Statistical Analysis and Investment Recommendation: BA vs GD Stocks

VerifiedAdded on 2023/04/20

|12

|4094

|443

Project

AI Summary

This assignment presents a statistical analysis comparing the stock performance of Boeing (BA) and General Dynamics (GD) from March 2012 to March 2017. The analysis utilizes historical monthly data, including S&P 500 returns and US 10-year Treasury yields, to calculate percentage returns and assess market volatility. The study employs MS Excel for data processing and visualization, including area charts to illustrate market returns. Statistical tests, such as the Jarque-Bera test, are used to evaluate the normality of market returns for both stocks, revealing that GD stock returns were nearly normal. The project also examines the risk-return relationship, calculating coefficients of variation to rank the stocks based on risk. Hypothesis testing, including one-sample t-tests and F-tests, is conducted to compare the average market returns and risks between the two stocks. The analysis concludes with investment recommendations based on the statistical findings, suggesting that GD stock was the less risky investment choice during the period of analysis due to its lower volatility and competitive returns.

Statistical Analysis and Comparison between Stock Prices of the

Boeing Company and the General Dynamics

Assignment 2: Which stock should be invested in?

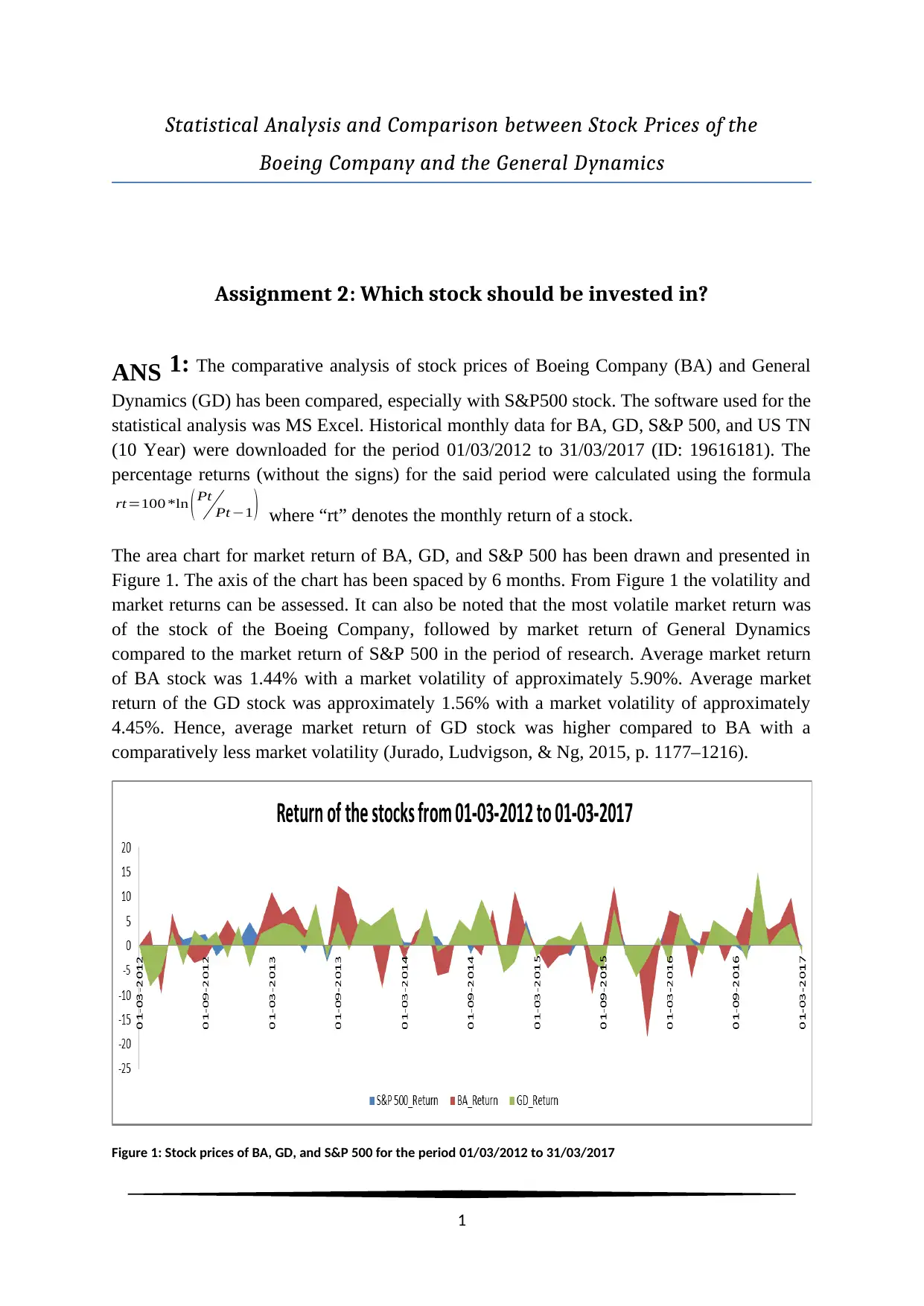

ANS 1: The comparative analysis of stock prices of Boeing Company (BA) and General

Dynamics (GD) has been compared, especially with S&P500 stock. The software used for the

statistical analysis was MS Excel. Historical monthly data for BA, GD, S&P 500, and US TN

(10 Year) were downloaded for the period 01/03/2012 to 31/03/2017 (ID: 19616181). The

percentage returns (without the signs) for the said period were calculated using the formula

rt=100 *ln ( Pt

Pt −1 ) where “rt” denotes the monthly return of a stock.

The area chart for market return of BA, GD, and S&P 500 has been drawn and presented in

Figure 1. The axis of the chart has been spaced by 6 months. From Figure 1 the volatility and

market returns can be assessed. It can also be noted that the most volatile market return was

of the stock of the Boeing Company, followed by market return of General Dynamics

compared to the market return of S&P 500 in the period of research. Average market return

of BA stock was 1.44% with a market volatility of approximately 5.90%. Average market

return of the GD stock was approximately 1.56% with a market volatility of approximately

4.45%. Hence, average market return of GD stock was higher compared to BA with a

comparatively less market volatility (Jurado, Ludvigson, & Ng, 2015, p. 1177–1216).

Figure 1: Stock prices of BA, GD, and S&P 500 for the period 01/03/2012 to 31/03/2017

1

Boeing Company and the General Dynamics

Assignment 2: Which stock should be invested in?

ANS 1: The comparative analysis of stock prices of Boeing Company (BA) and General

Dynamics (GD) has been compared, especially with S&P500 stock. The software used for the

statistical analysis was MS Excel. Historical monthly data for BA, GD, S&P 500, and US TN

(10 Year) were downloaded for the period 01/03/2012 to 31/03/2017 (ID: 19616181). The

percentage returns (without the signs) for the said period were calculated using the formula

rt=100 *ln ( Pt

Pt −1 ) where “rt” denotes the monthly return of a stock.

The area chart for market return of BA, GD, and S&P 500 has been drawn and presented in

Figure 1. The axis of the chart has been spaced by 6 months. From Figure 1 the volatility and

market returns can be assessed. It can also be noted that the most volatile market return was

of the stock of the Boeing Company, followed by market return of General Dynamics

compared to the market return of S&P 500 in the period of research. Average market return

of BA stock was 1.44% with a market volatility of approximately 5.90%. Average market

return of the GD stock was approximately 1.56% with a market volatility of approximately

4.45%. Hence, average market return of GD stock was higher compared to BA with a

comparatively less market volatility (Jurado, Ludvigson, & Ng, 2015, p. 1177–1216).

Figure 1: Stock prices of BA, GD, and S&P 500 for the period 01/03/2012 to 31/03/2017

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

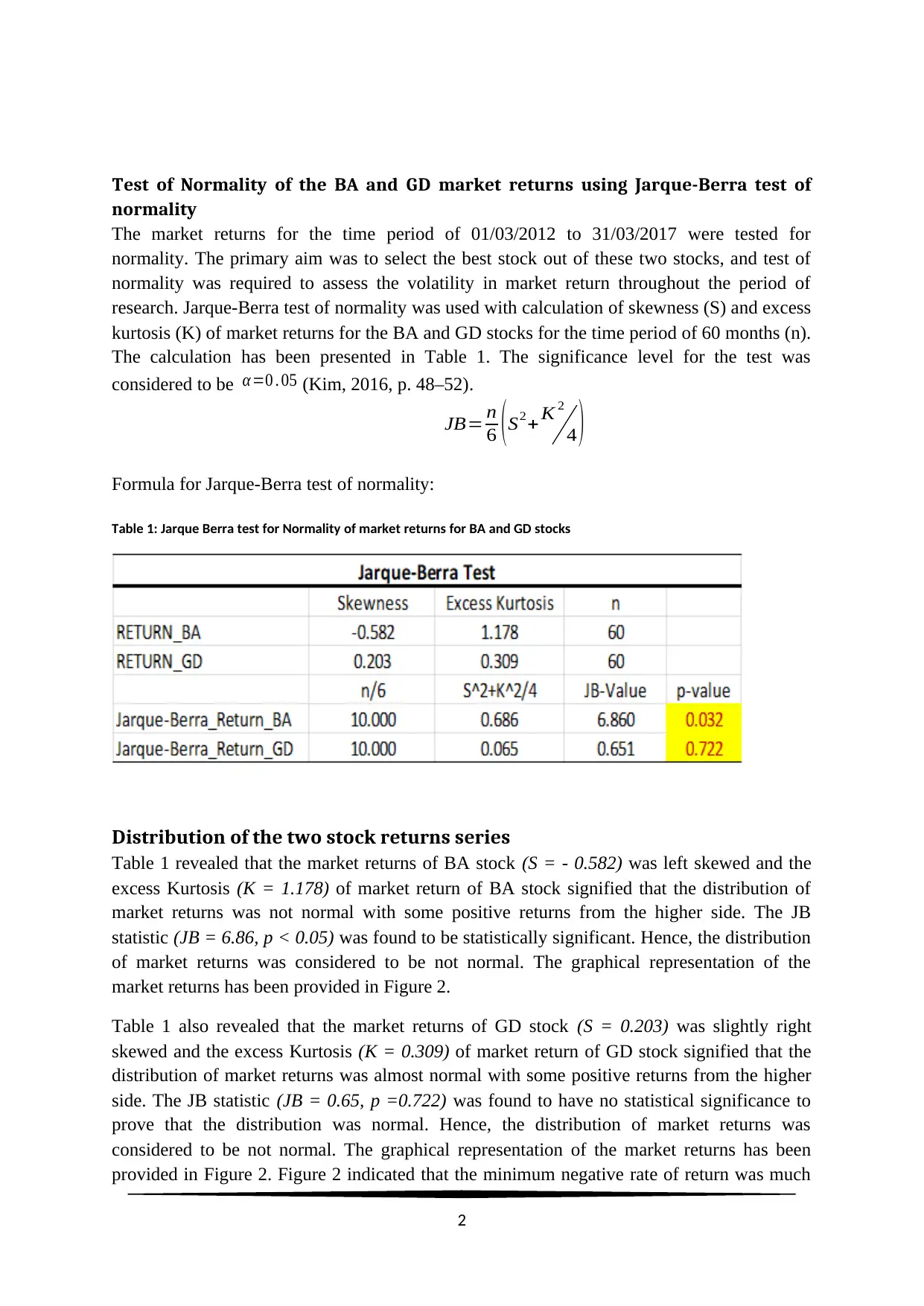

Test of Normality of the BA and GD market returns using Jarque-Berra test of

normality

The market returns for the time period of 01/03/2012 to 31/03/2017 were tested for

normality. The primary aim was to select the best stock out of these two stocks, and test of

normality was required to assess the volatility in market return throughout the period of

research. Jarque-Berra test of normality was used with calculation of skewness (S) and excess

kurtosis (K) of market returns for the BA and GD stocks for the time period of 60 months (n).

The calculation has been presented in Table 1. The significance level for the test was

considered to be α =0 . 05 (Kim, 2016, p. 48–52).

Formula for Jarque-Berra test of normality:

JB= n

6 ( S2+ K 2

4 )

Table 1: Jarque Berra test for Normality of market returns for BA and GD stocks

Distribution of the two stock returns series

Table 1 revealed that the market returns of BA stock (S = - 0.582) was left skewed and the

excess Kurtosis (K = 1.178) of market return of BA stock signified that the distribution of

market returns was not normal with some positive returns from the higher side. The JB

statistic (JB = 6.86, p < 0.05) was found to be statistically significant. Hence, the distribution

of market returns was considered to be not normal. The graphical representation of the

market returns has been provided in Figure 2.

Table 1 also revealed that the market returns of GD stock (S = 0.203) was slightly right

skewed and the excess Kurtosis (K = 0.309) of market return of GD stock signified that the

distribution of market returns was almost normal with some positive returns from the higher

side. The JB statistic (JB = 0.65, p =0.722) was found to have no statistical significance to

prove that the distribution was normal. Hence, the distribution of market returns was

considered to be not normal. The graphical representation of the market returns has been

provided in Figure 2. Figure 2 indicated that the minimum negative rate of return was much

2

normality

The market returns for the time period of 01/03/2012 to 31/03/2017 were tested for

normality. The primary aim was to select the best stock out of these two stocks, and test of

normality was required to assess the volatility in market return throughout the period of

research. Jarque-Berra test of normality was used with calculation of skewness (S) and excess

kurtosis (K) of market returns for the BA and GD stocks for the time period of 60 months (n).

The calculation has been presented in Table 1. The significance level for the test was

considered to be α =0 . 05 (Kim, 2016, p. 48–52).

Formula for Jarque-Berra test of normality:

JB= n

6 ( S2+ K 2

4 )

Table 1: Jarque Berra test for Normality of market returns for BA and GD stocks

Distribution of the two stock returns series

Table 1 revealed that the market returns of BA stock (S = - 0.582) was left skewed and the

excess Kurtosis (K = 1.178) of market return of BA stock signified that the distribution of

market returns was not normal with some positive returns from the higher side. The JB

statistic (JB = 6.86, p < 0.05) was found to be statistically significant. Hence, the distribution

of market returns was considered to be not normal. The graphical representation of the

market returns has been provided in Figure 2.

Table 1 also revealed that the market returns of GD stock (S = 0.203) was slightly right

skewed and the excess Kurtosis (K = 0.309) of market return of GD stock signified that the

distribution of market returns was almost normal with some positive returns from the higher

side. The JB statistic (JB = 0.65, p =0.722) was found to have no statistical significance to

prove that the distribution was normal. Hence, the distribution of market returns was

considered to be not normal. The graphical representation of the market returns has been

provided in Figure 2. Figure 2 indicated that the minimum negative rate of return was much

2

higher for BA stock, whereas GD gave positive return maximum better compared to BA

stock.

Figure 2: Histogram of market returns of BA and GD stocks

Risk and Average Return Relationship

The comparison of market returns of GD and BA stocks with respect to their statistical

distributions was also analysed by the risk and average return relationship. The comparative

analysis has been presented in Table 2.

Table 2: Risk-Return relationship of market returns of GD and BA stocks

Table 2 revealed that average market return of the stock of Boeing Company was the

preeminent compared to the stocks of General Dynamic and S&P500. Investment in this

stock looked very lucrative considering the average return in the time period of 01/03/2012 to

31/03/2017. But the risk analysis revealed that volatility due to presence of few high market

returns as well as few extreme low return up to -18.53% was the greatest among the three

stocks. High market volatility always creates uncertainty in the mind of investor. Those who

like to take risk for higher returns may opt for the Boeing Company stock. But, considering

the higher average return and comparative low market risk stock of the General Dynamic was

the prudent choice as an investor. The coefficient of variation for all the three stocks were

calculated as statistical measure between average return and market risk. Ranking the funds

based on coefficient of variation revealed that BA was the most risky stock, followed by

S&P500. GD stock was the least risky to invest with a risk profile better than risk profile of

BA and the overall market scenario (Read, & Vogel, 2015, p. 6381–6398).

3

stock.

Figure 2: Histogram of market returns of BA and GD stocks

Risk and Average Return Relationship

The comparison of market returns of GD and BA stocks with respect to their statistical

distributions was also analysed by the risk and average return relationship. The comparative

analysis has been presented in Table 2.

Table 2: Risk-Return relationship of market returns of GD and BA stocks

Table 2 revealed that average market return of the stock of Boeing Company was the

preeminent compared to the stocks of General Dynamic and S&P500. Investment in this

stock looked very lucrative considering the average return in the time period of 01/03/2012 to

31/03/2017. But the risk analysis revealed that volatility due to presence of few high market

returns as well as few extreme low return up to -18.53% was the greatest among the three

stocks. High market volatility always creates uncertainty in the mind of investor. Those who

like to take risk for higher returns may opt for the Boeing Company stock. But, considering

the higher average return and comparative low market risk stock of the General Dynamic was

the prudent choice as an investor. The coefficient of variation for all the three stocks were

calculated as statistical measure between average return and market risk. Ranking the funds

based on coefficient of variation revealed that BA was the most risky stock, followed by

S&P500. GD stock was the least risky to invest with a risk profile better than risk profile of

BA and the overall market scenario (Read, & Vogel, 2015, p. 6381–6398).

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

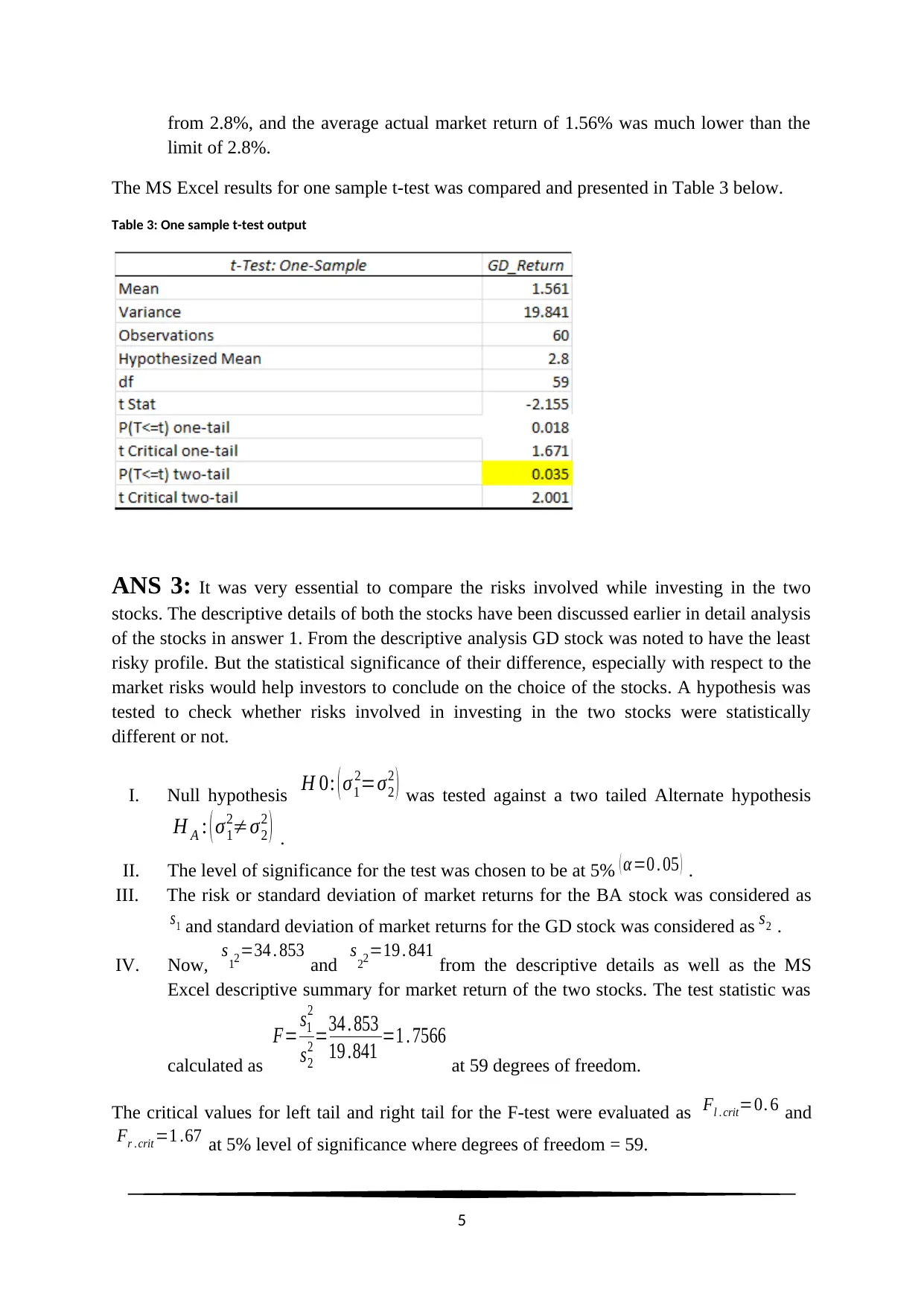

ANS 2: Reason and Choice of the test statistic to perform hypothesis testing:

Choice for the test statistic was based on the distribution and information about the

population and the sample data. The sample of calculated market returns for the period

01/03/2012 to 31/03/2017 in case of the GD stock was large enough (n >30) to assume that

the market returns would follow a standard normal distribution ( N ~ ( 0,1 ) ) . The argument

behind the assumption was obtained from Central Limit Theorem (CLT). Again, information

about the population regarding the market risk and average return were not available for the

research. Hence, a student’s t-distribution with 59 degrees of freedom was considered as the

appropriate choice as the test statistic.

To test the hypothesis that whether the average market return of the GD stock is different

from μ= 2.8% or not, a hypothesis testing for one-sample mean at 5% level of significance

was conducted.

I. Null hypothesis: H 0: ( μ=2 .8 ) was tested against the two tailed Alternate hypothesis

H A : ( μ≠2 . 8 ) .

II. Significance level of the test was considered to be at α=0 . 05 or 5%.

III. The average return of the GD stock for the period 01/03/2012 to 31/03/2017 was

considered normally distributed and the test statistic was calculated.

IV. Here, x

¿

=∑ xi

n =93 .653

60 =1 .561 and the risk or standard deviation was calculated as

s= √ ∑ ( xi−x

¿

)

2

n =4 . 454 .

The test statistic was

t= x

¿

−μ

s / √ n ~ N ( 0,1 ) and the statistic was calculated as,

t obs= x

¿

−μ

s / √ n =1 .561−2. 8

4 . 454 / √ 60 =−1 .239

0 .575 =−2. 155

Now critical value of the t-statistic at 5% level of significance for two tailed test is

t crit =1. 96 at 59 degrees of freedom. It was observed that tobs=−2 .155< tcrit =−1 . 96

on the left tail at 5% level. The value of the observed or calculated t-value falls in the

critical region in the left tail. The significance value or p-value was evaluated as p-

value = P ( t<−tobs ) + P¿ ¿

V. Hence, based on the statistical evidence the null hypothesis was rejected and it was

concluded that the average market return from GD stock was considerably different

4

Choice for the test statistic was based on the distribution and information about the

population and the sample data. The sample of calculated market returns for the period

01/03/2012 to 31/03/2017 in case of the GD stock was large enough (n >30) to assume that

the market returns would follow a standard normal distribution ( N ~ ( 0,1 ) ) . The argument

behind the assumption was obtained from Central Limit Theorem (CLT). Again, information

about the population regarding the market risk and average return were not available for the

research. Hence, a student’s t-distribution with 59 degrees of freedom was considered as the

appropriate choice as the test statistic.

To test the hypothesis that whether the average market return of the GD stock is different

from μ= 2.8% or not, a hypothesis testing for one-sample mean at 5% level of significance

was conducted.

I. Null hypothesis: H 0: ( μ=2 .8 ) was tested against the two tailed Alternate hypothesis

H A : ( μ≠2 . 8 ) .

II. Significance level of the test was considered to be at α=0 . 05 or 5%.

III. The average return of the GD stock for the period 01/03/2012 to 31/03/2017 was

considered normally distributed and the test statistic was calculated.

IV. Here, x

¿

=∑ xi

n =93 .653

60 =1 .561 and the risk or standard deviation was calculated as

s= √ ∑ ( xi−x

¿

)

2

n =4 . 454 .

The test statistic was

t= x

¿

−μ

s / √ n ~ N ( 0,1 ) and the statistic was calculated as,

t obs= x

¿

−μ

s / √ n =1 .561−2. 8

4 . 454 / √ 60 =−1 .239

0 .575 =−2. 155

Now critical value of the t-statistic at 5% level of significance for two tailed test is

t crit =1. 96 at 59 degrees of freedom. It was observed that tobs=−2 .155< tcrit =−1 . 96

on the left tail at 5% level. The value of the observed or calculated t-value falls in the

critical region in the left tail. The significance value or p-value was evaluated as p-

value = P ( t<−tobs ) + P¿ ¿

V. Hence, based on the statistical evidence the null hypothesis was rejected and it was

concluded that the average market return from GD stock was considerably different

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

from 2.8%, and the average actual market return of 1.56% was much lower than the

limit of 2.8%.

The MS Excel results for one sample t-test was compared and presented in Table 3 below.

Table 3: One sample t-test output

ANS 3: It was very essential to compare the risks involved while investing in the two

stocks. The descriptive details of both the stocks have been discussed earlier in detail analysis

of the stocks in answer 1. From the descriptive analysis GD stock was noted to have the least

risky profile. But the statistical significance of their difference, especially with respect to the

market risks would help investors to conclude on the choice of the stocks. A hypothesis was

tested to check whether risks involved in investing in the two stocks were statistically

different or not.

I. Null hypothesis H 0: ( σ1

2=σ2

2 ) was tested against a two tailed Alternate hypothesis

H A : ( σ1

2≠σ2

2 ) .

II. The level of significance for the test was chosen to be at 5% ( α=0 . 05 ) .

III. The risk or standard deviation of market returns for the BA stock was considered as

s1 and standard deviation of market returns for the GD stock was considered as s2 .

IV. Now, s12=34 . 853 and s22=19 . 841 from the descriptive details as well as the MS

Excel descriptive summary for market return of the two stocks. The test statistic was

calculated as

F= s1

2

s2

2 =34 . 853

19 .841 =1 . 7566

at 59 degrees of freedom.

The critical values for left tail and right tail for the F-test were evaluated as Fl . crit=0. 6 and

Fr . crit =1 .67 at 5% level of significance where degrees of freedom = 59.

5

limit of 2.8%.

The MS Excel results for one sample t-test was compared and presented in Table 3 below.

Table 3: One sample t-test output

ANS 3: It was very essential to compare the risks involved while investing in the two

stocks. The descriptive details of both the stocks have been discussed earlier in detail analysis

of the stocks in answer 1. From the descriptive analysis GD stock was noted to have the least

risky profile. But the statistical significance of their difference, especially with respect to the

market risks would help investors to conclude on the choice of the stocks. A hypothesis was

tested to check whether risks involved in investing in the two stocks were statistically

different or not.

I. Null hypothesis H 0: ( σ1

2=σ2

2 ) was tested against a two tailed Alternate hypothesis

H A : ( σ1

2≠σ2

2 ) .

II. The level of significance for the test was chosen to be at 5% ( α=0 . 05 ) .

III. The risk or standard deviation of market returns for the BA stock was considered as

s1 and standard deviation of market returns for the GD stock was considered as s2 .

IV. Now, s12=34 . 853 and s22=19 . 841 from the descriptive details as well as the MS

Excel descriptive summary for market return of the two stocks. The test statistic was

calculated as

F= s1

2

s2

2 =34 . 853

19 .841 =1 . 7566

at 59 degrees of freedom.

The critical values for left tail and right tail for the F-test were evaluated as Fl . crit=0. 6 and

Fr . crit =1 .67 at 5% level of significance where degrees of freedom = 59.

5

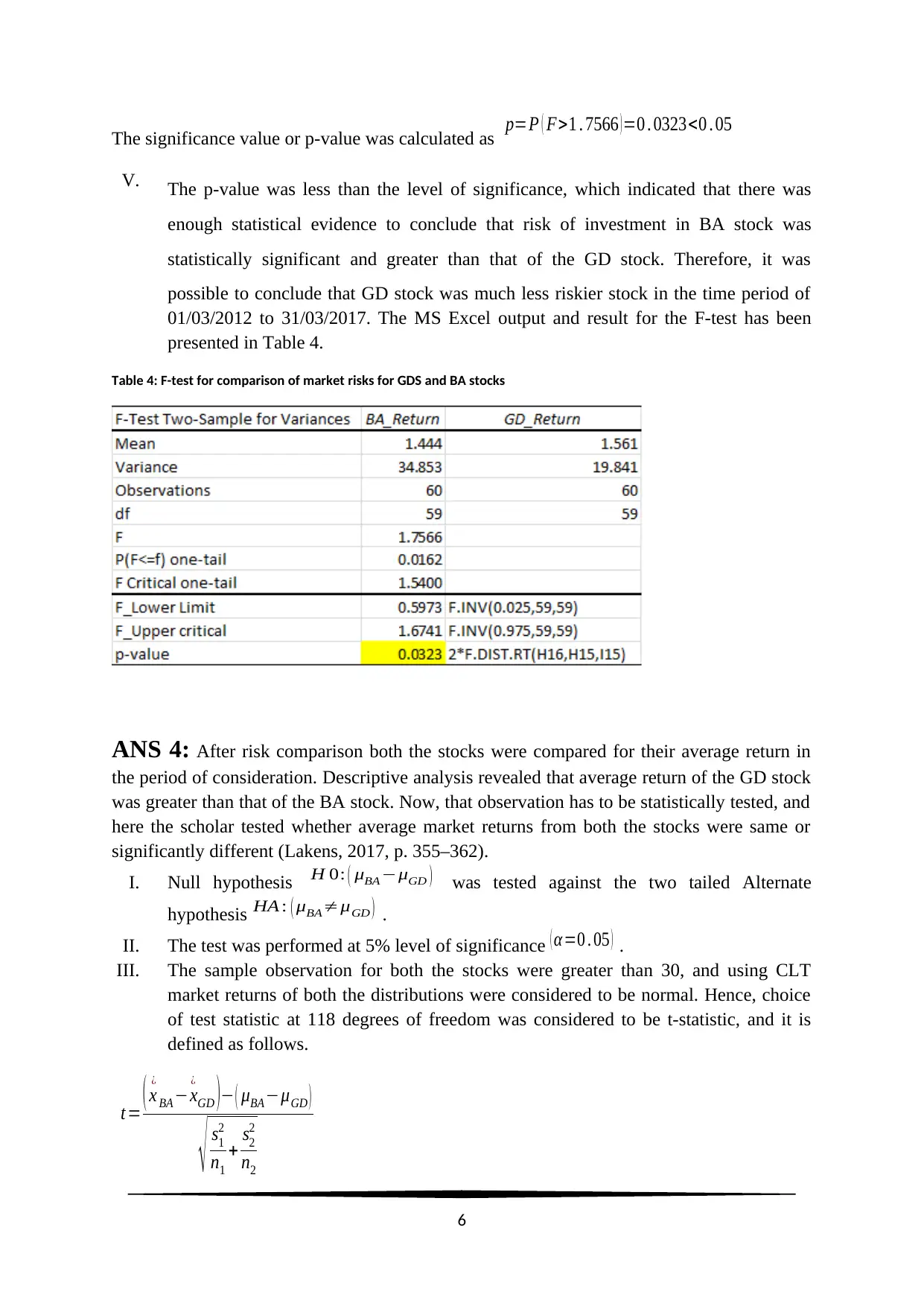

The significance value or p-value was calculated as p=P ( F>1 . 7566 ) =0 . 0323<0 . 05

V. The p-value was less than the level of significance, which indicated that there was

enough statistical evidence to conclude that risk of investment in BA stock was

statistically significant and greater than that of the GD stock. Therefore, it was

possible to conclude that GD stock was much less riskier stock in the time period of

01/03/2012 to 31/03/2017. The MS Excel output and result for the F-test has been

presented in Table 4.

Table 4: F-test for comparison of market risks for GDS and BA stocks

ANS 4: After risk comparison both the stocks were compared for their average return in

the period of consideration. Descriptive analysis revealed that average return of the GD stock

was greater than that of the BA stock. Now, that observation has to be statistically tested, and

here the scholar tested whether average market returns from both the stocks were same or

significantly different (Lakens, 2017, p. 355–362).

I. Null hypothesis H 0: ( μBA−μGD ) was tested against the two tailed Alternate

hypothesis HA : ( μBA≠μGD ) .

II. The test was performed at 5% level of significance ( α=0 . 05 ) .

III. The sample observation for both the stocks were greater than 30, and using CLT

market returns of both the distributions were considered to be normal. Hence, choice

of test statistic at 118 degrees of freedom was considered to be t-statistic, and it is

defined as follows.

t = ( x

¿

BA −x

¿

GD )− ( μBA−μGD )

√ s1

2

n1

+ s2

2

n2

6

V. The p-value was less than the level of significance, which indicated that there was

enough statistical evidence to conclude that risk of investment in BA stock was

statistically significant and greater than that of the GD stock. Therefore, it was

possible to conclude that GD stock was much less riskier stock in the time period of

01/03/2012 to 31/03/2017. The MS Excel output and result for the F-test has been

presented in Table 4.

Table 4: F-test for comparison of market risks for GDS and BA stocks

ANS 4: After risk comparison both the stocks were compared for their average return in

the period of consideration. Descriptive analysis revealed that average return of the GD stock

was greater than that of the BA stock. Now, that observation has to be statistically tested, and

here the scholar tested whether average market returns from both the stocks were same or

significantly different (Lakens, 2017, p. 355–362).

I. Null hypothesis H 0: ( μBA−μGD ) was tested against the two tailed Alternate

hypothesis HA : ( μBA≠μGD ) .

II. The test was performed at 5% level of significance ( α=0 . 05 ) .

III. The sample observation for both the stocks were greater than 30, and using CLT

market returns of both the distributions were considered to be normal. Hence, choice

of test statistic at 118 degrees of freedom was considered to be t-statistic, and it is

defined as follows.

t = ( x

¿

BA −x

¿

GD )− ( μBA−μGD )

√ s1

2

n1

+ s2

2

n2

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

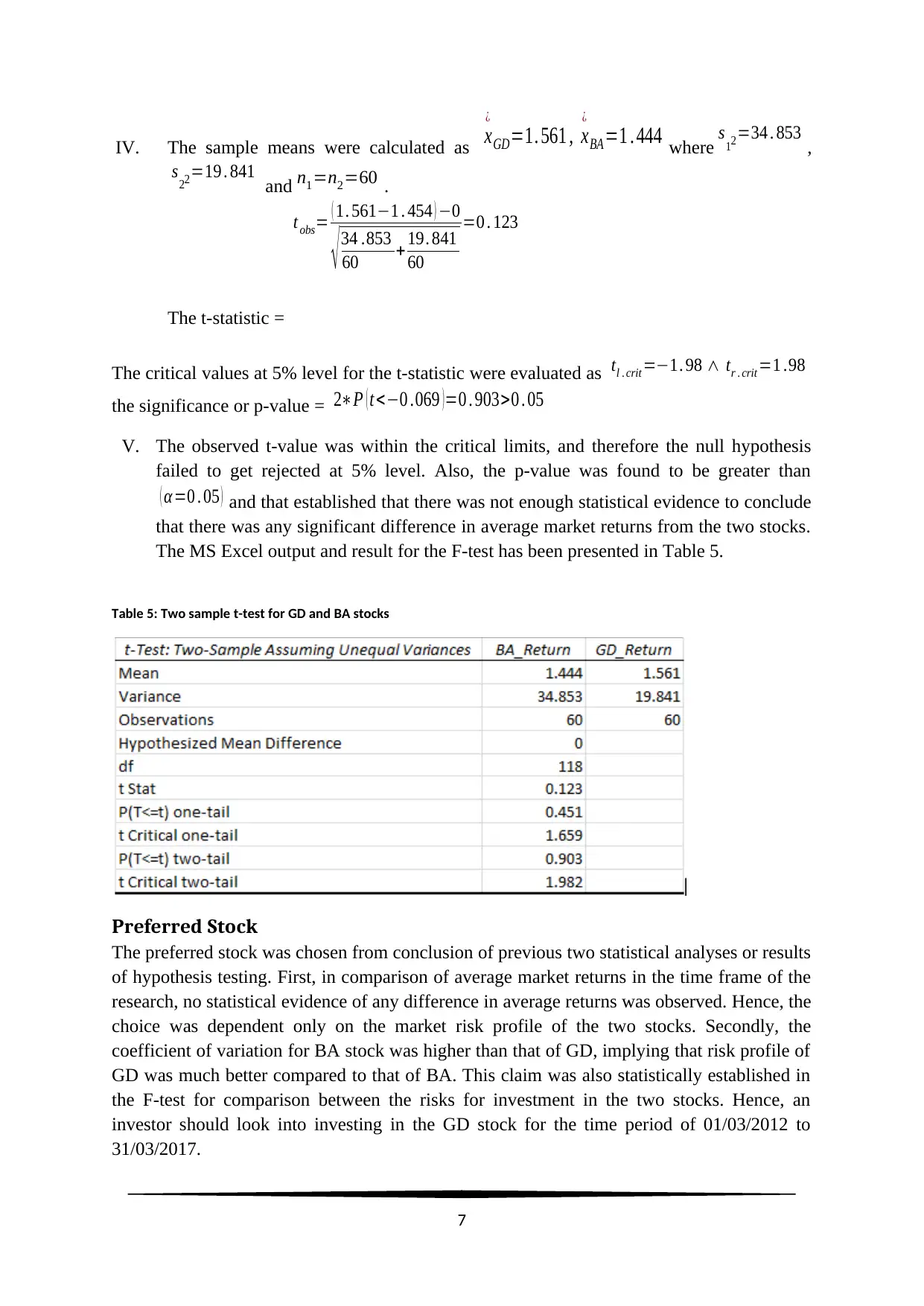

IV. The sample means were calculated as x

¿

GD=1. 561 , x

¿

BA =1 . 444 where s12=34 . 853 ,

s22=19 . 841 and n1=n2=60 .

The t-statistic =

tobs= ( 1. 561−1 . 454 ) −0

√ 34 .853

60 + 19. 841

60

=0 . 123

The critical values at 5% level for the t-statistic were evaluated as tl . crit =−1. 98 ∧ tr . crit =1 .98

the significance or p-value = 2∗P ( t<−0 .069 ) =0 . 903>0 . 05

V. The observed t-value was within the critical limits, and therefore the null hypothesis

failed to get rejected at 5% level. Also, the p-value was found to be greater than

( α=0 . 05 ) and that established that there was not enough statistical evidence to conclude

that there was any significant difference in average market returns from the two stocks.

The MS Excel output and result for the F-test has been presented in Table 5.

Table 5: Two sample t-test for GD and BA stocks

Preferred Stock

The preferred stock was chosen from conclusion of previous two statistical analyses or results

of hypothesis testing. First, in comparison of average market returns in the time frame of the

research, no statistical evidence of any difference in average returns was observed. Hence, the

choice was dependent only on the market risk profile of the two stocks. Secondly, the

coefficient of variation for BA stock was higher than that of GD, implying that risk profile of

GD was much better compared to that of BA. This claim was also statistically established in

the F-test for comparison between the risks for investment in the two stocks. Hence, an

investor should look into investing in the GD stock for the time period of 01/03/2012 to

31/03/2017.

7

¿

GD=1. 561 , x

¿

BA =1 . 444 where s12=34 . 853 ,

s22=19 . 841 and n1=n2=60 .

The t-statistic =

tobs= ( 1. 561−1 . 454 ) −0

√ 34 .853

60 + 19. 841

60

=0 . 123

The critical values at 5% level for the t-statistic were evaluated as tl . crit =−1. 98 ∧ tr . crit =1 .98

the significance or p-value = 2∗P ( t<−0 .069 ) =0 . 903>0 . 05

V. The observed t-value was within the critical limits, and therefore the null hypothesis

failed to get rejected at 5% level. Also, the p-value was found to be greater than

( α=0 . 05 ) and that established that there was not enough statistical evidence to conclude

that there was any significant difference in average market returns from the two stocks.

The MS Excel output and result for the F-test has been presented in Table 5.

Table 5: Two sample t-test for GD and BA stocks

Preferred Stock

The preferred stock was chosen from conclusion of previous two statistical analyses or results

of hypothesis testing. First, in comparison of average market returns in the time frame of the

research, no statistical evidence of any difference in average returns was observed. Hence, the

choice was dependent only on the market risk profile of the two stocks. Secondly, the

coefficient of variation for BA stock was higher than that of GD, implying that risk profile of

GD was much better compared to that of BA. This claim was also statistically established in

the F-test for comparison between the risks for investment in the two stocks. Hence, an

investor should look into investing in the GD stock for the time period of 01/03/2012 to

31/03/2017.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

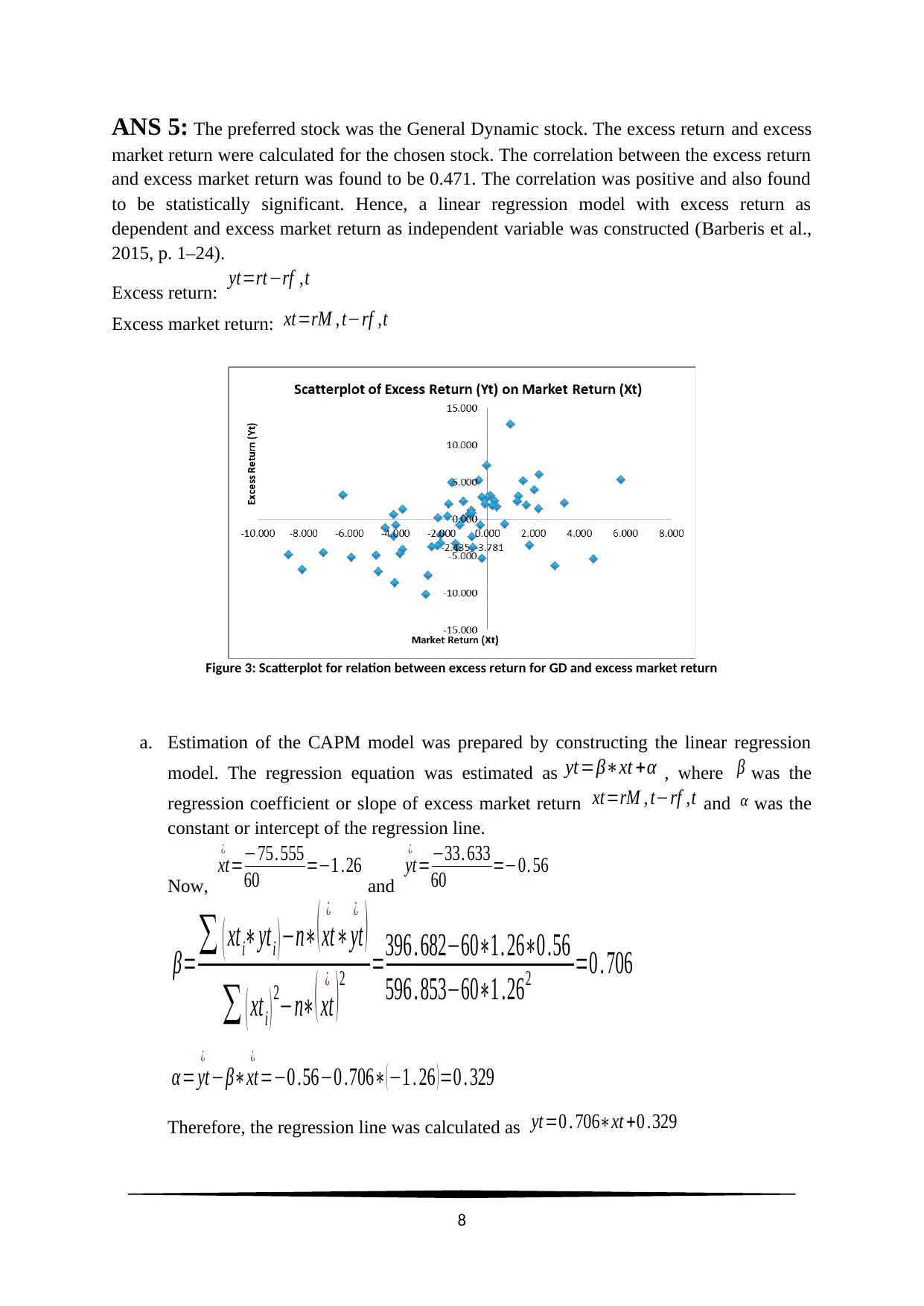

ANS 5: The preferred stock was the General Dynamic stock. The excess return and excess

market return were calculated for the chosen stock. The correlation between the excess return

and excess market return was found to be 0.471. The correlation was positive and also found

to be statistically significant. Hence, a linear regression model with excess return as

dependent and excess market return as independent variable was constructed (Barberis et al.,

2015, p. 1–24).

Excess return: yt=rt−rf ,t

Excess market return: xt=rM , t−rf ,t

Figure 3: Scatterplot for relation between excess return for GD and excess market return

a. Estimation of the CAPM model was prepared by constructing the linear regression

model. The regression equation was estimated as yt=β∗xt +α , where β was the

regression coefficient or slope of excess market return xt=rM , t−rf ,t and α was the

constant or intercept of the regression line.

Now,

xt

¿

=−75. 555

60 =−1 .26 and

yt

¿

=−33. 633

60 =−0. 56

β=∑ ( xti∗yti ) −n∗( xt

¿

∗yt

¿

)

∑ ( xti ) 2−n∗( xt

¿

) 2 =396 . 682−60∗1. 26∗0 .56

596 . 853−60∗1 .262 =0 . 706

α = yt

¿

−β∗xt

¿

=−0 .56−0 .706∗( −1 . 26 ) =0 . 329

Therefore, the regression line was calculated as yt=0 . 706∗xt +0 .329

8

market return were calculated for the chosen stock. The correlation between the excess return

and excess market return was found to be 0.471. The correlation was positive and also found

to be statistically significant. Hence, a linear regression model with excess return as

dependent and excess market return as independent variable was constructed (Barberis et al.,

2015, p. 1–24).

Excess return: yt=rt−rf ,t

Excess market return: xt=rM , t−rf ,t

Figure 3: Scatterplot for relation between excess return for GD and excess market return

a. Estimation of the CAPM model was prepared by constructing the linear regression

model. The regression equation was estimated as yt=β∗xt +α , where β was the

regression coefficient or slope of excess market return xt=rM , t−rf ,t and α was the

constant or intercept of the regression line.

Now,

xt

¿

=−75. 555

60 =−1 .26 and

yt

¿

=−33. 633

60 =−0. 56

β=∑ ( xti∗yti ) −n∗( xt

¿

∗yt

¿

)

∑ ( xti ) 2−n∗( xt

¿

) 2 =396 . 682−60∗1. 26∗0 .56

596 . 853−60∗1 .262 =0 . 706

α = yt

¿

−β∗xt

¿

=−0 .56−0 .706∗( −1 . 26 ) =0 . 329

Therefore, the regression line was calculated as yt=0 . 706∗xt +0 .329

8

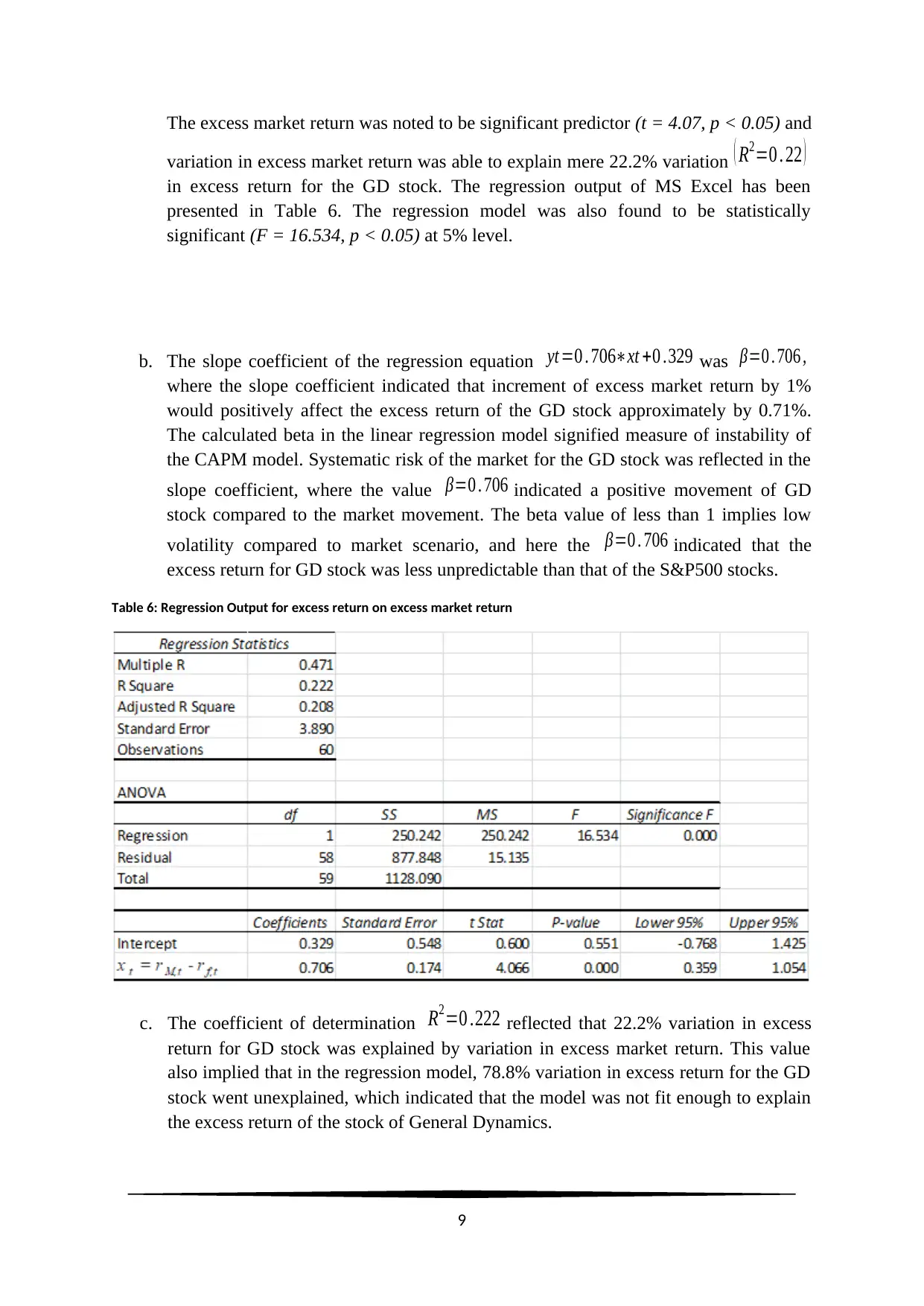

The excess market return was noted to be significant predictor (t = 4.07, p < 0.05) and

variation in excess market return was able to explain mere 22.2% variation ( R2=0 . 22 )

in excess return for the GD stock. The regression output of MS Excel has been

presented in Table 6. The regression model was also found to be statistically

significant (F = 16.534, p < 0.05) at 5% level.

b. The slope coefficient of the regression equation yt =0 . 706∗xt +0 .329 was β=0 . 706 ,

where the slope coefficient indicated that increment of excess market return by 1%

would positively affect the excess return of the GD stock approximately by 0.71%.

The calculated beta in the linear regression model signified measure of instability of

the CAPM model. Systematic risk of the market for the GD stock was reflected in the

slope coefficient, where the value β=0 . 706 indicated a positive movement of GD

stock compared to the market movement. The beta value of less than 1 implies low

volatility compared to market scenario, and here the β=0 . 706 indicated that the

excess return for GD stock was less unpredictable than that of the S&P500 stocks.

Table 6: Regression Output for excess return on excess market return

c. The coefficient of determination R2=0 .222 reflected that 22.2% variation in excess

return for GD stock was explained by variation in excess market return. This value

also implied that in the regression model, 78.8% variation in excess return for the GD

stock went unexplained, which indicated that the model was not fit enough to explain

the excess return of the stock of General Dynamics.

9

variation in excess market return was able to explain mere 22.2% variation ( R2=0 . 22 )

in excess return for the GD stock. The regression output of MS Excel has been

presented in Table 6. The regression model was also found to be statistically

significant (F = 16.534, p < 0.05) at 5% level.

b. The slope coefficient of the regression equation yt =0 . 706∗xt +0 .329 was β=0 . 706 ,

where the slope coefficient indicated that increment of excess market return by 1%

would positively affect the excess return of the GD stock approximately by 0.71%.

The calculated beta in the linear regression model signified measure of instability of

the CAPM model. Systematic risk of the market for the GD stock was reflected in the

slope coefficient, where the value β=0 . 706 indicated a positive movement of GD

stock compared to the market movement. The beta value of less than 1 implies low

volatility compared to market scenario, and here the β=0 . 706 indicated that the

excess return for GD stock was less unpredictable than that of the S&P500 stocks.

Table 6: Regression Output for excess return on excess market return

c. The coefficient of determination R2=0 .222 reflected that 22.2% variation in excess

return for GD stock was explained by variation in excess market return. This value

also implied that in the regression model, 78.8% variation in excess return for the GD

stock went unexplained, which indicated that the model was not fit enough to explain

the excess return of the stock of General Dynamics.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

d. The 95% confidence interval for the slope coefficient was calculated as

[ β

^¿±tcrit∗SE ]=[0 . 706±2 .0∗0 .174 ]=[ 0 .358 ,1 .054 ]

¿ . With 95% confidence it was

possible to surmise that slope coefficient of excess return for the GD stock would be

somewhere between 0.358 and 1.054. Therefore, it was possible to conclude that for

1% change in excess market return would impact the excess return of the GD stock

approximately by 0.36% to 1.05%. This reflected that GD stock was less volatile

compared to the market or at maximum volatile approximately at par with the market

returns.

ANS 6: In language of economics, a Neutral stock varies parallel with the overall market

(Bali, Hu, & Murray, 2017, p.1-5). In statistical language Neutral stock implies that the beta

of the regression model would be equal to 1. The risk profile of Neutral stock is same as that

of the market (S&P500). Now to test whether GD was a Neutral stock, a hypothesis testing

with a one-sample t-test was performed at 5% level of significance.

I. Null hypothesis H 0: ( β =1 ) was tested against a two tailed Alternate hypothesis

HA : ( β≠1 ) .

II. Significance level for the test was considered to be at α =5 % or 0 .05

III. The test statistic was considered as

t= β

^¿− β0

se ¿ ¿ ¿ ¿ ¿

IV. The calculated value of the statistic was t= 0. 706−1

0 . 1737 =−1. 691 at 58 degrees of

freedom. The significance or p-value was calculated as

p=2∗P (|t|>1 .691 ) =0 .096 >0 . 05

The 95% confidence interval was calculated as,

[ β

^¿±tcrit∗SE ]=[0 . 706±2 .0∗0 .174 ]=[ 0 .358 ,1 .054 ]

¿

V. As the p-value was greater than the level of significance ( α=0 . 05 ) , there was not

enough statistical evidence to reject the null hypothesis at 5% level of significance.

Also, the hypothetical value of the slope coefficient was found to be within the 95%

confidence interval. Hence, with 95% confidence it was possible to infer that the

estimated slope coefficient for the regression model will be approximately somewhere

within 0.358 and 1.054. Therefore, the null hypothesis could not be rejected and it

was concluded that the GD stock undeniably was a Neutral stock.

10

[ β

^¿±tcrit∗SE ]=[0 . 706±2 .0∗0 .174 ]=[ 0 .358 ,1 .054 ]

¿ . With 95% confidence it was

possible to surmise that slope coefficient of excess return for the GD stock would be

somewhere between 0.358 and 1.054. Therefore, it was possible to conclude that for

1% change in excess market return would impact the excess return of the GD stock

approximately by 0.36% to 1.05%. This reflected that GD stock was less volatile

compared to the market or at maximum volatile approximately at par with the market

returns.

ANS 6: In language of economics, a Neutral stock varies parallel with the overall market

(Bali, Hu, & Murray, 2017, p.1-5). In statistical language Neutral stock implies that the beta

of the regression model would be equal to 1. The risk profile of Neutral stock is same as that

of the market (S&P500). Now to test whether GD was a Neutral stock, a hypothesis testing

with a one-sample t-test was performed at 5% level of significance.

I. Null hypothesis H 0: ( β =1 ) was tested against a two tailed Alternate hypothesis

HA : ( β≠1 ) .

II. Significance level for the test was considered to be at α =5 % or 0 .05

III. The test statistic was considered as

t= β

^¿− β0

se ¿ ¿ ¿ ¿ ¿

IV. The calculated value of the statistic was t= 0. 706−1

0 . 1737 =−1. 691 at 58 degrees of

freedom. The significance or p-value was calculated as

p=2∗P (|t|>1 .691 ) =0 .096 >0 . 05

The 95% confidence interval was calculated as,

[ β

^¿±tcrit∗SE ]=[0 . 706±2 .0∗0 .174 ]=[ 0 .358 ,1 .054 ]

¿

V. As the p-value was greater than the level of significance ( α=0 . 05 ) , there was not

enough statistical evidence to reject the null hypothesis at 5% level of significance.

Also, the hypothetical value of the slope coefficient was found to be within the 95%

confidence interval. Hence, with 95% confidence it was possible to infer that the

estimated slope coefficient for the regression model will be approximately somewhere

within 0.358 and 1.054. Therefore, the null hypothesis could not be rejected and it

was concluded that the GD stock undeniably was a Neutral stock.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

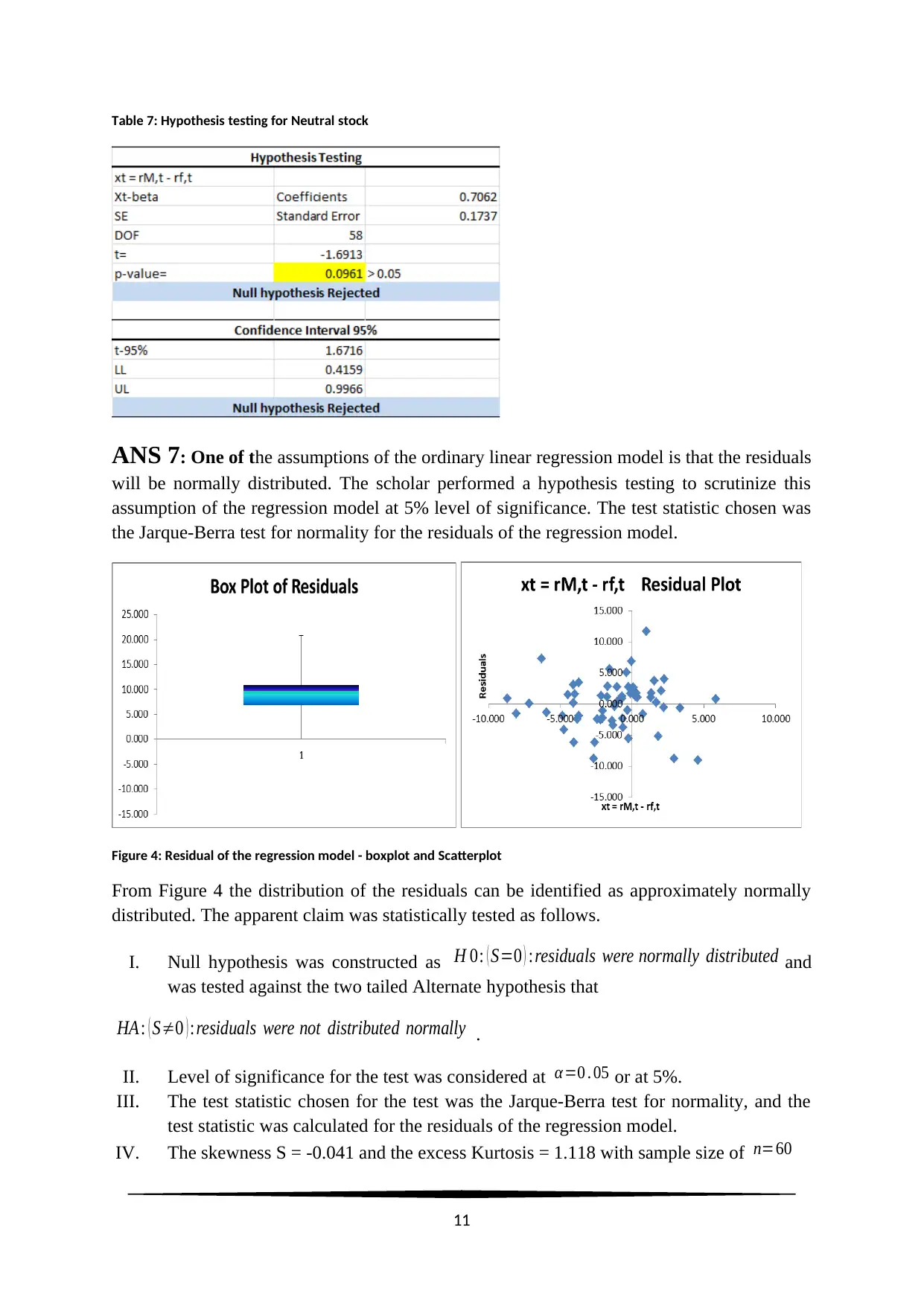

Table 7: Hypothesis testing for Neutral stock

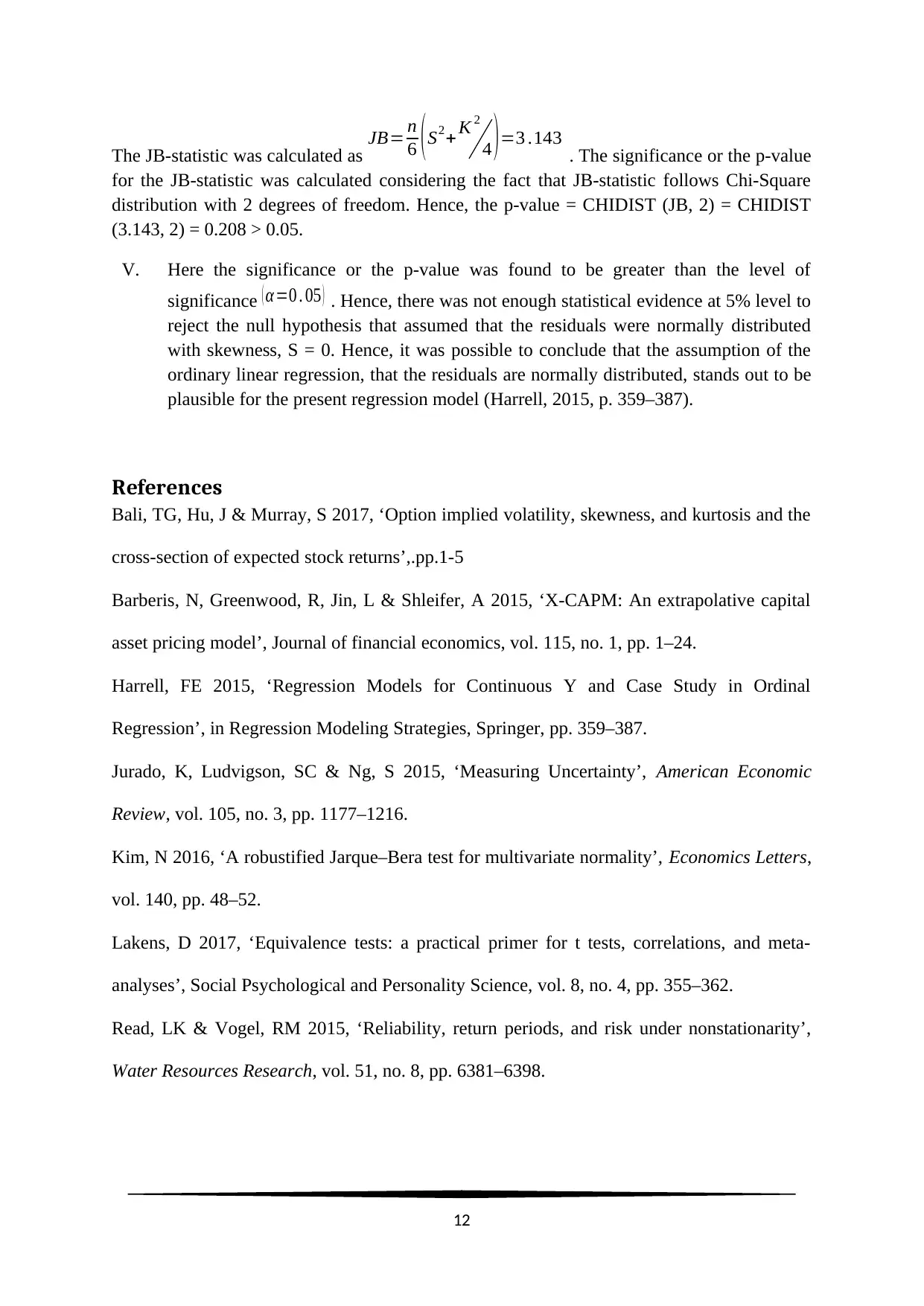

ANS 7: One of the assumptions of the ordinary linear regression model is that the residuals

will be normally distributed. The scholar performed a hypothesis testing to scrutinize this

assumption of the regression model at 5% level of significance. The test statistic chosen was

the Jarque-Berra test for normality for the residuals of the regression model.

Figure 4: Residual of the regression model - boxplot and Scatterplot

From Figure 4 the distribution of the residuals can be identified as approximately normally

distributed. The apparent claim was statistically tested as follows.

I. Null hypothesis was constructed as H 0: ( S=0 ) :residuals were normally distributed and

was tested against the two tailed Alternate hypothesis that

HA : ( S≠0 ) : residuals were not distributed normally .

II. Level of significance for the test was considered at α=0 . 05 or at 5%.

III. The test statistic chosen for the test was the Jarque-Berra test for normality, and the

test statistic was calculated for the residuals of the regression model.

IV. The skewness S = -0.041 and the excess Kurtosis = 1.118 with sample size of n=60

11

ANS 7: One of the assumptions of the ordinary linear regression model is that the residuals

will be normally distributed. The scholar performed a hypothesis testing to scrutinize this

assumption of the regression model at 5% level of significance. The test statistic chosen was

the Jarque-Berra test for normality for the residuals of the regression model.

Figure 4: Residual of the regression model - boxplot and Scatterplot

From Figure 4 the distribution of the residuals can be identified as approximately normally

distributed. The apparent claim was statistically tested as follows.

I. Null hypothesis was constructed as H 0: ( S=0 ) :residuals were normally distributed and

was tested against the two tailed Alternate hypothesis that

HA : ( S≠0 ) : residuals were not distributed normally .

II. Level of significance for the test was considered at α=0 . 05 or at 5%.

III. The test statistic chosen for the test was the Jarque-Berra test for normality, and the

test statistic was calculated for the residuals of the regression model.

IV. The skewness S = -0.041 and the excess Kurtosis = 1.118 with sample size of n=60

11

The JB-statistic was calculated as JB= n

6 ( S2+ K 2

4 ) =3 .143 . The significance or the p-value

for the JB-statistic was calculated considering the fact that JB-statistic follows Chi-Square

distribution with 2 degrees of freedom. Hence, the p-value = CHIDIST (JB, 2) = CHIDIST

(3.143, 2) = 0.208 > 0.05.

V. Here the significance or the p-value was found to be greater than the level of

significance ( α=0 . 05 ) . Hence, there was not enough statistical evidence at 5% level to

reject the null hypothesis that assumed that the residuals were normally distributed

with skewness, S = 0. Hence, it was possible to conclude that the assumption of the

ordinary linear regression, that the residuals are normally distributed, stands out to be

plausible for the present regression model (Harrell, 2015, p. 359–387).

References

Bali, TG, Hu, J & Murray, S 2017, ‘Option implied volatility, skewness, and kurtosis and the

cross-section of expected stock returns’,.pp.1-5

Barberis, N, Greenwood, R, Jin, L & Shleifer, A 2015, ‘X-CAPM: An extrapolative capital

asset pricing model’, Journal of financial economics, vol. 115, no. 1, pp. 1–24.

Harrell, FE 2015, ‘Regression Models for Continuous Y and Case Study in Ordinal

Regression’, in Regression Modeling Strategies, Springer, pp. 359–387.

Jurado, K, Ludvigson, SC & Ng, S 2015, ‘Measuring Uncertainty’, American Economic

Review, vol. 105, no. 3, pp. 1177–1216.

Kim, N 2016, ‘A robustified Jarque–Bera test for multivariate normality’, Economics Letters,

vol. 140, pp. 48–52.

Lakens, D 2017, ‘Equivalence tests: a practical primer for t tests, correlations, and meta-

analyses’, Social Psychological and Personality Science, vol. 8, no. 4, pp. 355–362.

Read, LK & Vogel, RM 2015, ‘Reliability, return periods, and risk under nonstationarity’,

Water Resources Research, vol. 51, no. 8, pp. 6381–6398.

12

6 ( S2+ K 2

4 ) =3 .143 . The significance or the p-value

for the JB-statistic was calculated considering the fact that JB-statistic follows Chi-Square

distribution with 2 degrees of freedom. Hence, the p-value = CHIDIST (JB, 2) = CHIDIST

(3.143, 2) = 0.208 > 0.05.

V. Here the significance or the p-value was found to be greater than the level of

significance ( α=0 . 05 ) . Hence, there was not enough statistical evidence at 5% level to

reject the null hypothesis that assumed that the residuals were normally distributed

with skewness, S = 0. Hence, it was possible to conclude that the assumption of the

ordinary linear regression, that the residuals are normally distributed, stands out to be

plausible for the present regression model (Harrell, 2015, p. 359–387).

References

Bali, TG, Hu, J & Murray, S 2017, ‘Option implied volatility, skewness, and kurtosis and the

cross-section of expected stock returns’,.pp.1-5

Barberis, N, Greenwood, R, Jin, L & Shleifer, A 2015, ‘X-CAPM: An extrapolative capital

asset pricing model’, Journal of financial economics, vol. 115, no. 1, pp. 1–24.

Harrell, FE 2015, ‘Regression Models for Continuous Y and Case Study in Ordinal

Regression’, in Regression Modeling Strategies, Springer, pp. 359–387.

Jurado, K, Ludvigson, SC & Ng, S 2015, ‘Measuring Uncertainty’, American Economic

Review, vol. 105, no. 3, pp. 1177–1216.

Kim, N 2016, ‘A robustified Jarque–Bera test for multivariate normality’, Economics Letters,

vol. 140, pp. 48–52.

Lakens, D 2017, ‘Equivalence tests: a practical primer for t tests, correlations, and meta-

analyses’, Social Psychological and Personality Science, vol. 8, no. 4, pp. 355–362.

Read, LK & Vogel, RM 2015, ‘Reliability, return periods, and risk under nonstationarity’,

Water Resources Research, vol. 51, no. 8, pp. 6381–6398.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.