well and even the Booze Ltd value of the

franchise has increased because of this reason. To keep it as par with the market value and to

depict the true position.

No. Particulars Debit Credit

Franchise A/c $1,00,000.00

Revaluation Reserve A/c $1,00,000.00

The franchise revalued

d.

In this case the actual cost incurred and the amount recoverable in future has a difference.

The recoverable amount is higher than the amount actually spent, which means that the

revalued amount of the cost is higher than the amount actually spent. So, the difference will

3

a.

Newspaper mastheads are internally generated intangible assets. They are termed as

identifiable intangible asset as they can be separately identified and sold. So, in this scenario

being an intangible asset as it can be sold in the future, we will consider the market value of

that time and pass the journal entry accordingly.

No. Particulars Debit Credit

Bank A/c

Newspaper Masthead

Being the sale of masthead

recorded.

This would be the journal entry passed at that time. Now no value has been shown, as the sale

will be recorded at the fair value at that time.

b.

Revaluation is a method to depict the true value of an asset of a company. Whenever there is

an increase or decrease in the market value of an asset, the changes are made to the asset and

a subsequent revaluation account to show the true and fair position of the company. In this

case as the value of the publishing title has increased, the following journal entry will be

passed to record the revaluation.

No. Particulars Debit Credit

Publishing Title $3,00,000.00

Revaluation Reserve A/c $3,00,000.00

The publishing title revalued.

c. Acquiring a franchise also becomes an asset for the company. Because of the goodwill of

the franchise name a company earns more and more money. Similarly in this case as the

franchise has a great demand at at other beaches as well and even the Booze Ltd value of the

franchise has increased because of this reason. To keep it as par with the market value and to

depict the true position.

No. Particulars Debit Credit

Franchise A/c $1,00,000.00

Revaluation Reserve A/c $1,00,000.00

The franchise revalued

d.

In this case the actual cost incurred and the amount recoverable in future has a difference.

The recoverable amount is higher than the amount actually spent, which means that the

revalued amount of the cost is higher than the amount actually spent. So, the difference will

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

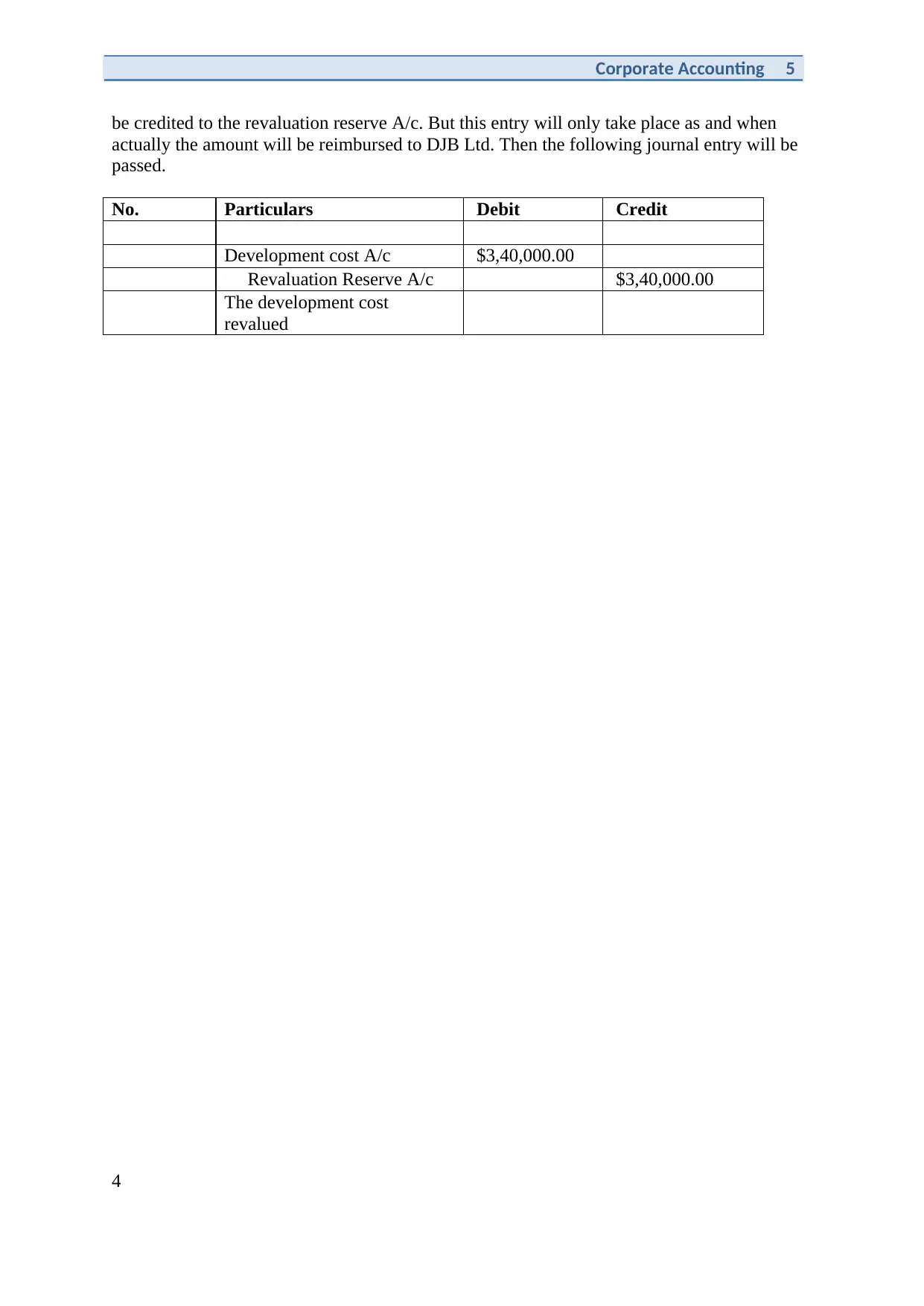

Corporate Accounting 5

be credited to the revaluation reserve A/c. But this entry will only take place as and when

actually the amount will be reimbursed to DJB Ltd. Then the following journal entry will be

passed.

No. Particulars Debit Credit

Development cost A/c $3,40,000.00

Revaluation Reserve A/c $3,40,000.00

The development cost

revalued

4

be credited to the revaluation reserve A/c. But this entry will only take place as and when

actually the amount will be reimbursed to DJB Ltd. Then the following journal entry will be

passed.

No. Particulars Debit Credit

Development cost A/c $3,40,000.00

Revaluation Reserve A/c $3,40,000.00

The development cost

revalued

4

Corporate Accounting

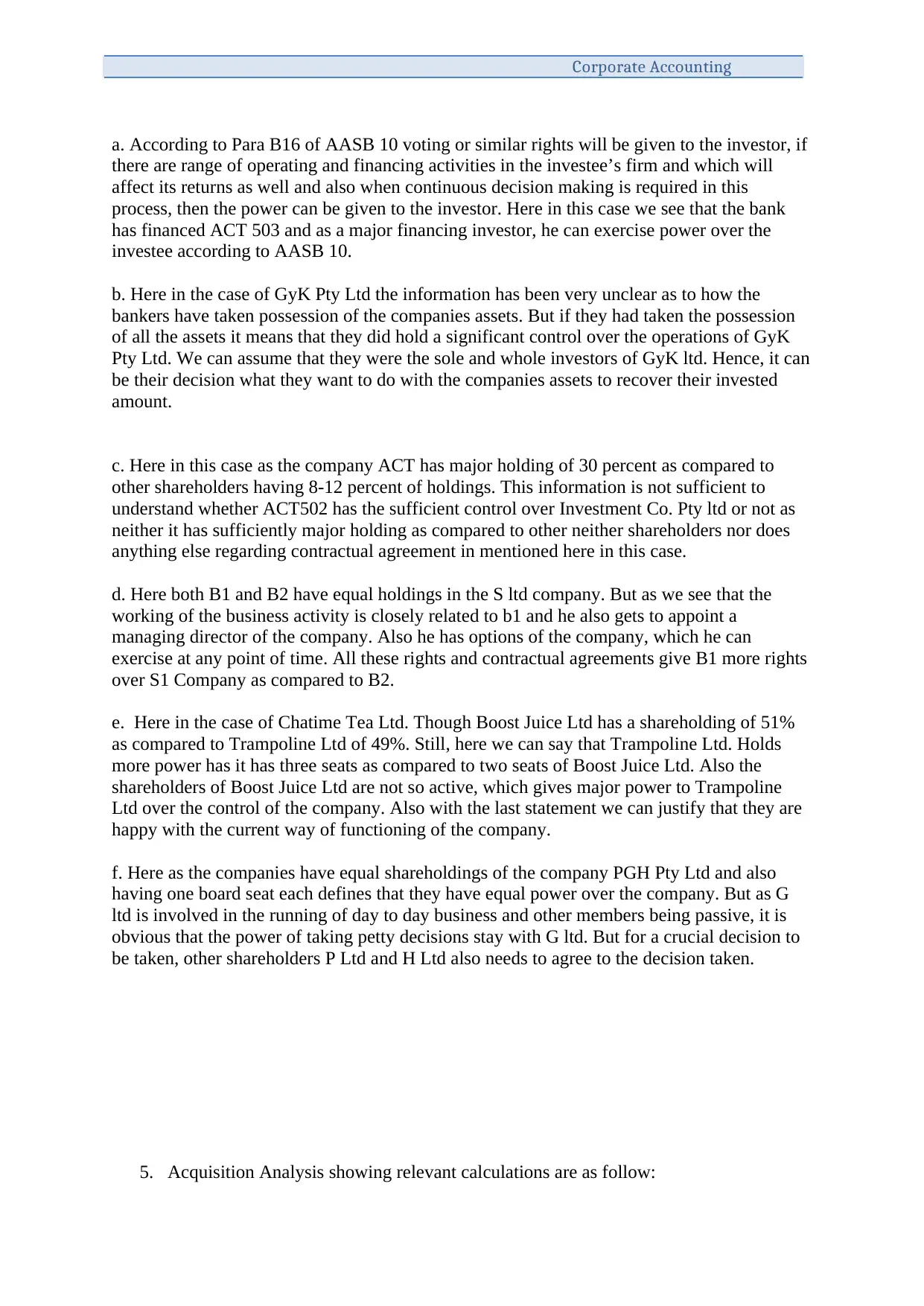

a. According to Para B16 of AASB 10 voting or similar rights will be given to the investor, if

there are range of operating and financing activities in the investee’s firm and which will

affect its returns as well and also when continuous decision making is required in this

process, then the power can be given to the investor. Here in this case we see that the bank

has financed ACT 503 and as a major financing investor, he can exercise power over the

investee according to AASB 10.

b. Here in the case of GyK Pty Ltd the information has been very unclear as to how the

bankers have taken possession of the companies assets. But if they had taken the possession

of all the assets it means that they did hold a significant control over the operations of GyK

Pty Ltd. We can assume that they were the sole and whole investors of GyK ltd. Hence, it can

be their decision what they want to do with the companies assets to recover their invested

amount.

c. Here in this case as the company ACT has major holding of 30 percent as compared to

other shareholders having 8-12 percent of holdings. This information is not sufficient to

understand whether ACT502 has the sufficient control over Investment Co. Pty ltd or not as

neither it has sufficiently major holding as compared to other neither shareholders nor does

anything else regarding contractual agreement in mentioned here in this case.

d. Here both B1 and B2 have equal holdings in the S ltd company. But as we see that the

working of the business activity is closely related to b1 and he also gets to appoint a

managing director of the company. Also he has options of the company, which he can

exercise at any point of time. All these rights and contractual agreements give B1 more rights

over S1 Company as compared to B2.

e. Here in the case of Chatime Tea Ltd. Though Boost Juice Ltd has a shareholding of 51%

as compared to Trampoline Ltd of 49%. Still, here we can say that Trampoline Ltd. Holds

more power has it has three seats as compared to two seats of Boost Juice Ltd. Also the

shareholders of Boost Juice Ltd are not so active, which gives major power to Trampoline

Ltd over the control of the company. Also with the last statement we can justify that they are

happy with the current way of functioning of the company.

f. Here as the companies have equal shareholdings of the company PGH Pty Ltd and also

having one board seat each defines that they have equal power over the company. But as G

ltd is involved in the running of day to day business and other members being passive, it is

obvious that the power of taking petty decisions stay with G ltd. But for a crucial decision to

be taken, other shareholders P Ltd and H Ltd also needs to agree to the decision taken.

5. Acquisition Analysis showing relevant calculations are as follow:

a. According to Para B16 of AASB 10 voting or similar rights will be given to the investor, if

there are range of operating and financing activities in the investee’s firm and which will

affect its returns as well and also when continuous decision making is required in this

process, then the power can be given to the investor. Here in this case we see that the bank

has financed ACT 503 and as a major financing investor, he can exercise power over the

investee according to AASB 10.

b. Here in the case of GyK Pty Ltd the information has been very unclear as to how the

bankers have taken possession of the companies assets. But if they had taken the possession

of all the assets it means that they did hold a significant control over the operations of GyK

Pty Ltd. We can assume that they were the sole and whole investors of GyK ltd. Hence, it can

be their decision what they want to do with the companies assets to recover their invested

amount.

c. Here in this case as the company ACT has major holding of 30 percent as compared to

other shareholders having 8-12 percent of holdings. This information is not sufficient to

understand whether ACT502 has the sufficient control over Investment Co. Pty ltd or not as

neither it has sufficiently major holding as compared to other neither shareholders nor does

anything else regarding contractual agreement in mentioned here in this case.

d. Here both B1 and B2 have equal holdings in the S ltd company. But as we see that the

working of the business activity is closely related to b1 and he also gets to appoint a

managing director of the company. Also he has options of the company, which he can

exercise at any point of time. All these rights and contractual agreements give B1 more rights

over S1 Company as compared to B2.

e. Here in the case of Chatime Tea Ltd. Though Boost Juice Ltd has a shareholding of 51%

as compared to Trampoline Ltd of 49%. Still, here we can say that Trampoline Ltd. Holds

more power has it has three seats as compared to two seats of Boost Juice Ltd. Also the

shareholders of Boost Juice Ltd are not so active, which gives major power to Trampoline

Ltd over the control of the company. Also with the last statement we can justify that they are

happy with the current way of functioning of the company.

f. Here as the companies have equal shareholdings of the company PGH Pty Ltd and also

having one board seat each defines that they have equal power over the company. But as G

ltd is involved in the running of day to day business and other members being passive, it is

obvious that the power of taking petty decisions stay with G ltd. But for a crucial decision to

be taken, other shareholders P Ltd and H Ltd also needs to agree to the decision taken.

5. Acquisition Analysis showing relevant calculations are as follow:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Accounting 7

First, we calculate the fair value of identifiable assets, liabilities and contingent

liability if any of the subsidiary company.

Net Fair Value in this case = Historical costs of net assets + changes in value of non

current asset and liabilities

Net Fair Value = $10,00,000 - $ 3,00,000 + $1,00,000

= $ 8,00,000

Here the changes in the value has been calculated as below:

The value of Property, plant and equipment = $ 7,00,000

Accumulated Depreciation = $ 2,70,000

Book Value = $ 4,30,000

Current Market value = $ 5,30,000

So, the increase in value = $ 1,00,000

Next we see the cost of combination. In our case it is $ 9,00,000

Goodwill = Cost- Fair Value of net assets

= $ 9,00,000 - $ 8,00,000

= $ 1,00,000

Fair value of asset adjustment entries are

No. Particulars Debit Credit

Property, Plant and Equipment $1,00,000.00

To Business combination valuation

reserve $1,00,000.00

Being the property, plant and equipment

revaluation recoded

Pre acquisition eliminating entries are as follow:

No. Particulars Debit Credit

Retained Earnings A/c $2,00,000.00

Share Capital A/c $5,00,000.00

Business combination revaluation reserve

A/c $1,00,000.00

Goodwill A/c $1,00,000.00

To Investment in TakeItEasy Ltd A/c $9,00,000.00

(Pre acquisition eliminating entries passed)

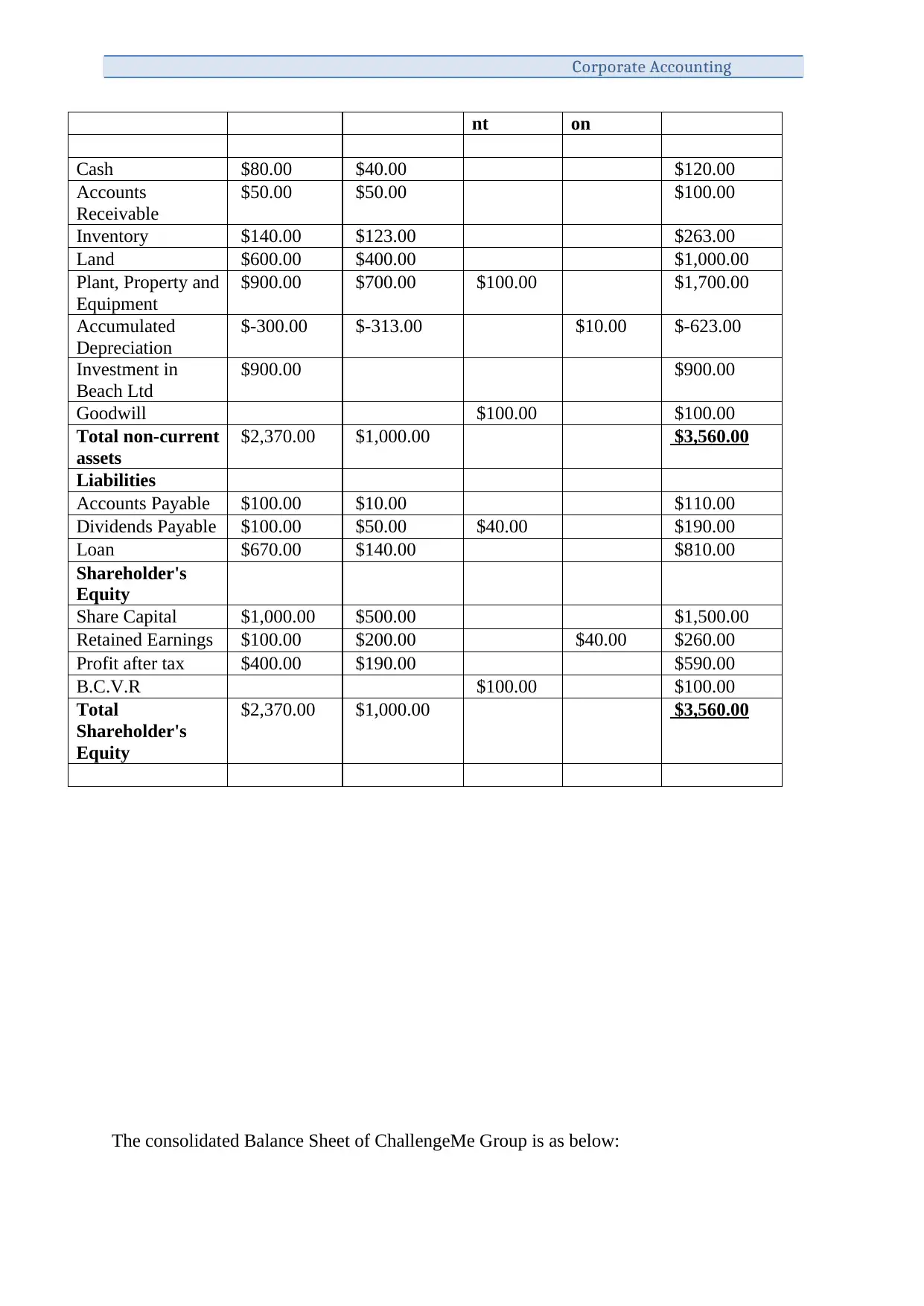

Consolidated worksheet showing column of elimination and adjustment are as follow

Consolidation Worksheet

Particulars Parent

($'000)

Subsidiary

($ '000) Adjustme Eliminati

Total

($'000)

First, we calculate the fair value of identifiable assets, liabilities and contingent

liability if any of the subsidiary company.

Net Fair Value in this case = Historical costs of net assets + changes in value of non

current asset and liabilities

Net Fair Value = $10,00,000 - $ 3,00,000 + $1,00,000

= $ 8,00,000

Here the changes in the value has been calculated as below:

The value of Property, plant and equipment = $ 7,00,000

Accumulated Depreciation = $ 2,70,000

Book Value = $ 4,30,000

Current Market value = $ 5,30,000

So, the increase in value = $ 1,00,000

Next we see the cost of combination. In our case it is $ 9,00,000

Goodwill = Cost- Fair Value of net assets

= $ 9,00,000 - $ 8,00,000

= $ 1,00,000

Fair value of asset adjustment entries are

No. Particulars Debit Credit

Property, Plant and Equipment $1,00,000.00

To Business combination valuation

reserve $1,00,000.00

Being the property, plant and equipment

revaluation recoded

Pre acquisition eliminating entries are as follow:

No. Particulars Debit Credit

Retained Earnings A/c $2,00,000.00

Share Capital A/c $5,00,000.00

Business combination revaluation reserve

A/c $1,00,000.00

Goodwill A/c $1,00,000.00

To Investment in TakeItEasy Ltd A/c $9,00,000.00

(Pre acquisition eliminating entries passed)

Consolidated worksheet showing column of elimination and adjustment are as follow

Consolidation Worksheet

Particulars Parent

($'000)

Subsidiary

($ '000) Adjustme Eliminati

Total

($'000)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting

nt on

Cash $80.00 $40.00 $120.00

Accounts

Receivable

$50.00 $50.00 $100.00

Inventory $140.00 $123.00 $263.00

Land $600.00 $400.00 $1,000.00

Plant, Property and

Equipment

$900.00 $700.00 $100.00 $1,700.00

Accumulated

Depreciation

$-300.00 $-313.00 $10.00 $-623.00

Investment in

Beach Ltd

$900.00 $900.00

Goodwill $100.00 $100.00

Total non-current

assets

$2,370.00 $1,000.00 $3,560.00

Liabilities

Accounts Payable $100.00 $10.00 $110.00

Dividends Payable $100.00 $50.00 $40.00 $190.00

Loan $670.00 $140.00 $810.00

Shareholder's

Equity

Share Capital $1,000.00 $500.00 $1,500.00

Retained Earnings $100.00 $200.00 $40.00 $260.00

Profit after tax $400.00 $190.00 $590.00

B.C.V.R $100.00 $100.00

Total

Shareholder's

Equity

$2,370.00 $1,000.00 $3,560.00

The consolidated Balance Sheet of ChallengeMe Group is as below:

nt on

Cash $80.00 $40.00 $120.00

Accounts

Receivable

$50.00 $50.00 $100.00

Inventory $140.00 $123.00 $263.00

Land $600.00 $400.00 $1,000.00

Plant, Property and

Equipment

$900.00 $700.00 $100.00 $1,700.00

Accumulated

Depreciation

$-300.00 $-313.00 $10.00 $-623.00

Investment in

Beach Ltd

$900.00 $900.00

Goodwill $100.00 $100.00

Total non-current

assets

$2,370.00 $1,000.00 $3,560.00

Liabilities

Accounts Payable $100.00 $10.00 $110.00

Dividends Payable $100.00 $50.00 $40.00 $190.00

Loan $670.00 $140.00 $810.00

Shareholder's

Equity

Share Capital $1,000.00 $500.00 $1,500.00

Retained Earnings $100.00 $200.00 $40.00 $260.00

Profit after tax $400.00 $190.00 $590.00

B.C.V.R $100.00 $100.00

Total

Shareholder's

Equity

$2,370.00 $1,000.00 $3,560.00

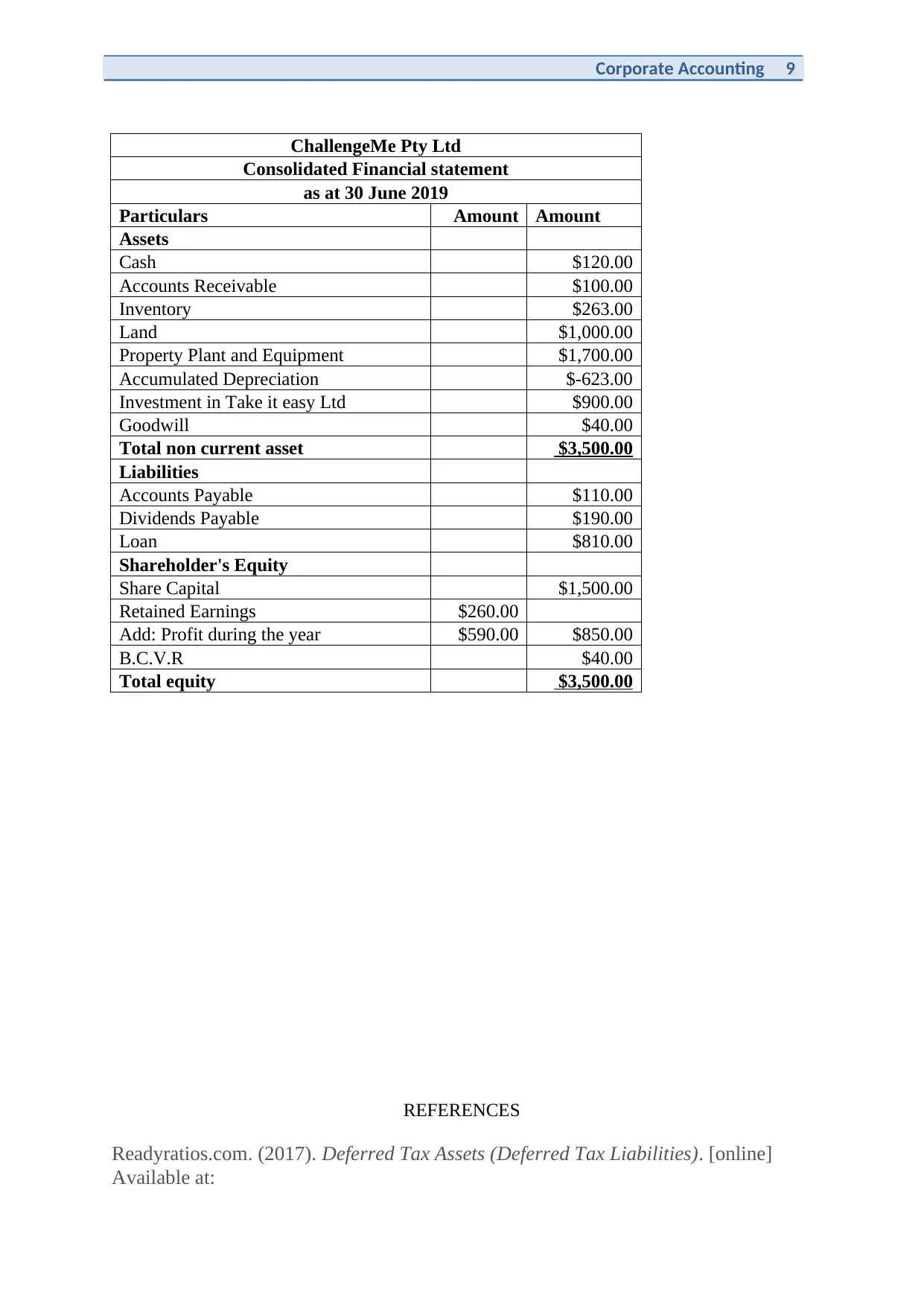

The consolidated Balance Sheet of ChallengeMe Group is as below:

Corporate Accounting 9

ChallengeMe Pty Ltd

Consolidated Financial statement

as at 30 June 2019

Particulars Amount Amount

Assets

Cash $120.00

Accounts Receivable $100.00

Inventory $263.00

Land $1,000.00

Property Plant and Equipment $1,700.00

Accumulated Depreciation $-623.00

Investment in Take it easy Ltd $900.00

Goodwill $40.00

Total non current asset $3,500.00

Liabilities

Accounts Payable $110.00

Dividends Payable $190.00

Loan $810.00

Shareholder's Equity

Share Capital $1,500.00

Retained Earnings $260.00

Add: Profit during the year $590.00 $850.00

B.C.V.R $40.00

Total equity $3,500.00

REFERENCES

Readyratios.com. (2017). Deferred Tax Assets (Deferred Tax Liabilities). [online]

Available at:

ChallengeMe Pty Ltd

Consolidated Financial statement

as at 30 June 2019

Particulars Amount Amount

Assets

Cash $120.00

Accounts Receivable $100.00

Inventory $263.00

Land $1,000.00

Property Plant and Equipment $1,700.00

Accumulated Depreciation $-623.00

Investment in Take it easy Ltd $900.00

Goodwill $40.00

Total non current asset $3,500.00

Liabilities

Accounts Payable $110.00

Dividends Payable $190.00

Loan $810.00

Shareholder's Equity

Share Capital $1,500.00

Retained Earnings $260.00

Add: Profit during the year $590.00 $850.00

B.C.V.R $40.00

Total equity $3,500.00

REFERENCES

Readyratios.com. (2017). Deferred Tax Assets (Deferred Tax Liabilities). [online]

Available at:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Accounting

https://www.readyratios.com/reference/accounting/deferred_tax_assets_deferred_tax_

liabilities.html [Accessed 20 Sep. 2017].

Simplestudies.com. (2017). Accounting for advances to employees and officers -

Accounting Guide | Simplestudies.com. [online] Available at:

http://simplestudies.com/accounting-for-advances-to-employees-and-officers.html/

page/2 [Accessed 20 Sep. 2017].

CAclubindia. (2017). Revaluation of Assets. [online] Available at:

http://www.caclubindia.com/articles/revaluation-of-assets-73.asp [Accessed 20 Sep.

2017].

Anon, (2017). [online] Available at:

https://studentvip-notes.s3.amazonaws.com/13447-sample.pdf [Accessed 20 Sep.

2017].

https://www.readyratios.com/reference/accounting/deferred_tax_assets_deferred_tax_

liabilities.html [Accessed 20 Sep. 2017].

Simplestudies.com. (2017). Accounting for advances to employees and officers -

Accounting Guide | Simplestudies.com. [online] Available at:

http://simplestudies.com/accounting-for-advances-to-employees-and-officers.html/

page/2 [Accessed 20 Sep. 2017].

CAclubindia. (2017). Revaluation of Assets. [online] Available at:

http://www.caclubindia.com/articles/revaluation-of-assets-73.asp [Accessed 20 Sep.

2017].

Anon, (2017). [online] Available at:

https://studentvip-notes.s3.amazonaws.com/13447-sample.pdf [Accessed 20 Sep.

2017].

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.