Estimation and Testing of Capital Asset Pricing Model Assignment

Added on 2020-10-23

12 Pages1900 Words98 Views

Estimation and Testing of Capital Asset Pricing Model

TABLE OF CONTENTS1. Regression analysis..................................................................................................................32. Interpreting the estimate of βj from your regression result above...........................................33. Testing null hypothesis that αj = 0 for Microsoft stock in against to an appropriatealternative hypotheses..................................................................................................................34. Performing a hypothesis test that βj = 0 against the alternative that βj ≠ 0 using theMicrosoft data..............................................................................................................................35. Evaluate whether Microsoft stock (a Tech stock) is an aggressive stock or not by applyingsuitable test..................................................................................................................................46. Stating R2 for the regression and interpreting the same...........................................................57. Stating predicted return in relation to Microsoft for January 2009 if the risk free rate doesnot change from December 2008 but the market return increases by 1%...................................58. Repeat Question 1 for GE, GM, IBM, Disney, and Mobil-Exxon..........................................5APPENDIX......................................................................................................................................81...................................................................................................................................................82...................................................................................................................................................83...................................................................................................................................................8

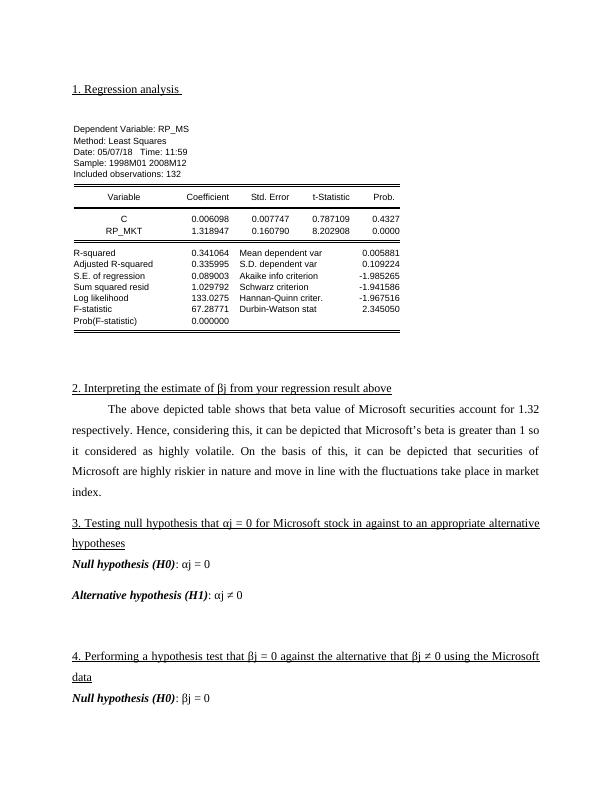

1. Regression analysis Dependent Variable: RP_MSMethod: Least SquaresDate: 05/07/18 Time: 11:59Sample: 1998M01 2008M12Included observations: 132VariableCoefficientStd. Errort-StatisticProb.C0.0060980.0077470.7871090.4327RP_MKT1.3189470.1607908.2029080.0000R-squared0.341064Mean dependent var0.005881Adjusted R-squared0.335995S.D. dependent var0.109224S.E. of regression0.089003Akaike info criterion-1.985265Sum squared resid1.029792Schwarz criterion-1.941586Log likelihood133.0275Hannan-Quinn criter.-1.967516F-statistic67.28771Durbin-Watson stat2.345050Prob(F-statistic)0.0000002. Interpreting the estimate of βj from your regression result aboveThe above depicted table shows that beta value of Microsoft securities account for 1.32respectively. Hence, considering this, it can be depicted that Microsoft’s beta is greater than 1 soit considered as highly volatile. On the basis of this, it can be depicted that securities ofMicrosoft are highly riskier in nature and move in line with the fluctuations take place in marketindex. 3. Testing null hypothesis that αj = 0 for Microsoft stock in against to an appropriate alternativehypothesesNull hypothesis (H0): αj = 0Alternative hypothesis (H1): αj ≠ 04. Performing a hypothesis test that βj = 0 against the alternative that βj ≠ 0 using the MicrosoftdataNull hypothesis (H0): βj = 0

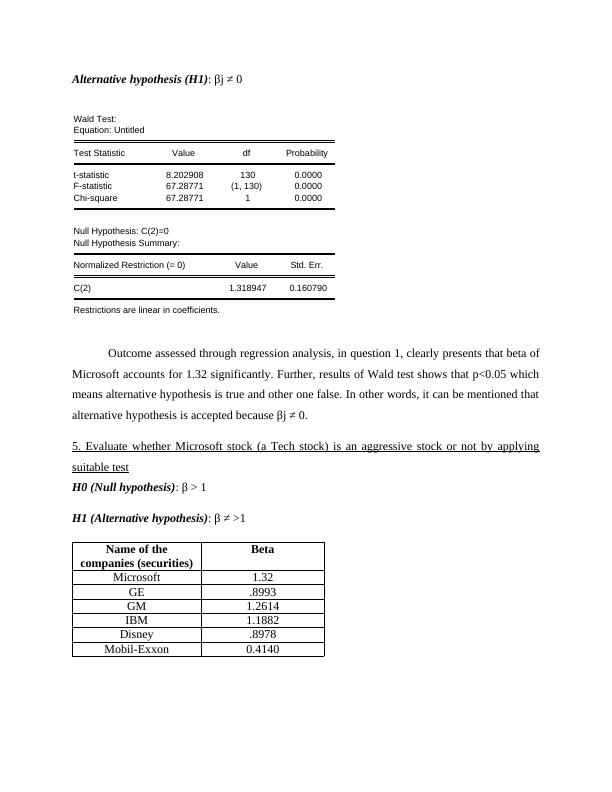

Alternative hypothesis (H1): βj ≠ 0Wald Test:Equation: UntitledTest StatisticValuedfProbabilityt-statistic8.2029081300.0000F-statistic67.28771(1, 130)0.0000Chi-square67.2877110.0000Null Hypothesis: C(2)=0Null Hypothesis Summary:Normalized Restriction (= 0)ValueStd. Err.C(2)1.3189470.160790Restrictions are linear in coefficients.Outcome assessed through regression analysis, in question 1, clearly presents that beta ofMicrosoft accounts for 1.32 significantly. Further, results of Wald test shows that p<0.05 whichmeans alternative hypothesis is true and other one false. In other words, it can be mentioned thatalternative hypothesis is accepted because βj ≠ 0. 5. Evaluate whether Microsoft stock (a Tech stock) is an aggressive stock or not by applyingsuitable testH0 (Null hypothesis): β > 1H1 (Alternative hypothesis): β ≠ >1Name of thecompanies (securities)BetaMicrosoft1.32GE.8993GM1.2614IBM1.1882Disney.8978Mobil-Exxon0.4140

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Beta Estimation for Risk Premium on the Market Portfoliolg...

|11

|705

|213

Report on Econometrics of Microsoftlg...

|11

|705

|106

Regression Analysis on Effect of Federally Funded School Lunch Program on Student Performance and Short-term Interest Ratelg...

|15

|2684

|375

Probability of Chi Square Statisticslg...

|17

|3311

|188

Econometrics and Business Statisticslg...

|15

|2830

|124

Regression Analysis in SPSSlg...

|16

|1866

|25