Module 6 Assessment: E-Surfboards Financial Report Analysis

VerifiedAdded on 2020/11/12

|9

|1816

|269

Homework Assignment

AI Summary

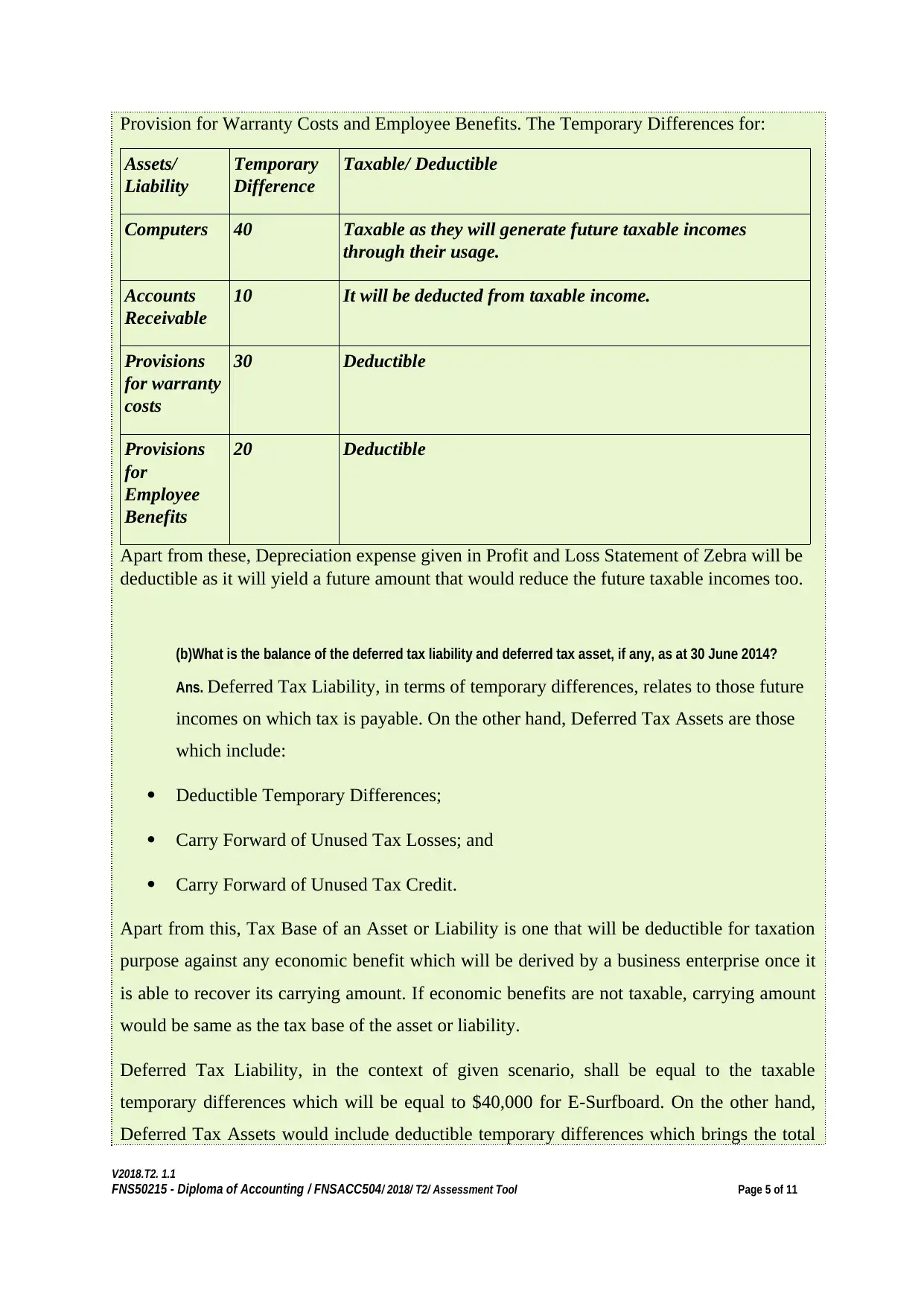

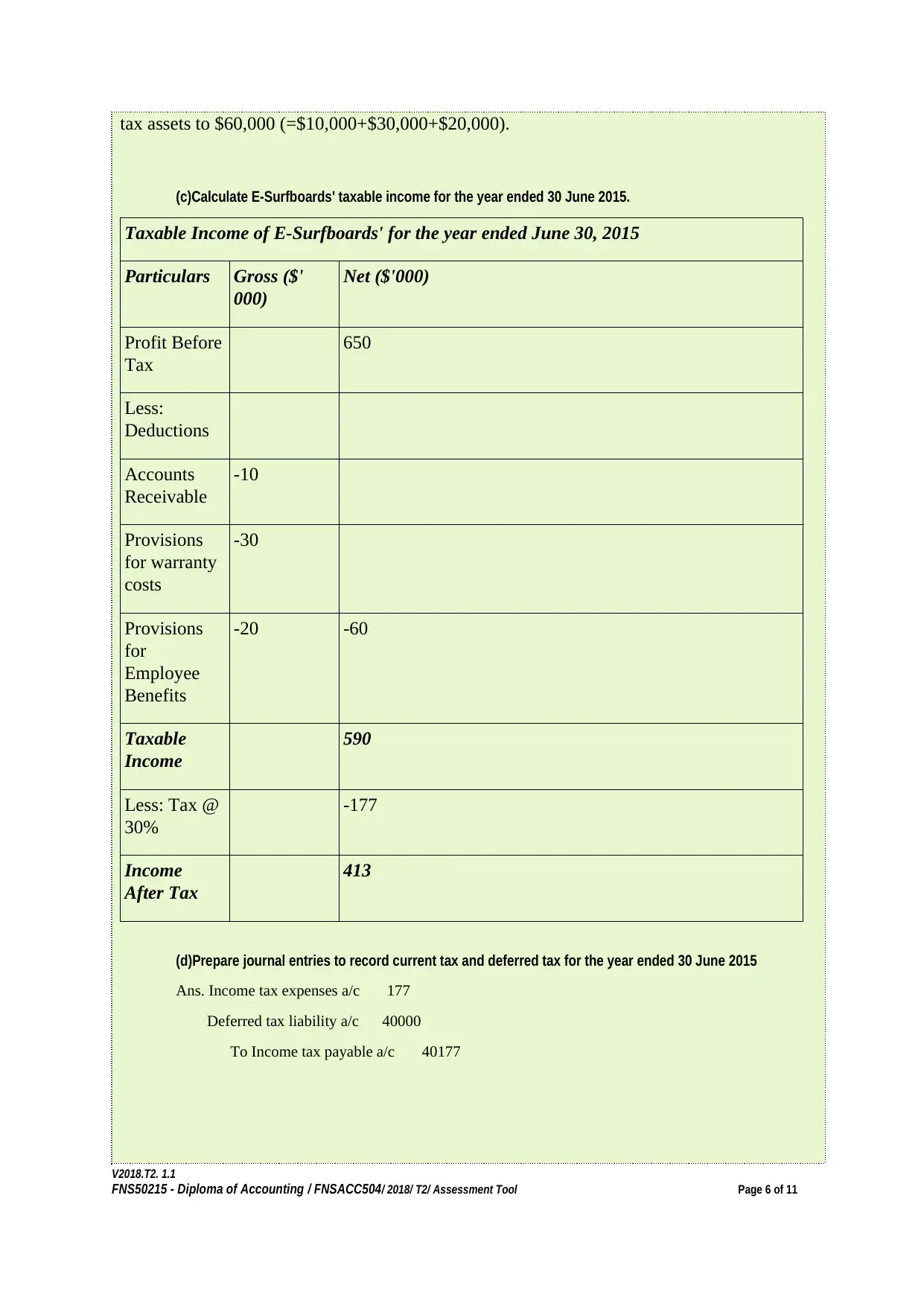

This assignment analyzes the financial report of E-Surfboards Limited, focusing on temporary differences, deferred tax liabilities and assets, and taxable income calculations. It provides a detailed breakdown of the company's financial position as of June 30, 2014, and the subsequent year ending June 30, 2015. The assignment calculates the amount of each temporary difference (taxable or deductible) and determines the balance of the deferred tax liability and asset. Furthermore, it calculates E-Surfboards' taxable income for the year and prepares the necessary journal entries to record current and deferred tax. The analysis covers aspects like depreciation, bad debts, warranty costs, and employee benefits, providing a comprehensive understanding of financial reporting and tax implications for corporate entities. The document is a student submission for the FNSACC504 module, demonstrating the application of accounting standards and financial reporting principles.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.