Financial Accounting: Detailed Client Case Study Analysis Report

VerifiedAdded on 2020/06/03

|33

|4290

|229

Report

AI Summary

This comprehensive financial accounting report delves into various aspects of the field through several client case studies. It begins with an introduction to financial accounting, covering key regulations, accounting rules, and principles, including consistency and materiality. The report then presents detailed analyses for six clients, including journal entries, ledgers, trial balances, income statements, and statements of financial position. Furthermore, the report covers the calculation of profit margins, assets, and liabilities, along with an evaluation of depreciation methods and bank reconciliation statements. Control accounts, suspense accounts, and the differences between suspense and clearing accounts are also explored. The report provides a practical understanding of financial accounting, making it a valuable resource for students studying accounting principles and their practical applications.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................1

LEARNING OUTCOMES........................................................................................................1

1. Financial accounting..........................................................................................................1

2. Key regulations with financial accounting.........................................................................2

3. Describing accounting rules and principles.......................................................................3

4. Explaining the concept and convention in relation to consistency & materiality..............4

CLIENT 1...................................................................................................................................4

a. Journal entries.....................................................................................................................4

b. Ledgers account.................................................................................................................7

c. Trial balance.....................................................................................................................16

CLIENT 2.................................................................................................................................16

a. Income statement..............................................................................................................16

b. Statement of financial position.........................................................................................17

CLIENT 3.................................................................................................................................19

a. Assessing gross and net profit margin of the business organization................................19

b. Calculating assets and liabilities of firm..........................................................................20

c. Presenting accounting concepts........................................................................................20

d. Evaluating different methods of depreciation..................................................................21

CLIENT 4.................................................................................................................................23

(A). Bank Reconciliation Statement....................................................................................23

(B). Reasons for differences in pass book and three column cash book..............................23

(C). (i) Opening bank reconciliations statement..................................................................24

(C). (ii) Closing bank reconciliation statement....................................................................24

(C). (iv). Corrected cash book..............................................................................................25

CLIENT 5.................................................................................................................................25

INTRODUCTION......................................................................................................................1

LEARNING OUTCOMES........................................................................................................1

1. Financial accounting..........................................................................................................1

2. Key regulations with financial accounting.........................................................................2

3. Describing accounting rules and principles.......................................................................3

4. Explaining the concept and convention in relation to consistency & materiality..............4

CLIENT 1...................................................................................................................................4

a. Journal entries.....................................................................................................................4

b. Ledgers account.................................................................................................................7

c. Trial balance.....................................................................................................................16

CLIENT 2.................................................................................................................................16

a. Income statement..............................................................................................................16

b. Statement of financial position.........................................................................................17

CLIENT 3.................................................................................................................................19

a. Assessing gross and net profit margin of the business organization................................19

b. Calculating assets and liabilities of firm..........................................................................20

c. Presenting accounting concepts........................................................................................20

d. Evaluating different methods of depreciation..................................................................21

CLIENT 4.................................................................................................................................23

(A). Bank Reconciliation Statement....................................................................................23

(B). Reasons for differences in pass book and three column cash book..............................23

(C). (i) Opening bank reconciliations statement..................................................................24

(C). (ii) Closing bank reconciliation statement....................................................................24

(C). (iv). Corrected cash book..............................................................................................25

CLIENT 5.................................................................................................................................25

A. (i). Sales Ledger control account.....................................................................................25

A. (ii). Purchase Ledger Control account.............................................................................25

B. Control account...............................................................................................................26

CLIENT 6.................................................................................................................................26

(A). Suspense account..........................................................................................................26

(B). Trial balance.................................................................................................................27

(C) Journal entries................................................................................................................27

(D). Difference between Suspense and clearing account.....................................................27

CONCLUSION........................................................................................................................28

REFERENCES.........................................................................................................................29

A. (ii). Purchase Ledger Control account.............................................................................25

B. Control account...............................................................................................................26

CLIENT 6.................................................................................................................................26

(A). Suspense account..........................................................................................................26

(B). Trial balance.................................................................................................................27

(C) Journal entries................................................................................................................27

(D). Difference between Suspense and clearing account.....................................................27

CONCLUSION........................................................................................................................28

REFERENCES.........................................................................................................................29

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting field of finance lays high level of emphasis on recording,

summarizing and evaluation of monetary information. Hence, it is highly associated with the

preparation of financial statements that furnishes highly valuable information to the

stakeholders and assists them in making suitable decision. Tools and techniques of financial

accounting are highly significant which in turn helps business organization in getting

information about the firm’s financial position and performance. The present report is based

on varied case situations which will provide deeper insight about the manner in which

financial statements are prepared. Besides this, report will also shed light on the concepts of

accounting, depreciation, suspense and clearance account.

LEARNING OUTCOMES

1. Financial accounting

In UK, it is legal compulsion for every entity to maintain proper records of their

trading activities in a proper way by making necessary accounts, called financial accounting.

There are three major accounts that ever entity needs to prepare includes following

statements, detailed below:

Profitability statement: It provides comprehensive details regarding company’s

revenues and spending level. Revenue are all the income and money received as a

consideration for giving something (Giles, 2014). However, expenses includes money spent

for acquiring necessary resources like material, labor and payment to others like overhead,

staffing expense, rent and others. It follows accrual concept and record all the results when

they takes place without knowing their cash impact. It is useful to know profitability results.

Balance sheet: It integrates three elements that are assets, liabilities and shareholders’

equity. Assets shows enterprise ownership, liabilities is obligations towards external parties

whereas equity is owner’s fund. This shows key results including liquidity health and

solvency position of the company.

Cash flow statement: As name itself, it follows cash concepts of accounting as it

integrates the results of transactions only when they either increase cash at bank balance or

Financial accounting field of finance lays high level of emphasis on recording,

summarizing and evaluation of monetary information. Hence, it is highly associated with the

preparation of financial statements that furnishes highly valuable information to the

stakeholders and assists them in making suitable decision. Tools and techniques of financial

accounting are highly significant which in turn helps business organization in getting

information about the firm’s financial position and performance. The present report is based

on varied case situations which will provide deeper insight about the manner in which

financial statements are prepared. Besides this, report will also shed light on the concepts of

accounting, depreciation, suspense and clearance account.

LEARNING OUTCOMES

1. Financial accounting

In UK, it is legal compulsion for every entity to maintain proper records of their

trading activities in a proper way by making necessary accounts, called financial accounting.

There are three major accounts that ever entity needs to prepare includes following

statements, detailed below:

Profitability statement: It provides comprehensive details regarding company’s

revenues and spending level. Revenue are all the income and money received as a

consideration for giving something (Giles, 2014). However, expenses includes money spent

for acquiring necessary resources like material, labor and payment to others like overhead,

staffing expense, rent and others. It follows accrual concept and record all the results when

they takes place without knowing their cash impact. It is useful to know profitability results.

Balance sheet: It integrates three elements that are assets, liabilities and shareholders’

equity. Assets shows enterprise ownership, liabilities is obligations towards external parties

whereas equity is owner’s fund. This shows key results including liquidity health and

solvency position of the company.

Cash flow statement: As name itself, it follows cash concepts of accounting as it

integrates the results of transactions only when they either increase cash at bank balance or

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

decline it as a result of payment to others. Thus, non-cash transactions are excluded from the

same like profit/loss on sale of assets, depreciation, provisions and others (Schipper, Francis

and Weil, 2017). Besides this, another reason of distinguish from profitability statement is

that it incorporate all the functions whether they are operating, investing or of financing

nature. Such statement helps firm knowing their net increase in cash position.

All these accounts are constructed applying necessary accounting principles i.e. going

principles, monetary measurements, prudence, separate entity, consistency and others. It not

helps companies only to determine their financial health but also helps outside stakeholders

like shareholders, lenders, creditors and others to extract useful information from the

accounts like gearing, liquidity, interest bearing capability and others and make well

informed decisions.

2. Key regulations with financial accounting

It is legally necessary for both the private and public companies in UK to prepare

their annual accounts complying with the accounting principles, called UK GAAP. It is

designed by the regulatory body in UK, named Financial Reporting Council. As per the

framed rules, all the companies whether private or public needs to follow accounting

concepts and key conventions while making their annual accounts. GAAPs, however, are the

domestic or localized principles and with the coming of liberalization in the economy, more

and more companies started and expanded business across worldwide. As a result,

international accounting and reporting standards were designed called IAS and IFRS with the

key target of maximizing transparency and comparability (Henderson and et.al.,2015). The

regulations required from the all the multinational or overseas companies to prepare their

accounts complying with such globalized standards. It helps in gaining trust among investors

as they take huge risk by investing their own money in various business units all over the

world. Thus, harmonization in all the companies’ accounts helps them comparing their

financial results easily and make better decisions.

In addition, in UK, companies are established as a separate legal entity by compliance

with the company act 2006. The act clearly presents that it is necessary for all organizations

to prepare all the accounts. Moreover, not only the preparation is sufficient, but also, needs to

be audited every year before final publishing with the key aim to inform all the stakeholders

with the true and valid information(Kaplan and Atkinson, 2015). Companies need to clearly

present their auditors opinion in their annual accounts, so that, user can easily know any

same like profit/loss on sale of assets, depreciation, provisions and others (Schipper, Francis

and Weil, 2017). Besides this, another reason of distinguish from profitability statement is

that it incorporate all the functions whether they are operating, investing or of financing

nature. Such statement helps firm knowing their net increase in cash position.

All these accounts are constructed applying necessary accounting principles i.e. going

principles, monetary measurements, prudence, separate entity, consistency and others. It not

helps companies only to determine their financial health but also helps outside stakeholders

like shareholders, lenders, creditors and others to extract useful information from the

accounts like gearing, liquidity, interest bearing capability and others and make well

informed decisions.

2. Key regulations with financial accounting

It is legally necessary for both the private and public companies in UK to prepare

their annual accounts complying with the accounting principles, called UK GAAP. It is

designed by the regulatory body in UK, named Financial Reporting Council. As per the

framed rules, all the companies whether private or public needs to follow accounting

concepts and key conventions while making their annual accounts. GAAPs, however, are the

domestic or localized principles and with the coming of liberalization in the economy, more

and more companies started and expanded business across worldwide. As a result,

international accounting and reporting standards were designed called IAS and IFRS with the

key target of maximizing transparency and comparability (Henderson and et.al.,2015). The

regulations required from the all the multinational or overseas companies to prepare their

accounts complying with such globalized standards. It helps in gaining trust among investors

as they take huge risk by investing their own money in various business units all over the

world. Thus, harmonization in all the companies’ accounts helps them comparing their

financial results easily and make better decisions.

In addition, in UK, companies are established as a separate legal entity by compliance

with the company act 2006. The act clearly presents that it is necessary for all organizations

to prepare all the accounts. Moreover, not only the preparation is sufficient, but also, needs to

be audited every year before final publishing with the key aim to inform all the stakeholders

with the true and valid information(Kaplan and Atkinson, 2015). Companies need to clearly

present their auditors opinion in their annual accounts, so that, user can easily know any

discrepancies or manipulation, if auditor had presented qualified report. Besides this, any

company who are keen to offer IPO (Initial Public Offer) to raise money need to list itself at

stock exchange and as per listing rules, they must present their true financial position and

profitability results by presenting annual reports.

3. Describing accounting rules and principles

Main accounting principles and concepts are enumerated below:

Dual aspects concept: As per this concept, accountant is required to present the dual

impact of transactions in the financial statements (Accounting Concepts, Principles

and Basic Terms, 2017). On the basis of such concept, for every debit there must be a

corresponding credit.

Assets = liabilities + shareholders equity

Accounting year concept: In accordance with such concept, financial statements and

reports need to be related with the specific time frame such as monthly, quarterly &

half yearly.

Going concern concept:According to the name, the applying the concept, companies

believes that they have long-lasting and never-ending business life means company

expects to continue their activities and functioning in future and there is no suspicion

that it can liquid in future. The concept believes deferring expenses over few years

like depreciation and write off preliminary expenses.

Accrual accounting concept:As discussed earlier, all the results of financial

activities should be entered in the final accounts at the period of their actual

occurrence without knowing their original cash incoming or outflow. Applying the

concept, current year’s outstanding payments are reported in P&L account whereas

prepaid expenses are shown in next year.

Monetary measurement concept: Final accounts display only the quantifiable

results which are easy to express or present quantitatively like cost, income, liabilities,

assets and others. However, other information like employees strength, talent,

consumer satisfaction which are qualitative are not expressed in the financial

accounts.

Matching principle: It follows double entry concepts as per which, every

activities has dual impact, therefore, entry must be passed both the sides.

company who are keen to offer IPO (Initial Public Offer) to raise money need to list itself at

stock exchange and as per listing rules, they must present their true financial position and

profitability results by presenting annual reports.

3. Describing accounting rules and principles

Main accounting principles and concepts are enumerated below:

Dual aspects concept: As per this concept, accountant is required to present the dual

impact of transactions in the financial statements (Accounting Concepts, Principles

and Basic Terms, 2017). On the basis of such concept, for every debit there must be a

corresponding credit.

Assets = liabilities + shareholders equity

Accounting year concept: In accordance with such concept, financial statements and

reports need to be related with the specific time frame such as monthly, quarterly &

half yearly.

Going concern concept:According to the name, the applying the concept, companies

believes that they have long-lasting and never-ending business life means company

expects to continue their activities and functioning in future and there is no suspicion

that it can liquid in future. The concept believes deferring expenses over few years

like depreciation and write off preliminary expenses.

Accrual accounting concept:As discussed earlier, all the results of financial

activities should be entered in the final accounts at the period of their actual

occurrence without knowing their original cash incoming or outflow. Applying the

concept, current year’s outstanding payments are reported in P&L account whereas

prepaid expenses are shown in next year.

Monetary measurement concept: Final accounts display only the quantifiable

results which are easy to express or present quantitatively like cost, income, liabilities,

assets and others. However, other information like employees strength, talent,

consumer satisfaction which are qualitative are not expressed in the financial

accounts.

Matching principle: It follows double entry concepts as per which, every

activities has dual impact, therefore, entry must be passed both the sides.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Full disclosure concept: Each and every detail needs to properly presents and

displayed in company’s financial accounts which make it free from any material

misstatement. Auditors focuses on it and present opinion whether company had fully

disclosed all the results or not and accounts are error free from any mistakes or errors

or not.

4. Explaining the concept and convention in relation to consistency & materiality

Consistency concept: This principle of accounting states that once specific principle

or rule is considered for dealing with business transaction then the same should be

continuously followed in the future period. It allows firm to change method or apply

new version only when it improves reported financial results. Thus, it can be

presented that such principle focuses on applying similar principles, methods,

practices and process over the years. IASB recognized consistency as one of the main

important element that makes accounting information highly valuable for the purpose

of decision making.

Material disclosure: In accounting, full disclosure principle is highly associated with

the concept or aspect of materiality. On the basis of such principle, accountant needs

to disclose all the material information either in the main financial statements or in

notes section (Materiality concept, 2017). Hence, materiality concept of accounting

lays emphasis on including all the information’s that may have influence on the

opinion of financial statement user’s.

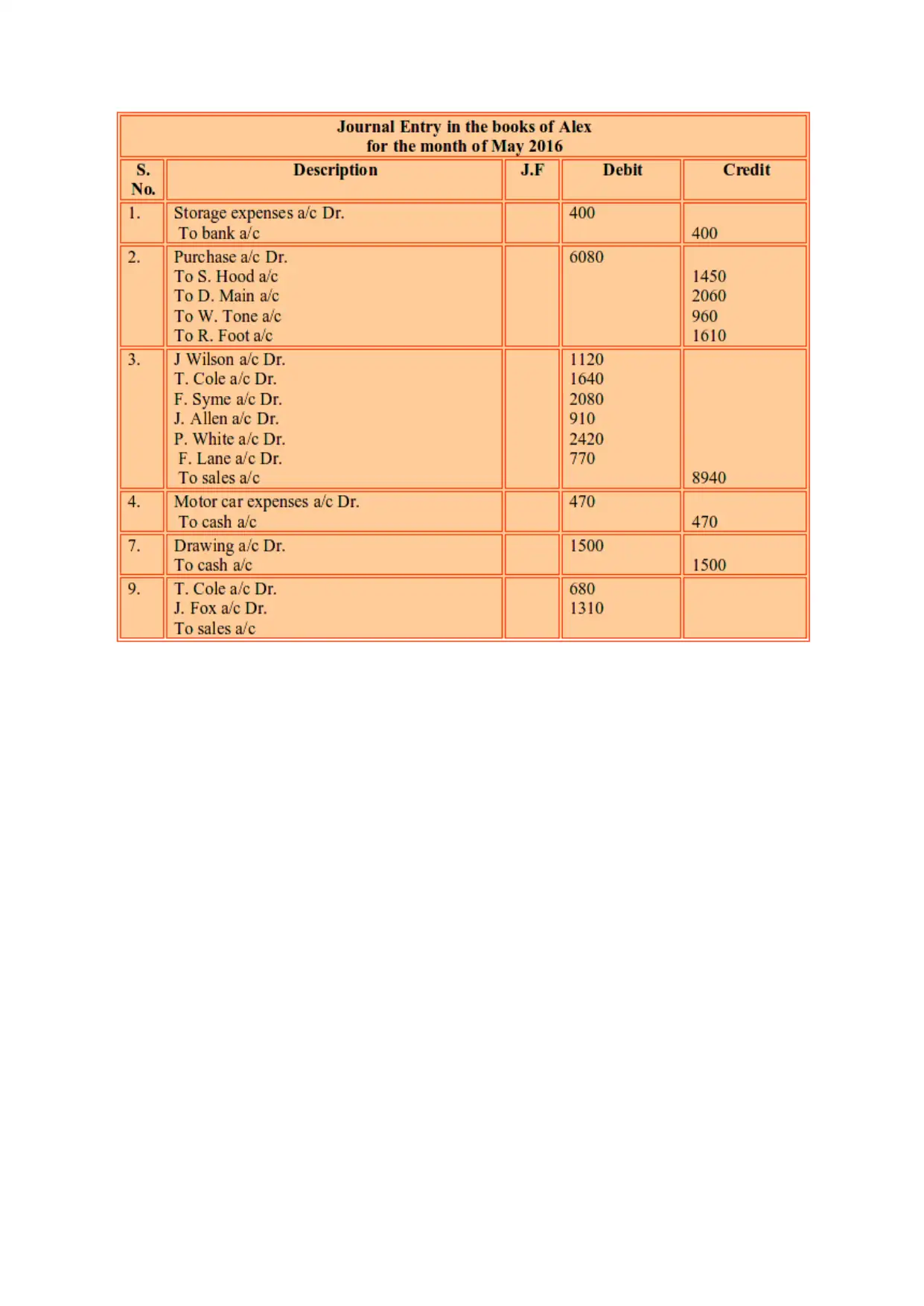

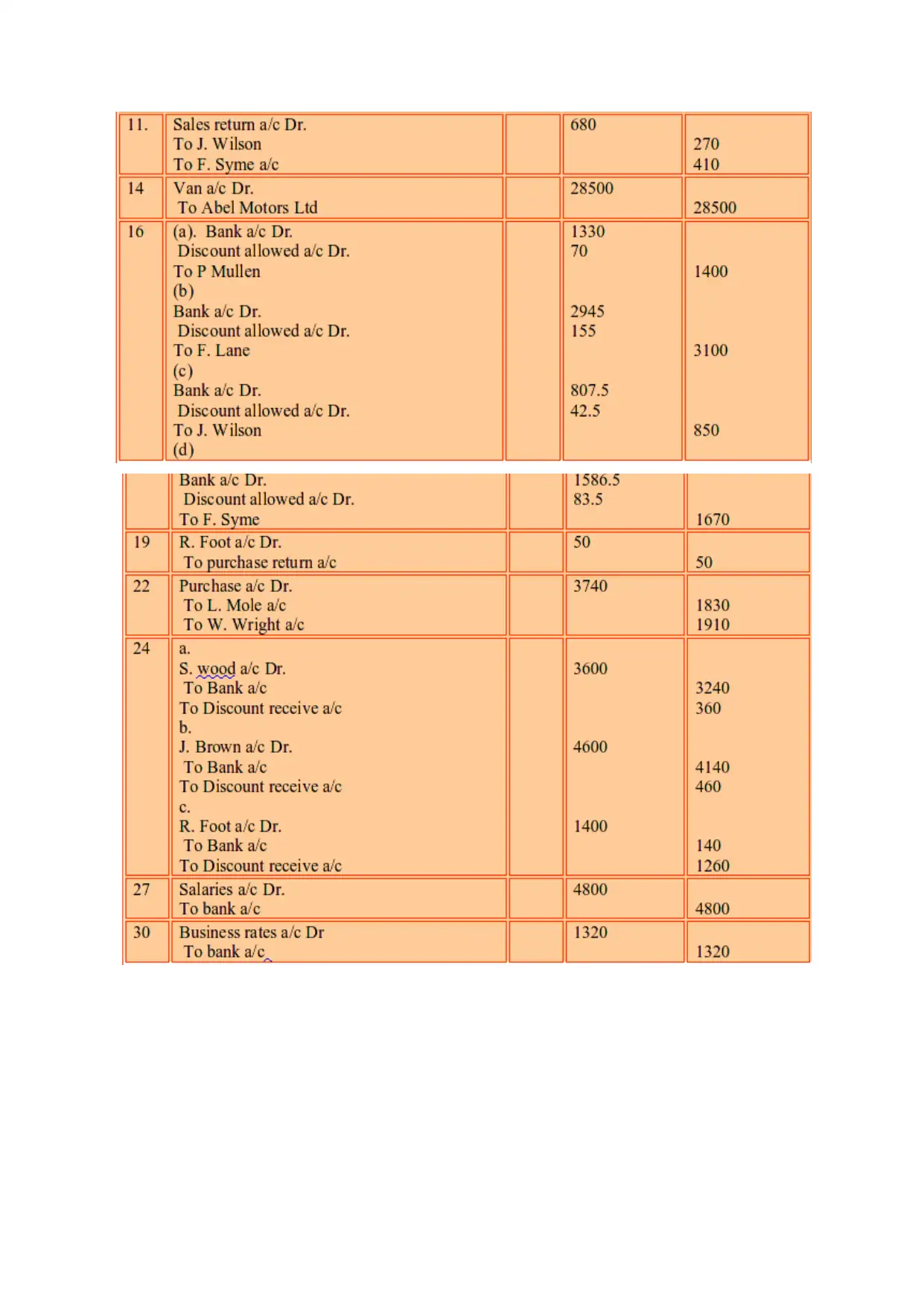

CLIENT 1

a. Journal entries

Journal of Alex Study’s

displayed in company’s financial accounts which make it free from any material

misstatement. Auditors focuses on it and present opinion whether company had fully

disclosed all the results or not and accounts are error free from any mistakes or errors

or not.

4. Explaining the concept and convention in relation to consistency & materiality

Consistency concept: This principle of accounting states that once specific principle

or rule is considered for dealing with business transaction then the same should be

continuously followed in the future period. It allows firm to change method or apply

new version only when it improves reported financial results. Thus, it can be

presented that such principle focuses on applying similar principles, methods,

practices and process over the years. IASB recognized consistency as one of the main

important element that makes accounting information highly valuable for the purpose

of decision making.

Material disclosure: In accounting, full disclosure principle is highly associated with

the concept or aspect of materiality. On the basis of such principle, accountant needs

to disclose all the material information either in the main financial statements or in

notes section (Materiality concept, 2017). Hence, materiality concept of accounting

lays emphasis on including all the information’s that may have influence on the

opinion of financial statement user’s.

CLIENT 1

a. Journal entries

Journal of Alex Study’s

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

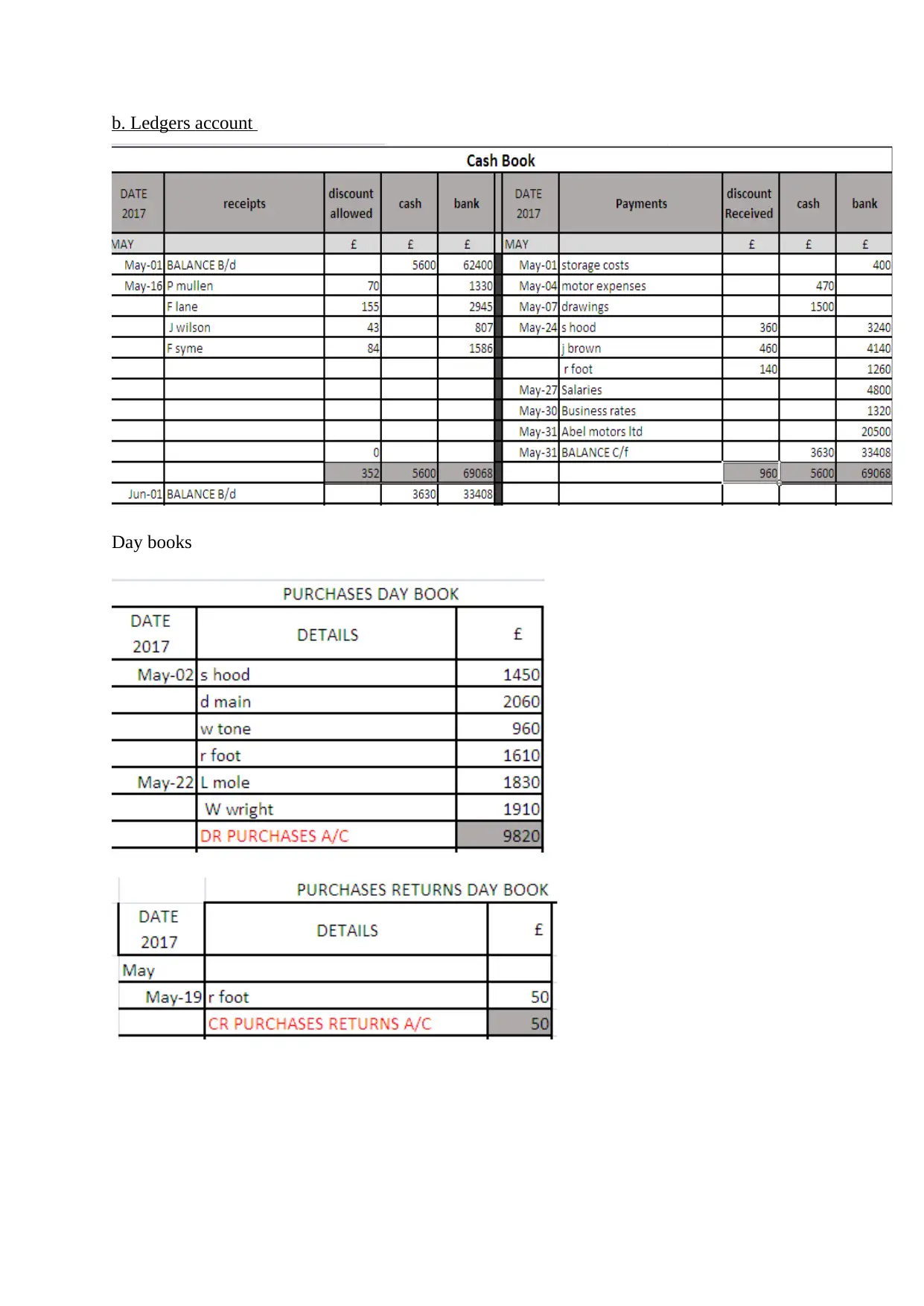

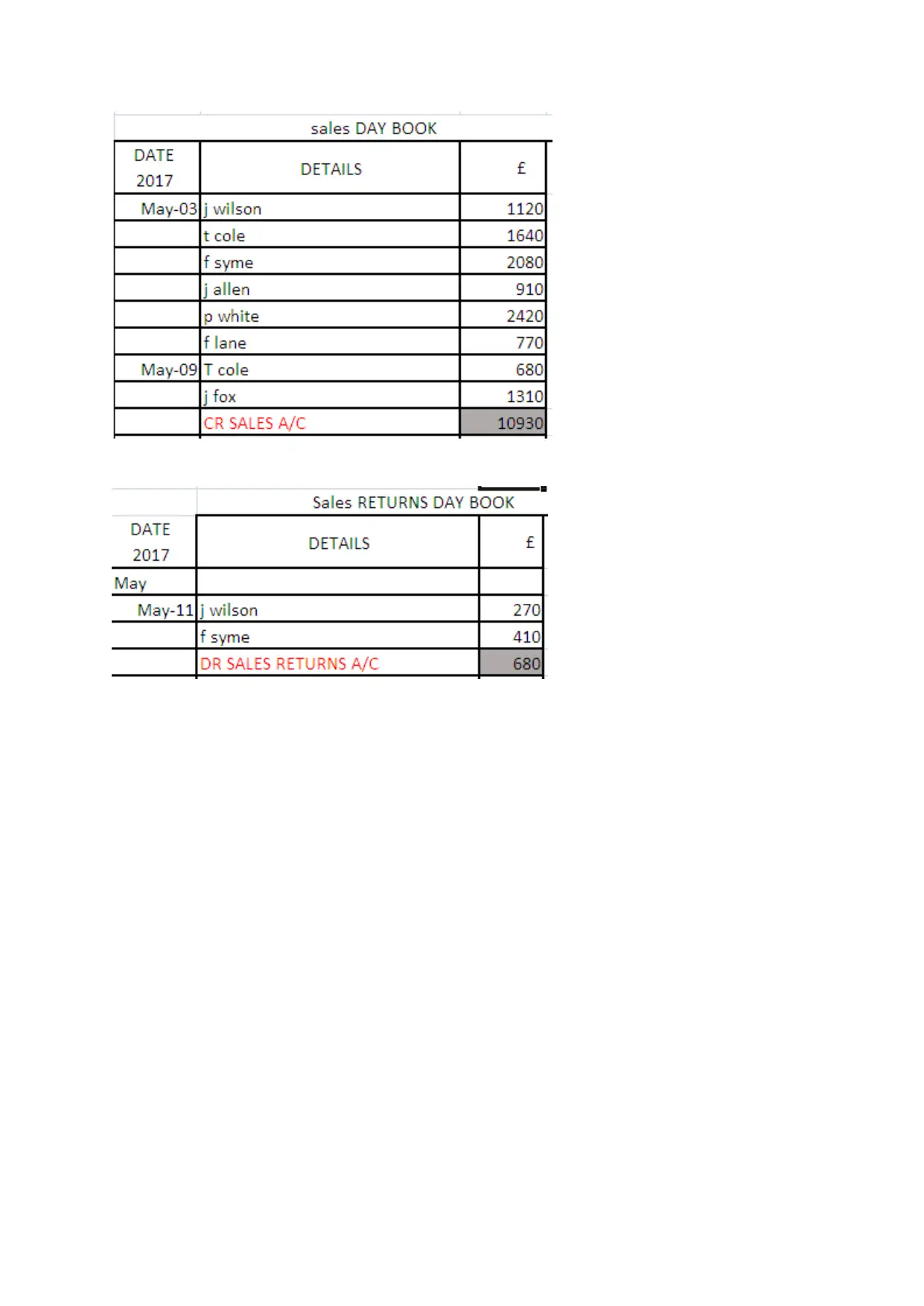

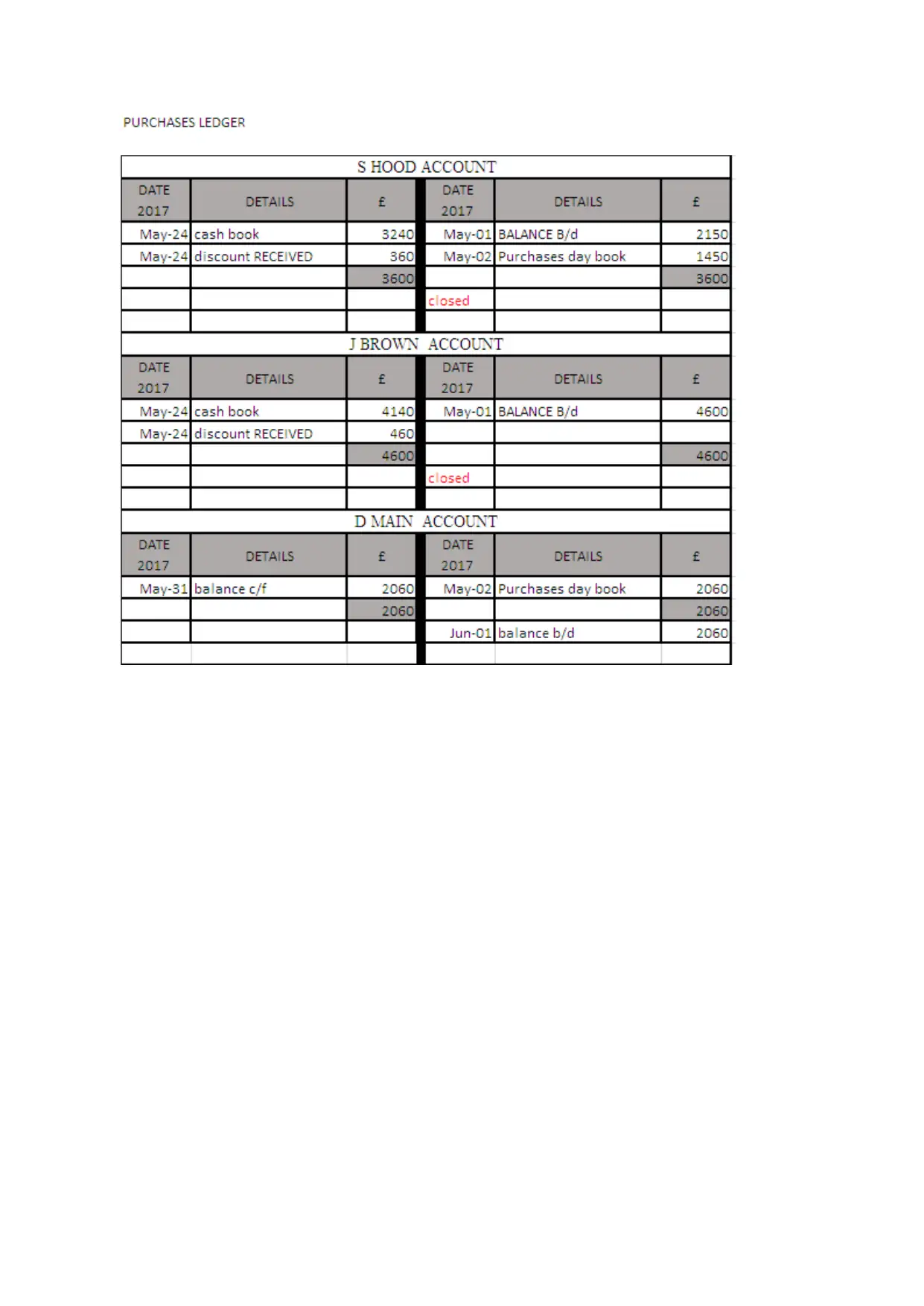

b. Ledgers account

Day books

Day books

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 33

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.