Strategic Information Systems: Bell Studio Cash Management Analysis

VerifiedAdded on 2022/12/23

|17

|2724

|91

Case Study

AI Summary

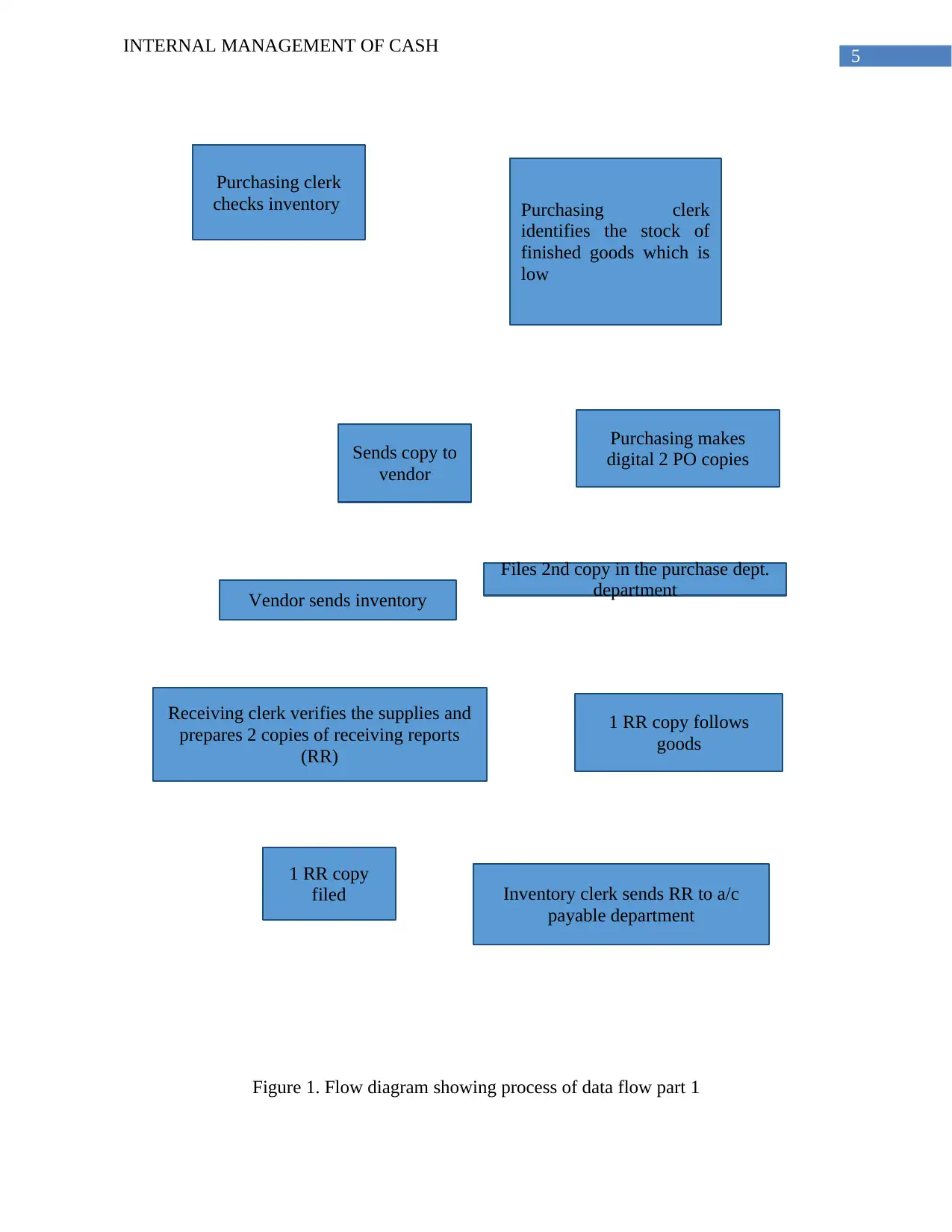

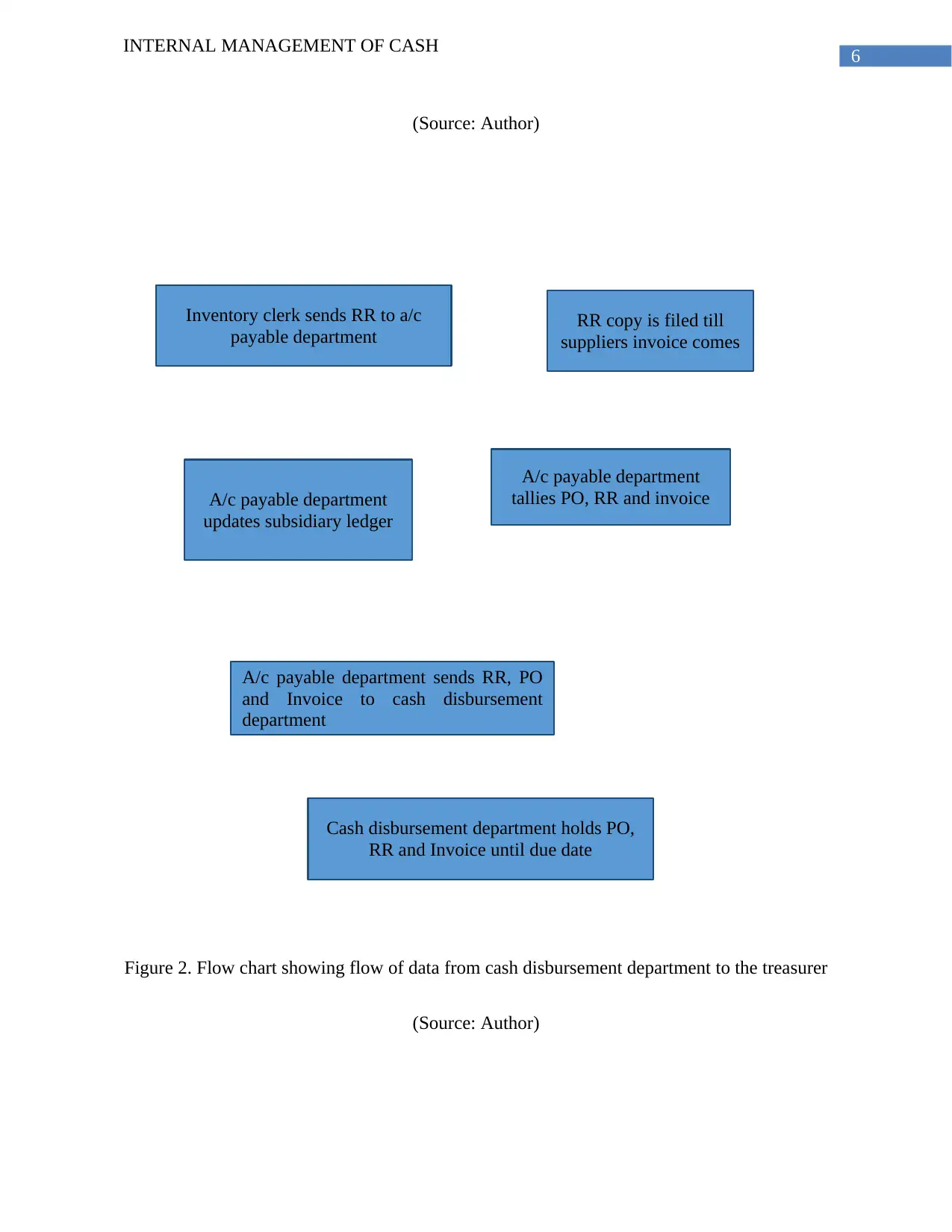

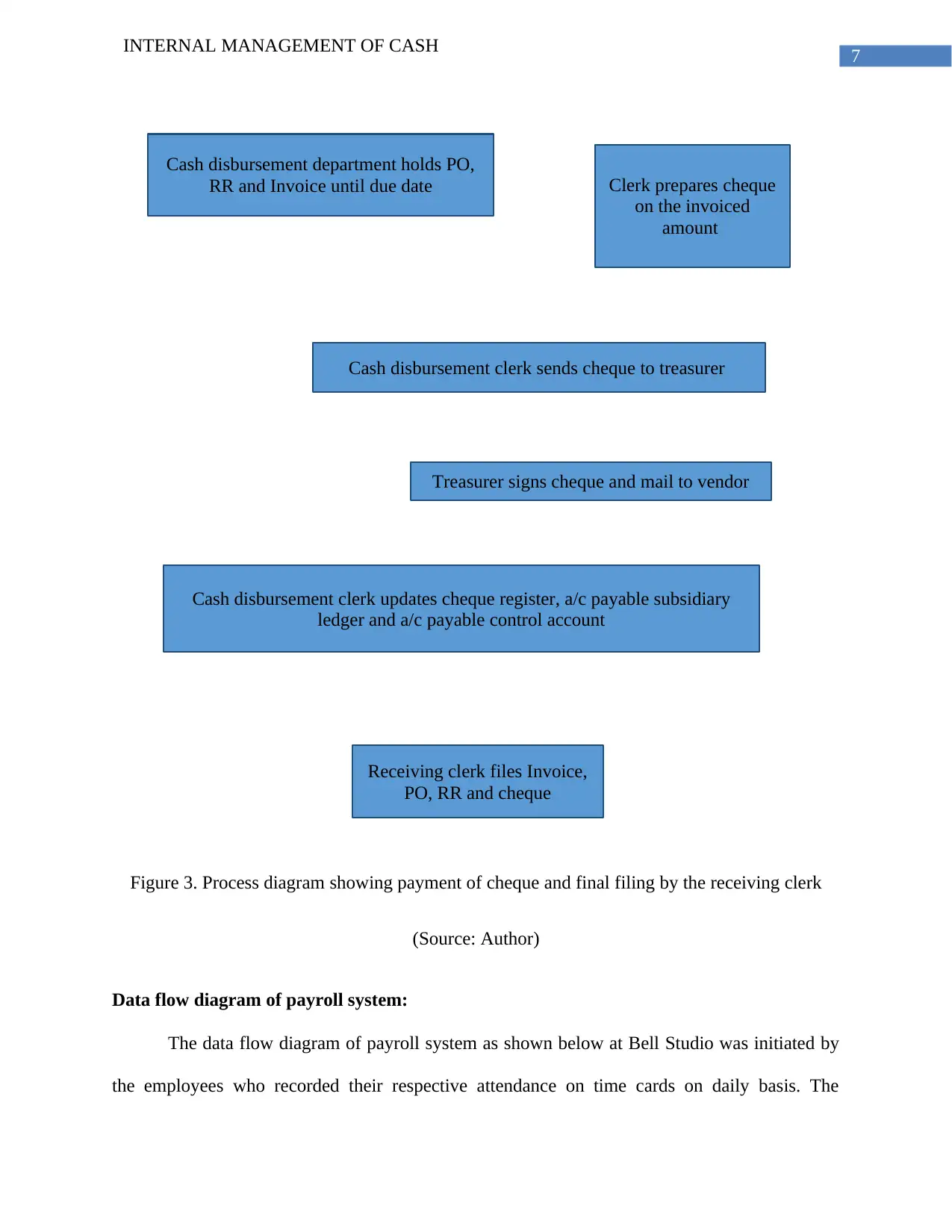

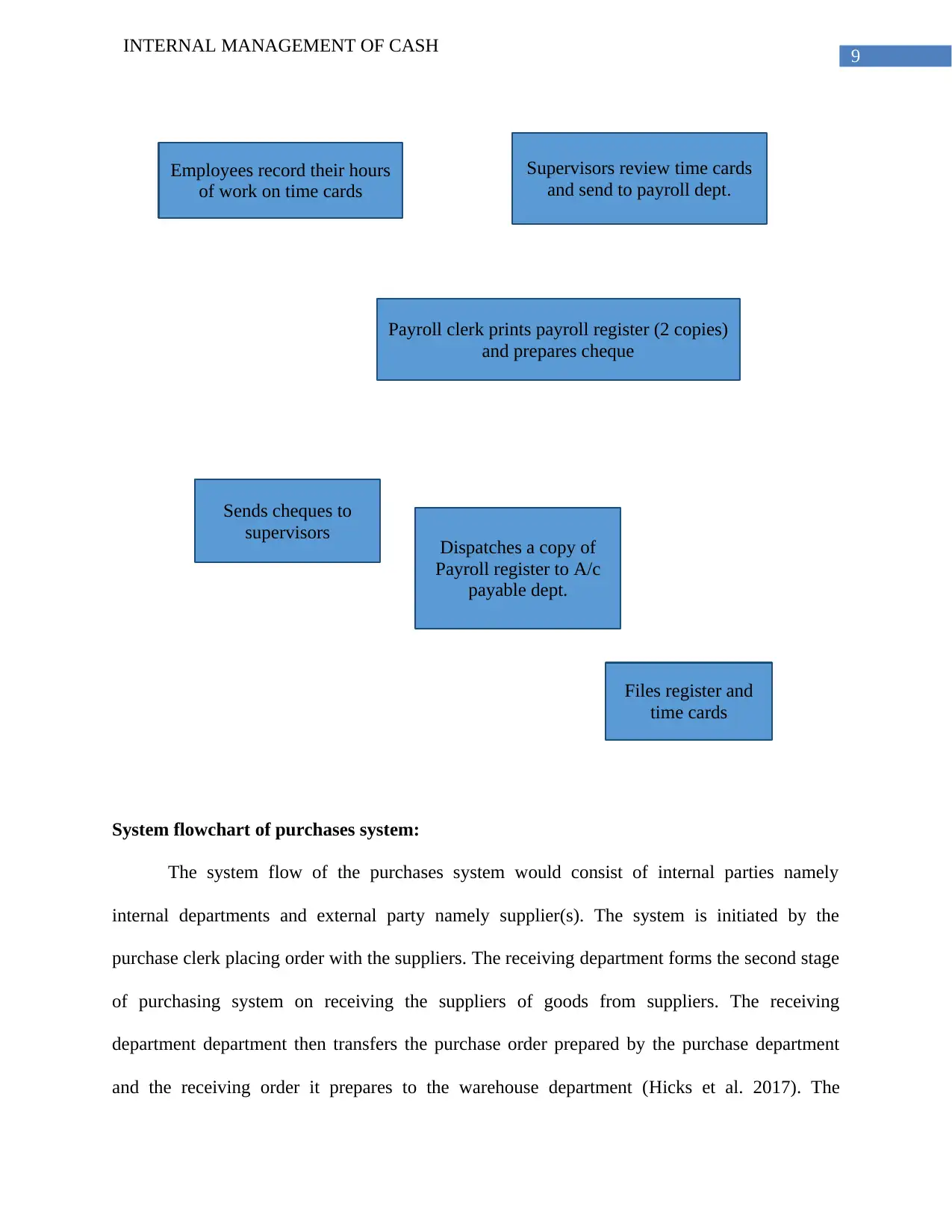

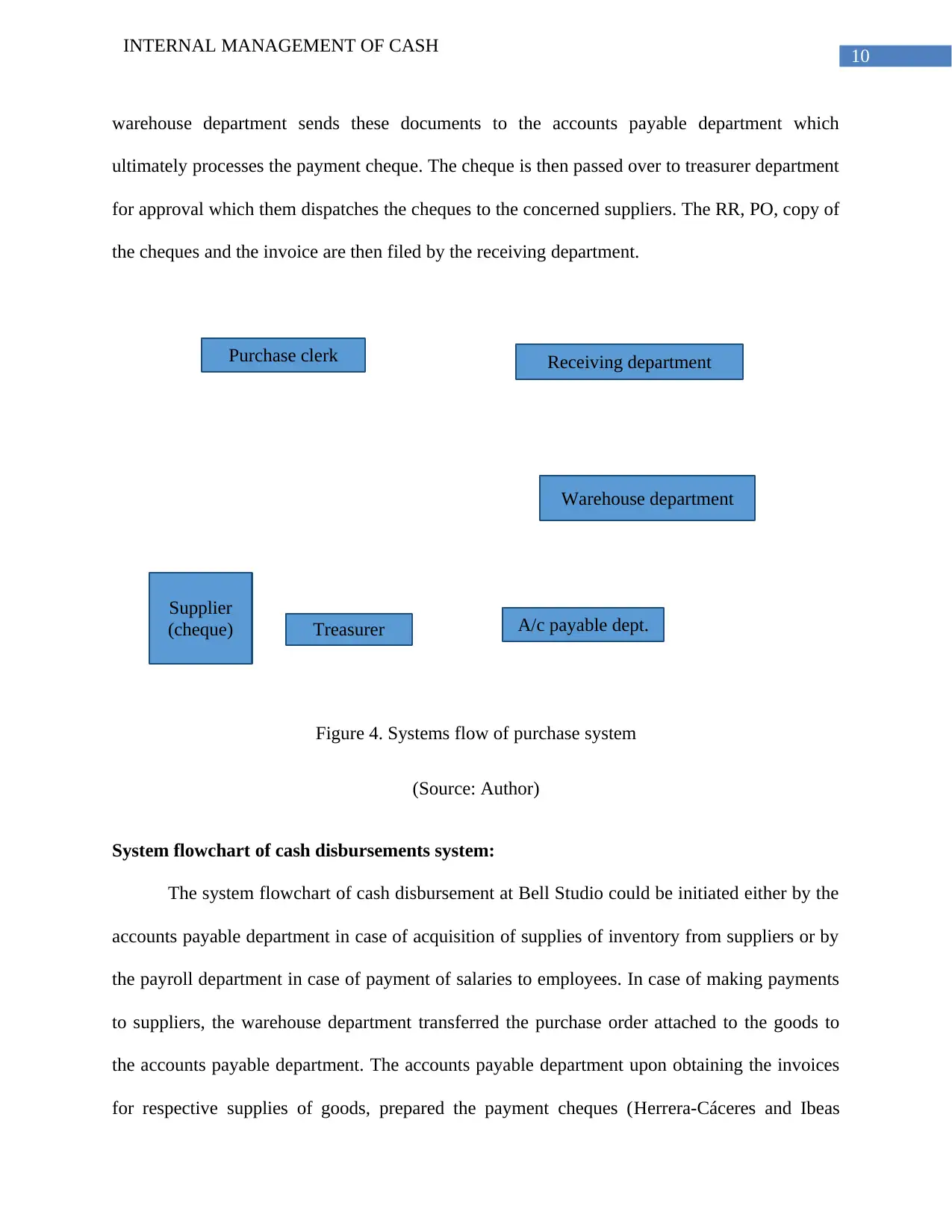

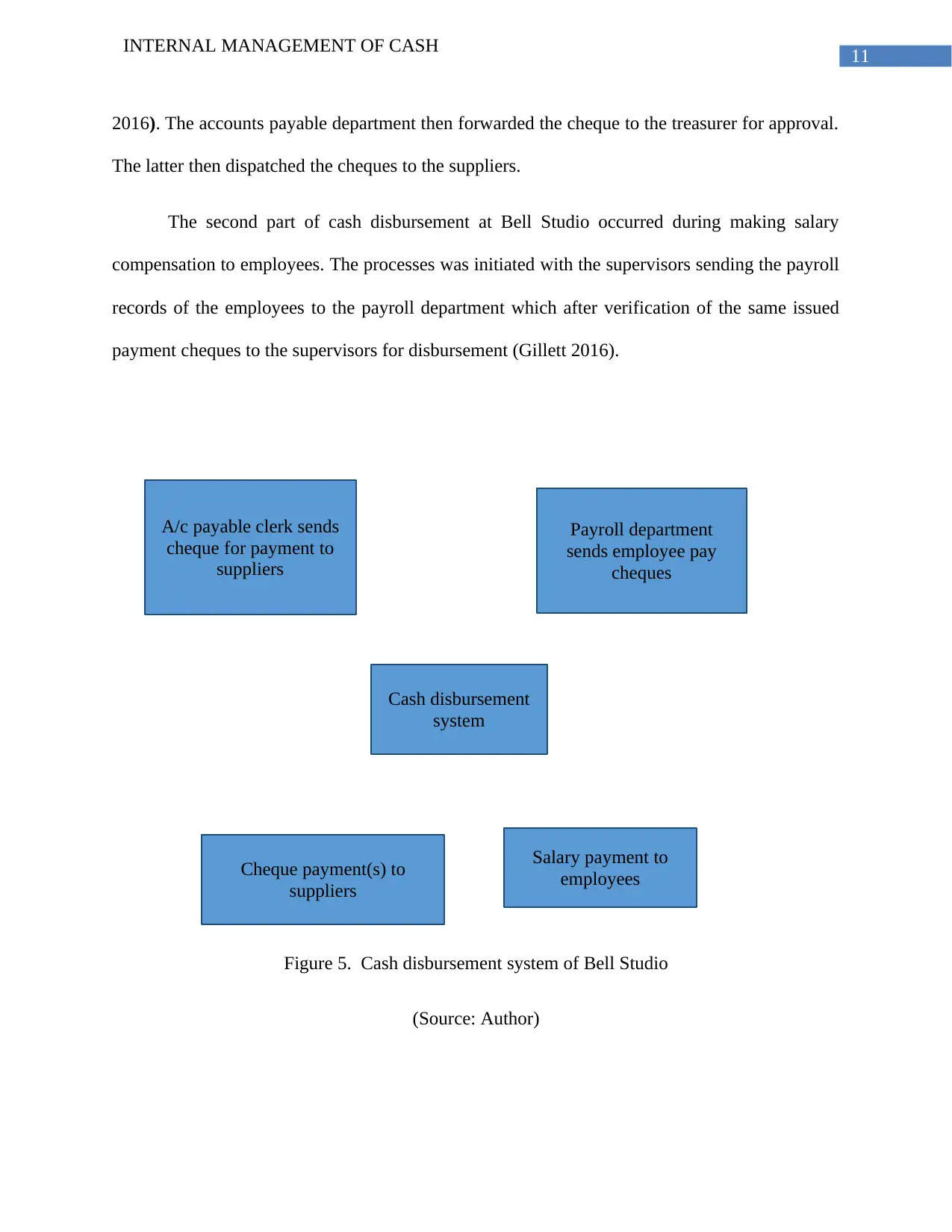

This case study evaluates the internal management of cash at Bell Studio, an Adelaide-based wholesaler, from a business analyst's perspective. The analysis encompasses the purchase, cash disbursement, and payroll systems, using data flow diagrams and system flowcharts to illustrate the processes. The study identifies internal control weaknesses, such as weak apex management control and unrealistic assumptions, and assesses the associated risks. The report examines the flow of data and documents within each system, highlighting the roles of various departments and personnel involved in cash management. The ultimate aim is to evaluate the effectiveness of the cash management process, the risks associated with the current system, and the internal controls in place to ensure financial accountability. The assignment offers an in-depth look at the financial processes of the business and offers insights into how the internal management of cash can be improved.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.