University Econometrics Assignment: Case Study Analysis and Modeling

VerifiedAdded on 2020/04/07

|17

|3311

|188

Homework Assignment

AI Summary

This econometrics assignment presents a comprehensive analysis of two case studies. The first case study focuses on predicting the Australian spot exchange rate using New Zealand money supply as a predictor variable. The analysis includes regression, hypothesis testing for significance of variables and model, and addressing issues like autocorrelation, heteroscedasticity, and non-normality of errors. The study also involves multiple regression with various economic indicators (money supply, GDP, interest rates) and forecasting the spot exchange rate. The second case study uses a market model to analyze Apple's share price, incorporating additive and event dummy variables to assess their significance. The assignment also covers the interpretation of coefficients, model diagnostics, and the impact of economic events on financial markets.

Running head: BASIC ECONOMETRICS

Basic Econometrics

Name of the Student

Name of the University

Author note

Basic Econometrics

Name of the Student

Name of the University

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1BASIC ECONOMETRICS

Table of Contents

Case Study One..........................................................................................................................2

Answer a.................................................................................................................................2

Answer b................................................................................................................................2

Answer c.................................................................................................................................3

Answer d................................................................................................................................3

Answer e.................................................................................................................................5

Answer f.................................................................................................................................6

Answer g................................................................................................................................7

Answer h................................................................................................................................7

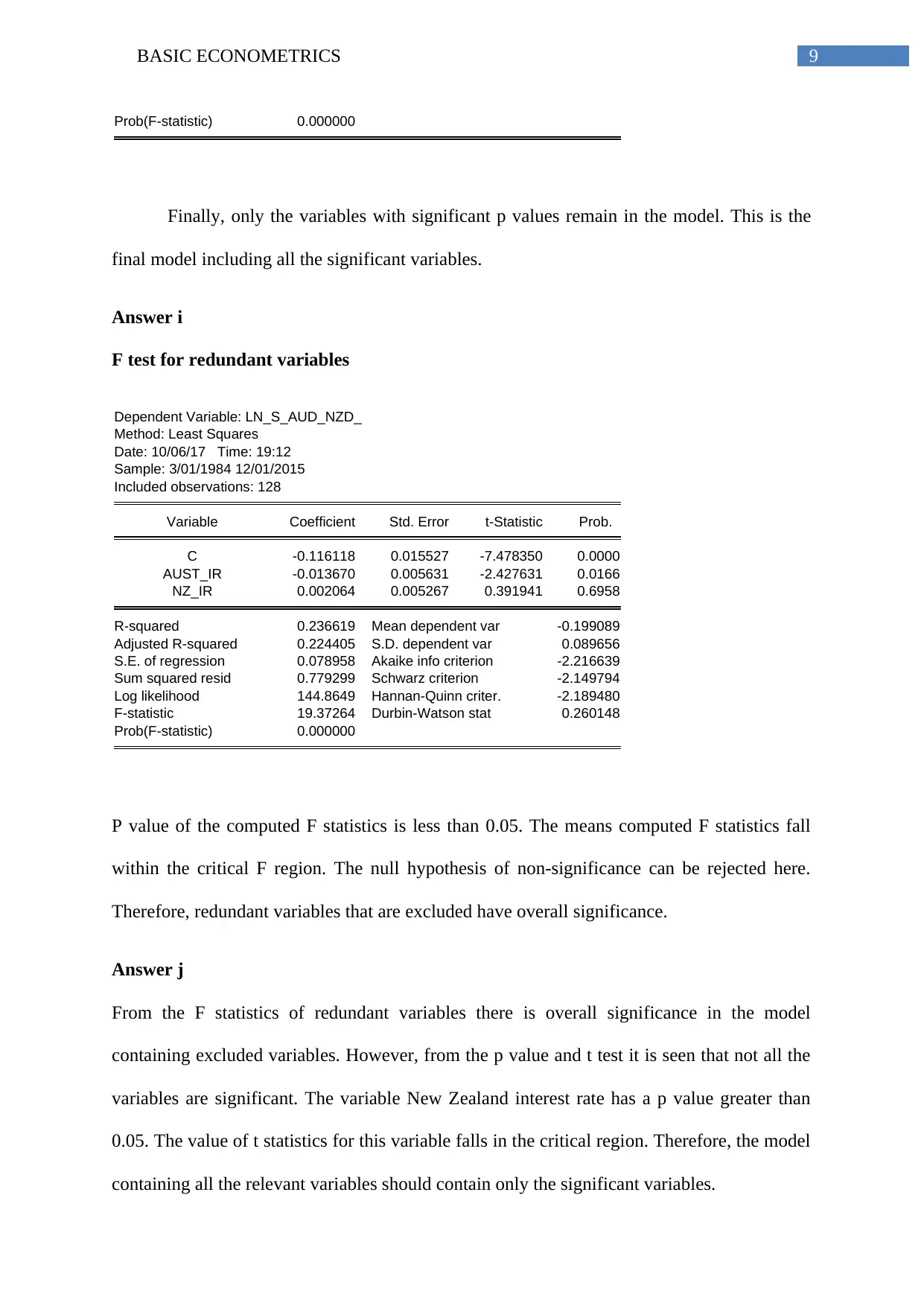

Answer i.................................................................................................................................9

Answer j.................................................................................................................................9

Answer k..............................................................................................................................10

Answer i...............................................................................................................................10

Case Study Two.......................................................................................................................11

Answer a...............................................................................................................................11

Answer b..............................................................................................................................12

Answer c...............................................................................................................................12

Answer d..............................................................................................................................14

Answer e..............................................................................................................................14

Bibliography.............................................................................................................................16

Table of Contents

Case Study One..........................................................................................................................2

Answer a.................................................................................................................................2

Answer b................................................................................................................................2

Answer c.................................................................................................................................3

Answer d................................................................................................................................3

Answer e.................................................................................................................................5

Answer f.................................................................................................................................6

Answer g................................................................................................................................7

Answer h................................................................................................................................7

Answer i.................................................................................................................................9

Answer j.................................................................................................................................9

Answer k..............................................................................................................................10

Answer i...............................................................................................................................10

Case Study Two.......................................................................................................................11

Answer a...............................................................................................................................11

Answer b..............................................................................................................................12

Answer c...............................................................................................................................12

Answer d..............................................................................................................................14

Answer e..............................................................................................................................14

Bibliography.............................................................................................................................16

2BASIC ECONOMETRICS

Case Study One

Answer a

Dependent Variable: LN_S_AUD_NZD_

Method: Least Squares

Date: 10/06/17 Time: 15:56

Sample: 3/01/1984 12/01/2015

Included observations: 128

Variable Coefficient Std. Error t-Statistic Prob.

C -0.958270 0.108660 -8.819010 0.0000

LN_NZ_MS_ 0.065974 0.009424 7.000309 0.0000

R-squared 0.280018 Mean dependent var -0.199089

Adjusted R-squared 0.274304 S.D. dependent var 0.089656

S.E. of regression 0.076376 Akaike info criterion -2.290794

Sum squared resid 0.734995 Schwarz criterion -2.246231

Log likelihood 148.6108 Hannan-Quinn criter. -2.272688

F-statistic 49.00433 Durbin-Watson stat 0.256500

Prob(F-statistic) 0.000000

The estimated model for predicting the exchange rate is

st =−0.958+ 0.06597 ln ¿

The model explains 28% variation in the exchange rate. The Predictor that is New Zealand

money supply is statistically significant as shown from the p value of the concerned variable.

Answer b

The p value of the intercept is 0.0000. This means the null hypothesis of non

significance of the model is rejected implying significance of the intercept term. Therefore,

the intercept is required for the model.

Case Study One

Answer a

Dependent Variable: LN_S_AUD_NZD_

Method: Least Squares

Date: 10/06/17 Time: 15:56

Sample: 3/01/1984 12/01/2015

Included observations: 128

Variable Coefficient Std. Error t-Statistic Prob.

C -0.958270 0.108660 -8.819010 0.0000

LN_NZ_MS_ 0.065974 0.009424 7.000309 0.0000

R-squared 0.280018 Mean dependent var -0.199089

Adjusted R-squared 0.274304 S.D. dependent var 0.089656

S.E. of regression 0.076376 Akaike info criterion -2.290794

Sum squared resid 0.734995 Schwarz criterion -2.246231

Log likelihood 148.6108 Hannan-Quinn criter. -2.272688

F-statistic 49.00433 Durbin-Watson stat 0.256500

Prob(F-statistic) 0.000000

The estimated model for predicting the exchange rate is

st =−0.958+ 0.06597 ln ¿

The model explains 28% variation in the exchange rate. The Predictor that is New Zealand

money supply is statistically significant as shown from the p value of the concerned variable.

Answer b

The p value of the intercept is 0.0000. This means the null hypothesis of non

significance of the model is rejected implying significance of the intercept term. Therefore,

the intercept is required for the model.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3BASIC ECONOMETRICS

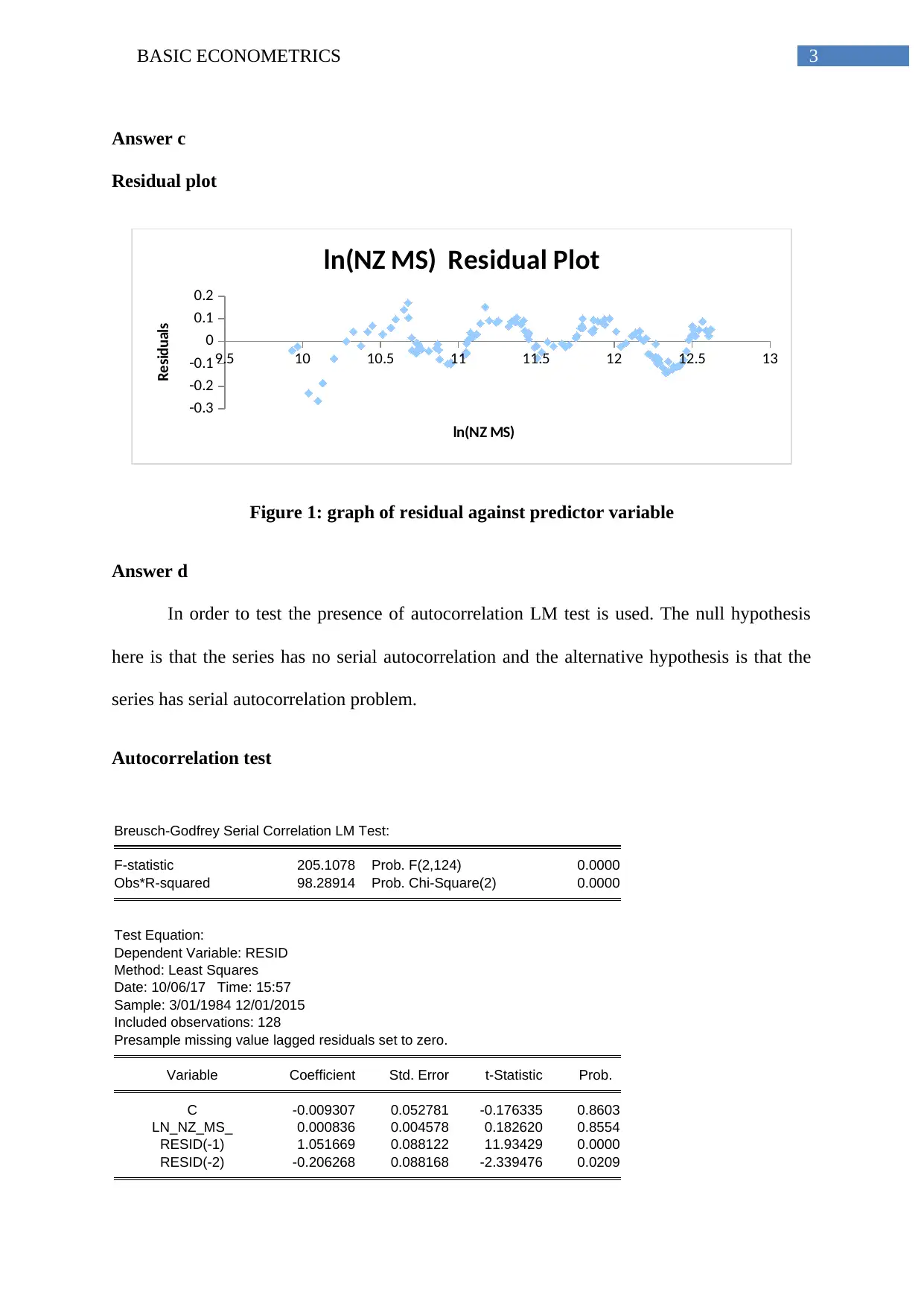

Answer c

Residual plot

9.5 10 10.5 11 11.5 12 12.5 13

-0.3

-0.2

-0.1

0

0.1

0.2

ln(NZ MS) Residual Plot

ln(NZ MS)

Residuals

Figure 1: graph of residual against predictor variable

Answer d

In order to test the presence of autocorrelation LM test is used. The null hypothesis

here is that the series has no serial autocorrelation and the alternative hypothesis is that the

series has serial autocorrelation problem.

Autocorrelation test

Breusch-Godfrey Serial Correlation LM Test:

F-statistic 205.1078 Prob. F(2,124) 0.0000

Obs*R-squared 98.28914 Prob. Chi-Square(2) 0.0000

Test Equation:

Dependent Variable: RESID

Method: Least Squares

Date: 10/06/17 Time: 15:57

Sample: 3/01/1984 12/01/2015

Included observations: 128

Presample missing value lagged residuals set to zero.

Variable Coefficient Std. Error t-Statistic Prob.

C -0.009307 0.052781 -0.176335 0.8603

LN_NZ_MS_ 0.000836 0.004578 0.182620 0.8554

RESID(-1) 1.051669 0.088122 11.93429 0.0000

RESID(-2) -0.206268 0.088168 -2.339476 0.0209

Answer c

Residual plot

9.5 10 10.5 11 11.5 12 12.5 13

-0.3

-0.2

-0.1

0

0.1

0.2

ln(NZ MS) Residual Plot

ln(NZ MS)

Residuals

Figure 1: graph of residual against predictor variable

Answer d

In order to test the presence of autocorrelation LM test is used. The null hypothesis

here is that the series has no serial autocorrelation and the alternative hypothesis is that the

series has serial autocorrelation problem.

Autocorrelation test

Breusch-Godfrey Serial Correlation LM Test:

F-statistic 205.1078 Prob. F(2,124) 0.0000

Obs*R-squared 98.28914 Prob. Chi-Square(2) 0.0000

Test Equation:

Dependent Variable: RESID

Method: Least Squares

Date: 10/06/17 Time: 15:57

Sample: 3/01/1984 12/01/2015

Included observations: 128

Presample missing value lagged residuals set to zero.

Variable Coefficient Std. Error t-Statistic Prob.

C -0.009307 0.052781 -0.176335 0.8603

LN_NZ_MS_ 0.000836 0.004578 0.182620 0.8554

RESID(-1) 1.051669 0.088122 11.93429 0.0000

RESID(-2) -0.206268 0.088168 -2.339476 0.0209

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4BASIC ECONOMETRICS

R-squared 0.767884 Mean dependent var -3.37E-16

Adjusted R-squared 0.762268 S.D. dependent var 0.076075

S.E. of regression 0.037092 Akaike info criterion -3.720062

Sum squared resid 0.170604 Schwarz criterion -3.630936

Log likelihood 242.0840 Hannan-Quinn criter. -3.683850

F-statistic 136.7385 Durbin-Watson stat 1.959557

Prob(F-statistic) 0.000000

The statistics used for LM test is chi square statistics. The probability estimate of chi

square statistics is 0.0000. This implies there is little evidence of accepting the null

hypothesis. Therefore, the null hypothesis of ‘no serial autocorrelation’ is rejected and there

is significant problem of autocorrelation.

The possible reason for serial autocorrelation is the relationship between money

supply and exchange rate of currencies. When money supply increases then income of a

nation expands. This affects the demand for import and hence, the exchange rate. Therefore,

there might be some common disturbance factor causing change in New Zealand money

supply and Spot exchange rate between Australia and New Zealand.

Correction of Autocorrelation

Breusch-Godfrey Serial Correlation LM Test:

F-statistic 0.316564 Prob. F(2,118) 0.7293

Obs*R-squared 0.667106 Prob. Chi-Square(2) 0.7164

Test Equation:

Dependent Variable: RESID

Method: Least Squares

Date: 10/06/17 Time: 16:19

Sample: 12/01/1984 12/01/2015

Included observations: 125

Presample missing value lagged residuals set to zero.

Variable Coefficient Std. Error t-Statistic Prob.

C 0.017671 0.065572 0.269494 0.7880

LN_NZ_MS_ -0.001235 0.005163 -0.239240 0.8113

LAGS 0.094069 0.143997 0.653271 0.5149

LAGS1 -0.069873 0.194327 -0.359565 0.7198

LAGS2 -0.005948 0.123890 -0.048011 0.9618

R-squared 0.767884 Mean dependent var -3.37E-16

Adjusted R-squared 0.762268 S.D. dependent var 0.076075

S.E. of regression 0.037092 Akaike info criterion -3.720062

Sum squared resid 0.170604 Schwarz criterion -3.630936

Log likelihood 242.0840 Hannan-Quinn criter. -3.683850

F-statistic 136.7385 Durbin-Watson stat 1.959557

Prob(F-statistic) 0.000000

The statistics used for LM test is chi square statistics. The probability estimate of chi

square statistics is 0.0000. This implies there is little evidence of accepting the null

hypothesis. Therefore, the null hypothesis of ‘no serial autocorrelation’ is rejected and there

is significant problem of autocorrelation.

The possible reason for serial autocorrelation is the relationship between money

supply and exchange rate of currencies. When money supply increases then income of a

nation expands. This affects the demand for import and hence, the exchange rate. Therefore,

there might be some common disturbance factor causing change in New Zealand money

supply and Spot exchange rate between Australia and New Zealand.

Correction of Autocorrelation

Breusch-Godfrey Serial Correlation LM Test:

F-statistic 0.316564 Prob. F(2,118) 0.7293

Obs*R-squared 0.667106 Prob. Chi-Square(2) 0.7164

Test Equation:

Dependent Variable: RESID

Method: Least Squares

Date: 10/06/17 Time: 16:19

Sample: 12/01/1984 12/01/2015

Included observations: 125

Presample missing value lagged residuals set to zero.

Variable Coefficient Std. Error t-Statistic Prob.

C 0.017671 0.065572 0.269494 0.7880

LN_NZ_MS_ -0.001235 0.005163 -0.239240 0.8113

LAGS 0.094069 0.143997 0.653271 0.5149

LAGS1 -0.069873 0.194327 -0.359565 0.7198

LAGS2 -0.005948 0.123890 -0.048011 0.9618

5BASIC ECONOMETRICS

RESID(-1) -0.133398 0.171783 -0.776549 0.4390

RESID(-2) -0.043803 0.163434 -0.268013 0.7892

R-squared 0.005337 Mean dependent var -1.60E-17

Adjusted R-squared -0.045239 S.D. dependent var 0.031082

S.E. of regression 0.031777 Akaike info criterion -4.005764

Sum squared resid 0.119155 Schwarz criterion -3.847378

Log likelihood 257.3602 Hannan-Quinn criter. -3.941420

F-statistic 0.105521 Durbin-Watson stat 1.968802

Prob(F-statistic) 0.995657

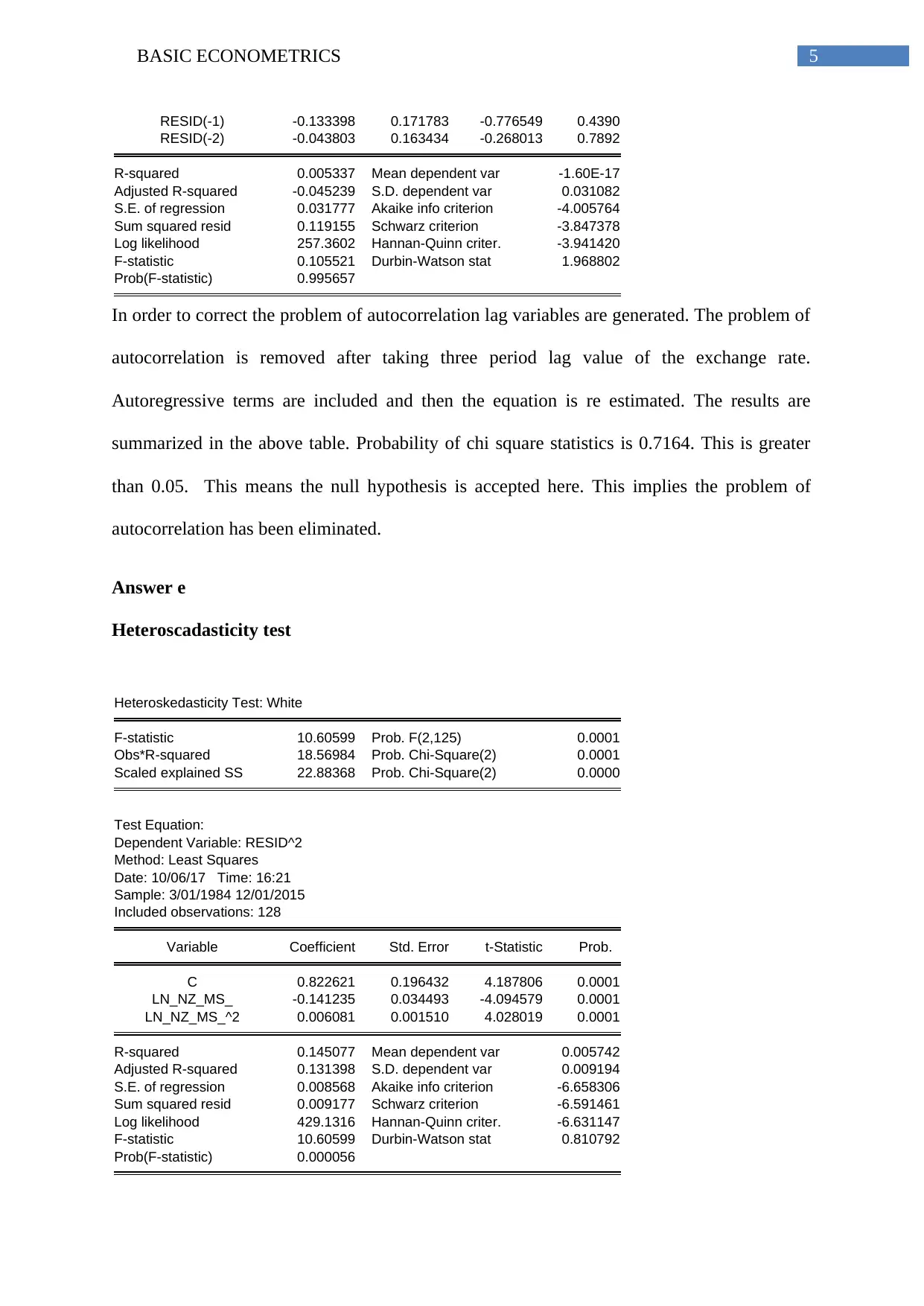

In order to correct the problem of autocorrelation lag variables are generated. The problem of

autocorrelation is removed after taking three period lag value of the exchange rate.

Autoregressive terms are included and then the equation is re estimated. The results are

summarized in the above table. Probability of chi square statistics is 0.7164. This is greater

than 0.05. This means the null hypothesis is accepted here. This implies the problem of

autocorrelation has been eliminated.

Answer e

Heteroscadasticity test

Heteroskedasticity Test: White

F-statistic 10.60599 Prob. F(2,125) 0.0001

Obs*R-squared 18.56984 Prob. Chi-Square(2) 0.0001

Scaled explained SS 22.88368 Prob. Chi-Square(2) 0.0000

Test Equation:

Dependent Variable: RESID^2

Method: Least Squares

Date: 10/06/17 Time: 16:21

Sample: 3/01/1984 12/01/2015

Included observations: 128

Variable Coefficient Std. Error t-Statistic Prob.

C 0.822621 0.196432 4.187806 0.0001

LN_NZ_MS_ -0.141235 0.034493 -4.094579 0.0001

LN_NZ_MS_^2 0.006081 0.001510 4.028019 0.0001

R-squared 0.145077 Mean dependent var 0.005742

Adjusted R-squared 0.131398 S.D. dependent var 0.009194

S.E. of regression 0.008568 Akaike info criterion -6.658306

Sum squared resid 0.009177 Schwarz criterion -6.591461

Log likelihood 429.1316 Hannan-Quinn criter. -6.631147

F-statistic 10.60599 Durbin-Watson stat 0.810792

Prob(F-statistic) 0.000056

RESID(-1) -0.133398 0.171783 -0.776549 0.4390

RESID(-2) -0.043803 0.163434 -0.268013 0.7892

R-squared 0.005337 Mean dependent var -1.60E-17

Adjusted R-squared -0.045239 S.D. dependent var 0.031082

S.E. of regression 0.031777 Akaike info criterion -4.005764

Sum squared resid 0.119155 Schwarz criterion -3.847378

Log likelihood 257.3602 Hannan-Quinn criter. -3.941420

F-statistic 0.105521 Durbin-Watson stat 1.968802

Prob(F-statistic) 0.995657

In order to correct the problem of autocorrelation lag variables are generated. The problem of

autocorrelation is removed after taking three period lag value of the exchange rate.

Autoregressive terms are included and then the equation is re estimated. The results are

summarized in the above table. Probability of chi square statistics is 0.7164. This is greater

than 0.05. This means the null hypothesis is accepted here. This implies the problem of

autocorrelation has been eliminated.

Answer e

Heteroscadasticity test

Heteroskedasticity Test: White

F-statistic 10.60599 Prob. F(2,125) 0.0001

Obs*R-squared 18.56984 Prob. Chi-Square(2) 0.0001

Scaled explained SS 22.88368 Prob. Chi-Square(2) 0.0000

Test Equation:

Dependent Variable: RESID^2

Method: Least Squares

Date: 10/06/17 Time: 16:21

Sample: 3/01/1984 12/01/2015

Included observations: 128

Variable Coefficient Std. Error t-Statistic Prob.

C 0.822621 0.196432 4.187806 0.0001

LN_NZ_MS_ -0.141235 0.034493 -4.094579 0.0001

LN_NZ_MS_^2 0.006081 0.001510 4.028019 0.0001

R-squared 0.145077 Mean dependent var 0.005742

Adjusted R-squared 0.131398 S.D. dependent var 0.009194

S.E. of regression 0.008568 Akaike info criterion -6.658306

Sum squared resid 0.009177 Schwarz criterion -6.591461

Log likelihood 429.1316 Hannan-Quinn criter. -6.631147

F-statistic 10.60599 Durbin-Watson stat 0.810792

Prob(F-statistic) 0.000056

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6BASIC ECONOMETRICS

There are a number of tests to measure the presence of heteroscedasticity. Here, white

test is used to test heteroscadasticity. The null hypothesis is that there is no problem of

heteroscadasticity that is the errors are homoscadastic. The alternative hypothesis is that the

errors are heteroscadastic. From the result of white test it is seen that probability of chi square

statistics is 0.0001. this is less than the significance level of 0.05. Therefore, the null

hypothesis is rejected at the 5% level of significance and accepts the alternative hypot5heisis

which suggests the presence of heteroscadasticity.

To get a improved t statistics the problem of heteroscadasticity needs to be eliminated.

This can be done either by taking logarithm from of the estimated variable or using weight

least square estimate.

Answer f

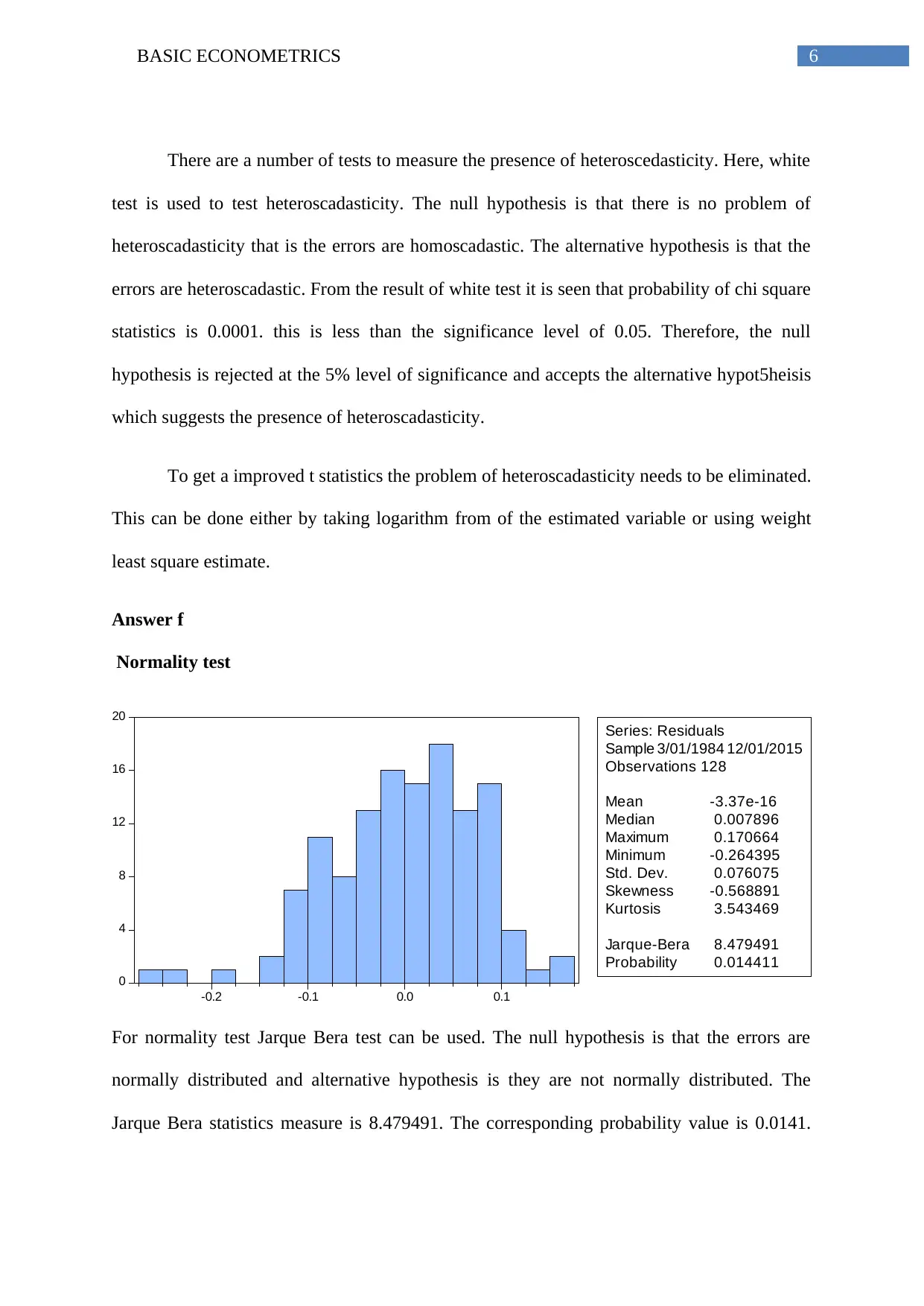

Normality test

0

4

8

12

16

20

-0.2 -0.1 0.0 0.1

Series: Residuals

Sample 3/01/1984 12/01/2015

Observations 128

Mean -3.37e-16

Median 0.007896

Maximum 0.170664

Minimum -0.264395

Std. Dev. 0.076075

Skewness -0.568891

Kurtosis 3.543469

Jarque-Bera 8.479491

Probability 0.014411

For normality test Jarque Bera test can be used. The null hypothesis is that the errors are

normally distributed and alternative hypothesis is they are not normally distributed. The

Jarque Bera statistics measure is 8.479491. The corresponding probability value is 0.0141.

There are a number of tests to measure the presence of heteroscedasticity. Here, white

test is used to test heteroscadasticity. The null hypothesis is that there is no problem of

heteroscadasticity that is the errors are homoscadastic. The alternative hypothesis is that the

errors are heteroscadastic. From the result of white test it is seen that probability of chi square

statistics is 0.0001. this is less than the significance level of 0.05. Therefore, the null

hypothesis is rejected at the 5% level of significance and accepts the alternative hypot5heisis

which suggests the presence of heteroscadasticity.

To get a improved t statistics the problem of heteroscadasticity needs to be eliminated.

This can be done either by taking logarithm from of the estimated variable or using weight

least square estimate.

Answer f

Normality test

0

4

8

12

16

20

-0.2 -0.1 0.0 0.1

Series: Residuals

Sample 3/01/1984 12/01/2015

Observations 128

Mean -3.37e-16

Median 0.007896

Maximum 0.170664

Minimum -0.264395

Std. Dev. 0.076075

Skewness -0.568891

Kurtosis 3.543469

Jarque-Bera 8.479491

Probability 0.014411

For normality test Jarque Bera test can be used. The null hypothesis is that the errors are

normally distributed and alternative hypothesis is they are not normally distributed. The

Jarque Bera statistics measure is 8.479491. The corresponding probability value is 0.0141.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7BASIC ECONOMETRICS

The p value is less than 0.05. Therefore, the null hypothesis of normal distribution is rejected.

Therefore, errors are not normally distributed.

From the three test performed above it is clear that the model suffers from the

problem of serial autocorrelation. There is problem heteroscadasticity. Moreover the errors

are not normally distributed. All these indicate the estimated model and test statistics are not

reliable at all. The model will be statistically significant only after suitable correction taken

for the model.

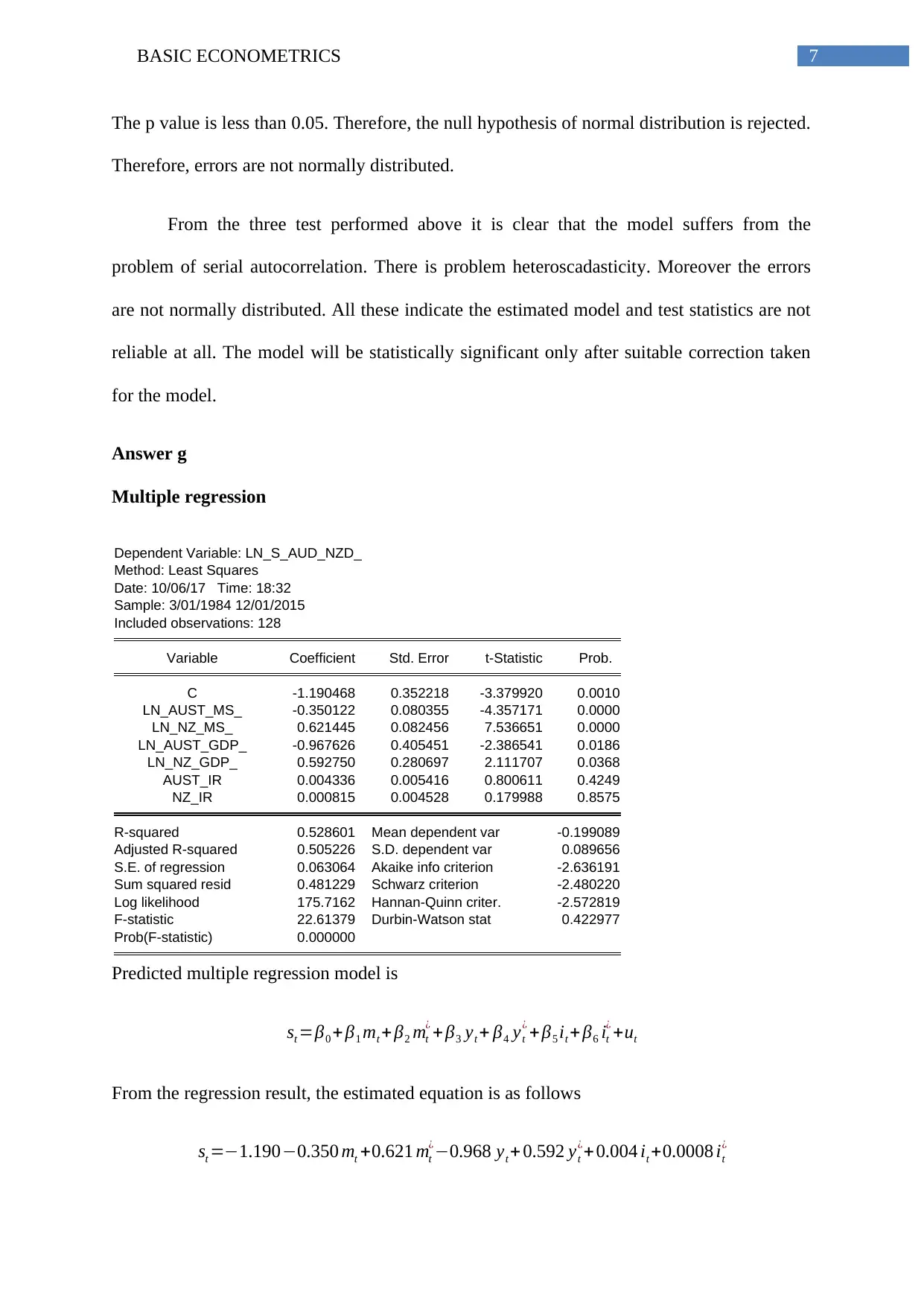

Answer g

Multiple regression

Dependent Variable: LN_S_AUD_NZD_

Method: Least Squares

Date: 10/06/17 Time: 18:32

Sample: 3/01/1984 12/01/2015

Included observations: 128

Variable Coefficient Std. Error t-Statistic Prob.

C -1.190468 0.352218 -3.379920 0.0010

LN_AUST_MS_ -0.350122 0.080355 -4.357171 0.0000

LN_NZ_MS_ 0.621445 0.082456 7.536651 0.0000

LN_AUST_GDP_ -0.967626 0.405451 -2.386541 0.0186

LN_NZ_GDP_ 0.592750 0.280697 2.111707 0.0368

AUST_IR 0.004336 0.005416 0.800611 0.4249

NZ_IR 0.000815 0.004528 0.179988 0.8575

R-squared 0.528601 Mean dependent var -0.199089

Adjusted R-squared 0.505226 S.D. dependent var 0.089656

S.E. of regression 0.063064 Akaike info criterion -2.636191

Sum squared resid 0.481229 Schwarz criterion -2.480220

Log likelihood 175.7162 Hannan-Quinn criter. -2.572819

F-statistic 22.61379 Durbin-Watson stat 0.422977

Prob(F-statistic) 0.000000

Predicted multiple regression model is

st =β0 + β1 mt + β2 mt

¿ + β3 yt + β4 yt

¿ + β5 it + β6 it

¿ +ut

From the regression result, the estimated equation is as follows

st =−1.190−0.350 mt +0.621 mt

¿−0.968 yt + 0.592 yt

¿+0.004 it +0.0008 it

¿

The p value is less than 0.05. Therefore, the null hypothesis of normal distribution is rejected.

Therefore, errors are not normally distributed.

From the three test performed above it is clear that the model suffers from the

problem of serial autocorrelation. There is problem heteroscadasticity. Moreover the errors

are not normally distributed. All these indicate the estimated model and test statistics are not

reliable at all. The model will be statistically significant only after suitable correction taken

for the model.

Answer g

Multiple regression

Dependent Variable: LN_S_AUD_NZD_

Method: Least Squares

Date: 10/06/17 Time: 18:32

Sample: 3/01/1984 12/01/2015

Included observations: 128

Variable Coefficient Std. Error t-Statistic Prob.

C -1.190468 0.352218 -3.379920 0.0010

LN_AUST_MS_ -0.350122 0.080355 -4.357171 0.0000

LN_NZ_MS_ 0.621445 0.082456 7.536651 0.0000

LN_AUST_GDP_ -0.967626 0.405451 -2.386541 0.0186

LN_NZ_GDP_ 0.592750 0.280697 2.111707 0.0368

AUST_IR 0.004336 0.005416 0.800611 0.4249

NZ_IR 0.000815 0.004528 0.179988 0.8575

R-squared 0.528601 Mean dependent var -0.199089

Adjusted R-squared 0.505226 S.D. dependent var 0.089656

S.E. of regression 0.063064 Akaike info criterion -2.636191

Sum squared resid 0.481229 Schwarz criterion -2.480220

Log likelihood 175.7162 Hannan-Quinn criter. -2.572819

F-statistic 22.61379 Durbin-Watson stat 0.422977

Prob(F-statistic) 0.000000

Predicted multiple regression model is

st =β0 + β1 mt + β2 mt

¿ + β3 yt + β4 yt

¿ + β5 it + β6 it

¿ +ut

From the regression result, the estimated equation is as follows

st =−1.190−0.350 mt +0.621 mt

¿−0.968 yt + 0.592 yt

¿+0.004 it +0.0008 it

¿

8BASIC ECONOMETRICS

Answer h

The variable New Zealand interest rate has the largest p value = 0.8575.

Therefore, this variable is dropped and a new regression is run.

Dependent Variable: LN_S_AUD_NZD_

Method: Least Squares

Date: 10/06/17 Time: 18:33

Sample: 3/01/1984 12/01/2015

Included observations: 128

Variable Coefficient Std. Error t-Statistic Prob.

C -1.180044 0.346043 -3.410107 0.0009

LN_AUST_MS_ -0.351726 0.079542 -4.421874 0.0000

LN_NZ_MS_ 0.620828 0.082058 7.565750 0.0000

LN_AUST_GDP_ -0.970876 0.403440 -2.406494 0.0176

LN_NZ_GDP_ 0.600427 0.276336 2.172818 0.0317

AUST_IR 0.005029 0.003792 1.326330 0.1872

R-squared 0.528475 Mean dependent var -0.199089

Adjusted R-squared 0.509150 S.D. dependent var 0.089656

S.E. of regression 0.062814 Akaike info criterion -2.651548

Sum squared resid 0.481358 Schwarz criterion -2.517859

Log likelihood 175.6991 Hannan-Quinn criter. -2.597230

F-statistic 27.34696 Durbin-Watson stat 0.419055

Prob(F-statistic) 0.000000

There still remains one insignificant variable. This variable is Australian interest rate.

Therefore, this is also dropped.

Dependent Variable: LN_S_AUD_NZD_

Method: Least Squares

Date: 10/06/17 Time: 18:33

Sample: 3/01/1984 12/01/2015

Included observations: 128

Variable Coefficient Std. Error t-Statistic Prob.

C -1.112594 0.343340 -3.240497 0.0015

LN_AUST_MS_ -0.298734 0.068992 -4.329994 0.0000

LN_NZ_MS_ 0.578929 0.075966 7.620840 0.0000

LN_AUST_GDP_ -1.173667 0.374495 -3.133995 0.0022

LN_NZ_GDP_ 0.743178 0.255298 2.911016 0.0043

R-squared 0.521676 Mean dependent var -0.199089

Adjusted R-squared 0.506120 S.D. dependent var 0.089656

S.E. of regression 0.063007 Akaike info criterion -2.652857

Sum squared resid 0.488298 Schwarz criterion -2.541449

Log likelihood 174.7828 Hannan-Quinn criter. -2.607591

F-statistic 33.53692 Durbin-Watson stat 0.419712

Answer h

The variable New Zealand interest rate has the largest p value = 0.8575.

Therefore, this variable is dropped and a new regression is run.

Dependent Variable: LN_S_AUD_NZD_

Method: Least Squares

Date: 10/06/17 Time: 18:33

Sample: 3/01/1984 12/01/2015

Included observations: 128

Variable Coefficient Std. Error t-Statistic Prob.

C -1.180044 0.346043 -3.410107 0.0009

LN_AUST_MS_ -0.351726 0.079542 -4.421874 0.0000

LN_NZ_MS_ 0.620828 0.082058 7.565750 0.0000

LN_AUST_GDP_ -0.970876 0.403440 -2.406494 0.0176

LN_NZ_GDP_ 0.600427 0.276336 2.172818 0.0317

AUST_IR 0.005029 0.003792 1.326330 0.1872

R-squared 0.528475 Mean dependent var -0.199089

Adjusted R-squared 0.509150 S.D. dependent var 0.089656

S.E. of regression 0.062814 Akaike info criterion -2.651548

Sum squared resid 0.481358 Schwarz criterion -2.517859

Log likelihood 175.6991 Hannan-Quinn criter. -2.597230

F-statistic 27.34696 Durbin-Watson stat 0.419055

Prob(F-statistic) 0.000000

There still remains one insignificant variable. This variable is Australian interest rate.

Therefore, this is also dropped.

Dependent Variable: LN_S_AUD_NZD_

Method: Least Squares

Date: 10/06/17 Time: 18:33

Sample: 3/01/1984 12/01/2015

Included observations: 128

Variable Coefficient Std. Error t-Statistic Prob.

C -1.112594 0.343340 -3.240497 0.0015

LN_AUST_MS_ -0.298734 0.068992 -4.329994 0.0000

LN_NZ_MS_ 0.578929 0.075966 7.620840 0.0000

LN_AUST_GDP_ -1.173667 0.374495 -3.133995 0.0022

LN_NZ_GDP_ 0.743178 0.255298 2.911016 0.0043

R-squared 0.521676 Mean dependent var -0.199089

Adjusted R-squared 0.506120 S.D. dependent var 0.089656

S.E. of regression 0.063007 Akaike info criterion -2.652857

Sum squared resid 0.488298 Schwarz criterion -2.541449

Log likelihood 174.7828 Hannan-Quinn criter. -2.607591

F-statistic 33.53692 Durbin-Watson stat 0.419712

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9BASIC ECONOMETRICS

Prob(F-statistic) 0.000000

Finally, only the variables with significant p values remain in the model. This is the

final model including all the significant variables.

Answer i

F test for redundant variables

Dependent Variable: LN_S_AUD_NZD_

Method: Least Squares

Date: 10/06/17 Time: 19:12

Sample: 3/01/1984 12/01/2015

Included observations: 128

Variable Coefficient Std. Error t-Statistic Prob.

C -0.116118 0.015527 -7.478350 0.0000

AUST_IR -0.013670 0.005631 -2.427631 0.0166

NZ_IR 0.002064 0.005267 0.391941 0.6958

R-squared 0.236619 Mean dependent var -0.199089

Adjusted R-squared 0.224405 S.D. dependent var 0.089656

S.E. of regression 0.078958 Akaike info criterion -2.216639

Sum squared resid 0.779299 Schwarz criterion -2.149794

Log likelihood 144.8649 Hannan-Quinn criter. -2.189480

F-statistic 19.37264 Durbin-Watson stat 0.260148

Prob(F-statistic) 0.000000

P value of the computed F statistics is less than 0.05. The means computed F statistics fall

within the critical F region. The null hypothesis of non-significance can be rejected here.

Therefore, redundant variables that are excluded have overall significance.

Answer j

From the F statistics of redundant variables there is overall significance in the model

containing excluded variables. However, from the p value and t test it is seen that not all the

variables are significant. The variable New Zealand interest rate has a p value greater than

0.05. The value of t statistics for this variable falls in the critical region. Therefore, the model

containing all the relevant variables should contain only the significant variables.

Prob(F-statistic) 0.000000

Finally, only the variables with significant p values remain in the model. This is the

final model including all the significant variables.

Answer i

F test for redundant variables

Dependent Variable: LN_S_AUD_NZD_

Method: Least Squares

Date: 10/06/17 Time: 19:12

Sample: 3/01/1984 12/01/2015

Included observations: 128

Variable Coefficient Std. Error t-Statistic Prob.

C -0.116118 0.015527 -7.478350 0.0000

AUST_IR -0.013670 0.005631 -2.427631 0.0166

NZ_IR 0.002064 0.005267 0.391941 0.6958

R-squared 0.236619 Mean dependent var -0.199089

Adjusted R-squared 0.224405 S.D. dependent var 0.089656

S.E. of regression 0.078958 Akaike info criterion -2.216639

Sum squared resid 0.779299 Schwarz criterion -2.149794

Log likelihood 144.8649 Hannan-Quinn criter. -2.189480

F-statistic 19.37264 Durbin-Watson stat 0.260148

Prob(F-statistic) 0.000000

P value of the computed F statistics is less than 0.05. The means computed F statistics fall

within the critical F region. The null hypothesis of non-significance can be rejected here.

Therefore, redundant variables that are excluded have overall significance.

Answer j

From the F statistics of redundant variables there is overall significance in the model

containing excluded variables. However, from the p value and t test it is seen that not all the

variables are significant. The variable New Zealand interest rate has a p value greater than

0.05. The value of t statistics for this variable falls in the critical region. Therefore, the model

containing all the relevant variables should contain only the significant variables.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10BASIC ECONOMETRICS

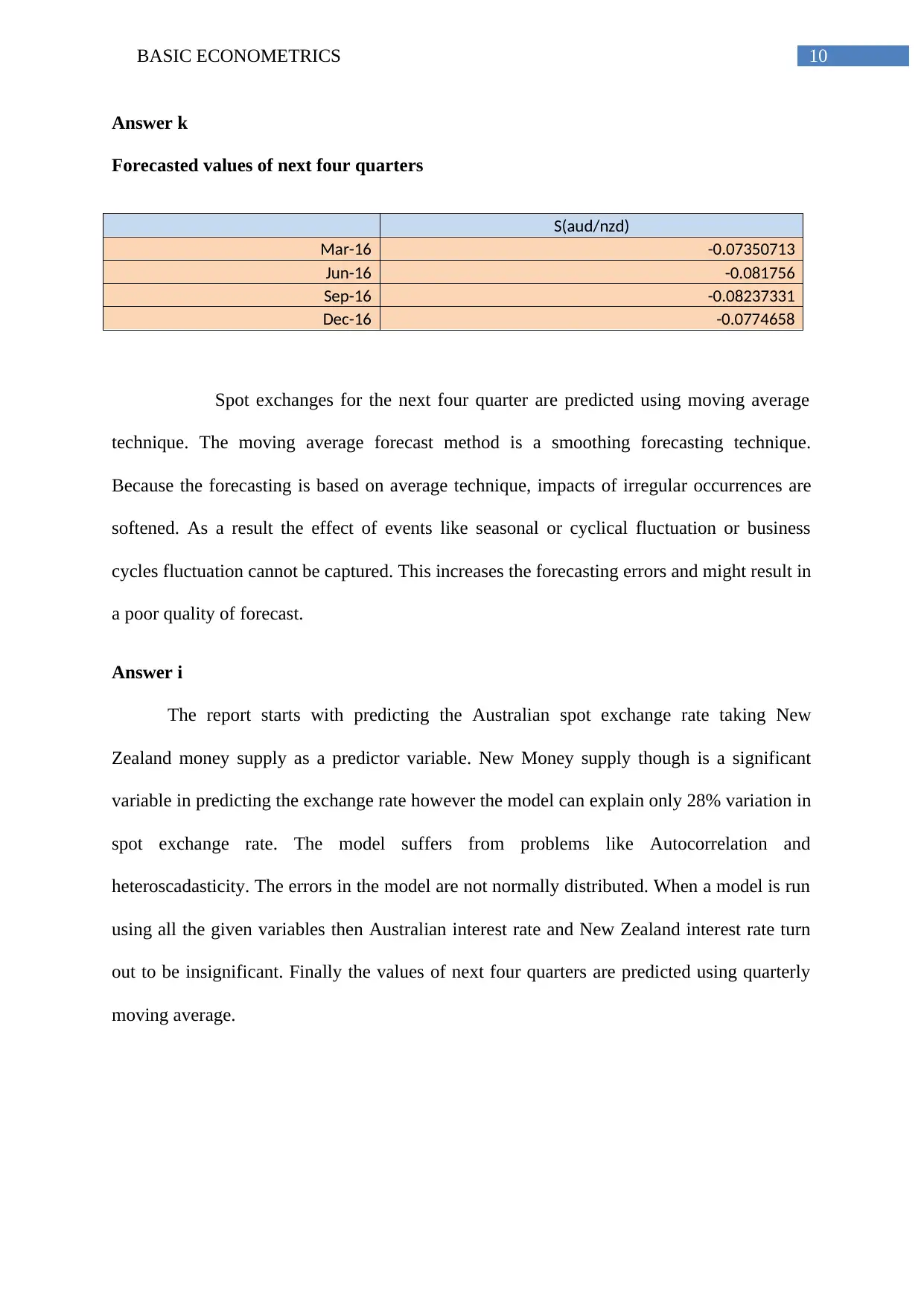

Answer k

Forecasted values of next four quarters

S(aud/nzd)

Mar-16 -0.07350713

Jun-16 -0.081756

Sep-16 -0.08237331

Dec-16 -0.0774658

Spot exchanges for the next four quarter are predicted using moving average

technique. The moving average forecast method is a smoothing forecasting technique.

Because the forecasting is based on average technique, impacts of irregular occurrences are

softened. As a result the effect of events like seasonal or cyclical fluctuation or business

cycles fluctuation cannot be captured. This increases the forecasting errors and might result in

a poor quality of forecast.

Answer i

The report starts with predicting the Australian spot exchange rate taking New

Zealand money supply as a predictor variable. New Money supply though is a significant

variable in predicting the exchange rate however the model can explain only 28% variation in

spot exchange rate. The model suffers from problems like Autocorrelation and

heteroscadasticity. The errors in the model are not normally distributed. When a model is run

using all the given variables then Australian interest rate and New Zealand interest rate turn

out to be insignificant. Finally the values of next four quarters are predicted using quarterly

moving average.

Answer k

Forecasted values of next four quarters

S(aud/nzd)

Mar-16 -0.07350713

Jun-16 -0.081756

Sep-16 -0.08237331

Dec-16 -0.0774658

Spot exchanges for the next four quarter are predicted using moving average

technique. The moving average forecast method is a smoothing forecasting technique.

Because the forecasting is based on average technique, impacts of irregular occurrences are

softened. As a result the effect of events like seasonal or cyclical fluctuation or business

cycles fluctuation cannot be captured. This increases the forecasting errors and might result in

a poor quality of forecast.

Answer i

The report starts with predicting the Australian spot exchange rate taking New

Zealand money supply as a predictor variable. New Money supply though is a significant

variable in predicting the exchange rate however the model can explain only 28% variation in

spot exchange rate. The model suffers from problems like Autocorrelation and

heteroscadasticity. The errors in the model are not normally distributed. When a model is run

using all the given variables then Australian interest rate and New Zealand interest rate turn

out to be insignificant. Finally the values of next four quarters are predicted using quarterly

moving average.

11BASIC ECONOMETRICS

Case Study Two

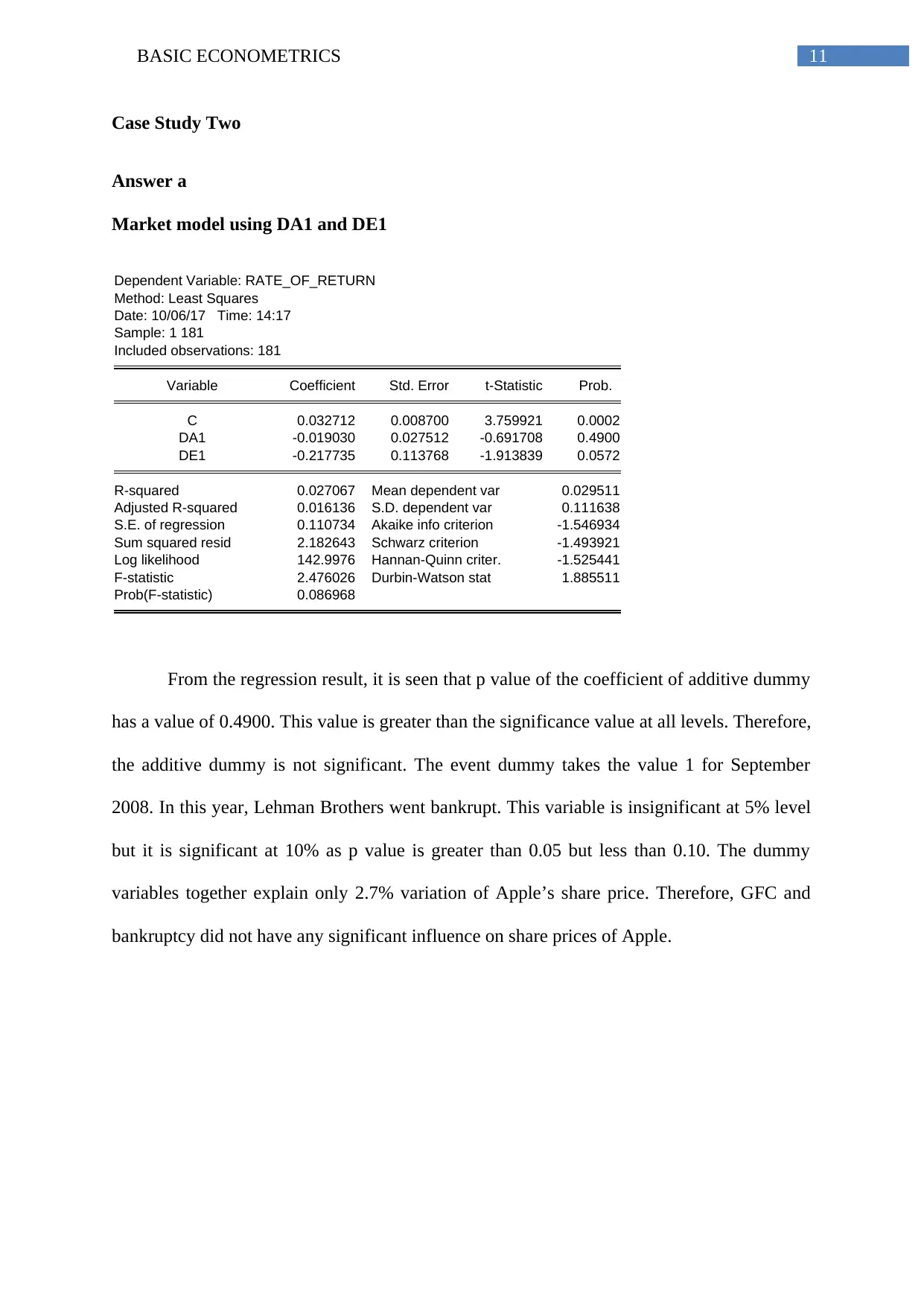

Answer a

Market model using DA1 and DE1

Dependent Variable: RATE_OF_RETURN

Method: Least Squares

Date: 10/06/17 Time: 14:17

Sample: 1 181

Included observations: 181

Variable Coefficient Std. Error t-Statistic Prob.

C 0.032712 0.008700 3.759921 0.0002

DA1 -0.019030 0.027512 -0.691708 0.4900

DE1 -0.217735 0.113768 -1.913839 0.0572

R-squared 0.027067 Mean dependent var 0.029511

Adjusted R-squared 0.016136 S.D. dependent var 0.111638

S.E. of regression 0.110734 Akaike info criterion -1.546934

Sum squared resid 2.182643 Schwarz criterion -1.493921

Log likelihood 142.9976 Hannan-Quinn criter. -1.525441

F-statistic 2.476026 Durbin-Watson stat 1.885511

Prob(F-statistic) 0.086968

From the regression result, it is seen that p value of the coefficient of additive dummy

has a value of 0.4900. This value is greater than the significance value at all levels. Therefore,

the additive dummy is not significant. The event dummy takes the value 1 for September

2008. In this year, Lehman Brothers went bankrupt. This variable is insignificant at 5% level

but it is significant at 10% as p value is greater than 0.05 but less than 0.10. The dummy

variables together explain only 2.7% variation of Apple’s share price. Therefore, GFC and

bankruptcy did not have any significant influence on share prices of Apple.

Case Study Two

Answer a

Market model using DA1 and DE1

Dependent Variable: RATE_OF_RETURN

Method: Least Squares

Date: 10/06/17 Time: 14:17

Sample: 1 181

Included observations: 181

Variable Coefficient Std. Error t-Statistic Prob.

C 0.032712 0.008700 3.759921 0.0002

DA1 -0.019030 0.027512 -0.691708 0.4900

DE1 -0.217735 0.113768 -1.913839 0.0572

R-squared 0.027067 Mean dependent var 0.029511

Adjusted R-squared 0.016136 S.D. dependent var 0.111638

S.E. of regression 0.110734 Akaike info criterion -1.546934

Sum squared resid 2.182643 Schwarz criterion -1.493921

Log likelihood 142.9976 Hannan-Quinn criter. -1.525441

F-statistic 2.476026 Durbin-Watson stat 1.885511

Prob(F-statistic) 0.086968

From the regression result, it is seen that p value of the coefficient of additive dummy

has a value of 0.4900. This value is greater than the significance value at all levels. Therefore,

the additive dummy is not significant. The event dummy takes the value 1 for September

2008. In this year, Lehman Brothers went bankrupt. This variable is insignificant at 5% level

but it is significant at 10% as p value is greater than 0.05 but less than 0.10. The dummy

variables together explain only 2.7% variation of Apple’s share price. Therefore, GFC and

bankruptcy did not have any significant influence on share prices of Apple.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.