Government Impact on CO2 Emissions Reduction by Organizations in Different Countries

VerifiedAdded on 2023/06/07

|27

|3739

|244

AI Summary

This research proposal aims to establish whether the policies developed by various governments globally have had an impact on the mitigation of climate change by observing whether climate change has been integrated into the business strategies of companies and organizations as well as observing the respective carbon emission percentages by each company or organization.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MGT723 Research Project

Semester 2 2018

Assessment Task 2: Research Proposal

Student Name:

Draft Research Question: “Whether there is a change observed in carbon emissions by the

influence of stakeholder interference?”

Title: Government Impact and the reduction in CO2 emissions by organisations in different

countries.

Submission Date:

Acknowledgement:

I certify that I have carefully reviewed the university’s academic misconduct policy. I

understand that the source of ideas must be referenced and that quotation marks and a

reference are required when directly quoting anyone else’s words.

Semester 2 2018

Assessment Task 2: Research Proposal

Student Name:

Draft Research Question: “Whether there is a change observed in carbon emissions by the

influence of stakeholder interference?”

Title: Government Impact and the reduction in CO2 emissions by organisations in different

countries.

Submission Date:

Acknowledgement:

I certify that I have carefully reviewed the university’s academic misconduct policy. I

understand that the source of ideas must be referenced and that quotation marks and a

reference are required when directly quoting anyone else’s words.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

INTRODUCTION

Climate change has over the past few decades emerged as a major global issue. This

has been due to its effects, which have become more visible with the increase in

extreme weather events and patterns. This has forced governments globally to get

involved in fighting climate change.

Governments are charged with making policies that govern the various aspects of the

lives of the citizens. The policies include manufacturing and processing policies that

applied during the Industrial Revolution to generate wealth. These policies have

proven to contribute to a surge in carbon emissions globally since the Industrial

Revolution (Ecolife, 2011).

In order to combat climate change, presently, governments have been forced to

develop and implement policies that would assist in reducing carbon emissions (Oba,

2014). The policies can only be successful if they are integrated into the business

strategies of the various companies and organizations in the country in question.

This paper focuses on establishing whether the policies developed by the various

governments globally have had an impact on mitigation of climate change. This will be

achieved by observing whether climate change has been integrated into the business

strategies of companies and organization as well as observing the respective carbon

emission percentages by each company or organization.

2 | P a g e

Climate change has over the past few decades emerged as a major global issue. This

has been due to its effects, which have become more visible with the increase in

extreme weather events and patterns. This has forced governments globally to get

involved in fighting climate change.

Governments are charged with making policies that govern the various aspects of the

lives of the citizens. The policies include manufacturing and processing policies that

applied during the Industrial Revolution to generate wealth. These policies have

proven to contribute to a surge in carbon emissions globally since the Industrial

Revolution (Ecolife, 2011).

In order to combat climate change, presently, governments have been forced to

develop and implement policies that would assist in reducing carbon emissions (Oba,

2014). The policies can only be successful if they are integrated into the business

strategies of the various companies and organizations in the country in question.

This paper focuses on establishing whether the policies developed by the various

governments globally have had an impact on mitigation of climate change. This will be

achieved by observing whether climate change has been integrated into the business

strategies of companies and organization as well as observing the respective carbon

emission percentages by each company or organization.

2 | P a g e

LITERATURE REVIEW - SUMMARY

Today, we live in a culture that has been significantly shaped by the forces of industry.

We live in a society that has come to place an extreme value on the consumption of

goods and services. However, the environmental cost of this kind of culture is not always

immediately visible. To produce any single good or service, there is a long chain of

processes that should also be accounted for when considering the environmental cost of

anything. (Greenberg, 2014)

Organisations are using resources at a very high rate which results into increase in

carbon emissions into the environment. Carbon Dioxide Emissions means the release

of greenhouse gases and/or their precursors into the atmosphere over a specified

area and period of time. (OECD, 2005). Since the industrial revolution the burning of

fossil fuels has increased, which directly correlates to the increase of co2 emissions

level in our atmosphere and thus the rapid increase of global warming. (Ecolife, 2011).

Co2 emissions have a very negative impact on the environment such as causing

global warming, ocean acidification, smog pollution, ozone depletion as well as

changes to plant growth and nutrition levels.

Now a days, most of the organisations consider corporate social responsibility in their

business strategies and plans. Corporate social responsibility goes a long way in for

creating a positive word of mouth for the organization on the whole. Doing something

for your environment, society, stake holders, customers would not only take your

business to a higher level but also ensure long term growth and success.

There are number of theories such as legitimacy, agency and stakeholder but in my

perspective stakeholder theory is best. So in order to develop a hypothesis I am

utilizing stakeholder theory. According to Edward Freeman, stakeholder theory holds that

a company’s stakeholders include just about anyone affected by the company and its

workings. Freeman suggests that a company’s stakeholders are "those groups without

whose support the organization would cease to exist." These groups would include

customers, employees, suppliers, society, managers, owners, government, creditors,

shareholders and more (Freeman, 1984).

3 | P a g e

Today, we live in a culture that has been significantly shaped by the forces of industry.

We live in a society that has come to place an extreme value on the consumption of

goods and services. However, the environmental cost of this kind of culture is not always

immediately visible. To produce any single good or service, there is a long chain of

processes that should also be accounted for when considering the environmental cost of

anything. (Greenberg, 2014)

Organisations are using resources at a very high rate which results into increase in

carbon emissions into the environment. Carbon Dioxide Emissions means the release

of greenhouse gases and/or their precursors into the atmosphere over a specified

area and period of time. (OECD, 2005). Since the industrial revolution the burning of

fossil fuels has increased, which directly correlates to the increase of co2 emissions

level in our atmosphere and thus the rapid increase of global warming. (Ecolife, 2011).

Co2 emissions have a very negative impact on the environment such as causing

global warming, ocean acidification, smog pollution, ozone depletion as well as

changes to plant growth and nutrition levels.

Now a days, most of the organisations consider corporate social responsibility in their

business strategies and plans. Corporate social responsibility goes a long way in for

creating a positive word of mouth for the organization on the whole. Doing something

for your environment, society, stake holders, customers would not only take your

business to a higher level but also ensure long term growth and success.

There are number of theories such as legitimacy, agency and stakeholder but in my

perspective stakeholder theory is best. So in order to develop a hypothesis I am

utilizing stakeholder theory. According to Edward Freeman, stakeholder theory holds that

a company’s stakeholders include just about anyone affected by the company and its

workings. Freeman suggests that a company’s stakeholders are "those groups without

whose support the organization would cease to exist." These groups would include

customers, employees, suppliers, society, managers, owners, government, creditors,

shareholders and more (Freeman, 1984).

3 | P a g e

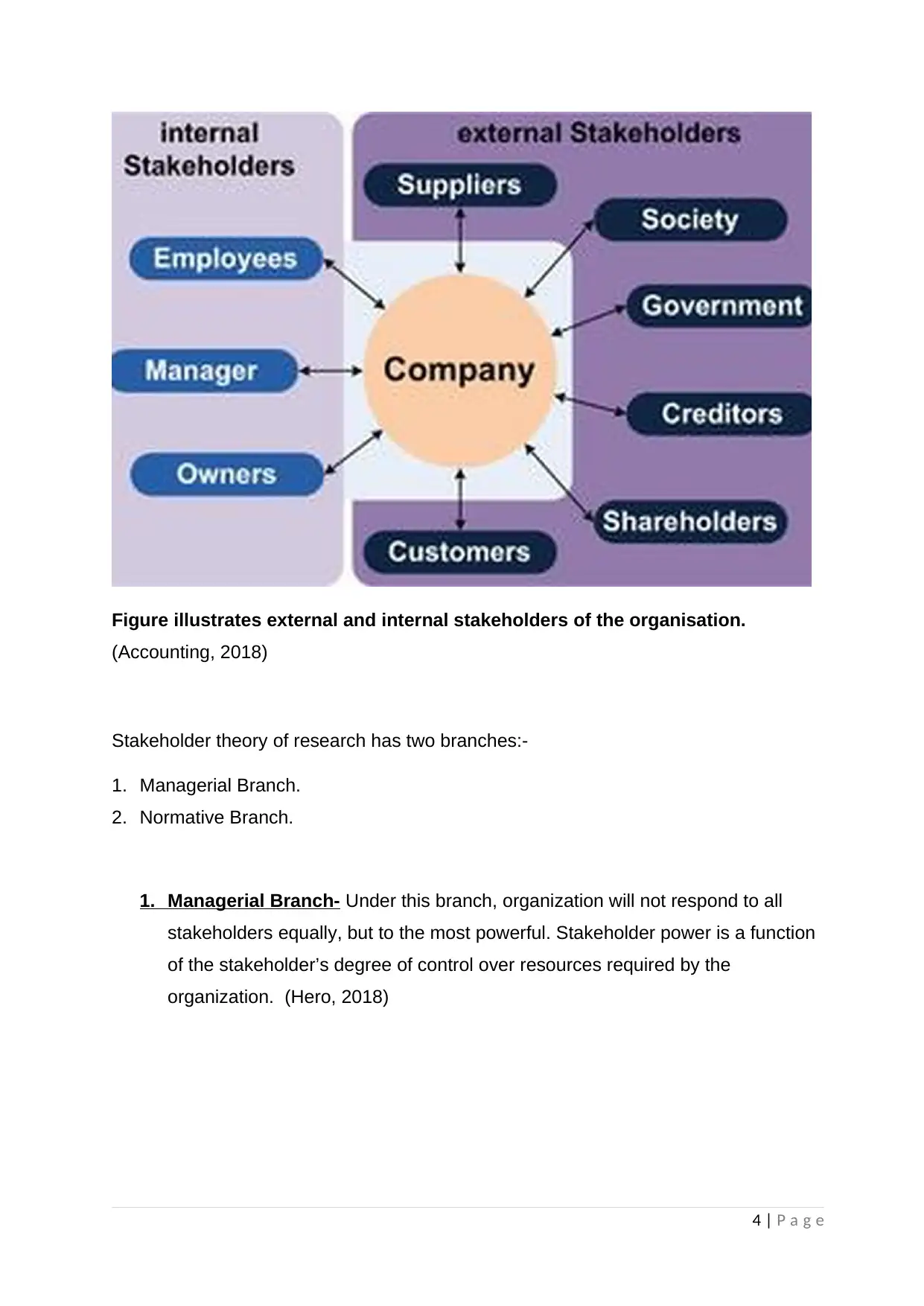

Figure illustrates external and internal stakeholders of the organisation.

(Accounting, 2018)

Stakeholder theory of research has two branches:-

1. Managerial Branch.

2. Normative Branch.

1. Managerial Branch- Under this branch, organization will not respond to all

stakeholders equally, but to the most powerful. Stakeholder power is a function

of the stakeholder’s degree of control over resources required by the

organization. (Hero, 2018)

4 | P a g e

(Accounting, 2018)

Stakeholder theory of research has two branches:-

1. Managerial Branch.

2. Normative Branch.

1. Managerial Branch- Under this branch, organization will not respond to all

stakeholders equally, but to the most powerful. Stakeholder power is a function

of the stakeholder’s degree of control over resources required by the

organization. (Hero, 2018)

4 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2. Normative Branch- This branch hold that managers ought to pay attention to

key stakeholder relationships. According to this perspective, managerial

relationships with stakeholders are based on normative, moral commitments.

Rather than on a desire to use those stakeholders solely to maximize profits.

(Zawaideh, 2006)

In order to consider environmental impact of the organization, out of these two

branches managerial branch of stakeholder theory is more effective and useful.

In order to identify the influence of stakeholders, organization can use stakeholder

salience. The Salience Model uses three parameters to categorize stakeholders:

Power, Legitimacy and Urgency. (Sharma, 2010)

1. The Stakeholders' Power to influence the firm.

2 Legitimacy of the stakeholders' relationships with the firm

3 The urgency of the stakeholders claim on the firm. (Morphy, 2008).

In my perspective, power is the best parameter to check the influence of the different

stakeholders on the firm. Out of the different stakeholders, government is the most

important and powerful stakeholder. There is a high degree of impact of government

on the organisations. This is because the government has many powers that could be

implemented on organisations depending on their environmental performance and

corporate social responsibility. Government can implement many policies such as

make new rules and regulations, impose taxes. Furthermore government can impose

penalties on the firms which are not considering their operational activities impact on

the environment.

5 | P a g e

key stakeholder relationships. According to this perspective, managerial

relationships with stakeholders are based on normative, moral commitments.

Rather than on a desire to use those stakeholders solely to maximize profits.

(Zawaideh, 2006)

In order to consider environmental impact of the organization, out of these two

branches managerial branch of stakeholder theory is more effective and useful.

In order to identify the influence of stakeholders, organization can use stakeholder

salience. The Salience Model uses three parameters to categorize stakeholders:

Power, Legitimacy and Urgency. (Sharma, 2010)

1. The Stakeholders' Power to influence the firm.

2 Legitimacy of the stakeholders' relationships with the firm

3 The urgency of the stakeholders claim on the firm. (Morphy, 2008).

In my perspective, power is the best parameter to check the influence of the different

stakeholders on the firm. Out of the different stakeholders, government is the most

important and powerful stakeholder. There is a high degree of impact of government

on the organisations. This is because the government has many powers that could be

implemented on organisations depending on their environmental performance and

corporate social responsibility. Government can implement many policies such as

make new rules and regulations, impose taxes. Furthermore government can impose

penalties on the firms which are not considering their operational activities impact on

the environment.

5 | P a g e

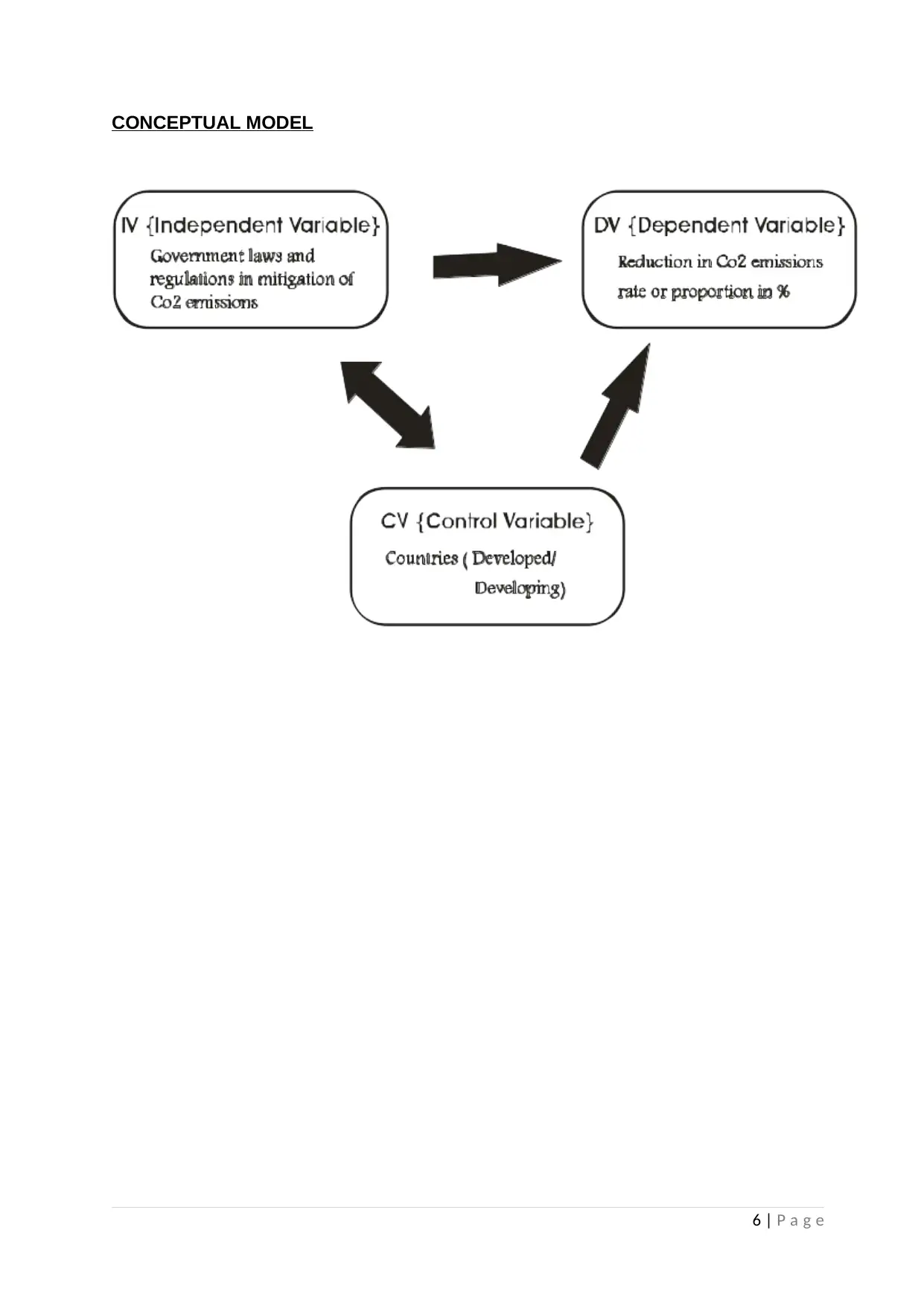

CONCEPTUAL MODEL

6 | P a g e

6 | P a g e

Hypotheses:-

H1: There is a positive relationship between government influence on industries and

reduction of carbon emissions in climate.

Ho: There is a no relationship between government influence on industries and

reduction of carbon emissions in climate.

7 | P a g e

H1: There is a positive relationship between government influence on industries and

reduction of carbon emissions in climate.

Ho: There is a no relationship between government influence on industries and

reduction of carbon emissions in climate.

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DATA DESCRIPTION AND PREPARATION

The sample data was collected from firms that are more directly involved in carbon

emissions. These firms were prioritized over other firms that are mostly consumers of

the products from firms that are directly involved in carbon emissions. The excluded

firms, which can be described as secondary contributors to carbon emissions, include

the firms in the financial industry. The firms considered for the samples were also

taken from four countries; Canada, United Kingdom, Brazil and United States of

America.

The sample data has three variables; Countries (those selected for observation and

research from which the firms originates), Government Role (in account of reduction of

CO2 emissions in the climate) and Emission Reduction Rate (in the rate of CO2

emissions by different companies).

The Countries variable is the Control Variable (CV) with four different categories.

These categories are the countries of Canada, United Kingdom, Brazil and United

States of America. This data variable is Nominal in nature.

The Government Role variable is the Independent Variable (IV) with two different

categories. Similar to the Countries variable, the Government Role is Nominal in

nature. The categories are 1 and 2; 1 represents “Yes” (the firm has climate change

integrated into its Business Strategy) while 2 represents “No” (the firm does not have

climate change integrated into its Business Strategy).

The Emission Reduction Rate is the dependent variable (DV). This data variable is

Ratio/Scale in nature representing the percentage change observed in 2013

compared to previous year’s data.

The sample data contains firms from various sectors or industries that can be

considered as primary contributors to carbon emissions. This therefore implies that the

analysis and findings from this research can be generalized for all sectors or industries

of the primary contributors.

However, the sample data only contains data collected from four countries; Canada,

United Kingdom, Brazil and United States of America. Whereas the list of countries

does include moderately industrialized to industrialized countries which are the

significant contributors to carbon emission, the list is not geographically balanced. The

8 | P a g e

The sample data was collected from firms that are more directly involved in carbon

emissions. These firms were prioritized over other firms that are mostly consumers of

the products from firms that are directly involved in carbon emissions. The excluded

firms, which can be described as secondary contributors to carbon emissions, include

the firms in the financial industry. The firms considered for the samples were also

taken from four countries; Canada, United Kingdom, Brazil and United States of

America.

The sample data has three variables; Countries (those selected for observation and

research from which the firms originates), Government Role (in account of reduction of

CO2 emissions in the climate) and Emission Reduction Rate (in the rate of CO2

emissions by different companies).

The Countries variable is the Control Variable (CV) with four different categories.

These categories are the countries of Canada, United Kingdom, Brazil and United

States of America. This data variable is Nominal in nature.

The Government Role variable is the Independent Variable (IV) with two different

categories. Similar to the Countries variable, the Government Role is Nominal in

nature. The categories are 1 and 2; 1 represents “Yes” (the firm has climate change

integrated into its Business Strategy) while 2 represents “No” (the firm does not have

climate change integrated into its Business Strategy).

The Emission Reduction Rate is the dependent variable (DV). This data variable is

Ratio/Scale in nature representing the percentage change observed in 2013

compared to previous year’s data.

The sample data contains firms from various sectors or industries that can be

considered as primary contributors to carbon emissions. This therefore implies that the

analysis and findings from this research can be generalized for all sectors or industries

of the primary contributors.

However, the sample data only contains data collected from four countries; Canada,

United Kingdom, Brazil and United States of America. Whereas the list of countries

does include moderately industrialized to industrialized countries which are the

significant contributors to carbon emission, the list is not geographically balanced. The

8 | P a g e

countries come from predominantly the Americas and Europe. Including countries

from the Middle East and Asia would have made the analysis and findings from this

research more generalizable in terms of region

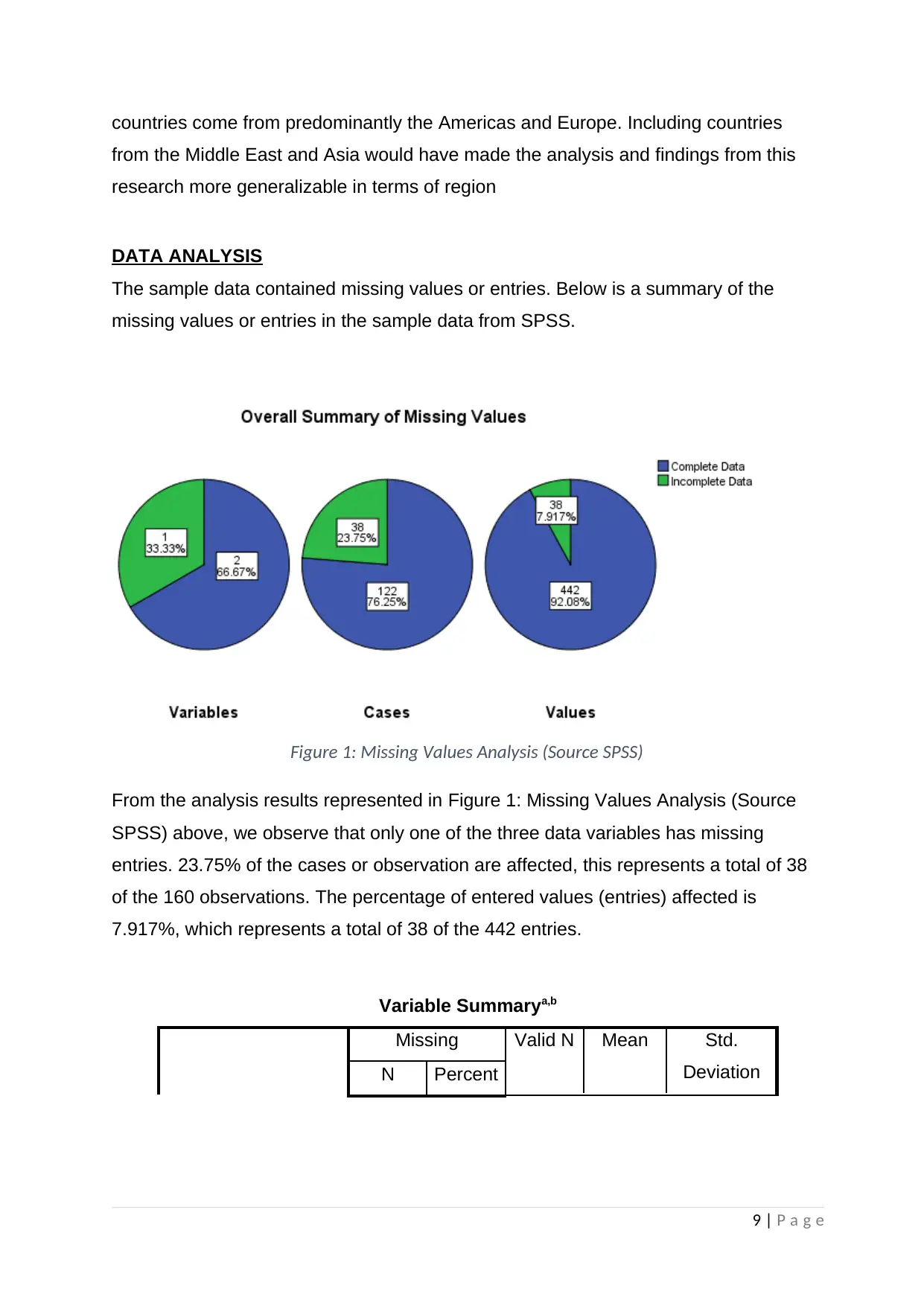

DATA ANALYSIS

The sample data contained missing values or entries. Below is a summary of the

missing values or entries in the sample data from SPSS.

Figure 1: Missing Values Analysis (Source SPSS)

From the analysis results represented in Figure 1: Missing Values Analysis (Source

SPSS) above, we observe that only one of the three data variables has missing

entries. 23.75% of the cases or observation are affected, this represents a total of 38

of the 160 observations. The percentage of entered values (entries) affected is

7.917%, which represents a total of 38 of the 442 entries.

Variable Summarya,b

Missing Valid N Mean Std.

DeviationN Percent

9 | P a g e

from the Middle East and Asia would have made the analysis and findings from this

research more generalizable in terms of region

DATA ANALYSIS

The sample data contained missing values or entries. Below is a summary of the

missing values or entries in the sample data from SPSS.

Figure 1: Missing Values Analysis (Source SPSS)

From the analysis results represented in Figure 1: Missing Values Analysis (Source

SPSS) above, we observe that only one of the three data variables has missing

entries. 23.75% of the cases or observation are affected, this represents a total of 38

of the 160 observations. The percentage of entered values (entries) affected is

7.917%, which represents a total of 38 of the 442 entries.

Variable Summarya,b

Missing Valid N Mean Std.

DeviationN Percent

9 | P a g e

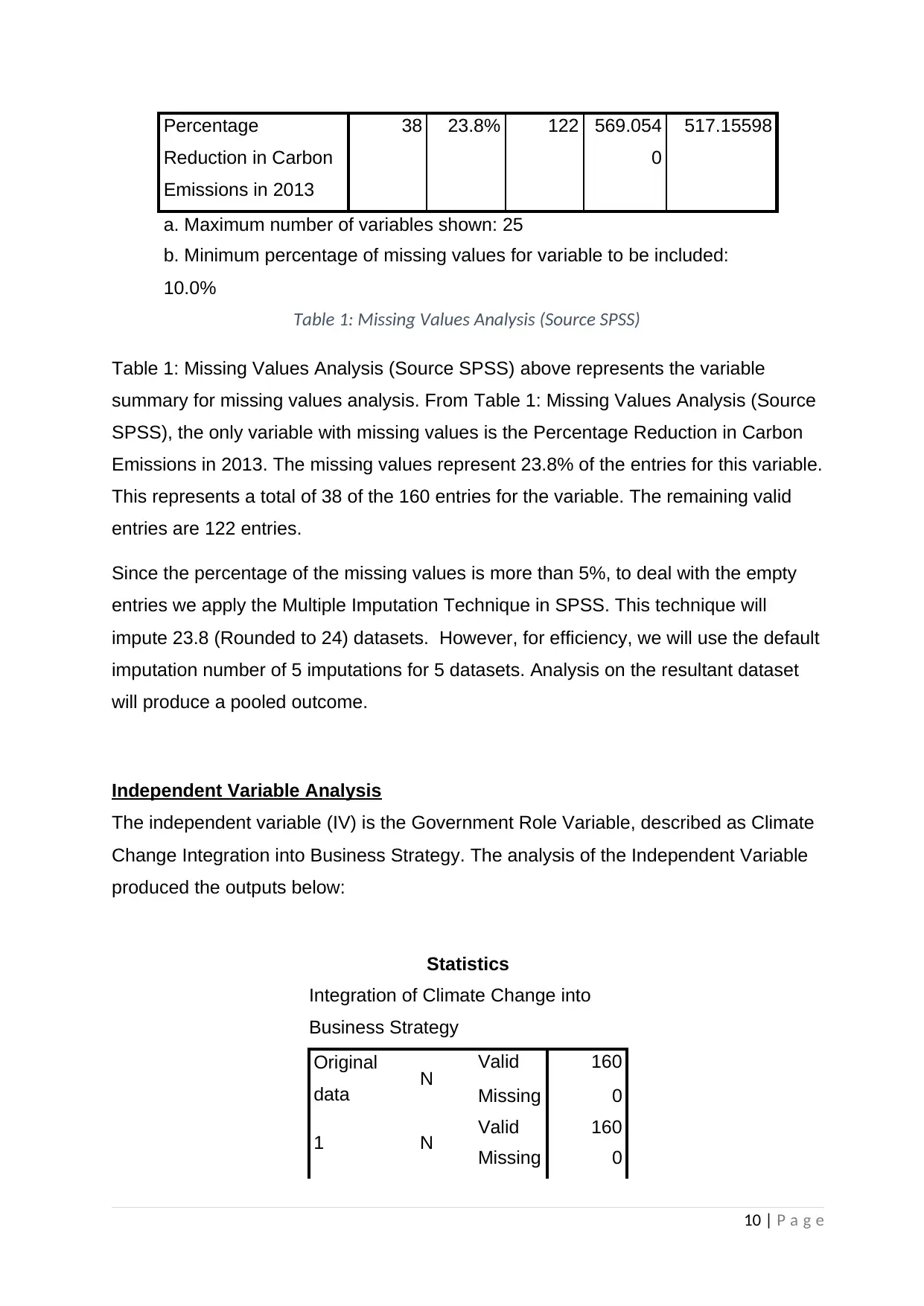

Percentage

Reduction in Carbon

Emissions in 2013

38 23.8% 122 569.054

0

517.15598

a. Maximum number of variables shown: 25

b. Minimum percentage of missing values for variable to be included:

10.0%

Table 1: Missing Values Analysis (Source SPSS)

Table 1: Missing Values Analysis (Source SPSS) above represents the variable

summary for missing values analysis. From Table 1: Missing Values Analysis (Source

SPSS), the only variable with missing values is the Percentage Reduction in Carbon

Emissions in 2013. The missing values represent 23.8% of the entries for this variable.

This represents a total of 38 of the 160 entries for the variable. The remaining valid

entries are 122 entries.

Since the percentage of the missing values is more than 5%, to deal with the empty

entries we apply the Multiple Imputation Technique in SPSS. This technique will

impute 23.8 (Rounded to 24) datasets. However, for efficiency, we will use the default

imputation number of 5 imputations for 5 datasets. Analysis on the resultant dataset

will produce a pooled outcome.

Independent Variable Analysis

The independent variable (IV) is the Government Role Variable, described as Climate

Change Integration into Business Strategy. The analysis of the Independent Variable

produced the outputs below:

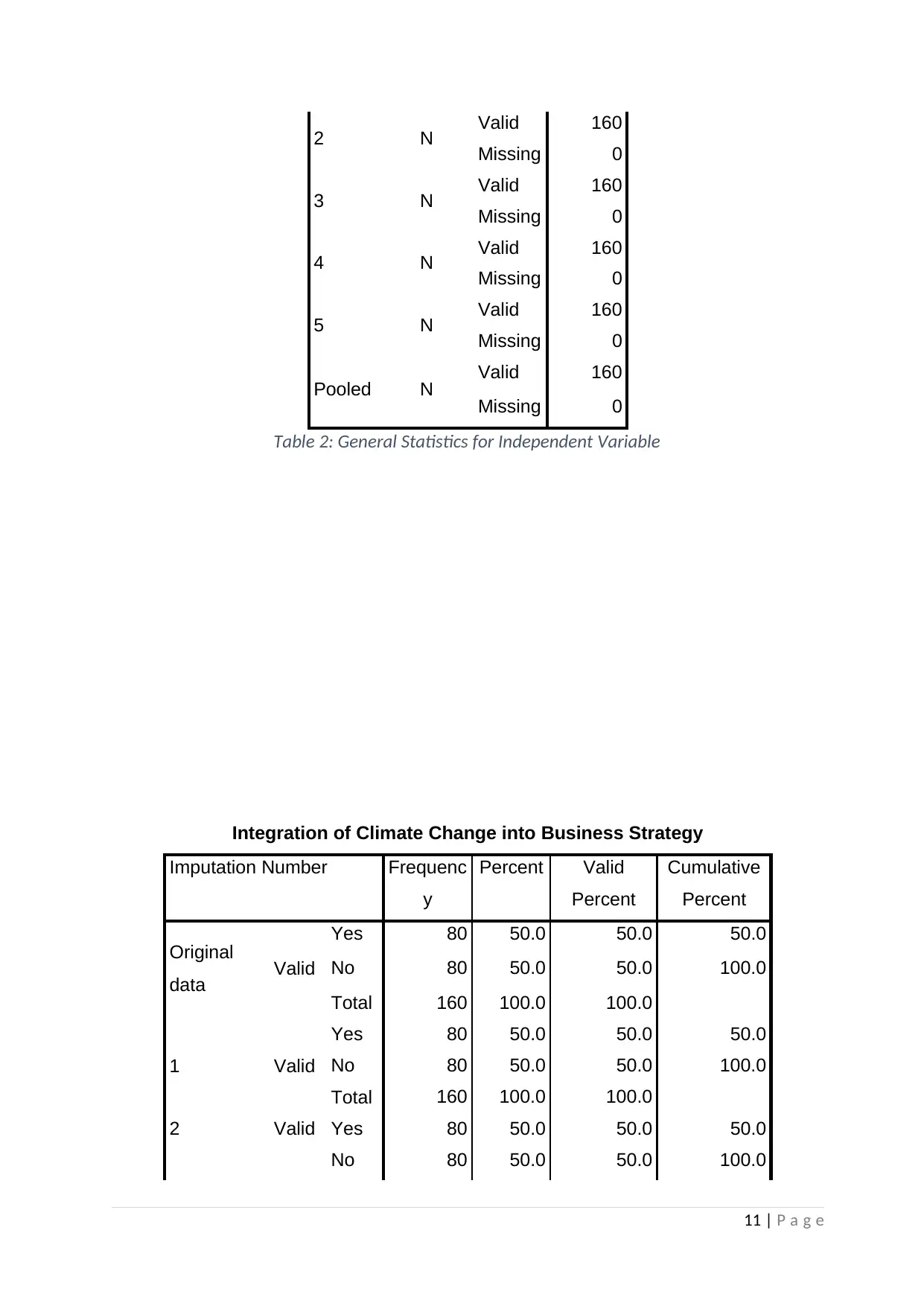

Statistics

Integration of Climate Change into

Business Strategy

Original

data N Valid 160

Missing 0

1 N Valid 160

Missing 0

10 | P a g e

Reduction in Carbon

Emissions in 2013

38 23.8% 122 569.054

0

517.15598

a. Maximum number of variables shown: 25

b. Minimum percentage of missing values for variable to be included:

10.0%

Table 1: Missing Values Analysis (Source SPSS)

Table 1: Missing Values Analysis (Source SPSS) above represents the variable

summary for missing values analysis. From Table 1: Missing Values Analysis (Source

SPSS), the only variable with missing values is the Percentage Reduction in Carbon

Emissions in 2013. The missing values represent 23.8% of the entries for this variable.

This represents a total of 38 of the 160 entries for the variable. The remaining valid

entries are 122 entries.

Since the percentage of the missing values is more than 5%, to deal with the empty

entries we apply the Multiple Imputation Technique in SPSS. This technique will

impute 23.8 (Rounded to 24) datasets. However, for efficiency, we will use the default

imputation number of 5 imputations for 5 datasets. Analysis on the resultant dataset

will produce a pooled outcome.

Independent Variable Analysis

The independent variable (IV) is the Government Role Variable, described as Climate

Change Integration into Business Strategy. The analysis of the Independent Variable

produced the outputs below:

Statistics

Integration of Climate Change into

Business Strategy

Original

data N Valid 160

Missing 0

1 N Valid 160

Missing 0

10 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2 N Valid 160

Missing 0

3 N Valid 160

Missing 0

4 N Valid 160

Missing 0

5 N Valid 160

Missing 0

Pooled N Valid 160

Missing 0

Table 2: General Statistics for Independent Variable

Integration of Climate Change into Business Strategy

Imputation Number Frequenc

y

Percent Valid

Percent

Cumulative

Percent

Original

data Valid

Yes 80 50.0 50.0 50.0

No 80 50.0 50.0 100.0

Total 160 100.0 100.0

1 Valid

Yes 80 50.0 50.0 50.0

No 80 50.0 50.0 100.0

Total 160 100.0 100.0

2 Valid Yes 80 50.0 50.0 50.0

No 80 50.0 50.0 100.0

11 | P a g e

Missing 0

3 N Valid 160

Missing 0

4 N Valid 160

Missing 0

5 N Valid 160

Missing 0

Pooled N Valid 160

Missing 0

Table 2: General Statistics for Independent Variable

Integration of Climate Change into Business Strategy

Imputation Number Frequenc

y

Percent Valid

Percent

Cumulative

Percent

Original

data Valid

Yes 80 50.0 50.0 50.0

No 80 50.0 50.0 100.0

Total 160 100.0 100.0

1 Valid

Yes 80 50.0 50.0 50.0

No 80 50.0 50.0 100.0

Total 160 100.0 100.0

2 Valid Yes 80 50.0 50.0 50.0

No 80 50.0 50.0 100.0

11 | P a g e

Total 160 100.0 100.0

3 Valid

Yes 80 50.0 50.0 50.0

No 80 50.0 50.0 100.0

Total 160 100.0 100.0

4 Valid

Yes 80 50.0 50.0 50.0

No 80 50.0 50.0 100.0

Total 160 100.0 100.0

5 Valid

Yes 80 50.0 50.0 50.0

No 80 50.0 50.0 100.0

Total 160 100.0 100.0

Pooled Valid

Yes 80

No 80

Total 160

Table 3: Detailed Statistics for Independent Variable

From Table 2: General Statistics for Independent Variable we observe that the

Independent Variable had no missing values in all the imputations with a total of 160

entries in each imputation. The pooled results show no missing values and a total of

160 entries as well.

From Table 3: Detailed Statistics for Independent Variable we observe 80 “Yes”

responses, representing 50% of the cases, and the remaining 80 responses being

“No”, equally representing 50%. This represents the results of the analysis in each of

the imputation as well as the pooled results.

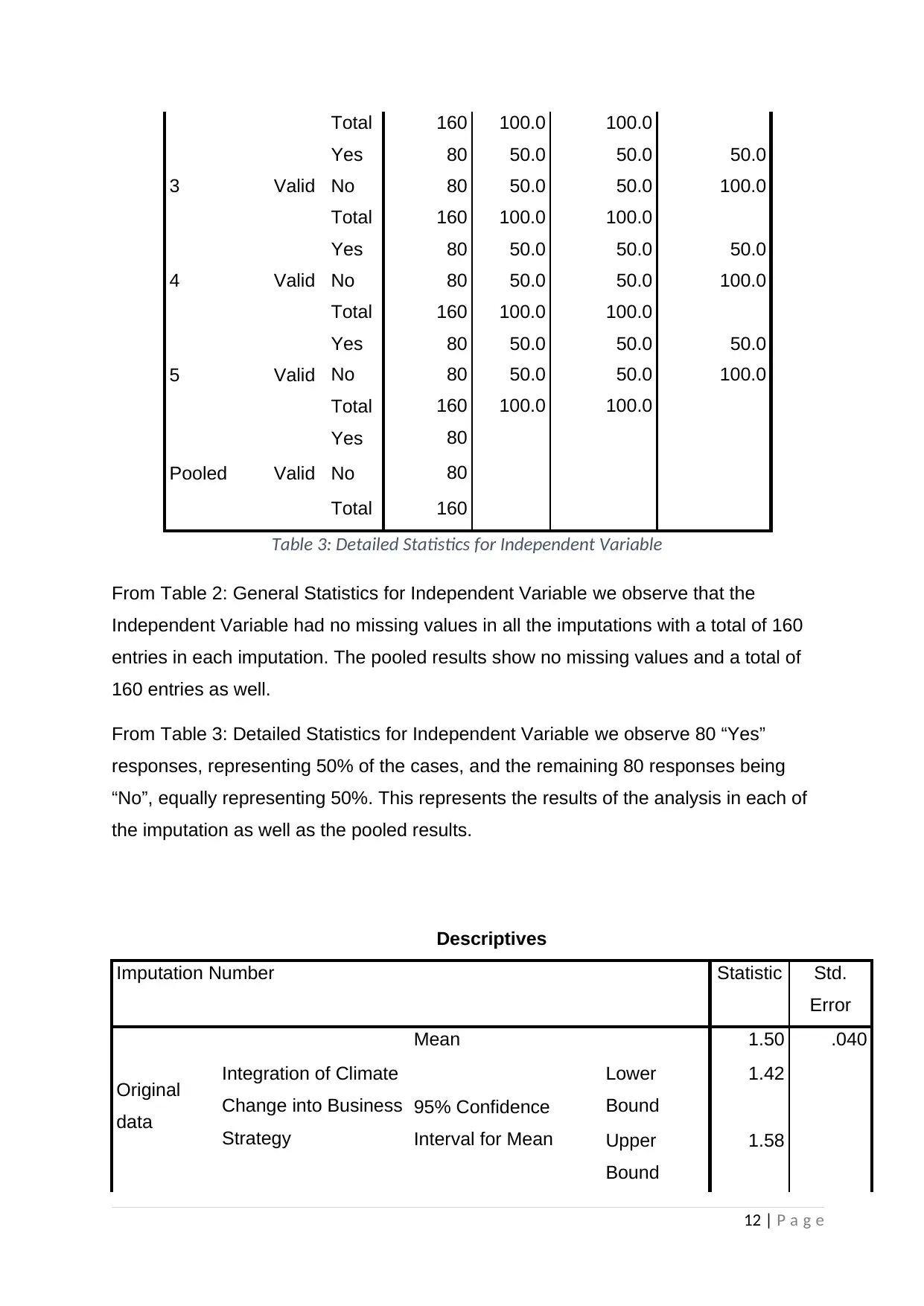

Descriptives

Imputation Number Statistic Std.

Error

Original

data

Integration of Climate

Change into Business

Strategy

Mean 1.50 .040

95% Confidence

Interval for Mean

Lower

Bound

1.42

Upper

Bound

1.58

12 | P a g e

3 Valid

Yes 80 50.0 50.0 50.0

No 80 50.0 50.0 100.0

Total 160 100.0 100.0

4 Valid

Yes 80 50.0 50.0 50.0

No 80 50.0 50.0 100.0

Total 160 100.0 100.0

5 Valid

Yes 80 50.0 50.0 50.0

No 80 50.0 50.0 100.0

Total 160 100.0 100.0

Pooled Valid

Yes 80

No 80

Total 160

Table 3: Detailed Statistics for Independent Variable

From Table 2: General Statistics for Independent Variable we observe that the

Independent Variable had no missing values in all the imputations with a total of 160

entries in each imputation. The pooled results show no missing values and a total of

160 entries as well.

From Table 3: Detailed Statistics for Independent Variable we observe 80 “Yes”

responses, representing 50% of the cases, and the remaining 80 responses being

“No”, equally representing 50%. This represents the results of the analysis in each of

the imputation as well as the pooled results.

Descriptives

Imputation Number Statistic Std.

Error

Original

data

Integration of Climate

Change into Business

Strategy

Mean 1.50 .040

95% Confidence

Interval for Mean

Lower

Bound

1.42

Upper

Bound

1.58

12 | P a g e

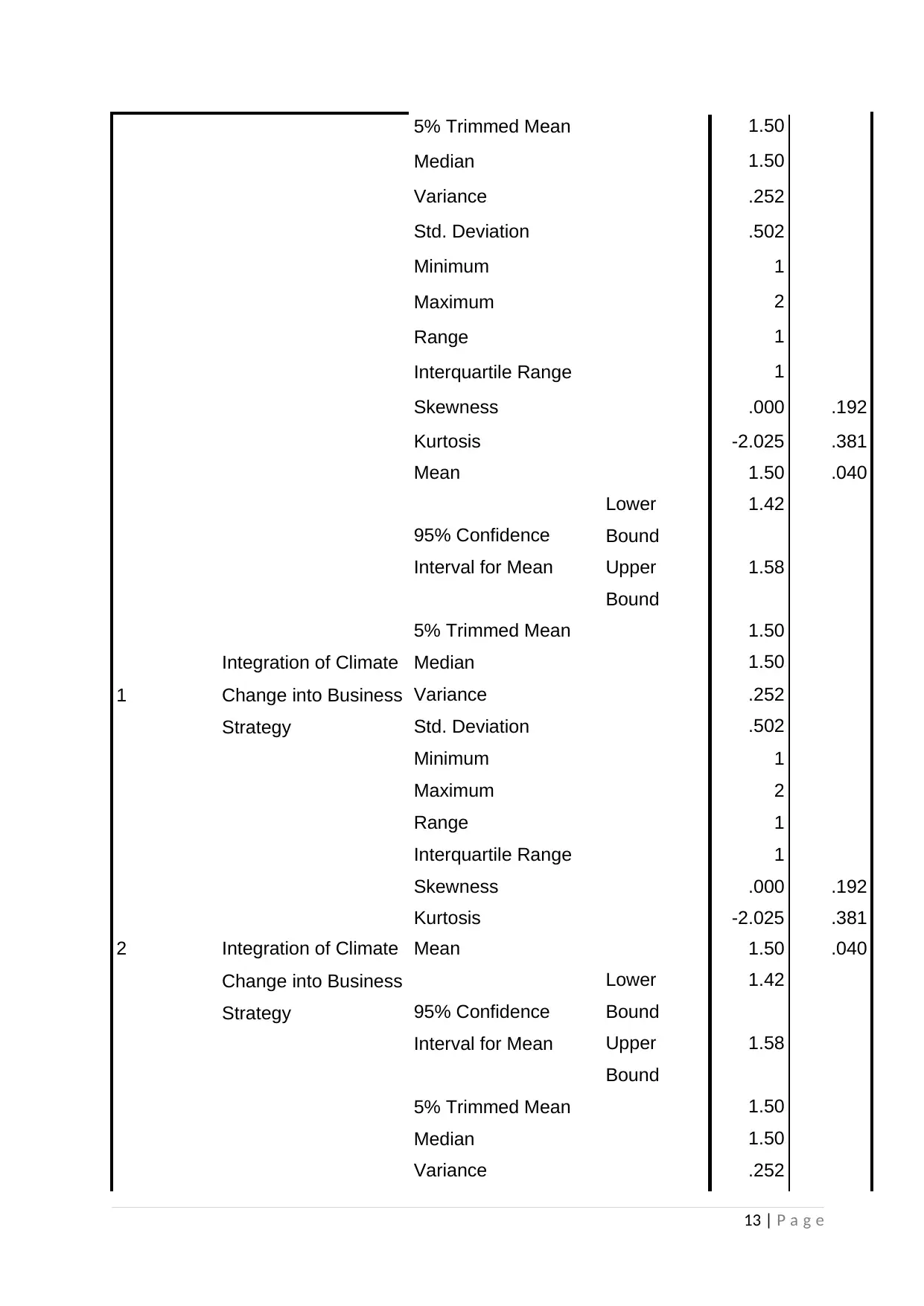

5% Trimmed Mean 1.50

Median 1.50

Variance .252

Std. Deviation .502

Minimum 1

Maximum 2

Range 1

Interquartile Range 1

Skewness .000 .192

Kurtosis -2.025 .381

1

Integration of Climate

Change into Business

Strategy

Mean 1.50 .040

95% Confidence

Interval for Mean

Lower

Bound

1.42

Upper

Bound

1.58

5% Trimmed Mean 1.50

Median 1.50

Variance .252

Std. Deviation .502

Minimum 1

Maximum 2

Range 1

Interquartile Range 1

Skewness .000 .192

Kurtosis -2.025 .381

2 Integration of Climate

Change into Business

Strategy

Mean 1.50 .040

95% Confidence

Interval for Mean

Lower

Bound

1.42

Upper

Bound

1.58

5% Trimmed Mean 1.50

Median 1.50

Variance .252

13 | P a g e

Median 1.50

Variance .252

Std. Deviation .502

Minimum 1

Maximum 2

Range 1

Interquartile Range 1

Skewness .000 .192

Kurtosis -2.025 .381

1

Integration of Climate

Change into Business

Strategy

Mean 1.50 .040

95% Confidence

Interval for Mean

Lower

Bound

1.42

Upper

Bound

1.58

5% Trimmed Mean 1.50

Median 1.50

Variance .252

Std. Deviation .502

Minimum 1

Maximum 2

Range 1

Interquartile Range 1

Skewness .000 .192

Kurtosis -2.025 .381

2 Integration of Climate

Change into Business

Strategy

Mean 1.50 .040

95% Confidence

Interval for Mean

Lower

Bound

1.42

Upper

Bound

1.58

5% Trimmed Mean 1.50

Median 1.50

Variance .252

13 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Std. Deviation .502

Minimum 1

Maximum 2

Range 1

Interquartile Range 1

Skewness .000 .192

Kurtosis -2.025 .381

3

Integration of Climate

Change into Business

Strategy

Mean 1.50 .040

95% Confidence

Interval for Mean

Lower

Bound

1.42

Upper

Bound

1.58

5% Trimmed Mean 1.50

Median 1.50

Variance .252

Std. Deviation .502

Minimum 1

Maximum 2

Range 1

Interquartile Range 1

Skewness .000 .192

Kurtosis -2.025 .381

4 Integration of Climate

Change into Business

Strategy

Mean 1.50 .040

95% Confidence

Interval for Mean

Lower

Bound

1.42

Upper

Bound

1.58

5% Trimmed Mean 1.50

Median 1.50

Variance .252

Std. Deviation .502

Minimum 1

Maximum 2

Range 1

14 | P a g e

Minimum 1

Maximum 2

Range 1

Interquartile Range 1

Skewness .000 .192

Kurtosis -2.025 .381

3

Integration of Climate

Change into Business

Strategy

Mean 1.50 .040

95% Confidence

Interval for Mean

Lower

Bound

1.42

Upper

Bound

1.58

5% Trimmed Mean 1.50

Median 1.50

Variance .252

Std. Deviation .502

Minimum 1

Maximum 2

Range 1

Interquartile Range 1

Skewness .000 .192

Kurtosis -2.025 .381

4 Integration of Climate

Change into Business

Strategy

Mean 1.50 .040

95% Confidence

Interval for Mean

Lower

Bound

1.42

Upper

Bound

1.58

5% Trimmed Mean 1.50

Median 1.50

Variance .252

Std. Deviation .502

Minimum 1

Maximum 2

Range 1

14 | P a g e

Interquartile Range 1

Skewness .000 .192

Kurtosis -2.025 .381

5

Integration of Climate

Change into Business

Strategy

Mean 1.50 .040

95% Confidence

Interval for Mean

Lower

Bound

1.42

Upper

Bound

1.58

5% Trimmed Mean 1.50

Median 1.50

Variance .252

Std. Deviation .502

Minimum 1

Maximum 2

Range 1

Interquartile Range 1

Skewness .000 .192

Kurtosis -2.025 .381

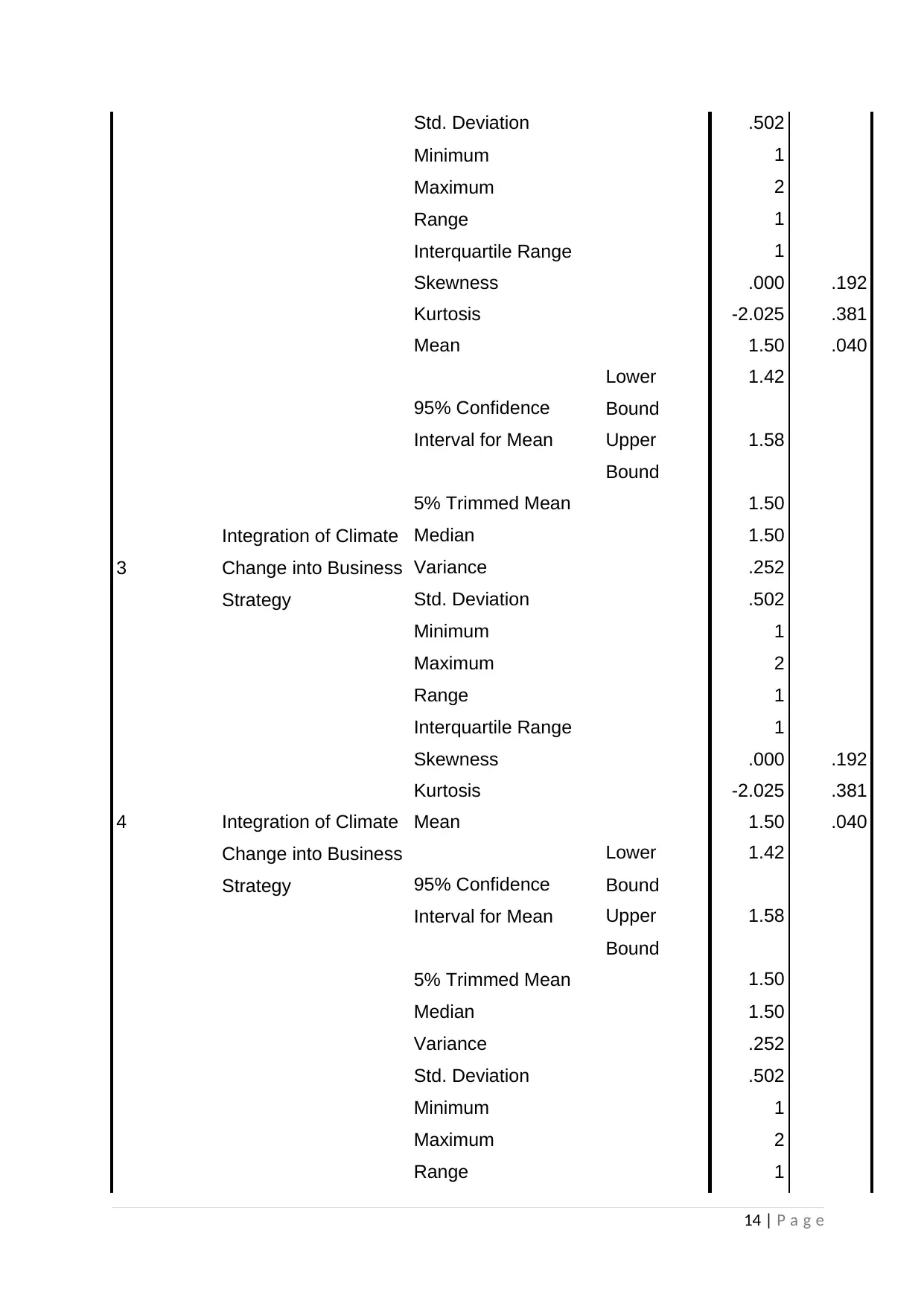

Table 4: Normality Analysis of Independent Variable

From Table 4: Normality Analysis of Independent Variable we observe that the

statistics for the normality are identical for all the imputations. Hence, the Independent

Variable can be said to have a Range = 2, Interquartile Range = 1, Skewness = 0,

Kurtosis = -2.025.

15 | P a g e

Skewness .000 .192

Kurtosis -2.025 .381

5

Integration of Climate

Change into Business

Strategy

Mean 1.50 .040

95% Confidence

Interval for Mean

Lower

Bound

1.42

Upper

Bound

1.58

5% Trimmed Mean 1.50

Median 1.50

Variance .252

Std. Deviation .502

Minimum 1

Maximum 2

Range 1

Interquartile Range 1

Skewness .000 .192

Kurtosis -2.025 .381

Table 4: Normality Analysis of Independent Variable

From Table 4: Normality Analysis of Independent Variable we observe that the

statistics for the normality are identical for all the imputations. Hence, the Independent

Variable can be said to have a Range = 2, Interquartile Range = 1, Skewness = 0,

Kurtosis = -2.025.

15 | P a g e

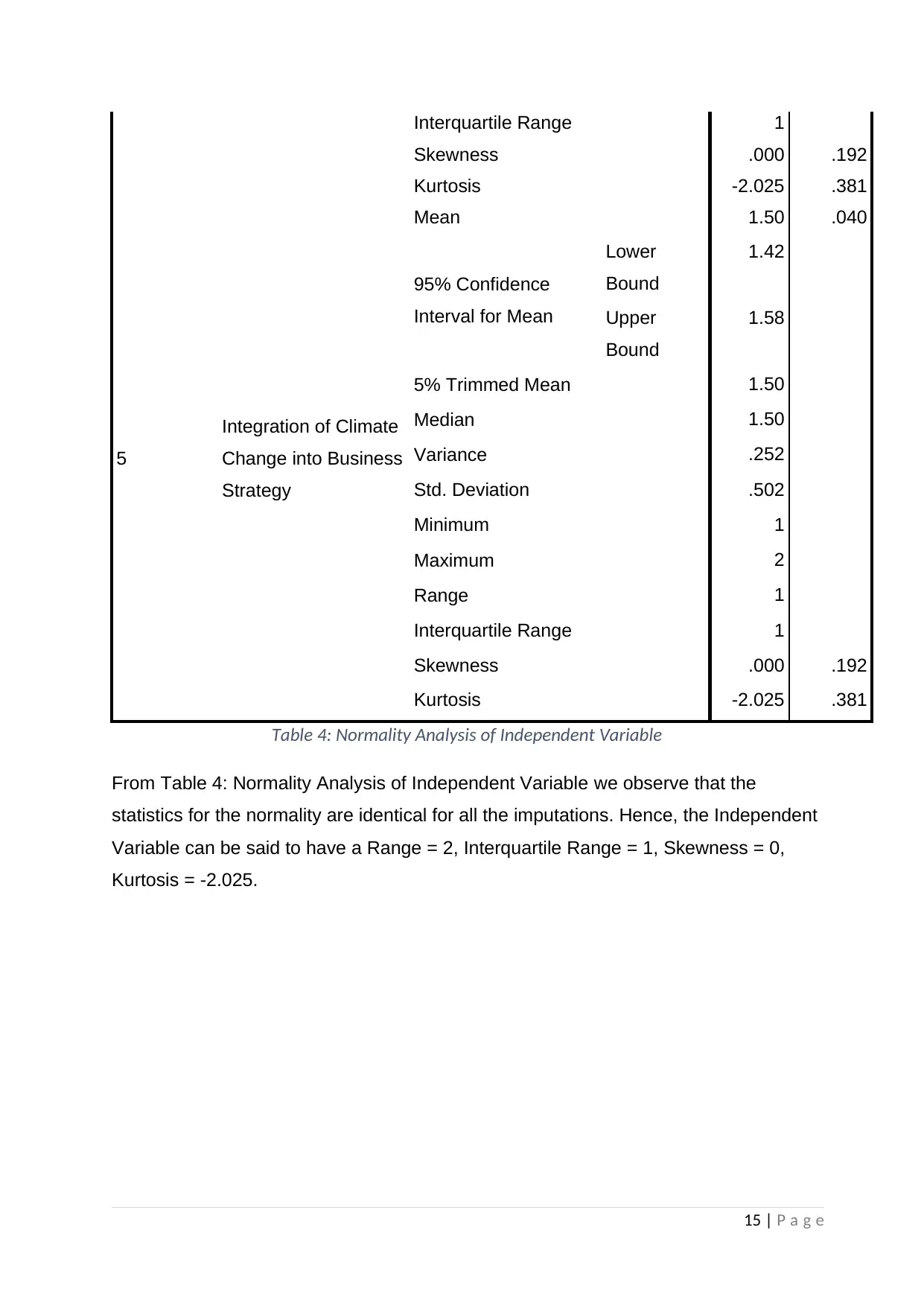

Figure 2: Graphical Analysis of the Independent Variable

Figure 2: Graphical Analysis of the Independent Variable confirms the analysis results

presented in Table 3: Detailed Statistics for Independent Variable above.

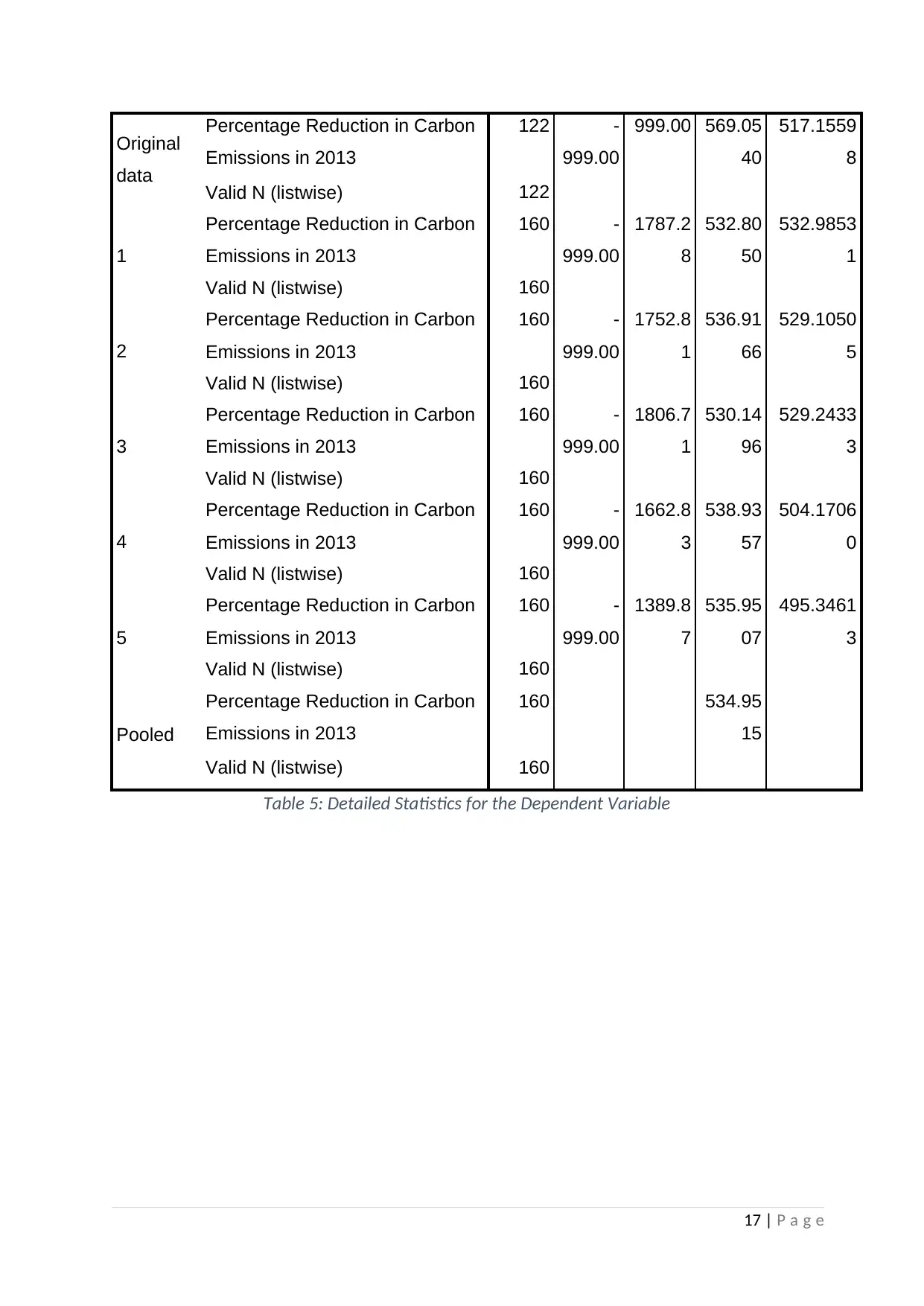

Dependent Variable Analysis

The dependent variable (DV) is the Emission Reduction Rate, described as

Percentage Reduction in Carbon Emission in 2013. The analysis of dependent

variable produced the outputs below:

Descriptive Statistics

Imputation Number N Minimu

m

Maxim

um

Mean Std.

Deviation

16 | P a g e

Figure 2: Graphical Analysis of the Independent Variable confirms the analysis results

presented in Table 3: Detailed Statistics for Independent Variable above.

Dependent Variable Analysis

The dependent variable (DV) is the Emission Reduction Rate, described as

Percentage Reduction in Carbon Emission in 2013. The analysis of dependent

variable produced the outputs below:

Descriptive Statistics

Imputation Number N Minimu

m

Maxim

um

Mean Std.

Deviation

16 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Original

data

Percentage Reduction in Carbon

Emissions in 2013

122 -

999.00

999.00 569.05

40

517.1559

8

Valid N (listwise) 122

1

Percentage Reduction in Carbon

Emissions in 2013

160 -

999.00

1787.2

8

532.80

50

532.9853

1

Valid N (listwise) 160

2

Percentage Reduction in Carbon

Emissions in 2013

160 -

999.00

1752.8

1

536.91

66

529.1050

5

Valid N (listwise) 160

3

Percentage Reduction in Carbon

Emissions in 2013

160 -

999.00

1806.7

1

530.14

96

529.2433

3

Valid N (listwise) 160

4

Percentage Reduction in Carbon

Emissions in 2013

160 -

999.00

1662.8

3

538.93

57

504.1706

0

Valid N (listwise) 160

5

Percentage Reduction in Carbon

Emissions in 2013

160 -

999.00

1389.8

7

535.95

07

495.3461

3

Valid N (listwise) 160

Pooled

Percentage Reduction in Carbon

Emissions in 2013

160 534.95

15

Valid N (listwise) 160

Table 5: Detailed Statistics for the Dependent Variable

17 | P a g e

data

Percentage Reduction in Carbon

Emissions in 2013

122 -

999.00

999.00 569.05

40

517.1559

8

Valid N (listwise) 122

1

Percentage Reduction in Carbon

Emissions in 2013

160 -

999.00

1787.2

8

532.80

50

532.9853

1

Valid N (listwise) 160

2

Percentage Reduction in Carbon

Emissions in 2013

160 -

999.00

1752.8

1

536.91

66

529.1050

5

Valid N (listwise) 160

3

Percentage Reduction in Carbon

Emissions in 2013

160 -

999.00

1806.7

1

530.14

96

529.2433

3

Valid N (listwise) 160

4

Percentage Reduction in Carbon

Emissions in 2013

160 -

999.00

1662.8

3

538.93

57

504.1706

0

Valid N (listwise) 160

5

Percentage Reduction in Carbon

Emissions in 2013

160 -

999.00

1389.8

7

535.95

07

495.3461

3

Valid N (listwise) 160

Pooled

Percentage Reduction in Carbon

Emissions in 2013

160 534.95

15

Valid N (listwise) 160

Table 5: Detailed Statistics for the Dependent Variable

17 | P a g e

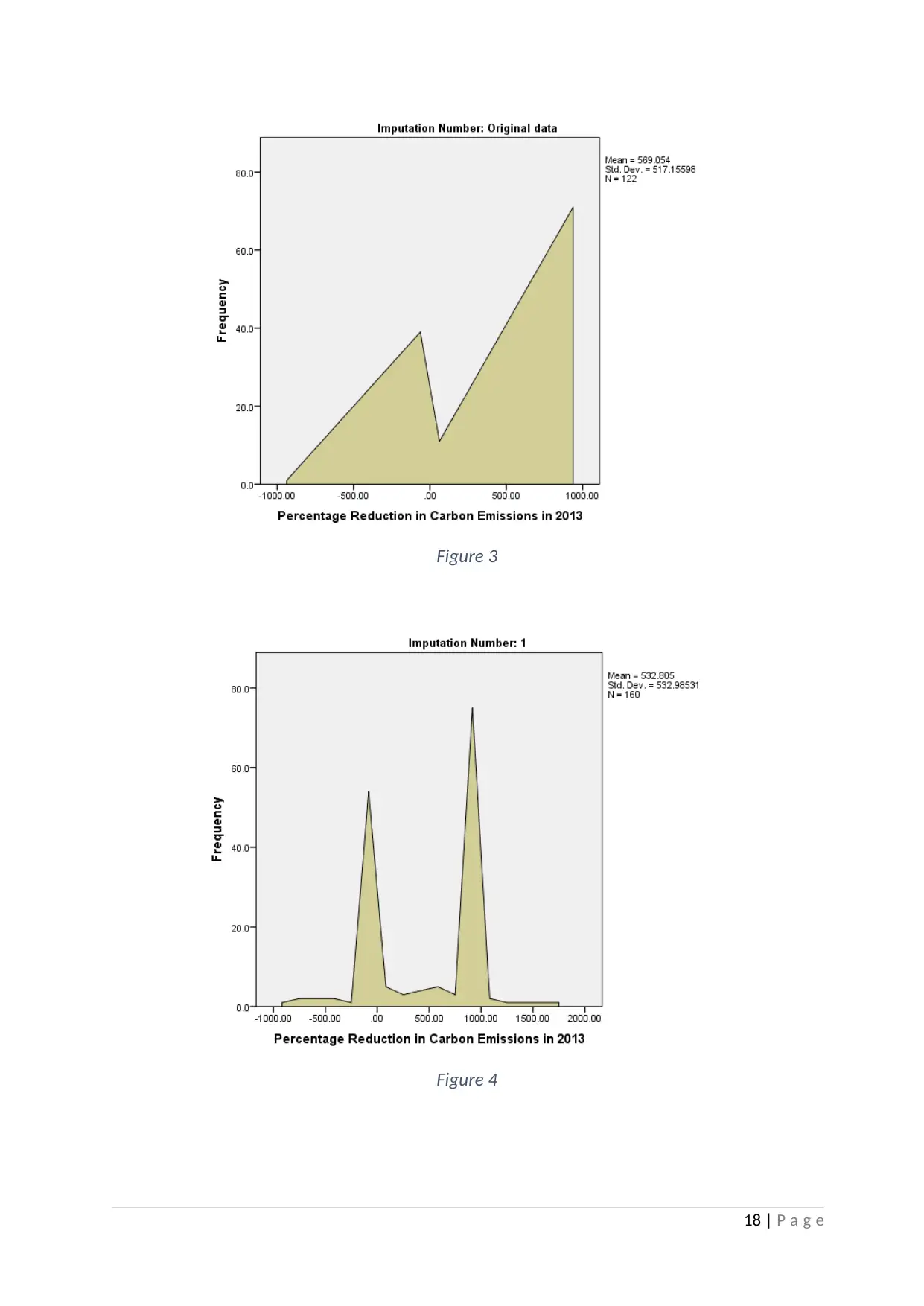

Figure 3

Figure 4

18 | P a g e

Figure 4

18 | P a g e

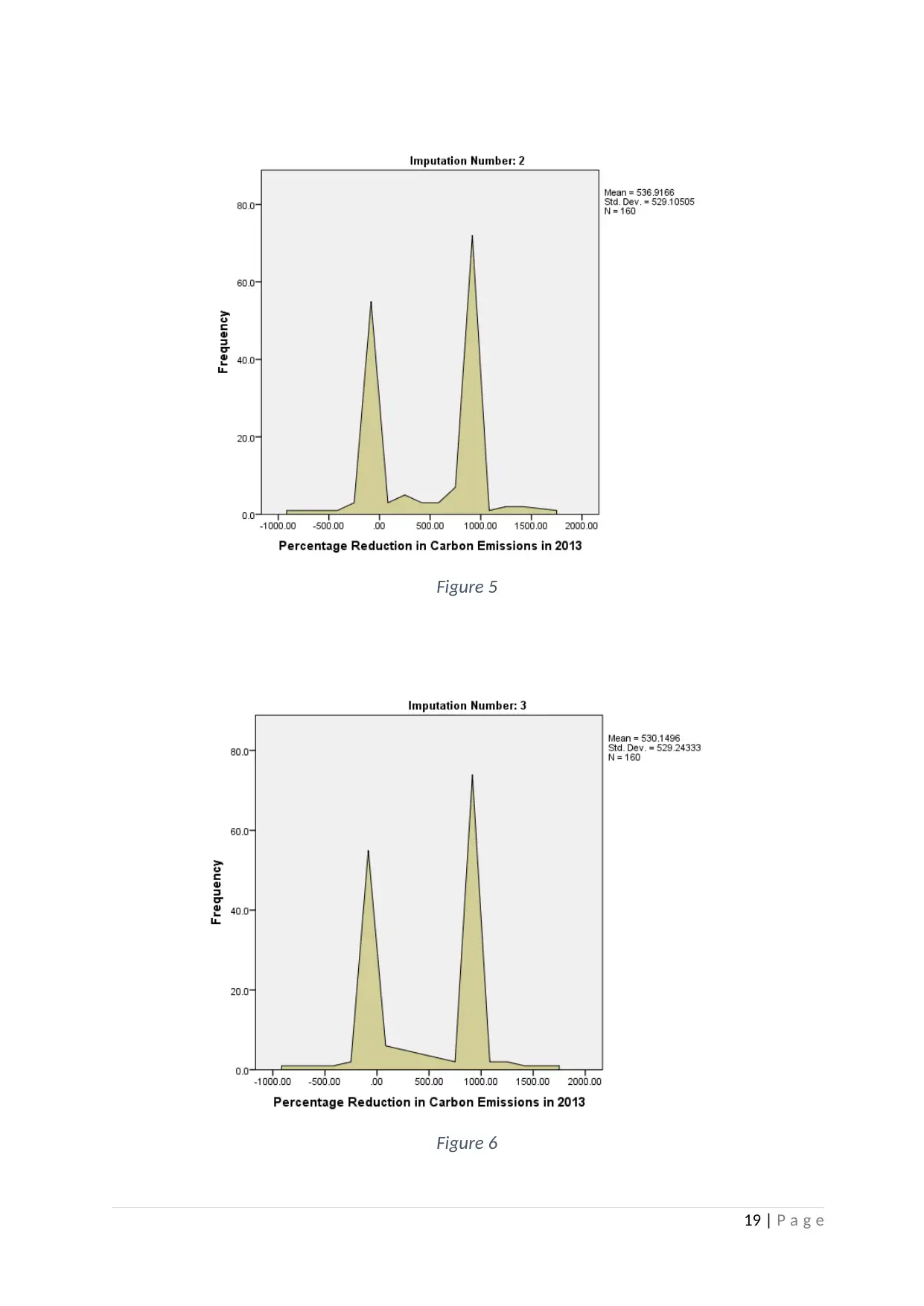

Figure 5

Figure 6

19 | P a g e

Figure 6

19 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

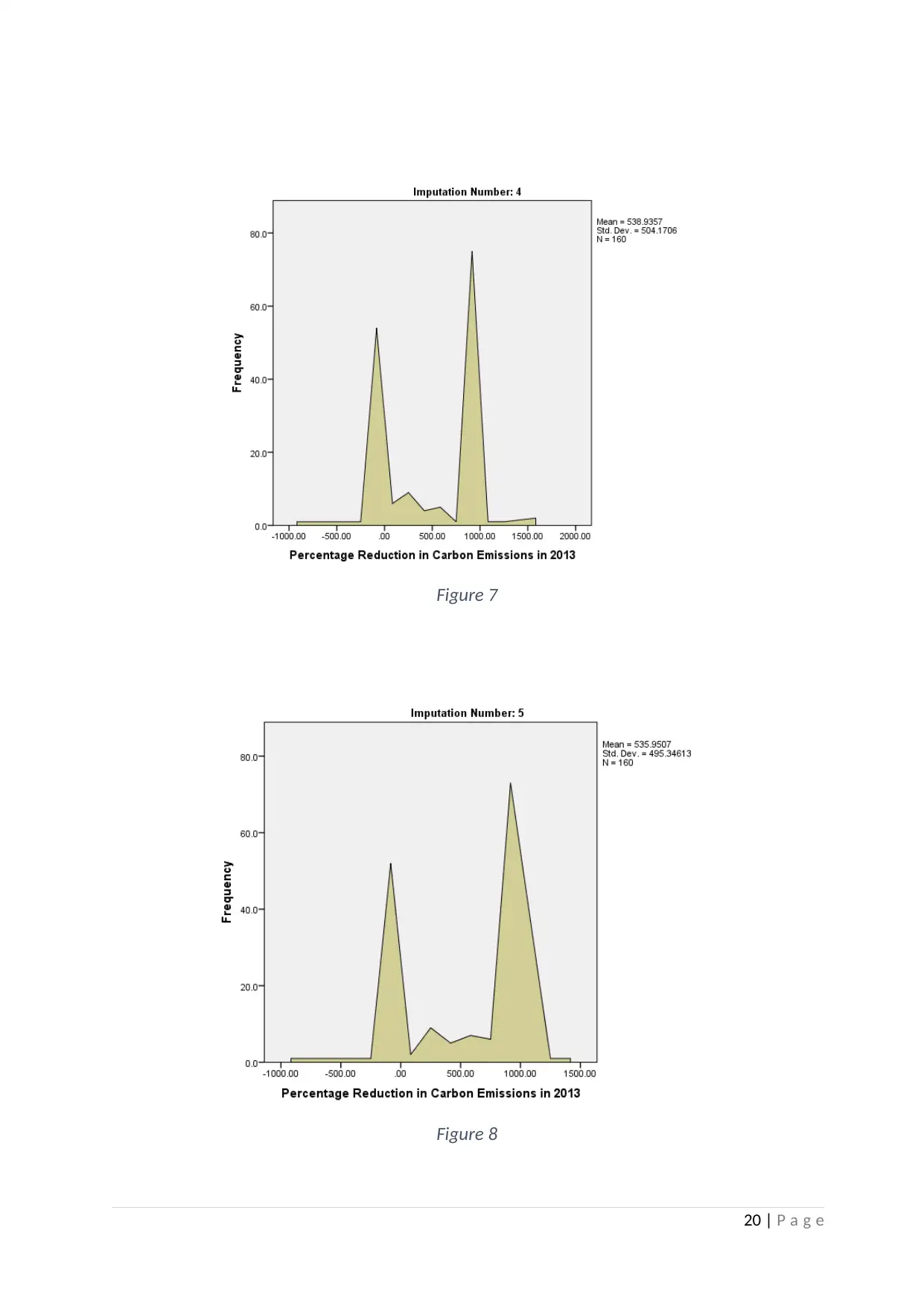

Figure 7

Figure 8

20 | P a g e

Figure 8

20 | P a g e

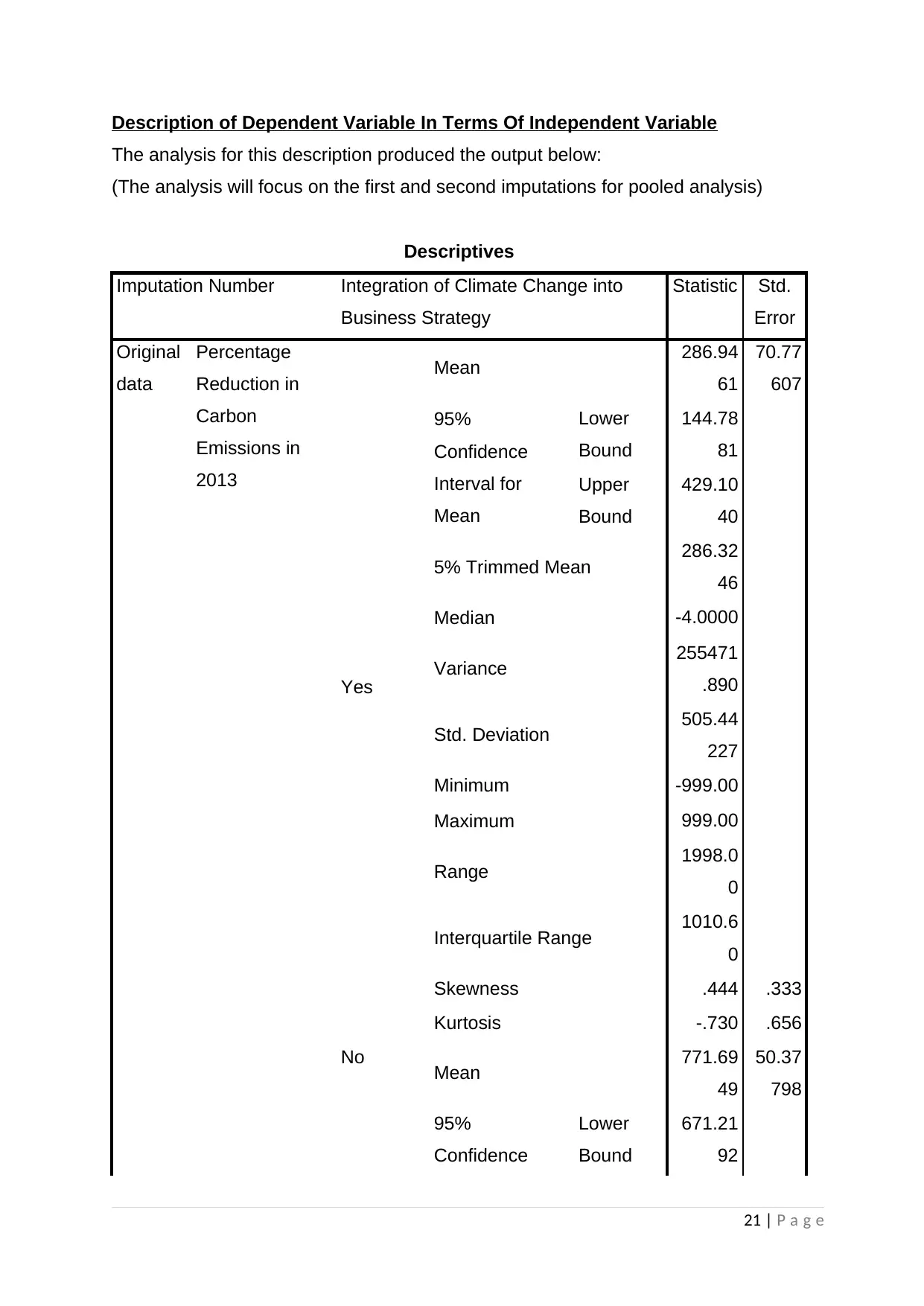

Description of Dependent Variable In Terms Of Independent Variable

The analysis for this description produced the output below:

(The analysis will focus on the first and second imputations for pooled analysis)

Descriptives

Imputation Number Integration of Climate Change into

Business Strategy

Statistic Std.

Error

Original

data

Percentage

Reduction in

Carbon

Emissions in

2013

Yes

Mean 286.94

61

70.77

607

95%

Confidence

Interval for

Mean

Lower

Bound

144.78

81

Upper

Bound

429.10

40

5% Trimmed Mean 286.32

46

Median -4.0000

Variance 255471

.890

Std. Deviation 505.44

227

Minimum -999.00

Maximum 999.00

Range 1998.0

0

Interquartile Range 1010.6

0

Skewness .444 .333

Kurtosis -.730 .656

No Mean 771.69

49

50.37

798

95%

Confidence

Lower

Bound

671.21

92

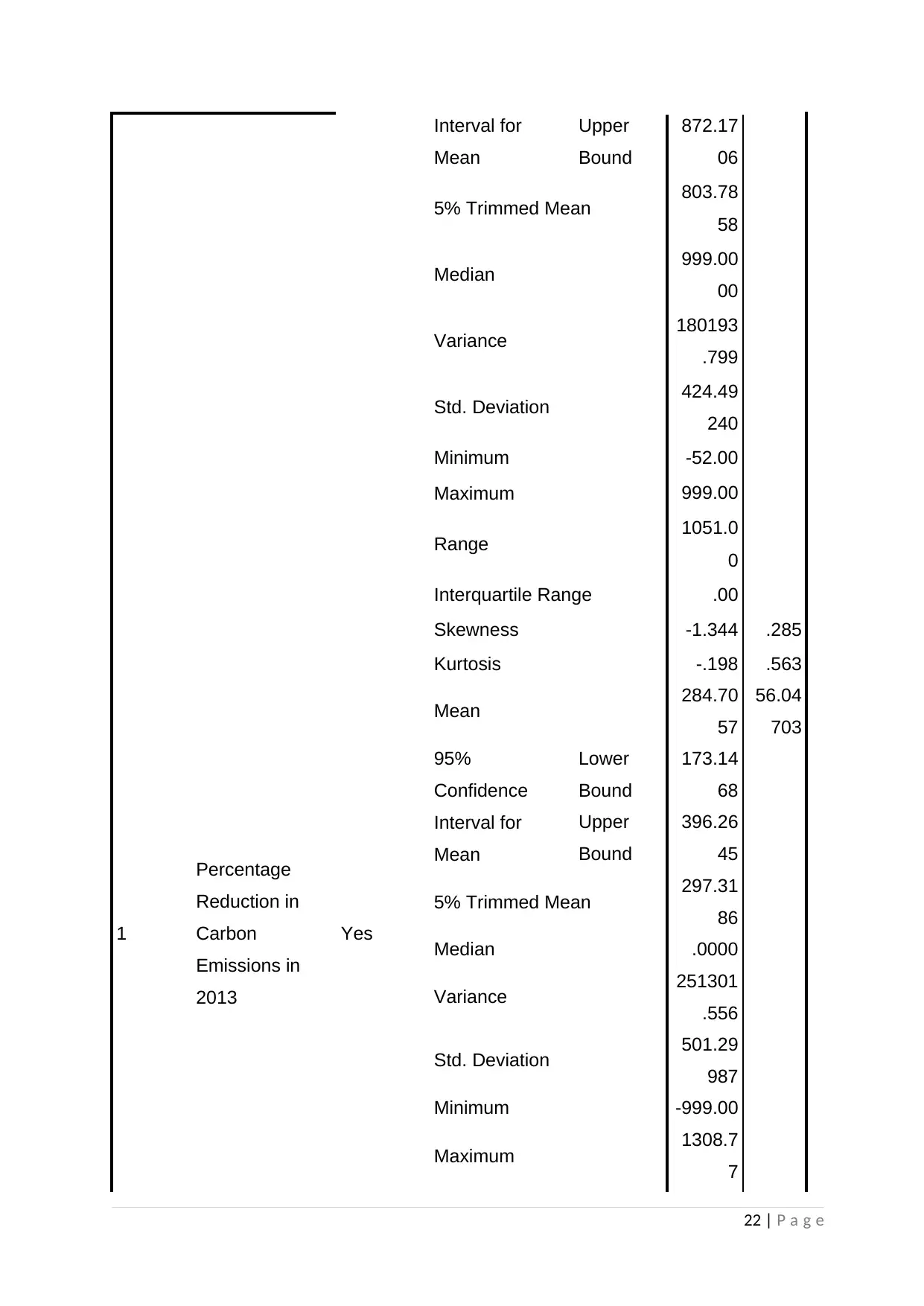

21 | P a g e

The analysis for this description produced the output below:

(The analysis will focus on the first and second imputations for pooled analysis)

Descriptives

Imputation Number Integration of Climate Change into

Business Strategy

Statistic Std.

Error

Original

data

Percentage

Reduction in

Carbon

Emissions in

2013

Yes

Mean 286.94

61

70.77

607

95%

Confidence

Interval for

Mean

Lower

Bound

144.78

81

Upper

Bound

429.10

40

5% Trimmed Mean 286.32

46

Median -4.0000

Variance 255471

.890

Std. Deviation 505.44

227

Minimum -999.00

Maximum 999.00

Range 1998.0

0

Interquartile Range 1010.6

0

Skewness .444 .333

Kurtosis -.730 .656

No Mean 771.69

49

50.37

798

95%

Confidence

Lower

Bound

671.21

92

21 | P a g e

Interval for

Mean

Upper

Bound

872.17

06

5% Trimmed Mean 803.78

58

Median 999.00

00

Variance 180193

.799

Std. Deviation 424.49

240

Minimum -52.00

Maximum 999.00

Range 1051.0

0

Interquartile Range .00

Skewness -1.344 .285

Kurtosis -.198 .563

1

Percentage

Reduction in

Carbon

Emissions in

2013

Yes

Mean 284.70

57

56.04

703

95%

Confidence

Interval for

Mean

Lower

Bound

173.14

68

Upper

Bound

396.26

45

5% Trimmed Mean 297.31

86

Median .0000

Variance 251301

.556

Std. Deviation 501.29

987

Minimum -999.00

Maximum 1308.7

7

22 | P a g e

Mean

Upper

Bound

872.17

06

5% Trimmed Mean 803.78

58

Median 999.00

00

Variance 180193

.799

Std. Deviation 424.49

240

Minimum -52.00

Maximum 999.00

Range 1051.0

0

Interquartile Range .00

Skewness -1.344 .285

Kurtosis -.198 .563

1

Percentage

Reduction in

Carbon

Emissions in

2013

Yes

Mean 284.70

57

56.04

703

95%

Confidence

Interval for

Mean

Lower

Bound

173.14

68

Upper

Bound

396.26

45

5% Trimmed Mean 297.31

86

Median .0000

Variance 251301

.556

Std. Deviation 501.29

987

Minimum -999.00

Maximum 1308.7

7

22 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

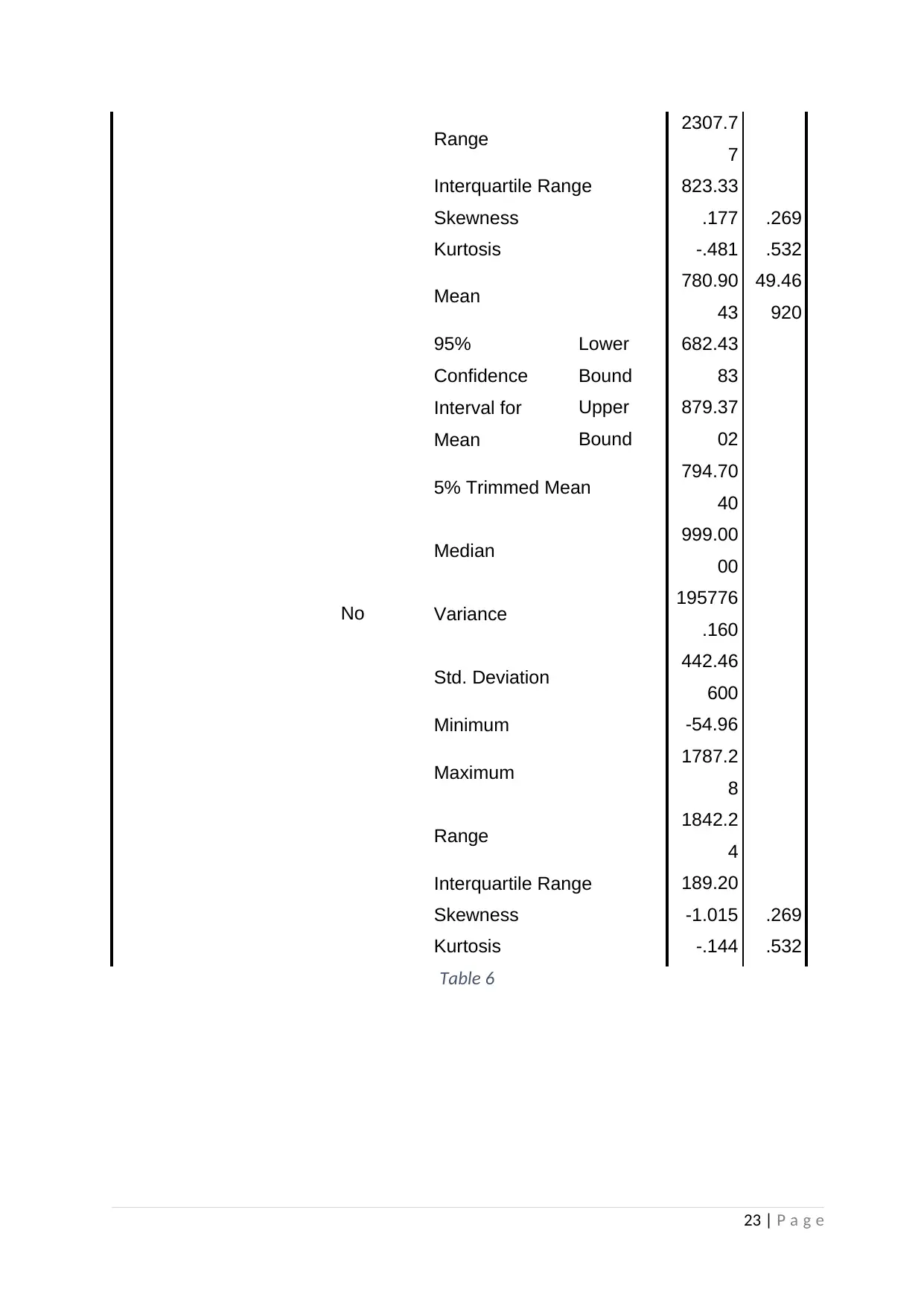

Range 2307.7

7

Interquartile Range 823.33

Skewness .177 .269

Kurtosis -.481 .532

No

Mean 780.90

43

49.46

920

95%

Confidence

Interval for

Mean

Lower

Bound

682.43

83

Upper

Bound

879.37

02

5% Trimmed Mean 794.70

40

Median 999.00

00

Variance 195776

.160

Std. Deviation 442.46

600

Minimum -54.96

Maximum 1787.2

8

Range 1842.2

4

Interquartile Range 189.20

Skewness -1.015 .269

Kurtosis -.144 .532

Table 6

23 | P a g e

7

Interquartile Range 823.33

Skewness .177 .269

Kurtosis -.481 .532

No

Mean 780.90

43

49.46

920

95%

Confidence

Interval for

Mean

Lower

Bound

682.43

83

Upper

Bound

879.37

02

5% Trimmed Mean 794.70

40

Median 999.00

00

Variance 195776

.160

Std. Deviation 442.46

600

Minimum -54.96

Maximum 1787.2

8

Range 1842.2

4

Interquartile Range 189.20

Skewness -1.015 .269

Kurtosis -.144 .532

Table 6

23 | P a g e

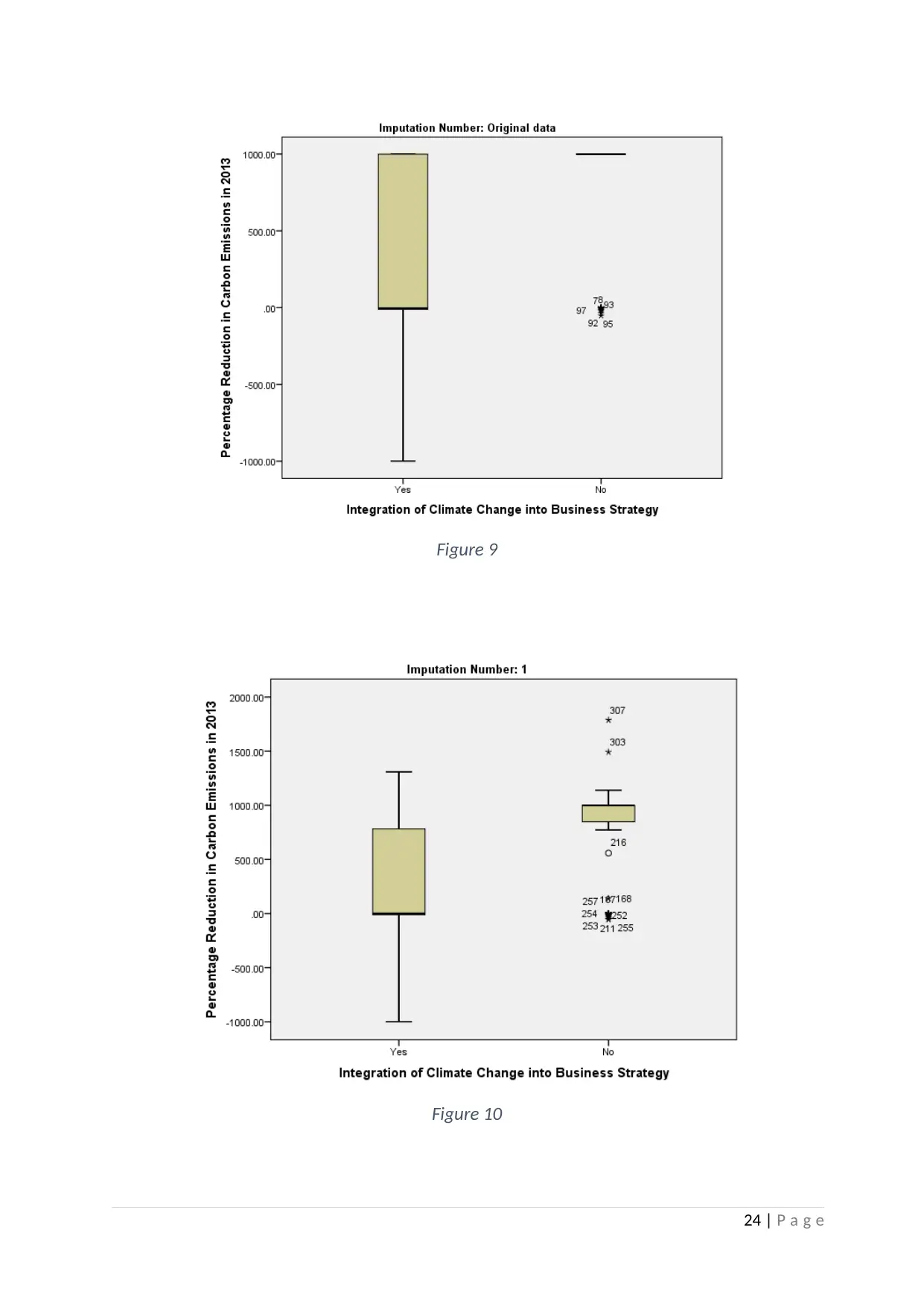

Figure 9

Figure 10

24 | P a g e

Figure 10

24 | P a g e

The data points identified outside of the right hand side boxplot in Figure 10 represent

the outlier values. To deal with the outliers, we conduct a transformation. It can either

be a log transformation or a square root transformation. The alternative option to

remove or drop the outliers would significantly reduce the observations, making the

sample data insufficient for analysis.

PROPOSED DATA ANALYSIS

Considering that the levels of measurements for the IV and DV are Nominal and Scale

respectively, the appropriate statistical test would be a One-Way ANOVA F-Test.

The Assumptions of the test are as follows:

1. The level of measurement of the dependent variable is assumed to be at the

ratio or interval level.

2. The independent variable is assumed to have two or more independent

categories or groups.

3. The observations are assumed to be independent of each other.

4. Significant outliers are assumed to be absent in the sample data.

5. For each category of the independent variable, the dependent variable is

assumed to be normally distributed.

6. The variances are assumed to be homogenous in nature.

The only assumption that the sample data does not satisfy is the assumption number

four. The sample data does contain significant outliers. Therefore, we can conclude

that after the transformation is carried out to deal with the outliers, the One-way

ANOVA F-Test can then be comfortably applied to the resultant dataset.

25 | P a g e

the outlier values. To deal with the outliers, we conduct a transformation. It can either

be a log transformation or a square root transformation. The alternative option to

remove or drop the outliers would significantly reduce the observations, making the

sample data insufficient for analysis.

PROPOSED DATA ANALYSIS

Considering that the levels of measurements for the IV and DV are Nominal and Scale

respectively, the appropriate statistical test would be a One-Way ANOVA F-Test.

The Assumptions of the test are as follows:

1. The level of measurement of the dependent variable is assumed to be at the

ratio or interval level.

2. The independent variable is assumed to have two or more independent

categories or groups.

3. The observations are assumed to be independent of each other.

4. Significant outliers are assumed to be absent in the sample data.

5. For each category of the independent variable, the dependent variable is

assumed to be normally distributed.

6. The variances are assumed to be homogenous in nature.

The only assumption that the sample data does not satisfy is the assumption number

four. The sample data does contain significant outliers. Therefore, we can conclude

that after the transformation is carried out to deal with the outliers, the One-way

ANOVA F-Test can then be comfortably applied to the resultant dataset.

25 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Accounting, B., 2018. Boundless Accounting. [Online]

Available at: https://courses.lumenlearning.com/boundless-accounting/chapter/overview-of-key-

elements-of-the-business/

[Accessed 10 08 2018].

Ecolife, 2011. Ecolife. [Online]

Available at: http://www.ecolife.com/define/carbon-emission.html

[Accessed 09 08 2018].

Freeman, R., 1984. Researchgate. [Online]

Available at: https://www.researchgate.net/figure/The-original-stakeholder-model-Freeman-

1984_fig1_259186795

[Accessed 09 08 2018].

Greenberg, R., 2014. Cerasis. [Online]

Available at: https://cerasis.com/2014/09/08/manufacturing-and-the-environment/

[Accessed 09 08 2018].

Hero, C., 2018. Course Hero. [Online]

Available at: https://www.coursehero.com/file/p18s4ec/Managerial-branch-of-Stakeholder-Theory-

Attempts-to-explain-when-corporate/

[Accessed 09 08 2018].

Morphy, T., 2008. Stakeholder Analysis, Project Management, templates and advice. [Online]

Available at: https://www.stakeholdermap.com/stakeholder-analysis/stakeholder-salience.html

[Accessed 09 08 2018].

Oba, P. G., 2014. Climate Change Adaptation in Africa. London: Taylor & Francis Group.

OECD, 2005. OECD. [Online]

Available at: https://stats.oecd.org/glossary/detail.asp?ID=6323

[Accessed 09 08 2018].

Sharma, R., 2010. Bright Hub Project Management. [Online]

Available at: https://www.brighthubpm.com/resource-management/81274-what-is-the-salience-

model/

[Accessed 09 08 2018].

Zawaideh, M., 2006. XING. [Online]

Available at: https://www.xing.com/communities/posts/the-normative-approach-explanation-of-

intrinsic-stakeholder-commitment-of-berman-wicks-kotha-jones-and-100417794

[Accessed 09 08 2018].

26 | P a g e

Accounting, B., 2018. Boundless Accounting. [Online]

Available at: https://courses.lumenlearning.com/boundless-accounting/chapter/overview-of-key-

elements-of-the-business/

[Accessed 10 08 2018].

Ecolife, 2011. Ecolife. [Online]

Available at: http://www.ecolife.com/define/carbon-emission.html

[Accessed 09 08 2018].

Freeman, R., 1984. Researchgate. [Online]

Available at: https://www.researchgate.net/figure/The-original-stakeholder-model-Freeman-

1984_fig1_259186795

[Accessed 09 08 2018].

Greenberg, R., 2014. Cerasis. [Online]

Available at: https://cerasis.com/2014/09/08/manufacturing-and-the-environment/

[Accessed 09 08 2018].

Hero, C., 2018. Course Hero. [Online]

Available at: https://www.coursehero.com/file/p18s4ec/Managerial-branch-of-Stakeholder-Theory-

Attempts-to-explain-when-corporate/

[Accessed 09 08 2018].

Morphy, T., 2008. Stakeholder Analysis, Project Management, templates and advice. [Online]

Available at: https://www.stakeholdermap.com/stakeholder-analysis/stakeholder-salience.html

[Accessed 09 08 2018].

Oba, P. G., 2014. Climate Change Adaptation in Africa. London: Taylor & Francis Group.

OECD, 2005. OECD. [Online]

Available at: https://stats.oecd.org/glossary/detail.asp?ID=6323

[Accessed 09 08 2018].

Sharma, R., 2010. Bright Hub Project Management. [Online]

Available at: https://www.brighthubpm.com/resource-management/81274-what-is-the-salience-

model/

[Accessed 09 08 2018].

Zawaideh, M., 2006. XING. [Online]

Available at: https://www.xing.com/communities/posts/the-normative-approach-explanation-of-

intrinsic-stakeholder-commitment-of-berman-wicks-kotha-jones-and-100417794

[Accessed 09 08 2018].

26 | P a g e

27 | P a g e

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.