Business Analysis and Valuation of Qantas Airline Corporation

VerifiedAdded on 2023/06/12

|15

|3729

|405

AI Summary

This report explains the Qantas Airline Corporation’s competitive policy. The Qantas’ competitive evaluation is based on Porter’s 5 Forces. The report has been prepared to evaluate the financial and non financial performance of Qantas Limited. The report evaluates the non financial performance of the company on the basis of porter’s five forces model, SWOT analysis, corporate strategy of the company etc. On the other hand, the financial performance of the company has been evaluated on the basis of accounting policies of the company, financial position and financial performance of company in year 2013 and financial performance and financial position of the company in year 2017

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running Head: Business Analysis and Valuation

1

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Business Analysis and Valuation 2

Executive summary

This report explains the Qantas Airline Corporation’s competitive policy. This report

is basically based on the many case studies that explains about achievements of Qantas. The

Qantas’ competitive evaluation is based on Porter’s 5 Forces. The report has been prepared to

evaluate the financial and non financial performance of Qantas Limited. The report evaluates

the non financial performance of the company on the basis of porter’s five forces model,

SWOT (strength, weakness, opportunity and threat) analysis, corporate strategy of the

company etc. On the other hand, the financial performance of the company has been

evaluated on the basis of accounting policies of the company, financial position and financial

performance of company in year 2013 and financial performance and financial position of the

company in year 2017

Executive summary

This report explains the Qantas Airline Corporation’s competitive policy. This report

is basically based on the many case studies that explains about achievements of Qantas. The

Qantas’ competitive evaluation is based on Porter’s 5 Forces. The report has been prepared to

evaluate the financial and non financial performance of Qantas Limited. The report evaluates

the non financial performance of the company on the basis of porter’s five forces model,

SWOT (strength, weakness, opportunity and threat) analysis, corporate strategy of the

company etc. On the other hand, the financial performance of the company has been

evaluated on the basis of accounting policies of the company, financial position and financial

performance of company in year 2013 and financial performance and financial position of the

company in year 2017

Business Analysis and Valuation 3

Contents

Introduction.......................................................................................................................4

Company overview...........................................................................................................4

Competitive analysis (Porter’s 5 forces model.................................................................4

Bargaining power of suppliers......................................................................................5

Bargaining power of buyers..........................................................................................5

Threats of new entry.....................................................................................................5

Threat of substitute.......................................................................................................6

Competition among the existing players......................................................................6

SWOT analysis.................................................................................................................7

Strength.........................................................................................................................7

Weakness......................................................................................................................7

Opportunity...................................................................................................................7

Threat............................................................................................................................7

Corporate strategy.............................................................................................................8

Accounting policies..........................................................................................................8

Leasing accounting policies..........................................................................................8

Depreciation policy.......................................................................................................9

Qantas financial position in 2013.....................................................................................9

Financial performance..................................................................................................9

Financial position..........................................................................................................9

Qantas financial position in 2017...................................................................................10

Financial performance................................................................................................10

Financial position........................................................................................................10

Contents

Introduction.......................................................................................................................4

Company overview...........................................................................................................4

Competitive analysis (Porter’s 5 forces model.................................................................4

Bargaining power of suppliers......................................................................................5

Bargaining power of buyers..........................................................................................5

Threats of new entry.....................................................................................................5

Threat of substitute.......................................................................................................6

Competition among the existing players......................................................................6

SWOT analysis.................................................................................................................7

Strength.........................................................................................................................7

Weakness......................................................................................................................7

Opportunity...................................................................................................................7

Threat............................................................................................................................7

Corporate strategy.............................................................................................................8

Accounting policies..........................................................................................................8

Leasing accounting policies..........................................................................................8

Depreciation policy.......................................................................................................9

Qantas financial position in 2013.....................................................................................9

Financial performance..................................................................................................9

Financial position..........................................................................................................9

Qantas financial position in 2017...................................................................................10

Financial performance................................................................................................10

Financial position........................................................................................................10

Business Analysis and Valuation 4

Similarities and differences among 2013 and 2016........................................................11

Similarities..................................................................................................................11

Differences..................................................................................................................11

Recommendation and conclusion...................................................................................11

References.......................................................................................................................12

Appendix.........................................................................................................................14

Similarities and differences among 2013 and 2016........................................................11

Similarities..................................................................................................................11

Differences..................................................................................................................11

Recommendation and conclusion...................................................................................11

References.......................................................................................................................12

Appendix.........................................................................................................................14

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Business Analysis and Valuation 5

Company overview:

Qantas airline is an international company. Headquarter of the company is in

Australia. The vision and mission statement of the company explains that the Qantas is soon

going to be fit in the best airlines worldwide. The company has been founded in 1920 in

Queensland. From 1920, the company has been developed to be the top leading Australian

local and international airline. The company has majorly focused on the customer services,

safety, engineering, maintenances and operational reliability. These factors have helped the

company to be successful (Qantas Limited, 2018).

Competitive analysis (Porter’s 5 forces model):

Porter’s 5 forces model is an evaluation technique to evaluate the external position of

the company. It is used to analyze the industry position of the company so that the better

policies and strategies could be made by the management of the company about the

performance of the company (Deegan, 2013).

Bargaining power of suppliers:

Bargaining power of suppliers explain about various rules and conditions which could

be imposed by the suppliers of an industry at the time of selling the raw material to the

company. The case study and the position of Qantas limited explains that the few suppliers

are available in the airline industry of Australia and thus the supplier are in the position to

impose some conditions (Bui et al, 2016). The suppliers are manipulating the company

according to their demands and choices. The availability and the supply of raw material have

impacted on the industry and thus the bargaining power of supplier has been enhanced.

Bargaining power of buyers:

Bargaining power of buyers explain about various rules and conditions which could

be imposed by the buyers of an industry at the time of buying the products and the services

from the company. The case study and the position of Qantas limited explain that the huge

number of buyers is available in the airline industry of Australia and thus the buyers are not

in the position to impose some conditions (Saunders and Cornett, 2014). The buyers could

not manipulate the prices and the services of the company as there are numerous buyers in the

market. The availability and the supply of products and services have impacted on the

industry and thus the bargaining power of buyers has been reduced.

Company overview:

Qantas airline is an international company. Headquarter of the company is in

Australia. The vision and mission statement of the company explains that the Qantas is soon

going to be fit in the best airlines worldwide. The company has been founded in 1920 in

Queensland. From 1920, the company has been developed to be the top leading Australian

local and international airline. The company has majorly focused on the customer services,

safety, engineering, maintenances and operational reliability. These factors have helped the

company to be successful (Qantas Limited, 2018).

Competitive analysis (Porter’s 5 forces model):

Porter’s 5 forces model is an evaluation technique to evaluate the external position of

the company. It is used to analyze the industry position of the company so that the better

policies and strategies could be made by the management of the company about the

performance of the company (Deegan, 2013).

Bargaining power of suppliers:

Bargaining power of suppliers explain about various rules and conditions which could

be imposed by the suppliers of an industry at the time of selling the raw material to the

company. The case study and the position of Qantas limited explains that the few suppliers

are available in the airline industry of Australia and thus the supplier are in the position to

impose some conditions (Bui et al, 2016). The suppliers are manipulating the company

according to their demands and choices. The availability and the supply of raw material have

impacted on the industry and thus the bargaining power of supplier has been enhanced.

Bargaining power of buyers:

Bargaining power of buyers explain about various rules and conditions which could

be imposed by the buyers of an industry at the time of buying the products and the services

from the company. The case study and the position of Qantas limited explain that the huge

number of buyers is available in the airline industry of Australia and thus the buyers are not

in the position to impose some conditions (Saunders and Cornett, 2014). The buyers could

not manipulate the prices and the services of the company as there are numerous buyers in the

market. The availability and the supply of products and services have impacted on the

industry and thus the bargaining power of buyers has been reduced.

Business Analysis and Valuation 6

Threats of new entry:

Threat of new entry explains about the companies and the firms which are willing to

enter into the market. The new entry of firms has major impacts on the existing business in

the industry as they enter into the new market with innovative services and the products. The

case study and the position of Qantas limited explains that the threat from the new entry in

the airline industry of Australia is quite lower as huge investment is required to enter into the

market as well as various legal perspective is also obligated to it. The company is still

required to launch some innovative services and must make few changes into the existing

services and the strategies.

Threat of substitute:

Threat of substitute explains about the product and services which are almost similar

to the company’s products and services and that could be used by the customers of the

company as a substitute of products and services of the industry. The case study and the

position of Qantas limited explains that the threat from the substitute products in the airline

industry of Australia is quite lower at international level but at domestic level, cars, taxies,

busses etc could be used as a substitute (Elliott and Elliott, 2007). The company is required to

launch some innovative services and must make few changes into the existing services and

the strategies to reduce the threat level (Glajnaric, 2016).

Competition among the existing players:

Threat of industry competition explains about the companies which already exist in

the market and offering the same services to the clients. The case study and the position of

Qantas limited explains that the industry competition in the airline industry of Australia is

quite lower at domestic level as the company is the oldest comapny and the company is the

leader in airline industry in Australia. Though, the case explains that the competition level is

quite higher at international level (Schroeder, Clark and Cathey, 2001). The company is

required to make few changes into the existing services and the strategies to reduce the threat

level such as company could use the cost leadership strategies to attract the clients.

SWOT analysis:

SWOT stands for strength, weakness, opportunity and threat position of an

organization. SWOT analysis explains about the internal strength and weakness of the

Threats of new entry:

Threat of new entry explains about the companies and the firms which are willing to

enter into the market. The new entry of firms has major impacts on the existing business in

the industry as they enter into the new market with innovative services and the products. The

case study and the position of Qantas limited explains that the threat from the new entry in

the airline industry of Australia is quite lower as huge investment is required to enter into the

market as well as various legal perspective is also obligated to it. The company is still

required to launch some innovative services and must make few changes into the existing

services and the strategies.

Threat of substitute:

Threat of substitute explains about the product and services which are almost similar

to the company’s products and services and that could be used by the customers of the

company as a substitute of products and services of the industry. The case study and the

position of Qantas limited explains that the threat from the substitute products in the airline

industry of Australia is quite lower at international level but at domestic level, cars, taxies,

busses etc could be used as a substitute (Elliott and Elliott, 2007). The company is required to

launch some innovative services and must make few changes into the existing services and

the strategies to reduce the threat level (Glajnaric, 2016).

Competition among the existing players:

Threat of industry competition explains about the companies which already exist in

the market and offering the same services to the clients. The case study and the position of

Qantas limited explains that the industry competition in the airline industry of Australia is

quite lower at domestic level as the company is the oldest comapny and the company is the

leader in airline industry in Australia. Though, the case explains that the competition level is

quite higher at international level (Schroeder, Clark and Cathey, 2001). The company is

required to make few changes into the existing services and the strategies to reduce the threat

level such as company could use the cost leadership strategies to attract the clients.

SWOT analysis:

SWOT stands for strength, weakness, opportunity and threat position of an

organization. SWOT analysis explains about the internal strength and weakness of the

Business Analysis and Valuation 7

company as well as external opportunities and threat of the company at the same time. The

SWOT analysis study of Qantas limited is as follows:

Strength:

1. Strong presence at domestic and

international level

2. Backing by the Australian

government offers a good business

presence.

3. Largest and oldest airline in Australia

4. Good advertising and sponsorship

exercises.

5. It is offering services around 80

domestic as well as international

destinations (Saunders and Cornett,

2014).

Weakness:

1. Price fixing issues

2. Limited international presence

3. Various incidents which have harmed

the image of the company.

Opportunity:

1. Company could become the leader in

Asian continent as no strong

competitor is there.

2. Various international destinations

could be covered by the company.

3. Company could tie up with

international airline brands.

Threat:

1. The main threat of the company is

continuously raising prices of fuel.

2. Labour prices are also enhancing

rapidly.

3. Competition from international

brands.

It explains that the various opportunities are there for the company to grab and

enhance the level of the profitability and the market share. Though, the company is also

facing some threats which should be removed by the company through using the new

strategies and policies.

company as well as external opportunities and threat of the company at the same time. The

SWOT analysis study of Qantas limited is as follows:

Strength:

1. Strong presence at domestic and

international level

2. Backing by the Australian

government offers a good business

presence.

3. Largest and oldest airline in Australia

4. Good advertising and sponsorship

exercises.

5. It is offering services around 80

domestic as well as international

destinations (Saunders and Cornett,

2014).

Weakness:

1. Price fixing issues

2. Limited international presence

3. Various incidents which have harmed

the image of the company.

Opportunity:

1. Company could become the leader in

Asian continent as no strong

competitor is there.

2. Various international destinations

could be covered by the company.

3. Company could tie up with

international airline brands.

Threat:

1. The main threat of the company is

continuously raising prices of fuel.

2. Labour prices are also enhancing

rapidly.

3. Competition from international

brands.

It explains that the various opportunities are there for the company to grab and

enhance the level of the profitability and the market share. Though, the company is also

facing some threats which should be removed by the company through using the new

strategies and policies.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business Analysis and Valuation 8

Corporate strategy:

The case study and the company analysis explain that in 1992, the corporate strategy

of the company was quite different. The company was offering the transportation services to

the travellers under Australia flagship airlines. In case of domestic market, the corporate

strategy of the company has not been changed. The company is still offering the services to

the travellers in low cost through its sub division “Jetstar”. The company has launched its

various new divisions to manage the low cost as well as high cost services. To assemble the

worldwide travellers, the company has launched the low cost services and products which are

absolutely the part of business division “Jetstar” (CAPA Centre for Aviation, 2018). Though,

the company has made few changes into the existing corporate strategy and the company has

also adopted new strategies such as frequent flyer loyalty agenda has been changed by the

company to attract more customers. Company has also adopted the low staff cost plan to

reduce the expenses level of the company.

Accounting policies:

An auditor is required to analyze and evaluate the financial statement of the company

on the basis of various accounting policies and the accounting standards. In case of airline

industry, an auditor should look over the following policies while evaluating the financial

statements of the company:

Leasing accounting policies:

The study on the airline industry explains that for entering into the airline industry, a

company is required to make huge investments as the equipments such as aircraft and the

process of the company is quite costly. Occasionally, the companies who are working under

airline industry find the leasing option more worthy then buying option. However, this option

could be used by the companies to track over the stockholders’ equity of the company (Laux

and Leuz, 2009). So, it becomes important for the auditor of the company to examine the

current leasing strategy of the company and evaluate the lease amount on the basis of that so

that it could be evaluated that whether the leasing amount has been recorded by the company

correctly or not.

Depreciation policy:

In addition, it has been found that it is a necessity for an auditor to evaluate the

depreciation technique of the company and calculate the depreciation figure accordingly.

Corporate strategy:

The case study and the company analysis explain that in 1992, the corporate strategy

of the company was quite different. The company was offering the transportation services to

the travellers under Australia flagship airlines. In case of domestic market, the corporate

strategy of the company has not been changed. The company is still offering the services to

the travellers in low cost through its sub division “Jetstar”. The company has launched its

various new divisions to manage the low cost as well as high cost services. To assemble the

worldwide travellers, the company has launched the low cost services and products which are

absolutely the part of business division “Jetstar” (CAPA Centre for Aviation, 2018). Though,

the company has made few changes into the existing corporate strategy and the company has

also adopted new strategies such as frequent flyer loyalty agenda has been changed by the

company to attract more customers. Company has also adopted the low staff cost plan to

reduce the expenses level of the company.

Accounting policies:

An auditor is required to analyze and evaluate the financial statement of the company

on the basis of various accounting policies and the accounting standards. In case of airline

industry, an auditor should look over the following policies while evaluating the financial

statements of the company:

Leasing accounting policies:

The study on the airline industry explains that for entering into the airline industry, a

company is required to make huge investments as the equipments such as aircraft and the

process of the company is quite costly. Occasionally, the companies who are working under

airline industry find the leasing option more worthy then buying option. However, this option

could be used by the companies to track over the stockholders’ equity of the company (Laux

and Leuz, 2009). So, it becomes important for the auditor of the company to examine the

current leasing strategy of the company and evaluate the lease amount on the basis of that so

that it could be evaluated that whether the leasing amount has been recorded by the company

correctly or not.

Depreciation policy:

In addition, it has been found that it is a necessity for an auditor to evaluate the

depreciation technique of the company and calculate the depreciation figure accordingly.

Business Analysis and Valuation 9

There are numerous depreciation techniques which could be used by the companies to

depreciate the equipments and machineries of the company. For instance, double

depreciation, declining units of production, straight line method etc. In case of airline

industry, all the depreciation methods are of no use for the industry as the machineries and

the equipments of the industry are quite different in nature (Lee, 2006). Thus, an auditor

should look on the depreciation technique of the firms in the airline industry and must

investigate and assure that whether the right depreciation techniques have been used by the

firms or not and whether the right % of depreciation has been used by the company (Ross,

Westerfield and Jordan, 2008).

However, various other policies and accounting standards are also there which should

be evaluated by the auditors to recognize the performance of the company in better way and

offer a fair auditor’s report to the stakeholders of the company.

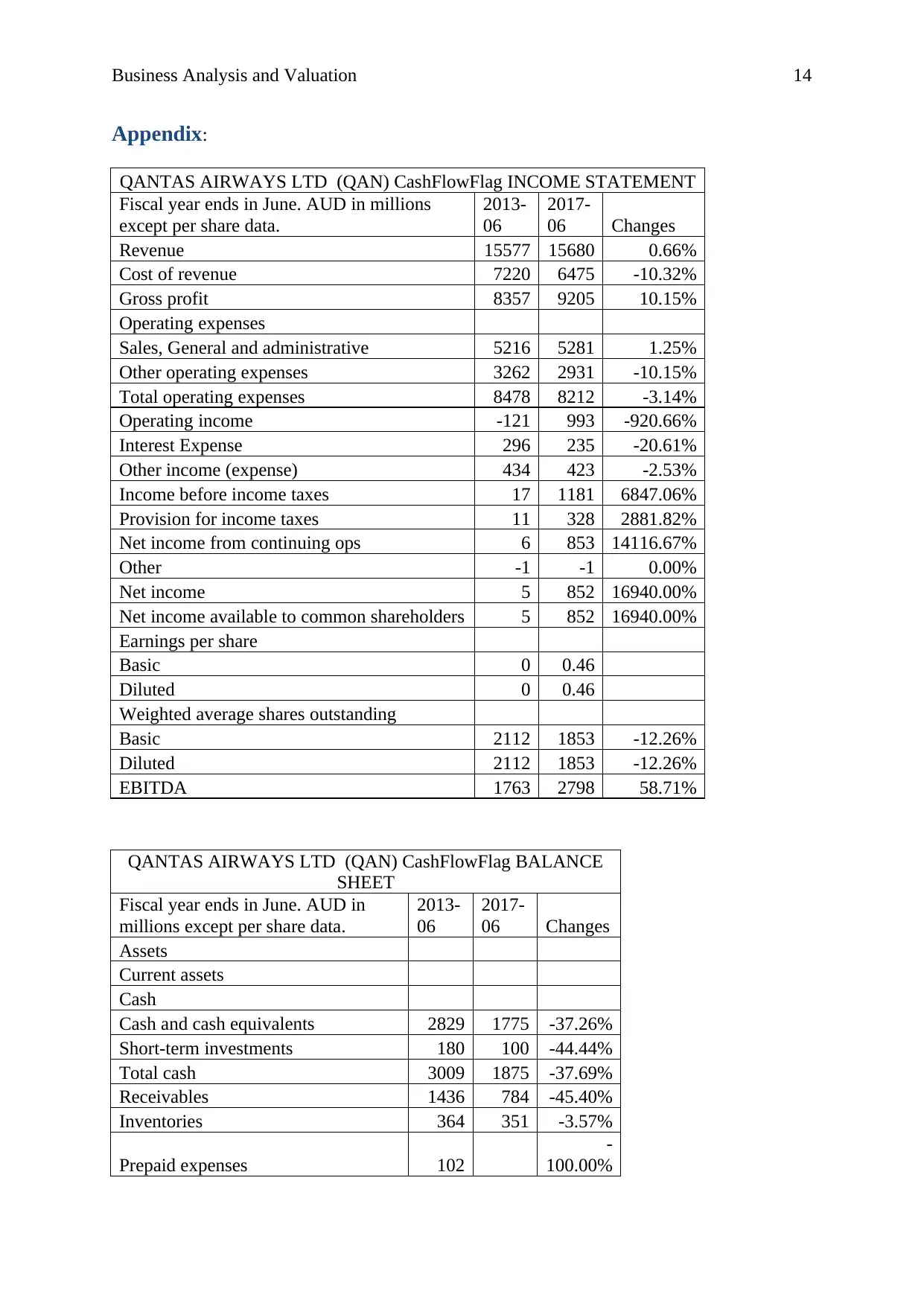

Qantas financial position in 2013:

The financial position and performance of the company in the year of 2013 is as

follows:

Financial performance:

The annual report (2013) of the company expresses that the total profit of the

company was $ 15,577 million in 2013. However, the cost of revenue of the company was $

7,220 million. It leads to the company to total gross profit of $ 8,357 million. The other cost

and the EBIT level of the company explains about the total income of $ 17 million before tax

expenses (Chung, 2018). And lastly, it briefs that the net profit of the company was $ 5

million in the year of 2013. The overall financial performance of the company has been better

in 2013 in terms of last few years.

Financial position:

Further, the annual report (2013) of the company expresses that the total current assets

of the company was $ 5,245 million in 2013. On the other hand, the noncurrent assets of the

company were $ 14,955 million. It leads to the company to total assets of $ 20,200 million.

On the other hand, the total liabilities of the company were $ 14,251 million in the year of

2013 and the total stockholder’s equity of the company was $ 5,949 million (The wall Street

Journal, 2018). The overall financial position of the company has been better in 2013 in terms

of last few years.

There are numerous depreciation techniques which could be used by the companies to

depreciate the equipments and machineries of the company. For instance, double

depreciation, declining units of production, straight line method etc. In case of airline

industry, all the depreciation methods are of no use for the industry as the machineries and

the equipments of the industry are quite different in nature (Lee, 2006). Thus, an auditor

should look on the depreciation technique of the firms in the airline industry and must

investigate and assure that whether the right depreciation techniques have been used by the

firms or not and whether the right % of depreciation has been used by the company (Ross,

Westerfield and Jordan, 2008).

However, various other policies and accounting standards are also there which should

be evaluated by the auditors to recognize the performance of the company in better way and

offer a fair auditor’s report to the stakeholders of the company.

Qantas financial position in 2013:

The financial position and performance of the company in the year of 2013 is as

follows:

Financial performance:

The annual report (2013) of the company expresses that the total profit of the

company was $ 15,577 million in 2013. However, the cost of revenue of the company was $

7,220 million. It leads to the company to total gross profit of $ 8,357 million. The other cost

and the EBIT level of the company explains about the total income of $ 17 million before tax

expenses (Chung, 2018). And lastly, it briefs that the net profit of the company was $ 5

million in the year of 2013. The overall financial performance of the company has been better

in 2013 in terms of last few years.

Financial position:

Further, the annual report (2013) of the company expresses that the total current assets

of the company was $ 5,245 million in 2013. On the other hand, the noncurrent assets of the

company were $ 14,955 million. It leads to the company to total assets of $ 20,200 million.

On the other hand, the total liabilities of the company were $ 14,251 million in the year of

2013 and the total stockholder’s equity of the company was $ 5,949 million (The wall Street

Journal, 2018). The overall financial position of the company has been better in 2013 in terms

of last few years.

Business Analysis and Valuation 10

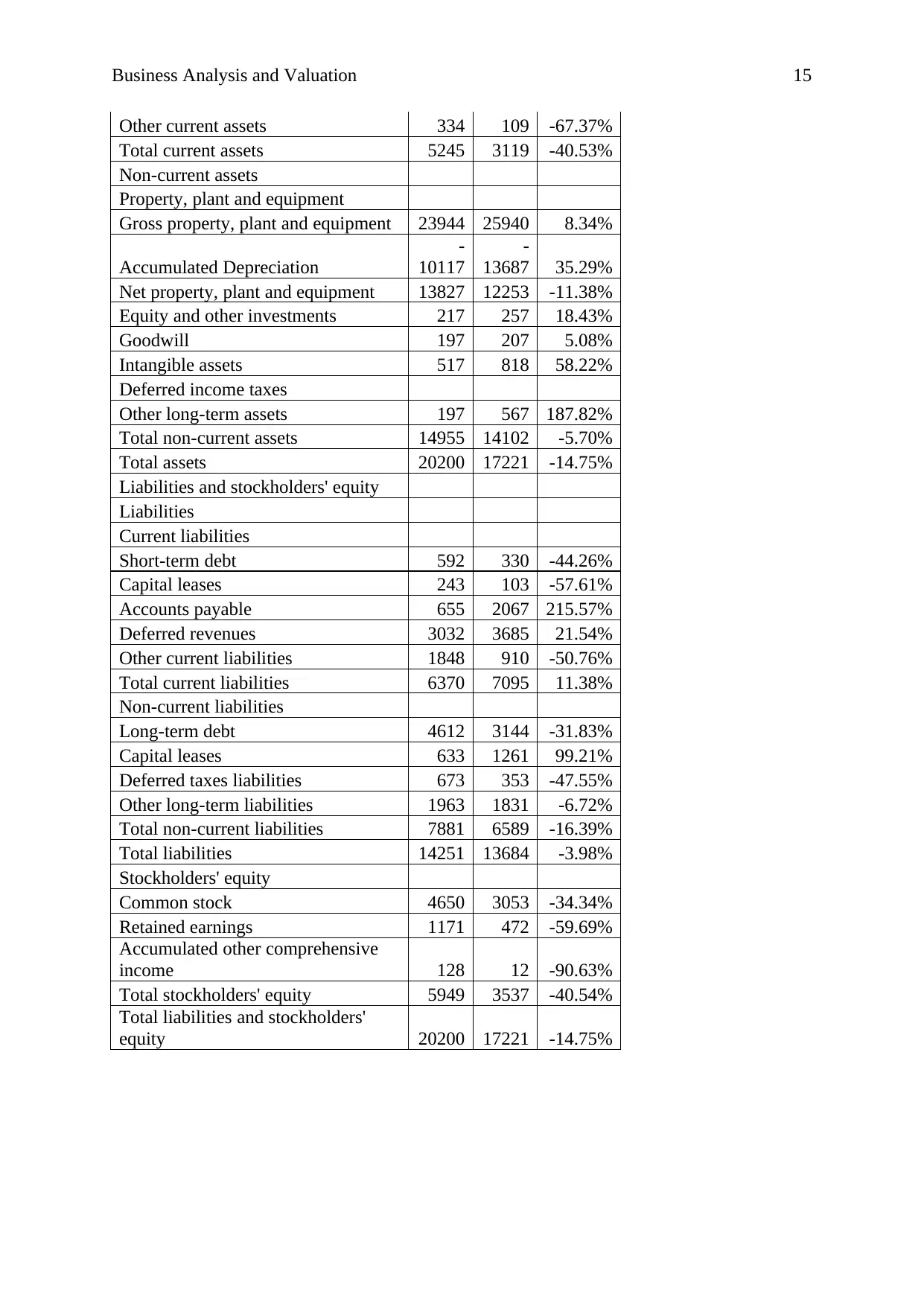

Qantas financial position in 2017:

The financial position and performance of the company in the year of 2013 is as

follows:

Financial performance:

The annual report (2017) of the company expresses that the total profit of the

company was $ 15,680 million in 2017. However, the cost of revenue of the company was $

9,205 million. It leads to the company to total gross profit of $ 9,205 million. The other cost

and the EBIT level of the company explains about the total income of $ 1181 million before

tax expenses. And lastly, it briefs that the net profit of the company was $ 853 million in the

year of 2013 (Annual report, 2017). Though, the comparative study has explains that the

company has faced various issues in last few years though, the current performance of the

company is quite better.

Financial position:

Further, the annual report (2017) of the company expresses that the total current assets

of the company was $ 3,119 million in 2017. On the other hand, the noncurrent assets of the

company were $ 14,102 million (SKIFT, 2018). It leads to the company to total assets of $

17,221 million. On the other hand, the total liabilities of the company were $ 13,684 million

in the year of 2017 and the total stockholder’s equity of the company was $ 3,537 million.

The overall financial position of the company has been lower in 2017 in terms of last few

years.

Similarities and differences among 2013 and 2016:

Similarities:

It has been evaluated after analysing the statement of financial position and statement

of financial performance of the company that the performance of the company has been better

as well as the company has also made few changes into the financial position to manage the

risk and cost position of the company in both the years (2013 and 2017).

Differences:

Further, it has been evaluated after analysing the statement of financial position and

statement of financial performance of the company that the few changes have taken place into

the financial performance and position of the company in 2017 in context with the 2013. The

Qantas financial position in 2017:

The financial position and performance of the company in the year of 2013 is as

follows:

Financial performance:

The annual report (2017) of the company expresses that the total profit of the

company was $ 15,680 million in 2017. However, the cost of revenue of the company was $

9,205 million. It leads to the company to total gross profit of $ 9,205 million. The other cost

and the EBIT level of the company explains about the total income of $ 1181 million before

tax expenses. And lastly, it briefs that the net profit of the company was $ 853 million in the

year of 2013 (Annual report, 2017). Though, the comparative study has explains that the

company has faced various issues in last few years though, the current performance of the

company is quite better.

Financial position:

Further, the annual report (2017) of the company expresses that the total current assets

of the company was $ 3,119 million in 2017. On the other hand, the noncurrent assets of the

company were $ 14,102 million (SKIFT, 2018). It leads to the company to total assets of $

17,221 million. On the other hand, the total liabilities of the company were $ 13,684 million

in the year of 2017 and the total stockholder’s equity of the company was $ 3,537 million.

The overall financial position of the company has been lower in 2017 in terms of last few

years.

Similarities and differences among 2013 and 2016:

Similarities:

It has been evaluated after analysing the statement of financial position and statement

of financial performance of the company that the performance of the company has been better

as well as the company has also made few changes into the financial position to manage the

risk and cost position of the company in both the years (2013 and 2017).

Differences:

Further, it has been evaluated after analysing the statement of financial position and

statement of financial performance of the company that the few changes have taken place into

the financial performance and position of the company in 2017 in context with the 2013. The

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Business Analysis and Valuation 11

new profit level of the company has been enhanced from 0.04% to 5.44% whereas the

liability and equity level has also been changed in 2017.

Recommendation and conclusion:

According to the evaluation and the study, it has been found that the financial position

and performance of the company has been better in 2017. The annual report of the company

express about the development and the growth position of the company which has been

higher. The case explains that the future performance of the company would be much better

and thus the company should invest more in the company to generate more returns in next 1-2

year.

new profit level of the company has been enhanced from 0.04% to 5.44% whereas the

liability and equity level has also been changed in 2017.

Recommendation and conclusion:

According to the evaluation and the study, it has been found that the financial position

and performance of the company has been better in 2017. The annual report of the company

express about the development and the growth position of the company which has been

higher. The case explains that the future performance of the company would be much better

and thus the company should invest more in the company to generate more returns in next 1-2

year.

Business Analysis and Valuation 12

References:

Annual Report. 2013. Qantas Airline group. (Online). Available at:

http://investor.qantas.com/FormBuilder/_Resource/_module/doLLG5ufYkCyEPjF1tpgyw/

file/annual-reports/2013AnnualReport.pdf (Accessed as on 21st April 2018).

Annual Report. 2013. Qantas Airline group. (Online). Available at:

https://www.qantasnewsroom.com.au/media-releases/qantas-201213-full-year-financial-

results/ (Accessed as on 21st April 2018).

Annual Report. 2017. Qantas Airline group. (Online). Available at:

http://investor.qantas.com/annual-report-2017/ (Accessed as on 21st April 2018).

Bui, S.B.D., Petersen, T., Poulsen, J.N. and Gazerani, P., 2016. Headaches attributed to

airplane travel: a Danish survey. The journal of headache and pain, 17(1), p.33.

CAPA Centre for Aviation. 2018. Qantas Airline group. (Online). Available at:

https://centreforaviation.com/data/profiles/airline-groups/qantas-group (Accessed as on 21st

April 2018).

Chung, F. 2018. Qantas posts record $1.53 billion full-year profit. (Online). Available at:

http://www.news.com.au/finance/business/travel/qantas-just-had-its-best-year-ever/news-

story/f19ad5ddc1320591487eec0a5ffab7ab (Accessed as on 21st April 2018).

Deegan, C. 2013. Financial accounting theory. McGraw-Hill Education Australia.

Elliott, B., and Elliott, J. 2007. Financial accounting and reporting. Pearson Education.

Glajnaric, M., 2016. The importance of dividend paying stocks. Equity, 30(2), p.6.

Laux, C. and Leuz, C., 2009. The crisis of fair-value accounting: Making sense of the recent

debate. Accounting, organizations and society, 34(6), pp.826-834.

Lee, T.A., 2006. The FASB and accounting for economic reality. Accounting and the Public

Interest, 6(1), pp.1-21.

Qantas limited. 2018. Home. (Online). Available at: https://www.qantaslimited.com/

(Accessed as on 21st April 2018).

Ross, S.A., Westerfield, R. and Jordan, B.D., 2008. Fundamentals of corporate finance. Tata

McGraw-Hill Education.

References:

Annual Report. 2013. Qantas Airline group. (Online). Available at:

http://investor.qantas.com/FormBuilder/_Resource/_module/doLLG5ufYkCyEPjF1tpgyw/

file/annual-reports/2013AnnualReport.pdf (Accessed as on 21st April 2018).

Annual Report. 2013. Qantas Airline group. (Online). Available at:

https://www.qantasnewsroom.com.au/media-releases/qantas-201213-full-year-financial-

results/ (Accessed as on 21st April 2018).

Annual Report. 2017. Qantas Airline group. (Online). Available at:

http://investor.qantas.com/annual-report-2017/ (Accessed as on 21st April 2018).

Bui, S.B.D., Petersen, T., Poulsen, J.N. and Gazerani, P., 2016. Headaches attributed to

airplane travel: a Danish survey. The journal of headache and pain, 17(1), p.33.

CAPA Centre for Aviation. 2018. Qantas Airline group. (Online). Available at:

https://centreforaviation.com/data/profiles/airline-groups/qantas-group (Accessed as on 21st

April 2018).

Chung, F. 2018. Qantas posts record $1.53 billion full-year profit. (Online). Available at:

http://www.news.com.au/finance/business/travel/qantas-just-had-its-best-year-ever/news-

story/f19ad5ddc1320591487eec0a5ffab7ab (Accessed as on 21st April 2018).

Deegan, C. 2013. Financial accounting theory. McGraw-Hill Education Australia.

Elliott, B., and Elliott, J. 2007. Financial accounting and reporting. Pearson Education.

Glajnaric, M., 2016. The importance of dividend paying stocks. Equity, 30(2), p.6.

Laux, C. and Leuz, C., 2009. The crisis of fair-value accounting: Making sense of the recent

debate. Accounting, organizations and society, 34(6), pp.826-834.

Lee, T.A., 2006. The FASB and accounting for economic reality. Accounting and the Public

Interest, 6(1), pp.1-21.

Qantas limited. 2018. Home. (Online). Available at: https://www.qantaslimited.com/

(Accessed as on 21st April 2018).

Ross, S.A., Westerfield, R. and Jordan, B.D., 2008. Fundamentals of corporate finance. Tata

McGraw-Hill Education.

Business Analysis and Valuation 13

Saunders, A., and Cornett, M. M. 2014. Financial institutions management. McGraw-Hill

Education,.

Schroeder, R.G., Clark, M.W. and Cathey, J.M., 2001. Accounting theory and

analysis. Chapel Hill: University of North Carolina.

SKIFT. 2018. Qantas Airline group. (Online). Available at:

https://skift.com/2017/02/23/qantas-profit-dips-7-5-percent-amid-overseas-competition/

(Accessed as on 21st April 2018).

The wall street Journal. 2018. Qantas Airline group. (Online). Available at:

http://quotes.wsj.com/AU/XASX/QAN/financials/annual/balance-sheet (Accessed as on 21st

April 2018).

Saunders, A., and Cornett, M. M. 2014. Financial institutions management. McGraw-Hill

Education,.

Schroeder, R.G., Clark, M.W. and Cathey, J.M., 2001. Accounting theory and

analysis. Chapel Hill: University of North Carolina.

SKIFT. 2018. Qantas Airline group. (Online). Available at:

https://skift.com/2017/02/23/qantas-profit-dips-7-5-percent-amid-overseas-competition/

(Accessed as on 21st April 2018).

The wall street Journal. 2018. Qantas Airline group. (Online). Available at:

http://quotes.wsj.com/AU/XASX/QAN/financials/annual/balance-sheet (Accessed as on 21st

April 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business Analysis and Valuation 14

Appendix:

QANTAS AIRWAYS LTD (QAN) CashFlowFlag INCOME STATEMENT

Fiscal year ends in June. AUD in millions

except per share data.

2013-

06

2017-

06 Changes

Revenue 15577 15680 0.66%

Cost of revenue 7220 6475 -10.32%

Gross profit 8357 9205 10.15%

Operating expenses

Sales, General and administrative 5216 5281 1.25%

Other operating expenses 3262 2931 -10.15%

Total operating expenses 8478 8212 -3.14%

Operating income -121 993 -920.66%

Interest Expense 296 235 -20.61%

Other income (expense) 434 423 -2.53%

Income before income taxes 17 1181 6847.06%

Provision for income taxes 11 328 2881.82%

Net income from continuing ops 6 853 14116.67%

Other -1 -1 0.00%

Net income 5 852 16940.00%

Net income available to common shareholders 5 852 16940.00%

Earnings per share

Basic 0 0.46

Diluted 0 0.46

Weighted average shares outstanding

Basic 2112 1853 -12.26%

Diluted 2112 1853 -12.26%

EBITDA 1763 2798 58.71%

QANTAS AIRWAYS LTD (QAN) CashFlowFlag BALANCE

SHEET

Fiscal year ends in June. AUD in

millions except per share data.

2013-

06

2017-

06 Changes

Assets

Current assets

Cash

Cash and cash equivalents 2829 1775 -37.26%

Short-term investments 180 100 -44.44%

Total cash 3009 1875 -37.69%

Receivables 1436 784 -45.40%

Inventories 364 351 -3.57%

Prepaid expenses 102

-

100.00%

Appendix:

QANTAS AIRWAYS LTD (QAN) CashFlowFlag INCOME STATEMENT

Fiscal year ends in June. AUD in millions

except per share data.

2013-

06

2017-

06 Changes

Revenue 15577 15680 0.66%

Cost of revenue 7220 6475 -10.32%

Gross profit 8357 9205 10.15%

Operating expenses

Sales, General and administrative 5216 5281 1.25%

Other operating expenses 3262 2931 -10.15%

Total operating expenses 8478 8212 -3.14%

Operating income -121 993 -920.66%

Interest Expense 296 235 -20.61%

Other income (expense) 434 423 -2.53%

Income before income taxes 17 1181 6847.06%

Provision for income taxes 11 328 2881.82%

Net income from continuing ops 6 853 14116.67%

Other -1 -1 0.00%

Net income 5 852 16940.00%

Net income available to common shareholders 5 852 16940.00%

Earnings per share

Basic 0 0.46

Diluted 0 0.46

Weighted average shares outstanding

Basic 2112 1853 -12.26%

Diluted 2112 1853 -12.26%

EBITDA 1763 2798 58.71%

QANTAS AIRWAYS LTD (QAN) CashFlowFlag BALANCE

SHEET

Fiscal year ends in June. AUD in

millions except per share data.

2013-

06

2017-

06 Changes

Assets

Current assets

Cash

Cash and cash equivalents 2829 1775 -37.26%

Short-term investments 180 100 -44.44%

Total cash 3009 1875 -37.69%

Receivables 1436 784 -45.40%

Inventories 364 351 -3.57%

Prepaid expenses 102

-

100.00%

Business Analysis and Valuation 15

Other current assets 334 109 -67.37%

Total current assets 5245 3119 -40.53%

Non-current assets

Property, plant and equipment

Gross property, plant and equipment 23944 25940 8.34%

Accumulated Depreciation

-

10117

-

13687 35.29%

Net property, plant and equipment 13827 12253 -11.38%

Equity and other investments 217 257 18.43%

Goodwill 197 207 5.08%

Intangible assets 517 818 58.22%

Deferred income taxes

Other long-term assets 197 567 187.82%

Total non-current assets 14955 14102 -5.70%

Total assets 20200 17221 -14.75%

Liabilities and stockholders' equity

Liabilities

Current liabilities

Short-term debt 592 330 -44.26%

Capital leases 243 103 -57.61%

Accounts payable 655 2067 215.57%

Deferred revenues 3032 3685 21.54%

Other current liabilities 1848 910 -50.76%

Total current liabilities 6370 7095 11.38%

Non-current liabilities

Long-term debt 4612 3144 -31.83%

Capital leases 633 1261 99.21%

Deferred taxes liabilities 673 353 -47.55%

Other long-term liabilities 1963 1831 -6.72%

Total non-current liabilities 7881 6589 -16.39%

Total liabilities 14251 13684 -3.98%

Stockholders' equity

Common stock 4650 3053 -34.34%

Retained earnings 1171 472 -59.69%

Accumulated other comprehensive

income 128 12 -90.63%

Total stockholders' equity 5949 3537 -40.54%

Total liabilities and stockholders'

equity 20200 17221 -14.75%

Other current assets 334 109 -67.37%

Total current assets 5245 3119 -40.53%

Non-current assets

Property, plant and equipment

Gross property, plant and equipment 23944 25940 8.34%

Accumulated Depreciation

-

10117

-

13687 35.29%

Net property, plant and equipment 13827 12253 -11.38%

Equity and other investments 217 257 18.43%

Goodwill 197 207 5.08%

Intangible assets 517 818 58.22%

Deferred income taxes

Other long-term assets 197 567 187.82%

Total non-current assets 14955 14102 -5.70%

Total assets 20200 17221 -14.75%

Liabilities and stockholders' equity

Liabilities

Current liabilities

Short-term debt 592 330 -44.26%

Capital leases 243 103 -57.61%

Accounts payable 655 2067 215.57%

Deferred revenues 3032 3685 21.54%

Other current liabilities 1848 910 -50.76%

Total current liabilities 6370 7095 11.38%

Non-current liabilities

Long-term debt 4612 3144 -31.83%

Capital leases 633 1261 99.21%

Deferred taxes liabilities 673 353 -47.55%

Other long-term liabilities 1963 1831 -6.72%

Total non-current liabilities 7881 6589 -16.39%

Total liabilities 14251 13684 -3.98%

Stockholders' equity

Common stock 4650 3053 -34.34%

Retained earnings 1171 472 -59.69%

Accumulated other comprehensive

income 128 12 -90.63%

Total stockholders' equity 5949 3537 -40.54%

Total liabilities and stockholders'

equity 20200 17221 -14.75%

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.