Cash Flow Statement Analysis

VerifiedAdded on 2021/04/16

|11

|2741

|112

AI Summary

This assignment requires the calculation and analysis of a company's cash flow statement for a specific quarter. The student is given information about cash receipts, payments, and other expenses, and must determine how much finance the company needs to maintain a desired closing cash balance. The assignment also includes references and bibliography from relevant academic sources.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

T-1.8.1

Details of Assessment

Term and Year 1, 2018 Time allowed 8 weeks

Assessment No 2 Assessment Weighting 40%

Assessment Type Assignment

Due Date Week No. 8 Room TBA

Details of Subject

Qualification BSBFIM501 Diploma of Leadership and Management

Subject Name Finance

Details of Unit(s) of competency

Unit Code (s) and

Names

BSBFIM501 Manage Budgets and Financial Plans

Details of Student

Student Name

College Student ID

Student Declaration: I declare that the work

submitted is my own, and has not been

copied or plagiarised from any person or

source.

Signature: ___________________________

Date: _______/________/_______________

Details of Assessor

Assessor’s Name Nadia Chowdhury

Assessment Outcome

Results Satisfactory Not

Satisfactory Marks / 40

FEEDBACK TO STUDENT

Progressive feedback to students, identifying gaps in competency and comments on positive improvements:

______________________________________________________________________________________

______________________________________________________________________________________

______________________________________________________________________________________

______________________________________________________________________________________

Student Declaration: I declare that I have been

assessed in this unit, and I have been advised of my

result. I also am aware of my appeal rights and

reassessment procedure.

Signature: ____________________________

Date: ____/_____/_____

Assessor Declaration: I declare that I have

conducted a fair, valid, reliable and flexible

assessment with this student, and I have provided

appropriate feedback

Student did not attend the feedback session.

Feedback provided on assessment.

Signature: ____________________________

Date: ____/_____/_____

Finance, Assessment No.2 Page 1

v1.1, Last updated on 02/09/2017

Details of Assessment

Term and Year 1, 2018 Time allowed 8 weeks

Assessment No 2 Assessment Weighting 40%

Assessment Type Assignment

Due Date Week No. 8 Room TBA

Details of Subject

Qualification BSBFIM501 Diploma of Leadership and Management

Subject Name Finance

Details of Unit(s) of competency

Unit Code (s) and

Names

BSBFIM501 Manage Budgets and Financial Plans

Details of Student

Student Name

College Student ID

Student Declaration: I declare that the work

submitted is my own, and has not been

copied or plagiarised from any person or

source.

Signature: ___________________________

Date: _______/________/_______________

Details of Assessor

Assessor’s Name Nadia Chowdhury

Assessment Outcome

Results Satisfactory Not

Satisfactory Marks / 40

FEEDBACK TO STUDENT

Progressive feedback to students, identifying gaps in competency and comments on positive improvements:

______________________________________________________________________________________

______________________________________________________________________________________

______________________________________________________________________________________

______________________________________________________________________________________

Student Declaration: I declare that I have been

assessed in this unit, and I have been advised of my

result. I also am aware of my appeal rights and

reassessment procedure.

Signature: ____________________________

Date: ____/_____/_____

Assessor Declaration: I declare that I have

conducted a fair, valid, reliable and flexible

assessment with this student, and I have provided

appropriate feedback

Student did not attend the feedback session.

Feedback provided on assessment.

Signature: ____________________________

Date: ____/_____/_____

Finance, Assessment No.2 Page 1

v1.1, Last updated on 02/09/2017

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

T-1.8.1

Purpose of the Assessment

The purpose of this assessment is to assess the

student in the following learning outcomes:

Satisfactory

(S)

Not yet Satisfactory

(NS)

Plan financial management approaches

Implement financial management approaches

Monitor and control finances

Review and evaluate financial management

processes

Assessment/evidence gathering conditions

Each assessment component is recorded as either Satisfactory (S) or Not

Satisfactory (NS). A student can only achieve competence when all assessment

components listed under Purpose of the assessment section are Satisfactory.

Your trainer will give you feedback after the completion of each assessment. A

student who is assessed as NS (Not Satisfactory) is eligible for re-assessment.

Resources required for this Assessment

Upon completion, submit the assessment to your trainer along with assessment coversheet

Refer to the subject notes on E-Learning prior to responding to the tasks/questions

Any additional material will be provided by Trainer

Instructions for Students

Please read the following instructions carefully

This assessment has to be completed In class At home

The assessment is to be completed according to the instructions given by your assessor.

Feedback on each task will be provided to enable you to determine how your work could be improved.

You will be provided with feedback on your work within 2 weeks of the assessment due date. All other

feedbacks will be provided by the end of the term.

Should you not answer the questions correctly, you will be given feedback on the results and your gaps

in knowledge. You will be given another opportunity to demonstrate your knowledge and skills to be

deemed competent for this unit of competency.

If you are not sure about any aspects of this assessment, please ask for clarification from your

assessor.

Please refer to the College re-assessment and re-sit policy for more information.

Finance, Assessment No.2 Page 2

v1.1, Last updated on 02/09/2017

Purpose of the Assessment

The purpose of this assessment is to assess the

student in the following learning outcomes:

Satisfactory

(S)

Not yet Satisfactory

(NS)

Plan financial management approaches

Implement financial management approaches

Monitor and control finances

Review and evaluate financial management

processes

Assessment/evidence gathering conditions

Each assessment component is recorded as either Satisfactory (S) or Not

Satisfactory (NS). A student can only achieve competence when all assessment

components listed under Purpose of the assessment section are Satisfactory.

Your trainer will give you feedback after the completion of each assessment. A

student who is assessed as NS (Not Satisfactory) is eligible for re-assessment.

Resources required for this Assessment

Upon completion, submit the assessment to your trainer along with assessment coversheet

Refer to the subject notes on E-Learning prior to responding to the tasks/questions

Any additional material will be provided by Trainer

Instructions for Students

Please read the following instructions carefully

This assessment has to be completed In class At home

The assessment is to be completed according to the instructions given by your assessor.

Feedback on each task will be provided to enable you to determine how your work could be improved.

You will be provided with feedback on your work within 2 weeks of the assessment due date. All other

feedbacks will be provided by the end of the term.

Should you not answer the questions correctly, you will be given feedback on the results and your gaps

in knowledge. You will be given another opportunity to demonstrate your knowledge and skills to be

deemed competent for this unit of competency.

If you are not sure about any aspects of this assessment, please ask for clarification from your

assessor.

Please refer to the College re-assessment and re-sit policy for more information.

Finance, Assessment No.2 Page 2

v1.1, Last updated on 02/09/2017

T-1.8.1

Question 1: Metropolitan Furniture

(10 mark)

Peter works in the accounts unit of the Metropolitan Furniture

Manufacturing. He was asked to prepare a proposed budget for the

forthcoming quarter. He consults with the sales manager and finds that:

Estimated sales are as follows:

February $265,000 April $290,000

March $255,000 May $250,000

June $280,000

In consultation with the production manager he estimates that the cost of

goods sold is to be budgeted at 45% of the sales figure. The salaries are

expected to be $65,000 per month. When sales exceed $260,000 in any

one month, the sales team is entitled to an additional 5% commission on

the excess sales over this figure. Other expenses are estimated to be

$35,000 per month.

The owner of the organisation is concerned about the cash flow which was

not thought of before. The owner is of the opinion that the collection of

cash from sales is slow and this could possibly lead to cash flow problems

to the organisation. As Peter has never forecasted cash flow before he

sets about collecting information on this.

Peter estimates that 80% of the total sales are going to be cash sales

where the bill is settled when the goods are purchased or delivered. 10%

of the month’s sales settle the accounts owed in the month following

sales. Others (i.e. 10% of the month’s sales) settle in the month after.

Additional information for Cash Flow Statement:

The organisation gets a month’s credit on its purchases. That is, the

accounts for the purchases (COGS) made in one month is settled in the

following month.

All salaries are paid in the month as they are incurred.

The additional commission is paid in the month after the month in

which it was earned.

Other expenses are paid in the month they were incurred.

The bank balance at the beginning of the first month is estimated to be

$40,000.

1. Show the profit and loss calculations for the April, May and June

2. Show the cash flow projection calculations for April, May and June

3. What Peter is required to advise the owner of the organisation?

4. Will the business adequate financial provision to pay tax? Why?

5. If the cash flow statement and the P & L are productive, then what are the

relevant people Peter needs to communicate if he establishes a business

plan?

Finance, Assessment No.2 Page 3

v1.1, Last updated on 02/09/2017

Question 1: Metropolitan Furniture

(10 mark)

Peter works in the accounts unit of the Metropolitan Furniture

Manufacturing. He was asked to prepare a proposed budget for the

forthcoming quarter. He consults with the sales manager and finds that:

Estimated sales are as follows:

February $265,000 April $290,000

March $255,000 May $250,000

June $280,000

In consultation with the production manager he estimates that the cost of

goods sold is to be budgeted at 45% of the sales figure. The salaries are

expected to be $65,000 per month. When sales exceed $260,000 in any

one month, the sales team is entitled to an additional 5% commission on

the excess sales over this figure. Other expenses are estimated to be

$35,000 per month.

The owner of the organisation is concerned about the cash flow which was

not thought of before. The owner is of the opinion that the collection of

cash from sales is slow and this could possibly lead to cash flow problems

to the organisation. As Peter has never forecasted cash flow before he

sets about collecting information on this.

Peter estimates that 80% of the total sales are going to be cash sales

where the bill is settled when the goods are purchased or delivered. 10%

of the month’s sales settle the accounts owed in the month following

sales. Others (i.e. 10% of the month’s sales) settle in the month after.

Additional information for Cash Flow Statement:

The organisation gets a month’s credit on its purchases. That is, the

accounts for the purchases (COGS) made in one month is settled in the

following month.

All salaries are paid in the month as they are incurred.

The additional commission is paid in the month after the month in

which it was earned.

Other expenses are paid in the month they were incurred.

The bank balance at the beginning of the first month is estimated to be

$40,000.

1. Show the profit and loss calculations for the April, May and June

2. Show the cash flow projection calculations for April, May and June

3. What Peter is required to advise the owner of the organisation?

4. Will the business adequate financial provision to pay tax? Why?

5. If the cash flow statement and the P & L are productive, then what are the

relevant people Peter needs to communicate if he establishes a business

plan?

Finance, Assessment No.2 Page 3

v1.1, Last updated on 02/09/2017

T-1.8.1

6. If the P & L showing good profit trend and the

forecasted cash flow statement returns positive results, then marketing

and operational departments may tend to expand their budget and

therefore the business may have cash shortage in future. How Peter can

monitor financial performance on a continuous basis?

7. Does Peter require advising the owner about any immediate change in the

financial plan? Why?

Answer (1):

Profit and Loss calculations

April May June

$ $ $

Sales 290,000.0

0

250,000.00 280,000.00

Less Cost of Goods Sold 130,500.0

0

112,500.00 126,000.00

Gross Profit 159,500.0

0

137,500.00 154,000.00

Sales Salaries 65,000.0

0

65,000.00 65,000.00

Commission 1,500.0

0

- 1,000.00

Other expenses 35,000.0

0

35,000.00 35,000.00

Total expenses 101,500.0

0

100,000.00 101,000.00

Net Profit 58,000.0

0

37,500.00 53,000.00

Answer (2):

Cash flow projections

April May June

$ $ $

Opening Cash 40,000.0

0

109,250.00 131,750.00

Plus cash in:

This month 232,000.0

0

200,000.00 224,000.00

From last month 25,500.0

0

29,000.00 25,000.00

From two months ago 26,500.0

0

25,500.00 29,000.00

Total Cash available 284,000. 254,500.00 278,000.00

Finance, Assessment No.2 Page 4

v1.1, Last updated on 02/09/2017

6. If the P & L showing good profit trend and the

forecasted cash flow statement returns positive results, then marketing

and operational departments may tend to expand their budget and

therefore the business may have cash shortage in future. How Peter can

monitor financial performance on a continuous basis?

7. Does Peter require advising the owner about any immediate change in the

financial plan? Why?

Answer (1):

Profit and Loss calculations

April May June

$ $ $

Sales 290,000.0

0

250,000.00 280,000.00

Less Cost of Goods Sold 130,500.0

0

112,500.00 126,000.00

Gross Profit 159,500.0

0

137,500.00 154,000.00

Sales Salaries 65,000.0

0

65,000.00 65,000.00

Commission 1,500.0

0

- 1,000.00

Other expenses 35,000.0

0

35,000.00 35,000.00

Total expenses 101,500.0

0

100,000.00 101,000.00

Net Profit 58,000.0

0

37,500.00 53,000.00

Answer (2):

Cash flow projections

April May June

$ $ $

Opening Cash 40,000.0

0

109,250.00 131,750.00

Plus cash in:

This month 232,000.0

0

200,000.00 224,000.00

From last month 25,500.0

0

29,000.00 25,000.00

From two months ago 26,500.0

0

25,500.00 29,000.00

Total Cash available 284,000. 254,500.00 278,000.00

Finance, Assessment No.2 Page 4

v1.1, Last updated on 02/09/2017

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

T-1.8.1

00

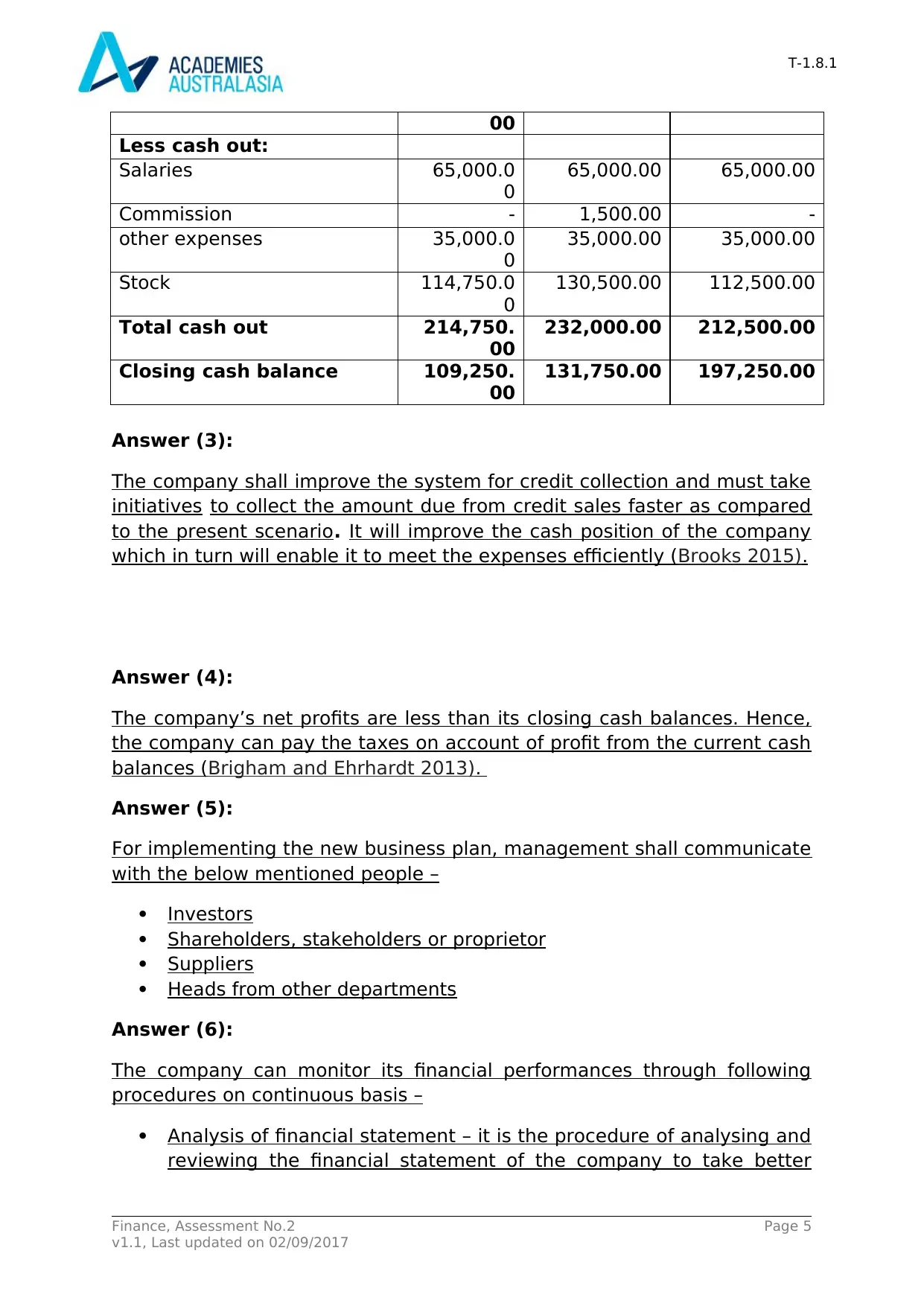

Less cash out:

Salaries 65,000.0

0

65,000.00 65,000.00

Commission - 1,500.00 -

other expenses 35,000.0

0

35,000.00 35,000.00

Stock 114,750.0

0

130,500.00 112,500.00

Total cash out 214,750.

00

232,000.00 212,500.00

Closing cash balance 109,250.

00

131,750.00 197,250.00

Answer (3):

The company shall improve the system for credit collection and must take

initiatives to collect the amount due from credit sales faster as compared

to the present scenario. It will improve the cash position of the company

which in turn will enable it to meet the expenses efficiently (Brooks 2015).

Answer (4):

The company’s net profits are less than its closing cash balances. Hence,

the company can pay the taxes on account of profit from the current cash

balances (Brigham and Ehrhardt 2013).

Answer (5):

For implementing the new business plan, management shall communicate

with the below mentioned people –

Investors

Shareholders, stakeholders or proprietor

Suppliers

Heads from other departments

Answer (6):

The company can monitor its financial performances through following

procedures on continuous basis –

Analysis of financial statement – it is the procedure of analysing and

reviewing the financial statement of the company to take better

Finance, Assessment No.2 Page 5

v1.1, Last updated on 02/09/2017

00

Less cash out:

Salaries 65,000.0

0

65,000.00 65,000.00

Commission - 1,500.00 -

other expenses 35,000.0

0

35,000.00 35,000.00

Stock 114,750.0

0

130,500.00 112,500.00

Total cash out 214,750.

00

232,000.00 212,500.00

Closing cash balance 109,250.

00

131,750.00 197,250.00

Answer (3):

The company shall improve the system for credit collection and must take

initiatives to collect the amount due from credit sales faster as compared

to the present scenario. It will improve the cash position of the company

which in turn will enable it to meet the expenses efficiently (Brooks 2015).

Answer (4):

The company’s net profits are less than its closing cash balances. Hence,

the company can pay the taxes on account of profit from the current cash

balances (Brigham and Ehrhardt 2013).

Answer (5):

For implementing the new business plan, management shall communicate

with the below mentioned people –

Investors

Shareholders, stakeholders or proprietor

Suppliers

Heads from other departments

Answer (6):

The company can monitor its financial performances through following

procedures on continuous basis –

Analysis of financial statement – it is the procedure of analysing and

reviewing the financial statement of the company to take better

Finance, Assessment No.2 Page 5

v1.1, Last updated on 02/09/2017

T-1.8.1

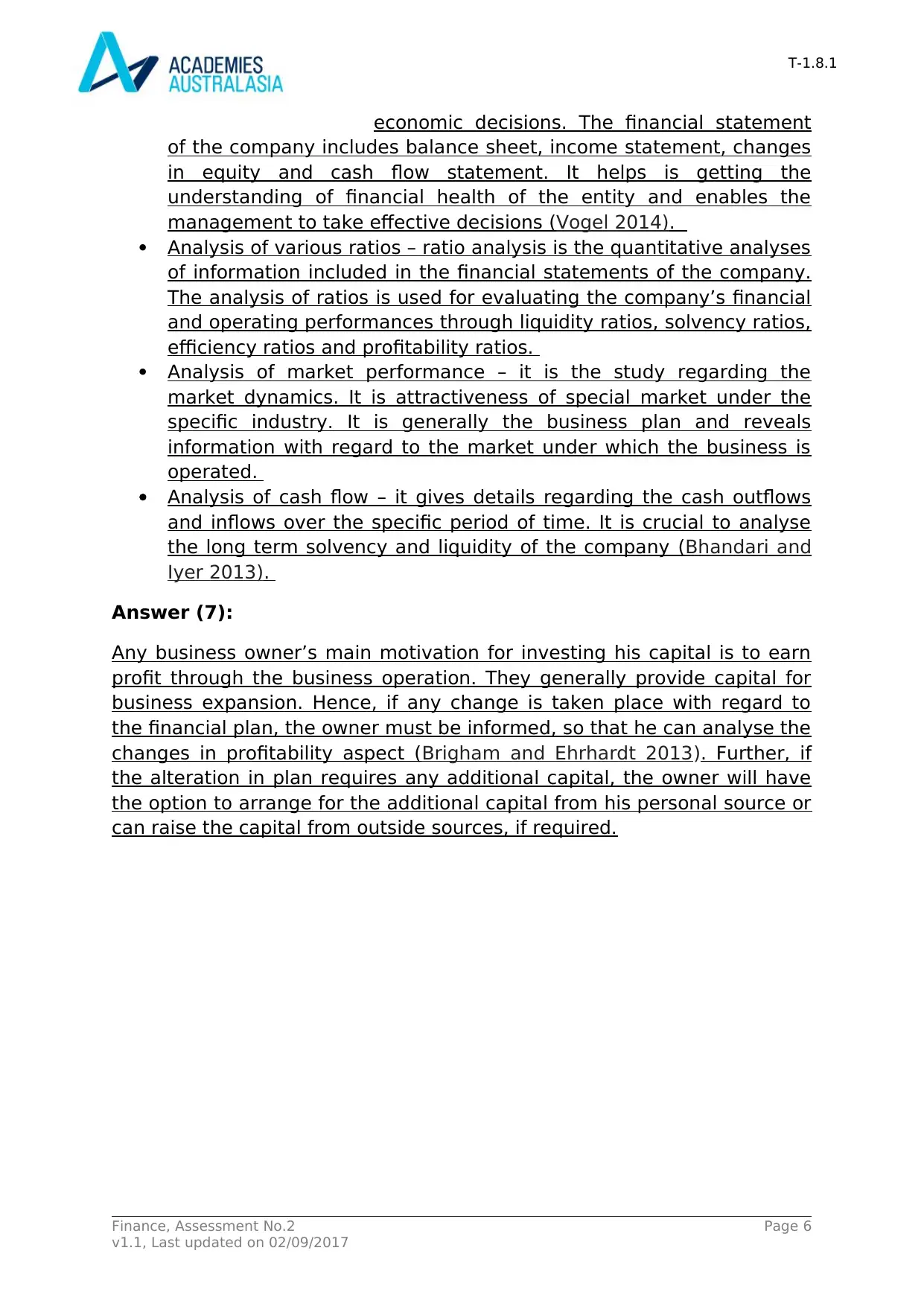

economic decisions. The financial statement

of the company includes balance sheet, income statement, changes

in equity and cash flow statement. It helps is getting the

understanding of financial health of the entity and enables the

management to take effective decisions (Vogel 2014).

Analysis of various ratios – ratio analysis is the quantitative analyses

of information included in the financial statements of the company.

The analysis of ratios is used for evaluating the company’s financial

and operating performances through liquidity ratios, solvency ratios,

efficiency ratios and profitability ratios.

Analysis of market performance – it is the study regarding the

market dynamics. It is attractiveness of special market under the

specific industry. It is generally the business plan and reveals

information with regard to the market under which the business is

operated.

Analysis of cash flow – it gives details regarding the cash outflows

and inflows over the specific period of time. It is crucial to analyse

the long term solvency and liquidity of the company (Bhandari and

Iyer 2013).

Answer (7):

Any business owner’s main motivation for investing his capital is to earn

profit through the business operation. They generally provide capital for

business expansion. Hence, if any change is taken place with regard to

the financial plan, the owner must be informed, so that he can analyse the

changes in profitability aspect (Brigham and Ehrhardt 2013). Further, if

the alteration in plan requires any additional capital, the owner will have

the option to arrange for the additional capital from his personal source or

can raise the capital from outside sources, if required.

Finance, Assessment No.2 Page 6

v1.1, Last updated on 02/09/2017

economic decisions. The financial statement

of the company includes balance sheet, income statement, changes

in equity and cash flow statement. It helps is getting the

understanding of financial health of the entity and enables the

management to take effective decisions (Vogel 2014).

Analysis of various ratios – ratio analysis is the quantitative analyses

of information included in the financial statements of the company.

The analysis of ratios is used for evaluating the company’s financial

and operating performances through liquidity ratios, solvency ratios,

efficiency ratios and profitability ratios.

Analysis of market performance – it is the study regarding the

market dynamics. It is attractiveness of special market under the

specific industry. It is generally the business plan and reveals

information with regard to the market under which the business is

operated.

Analysis of cash flow – it gives details regarding the cash outflows

and inflows over the specific period of time. It is crucial to analyse

the long term solvency and liquidity of the company (Bhandari and

Iyer 2013).

Answer (7):

Any business owner’s main motivation for investing his capital is to earn

profit through the business operation. They generally provide capital for

business expansion. Hence, if any change is taken place with regard to

the financial plan, the owner must be informed, so that he can analyse the

changes in profitability aspect (Brigham and Ehrhardt 2013). Further, if

the alteration in plan requires any additional capital, the owner will have

the option to arrange for the additional capital from his personal source or

can raise the capital from outside sources, if required.

Finance, Assessment No.2 Page 6

v1.1, Last updated on 02/09/2017

T-1.8.1

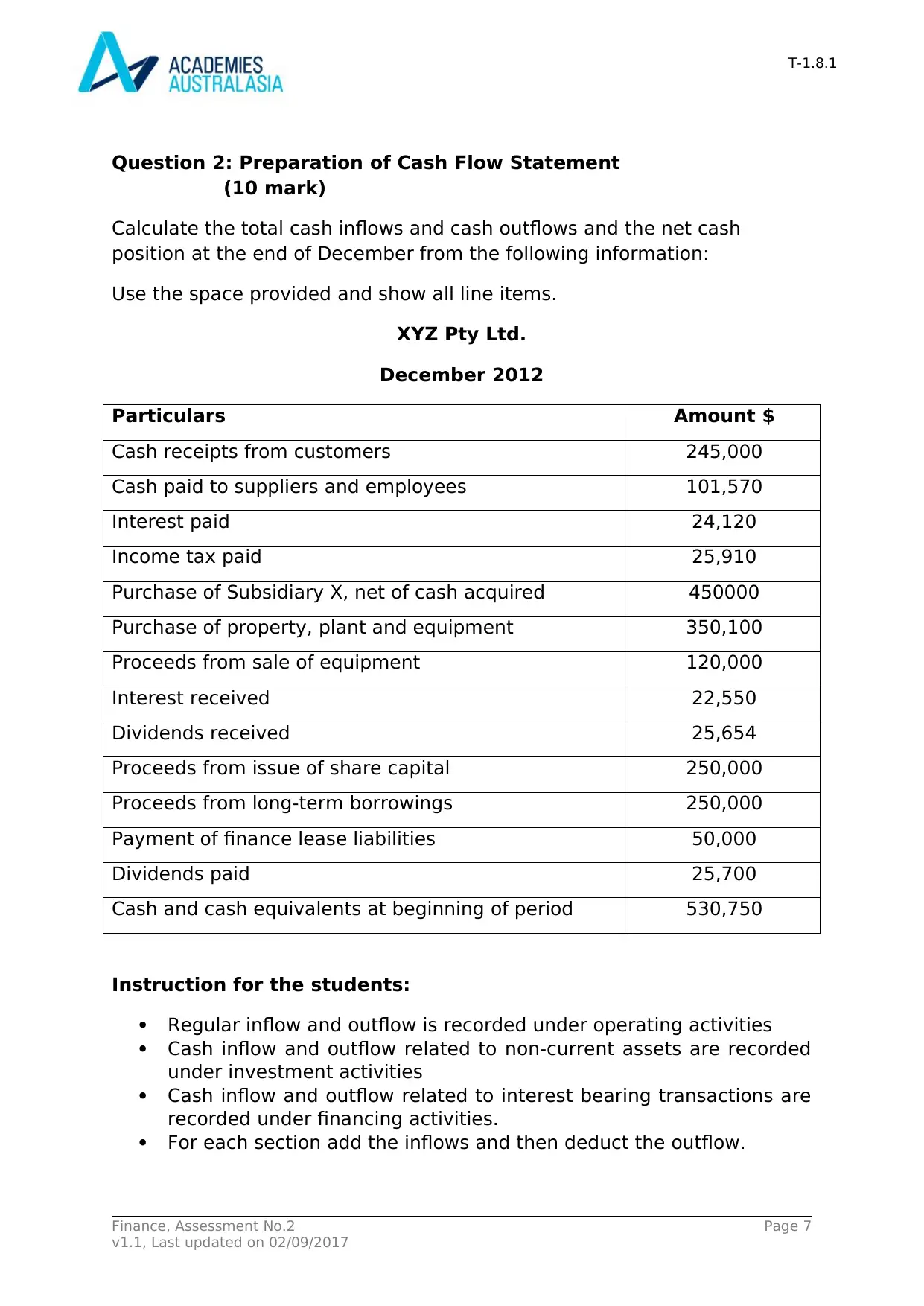

Question 2: Preparation of Cash Flow Statement

(10 mark)

Calculate the total cash inflows and cash outflows and the net cash

position at the end of December from the following information:

Use the space provided and show all line items.

XYZ Pty Ltd.

December 2012

Particulars Amount $

Cash receipts from customers 245,000

Cash paid to suppliers and employees 101,570

Interest paid 24,120

Income tax paid 25,910

Purchase of Subsidiary X, net of cash acquired 450000

Purchase of property, plant and equipment 350,100

Proceeds from sale of equipment 120,000

Interest received 22,550

Dividends received 25,654

Proceeds from issue of share capital 250,000

Proceeds from long-term borrowings 250,000

Payment of finance lease liabilities 50,000

Dividends paid 25,700

Cash and cash equivalents at beginning of period 530,750

Instruction for the students:

Regular inflow and outflow is recorded under operating activities

Cash inflow and outflow related to non-current assets are recorded

under investment activities

Cash inflow and outflow related to interest bearing transactions are

recorded under financing activities.

For each section add the inflows and then deduct the outflow.

Finance, Assessment No.2 Page 7

v1.1, Last updated on 02/09/2017

Question 2: Preparation of Cash Flow Statement

(10 mark)

Calculate the total cash inflows and cash outflows and the net cash

position at the end of December from the following information:

Use the space provided and show all line items.

XYZ Pty Ltd.

December 2012

Particulars Amount $

Cash receipts from customers 245,000

Cash paid to suppliers and employees 101,570

Interest paid 24,120

Income tax paid 25,910

Purchase of Subsidiary X, net of cash acquired 450000

Purchase of property, plant and equipment 350,100

Proceeds from sale of equipment 120,000

Interest received 22,550

Dividends received 25,654

Proceeds from issue of share capital 250,000

Proceeds from long-term borrowings 250,000

Payment of finance lease liabilities 50,000

Dividends paid 25,700

Cash and cash equivalents at beginning of period 530,750

Instruction for the students:

Regular inflow and outflow is recorded under operating activities

Cash inflow and outflow related to non-current assets are recorded

under investment activities

Cash inflow and outflow related to interest bearing transactions are

recorded under financing activities.

For each section add the inflows and then deduct the outflow.

Finance, Assessment No.2 Page 7

v1.1, Last updated on 02/09/2017

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

T-1.8.1

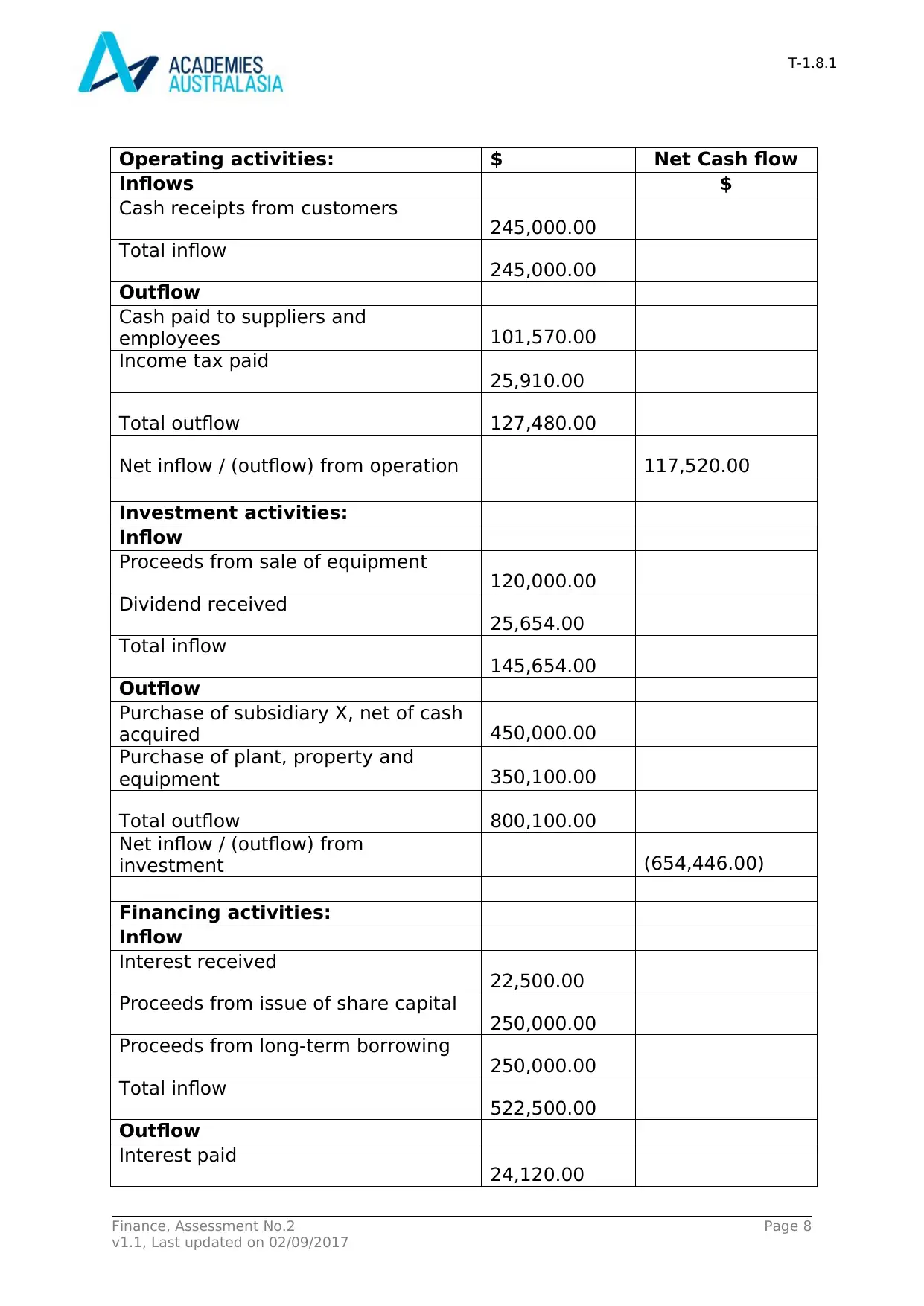

Operating activities: $ Net Cash flow

Inflows $

Cash receipts from customers

245,000.00

Total inflow

245,000.00

Outflow

Cash paid to suppliers and

employees 101,570.00

Income tax paid

25,910.00

Total outflow 127,480.00

Net inflow / (outflow) from operation 117,520.00

Investment activities:

Inflow

Proceeds from sale of equipment

120,000.00

Dividend received

25,654.00

Total inflow

145,654.00

Outflow

Purchase of subsidiary X, net of cash

acquired 450,000.00

Purchase of plant, property and

equipment 350,100.00

Total outflow 800,100.00

Net inflow / (outflow) from

investment (654,446.00)

Financing activities:

Inflow

Interest received

22,500.00

Proceeds from issue of share capital

250,000.00

Proceeds from long-term borrowing

250,000.00

Total inflow

522,500.00

Outflow

Interest paid

24,120.00

Finance, Assessment No.2 Page 8

v1.1, Last updated on 02/09/2017

Operating activities: $ Net Cash flow

Inflows $

Cash receipts from customers

245,000.00

Total inflow

245,000.00

Outflow

Cash paid to suppliers and

employees 101,570.00

Income tax paid

25,910.00

Total outflow 127,480.00

Net inflow / (outflow) from operation 117,520.00

Investment activities:

Inflow

Proceeds from sale of equipment

120,000.00

Dividend received

25,654.00

Total inflow

145,654.00

Outflow

Purchase of subsidiary X, net of cash

acquired 450,000.00

Purchase of plant, property and

equipment 350,100.00

Total outflow 800,100.00

Net inflow / (outflow) from

investment (654,446.00)

Financing activities:

Inflow

Interest received

22,500.00

Proceeds from issue of share capital

250,000.00

Proceeds from long-term borrowing

250,000.00

Total inflow

522,500.00

Outflow

Interest paid

24,120.00

Finance, Assessment No.2 Page 8

v1.1, Last updated on 02/09/2017

T-1.8.1

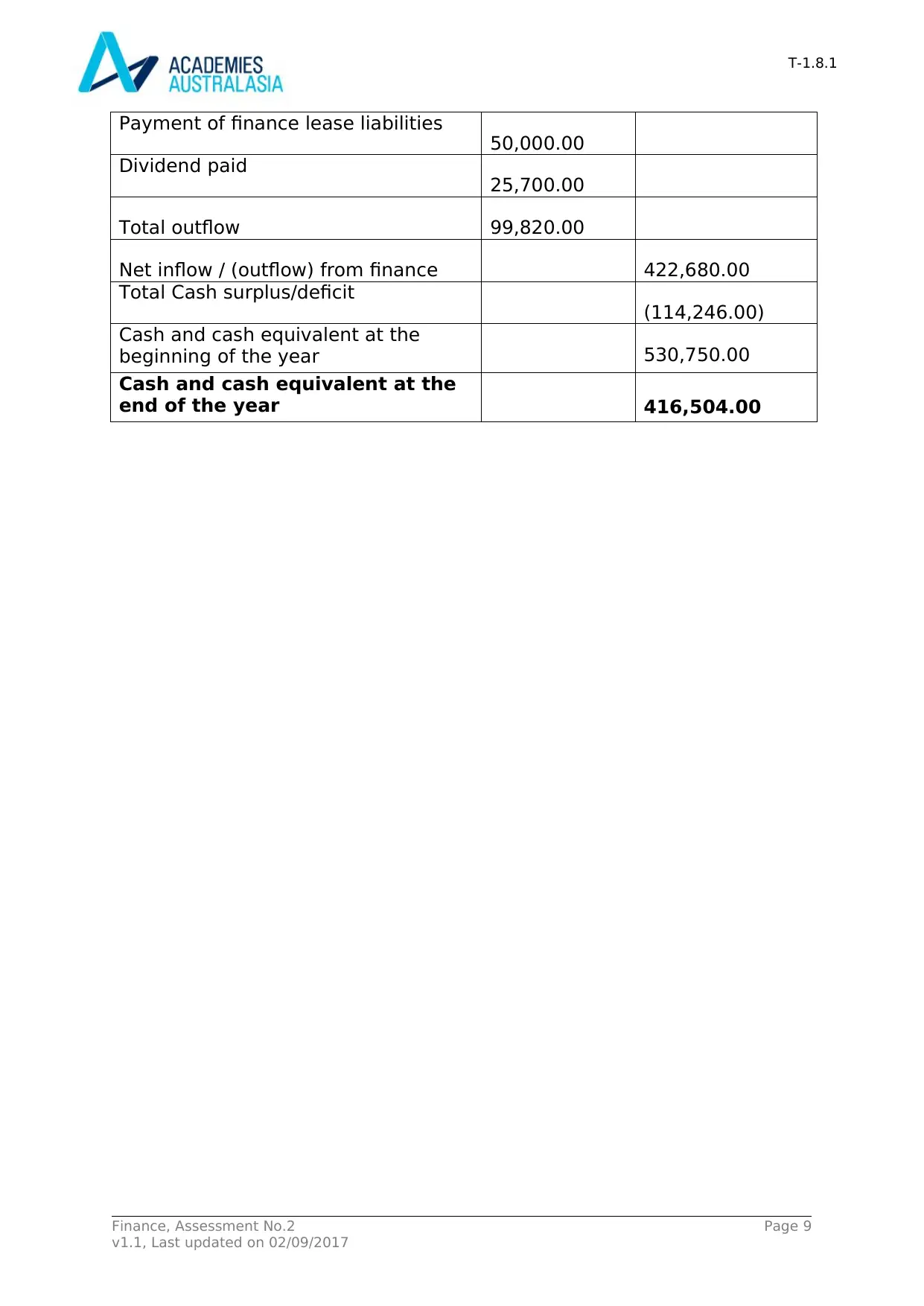

Payment of finance lease liabilities

50,000.00

Dividend paid

25,700.00

Total outflow 99,820.00

Net inflow / (outflow) from finance 422,680.00

Total Cash surplus/deficit

(114,246.00)

Cash and cash equivalent at the

beginning of the year 530,750.00

Cash and cash equivalent at the

end of the year 416,504.00

Finance, Assessment No.2 Page 9

v1.1, Last updated on 02/09/2017

Payment of finance lease liabilities

50,000.00

Dividend paid

25,700.00

Total outflow 99,820.00

Net inflow / (outflow) from finance 422,680.00

Total Cash surplus/deficit

(114,246.00)

Cash and cash equivalent at the

beginning of the year 530,750.00

Cash and cash equivalent at the

end of the year 416,504.00

Finance, Assessment No.2 Page 9

v1.1, Last updated on 02/09/2017

T-1.8.1

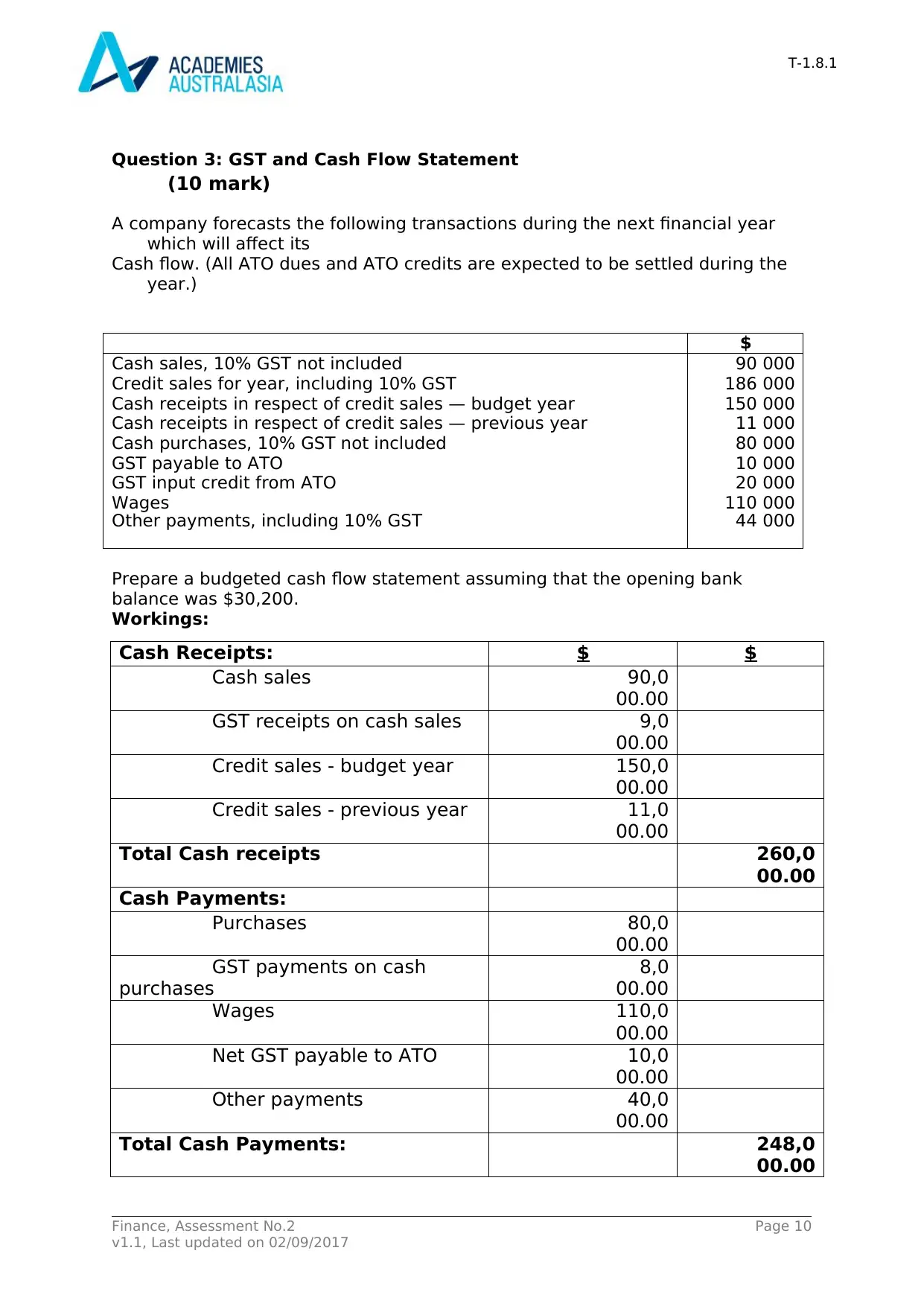

Question 3: GST and Cash Flow Statement

(10 mark)

A company forecasts the following transactions during the next financial year

which will affect its

Cash flow. (All ATO dues and ATO credits are expected to be settled during the

year.)

$

Cash sales, 10% GST not included

Credit sales for year, including 10% GST

Cash receipts in respect of credit sales — budget year

Cash receipts in respect of credit sales — previous year

Cash purchases, 10% GST not included

GST payable to ATO

GST input credit from ATO

Wages

Other payments, including 10% GST

90 000

186 000

150 000

11 000

80 000

10 000

20 000

110 000

44 000

Prepare a budgeted cash flow statement assuming that the opening bank

balance was $30,200.

Workings:

Cash Receipts: $ $

Cash sales 90,0

00.00

GST receipts on cash sales 9,0

00.00

Credit sales - budget year 150,0

00.00

Credit sales - previous year 11,0

00.00

Total Cash receipts 260,0

00.00

Cash Payments:

Purchases 80,0

00.00

GST payments on cash

purchases

8,0

00.00

Wages 110,0

00.00

Net GST payable to ATO 10,0

00.00

Other payments 40,0

00.00

Total Cash Payments: 248,0

00.00

Finance, Assessment No.2 Page 10

v1.1, Last updated on 02/09/2017

Question 3: GST and Cash Flow Statement

(10 mark)

A company forecasts the following transactions during the next financial year

which will affect its

Cash flow. (All ATO dues and ATO credits are expected to be settled during the

year.)

$

Cash sales, 10% GST not included

Credit sales for year, including 10% GST

Cash receipts in respect of credit sales — budget year

Cash receipts in respect of credit sales — previous year

Cash purchases, 10% GST not included

GST payable to ATO

GST input credit from ATO

Wages

Other payments, including 10% GST

90 000

186 000

150 000

11 000

80 000

10 000

20 000

110 000

44 000

Prepare a budgeted cash flow statement assuming that the opening bank

balance was $30,200.

Workings:

Cash Receipts: $ $

Cash sales 90,0

00.00

GST receipts on cash sales 9,0

00.00

Credit sales - budget year 150,0

00.00

Credit sales - previous year 11,0

00.00

Total Cash receipts 260,0

00.00

Cash Payments:

Purchases 80,0

00.00

GST payments on cash

purchases

8,0

00.00

Wages 110,0

00.00

Net GST payable to ATO 10,0

00.00

Other payments 40,0

00.00

Total Cash Payments: 248,0

00.00

Finance, Assessment No.2 Page 10

v1.1, Last updated on 02/09/2017

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

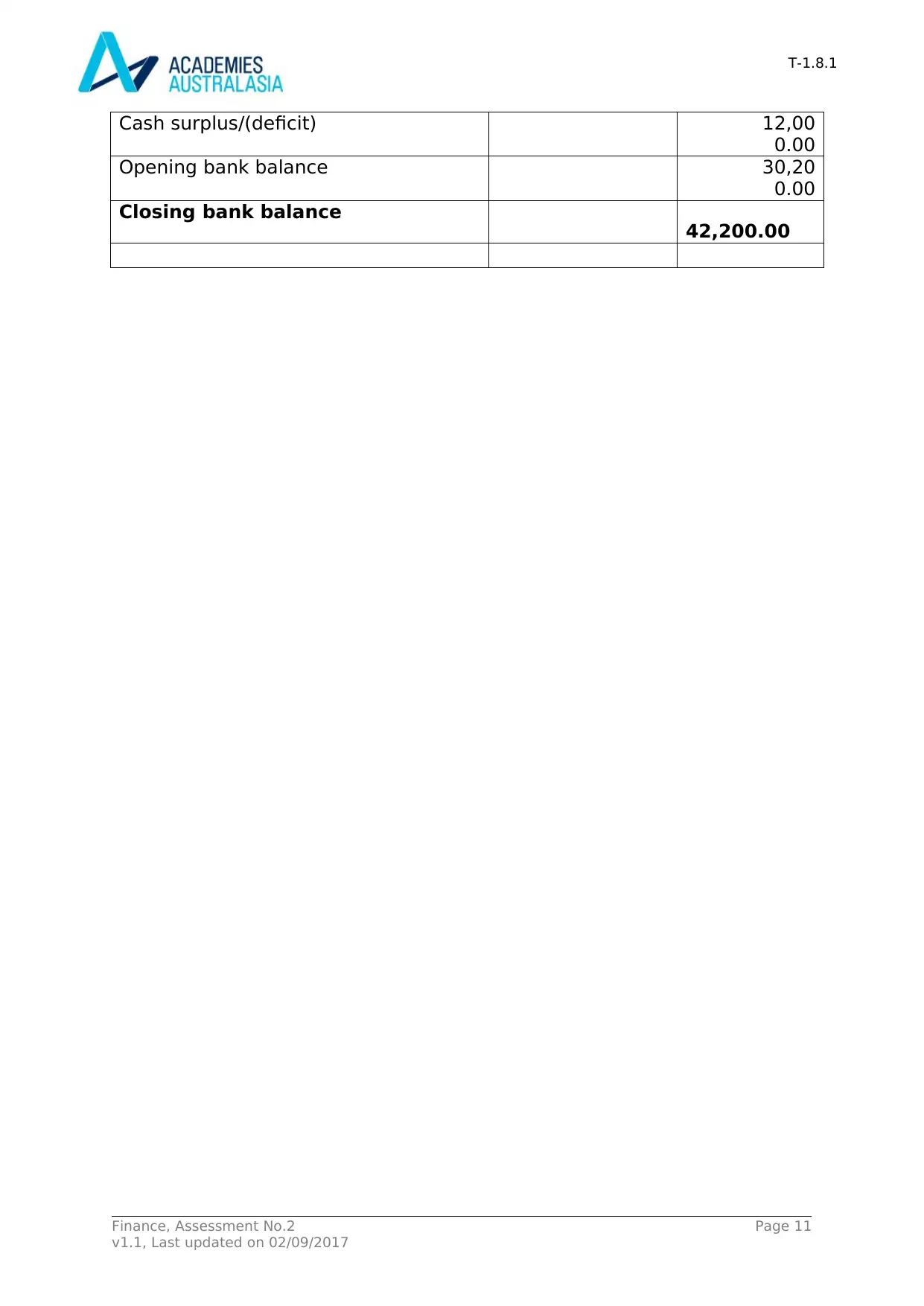

T-1.8.1

Cash surplus/(deficit) 12,00

0.00

Opening bank balance 30,20

0.00

Closing bank balance

42,200.00

Finance, Assessment No.2 Page 11

v1.1, Last updated on 02/09/2017

Cash surplus/(deficit) 12,00

0.00

Opening bank balance 30,20

0.00

Closing bank balance

42,200.00

Finance, Assessment No.2 Page 11

v1.1, Last updated on 02/09/2017

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.